Investment Appraisal, WACC & Financial Analysis of AMP Limited

VerifiedAdded on 2023/06/04

|17

|3725

|366

Report

AI Summary

This report provides a comprehensive analysis of investment decisions and capital structure, focusing on AMP Limited. Part A involves calculating after-tax cash flows, payback period, net present value (NPV), and profitability index for proposed investment projects under different scenarios. It also includes a comparison of two investment options based on annualized cost. Part B presents an executive summary, introduction, comparative analysis of Weighted Average Cost of Capital (WACC) and capital structure, financial analysis of AMP Limited using key financial ratios, examination of major changes in AMP Limited's capital structure over the past three years, and a risk analysis. The analysis utilizes financial statements and ratios to assess the company's financial performance and stability, concluding with recommendations based on the findings. Desklib provides access to similar solved assignments.

Accounting and finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

Part A.........................................................................................................................................3

(i)............................................................................................................................................3

(ii)...........................................................................................................................................5

A.........................................................................................................................................5

B.........................................................................................................................................6

C.........................................................................................................................................7

(iii)..........................................................................................................................................7

Option A.............................................................................................................................7

Option B.............................................................................................................................8

Part B........................................................................................................................................10

Executive summary..............................................................................................................10

Introduction..........................................................................................................................10

Comparative analysis of WAACC and capital structure..................................................10

Financial analysis of AMP Limited.................................................................................12

Major changes held in the capital structure of AMP limited in past three years.............13

AMP Limited’s Risk analysis..........................................................................................14

Conclusion............................................................................................................................15

References................................................................................................................................16

Part A.........................................................................................................................................3

(i)............................................................................................................................................3

(ii)...........................................................................................................................................5

A.........................................................................................................................................5

B.........................................................................................................................................6

C.........................................................................................................................................7

(iii)..........................................................................................................................................7

Option A.............................................................................................................................7

Option B.............................................................................................................................8

Part B........................................................................................................................................10

Executive summary..............................................................................................................10

Introduction..........................................................................................................................10

Comparative analysis of WAACC and capital structure..................................................10

Financial analysis of AMP Limited.................................................................................12

Major changes held in the capital structure of AMP limited in past three years.............13

AMP Limited’s Risk analysis..........................................................................................14

Conclusion............................................................................................................................15

References................................................................................................................................16

