Corporate Accounting Analysis: Commonwealth vs Westpac Banks

VerifiedAdded on 2023/06/05

|22

|4540

|97

Report

AI Summary

This report undertakes a comprehensive financial analysis of two prominent Australian banks, Commonwealth Bank and Westpac Bank, examining their financial performance through various components of their financial reports. The analysis delves into the equity section, discussing share capital, retained earnings, and reserves, and comparing the debt-equity ratios of both banks. The cash flow statements are scrutinized to understand the flow of cash from operating, investing, and financing activities, with a comparative analysis over three years. Furthermore, the report explores the comprehensive income statements, focusing on items reported in other comprehensive income, and their impact on managerial performance evaluation. Corporate income tax is also analyzed, including tax expenses, effective tax rates, deferred tax liabilities and assets, and cash tax calculations. The report concludes by providing insights into the efficiency of the organizations' working, based on the financial data and analysis.

CORPORATE ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

EXECUTIVE SUMMARY

This assignment is prepared to financially analyse two listed companies of Australia that

operates in the same industry. The financial reports of Common Wealth and Westpac Banks

has been analysed in this assignment. At the end of this report, the users will be able to have a

view about the efficiency of the organisation’s working.

This assignment is prepared to financially analyse two listed companies of Australia that

operates in the same industry. The financial reports of Common Wealth and Westpac Banks

has been analysed in this assignment. At the end of this report, the users will be able to have a

view about the efficiency of the organisation’s working.

Contents

INTRODUCTION......................................................................................................................3

ANALYSIS OF EQUITY..........................................................................................................4

Discussion on each item of equity for both the companies....................................................4

Discussion and debt and equity of both the companies..........................................................6

Analysis of Cash flow statement................................................................................................7

Discussion on the cash flow statement of both the companies..............................................7

Comparison of cash flow of three years of both the companies.............................................8

Description of analysis of cash flow of both the companies................................................10

Analysis of comprehensive income statement.........................................................................11

Items reported in the other comprehensive income statement.............................................11

Reasons for not reporting these items in the profit and loss statement................................11

Comparative analysis of the items of the other comprehensive income statement..............11

Use of other comprehensive income in evaluation of performance of managers................12

Analysis of corporate income tax.............................................................................................13

Tax expense for the companies for the current year.............................................................13

Effective income tax rate......................................................................................................13

Deferred tax liabilities and assets.........................................................................................13

Increase in DTA and DTL....................................................................................................14

Calculation of cash tax using the book tax...........................................................................14

Calculation of cash tax rate..................................................................................................16

Difference in cash tax and book tax.....................................................................................16

Conclusion............................................................................................................................17

Bibliography.............................................................................................................................18

INTRODUCTION......................................................................................................................3

ANALYSIS OF EQUITY..........................................................................................................4

Discussion on each item of equity for both the companies....................................................4

Discussion and debt and equity of both the companies..........................................................6

Analysis of Cash flow statement................................................................................................7

Discussion on the cash flow statement of both the companies..............................................7

Comparison of cash flow of three years of both the companies.............................................8

Description of analysis of cash flow of both the companies................................................10

Analysis of comprehensive income statement.........................................................................11

Items reported in the other comprehensive income statement.............................................11

Reasons for not reporting these items in the profit and loss statement................................11

Comparative analysis of the items of the other comprehensive income statement..............11

Use of other comprehensive income in evaluation of performance of managers................12

Analysis of corporate income tax.............................................................................................13

Tax expense for the companies for the current year.............................................................13

Effective income tax rate......................................................................................................13

Deferred tax liabilities and assets.........................................................................................13

Increase in DTA and DTL....................................................................................................14

Calculation of cash tax using the book tax...........................................................................14

Calculation of cash tax rate..................................................................................................16

Difference in cash tax and book tax.....................................................................................16

Conclusion............................................................................................................................17

Bibliography.............................................................................................................................18

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION

A financial report comprises of several components in it. In order to understand these parts

of the financial report, we need to know about its characteristics and their nature. In this

assignment various components of the companies in Australia has been discussed. The

discussion has been done on Commonwealth bank of Australia and Westpac bank are as

follows (Atkinson, 2012).

Commonwealth bank is considered to be one of the biggest banks operating in Australia.

