CW1 Business Report: Financial Analysis and Investment Evaluation

VerifiedAdded on 2023/06/04

|14

|1510

|346

AI Summary

This report provides a financial analysis of a company's income statement and balance sheet, along with an evaluation of potential investments using ARR, payback period, and IRR. It also suggests five factors to consider before making investments.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

CW1 Business Report

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TABLE OF CONTENT

INTRODUCTION ..........................................................................................................................3

MAIN BODY...................................................................................................................................3

Heading 1.....................................................................................................................................3

Heading 2.....................................................................................................................................3

Heading 3.....................................................................................................................................3

CONCLUSION ...............................................................................................................................3

REFERENCES................................................................................................................................4

INTRODUCTION ..........................................................................................................................3

MAIN BODY...................................................................................................................................3

Heading 1.....................................................................................................................................3

Heading 2.....................................................................................................................................3

Heading 3.....................................................................................................................................3

CONCLUSION ...............................................................................................................................3

REFERENCES................................................................................................................................4

SECTION A

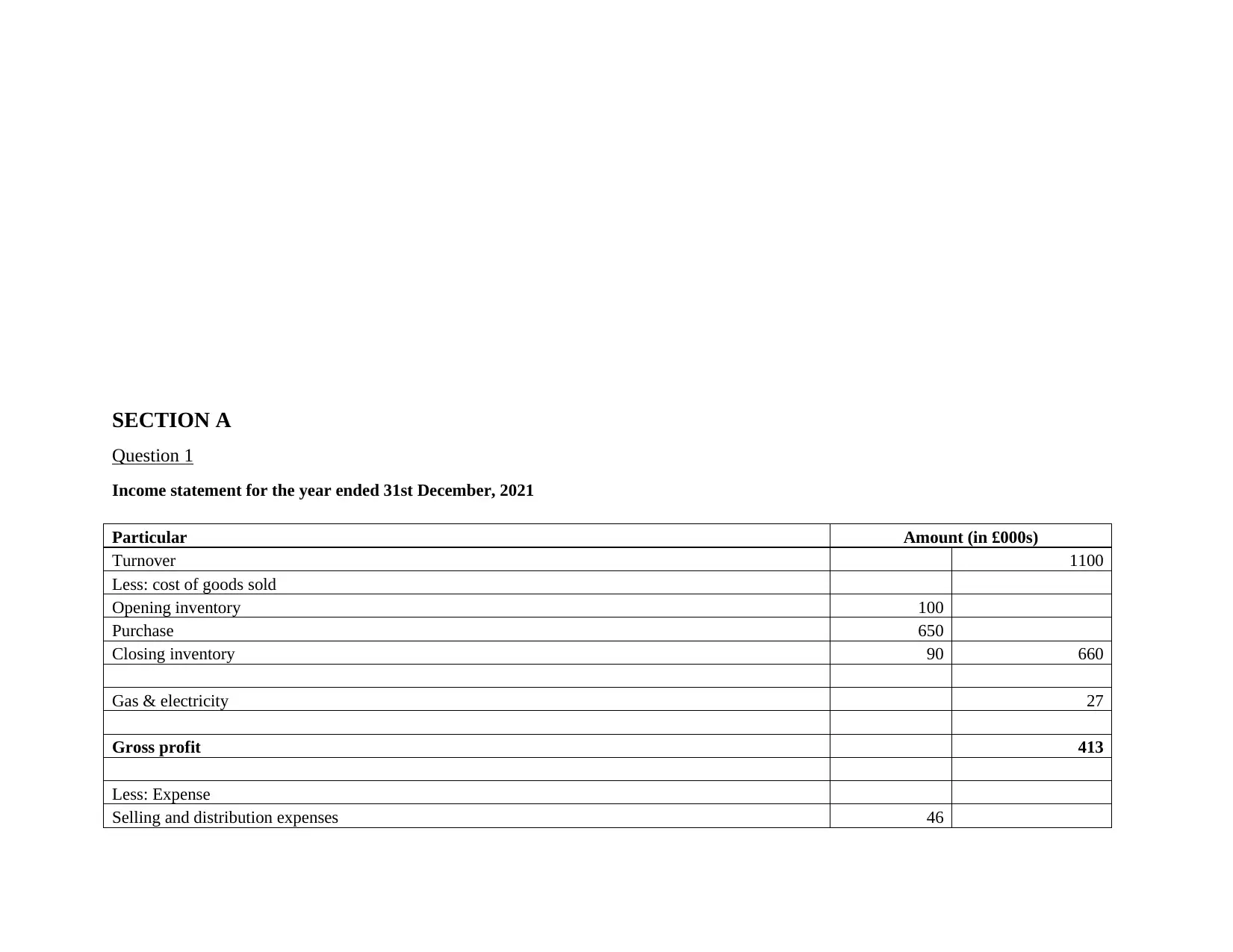

Question 1

Income statement for the year ended 31st December, 2021

Particular Amount (in £000s)

Turnover 1100

Less: cost of goods sold

Opening inventory 100

Purchase 650

Closing inventory 90 660

Gas & electricity 27

Gross profit 413

Less: Expense

Selling and distribution expenses 46

Question 1

Income statement for the year ended 31st December, 2021

Particular Amount (in £000s)

