International Finance: Investment Appraisal and Ratio Analysis Report

VerifiedAdded on 2023/06/18

|17

|3692

|468

Report

AI Summary

This report delves into international finance, focusing on the financial analysis of CWIRE LTD and Oxford Biomedica. It includes a comparative analysis of financial ratios such as profitability, liquidity, gearing, and investor ratios for both companies. The report calculates the Weighted Average Cost of Capital (WACC) using the Dividend Valuation Model (DVM) and Capital Asset Pricing Model (CAPM), justifying the selection of one WACC for investment appraisal. It identifies and contrasts traditional (venture capital) and modern (crowdfunding) techniques for raising capital, evaluating their pros and cons. Furthermore, the report explores investment appraisal techniques, providing a comprehensive overview of financial decision-making in an international context. Desklib provides this and other solved assignments for students.

International Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................................3

PART A.........................................................................................................................................................3

Introduction of Proxy Company...............................................................................................................3

Ratios for CWIRE LTD...............................................................................................................................3

Ratios for Oxford Biomedica....................................................................................................................5

PART B.........................................................................................................................................................8

Weighted average cost of capital............................................................................................................8

Identify traditional and modern techniques of raising capital...............................................................10

PART C.......................................................................................................................................................12

Investment appraisal techniques...........................................................................................................12

CONCLUSION.............................................................................................................................................16

REFERENCES..............................................................................................................................................17

INTRODUCTION...........................................................................................................................................3

PART A.........................................................................................................................................................3

Introduction of Proxy Company...............................................................................................................3

Ratios for CWIRE LTD...............................................................................................................................3

Ratios for Oxford Biomedica....................................................................................................................5

PART B.........................................................................................................................................................8

Weighted average cost of capital............................................................................................................8

Identify traditional and modern techniques of raising capital...............................................................10

PART C.......................................................................................................................................................12

Investment appraisal techniques...........................................................................................................12

CONCLUSION.............................................................................................................................................16

REFERENCES..............................................................................................................................................17

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

The administration of money in a worldwide corporation is the subject of international finance. It

demonstrates how to engage on global marketplaces, convert public funds, and benefit from certain

endeavors. International finance is, in reality, an essential component of financial systems. It mostly

addresses concerns of monetary relations between multiple countries. Currency exchange rates, currency

institutions throughout the globe, overseas investment (FDI), and other key topics related to world

monetary administration are all covered under international finance (Zhang, Wang and Hao, 2021. This

report based on the Landtech business which is provided financial services to their customer. From the

various customer one client of Cwire Ltd take consultancy. It is privately owned technology production

based corporation in Corby, England. Another proxy company selected in this report which is Oxford

Biomedica is a genetic and tissue engineering business that focuses on developing gene-based

therapeutics. In this report consist of financial ratios, WACC and investment appraisal techniques.

PART A

Introduction of Proxy Company

Oxford Biomedica engages in the production of biomarker therapeutics and is a genetics and tissue

regeneration firm. It is a component of the FTSE 250 Index and is traded on the London Stock Exchange.

The firm began as a spin-off from Oxford University in 1995. In 1996, it became the object of a stock

offering (IPO) on the Independent Property Sector.

Ratios for CWIRE LTD

Profitability ratio

Net profit ratio: The profitability of a corporation is measured by this proportion. When comparing

Cwire with Oxford BioMedia, it was discovered that Cwire's net income will be 43 percent in 2019 and

2020, whereas Oxford BioMedia's will be 100 percent in 2019 and 99 percent in 2020. This illustrates that

the proxies firm, Oxford BioMedia, has a larger profitability percentage than the benchmarking business,

Cwire. This demonstrates that the proxy financial position meets the criteria and ensures profit margin.

Return on capital employed: This ratio assesses a firm's financial position in terms of revenue creation

and capital use efficiency. The ROCE for Cwire is 43 percent in 2019 and 17 percent in 2020, whereas

the ratio for Oxford BioMedia is 84 percent in 2019 and 78 percent in 2020. This demonstrates that the

proxy firm has strong financial results in comparison to the benchmarking business. Similarly, it is

The administration of money in a worldwide corporation is the subject of international finance. It

demonstrates how to engage on global marketplaces, convert public funds, and benefit from certain

endeavors. International finance is, in reality, an essential component of financial systems. It mostly

addresses concerns of monetary relations between multiple countries. Currency exchange rates, currency

institutions throughout the globe, overseas investment (FDI), and other key topics related to world

monetary administration are all covered under international finance (Zhang, Wang and Hao, 2021. This

report based on the Landtech business which is provided financial services to their customer. From the

various customer one client of Cwire Ltd take consultancy. It is privately owned technology production

based corporation in Corby, England. Another proxy company selected in this report which is Oxford

Biomedica is a genetic and tissue engineering business that focuses on developing gene-based

therapeutics. In this report consist of financial ratios, WACC and investment appraisal techniques.

PART A

Introduction of Proxy Company

Oxford Biomedica engages in the production of biomarker therapeutics and is a genetics and tissue

regeneration firm. It is a component of the FTSE 250 Index and is traded on the London Stock Exchange.

The firm began as a spin-off from Oxford University in 1995. In 1996, it became the object of a stock

offering (IPO) on the Independent Property Sector.