However, this bank also carries out its business in various other countries such as Unite

Kingdom, New Zealand and also United states. It was establishes in the year 1991 also in the

same year it got listed in the Australian stock exchange (ASX). There are huge number of

branches of this bank which is nearly 1100 and also there are 51800 people employed in this

bank. This is not only considered as the biggest bank in Australia but also in the entire

southern hemisphere. The bank engages in providing many services such as superannuation,

institutional banking, insurance, fund management, broking services (Armstrong, 2015).

Westpac bank is located in Sydney and is considered to be among the four largest banks of

Australia. This bank is highly reputed as it has been ranked as the most sustainable bank

across the globe for four consecutive years (Berry, 2009). In 1817 there was an establishment

of a bank which was known as New south Wales. Later, in 1982 this bank it changed to

Westpac bank. This bank got listed in the Australian stock exchange in the year 1970. There

are about 14 million people that are associated with this bank and also there are 32620 people

who are employed in this bank. The bank believes in providing its services worldwide and so

there is huge number of branches set up which is nearly 1490.

In order to understand the financial position and performance of both these companies,

various components of the financial reports are studied and discussed in this report (Boyd,

2013).

A financial report comprises of several components in it. In order to understand these parts

of the financial report, we need to know about its characteristics and their nature. In this

assignment various components of the companies in Australia has been discussed. The

discussion has been done on Commonwealth bank of Australia and Westpac bank are as

follows (Atkinson, 2012).

Commonwealth bank is considered to be one of the biggest banks operating in Australia.

However, this bank also carries out its business in various other countries such as Unite

Kingdom, New Zealand and also United states. It was establishes in the year 1991 also in the

same year it got listed in the Australian stock exchange (ASX). There are huge number of

branches of this bank which is nearly 1100 and also there are 51800 people employed in this

bank. This is not only considered as the biggest bank in Australia but also in the entire

southern hemisphere. The bank engages in providing many services such as superannuation,

institutional banking, insurance, fund management, broking services (Armstrong, 2015).

Westpac bank is located in Sydney and is considered to be among the four largest banks of

Australia. This bank is highly reputed as it has been ranked as the most sustainable bank

across the globe for four consecutive years (Berry, 2009). In 1817 there was an establishment

of a bank which was known as New south Wales. Later, in 1982 this bank it changed to

Westpac bank. This bank got listed in the Australian stock exchange in the year 1970. There

are about 14 million people that are associated with this bank and also there are 32620 people

who are employed in this bank. The bank believes in providing its services worldwide and so

there is huge number of branches set up which is nearly 1490.

In order to understand the financial position and performance of both these companies,

various components of the financial reports are studied and discussed in this report (Boyd,

2013).

ANALYSIS OF EQUITY

The equity shareholders fund comprises of the funds that are raised from the public in

exchange of equity shares, reserves and also the profits that are ploughed back by the

company which is also known as retained earnings.

Discussion on each item of equity for both the companies

The components of the equity portion of Commonwealth bank comprises of share capital,

retained as well as certain reserves that were created. The total share capital of the company

for the year 2017 amounts to $34971 which can be divided into two parts (Case, 2012). The

first part consist of ordinary equity share that amounts to $ 35266 and the second part consists

of the treasury stock which amounts to $295. There was an increase in the share capital of the

company which happened because of the issue of new equity shares which was planned by

the company under dividend reinvestment plan. There was increase in the retained earnings

of the company. It increased from $23435 to $ 26330 million. This was the result of the

phenomenal performance of the company during 2017 which was reflected in the increased

operating profits of the company. However, it was noticed that the reserves of the company

fell from $ 2734 to $1869 in the year 2017. This fall in the reserves was because of the

change in the foreign currency exchange rate as well as loss that has arisen because of

disposal of certain assets (Bragg, 2016). The equity of the company increased from $60014 in

2016 to $ 63170 in 2017.

Commonwealth Bank

2Shareholder’s Equity 2017 2016

Share capital 34,971 33,845

Reserves

1,86

9 2,734

Retained earning 26,330 23,435

Total 63,170 60,014

The equity shareholders fund comprises of the funds that are raised from the public in

exchange of equity shares, reserves and also the profits that are ploughed back by the

company which is also known as retained earnings.