Turnover 1100

Less: cost of goods sold

Opening inventory 100

Purchase 650

Closing inventory 90 660

Gas & electricity 27

Gross profit 413

Less: Expense

Selling and distribution expenses 46

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Rent, rates and insurance 36

Staff salaries 100

Advertisement 20

Audit fees 11

Bad debt 4

Depreciation 40

Debenture interest 11

Director's remuneration 34

Bank loan Interest 7

Total expenses 309

Net profit before tax 104

Less: tax payable 25

Net profit after tax before dividend 79

Interim dividend 48

Net profit after dividend 31

Balance sheet as at 31 December, 2021

Particulars Amount (in £)

Assets

Non-current assets

Intangible assets

Premises 600

Equipment 80

Furniture & fitting 20

Total non-current assets 700

Current assets

Inventory 90

Staff salaries 100

Advertisement 20

Audit fees 11

Bad debt 4

Depreciation 40

Debenture interest 11

Director's remuneration 34

Bank loan Interest 7

Total expenses 309

Net profit before tax 104

Less: tax payable 25

Net profit after tax before dividend 79

Interim dividend 48

Net profit after dividend 31

Balance sheet as at 31 December, 2021

Particulars Amount (in £)

Assets

Non-current assets

Intangible assets

Premises 600

Equipment 80

Furniture & fitting 20

Total non-current assets 700

Current assets

Inventory 90

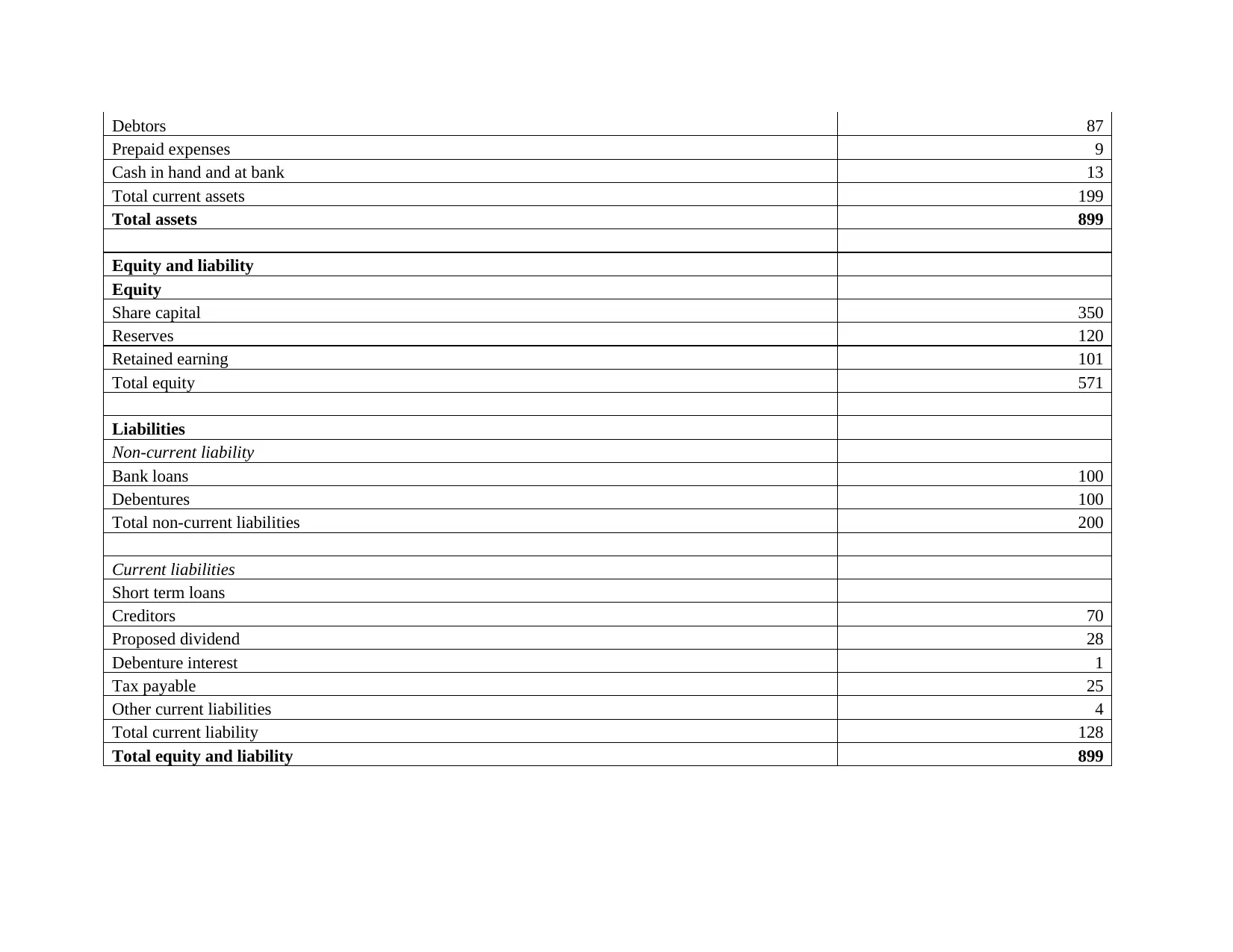

Debtors 87

Prepaid expenses 9

Cash in hand and at bank 13

Total current assets 199

Total assets 899

Equity and liability

Equity

Share capital 350

Reserves 120

Retained earning 101

Total equity 571

Liabilities

Non-current liability

Bank loans 100

Debentures 100

Total non-current liabilities 200

Current liabilities

Short term loans