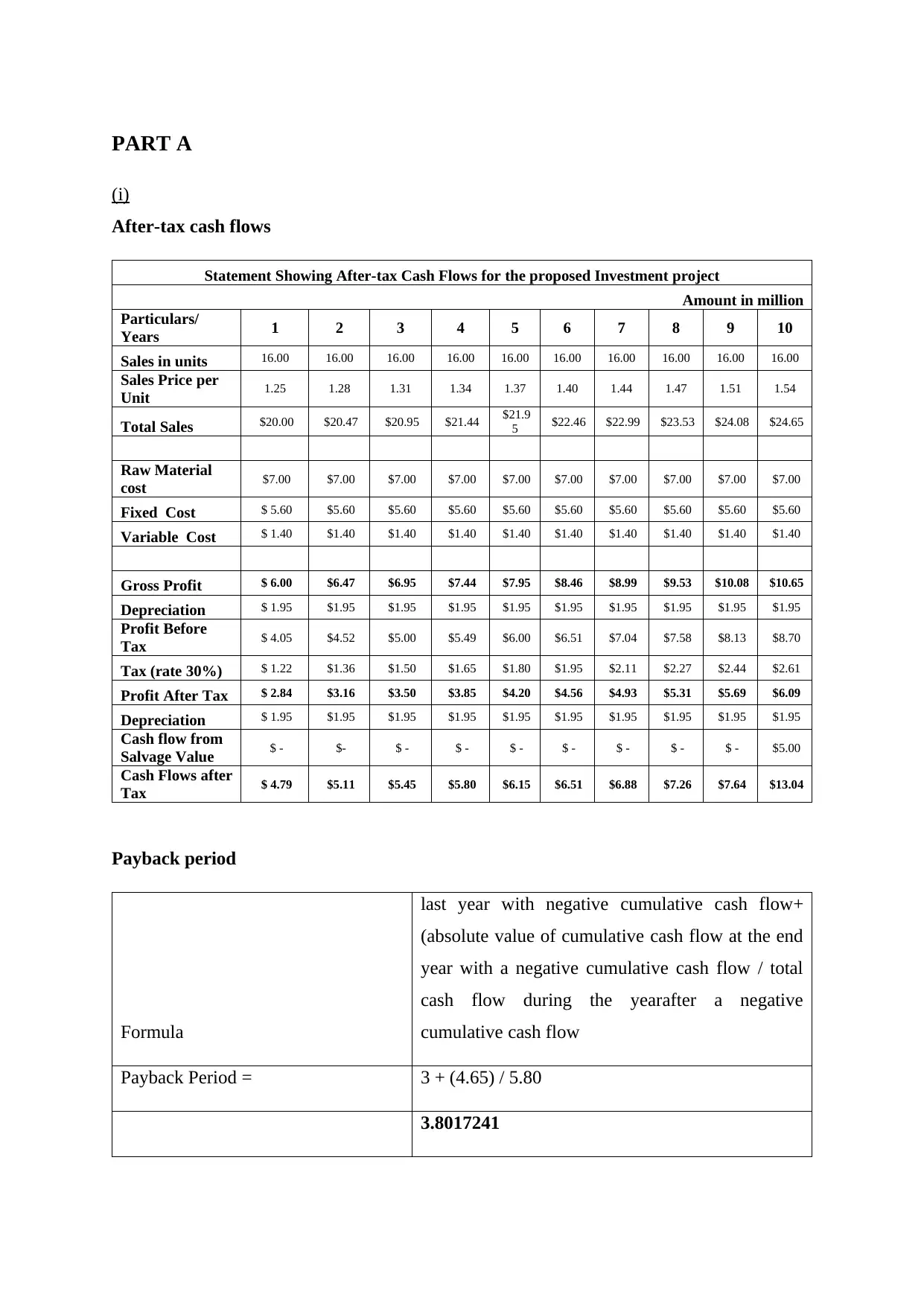

PART A

(i)

After-tax cash flows

Statement Showing After-tax Cash Flows for the proposed Investment project

Amount in million

Particulars/

Years 1 2 3 4 5 6 7 8 9 10

Sales in units 16.00 16.00 16.00 16.00 16.00 16.00 16.00 16.00 16.00 16.00

Sales Price per

Unit 1.25 1.28 1.31 1.34 1.37 1.40 1.44 1.47 1.51 1.54

Total Sales $20.00 $20.47 $20.95 $21.44 $21.9

5 $22.46 $22.99 $23.53 $24.08 $24.65

Raw Material

cost $7.00 $7.00 $7.00 $7.00 $7.00 $7.00 $7.00 $7.00 $7.00 $7.00

Fixed Cost $ 5.60 $5.60 $5.60 $5.60 $5.60 $5.60 $5.60 $5.60 $5.60 $5.60

Variable Cost $ 1.40 $1.40 $1.40 $1.40 $1.40 $1.40 $1.40 $1.40 $1.40 $1.40

Gross Profit $ 6.00 $6.47 $6.95 $7.44 $7.95 $8.46 $8.99 $9.53 $10.08 $10.65

Depreciation $ 1.95 $1.95 $1.95 $1.95 $1.95 $1.95 $1.95 $1.95 $1.95 $1.95

Profit Before

Tax $ 4.05 $4.52 $5.00 $5.49 $6.00 $6.51 $7.04 $7.58 $8.13 $8.70

Tax (rate 30%) $ 1.22 $1.36 $1.50 $1.65 $1.80 $1.95 $2.11 $2.27 $2.44 $2.61

Profit After Tax $ 2.84 $3.16 $3.50 $3.85 $4.20 $4.56 $4.93 $5.31 $5.69 $6.09

Depreciation $ 1.95 $1.95 $1.95 $1.95 $1.95 $1.95 $1.95 $1.95 $1.95 $1.95

Cash flow from

Salvage Value $ - $- $ - $ - $ - $ - $ - $ - $ - $5.00

Cash Flows after

Tax $ 4.79 $5.11 $5.45 $5.80 $6.15 $6.51 $6.88 $7.26 $7.64 $13.04

Payback period

Formula

last year with negative cumulative cash flow+

(absolute value of cumulative cash flow at the end

year with a negative cumulative cash flow / total

cash flow during the yearafter a negative

cumulative cash flow

Payback Period = 3 + (4.65) / 5.80

3.8017241

(i)