Discussion on each item of equity for both the companies

The components of the equity portion of Commonwealth bank comprises of share capital,

retained as well as certain reserves that were created. The total share capital of the company

for the year 2017 amounts to $34971 which can be divided into two parts (Case, 2012). The

first part consist of ordinary equity share that amounts to $ 35266 and the second part consists

of the treasury stock which amounts to $295. There was an increase in the share capital of the

company which happened because of the issue of new equity shares which was planned by

the company under dividend reinvestment plan. There was increase in the retained earnings

of the company. It increased from $23435 to $ 26330 million. This was the result of the

phenomenal performance of the company during 2017 which was reflected in the increased

operating profits of the company. However, it was noticed that the reserves of the company

fell from $ 2734 to $1869 in the year 2017. This fall in the reserves was because of the

change in the foreign currency exchange rate as well as loss that has arisen because of

disposal of certain assets (Bragg, 2016). The equity of the company increased from $60014 in

2016 to $ 63170 in 2017.

Commonwealth Bank

2Shareholder’s Equity 2017 2016

Share capital 34,971 33,845

Reserves

1,86

9 2,734

Retained earning 26,330 23,435

Total 63,170 60,014

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2017 2016

58,000

59,000

60,000

61,000

62,000

63,000

64,000

Commonwealth Bank

Shareholders

Equity

The components of the equity capital of Westpac bank are same as of the common wealth

bank which is share capital, reserves and retained earnings (Dickson, 2017). The ordinary

share capital of the company amounted to $34889 and the treasury stock amounted to $495

which made the total share capital of the company amount to $34394. It was observed that

the share capital in 2016 was $ 33014 but in 2017 it amounted to $34394. Also, there was an

increase in the retained earnings of the company from $ 24379 to $ 26100 which happened

because of the increasing operating profits earned by the company. The reserves of the

company increased from $727 in 2016 to $ 794 in 2017 because the gains that occurred from

the fair value changes. So, we can conclude that the shareholder’s fund has increased in 2017

when compared to 2016.

Westpac Bank

Shareholder’s Equity 2017 2016

Share capital 34,394 33,014

Reserves

79

4 727

Retained earning 26,100 24,379

Total 61,288 58,120

58,000

59,000

60,000

61,000

62,000

63,000

64,000

Commonwealth Bank

Shareholders

Equity

The components of the equity capital of Westpac bank are same as of the common wealth

bank which is share capital, reserves and retained earnings (Dickson, 2017). The ordinary

share capital of the company amounted to $34889 and the treasury stock amounted to $495

which made the total share capital of the company amount to $34394. It was observed that

the share capital in 2016 was $ 33014 but in 2017 it amounted to $34394. Also, there was an

increase in the retained earnings of the company from $ 24379 to $ 26100 which happened

because of the increasing operating profits earned by the company. The reserves of the

company increased from $727 in 2016 to $ 794 in 2017 because the gains that occurred from

the fair value changes. So, we can conclude that the shareholder’s fund has increased in 2017

when compared to 2016.

Westpac Bank

Shareholder’s Equity 2017 2016

Share capital 34,394 33,014

Reserves

79

4 727

Retained earning 26,100 24,379

Total 61,288 58,120

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2017 2016

56,000

57,000

58,000

59,000

60,000

61,000

62,000

Westpac Bank

Shareholders

Equity

Discussion and debt and equity of both the companies

A company can raise funds either buy issuing common shares to the public or by raising debt

from the third parties (Donanldson, 2012). There are certain pros and cons of raising funds by

either of the ways. There are various factors that the company has to look upon before taking

the final decision regarding the source of finance. The few factors that the company must

look upon are industry to which the company belongs, the cost of capital, etc.

The data of debt and equity of both the companies are stated in the below table:

Particulars Equity Share Cap Debt Debt Equity ratio

Commonwealth Bank

63,17

0 6,26,655 9.92

Westpac Bank

61,28

8 5,33,591 8.71

The information provided above has helped us to calculate the debt equity ratio of both the

companies. The debt equity ratio of Commonwealth bank and Westpac bank is 9.92 and 8.71

times respectively.

As we can see, the debt equity ratio for both the companies is very high. This may be because

debt is preferred more as a source of finance in the banking sector. So, we can conclude that

both the banks have a similar capital structure (Edwards, 2014).