Ratios for CWIRE LTD

Profitability ratio

Net profit ratio: The profitability of a corporation is measured by this proportion. When comparing

Cwire with Oxford BioMedia, it was discovered that Cwire's net income will be 43 percent in 2019 and

2020, whereas Oxford BioMedia's will be 100 percent in 2019 and 99 percent in 2020. This illustrates that

the proxies firm, Oxford BioMedia, has a larger profitability percentage than the benchmarking business,

Cwire. This demonstrates that the proxy financial position meets the criteria and ensures profit margin.

Return on capital employed: This ratio assesses a firm's financial position in terms of revenue creation

and capital use efficiency. The ROCE for Cwire is 43 percent in 2019 and 17 percent in 2020, whereas

the ratio for Oxford BioMedia is 84 percent in 2019 and 78 percent in 2020. This demonstrates that the

proxy firm has strong financial results in comparison to the benchmarking business. Similarly, it is

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

estimated that Oxford BioMedia will exhibit a dropping trend in 2020, with a lower ratio, but it will still

do well in contrast to the benchmark business.

Liquidity ratio

Current ratio: This ratio assesses a liquidity position, indicating how efficient it is or if it has enough

current assets to cover its current liabilities. This ratio may also be used to assess a firm's competence in

terms of analyzing its functional capacity or demonstrating that the organisation has sufficient finances to

satisfy its regular activities. The current ratio for Oxford BioMedia is 1.97 in 2019 and 2.08 in 2020. This

demonstrates a high and increasing current ratio, indicating that the firm's creditworthiness its current

commitments are improving. This demonstrates the company's strong cash situation.

Gearing ratio

Debt equity ratio: The ratio refers to the measuring of lenders', investors', and owners' contributions to the

invested capital by the company. Cwire Ltd will have a ratio of 4% in 2019 and 2020, whereas Oxford

BioMedia will have a ratio of 3.81 (29/76000) in 2019 and 4.60 (52/113000) in 2020. This demonstrates

that the proxy firm's profitability is modest when matched to the benchmarking business. Since the debt

ratio of Oxford BioMedia is dropping from 2019 to 2020, this really is the case. This indicates that the

firm is unable to satisfy the standard.

Investor ratio

Return on equity ratio: This ratio represents the rate of interest that investors would get on their

common stock holdings. In the instance of Cwire, the ratio is 36 percent in 2019, but drops to 14 percent

in 2020. When compared to Oxford BioMedia, the ratio is dropping, albeit at a lesser speed than the

reference business, i.e. 84 percent in 2019 and 77 percent in 2020. This demonstrates that when

contrasted to the comparable firm, the proxy business delivers higher.

Earnings per share: It calculates the amount of net income that will be utilised to pay common

stockholders. An increase in the firm's earnings per share (EPS) indicates that the company is performing

well. When analysing Cwire Ltd, it was discovered that the proportion was decreasing, as it was 360.74 in

2019 but 144.74 in 2020, however in the case of Oxford BioMedia, the ratio was 85.33 in 2019 and

115.684 in 2020. This demonstrates that the proxy firm's result is strong and good when contrasted to the

reference business.

In conclusion, when comparing the financial results of Cwire Ltd (Benchmark business) with

those of Oxford BioMedia (Proxy firm) using accounting ratios, the profitability of Oxford BioMedia

do well in contrast to the benchmark business.

Liquidity ratio

Current ratio: This ratio assesses a liquidity position, indicating how efficient it is or if it has enough

current assets to cover its current liabilities. This ratio may also be used to assess a firm's competence in

terms of analyzing its functional capacity or demonstrating that the organisation has sufficient finances to

satisfy its regular activities. The current ratio for Oxford BioMedia is 1.97 in 2019 and 2.08 in 2020. This

demonstrates a high and increasing current ratio, indicating that the firm's creditworthiness its current

commitments are improving. This demonstrates the company's strong cash situation.

Gearing ratio

Debt equity ratio: The ratio refers to the measuring of lenders', investors', and owners' contributions to the

invested capital by the company. Cwire Ltd will have a ratio of 4% in 2019 and 2020, whereas Oxford

BioMedia will have a ratio of 3.81 (29/76000) in 2019 and 4.60 (52/113000) in 2020. This demonstrates

that the proxy firm's profitability is modest when matched to the benchmarking business. Since the debt

ratio of Oxford BioMedia is dropping from 2019 to 2020, this really is the case. This indicates that the

firm is unable to satisfy the standard.

Investor ratio

Return on equity ratio: This ratio represents the rate of interest that investors would get on their

common stock holdings. In the instance of Cwire, the ratio is 36 percent in 2019, but drops to 14 percent

in 2020. When compared to Oxford BioMedia, the ratio is dropping, albeit at a lesser speed than the

reference business, i.e. 84 percent in 2019 and 77 percent in 2020. This demonstrates that when

contrasted to the comparable firm, the proxy business delivers higher.

Earnings per share: It calculates the amount of net income that will be utilised to pay common

stockholders. An increase in the firm's earnings per share (EPS) indicates that the company is performing

well. When analysing Cwire Ltd, it was discovered that the proportion was decreasing, as it was 360.74 in

2019 but 144.74 in 2020, however in the case of Oxford BioMedia, the ratio was 85.33 in 2019 and

115.684 in 2020. This demonstrates that the proxy firm's result is strong and good when contrasted to the

reference business.

