AC4410: Financial Analysis Report of Hikma Pharmaceutical Plc

VerifiedAdded on 2023/06/14

|11

|1860

|442

Report

AI Summary

This report presents a financial analysis of Hikma Pharmaceutical Plc, focusing on key financial ratios and performance indicators. The analysis covers profitability ratios (gross profit ratio, operating profit ratio, and return on capital employed), liquidity ratios (current ratio and acid test ratio), and gearing ratios (gearing ratio and interest coverage ratio) for the period of 2014-2017. The report reveals a deteriorating trend in the company's performance over the last four years, with a decline in profitability and an increase in gearing, although liquidity improved in 2017. The conclusion highlights that in 2017, the company lacked positive earnings to cover expenses or generate returns for shareholders.

Running head: ACCOUNTING FINANCIAL ANALYSIS REPORT

Accounting financial analysis report

Name of the student

Name of the university

Student ID

Author note

Accounting financial analysis report

Name of the student

Name of the university

Student ID

Author note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING FINANCIAL ANALYSIS REPORT 1

Table of Contents

1.0 Introduction.....................................................................................................................2

2.0 Ratio analysis..................................................................................................................2

2.1 Advantages of ratio analysis............................................................................................2

2.2 Limitations of ratio analysis.............................................................................................3

3.0 Profitability ratios.................................................................................................................3

3.1 Gross profit ratio..............................................................................................................4

3.2 Operating profit ratio........................................................................................................4

3.3 Return on capital employed.............................................................................................5

3.0 Liquidity ratio..................................................................................................................5

4.1 Current ratio.....................................................................................................................5

4.2 Acid test or liquid ratio....................................................................................................6

5.0 Gearing ratio.........................................................................................................................6

5.1 Gearing ratio.....................................................................................................................7

5.2 Interest coverage ratio......................................................................................................7

6.0 Conclusion............................................................................................................................7

7.0 References............................................................................................................................8

8.0 Appendix..............................................................................................................................9

Table of Contents

1.0 Introduction.....................................................................................................................2

2.0 Ratio analysis..................................................................................................................2

2.1 Advantages of ratio analysis............................................................................................2

2.2 Limitations of ratio analysis.............................................................................................3

3.0 Profitability ratios.................................................................................................................3

3.1 Gross profit ratio..............................................................................................................4

3.2 Operating profit ratio........................................................................................................4

3.3 Return on capital employed.............................................................................................5

3.0 Liquidity ratio..................................................................................................................5

4.1 Current ratio.....................................................................................................................5

4.2 Acid test or liquid ratio....................................................................................................6

5.0 Gearing ratio.........................................................................................................................6

5.1 Gearing ratio.....................................................................................................................7

5.2 Interest coverage ratio......................................................................................................7

6.0 Conclusion............................................................................................................................7

7.0 References............................................................................................................................8

8.0 Appendix..............................................................................................................................9

ACCOUNTING FINANCIAL ANALYSIS REPORT 2

1.0 Introduction

Hikma Pharmaceutical Plc was formed with the objective of transforming the lives of

the people through delivering quality support and medicines they require on daily basis. The

company manufactures, develops and markets wide range of non-branded as well as branded

generic medicines. Further the company creates affordable and high quality medicines and

makes them accessible to the people who require them. The therapeutic categories involve

cardiovascular, diabetes, pain management, respiratory and anti-infective. The vision of the

company is to move towards the healthier world that will enrich all the communities (Hikma

2018).

2.0 Ratio analysis

Ratio analysis is the analysis of the financial information that helps in evaluating

different aspects of the financial and operating aspects of the company. It includes the

measurement of performance with the solvency, profitability, liquidity and efficiency aspects.

It is done for evaluating the relationships among the items from the financial statement

(Palepu, Healy and Peek 2013).

2.1 Advantages of ratio analysis

Various advantages that can be obtained through the analysis of financial ratios are as

follows –

It is used to analyse the liquidity of the company for evaluating whether the company

is able to meet its future obligations or not

It is helpful to compare the values of the current year with the previous year. Further,

the comparisons assist the analyst to recognize the weaknesses and strengths of the

company’s financial position and assess the future risks (Vogel 2014).

1.0 Introduction

Hikma Pharmaceutical Plc was formed with the objective of transforming the lives of

the people through delivering quality support and medicines they require on daily basis. The

company manufactures, develops and markets wide range of non-branded as well as branded

generic medicines. Further the company creates affordable and high quality medicines and

makes them accessible to the people who require them. The therapeutic categories involve

cardiovascular, diabetes, pain management, respiratory and anti-infective. The vision of the

company is to move towards the healthier world that will enrich all the communities (Hikma

2018).