Creditors 70

Proposed dividend 28

Debenture interest 1

Tax payable 25

Other current liabilities 4

Total current liability 128

Total equity and liability 899

Prepaid expenses 9

Cash in hand and at bank 13

Total current assets 199

Total assets 899

Equity and liability

Equity

Share capital 350

Reserves 120

Retained earning 101

Total equity 571

Liabilities

Non-current liability

Bank loans 100

Debentures 100

Total non-current liabilities 200

Current liabilities

Short term loans

Creditors 70

Proposed dividend 28

Debenture interest 1

Tax payable 25

Other current liabilities 4

Total current liability 128

Total equity and liability 899

According to financial statement of company it can be said that the performance of the company is good and it is earning a

good profit and providing dividend to its shareholders. It is advised to company to increase its retained earning which will help it in

investing in future and enable growth and development.

SECTION B

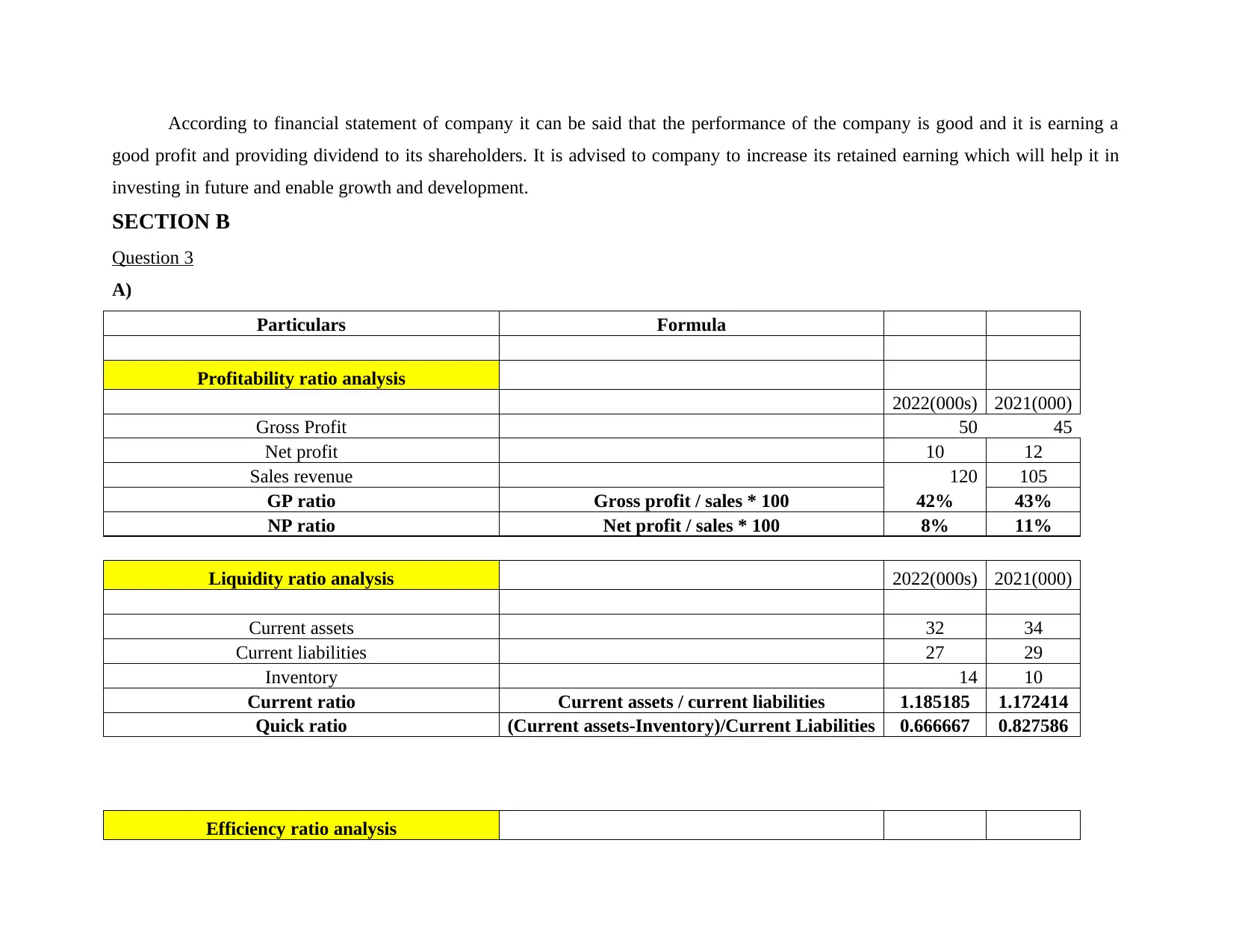

Question 3

A)

Particulars Formula

Profitability ratio analysis

2022(000s) 2021(000)

Gross Profit 50 45

Net profit 10 12

Sales revenue 120 105

GP ratio Gross profit / sales * 100 42% 43%

NP ratio Net profit / sales * 100 8% 11%

Liquidity ratio analysis 2022(000s) 2021(000)

Current assets 32 34

Current liabilities 27 29

Inventory 14 10

Current ratio Current assets / current liabilities 1.185185 1.172414

Quick ratio (Current assets-Inventory)/Current Liabilities 0.666667 0.827586

Efficiency ratio analysis

good profit and providing dividend to its shareholders. It is advised to company to increase its retained earning which will help it in

investing in future and enable growth and development.