In conclusion, when comparing the financial results of Cwire Ltd (Benchmark business) with

those of Oxford BioMedia (Proxy firm) using accounting ratios, the profitability of Oxford BioMedia

would be higher and more effective when comparing to the benchmark business. It also implies that the

proxy firm is reaching the standard while also delivering strong financial results.

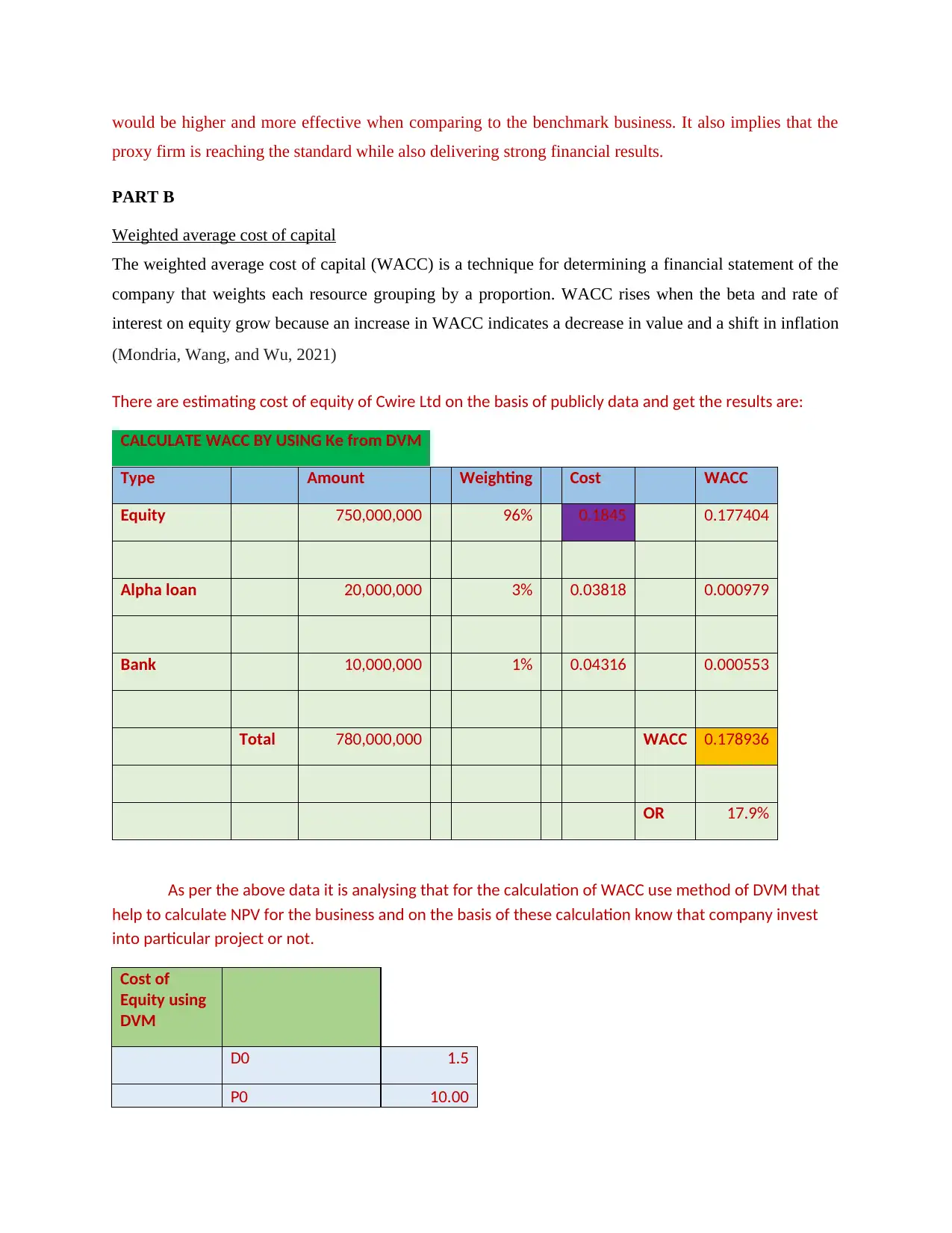

PART B

Weighted average cost of capital

The weighted average cost of capital (WACC) is a technique for determining a financial statement of the

company that weights each resource grouping by a proportion. WACC rises when the beta and rate of

interest on equity grow because an increase in WACC indicates a decrease in value and a shift in inflation

(Mondria, Wang, and Wu, 2021)

There are estimating cost of equity of Cwire Ltd on the basis of publicly data and get the results are:

CALCULATE WACC BY USING Ke from DVM

Type Amount Weighting Cost WACC

Equity 750,000,000 96% 0.1845 0.177404

Alpha loan 20,000,000 3% 0.03818 0.000979

Bank 10,000,000 1% 0.04316 0.000553

Total 780,000,000 WACC 0.178936

OR 17.9%

As per the above data it is analysing that for the calculation of WACC use method of DVM that

help to calculate NPV for the business and on the basis of these calculation know that company invest

into particular project or not.

Cost of

Equity using

DVM

D0 1.5

P0 10.00

proxy firm is reaching the standard while also delivering strong financial results.