2.0 Ratio analysis

Ratio analysis is the analysis of the financial information that helps in evaluating

different aspects of the financial and operating aspects of the company. It includes the

measurement of performance with the solvency, profitability, liquidity and efficiency aspects.

It is done for evaluating the relationships among the items from the financial statement

(Palepu, Healy and Peek 2013).

2.1 Advantages of ratio analysis

Various advantages that can be obtained through the analysis of financial ratios are as

follows –

It is used to analyse the liquidity of the company for evaluating whether the company

is able to meet its future obligations or not

It is helpful to compare the values of the current year with the previous year. Further,

the comparisons assist the analyst to recognize the weaknesses and strengths of the

company’s financial position and assess the future risks (Vogel 2014).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ACCOUNTING FINANCIAL ANALYSIS REPORT 3

It helps in implementing the plans for improving the liquidity, profitability and market

value and gearing issues of the company.

2.2 Limitations of ratio analysis

Apart from the advantages, the ratio analyses are associated with various limitations

as follows –

Ratios are generally calculated and analysed based on the past figures and not on the

projected future figures. However, the the analyst makes various assumptions

regarding the future performance through the ratios.

Ratios are only useful when used for comparing the performance over the long period

of time or is compared against the peer company in the same industry (Brigham and

Ehrhardt 2013)

Ratios mainly deal with the numbers and various other factors like customer service,

product quality are not taken into consideration that plays major role in financial

performances.

3.0 Profitability ratios

Ratio Formula 2017 2016 2015 2014

Profitability

Ratio

Gross profit ratio

Gross profit / sales

*100 49.95 50.56 54.94 57.15

Operating profit

ratio

Operating profit / Sales

*100 -38.58 15.49 25.59 27.00

Return on capital

employed

PBIT/ Capital

employed * 100 -28.83 8.77 19.00 28.51

It helps in implementing the plans for improving the liquidity, profitability and market

value and gearing issues of the company.

2.2 Limitations of ratio analysis

Apart from the advantages, the ratio analyses are associated with various limitations

as follows –

Ratios are generally calculated and analysed based on the past figures and not on the

projected future figures. However, the the analyst makes various assumptions

regarding the future performance through the ratios.

Ratios are only useful when used for comparing the performance over the long period

of time or is compared against the peer company in the same industry (Brigham and

Ehrhardt 2013)

Ratios mainly deal with the numbers and various other factors like customer service,

product quality are not taken into consideration that plays major role in financial

performances.

3.0 Profitability ratios

Ratio Formula 2017 2016 2015 2014

Profitability

Ratio

Gross profit ratio

Gross profit / sales

*100 49.95 50.56 54.94 57.15

Operating profit

ratio

Operating profit / Sales

*100 -38.58 15.49 25.59 27.00

Return on capital

employed

PBIT/ Capital

employed * 100 -28.83 8.77 19.00 28.51

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING FINANCIAL ANALYSIS REPORT 4