SECTION B

Question 3

A)

Particulars Formula

Profitability ratio analysis

2022(000s) 2021(000)

Gross Profit 50 45

Net profit 10 12

Sales revenue 120 105

GP ratio Gross profit / sales * 100 42% 43%

NP ratio Net profit / sales * 100 8% 11%

Liquidity ratio analysis 2022(000s) 2021(000)

Current assets 32 34

Current liabilities 27 29

Inventory 14 10

Current ratio Current assets / current liabilities 1.185185 1.172414

Quick ratio (Current assets-Inventory)/Current Liabilities 0.666667 0.827586

Efficiency ratio analysis

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

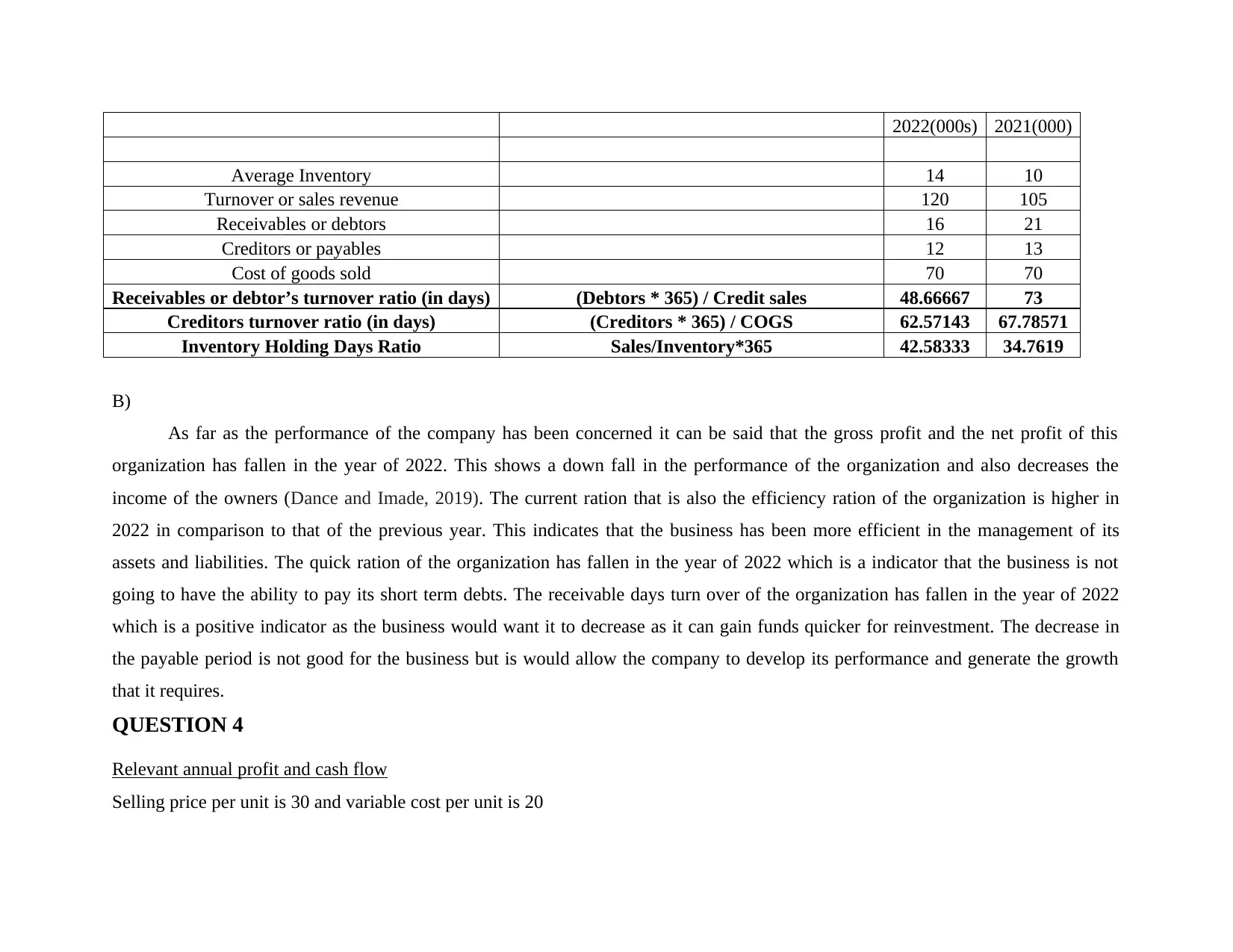

2022(000s) 2021(000)

Average Inventory 14 10

Turnover or sales revenue 120 105

Receivables or debtors 16 21

Creditors or payables 12 13

Cost of goods sold 70 70

Receivables or debtor’s turnover ratio (in days) (Debtors * 365) / Credit sales 48.66667 73