After-tax cash flows

Statement Showing After-tax Cash Flows for the proposed Investment project

Amount in million

Particulars/

Years 1 2 3 4 5 6 7 8 9 10

Sales in units 16.00 16.00 16.00 16.00 16.00 16.00 16.00 16.00 16.00 16.00

Sales Price per

Unit 1.25 1.28 1.31 1.34 1.37 1.40 1.44 1.47 1.51 1.54

Total Sales $20.00 $20.47 $20.95 $21.44 $21.9

5 $22.46 $22.99 $23.53 $24.08 $24.65

Raw Material

cost $7.00 $7.00 $7.00 $7.00 $7.00 $7.00 $7.00 $7.00 $7.00 $7.00

Fixed Cost $ 5.60 $5.60 $5.60 $5.60 $5.60 $5.60 $5.60 $5.60 $5.60 $5.60

Variable Cost $ 1.40 $1.40 $1.40 $1.40 $1.40 $1.40 $1.40 $1.40 $1.40 $1.40

Gross Profit $ 6.00 $6.47 $6.95 $7.44 $7.95 $8.46 $8.99 $9.53 $10.08 $10.65

Depreciation $ 1.95 $1.95 $1.95 $1.95 $1.95 $1.95 $1.95 $1.95 $1.95 $1.95

Profit Before

Tax $ 4.05 $4.52 $5.00 $5.49 $6.00 $6.51 $7.04 $7.58 $8.13 $8.70

Tax (rate 30%) $ 1.22 $1.36 $1.50 $1.65 $1.80 $1.95 $2.11 $2.27 $2.44 $2.61

Profit After Tax $ 2.84 $3.16 $3.50 $3.85 $4.20 $4.56 $4.93 $5.31 $5.69 $6.09

Depreciation $ 1.95 $1.95 $1.95 $1.95 $1.95 $1.95 $1.95 $1.95 $1.95 $1.95

Cash flow from

Salvage Value $ - $- $ - $ - $ - $ - $ - $ - $ - $5.00

Cash Flows after

Tax $ 4.79 $5.11 $5.45 $5.80 $6.15 $6.51 $6.88 $7.26 $7.64 $13.04

Payback period

Formula

last year with negative cumulative cash flow+

(absolute value of cumulative cash flow at the end