2017 2016 2015 2014

-40

-30

-20

-10

0

10

20

30

40

50

60

Profitability ratio

Gross profit margin

Operating profit margin

Return on capital

employed

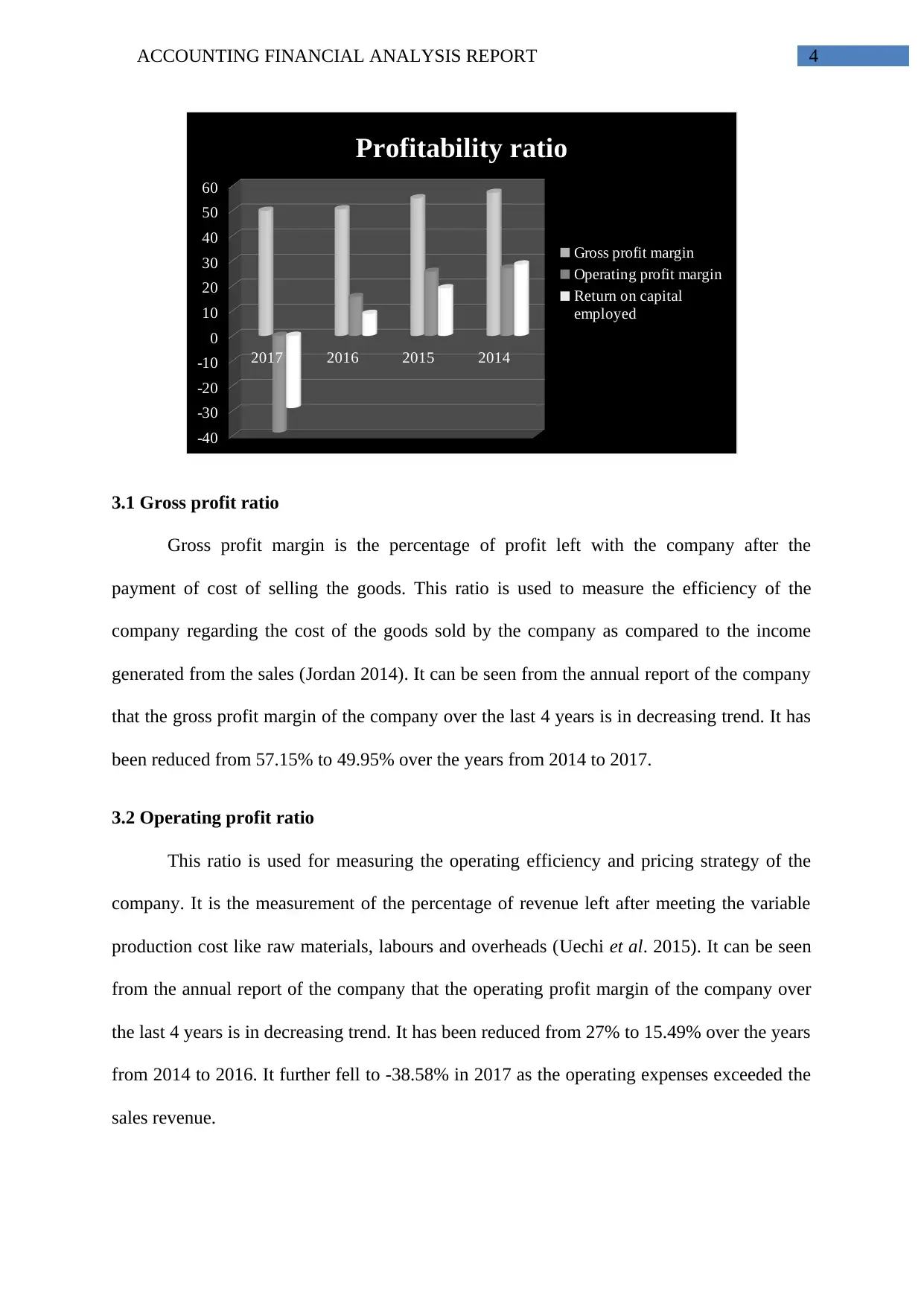

3.1 Gross profit ratio

Gross profit margin is the percentage of profit left with the company after the

payment of cost of selling the goods. This ratio is used to measure the efficiency of the

company regarding the cost of the goods sold by the company as compared to the income

generated from the sales (Jordan 2014). It can be seen from the annual report of the company

that the gross profit margin of the company over the last 4 years is in decreasing trend. It has

been reduced from 57.15% to 49.95% over the years from 2014 to 2017.

3.2 Operating profit ratio

This ratio is used for measuring the operating efficiency and pricing strategy of the

company. It is the measurement of the percentage of revenue left after meeting the variable

production cost like raw materials, labours and overheads (Uechi et al. 2015). It can be seen

from the annual report of the company that the operating profit margin of the company over

the last 4 years is in decreasing trend. It has been reduced from 27% to 15.49% over the years

from 2014 to 2016. It further fell to -38.58% in 2017 as the operating expenses exceeded the

sales revenue.

2017 2016 2015 2014

-40

-30

-20

-10

0

10

20

30

40

50

60

Profitability ratio

Gross profit margin

Operating profit margin

Return on capital

employed

3.1 Gross profit ratio

Gross profit margin is the percentage of profit left with the company after the

payment of cost of selling the goods. This ratio is used to measure the efficiency of the

company regarding the cost of the goods sold by the company as compared to the income

generated from the sales (Jordan 2014). It can be seen from the annual report of the company

that the gross profit margin of the company over the last 4 years is in decreasing trend. It has

been reduced from 57.15% to 49.95% over the years from 2014 to 2017.

3.2 Operating profit ratio

This ratio is used for measuring the operating efficiency and pricing strategy of the

company. It is the measurement of the percentage of revenue left after meeting the variable

production cost like raw materials, labours and overheads (Uechi et al. 2015). It can be seen

from the annual report of the company that the operating profit margin of the company over

the last 4 years is in decreasing trend. It has been reduced from 27% to 15.49% over the years

from 2014 to 2016. It further fell to -38.58% in 2017 as the operating expenses exceeded the

sales revenue.