Creditors turnover ratio (in days) (Creditors * 365) / COGS 62.57143 67.78571

Inventory Holding Days Ratio Sales/Inventory*365 42.58333 34.7619

B)

As far as the performance of the company has been concerned it can be said that the gross profit and the net profit of this

organization has fallen in the year of 2022. This shows a down fall in the performance of the organization and also decreases the

income of the owners (Dance and Imade, 2019). The current ration that is also the efficiency ration of the organization is higher in

2022 in comparison to that of the previous year. This indicates that the business has been more efficient in the management of its

assets and liabilities. The quick ration of the organization has fallen in the year of 2022 which is a indicator that the business is not

going to have the ability to pay its short term debts. The receivable days turn over of the organization has fallen in the year of 2022

which is a positive indicator as the business would want it to decrease as it can gain funds quicker for reinvestment. The decrease in

the payable period is not good for the business but is would allow the company to develop its performance and generate the growth

that it requires.

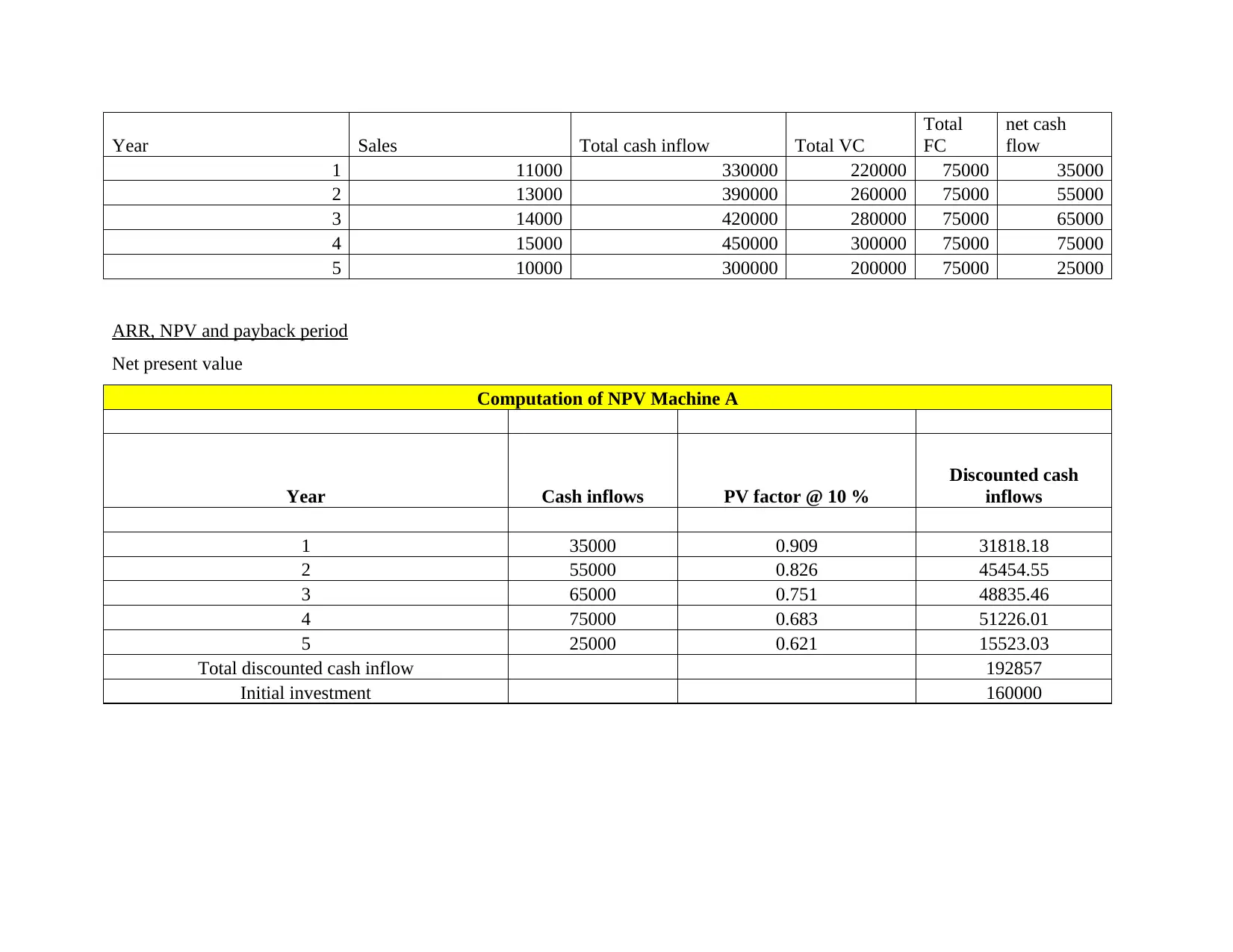

QUESTION 4

Relevant annual profit and cash flow

Selling price per unit is 30 and variable cost per unit is 20

Average Inventory 14 10

Turnover or sales revenue 120 105

Receivables or debtors 16 21

Creditors or payables 12 13

Cost of goods sold 70 70

Receivables or debtor’s turnover ratio (in days) (Debtors * 365) / Credit sales 48.66667 73