year with a negative cumulative cash flow / total

cash flow during the yearafter a negative

cumulative cash flow

Payback Period = 3 + (4.65) / 5.80

3.8017241

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

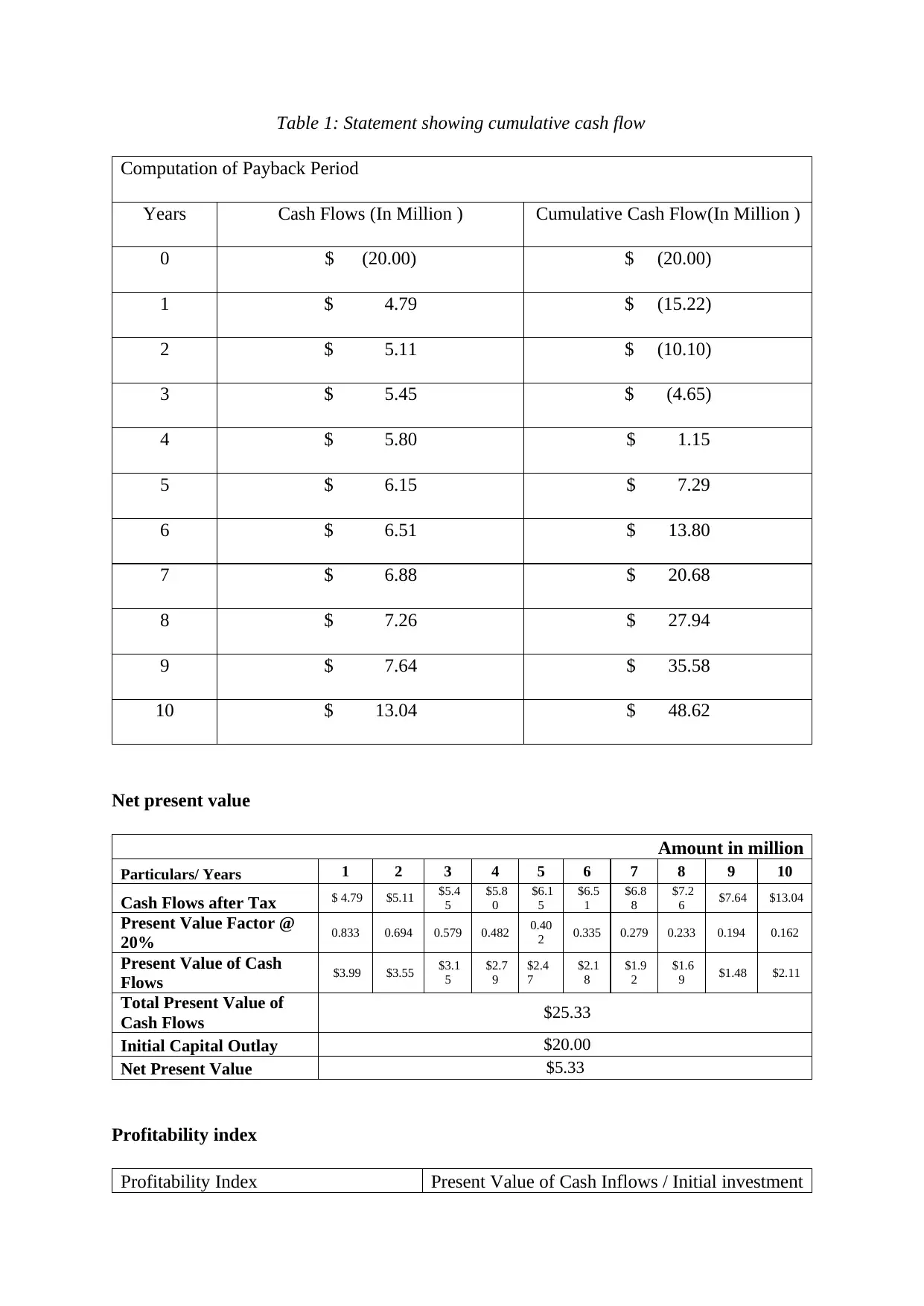

Table 1: Statement showing cumulative cash flow

Computation of Payback Period

Years Cash Flows (In Million ) Cumulative Cash Flow(In Million )

0 $ (20.00) $ (20.00)

1 $ 4.79 $ (15.22)

2 $ 5.11 $ (10.10)

3 $ 5.45 $ (4.65)

4 $ 5.80 $ 1.15

5 $ 6.15 $ 7.29

6 $ 6.51 $ 13.80

7 $ 6.88 $ 20.68

8 $ 7.26 $ 27.94

9 $ 7.64 $ 35.58

10 $ 13.04 $ 48.62

Net present value

Amount in million

Particulars/ Years 1 2 3 4 5 6 7 8 9 10

Cash Flows after Tax $ 4.79 $5.11 $5.4

5

$5.8

0

$6.1

5

$6.5

1

$6.8

8

$7.2

6 $7.64 $13.04

Present Value Factor @

20% 0.833 0.694 0.579 0.482 0.40

2 0.335 0.279 0.233 0.194 0.162

Present Value of Cash

Flows $3.99 $3.55 $3.1

5

$2.7

9

$2.4

7

$2.1

8

$1.9

2

$1.6

9 $1.48 $2.11

Total Present Value of

Cash Flows $25.33

Initial Capital Outlay $20.00

Net Present Value $5.33

Profitability index

Profitability Index Present Value of Cash Inflows / Initial investment

Computation of Payback Period

Years Cash Flows (In Million ) Cumulative Cash Flow(In Million )

0 $ (20.00) $ (20.00)

1 $ 4.79 $ (15.22)

2 $ 5.11 $ (10.10)

3 $ 5.45 $ (4.65)