ACCOUNTING FINANCIAL ANALYSIS REPORT 5

3.3 Return on capital employed

This profitability ratio measures the efficiency of a company with regard to the

employed capital of the company as compared to the net operating earnings. Generally the

amount of capital employed is equal to total assets of the company reduced by current

liabilities. It has been reduced from 28.51% to 8.77% over the years from 2014 to 2016. It

further fell to -28.83% in 2017 as the operating expenses of the company was more than the

revenue generated from sales (Hikma 2018).

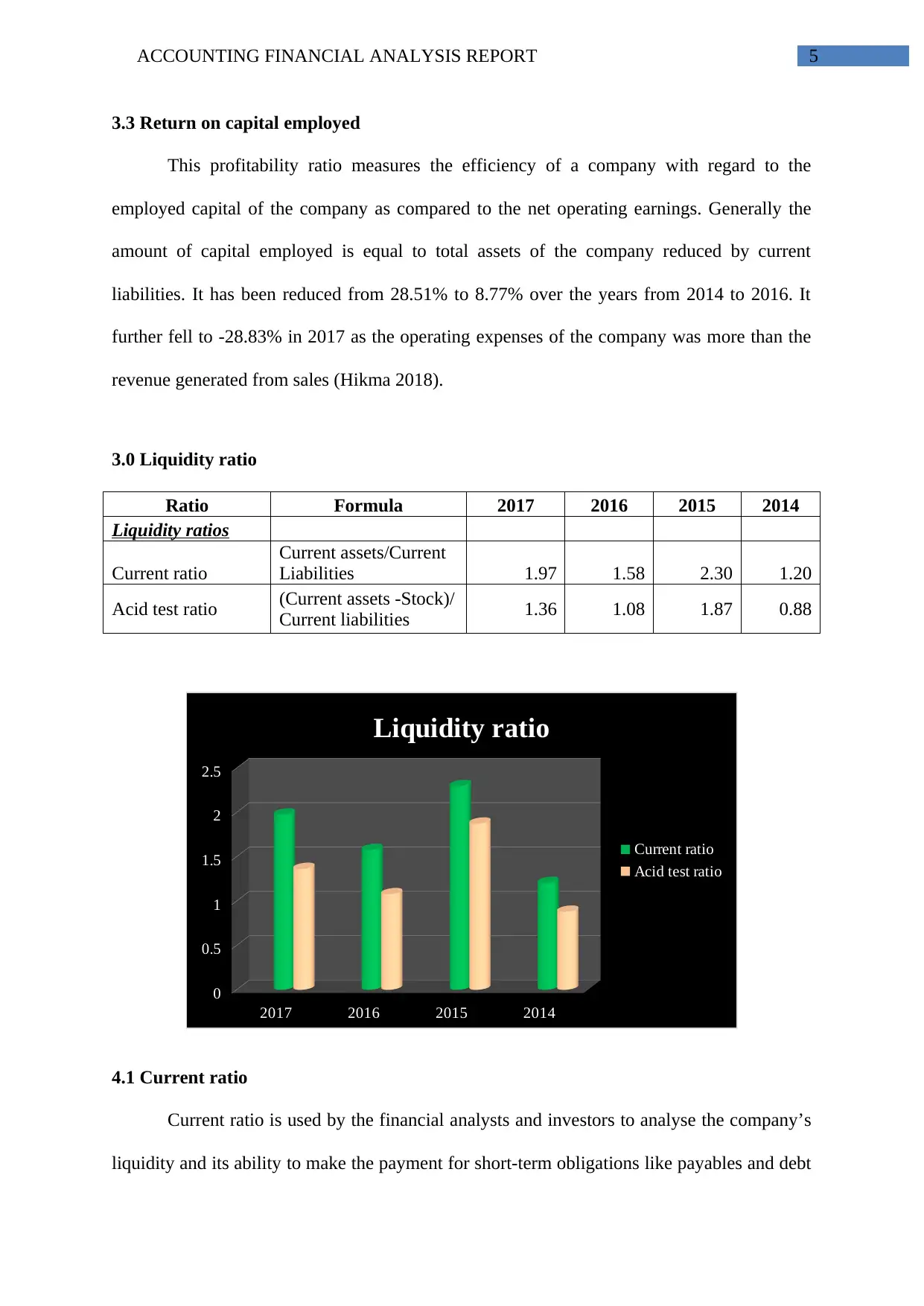

3.0 Liquidity ratio

Ratio Formula 2017 2016 2015 2014

Liquidity ratios

Current ratio

Current assets/Current

Liabilities 1.97 1.58 2.30 1.20

Acid test ratio (Current assets -Stock)/

Current liabilities 1.36 1.08 1.87 0.88

2017 2016 2015 2014

0

0.5

1

1.5

2

2.5

Liquidity ratio

Current ratio

Acid test ratio

4.1 Current ratio

Current ratio is used by the financial analysts and investors to analyse the company’s

liquidity and its ability to make the payment for short-term obligations like payables and debt

