Financial Analysis of Two Companies

VerifiedAdded on 2020/03/23

|8

|2385

|45

AI Summary

This assignment provides a comparative financial analysis of two companies. It calculates various financial ratios including liquidity (current ratio, quick ratio), profitability (profit margin, return on equity), and solvency (debt-to-equity ratio, debt ratio). The analysis reveals insights into the financial performance and health of each company, highlighting strengths and weaknesses based on calculated ratios.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Financial Analysis

ERM Electricity Limited vs. Mercury NZ Limited

[Type the abstract of the document here. The abstract is typically a short summary of the contents

of the document. Type the abstract of the document here. The abstract is typically a short

summary of the contents of the document.]

ERM Electricity Limited vs. Mercury NZ Limited

[Type the abstract of the document here. The abstract is typically a short summary of the contents

of the document. Type the abstract of the document here. The abstract is typically a short

summary of the contents of the document.]

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Question 1

Cash conversion cycle (CCC) is the time taken to convert the investment tied up in inventory

into cash. The cash conversion cycle for both the companies is as below:

2015 2016

EPW -7.8 days -5.02 days

MCY -10.2 days -5.43 days

(Morningstar, ERM Power Limited)

We see that EPW has a negative cash conversion cycle for the years 2015 and 2016. This

shows working capital efficiency as a negative cycle is desirable. The company has more

days of payables outstanding than the combined days of inventory and receivables

outstanding. This means ERM is taking more time to pay its suppliers and it is giving a credit

of lesser period and also its inventory is fast converting into sales. However, the cycle has

increased from 2015 to 2016. This has been majorly on accounting of an increase in the

receivables as the days outstanding receivables increased from 33 days to 43 days. The

receivables have increased due to an increase in loan in both Australia and US.

Mercury NZ Limited’s CCC is also negative for both the years because the day’s payables

outstanding are more than the day’s inventory and receivables outstanding. However, the

CCC has reduced in 2016 due to a higher increased inventory and receivables costs as

compared to payables cost. There was an increase in inventory of Consumables stores to $31

million (2015:$22 million) and Meter stock to $14 million (2015: $22 million). The

receivables were high due to a decrease in cash flow from sale of electricity and metering

services by $20 million as compared to 2015.

Question 2

Capital Structure is the mix of debt and equity in the company’s invested capital. The ratios

used to measure the same are debt to equity ratio and debt ratio.

2015 2016 2015 2016

EPW MCY

Debt to Equity ratio 76% 47% 35% 36%

Debt ratio 65% 62% 46% 46%

(Morningstar, Mercury NZ Limited)

Cash conversion cycle (CCC) is the time taken to convert the investment tied up in inventory

into cash. The cash conversion cycle for both the companies is as below:

2015 2016

EPW -7.8 days -5.02 days

MCY -10.2 days -5.43 days

(Morningstar, ERM Power Limited)

We see that EPW has a negative cash conversion cycle for the years 2015 and 2016. This

shows working capital efficiency as a negative cycle is desirable. The company has more

days of payables outstanding than the combined days of inventory and receivables

outstanding. This means ERM is taking more time to pay its suppliers and it is giving a credit

of lesser period and also its inventory is fast converting into sales. However, the cycle has

increased from 2015 to 2016. This has been majorly on accounting of an increase in the

receivables as the days outstanding receivables increased from 33 days to 43 days. The

receivables have increased due to an increase in loan in both Australia and US.

Mercury NZ Limited’s CCC is also negative for both the years because the day’s payables

outstanding are more than the day’s inventory and receivables outstanding. However, the

CCC has reduced in 2016 due to a higher increased inventory and receivables costs as

compared to payables cost. There was an increase in inventory of Consumables stores to $31

million (2015:$22 million) and Meter stock to $14 million (2015: $22 million). The

receivables were high due to a decrease in cash flow from sale of electricity and metering

services by $20 million as compared to 2015.

Question 2

Capital Structure is the mix of debt and equity in the company’s invested capital. The ratios

used to measure the same are debt to equity ratio and debt ratio.

