Financial Statement Analysis of Crystal Hotels - Detailed Report

VerifiedAdded on 2023/06/08

|12

|1845

|79

Report

AI Summary

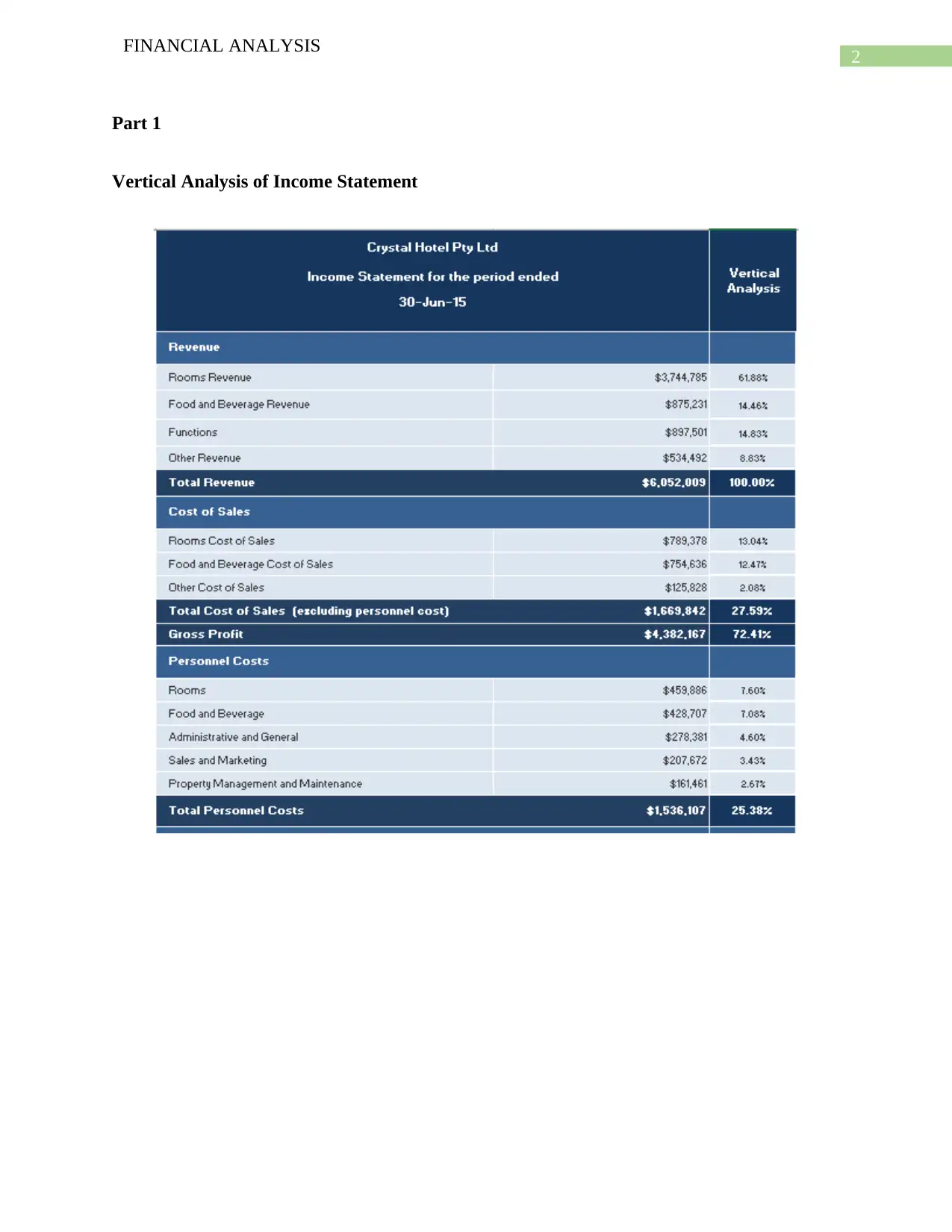

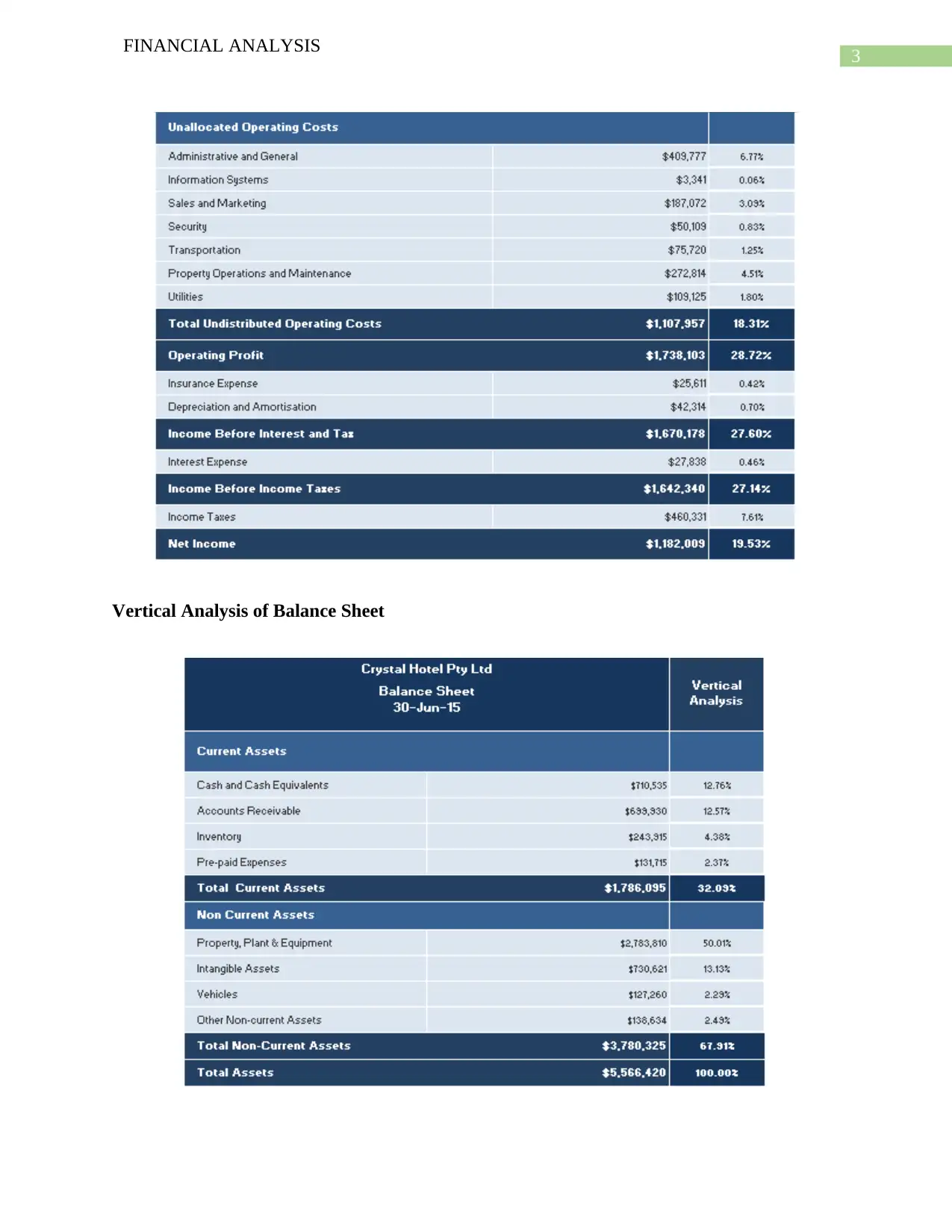

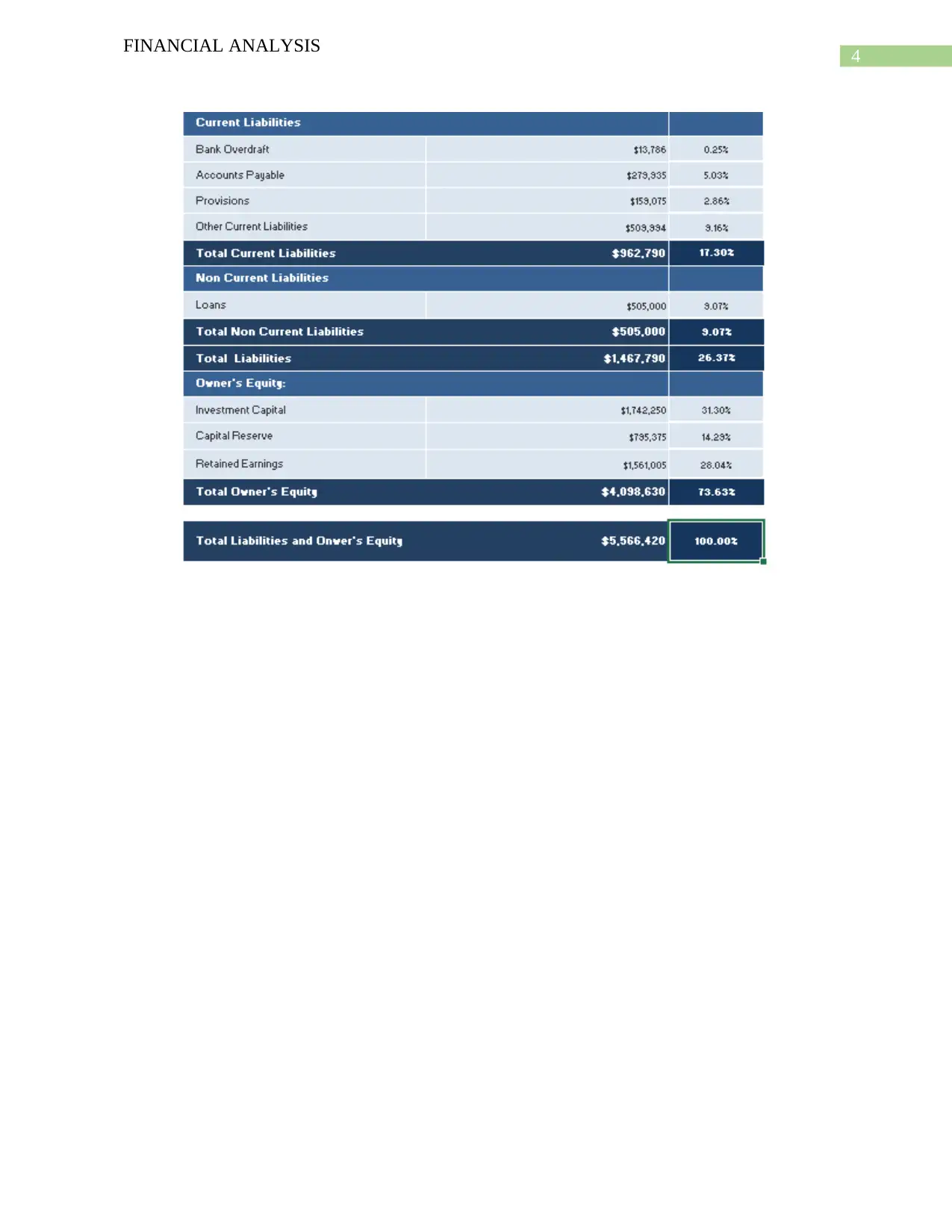

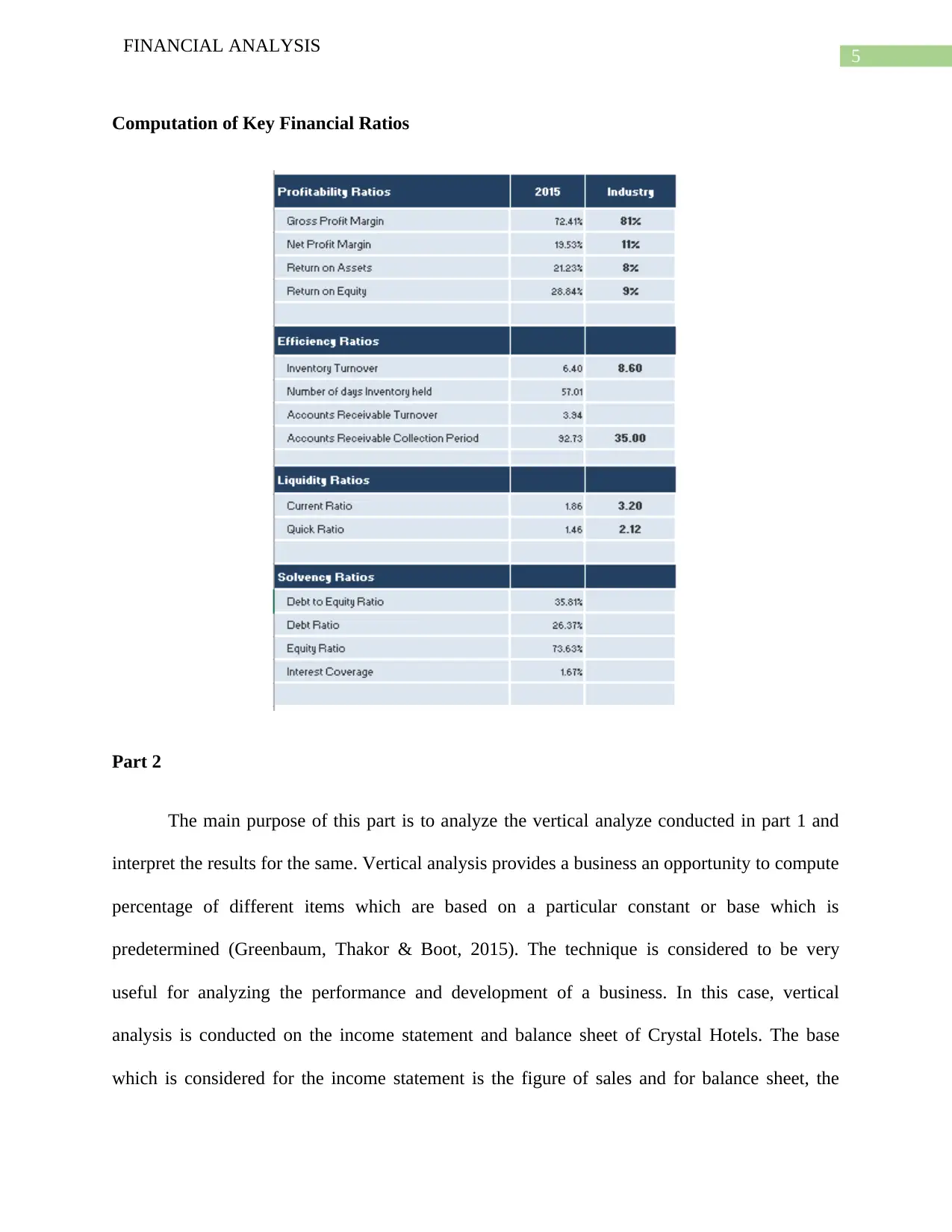

This report provides a financial analysis of Crystal Hotels, employing vertical analysis of both the income statement and balance sheet, alongside key financial ratio computations. The vertical analysis assesses various income statement items as a percentage of total revenue, revealing strengths in room service revenue and areas for improvement in cost of sales and unallocated expenses. Ratio analysis, including profitability, efficiency, and liquidity ratios, highlights the hotel's strong net profit margin and returns on assets and equity, but also identifies concerns with inventory turnover, account receivable periods, and liquidity positions relative to industry averages. The report concludes with recommendations for enhancing food and beverage services, reducing costs, improving debt policies, and balancing debt and equity capital sources to optimize the hotel's financial performance. Desklib offers a range of solved assignments and past papers to aid students in their studies.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

© 2024 | Zucol Services PVT LTD | All rights reserved.