PART B

Weighted average cost of capital

The weighted average cost of capital (WACC) is a technique for determining a financial statement of the

company that weights each resource grouping by a proportion. WACC rises when the beta and rate of

interest on equity grow because an increase in WACC indicates a decrease in value and a shift in inflation

(Mondria, Wang, and Wu, 2021)

There are estimating cost of equity of Cwire Ltd on the basis of publicly data and get the results are:

CALCULATE WACC BY USING Ke from DVM

Type Amount Weighting Cost WACC

Equity 750,000,000 96% 0.1845 0.177404

Alpha loan 20,000,000 3% 0.03818 0.000979

Bank 10,000,000 1% 0.04316 0.000553

Total 780,000,000 WACC 0.178936

OR 17.9%

As per the above data it is analysing that for the calculation of WACC use method of DVM that

help to calculate NPV for the business and on the basis of these calculation know that company invest

into particular project or not.

Cost of

Equity using

DVM

D0 1.5

P0 10.00

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

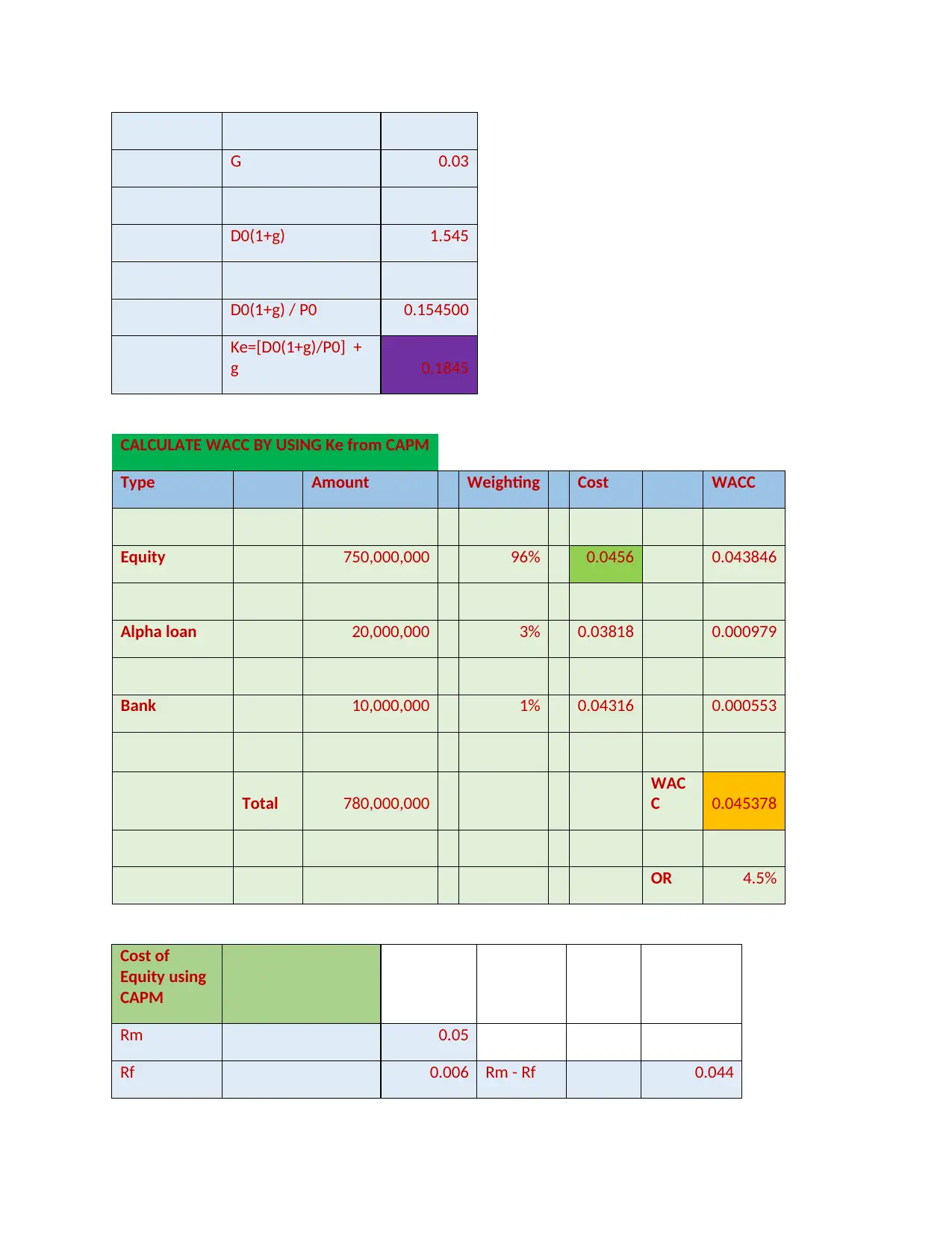

G 0.03

D0(1+g) 1.545

D0(1+g) / P0 0.154500

Ke=[D0(1+g)/P0] +

g 0.1845

CALCULATE WACC BY USING Ke from CAPM

Type Amount Weighting Cost WACC

Equity 750,000,000 96% 0.0456 0.043846