Creditors turnover ratio (in days) (Creditors * 365) / COGS 62.57143 67.78571

Inventory Holding Days Ratio Sales/Inventory*365 42.58333 34.7619

B)

As far as the performance of the company has been concerned it can be said that the gross profit and the net profit of this

organization has fallen in the year of 2022. This shows a down fall in the performance of the organization and also decreases the

income of the owners (Dance and Imade, 2019). The current ration that is also the efficiency ration of the organization is higher in

2022 in comparison to that of the previous year. This indicates that the business has been more efficient in the management of its

assets and liabilities. The quick ration of the organization has fallen in the year of 2022 which is a indicator that the business is not

going to have the ability to pay its short term debts. The receivable days turn over of the organization has fallen in the year of 2022

which is a positive indicator as the business would want it to decrease as it can gain funds quicker for reinvestment. The decrease in

the payable period is not good for the business but is would allow the company to develop its performance and generate the growth

that it requires.

QUESTION 4

Relevant annual profit and cash flow

Selling price per unit is 30 and variable cost per unit is 20

Year Sales Total cash inflow Total VC

Total

FC

net cash

flow

1 11000 330000 220000 75000 35000

2 13000 390000 260000 75000 55000

3 14000 420000 280000 75000 65000

4 15000 450000 300000 75000 75000

5 10000 300000 200000 75000 25000

ARR, NPV and payback period

Net present value

Computation of NPV Machine A

Year Cash inflows PV factor @ 10 %

Discounted cash

inflows

1 35000 0.909 31818.18

2 55000 0.826 45454.55

3 65000 0.751 48835.46