2015 2016 2015 2016

EPW MCY

Debt to Equity ratio 76% 47% 35% 36%

Debt ratio 65% 62% 46% 46%

(Morningstar, Mercury NZ Limited)

ERM has more of debt as compared to equity in 2015 and more equity than debt in 2016. The

equity has increased in 2016 as a result of the cash flow hedge reserve recognised as part of

equity. The company uses cash flow hedges to hedge price exposures in electricity industry in

Australia (Limited E. P., 2016) Also there has been a reduction in debt by 8% as the company

has repaid part of its long term debt. The debt ratio has remained more or less stable in both

the years. A debt ratio of 65% means that the company has more liabilities than assets and

hence can be considered as risky. The ratio is high as compared to industry average of 45%

which means the company has more liabilities than assets.

Mercury has a lower debt ratio and equity to debt ratio. With regards to the equity to debt

ratio, the company has higher equity than debt and the ratio has remained more or less the

same in both the years. The debt ratio has also remained stable at 45% in both years and is as

per the industry average. The company has more assets as compared to liabilities and the

assets have further increased in 2016 by $27 million due to revaluation of the generation

assets a capital expenditure of $72 million. This shows the company is less risky as compared

to ERM.

Question 3

DuPont analysis is an analysis of the profitability of a company focusing on the return

available to shareholders. The ratio for both companies is as follow:

2015 2016

EPW 29% 11%

MCY 4% 5%

ERM has a high return on equity in both the years but the return has decreased in 2016. This

is as a result of the fall in profit margins. The net income has decreased by 54% due to fall in

the revenue, increased operating costs in the form of depreciation and finance costs resulting

from the operations in the US. Also there was a reduction in the interest income. The total

asset turnover increased marginally as the increase in revenue was higher than the increase in

total assets. For every dollar invested in assets, the company is able to generate $2 revenue.

The company is well leveraged with capital structure comprising more debt than equity.

Mercury has lower return on equity; however, the return has increased by 1% in 2016. This is

because of an increase in the profit margin. The profit margin is higher than ERM. The

equity has increased in 2016 as a result of the cash flow hedge reserve recognised as part of

equity. The company uses cash flow hedges to hedge price exposures in electricity industry in

Australia (Limited E. P., 2016) Also there has been a reduction in debt by 8% as the company

has repaid part of its long term debt. The debt ratio has remained more or less stable in both

the years. A debt ratio of 65% means that the company has more liabilities than assets and

hence can be considered as risky. The ratio is high as compared to industry average of 45%

which means the company has more liabilities than assets.

Mercury has a lower debt ratio and equity to debt ratio. With regards to the equity to debt

ratio, the company has higher equity than debt and the ratio has remained more or less the

same in both the years. The debt ratio has also remained stable at 45% in both years and is as

per the industry average. The company has more assets as compared to liabilities and the

assets have further increased in 2016 by $27 million due to revaluation of the generation

assets a capital expenditure of $72 million. This shows the company is less risky as compared

to ERM.

Question 3

DuPont analysis is an analysis of the profitability of a company focusing on the return

available to shareholders. The ratio for both companies is as follow:

2015 2016

EPW 29% 11%

MCY 4% 5%

ERM has a high return on equity in both the years but the return has decreased in 2016. This

is as a result of the fall in profit margins. The net income has decreased by 54% due to fall in

the revenue, increased operating costs in the form of depreciation and finance costs resulting

from the operations in the US. Also there was a reduction in the interest income. The total

asset turnover increased marginally as the increase in revenue was higher than the increase in

total assets. For every dollar invested in assets, the company is able to generate $2 revenue.

The company is well leveraged with capital structure comprising more debt than equity.

Mercury has lower return on equity; however, the return has increased by 1% in 2016. This is

because of an increase in the profit margin. The profit margin is higher than ERM. The

company’s profits increased as a result of very high geothermal generation at 2830 Wh. And

benefit of replacement of Turbine at Nga Awa Purua. Also there were high impairment costs

in 2015 resulting in lower profits. The total assets turnover is below 1 for both years and the

financial leverage has also remained at a constant level of 1.85 for both the years. Even

though the electricity sales have increased, the assets have also increased in the same

proportion.