3.3 Return on capital employed

This profitability ratio measures the efficiency of a company with regard to the

employed capital of the company as compared to the net operating earnings. Generally the

amount of capital employed is equal to total assets of the company reduced by current

liabilities. It has been reduced from 28.51% to 8.77% over the years from 2014 to 2016. It

further fell to -28.83% in 2017 as the operating expenses of the company was more than the

revenue generated from sales (Hikma 2018).

3.0 Liquidity ratio

Ratio Formula 2017 2016 2015 2014

Liquidity ratios

Current ratio

Current assets/Current

Liabilities 1.97 1.58 2.30 1.20

Acid test ratio (Current assets -Stock)/

Current liabilities 1.36 1.08 1.87 0.88

2017 2016 2015 2014

0

0.5

1

1.5

2

2.5

Liquidity ratio

Current ratio

Acid test ratio

4.1 Current ratio

Current ratio is used by the financial analysts and investors to analyse the company’s

liquidity and its ability to make the payment for short-term obligations like payables and debt

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ACCOUNTING FINANCIAL ANALYSIS REPORT 6

with the short term assets like receivables, inventories and cash. It is calculated through

dividing the currents assets by its current liabilities. Looking into the calculation table it is

observed that the current ratio of the company is fluctuating. However, the company was able

to improve the liquidity position in 2017 as compared to 2016 (Hikma 2018).

4.2 Acid test or liquid ratio

Quick ratio is the liquidity indicator and it filters current ratio through measuring most

liquid current asset amount for covering up the current obligations (Ozturk and Acaravci

2013). Looking into the calculation table it is observed that the quick ratio of the company is

fluctuating like current assets of the company. However, the company was able to improve

the liquidity position in 2017 as compared to 2016 (Hikma 2018).