4 75000 0.683 51226.01

5 25000 0.621 15523.03

Total discounted cash inflow 192857

Initial investment 160000

Total

FC

net cash

flow

1 11000 330000 220000 75000 35000

2 13000 390000 260000 75000 55000

3 14000 420000 280000 75000 65000

4 15000 450000 300000 75000 75000

5 10000 300000 200000 75000 25000

ARR, NPV and payback period

Net present value

Computation of NPV Machine A

Year Cash inflows PV factor @ 10 %

Discounted cash

inflows

1 35000 0.909 31818.18

2 55000 0.826 45454.55

3 65000 0.751 48835.46

4 75000 0.683 51226.01

5 25000 0.621 15523.03

Total discounted cash inflow 192857

Initial investment 160000

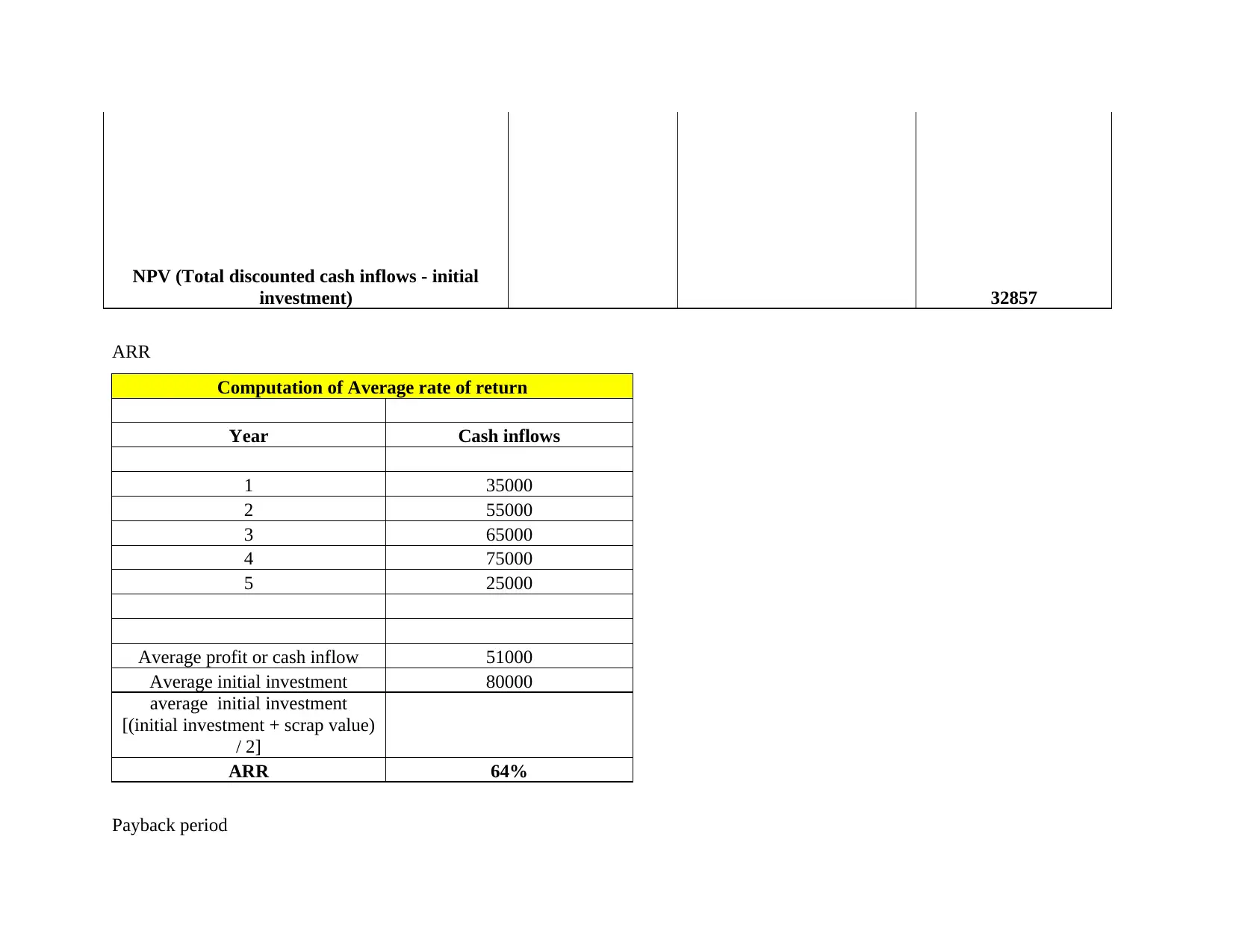

NPV (Total discounted cash inflows - initial

investment) 32857

ARR

Computation of Average rate of return

Year Cash inflows

1 35000

2 55000

3 65000

4 75000

5 25000

Average profit or cash inflow 51000

Average initial investment 80000

average initial investment

[(initial investment + scrap value)

/ 2]

ARR 64%

Payback period

investment) 32857

ARR

Computation of Average rate of return

Year Cash inflows

1 35000

2 55000

3 65000

4 75000

5 25000

Average profit or cash inflow 51000

Average initial investment 80000

average initial investment

[(initial investment + scrap value)

/ 2]

ARR 64%

Payback period

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

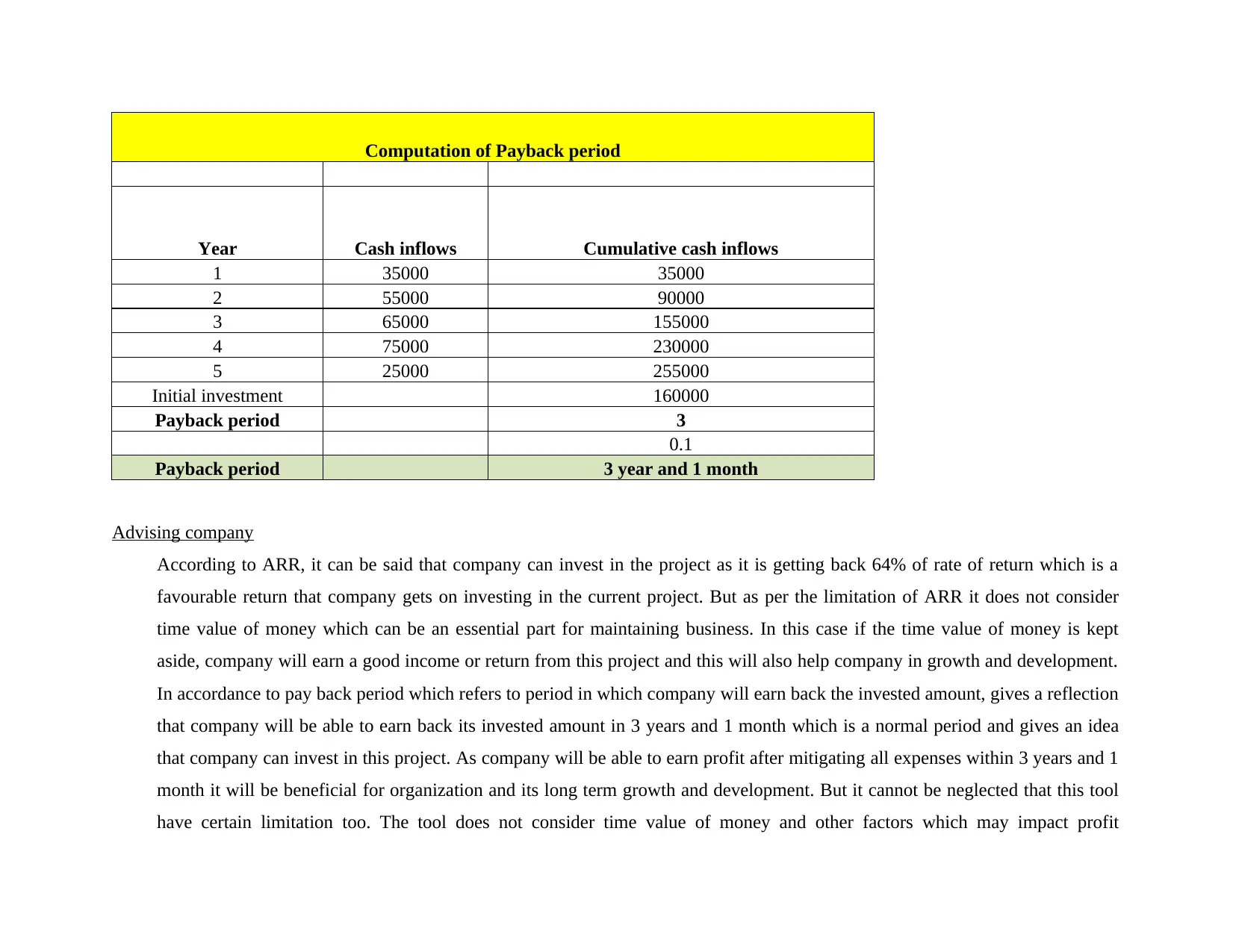

Computation of Payback period

Year Cash inflows Cumulative cash inflows

1 35000 35000

2 55000 90000

3 65000 155000

4 75000 230000

5 25000 255000

Initial investment 160000

Payback period 3

0.1

Payback period 3 year and 1 month

Advising company

According to ARR, it can be said that company can invest in the project as it is getting back 64% of rate of return which is a