As far as return on equity is concerned, ERM has a better profitability with higher returns for

equity shareholders. The returns on equity are high for ERM because they have low equity

and more debt in their balance sheet and also they are efficiently utilizing their assets in

generating sales. ERM has very low profit margin as compared to Mercury and hence would

require working on its profitability to further improve its profitability. The company can do

so by increasing their sales and also working on reducing their operating costs. On the other

hand, Mercury has an impressive profit margin but they have a very poor total assets

turnover. The company has large amount of assets at its disposal but it is not using it

efficiently to generate sales. Thus, Mercury should work towards better asset utilisation.

Question 4

The price earnings ratio and market to book ratios are measures of the investment

performance of a company. The ratios for both the companies are as below:

2015 2016 2015 2016

EPW MCY

Price earnings ratio 0.06 0.04 0.27 0.25

Market to book ratio 1.76 0.44 1.18 1.28

The price earnings ratio for ERM is very low in both the years because the share price is low

as compared to the company’s earnings. The ratio has decreased in 2016 as a result of a

decrease in the share price resulting from decreased EPS. The fall in share price is more than

the fall in EPS. The market to book ratio has decreased in 2016. This is because the market

value has decreased and book value has decreased. The company’s market value has

decreased as the price of share has decreased. The share price has fallen due to falling

earnings on account of Oakey power station and lower margins as competition increases

(Newman, 2016). The company has good future prospects as the price earnings ratio is very

benefit of replacement of Turbine at Nga Awa Purua. Also there were high impairment costs

in 2015 resulting in lower profits. The total assets turnover is below 1 for both years and the

financial leverage has also remained at a constant level of 1.85 for both the years. Even

though the electricity sales have increased, the assets have also increased in the same

proportion.

As far as return on equity is concerned, ERM has a better profitability with higher returns for

equity shareholders. The returns on equity are high for ERM because they have low equity

and more debt in their balance sheet and also they are efficiently utilizing their assets in

generating sales. ERM has very low profit margin as compared to Mercury and hence would

require working on its profitability to further improve its profitability. The company can do

so by increasing their sales and also working on reducing their operating costs. On the other

hand, Mercury has an impressive profit margin but they have a very poor total assets

turnover. The company has large amount of assets at its disposal but it is not using it

efficiently to generate sales. Thus, Mercury should work towards better asset utilisation.

Question 4

The price earnings ratio and market to book ratios are measures of the investment

performance of a company. The ratios for both the companies are as below:

2015 2016 2015 2016

EPW MCY

Price earnings ratio 0.06 0.04 0.27 0.25

Market to book ratio 1.76 0.44 1.18 1.28

The price earnings ratio for ERM is very low in both the years because the share price is low

as compared to the company’s earnings. The ratio has decreased in 2016 as a result of a

decrease in the share price resulting from decreased EPS. The fall in share price is more than

the fall in EPS. The market to book ratio has decreased in 2016. This is because the market

value has decreased and book value has decreased. The company’s market value has

decreased as the price of share has decreased. The share price has fallen due to falling

earnings on account of Oakey power station and lower margins as competition increases

(Newman, 2016). The company has good future prospects as the price earnings ratio is very

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

low. A decrease in market to book value means that investors do not view the company as

profitable

The price earnings ratio of Mercury has remained almost stable for the two years at 0.26 as

both the EPS and the share price have increased but EPS has increased at a higher rate. The

market to book ratio has increased marginally in 2016 due to an increase in the market value.

The market value has increased as a result of an increase in the share price. The book value

has also increased but at a lower rate. Even Mercury has a low price earnings ratio which

means the future prospects are good. Also an increase in market to book value means the

investors view the company with good profitability.

Based on the analysis of the capital structure ratios and the profitability ratios, it is

recommended that a potential investor should invest in shares of Mercury NZ Limited and

should refrain from buying or sell the shares of ERM Electricity Limited. This is because

Mercury has a debt ratio of 45% which is as per industry standards and also shows the

stability of the company, whereas ERM has debt ratio of more than 50% which shows high

amount of leverage and this may pose threat to the stability of the company. Mercury uses its

strong cash balance to fund its capital expenditures whereas ERM relies heavily on debt.