4 $ 5.80 $ 1.15

5 $ 6.15 $ 7.29

6 $ 6.51 $ 13.80

7 $ 6.88 $ 20.68

8 $ 7.26 $ 27.94

9 $ 7.64 $ 35.58

10 $ 13.04 $ 48.62

Net present value

Amount in million

Particulars/ Years 1 2 3 4 5 6 7 8 9 10

Cash Flows after Tax $ 4.79 $5.11 $5.4

5

$5.8

0

$6.1

5

$6.5

1

$6.8

8

$7.2

6 $7.64 $13.04

Present Value Factor @

20% 0.833 0.694 0.579 0.482 0.40

2 0.335 0.279 0.233 0.194 0.162

Present Value of Cash

Flows $3.99 $3.55 $3.1

5

$2.7

9

$2.4

7

$2.1

8

$1.9

2

$1.6

9 $1.48 $2.11

Total Present Value of

Cash Flows $25.33

Initial Capital Outlay $20.00

Net Present Value $5.33

Profitability index

Profitability Index Present Value of Cash Inflows / Initial investment

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

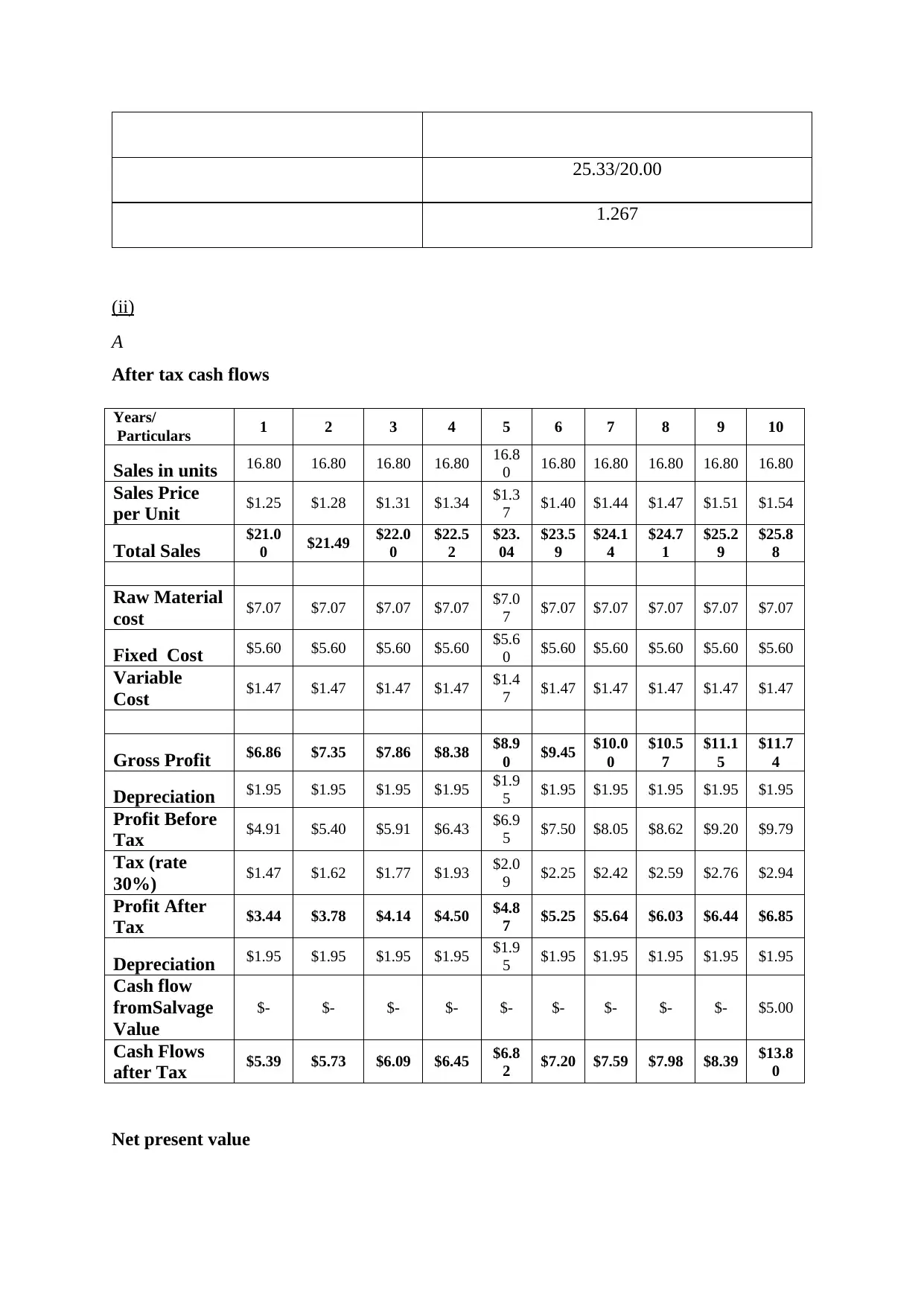

25.33/20.00

1.267

(ii)

A

After tax cash flows

Years/

Particulars 1 2 3 4 5 6 7 8 9 10

Sales in units 16.80 16.80 16.80 16.80 16.8

0 16.80 16.80 16.80 16.80 16.80

Sales Price

per Unit $1.25 $1.28 $1.31 $1.34 $1.3

7 $1.40 $1.44 $1.47 $1.51 $1.54

Total Sales $21.0

0 $21.49 $22.0

0

$22.5

2

$23.