favourable return that company gets on investing in the current project. But as per the limitation of ARR it does not consider

time value of money which can be an essential part for maintaining business. In this case if the time value of money is kept

aside, company will earn a good income or return from this project and this will also help company in growth and development.

In accordance to pay back period which refers to period in which company will earn back the invested amount, gives a reflection

that company will be able to earn back its invested amount in 3 years and 1 month which is a normal period and gives an idea

that company can invest in this project. As company will be able to earn profit after mitigating all expenses within 3 years and 1

month it will be beneficial for organization and its long term growth and development. But it cannot be neglected that this tool

have certain limitation too. The tool does not consider time value of money and other factors which may impact profit

Year Cash inflows Cumulative cash inflows

1 35000 35000

2 55000 90000

3 65000 155000

4 75000 230000

5 25000 255000

Initial investment 160000

Payback period 3

0.1

Payback period 3 year and 1 month

Advising company

According to ARR, it can be said that company can invest in the project as it is getting back 64% of rate of return which is a

favourable return that company gets on investing in the current project. But as per the limitation of ARR it does not consider

time value of money which can be an essential part for maintaining business. In this case if the time value of money is kept

aside, company will earn a good income or return from this project and this will also help company in growth and development.

In accordance to pay back period which refers to period in which company will earn back the invested amount, gives a reflection

that company will be able to earn back its invested amount in 3 years and 1 month which is a normal period and gives an idea

that company can invest in this project. As company will be able to earn profit after mitigating all expenses within 3 years and 1

month it will be beneficial for organization and its long term growth and development. But it cannot be neglected that this tool

have certain limitation too. The tool does not consider time value of money and other factors which may impact profit

estimation of company. It is advisable to company to overlook on these limitations of both tools and then take decision

regarding to invest in the project or not. If all other factors are neglected then it will be a favourable project for long term growth

of company and it will help company in earning higher profit and revenue and capture higher market shares.

Five other factors to be considered

The five factors that are to be considered by the company before making such investments are going to be the following,

Analysation of the current and projected profitability is required from the investment.

The effective utilization of the assets is also important to be evaluated before investments.

Conservative capital structure is said to be required for the referring to the company funds and its business operations.

Earnings and momentum is said to be the reason for the fixation of the many investments that are made.

The intrinsic value is also a key part of the market value for the project and the analysation of the operations.

IRR and its advantages

IRR is the metric that has been considered to be used as the financial analysis for the estimation of the profitability of the potential

investments (Siziba and Hall, 2021). It is considered that the IRR is the discount rate that makes the net present value of the cash flow

equal to zero in the discounted cash flow analysis. The advantages of IRR include the following,

It helps in finding the time value of money in the capital budgeting method.

It is said to be the simplest form of capital budgeting tool.

The hurdle rate is not required for the calculation of the IRR.

regarding to invest in the project or not. If all other factors are neglected then it will be a favourable project for long term growth

of company and it will help company in earning higher profit and revenue and capture higher market shares.

Five other factors to be considered

The five factors that are to be considered by the company before making such investments are going to be the following,

Analysation of the current and projected profitability is required from the investment.

The effective utilization of the assets is also important to be evaluated before investments.

Conservative capital structure is said to be required for the referring to the company funds and its business operations.

Earnings and momentum is said to be the reason for the fixation of the many investments that are made.

The intrinsic value is also a key part of the market value for the project and the analysation of the operations.

IRR and its advantages

IRR is the metric that has been considered to be used as the financial analysis for the estimation of the profitability of the potential

investments (Siziba and Hall, 2021). It is considered that the IRR is the discount rate that makes the net present value of the cash flow

equal to zero in the discounted cash flow analysis. The advantages of IRR include the following,

It helps in finding the time value of money in the capital budgeting method.

It is said to be the simplest form of capital budgeting tool.

The hurdle rate is not required for the calculation of the IRR.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Siziba, S. and Hall, J. H., 2021. The evolution of the application of capital budgeting techniques in enterprises. Global Finance

Journal. 47. p.100504.

Dance, M. and Imade, S., 2019. Financial ratio analysis in predicting financial conditions distress in indonesia stock

exchange. Russian Journal of Agricultural and Socio-Economic Sciences. 86(2). pp.155-165.

Books and Journals

Siziba, S. and Hall, J. H., 2021. The evolution of the application of capital budgeting techniques in enterprises. Global Finance

Journal. 47. p.100504.

Dance, M. and Imade, S., 2019. Financial ratio analysis in predicting financial conditions distress in indonesia stock

exchange. Russian Journal of Agricultural and Socio-Economic Sciences. 86(2). pp.155-165.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.