Alpha loan 20,000,000 3% 0.03818 0.000979

Bank 10,000,000 1% 0.04316 0.000553

Total 780,000,000

WAC

C 0.045378

OR 4.5%

Cost of

Equity using

CAPM

Rm 0.05

Rf 0.006 Rm - Rf 0.044

D0(1+g) 1.545

D0(1+g) / P0 0.154500

Ke=[D0(1+g)/P0] +

g 0.1845

CALCULATE WACC BY USING Ke from CAPM

Type Amount Weighting Cost WACC

Equity 750,000,000 96% 0.0456 0.043846

Alpha loan 20,000,000 3% 0.03818 0.000979

Bank 10,000,000 1% 0.04316 0.000553

Total 780,000,000

WAC

C 0.045378

OR 4.5%

Cost of

Equity using

CAPM

Rm 0.05

Rf 0.006 Rm - Rf 0.044

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

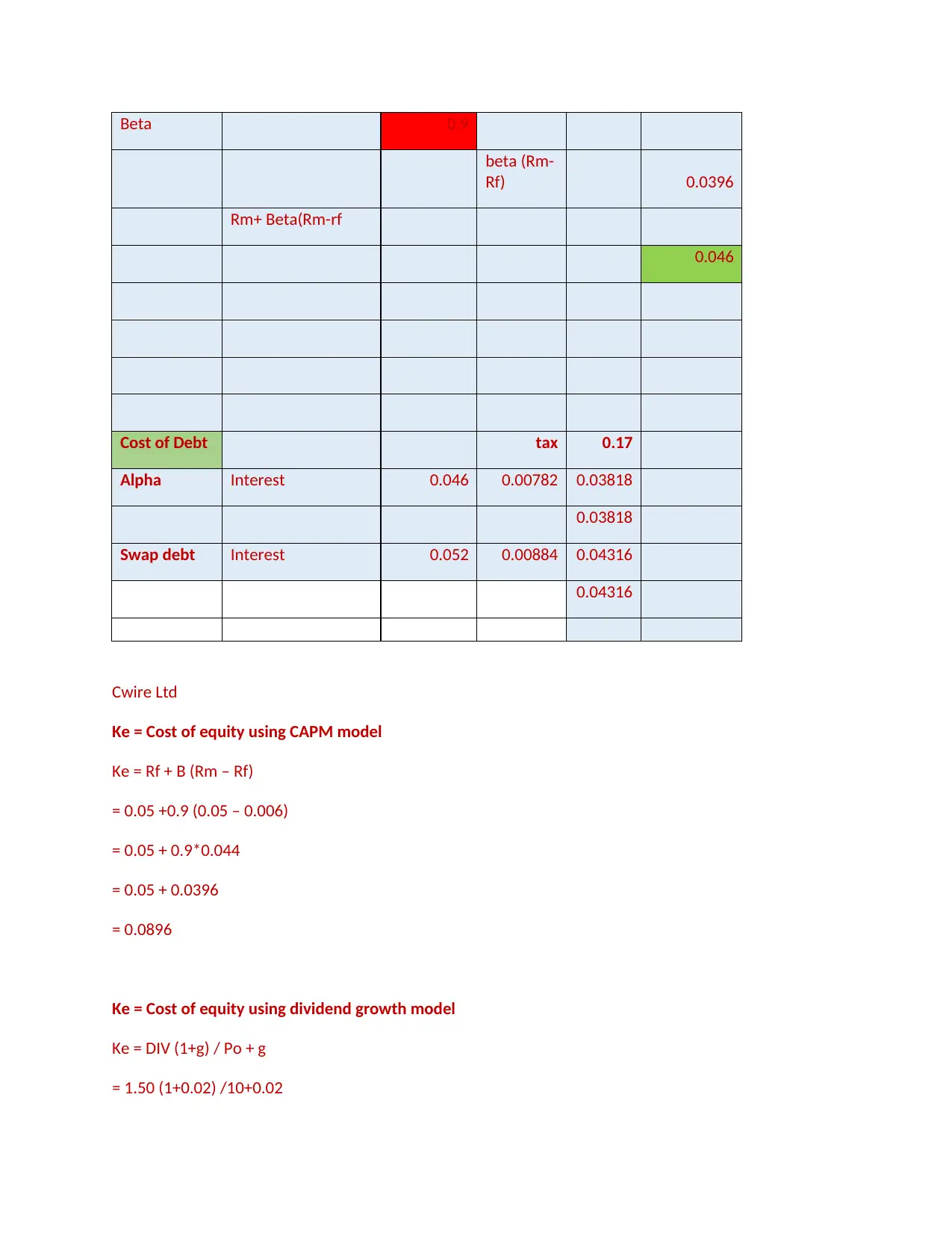

Beta 0.9

beta (Rm-

Rf) 0.0396

Rm+ Beta(Rm-rf

0.046

Cost of Debt tax 0.17

Alpha Interest 0.046 0.00782 0.03818

0.03818

Swap debt Interest 0.052 0.00884 0.04316

0.04316

Cwire Ltd

Ke = Cost of equity using CAPM model

Ke = Rf + B (Rm – Rf)

= 0.05 +0.9 (0.05 – 0.006)

= 0.05 + 0.9*0.044

= 0.05 + 0.0396

= 0.0896

Ke = Cost of equity using dividend growth model

Ke = DIV (1+g) / Po + g

= 1.50 (1+0.02) /10+0.02

beta (Rm-

Rf) 0.0396

Rm+ Beta(Rm-rf

0.046

Cost of Debt tax 0.17

Alpha Interest 0.046 0.00782 0.03818

0.03818

Swap debt Interest 0.052 0.00884 0.04316

0.04316

Cwire Ltd

Ke = Cost of equity using CAPM model

Ke = Rf + B (Rm – Rf)