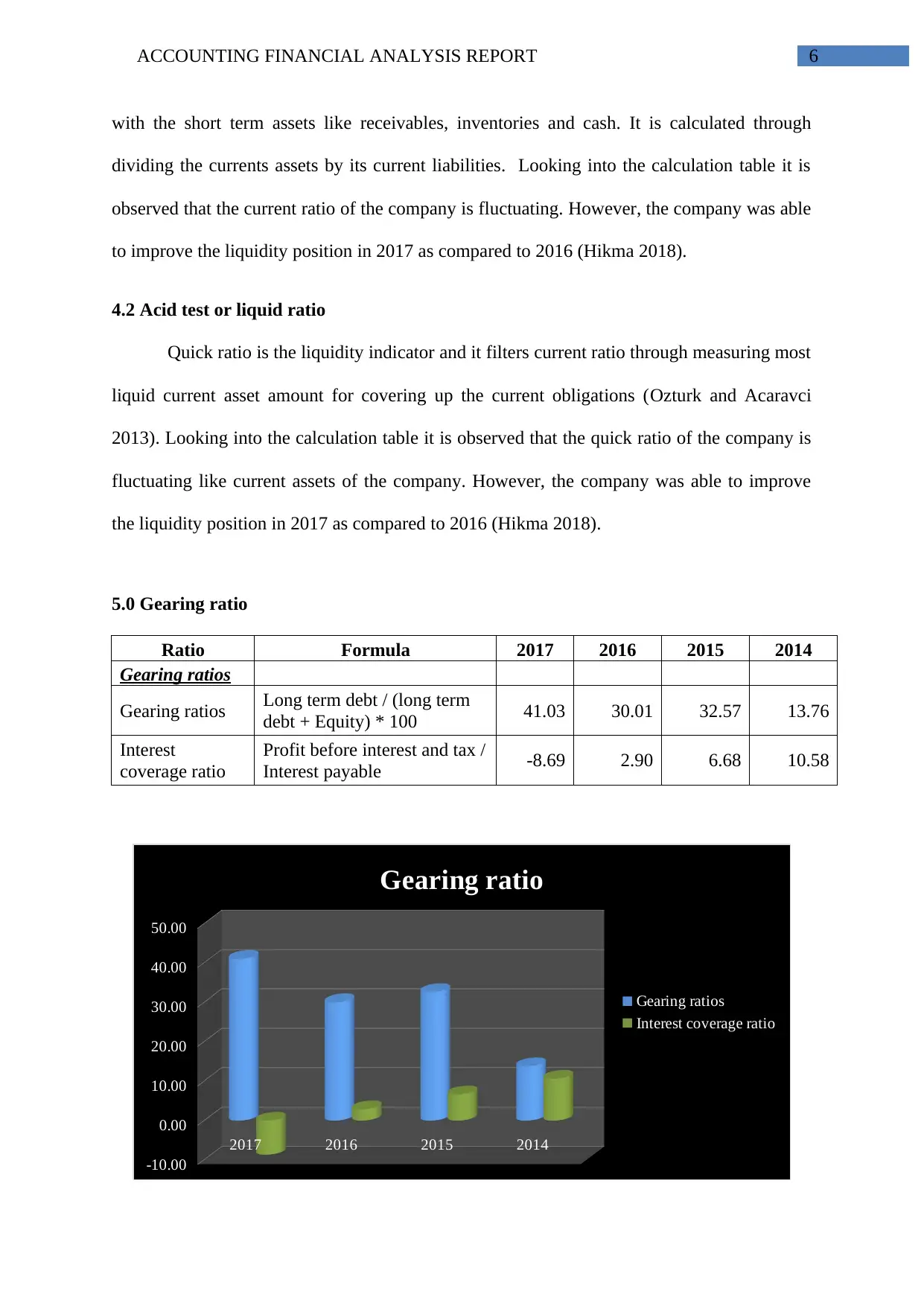

5.0 Gearing ratio

Ratio Formula 2017 2016 2015 2014

Gearing ratios

Gearing ratios Long term debt / (long term

debt + Equity) * 100 41.03 30.01 32.57 13.76

Interest

coverage ratio

Profit before interest and tax /

Interest payable -8.69 2.90 6.68 10.58

2017 2016 2015 2014

-10.00

0.00

10.00

20.00

30.00

40.00

50.00

Gearing ratio

Gearing ratios

Interest coverage ratio

with the short term assets like receivables, inventories and cash. It is calculated through

dividing the currents assets by its current liabilities. Looking into the calculation table it is

observed that the current ratio of the company is fluctuating. However, the company was able

to improve the liquidity position in 2017 as compared to 2016 (Hikma 2018).

4.2 Acid test or liquid ratio

Quick ratio is the liquidity indicator and it filters current ratio through measuring most

liquid current asset amount for covering up the current obligations (Ozturk and Acaravci

2013). Looking into the calculation table it is observed that the quick ratio of the company is

fluctuating like current assets of the company. However, the company was able to improve

the liquidity position in 2017 as compared to 2016 (Hikma 2018).

5.0 Gearing ratio

Ratio Formula 2017 2016 2015 2014

Gearing ratios

Gearing ratios Long term debt / (long term

debt + Equity) * 100 41.03 30.01 32.57 13.76

Interest

coverage ratio

Profit before interest and tax /

Interest payable -8.69 2.90 6.68 10.58

2017 2016 2015 2014

-10.00

0.00

10.00

20.00

30.00

40.00

50.00

Gearing ratio

Gearing ratios

Interest coverage ratio

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING FINANCIAL ANALYSIS REPORT 7

5.1 Gearing ratio

It states the percentage of assets that is held by the shareholders of the company and

percentage of assets that is generated through borrowing. If the company’s gearing ratio is

50% or lower than that it is considered as the company is in better position. It can be

observed that the gearing ratio of the company has significantly increased over the last 4

years and it went up to 41.03 in 2017 from 13.76 in 2014 (Hikma 2018).

5.2 Interest coverage ratio

It states the efficiency of the company in paying off the interest on the debt

outstanding. It can be observed that the interest coverage ratio of the company is in

decreasing trend over the last 4 years. Moreover, during the year 2017 the company did not

have any positive earning to pay off its interest (Zack 2013).

6.0 Conclusion

From the above discussion it can be concluded that the performance of the company

over the last 4 years are deteriorating. Except the liquidity position, the company’s gearing

position as well as the profitability position during the year 2017 were significantly lower.

Moreover, during the year 2017 the company did not have any positive earnings to cover up

any further expenses or creating returns to the shareholders.

5.1 Gearing ratio

It states the percentage of assets that is held by the shareholders of the company and

percentage of assets that is generated through borrowing. If the company’s gearing ratio is

50% or lower than that it is considered as the company is in better position. It can be

observed that the gearing ratio of the company has significantly increased over the last 4

years and it went up to 41.03 in 2017 from 13.76 in 2014 (Hikma 2018).