Though the return on equity is higher for ERM as per DuPont analysis but that is because of

the high amount of leverage. The profitability of ERM is very low at average 3% whereas the

profitability of Mercury is good at approx.10%. Mercury is currently performing poorly as far

as the utilisation of its assets for revenue generation is concerned, however the company is in

the process of selling off non -core land to improve profitability and the capital investments

being made by the company currently are to improve operational efficiency and increase the

reliability of the key stations under its technological advancement program (Limited M. N.,

2016)Moreover the electricity market of New Zealand is relatively healthy with increasing

demands whereas the Australian electricity market has is highly competitive leading to lower

margins. The future prospects of Mercury look better than ERM and hence it is recommended

to invest in Mercury.

Bibliography

Limited, E. P. (2016). ERM Power Limited, Annual Financial Report for the Year Ended 30 June 2016.

Australia: ERM Power Limited.

profitable

The price earnings ratio of Mercury has remained almost stable for the two years at 0.26 as

both the EPS and the share price have increased but EPS has increased at a higher rate. The

market to book ratio has increased marginally in 2016 due to an increase in the market value.

The market value has increased as a result of an increase in the share price. The book value

has also increased but at a lower rate. Even Mercury has a low price earnings ratio which

means the future prospects are good. Also an increase in market to book value means the

investors view the company with good profitability.

Based on the analysis of the capital structure ratios and the profitability ratios, it is

recommended that a potential investor should invest in shares of Mercury NZ Limited and

should refrain from buying or sell the shares of ERM Electricity Limited. This is because

Mercury has a debt ratio of 45% which is as per industry standards and also shows the

stability of the company, whereas ERM has debt ratio of more than 50% which shows high

amount of leverage and this may pose threat to the stability of the company. Mercury uses its

strong cash balance to fund its capital expenditures whereas ERM relies heavily on debt.

Though the return on equity is higher for ERM as per DuPont analysis but that is because of

the high amount of leverage. The profitability of ERM is very low at average 3% whereas the

profitability of Mercury is good at approx.10%. Mercury is currently performing poorly as far

as the utilisation of its assets for revenue generation is concerned, however the company is in

the process of selling off non -core land to improve profitability and the capital investments

being made by the company currently are to improve operational efficiency and increase the

reliability of the key stations under its technological advancement program (Limited M. N.,

2016)Moreover the electricity market of New Zealand is relatively healthy with increasing

demands whereas the Australian electricity market has is highly competitive leading to lower

margins. The future prospects of Mercury look better than ERM and hence it is recommended

to invest in Mercury.

Bibliography

Limited, E. P. (2016). ERM Power Limited, Annual Financial Report for the Year Ended 30 June 2016.

Australia: ERM Power Limited.

Limited, M. N. (2016). 2016 Annual Report, Mercury. New Zealand: Mercury NZ Limited.

Morningstar. (n.d.). ERM Power Limited. Retrieved September 28, 2017, from Morningstar

DatAnalysis Premium:

http://datanalysis.morningstar.com.au.ezproxy.uws.edu.au/ftl/company/profitloss?

ASXCode=EPW&rt=A&sy=2007-01-01&ey=2017-12-31&xtm-licensee=datpremium

Morningstar. (n.d.). Mercury NZ Limited. Retrieved September 28, 2017, from Morningstar

DatAnalysis Premium:

http://datanalysis.morningstar.com.au.ezproxy.uws.edu.au/af/company/corpdetails?

ASXCode=MCY-NZ&xtm-licensee=datpremium

Newman, R. (2016, June 20). CRASH! Here’s why the ERM Power Ltd share price crashed 22% today.