= 0.05 +0.9 (0.05 – 0.006)

= 0.05 + 0.9*0.044

= 0.05 + 0.0396

= 0.0896

Ke = Cost of equity using dividend growth model

Ke = DIV (1+g) / Po + g

= 1.50 (1+0.02) /10+0.02

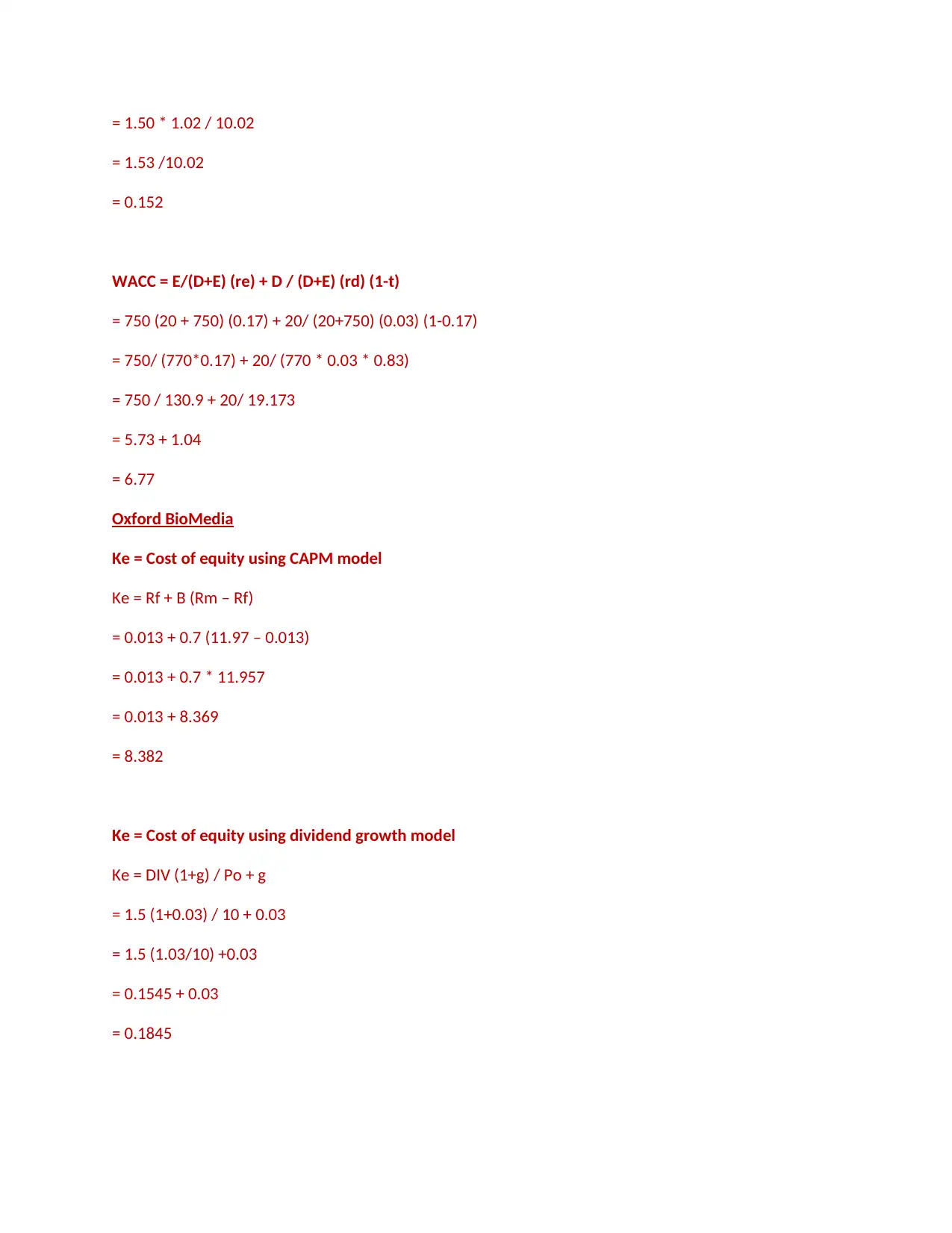

= 1.50 * 1.02 / 10.02

= 1.53 /10.02

= 0.152

WACC = E/(D+E) (re) + D / (D+E) (rd) (1-t)

= 750 (20 + 750) (0.17) + 20/ (20+750) (0.03) (1-0.17)

= 750/ (770*0.17) + 20/ (770 * 0.03 * 0.83)

= 750 / 130.9 + 20/ 19.173

= 5.73 + 1.04

= 6.77

Oxford BioMedia

Ke = Cost of equity using CAPM model

Ke = Rf + B (Rm – Rf)

= 0.013 + 0.7 (11.97 – 0.013)

= 0.013 + 0.7 * 11.957

= 0.013 + 8.369

= 8.382

Ke = Cost of equity using dividend growth model

Ke = DIV (1+g) / Po + g

= 1.5 (1+0.03) / 10 + 0.03

= 1.5 (1.03/10) +0.03

= 0.1545 + 0.03

= 0.1845

= 1.53 /10.02

= 0.152

WACC = E/(D+E) (re) + D / (D+E) (rd) (1-t)