5.2 Interest coverage ratio

It states the efficiency of the company in paying off the interest on the debt

outstanding. It can be observed that the interest coverage ratio of the company is in

decreasing trend over the last 4 years. Moreover, during the year 2017 the company did not

have any positive earning to pay off its interest (Zack 2013).

6.0 Conclusion

From the above discussion it can be concluded that the performance of the company

over the last 4 years are deteriorating. Except the liquidity position, the company’s gearing

position as well as the profitability position during the year 2017 were significantly lower.

Moreover, during the year 2017 the company did not have any positive earnings to cover up

any further expenses or creating returns to the shareholders.

ACCOUNTING FINANCIAL ANALYSIS REPORT 8

7.0 References

Brigham, E.F. and Ehrhardt, M.C., 2013. Financial management: Theory & practice.

Cengage Learning.

Hikma. 2018. Home. [online] Available at: https://www.hikma.com/home/ [Accessed 4 Apr.

2018].

Jordan, B., 2014. Fundamentals of investments. McGraw-Hill Higher Education.

Ozturk, I. and Acaravci, A., 2013. The long-run and causal analysis of energy, growth,

openness and financial development on carbon emissions in Turkey. Energy Economics, 36,

pp.262-267.

Palepu, K.G., Healy, P.M. and Peek, E., 2013. Business analysis and valuation: IFRS edition.

Cengage Learning.

Uechi, L., Akutsu, T., Stanley, H.E., Marcus, A.J. and Kenett, D.Y., 2015. Sector dominance

ratio analysis of financial markets. Physica A: Statistical Mechanics and its

Applications, 421, pp.488-509.

Vogel, H.L., 2014. Entertainment industry economics: A guide for financial analysis.

Cambridge University Press.

Zack, G.M., 2013. Financial Statement Analysis. Financial Statement Fraud: Strategies for

Detection and Investigation, pp.209-213.

7.0 References

Brigham, E.F. and Ehrhardt, M.C., 2013. Financial management: Theory & practice.

Cengage Learning.

Hikma. 2018. Home. [online] Available at: https://www.hikma.com/home/ [Accessed 4 Apr.

2018].

Jordan, B., 2014. Fundamentals of investments. McGraw-Hill Higher Education.

Ozturk, I. and Acaravci, A., 2013. The long-run and causal analysis of energy, growth,

openness and financial development on carbon emissions in Turkey. Energy Economics, 36,

pp.262-267.

Palepu, K.G., Healy, P.M. and Peek, E., 2013. Business analysis and valuation: IFRS edition.

Cengage Learning.

Uechi, L., Akutsu, T., Stanley, H.E., Marcus, A.J. and Kenett, D.Y., 2015. Sector dominance

ratio analysis of financial markets. Physica A: Statistical Mechanics and its

Applications, 421, pp.488-509.

Vogel, H.L., 2014. Entertainment industry economics: A guide for financial analysis.

Cambridge University Press.

Zack, G.M., 2013. Financial Statement Analysis. Financial Statement Fraud: Strategies for

Detection and Investigation, pp.209-213.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ACCOUNTING FINANCIAL ANALYSIS REPORT 9