Retrieved September 27, 2017, from The Motley Fool:

https://www.fool.com.au/2016/06/20/crash-heres-why-the-erm-power-ltd-share-price-

crashed-22-today/

Appendix

Ratio calculations for ERM Electricity Limited

Ratio Formula 2015 2016

Cash Conversion cycle Days inventory

outstanding+ days

sales outstanding –

days payables

outstanding

Days inventory outstanding (Inventory/cost of

sales)*365

=(36.43/2173.7)*365

= 6.1 days

=(22.08/2618.98)*365

= 3.1 days

Days sales outstanding (receivables/credit

sales)*365

=(218.3/2418.55)*36

5

= 33 days

=(330.6/2802.83)*365

= 43.1 days

Days payables outstanding (payables/cost of

sales)*365

(279.24/2173.7)*365 (367.04/2618.98)*365

Morningstar. (n.d.). ERM Power Limited. Retrieved September 28, 2017, from Morningstar

DatAnalysis Premium:

http://datanalysis.morningstar.com.au.ezproxy.uws.edu.au/ftl/company/profitloss?

ASXCode=EPW&rt=A&sy=2007-01-01&ey=2017-12-31&xtm-licensee=datpremium

Morningstar. (n.d.). Mercury NZ Limited. Retrieved September 28, 2017, from Morningstar

DatAnalysis Premium:

http://datanalysis.morningstar.com.au.ezproxy.uws.edu.au/af/company/corpdetails?

ASXCode=MCY-NZ&xtm-licensee=datpremium

Newman, R. (2016, June 20). CRASH! Here’s why the ERM Power Ltd share price crashed 22% today.

Retrieved September 27, 2017, from The Motley Fool:

https://www.fool.com.au/2016/06/20/crash-heres-why-the-erm-power-ltd-share-price-