56,000

57,000

58,000

59,000

60,000

61,000

62,000

Westpac Bank

Shareholders

Equity

Discussion and debt and equity of both the companies

A company can raise funds either buy issuing common shares to the public or by raising debt

from the third parties (Donanldson, 2012). There are certain pros and cons of raising funds by

either of the ways. There are various factors that the company has to look upon before taking

the final decision regarding the source of finance. The few factors that the company must

look upon are industry to which the company belongs, the cost of capital, etc.

The data of debt and equity of both the companies are stated in the below table:

Particulars Equity Share Cap Debt Debt Equity ratio

Commonwealth Bank

63,17

0 6,26,655 9.92

Westpac Bank

61,28

8 5,33,591 8.71

The information provided above has helped us to calculate the debt equity ratio of both the

companies. The debt equity ratio of Commonwealth bank and Westpac bank is 9.92 and 8.71

times respectively.

As we can see, the debt equity ratio for both the companies is very high. This may be because

debt is preferred more as a source of finance in the banking sector. So, we can conclude that

both the banks have a similar capital structure (Edwards, 2014).

Analysis of Cash flow statement

The books of accounts that are prepared by the management of the company follows accrual

basis. The cash flow statement of the company is prepared in order to know about the

medium through which cash is flowing in the organisation. The company can use the

statement of cash flows in order to know about its liquidity position (Flood, 2017).

Discussion on the cash flow statement of both the companies

There was a decline in the cash outflow from operating activities from $4561 million to $807

million. The reason behind the decline from operating activities is the increase of cash inflow

from investments as well as interest income. The cash inflow from operating activity is a

company involved in banking sector usually comprises of cash inflow from interests and

income from investments as they are considered to be the main business activities in the

banking sector.

The cash flows from investing activities for common wealth bank consists of cash flows from

sale or acquisition of associate and subsidiaries, investments, fixed assets as well as the

dividend received from investments (Girard, 2014). It is observable that the cash outflow

from investing activities in the year 2016 was $ 2032 million but late on in the year 2017 it

decreased to $ 677. The reason behind this downfall in cash outflow from investing activity

was because of decrease in the payments made for acquisition of controlled entities, purchase

of certain plant and property along with some intangible assets.

Now, let’s talk about the cash flows from financing activities of Commonwealth bank.

Financing activity mainly comprises of raising funds as well as repayments of equity and

debt. The cash outflow from financing activity increased to $10472 million in 2017 whereas

it was $1620 million in 2016. The debt securities that were repaid were comparatively lower

because of which the cash inflow from financing activity was higher (Gow, 2016).

On analysing the cash flow statement, we can conclude that the net cash flow of

commonwealth bank was negative $4973 million but it increased to positive $8988 million in

the year 2018.

Westpac’s bank operating activities consisted of cash flows from insurance proceeds, interest

as well income tax. There was a decline in the cash inflow from operating activities because

The books of accounts that are prepared by the management of the company follows accrual

basis. The cash flow statement of the company is prepared in order to know about the

medium through which cash is flowing in the organisation. The company can use the

statement of cash flows in order to know about its liquidity position (Flood, 2017).

Discussion on the cash flow statement of both the companies

There was a decline in the cash outflow from operating activities from $4561 million to $807

million. The reason behind the decline from operating activities is the increase of cash inflow

from investments as well as interest income. The cash inflow from operating activity is a

company involved in banking sector usually comprises of cash inflow from interests and

income from investments as they are considered to be the main business activities in the

banking sector.

The cash flows from investing activities for common wealth bank consists of cash flows from

sale or acquisition of associate and subsidiaries, investments, fixed assets as well as the

dividend received from investments (Girard, 2014). It is observable that the cash outflow

from investing activities in the year 2016 was $ 2032 million but late on in the year 2017 it

decreased to $ 677. The reason behind this downfall in cash outflow from investing activity

was because of decrease in the payments made for acquisition of controlled entities, purchase

of certain plant and property along with some intangible assets.

Now, let’s talk about the cash flows from financing activities of Commonwealth bank.

Financing activity mainly comprises of raising funds as well as repayments of equity and

debt. The cash outflow from financing activity increased to $10472 million in 2017 whereas

it was $1620 million in 2016. The debt securities that were repaid were comparatively lower

because of which the cash inflow from financing activity was higher (Gow, 2016).

On analysing the cash flow statement, we can conclude that the net cash flow of

commonwealth bank was negative $4973 million but it increased to positive $8988 million in

the year 2018.