04

$23.5

9

$24.1

4

$24.7

1

$25.2

9

$25.8

8

Raw Material

cost $7.07 $7.07 $7.07 $7.07 $7.0

7 $7.07 $7.07 $7.07 $7.07 $7.07

Fixed Cost $5.60 $5.60 $5.60 $5.60 $5.6

0 $5.60 $5.60 $5.60 $5.60 $5.60

Variable

Cost $1.47 $1.47 $1.47 $1.47 $1.4

7 $1.47 $1.47 $1.47 $1.47 $1.47

Gross Profit $6.86 $7.35 $7.86 $8.38 $8.9

0 $9.45 $10.0

0

$10.5

7

$11.1

5

$11.7

4

Depreciation $1.95 $1.95 $1.95 $1.95 $1.9

5 $1.95 $1.95 $1.95 $1.95 $1.95

Profit Before

Tax $4.91 $5.40 $5.91 $6.43 $6.9

5 $7.50 $8.05 $8.62 $9.20 $9.79

Tax (rate

30%) $1.47 $1.62 $1.77 $1.93 $2.0

9 $2.25 $2.42 $2.59 $2.76 $2.94

Profit After

Tax $3.44 $3.78 $4.14 $4.50 $4.8

7 $5.25 $5.64 $6.03 $6.44 $6.85

Depreciation $1.95 $1.95 $1.95 $1.95 $1.9

5 $1.95 $1.95 $1.95 $1.95 $1.95

Cash flow

fromSalvage

Value

$- $- $- $- $- $- $- $- $- $5.00

Cash Flows

after Tax $5.39 $5.73 $6.09 $6.45 $6.8

2 $7.20 $7.59 $7.98 $8.39 $13.8

0

Net present value

1.267

(ii)

A

After tax cash flows

Years/

Particulars 1 2 3 4 5 6 7 8 9 10

Sales in units 16.80 16.80 16.80 16.80 16.8

0 16.80 16.80 16.80 16.80 16.80

Sales Price

per Unit $1.25 $1.28 $1.31 $1.34 $1.3

7 $1.40 $1.44 $1.47 $1.51 $1.54

Total Sales $21.0

0 $21.49 $22.0

0

$22.5

2

$23.