crashed-22-today/

Appendix

Ratio calculations for ERM Electricity Limited

Ratio Formula 2015 2016

Cash Conversion cycle Days inventory

outstanding+ days

sales outstanding –

days payables

outstanding

Days inventory outstanding (Inventory/cost of

sales)*365

=(36.43/2173.7)*365

= 6.1 days

=(22.08/2618.98)*365

= 3.1 days

Days sales outstanding (receivables/credit

sales)*365

=(218.3/2418.55)*36

5

= 33 days

=(330.6/2802.83)*365

= 43.1 days

Days payables outstanding (payables/cost of

sales)*365

(279.24/2173.7)*365 (367.04/2618.98)*365

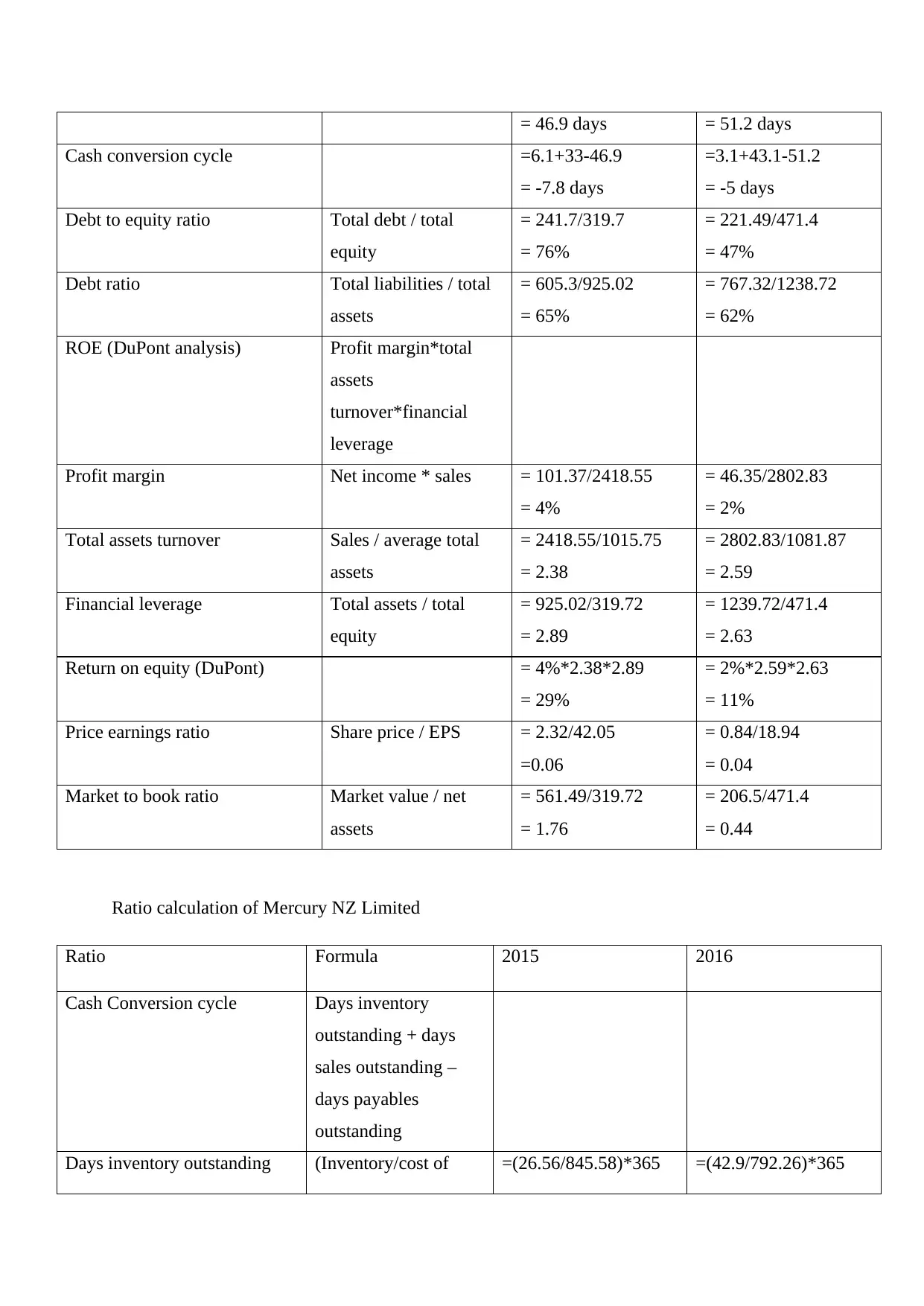

= 46.9 days = 51.2 days

Cash conversion cycle =6.1+33-46.9

= -7.8 days

=3.1+43.1-51.2

= -5 days

Debt to equity ratio Total debt / total

equity

= 241.7/319.7

= 76%

= 221.49/471.4

= 47%

Debt ratio Total liabilities / total

assets

= 605.3/925.02

= 65%

= 767.32/1238.72

= 62%

ROE (DuPont analysis) Profit margin*total

assets

turnover*financial

leverage

Profit margin Net income * sales = 101.37/2418.55

= 4%

= 46.35/2802.83

= 2%

Total assets turnover Sales / average total

assets

= 2418.55/1015.75

= 2.38

= 2802.83/1081.87

= 2.59

Financial leverage Total assets / total

equity

= 925.02/319.72

= 2.89

= 1239.72/471.4

= 2.63

Return on equity (DuPont) = 4%*2.38*2.89

= 29%

= 2%*2.59*2.63

= 11%

Price earnings ratio Share price / EPS = 2.32/42.05

=0.06

= 0.84/18.94

= 0.04

Market to book ratio Market value / net

assets

= 561.49/319.72

= 1.76

= 206.5/471.4

= 0.44

Ratio calculation of Mercury NZ Limited

Ratio Formula 2015 2016

Cash Conversion cycle Days inventory

outstanding + days

sales outstanding –

days payables

outstanding

Days inventory outstanding (Inventory/cost of =(26.56/845.58)*365 =(42.9/792.26)*365