= 750 (20 + 750) (0.17) + 20/ (20+750) (0.03) (1-0.17)

= 750/ (770*0.17) + 20/ (770 * 0.03 * 0.83)

= 750 / 130.9 + 20/ 19.173

= 5.73 + 1.04

= 6.77

Oxford BioMedia

Ke = Cost of equity using CAPM model

Ke = Rf + B (Rm – Rf)

= 0.013 + 0.7 (11.97 – 0.013)

= 0.013 + 0.7 * 11.957

= 0.013 + 8.369

= 8.382

Ke = Cost of equity using dividend growth model

Ke = DIV (1+g) / Po + g

= 1.5 (1+0.03) / 10 + 0.03

= 1.5 (1.03/10) +0.03

= 0.1545 + 0.03

= 0.1845

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Identify traditional and modern techniques of raising capital.

Based on the quantity of money necessary and the time for which it is necessary, a firm might pick

from a variety of financing options. Traditional sources, ownership capital, and non-ownership capital are

the 3 kinds of financing available. Internal resources have always been a government's primary funding

source. Internal factors might include a corporate resources, factorization or invoicing discounting,

retirement funds, and earnings that haven't been re-invested or given to owners. Working capital is a

quick funding source that is used to fund a business's day-to-day operations, such as employees, leases,

and purchases for natural resources (Karimov and Cheng, 2021).

Traditional Technique

Venture capital: Venture capital is a type of funding for businesses as well as a financial

instrument for rich people and investment banks. To put it another way, it's a method for businesses to get

cash fast while individuals build their money over time. Venture capital businesses raise cash from

shareholders to form venture funds, which can be used to purchase shares in onset or delayed enterprises,

dependent on the company's expertise. Those funds are tied till a liquid event occurs, like the business

being bought or going public, at which point VCs benefit on their upfront outlay.

Pros:

Invest a huge quantity of money in a beginning or a local company: A start-up or a local company

needs a significant sum of money to get their idea off the ground. The firm will need capital and a

significant quantity of working capital to get off to a solid start (Kammoun and Power, 2021).

A venture capitalist, in addition to providing funds, also gives knowledge, leadership

responsibilities, and coaching expertise. Furthermore, a venture investor may serve as a valuable

company counselor. Many choices, including as finance management and managers, can be aided

by a venture capital firms.

Cons:

A venture capital lends cash to a company and then obtains shares in the company in exchange

for those funding. As a result, the previous residents' and investors' ownership and control

interests have been diluted.

Obtaining funding from a venture capitalist is a moment and laborious procedure. Most of this

investigative work on the firm and the present proprietors would be done by the venturing

investor. In addition, the capitalists would do a risk assessment and industry research on the

company they intends to engage in.

Based on the quantity of money necessary and the time for which it is necessary, a firm might pick

from a variety of financing options. Traditional sources, ownership capital, and non-ownership capital are

the 3 kinds of financing available. Internal resources have always been a government's primary funding

source. Internal factors might include a corporate resources, factorization or invoicing discounting,

retirement funds, and earnings that haven't been re-invested or given to owners. Working capital is a

quick funding source that is used to fund a business's day-to-day operations, such as employees, leases,

and purchases for natural resources (Karimov and Cheng, 2021).

Traditional Technique

Venture capital: Venture capital is a type of funding for businesses as well as a financial

instrument for rich people and investment banks. To put it another way, it's a method for businesses to get

cash fast while individuals build their money over time. Venture capital businesses raise cash from

shareholders to form venture funds, which can be used to purchase shares in onset or delayed enterprises,

dependent on the company's expertise. Those funds are tied till a liquid event occurs, like the business

being bought or going public, at which point VCs benefit on their upfront outlay.

Pros:

Invest a huge quantity of money in a beginning or a local company: A start-up or a local company

needs a significant sum of money to get their idea off the ground. The firm will need capital and a

significant quantity of working capital to get off to a solid start (Kammoun and Power, 2021).

A venture capitalist, in addition to providing funds, also gives knowledge, leadership

responsibilities, and coaching expertise. Furthermore, a venture investor may serve as a valuable

company counselor. Many choices, including as finance management and managers, can be aided

by a venture capital firms.

Cons:

A venture capital lends cash to a company and then obtains shares in the company in exchange

for those funding. As a result, the previous residents' and investors' ownership and control

interests have been diluted.

Obtaining funding from a venture capitalist is a moment and laborious procedure. Most of this

investigative work on the firm and the present proprietors would be done by the venturing

investor. In addition, the capitalists would do a risk assessment and industry research on the

company they intends to engage in.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Modern technique

Crowd funding: Individuals may now communicate their issues on an engaging media network

thanks to modern technologies. Entrepreneurs may utilize financial capital to propose their company

concepts or issues to a network of investors or people who want to help their efforts. It generally works

like this: a person decides an entrepreneurship on a crowd-funding site, where he reveals his company

idea and development prospects. If crowd funders on the site like concept, they'll give a public

willingness to sustainability for strategic plan and give money (Tanjung and Affiah, 2021).

Pros

Crowd-funding simply generates public stake in the organization, allowing you doing some free

advertising while also raising funds for it.