04

$23.5

9

$24.1

4

$24.7

1

$25.2

9

$25.8

8

Raw Material

cost $7.07 $7.07 $7.07 $7.07 $7.0

7 $7.07 $7.07 $7.07 $7.07 $7.07

Fixed Cost $5.60 $5.60 $5.60 $5.60 $5.6

0 $5.60 $5.60 $5.60 $5.60 $5.60

Variable

Cost $1.47 $1.47 $1.47 $1.47 $1.4

7 $1.47 $1.47 $1.47 $1.47 $1.47

Gross Profit $6.86 $7.35 $7.86 $8.38 $8.9

0 $9.45 $10.0

0

$10.5

7

$11.1

5

$11.7

4

Depreciation $1.95 $1.95 $1.95 $1.95 $1.9

5 $1.95 $1.95 $1.95 $1.95 $1.95

Profit Before

Tax $4.91 $5.40 $5.91 $6.43 $6.9

5 $7.50 $8.05 $8.62 $9.20 $9.79

Tax (rate

30%) $1.47 $1.62 $1.77 $1.93 $2.0

9 $2.25 $2.42 $2.59 $2.76 $2.94

Profit After

Tax $3.44 $3.78 $4.14 $4.50 $4.8

7 $5.25 $5.64 $6.03 $6.44 $6.85

Depreciation $1.95 $1.95 $1.95 $1.95 $1.9

5 $1.95 $1.95 $1.95 $1.95 $1.95

Cash flow

fromSalvage

Value

$- $- $- $- $- $- $- $- $- $5.00

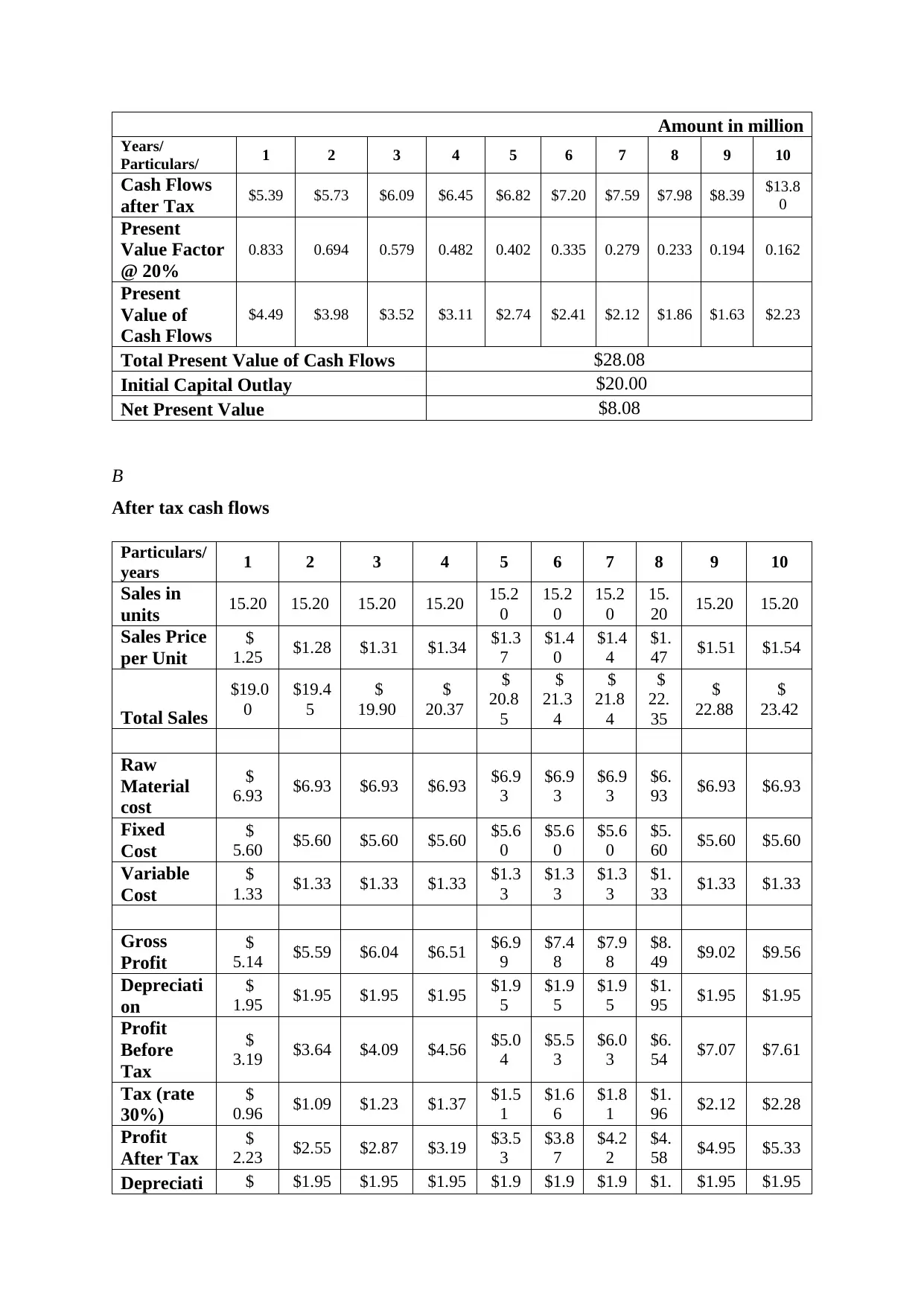

Cash Flows

after Tax $5.39 $5.73 $6.09 $6.45 $6.8

2 $7.20 $7.59 $7.98 $8.39 $13.8

0

Net present value

Amount in million

Years/

Particulars/ 1 2 3 4 5 6 7 8 9 10

Cash Flows

after Tax $5.39 $5.73 $6.09 $6.45 $6.82 $7.20 $7.59 $7.98 $8.39 $13.8

0

Present

Value Factor

@ 20%

0.833 0.694 0.579 0.482 0.402 0.335 0.279 0.233 0.194 0.162

Present

Value of

Cash Flows

$4.49 $3.98 $3.52 $3.11 $2.74 $2.41 $2.12 $1.86 $1.63 $2.23

Total Present Value of Cash Flows $28.08

Initial Capital Outlay $20.00

Net Present Value $8.08

B

After tax cash flows

Particulars/

years 1 2 3 4 5 6 7 8 9 10

Sales in

units 15.20 15.20 15.20 15.20 15.2

0

15.2

0

15.2

0

15.

20 15.20 15.20

Sales Price

per Unit

$

1.25 $1.28 $1.31 $1.34 $1.3

7

$1.4

0

$1.4

4

$1.

47 $1.51 $1.54

Total Sales

$19.0

0

$19.4

5

$

19.90

$

20.37

$

20.8

5

$

21.3

4

$

21.8

4

$

22.

35

$

22.88

$

23.42

Raw

Material

cost

$

6.93 $6.93 $6.93 $6.93 $6.9

3

$6.9

3

$6.9

3

$6.

93 $6.93 $6.93

Fixed

Cost

$

5.60 $5.60 $5.60 $5.60 $5.6

0

$5.6

0

$5.6

0

$5.

60 $5.60 $5.60

Variable

Cost

$

1.33 $1.33 $1.33 $1.33 $1.3

3

$1.3

3

$1.3

3

$1.

33 $1.33 $1.33

Gross

Profit

$

5.14 $5.59 $6.04 $6.51 $6.9

9

$7.4

8

$7.9

8

$8.

49 $9.02 $9.56

Depreciati

on

$

1.95 $1.95 $1.95 $1.95 $1.9

5

$1.9

5

$1.9

5

$1.