Cash conversion cycle =6.1+33-46.9

= -7.8 days

=3.1+43.1-51.2

= -5 days

Debt to equity ratio Total debt / total

equity

= 241.7/319.7

= 76%

= 221.49/471.4

= 47%

Debt ratio Total liabilities / total

assets

= 605.3/925.02

= 65%

= 767.32/1238.72

= 62%

ROE (DuPont analysis) Profit margin*total

assets

turnover*financial

leverage

Profit margin Net income * sales = 101.37/2418.55

= 4%

= 46.35/2802.83

= 2%

Total assets turnover Sales / average total

assets

= 2418.55/1015.75

= 2.38

= 2802.83/1081.87

= 2.59

Financial leverage Total assets / total

equity

= 925.02/319.72

= 2.89

= 1239.72/471.4

= 2.63

Return on equity (DuPont) = 4%*2.38*2.89

= 29%

= 2%*2.59*2.63

= 11%

Price earnings ratio Share price / EPS = 2.32/42.05

=0.06

= 0.84/18.94

= 0.04

Market to book ratio Market value / net

assets

= 561.49/319.72

= 1.76

= 206.5/471.4

= 0.44

Ratio calculation of Mercury NZ Limited

Ratio Formula 2015 2016

Cash Conversion cycle Days inventory

outstanding + days

sales outstanding –

days payables

outstanding

Days inventory outstanding (Inventory/cost of =(26.56/845.58)*365 =(42.9/792.26)*365