Westpac’s bank operating activities consisted of cash flows from insurance proceeds, interest

as well income tax. There was a decline in the cash inflow from operating activities because

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

of the fall in the fair value of the investments. The cash inflow declined from $5497 in 2016

to $2820 in 2017.

Westpac’s investing activities consists of buying and selling of different securities or assets

(tangible as well as intangible). There was a decline in the cash outflow from investing

activities from $7245 in 2016 to $1698 in 2017. There were a lot of securities that were sold

and therefore, the cash outflow declined (Holtzman, 2013).

The financing activity of the Westpac’s bank consisted of raising funds or making repayment

of equity and debt securities. There was a fall in the cash inflow from financing activity to

552 million whereas it was $4573 in 2016. The reason behind this decreased cash inflow was

the cash outflow for repayments of debt (Horngren, 2012).

The overall cash flow for Westpac’s bank was $1674 million in 2017 and $2825 in 2016.

Comparison of cash flow of three years of both the companies

The information about the cash flows from operating activities for both the banks is provided

in the table below:

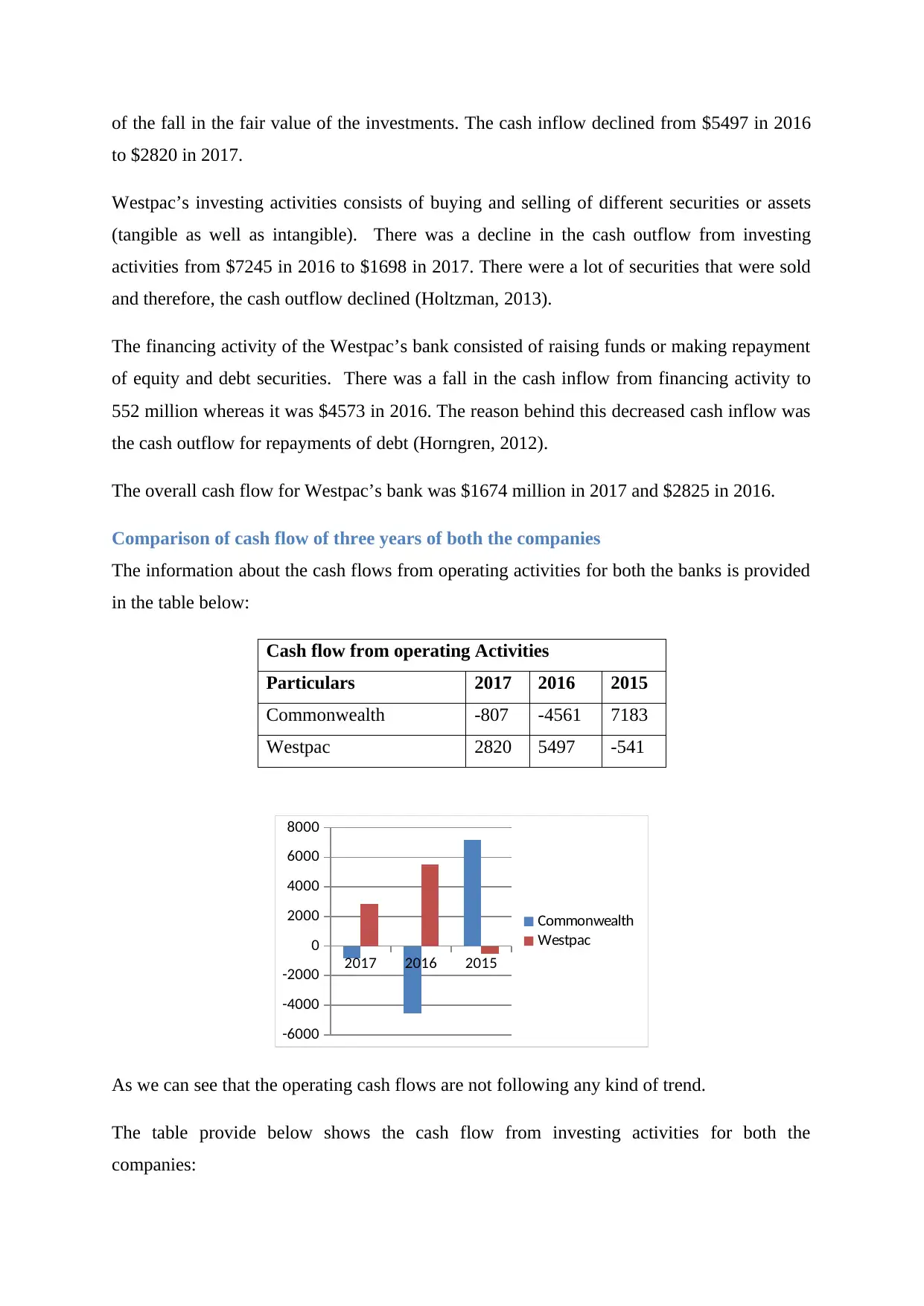

Cash flow from operating Activities

Particulars 2017 2016 2015

Commonwealth -807 -4561 7183

Westpac 2820 5497 -541

2017 2016 2015

-6000

-4000

-2000

0

2000

4000

6000

8000