Crowd-funding takes away the complexities of putting their company in the disposal of an investment or

a brokerage and gives it to regular people on the crowd-funding site (Wang and et.al, 2021).

Cons

When someone or individuals are presenting the same company concept as you, the fierce rivalry implicit

in crowd-funding sites might be tough to overcome.

If company pitch isn't as strong as the team's, they set - up may be disregarded or discarded (He, Fu and

Lucey, 2021).

Businesses can obtain funds using either debt or equity capital, with the cost of debt often being cheaper

than the cost of equity due to debt's accountability. Debt capital takes the form of mortgages or bond fund

issuance. Cash is exchanged for firm participation in the direct equity capital, which is usually in the

shape of securities. Debt holders often charge interest to firms, whereas equity investors rely on looking

to increase or dividends to make a profit. When opposed to ordinary stock, preferred equity has a superior

right on a property, lowering the price of financing.

Venture capital is good way for raising capital for Cwire Ltd because in this method has less risk

and help to manage working capital properly.

Crowd funding: Individuals may now communicate their issues on an engaging media network

thanks to modern technologies. Entrepreneurs may utilize financial capital to propose their company

concepts or issues to a network of investors or people who want to help their efforts. It generally works

like this: a person decides an entrepreneurship on a crowd-funding site, where he reveals his company

idea and development prospects. If crowd funders on the site like concept, they'll give a public

willingness to sustainability for strategic plan and give money (Tanjung and Affiah, 2021).

Pros

Crowd-funding simply generates public stake in the organization, allowing you doing some free

advertising while also raising funds for it.

Crowd-funding takes away the complexities of putting their company in the disposal of an investment or

a brokerage and gives it to regular people on the crowd-funding site (Wang and et.al, 2021).

Cons

When someone or individuals are presenting the same company concept as you, the fierce rivalry implicit

in crowd-funding sites might be tough to overcome.

If company pitch isn't as strong as the team's, they set - up may be disregarded or discarded (He, Fu and

Lucey, 2021).

Businesses can obtain funds using either debt or equity capital, with the cost of debt often being cheaper

than the cost of equity due to debt's accountability. Debt capital takes the form of mortgages or bond fund

issuance. Cash is exchanged for firm participation in the direct equity capital, which is usually in the

shape of securities. Debt holders often charge interest to firms, whereas equity investors rely on looking

to increase or dividends to make a profit. When opposed to ordinary stock, preferred equity has a superior

right on a property, lowering the price of financing.

Venture capital is good way for raising capital for Cwire Ltd because in this method has less risk

and help to manage working capital properly.

PART C

Investment appraisal techniques

Payback period: Payback period is a method of valuing capital investments considering the time it

will take to recoup your original cost. Another of the simplest private capital assessment methodologies is

the payback period. Especially opposed to enterprises with longer payback periods, businesses with short

repayment time frames are typically favored for investments (Cumming, Meoli and Vismara, 2021).

Project A -

Year Net Cash flows Cumulative cash flows

1 45000 45000.000

2 45000 90000.000

3 35000 125000.000

4 70000

5 82000

Initial Investment 170000

Payback period = 3 years + [(170000 - 125000) / 70000 * 12

months

3 Years + (45000 / 70000) * 12 months

3 years + (0.643 * 12 months)

3 years + 7.71 months

Net present value: After normal debt payments are satisfied, this strategic asset valuation approach

assesses the cash in-flow, either surplus or deficiency. The goal of all private capital assessments is to

achieve a positive net present value (NPV). The net present value (NPV) is a quantitative computation

incorporating cash flows at a certain point in time 't' and a discount rate, i.e. (t – upfront capital

expenditure). As a result, the leverage ratio and the net present value have an inversely relationship. The

present value of assets would be reduced if the leverage ratio was too large. Over term, a cost of

borrowing raises rebates, but most private capital evaluations are apprehensive of such a rise (Meisenzahl,

Niepmann and Schmidt-Eisenlohr, 2021).

Investment appraisal techniques

Payback period: Payback period is a method of valuing capital investments considering the time it

will take to recoup your original cost. Another of the simplest private capital assessment methodologies is

the payback period. Especially opposed to enterprises with longer payback periods, businesses with short

repayment time frames are typically favored for investments (Cumming, Meoli and Vismara, 2021).

Project A -

Year Net Cash flows Cumulative cash flows

1 45000 45000.000

2 45000 90000.000

3 35000 125000.000

4 70000

5 82000

Initial Investment 170000

Payback period = 3 years + [(170000 - 125000) / 70000 * 12

months

3 Years + (45000 / 70000) * 12 months

3 years + (0.643 * 12 months)

3 years + 7.71 months

Net present value: After normal debt payments are satisfied, this strategic asset valuation approach

assesses the cash in-flow, either surplus or deficiency. The goal of all private capital assessments is to

achieve a positive net present value (NPV). The net present value (NPV) is a quantitative computation

incorporating cash flows at a certain point in time 't' and a discount rate, i.e. (t – upfront capital

expenditure). As a result, the leverage ratio and the net present value have an inversely relationship. The

present value of assets would be reduced if the leverage ratio was too large. Over term, a cost of

borrowing raises rebates, but most private capital evaluations are apprehensive of such a rise (Meisenzahl,

Niepmann and Schmidt-Eisenlohr, 2021).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.