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

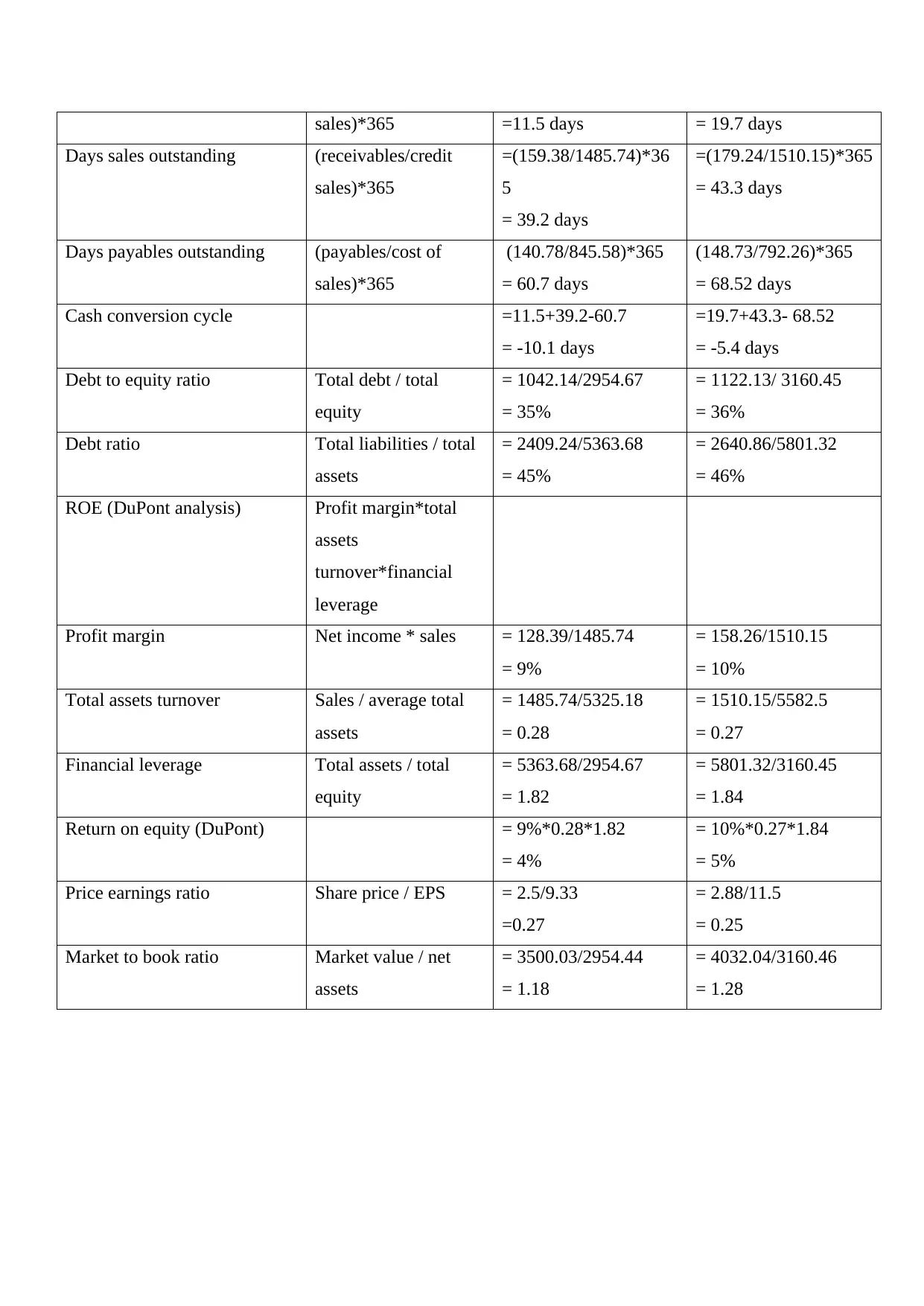

sales)*365 =11.5 days = 19.7 days

Days sales outstanding (receivables/credit

sales)*365

=(159.38/1485.74)*36

5

= 39.2 days

=(179.24/1510.15)*365

= 43.3 days

Days payables outstanding (payables/cost of

sales)*365

(140.78/845.58)*365

= 60.7 days

(148.73/792.26)*365

= 68.52 days

Cash conversion cycle =11.5+39.2-60.7

= -10.1 days

=19.7+43.3- 68.52

= -5.4 days

Debt to equity ratio Total debt / total

equity

= 1042.14/2954.67

= 35%

= 1122.13/ 3160.45

= 36%

Debt ratio Total liabilities / total

assets

= 2409.24/5363.68

= 45%

= 2640.86/5801.32

= 46%

ROE (DuPont analysis) Profit margin*total

assets

turnover*financial

leverage

Profit margin Net income * sales = 128.39/1485.74

= 9%

= 158.26/1510.15

= 10%

Total assets turnover Sales / average total

assets

= 1485.74/5325.18

= 0.28

= 1510.15/5582.5

= 0.27

Financial leverage Total assets / total

equity

= 5363.68/2954.67

= 1.82

= 5801.32/3160.45

= 1.84

Return on equity (DuPont) = 9%*0.28*1.82

= 4%

= 10%*0.27*1.84

= 5%

Price earnings ratio Share price / EPS = 2.5/9.33

=0.27

= 2.88/11.5

= 0.25

Market to book ratio Market value / net

assets

= 3500.03/2954.44

= 1.18

= 4032.04/3160.46

= 1.28

Days sales outstanding (receivables/credit

sales)*365

=(159.38/1485.74)*36

5

= 39.2 days

=(179.24/1510.15)*365

= 43.3 days

Days payables outstanding (payables/cost of

sales)*365

(140.78/845.58)*365

= 60.7 days

(148.73/792.26)*365

= 68.52 days

Cash conversion cycle =11.5+39.2-60.7

= -10.1 days

=19.7+43.3- 68.52

= -5.4 days

Debt to equity ratio Total debt / total

equity

= 1042.14/2954.67

= 35%

= 1122.13/ 3160.45

= 36%

Debt ratio Total liabilities / total

assets

= 2409.24/5363.68

= 45%

= 2640.86/5801.32

= 46%

ROE (DuPont analysis) Profit margin*total

assets

turnover*financial

leverage

Profit margin Net income * sales = 128.39/1485.74

= 9%

= 158.26/1510.15

= 10%

Total assets turnover Sales / average total

assets

= 1485.74/5325.18

= 0.28

= 1510.15/5582.5

= 0.27

Financial leverage Total assets / total

equity

= 5363.68/2954.67

= 1.82

= 5801.32/3160.45

= 1.84

Return on equity (DuPont) = 9%*0.28*1.82

= 4%

= 10%*0.27*1.84

= 5%

Price earnings ratio Share price / EPS = 2.5/9.33

=0.27

= 2.88/11.5

= 0.25

Market to book ratio Market value / net

assets

= 3500.03/2954.44

= 1.18

= 4032.04/3160.46

= 1.28

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.