Commonwealth

Westpac

As we can see that the operating cash flows are not following any kind of trend.

The table provide below shows the cash flow from investing activities for both the

companies:

to $2820 in 2017.

Westpac’s investing activities consists of buying and selling of different securities or assets

(tangible as well as intangible). There was a decline in the cash outflow from investing

activities from $7245 in 2016 to $1698 in 2017. There were a lot of securities that were sold

and therefore, the cash outflow declined (Holtzman, 2013).

The financing activity of the Westpac’s bank consisted of raising funds or making repayment

of equity and debt securities. There was a fall in the cash inflow from financing activity to

552 million whereas it was $4573 in 2016. The reason behind this decreased cash inflow was

the cash outflow for repayments of debt (Horngren, 2012).

The overall cash flow for Westpac’s bank was $1674 million in 2017 and $2825 in 2016.

Comparison of cash flow of three years of both the companies

The information about the cash flows from operating activities for both the banks is provided

in the table below:

Cash flow from operating Activities

Particulars 2017 2016 2015

Commonwealth -807 -4561 7183

Westpac 2820 5497 -541

2017 2016 2015

-6000

-4000

-2000

0

2000

4000

6000

8000

Commonwealth

Westpac

As we can see that the operating cash flows are not following any kind of trend.

The table provide below shows the cash flow from investing activities for both the