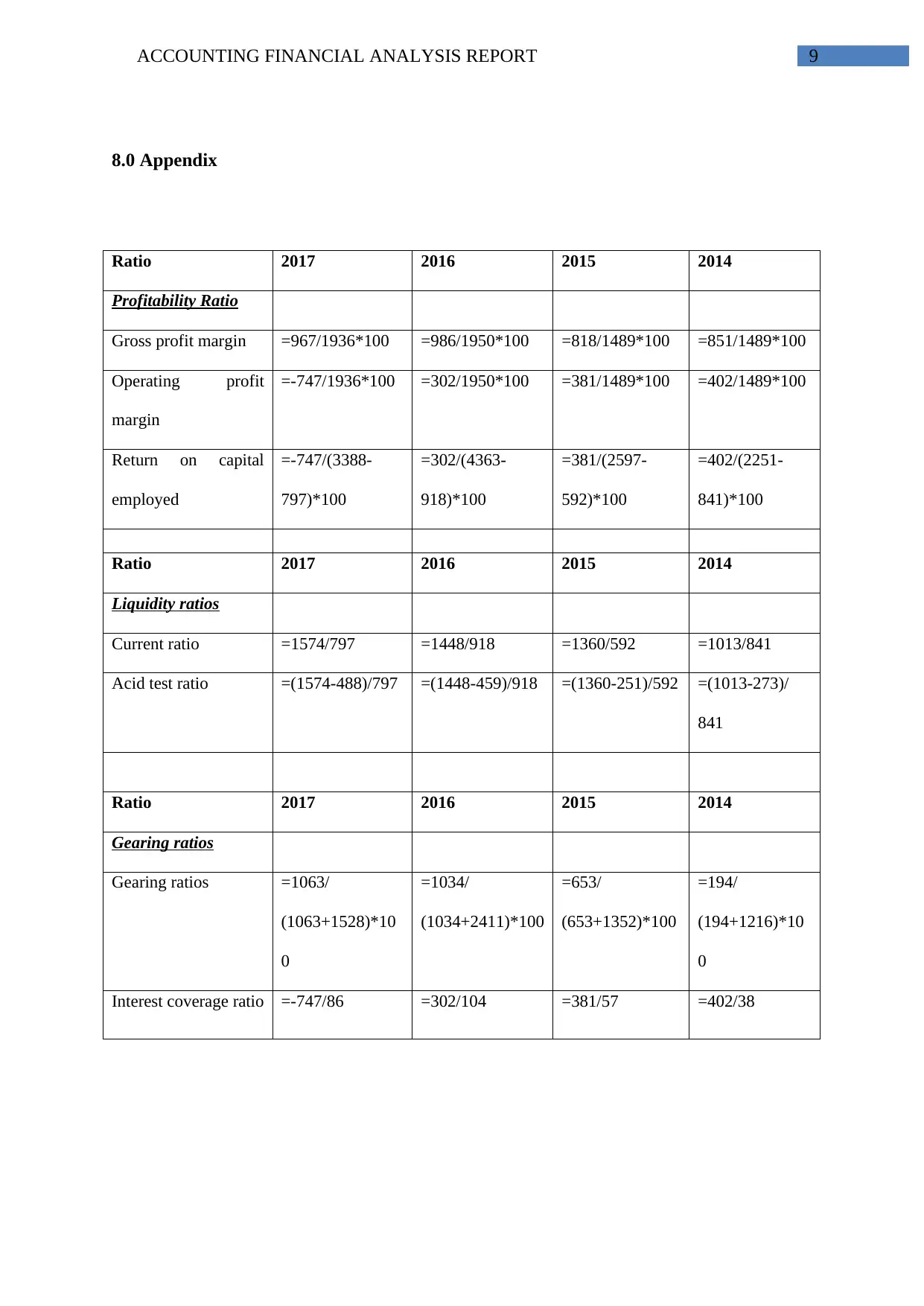

8.0 Appendix

Ratio 2017 2016 2015 2014

Profitability Ratio

Gross profit margin =967/1936*100 =986/1950*100 =818/1489*100 =851/1489*100

Operating profit

margin

=-747/1936*100 =302/1950*100 =381/1489*100 =402/1489*100

Return on capital

employed

=-747/(3388-

797)*100

=302/(4363-

918)*100

=381/(2597-

592)*100

=402/(2251-

841)*100

Ratio 2017 2016 2015 2014

Liquidity ratios

Current ratio =1574/797 =1448/918 =1360/592 =1013/841

Acid test ratio =(1574-488)/797 =(1448-459)/918 =(1360-251)/592 =(1013-273)/

841

Ratio 2017 2016 2015 2014

Gearing ratios

Gearing ratios =1063/

(1063+1528)*10

0

=1034/

(1034+2411)*100

=653/

(653+1352)*100

=194/

(194+1216)*10

0

Interest coverage ratio =-747/86 =302/104 =381/57 =402/38

8.0 Appendix

Ratio 2017 2016 2015 2014

Profitability Ratio

Gross profit margin =967/1936*100 =986/1950*100 =818/1489*100 =851/1489*100

Operating profit

margin

=-747/1936*100 =302/1950*100 =381/1489*100 =402/1489*100

Return on capital

employed

=-747/(3388-

797)*100

=302/(4363-

918)*100

=381/(2597-

592)*100

=402/(2251-

841)*100

Ratio 2017 2016 2015 2014

Liquidity ratios

Current ratio =1574/797 =1448/918 =1360/592 =1013/841

Acid test ratio =(1574-488)/797 =(1448-459)/918 =(1360-251)/592 =(1013-273)/

841

Ratio 2017 2016 2015 2014

Gearing ratios

Gearing ratios =1063/

(1063+1528)*10

0

=1034/

(1034+2411)*100

=653/

(653+1352)*100

=194/

(194+1216)*10

0

Interest coverage ratio =-747/86 =302/104 =381/57 =402/38

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING FINANCIAL ANALYSIS REPORT 10

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.