companies:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

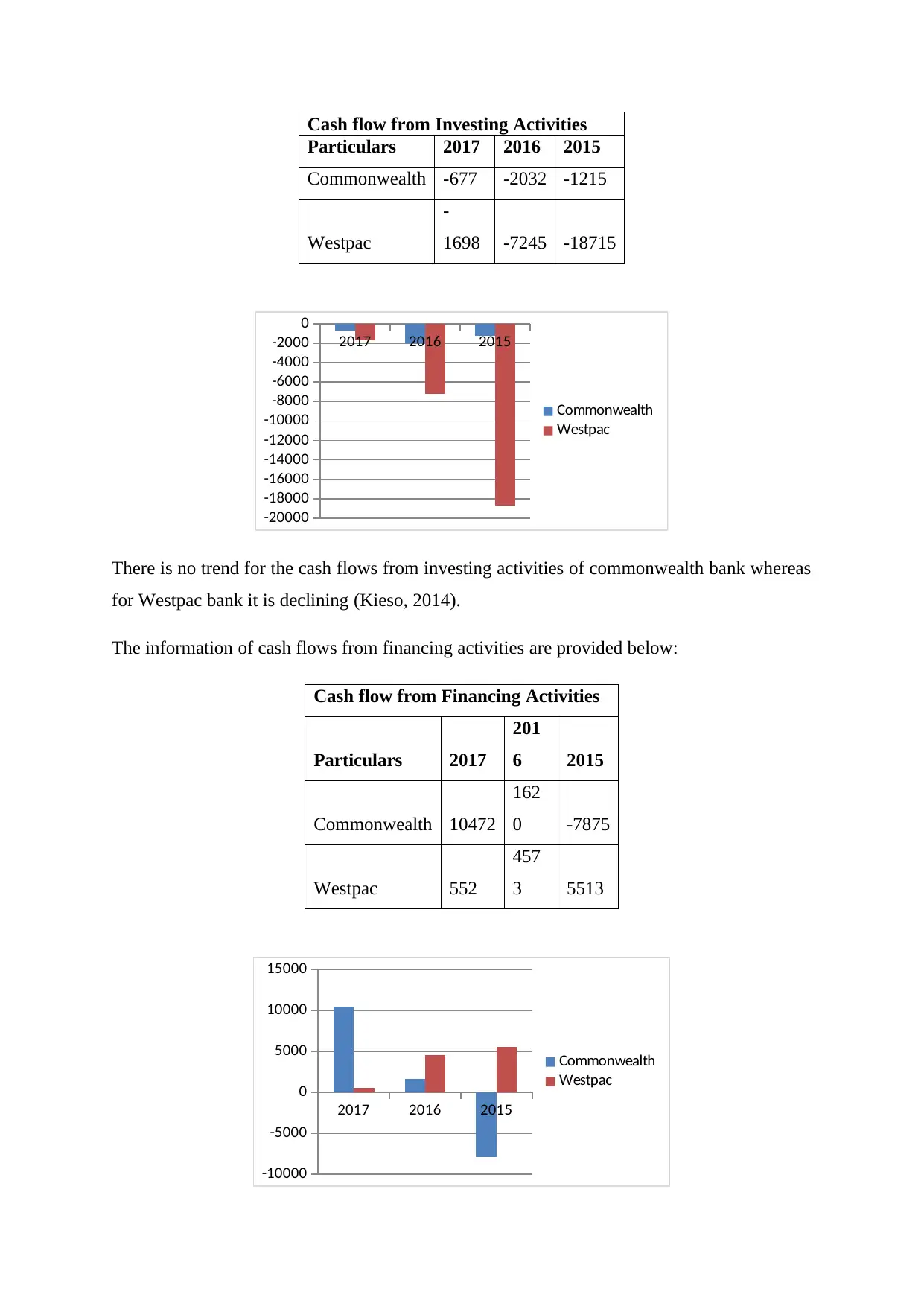

Cash flow from Investing Activities

Particulars 2017 2016 2015

Commonwealth -677 -2032 -1215

Westpac

-

1698 -7245 -18715

2017 2016 2015

-20000

-18000

-16000

-14000

-12000

-10000

-8000

-6000

-4000

-2000

0

Commonwealth

Westpac

There is no trend for the cash flows from investing activities of commonwealth bank whereas

for Westpac bank it is declining (Kieso, 2014).

The information of cash flows from financing activities are provided below:

Cash flow from Financing Activities

Particulars 2017

201

6 2015

Commonwealth 10472

162

0 -7875

Westpac 552

457

3 5513

2017 2016 2015

-10000

-5000

0

5000

10000

15000

Commonwealth

Westpac

Particulars 2017 2016 2015

Commonwealth -677 -2032 -1215

Westpac

-

1698 -7245 -18715

2017 2016 2015

-20000

-18000

-16000

-14000

-12000

-10000

-8000

-6000

-4000

-2000

0

Commonwealth

Westpac

There is no trend for the cash flows from investing activities of commonwealth bank whereas

for Westpac bank it is declining (Kieso, 2014).

The information of cash flows from financing activities are provided below:

Cash flow from Financing Activities

Particulars 2017

201

6 2015

Commonwealth 10472

162

0 -7875

Westpac 552

457

3 5513

2017 2016 2015

-10000

-5000

0

5000

10000

15000

Commonwealth

Westpac

The trend of cash flow from financing activities is in opposite direction. The cash flow of

Commonwealth group is increasing whereas it is declining in case of Westpac’s bank (Hubig,

2013).

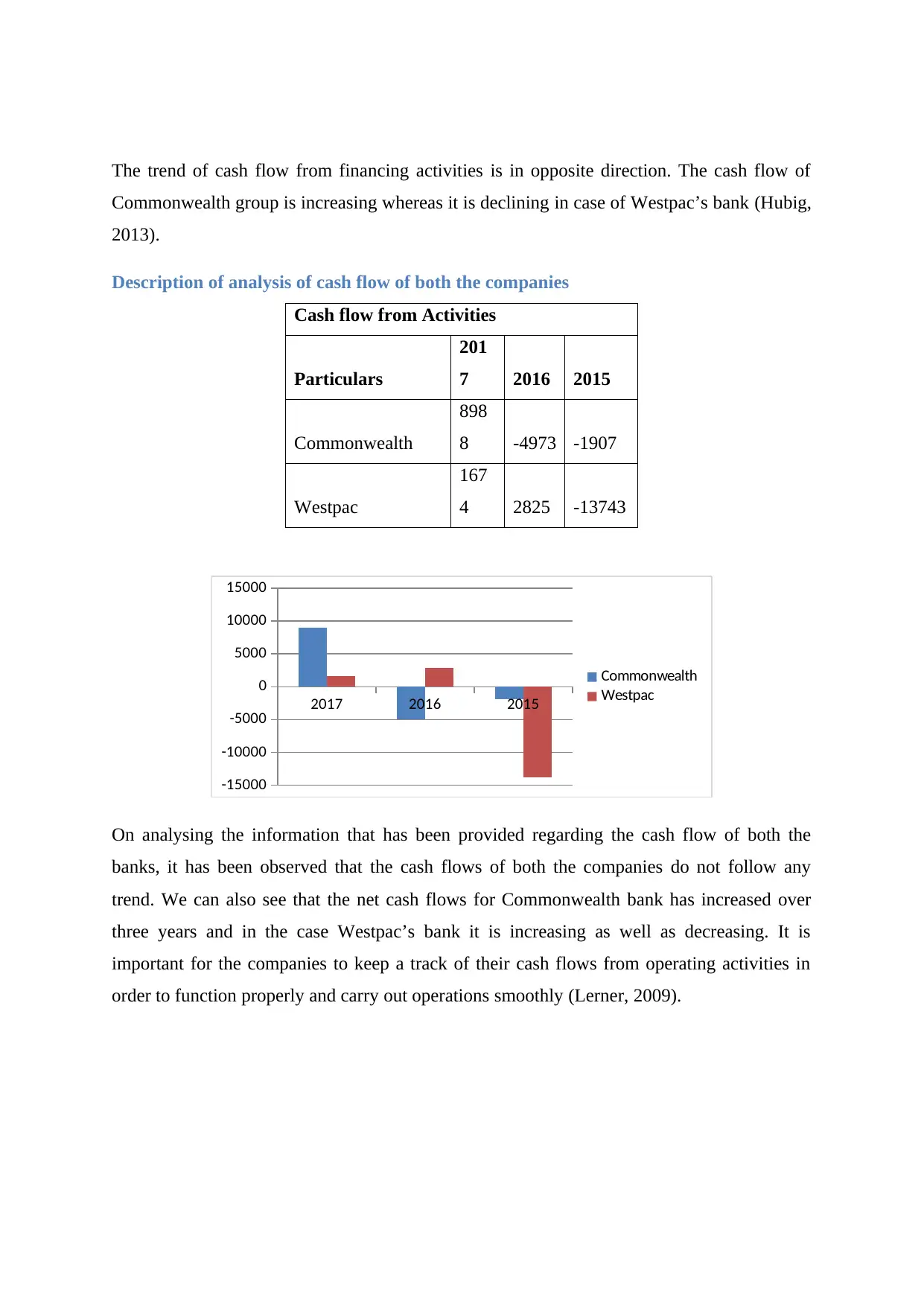

Description of analysis of cash flow of both the companies

Cash flow from Activities

Particulars

201

7 2016 2015

Commonwealth

898

8 -4973 -1907

Westpac

167

4 2825 -13743

2017 2016 2015

-15000

-10000

-5000

0

5000

10000

15000

Commonwealth

Westpac

On analysing the information that has been provided regarding the cash flow of both the

banks, it has been observed that the cash flows of both the companies do not follow any

trend. We can also see that the net cash flows for Commonwealth bank has increased over

three years and in the case Westpac’s bank it is increasing as well as decreasing. It is

important for the companies to keep a track of their cash flows from operating activities in

order to function properly and carry out operations smoothly (Lerner, 2009).

Commonwealth group is increasing whereas it is declining in case of Westpac’s bank (Hubig,

2013).

Description of analysis of cash flow of both the companies

Cash flow from Activities

Particulars

201

7 2016 2015

Commonwealth

898

8 -4973 -1907

Westpac

167

4 2825 -13743

2017 2016 2015

-15000

-10000

-5000

0

5000

10000

15000

Commonwealth

Westpac

On analysing the information that has been provided regarding the cash flow of both the

banks, it has been observed that the cash flows of both the companies do not follow any

trend. We can also see that the net cash flows for Commonwealth bank has increased over

three years and in the case Westpac’s bank it is increasing as well as decreasing. It is

important for the companies to keep a track of their cash flows from operating activities in

order to function properly and carry out operations smoothly (Lerner, 2009).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.