95 $1.95 $1.95

Profit

Before

Tax

$

3.19 $3.64 $4.09 $4.56 $5.0

4

$5.5

3

$6.0

3

$6.

54 $7.07 $7.61

Tax (rate

30%)

$

0.96 $1.09 $1.23 $1.37 $1.5

1

$1.6

6

$1.8

1

$1.

96 $2.12 $2.28

Profit

After Tax

$

2.23 $2.55 $2.87 $3.19 $3.5

3

$3.8

7

$4.2

2

$4.

58 $4.95 $5.33

Depreciati $ $1.95 $1.95 $1.95 $1.9 $1.9 $1.9 $1. $1.95 $1.95

Years/

Particulars/ 1 2 3 4 5 6 7 8 9 10

Cash Flows

after Tax $5.39 $5.73 $6.09 $6.45 $6.82 $7.20 $7.59 $7.98 $8.39 $13.8

0

Present

Value Factor

@ 20%

0.833 0.694 0.579 0.482 0.402 0.335 0.279 0.233 0.194 0.162

Present

Value of

Cash Flows

$4.49 $3.98 $3.52 $3.11 $2.74 $2.41 $2.12 $1.86 $1.63 $2.23

Total Present Value of Cash Flows $28.08

Initial Capital Outlay $20.00

Net Present Value $8.08

B

After tax cash flows

Particulars/

years 1 2 3 4 5 6 7 8 9 10

Sales in

units 15.20 15.20 15.20 15.20 15.2

0

15.2

0

15.2

0

15.

20 15.20 15.20

Sales Price

per Unit

$

1.25 $1.28 $1.31 $1.34 $1.3

7

$1.4

0

$1.4

4

$1.

47 $1.51 $1.54

Total Sales

$19.0

0

$19.4

5

$

19.90

$

20.37

$

20.8

5

$

21.3

4

$

21.8

4

$

22.

35

$

22.88

$

23.42

Raw

Material

cost

$

6.93 $6.93 $6.93 $6.93 $6.9

3

$6.9

3

$6.9

3

$6.

93 $6.93 $6.93

Fixed

Cost

$

5.60 $5.60 $5.60 $5.60 $5.6

0

$5.6

0

$5.6

0

$5.

60 $5.60 $5.60

Variable

Cost

$

1.33 $1.33 $1.33 $1.33 $1.3

3

$1.3

3

$1.3

3

$1.

33 $1.33 $1.33

Gross

Profit

$

5.14 $5.59 $6.04 $6.51 $6.9

9

$7.4

8

$7.9

8

$8.

49 $9.02 $9.56

Depreciati

on

$

1.95 $1.95 $1.95 $1.95 $1.9

5

$1.9

5

$1.9

5

$1.

95 $1.95 $1.95

Profit

Before

Tax

$

3.19 $3.64 $4.09 $4.56 $5.0

4

$5.5

3

$6.0

3

$6.

54 $7.07 $7.61

Tax (rate

30%)

$

0.96 $1.09 $1.23 $1.37 $1.5

1

$1.6

6

$1.8

1

$1.

96 $2.12 $2.28

Profit

After Tax

$

2.23 $2.55 $2.87 $3.19 $3.5

3

$3.8

7

$4.2

2

$4.

58 $4.95 $5.33

Depreciati $ $1.95 $1.95 $1.95 $1.9 $1.9 $1.9 $1. $1.95 $1.95

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

on 1.95 5 5 5 95

Cash flow

fromSalva

ge Value

$ - $ - $ - $ - $ - $ - $ - $ - $ - $5.00

Cash

Flows

after Tax

$

4.18 $4.50 $4.82 $5.14 $5.4

8

$5.8

2

$6.1

7

$6.

53 $6.90 $

12.28

Net present value

Particulars/

years 1 2 3 4 5 6 7 8 9 10

Cash Flows

after Tax $4.18 $4.5

0

$4.8

2

$

5.14

$

5.48

$

5.82

$

6.17

$

6.53 $ 6.90 $12.28

Present Value

Factor @

20%

0.833 0.694 0.579 0.482 0.40

2 0.335 0.27

9 0.233 0.194 0.162

Present Value

of Cash Flows $3.49 $3.12 $2.79 $2.48 $2.2

0 $1.95 $1.7

2 $1.52 $1.34 $1.98

Total Present Value of Cash Flows $22.59

Initial Capital Outlay $20.00

Net Present Value $2.59

C

By considering the above calculations, it can be noticed that the project should be accepted as

even by consideration of decline project is generating a positive return, i.e. positive net

present value. Therefore, even if the projection of cash flows are not as per expectations, the

proposed investment will provide benefit to the company.

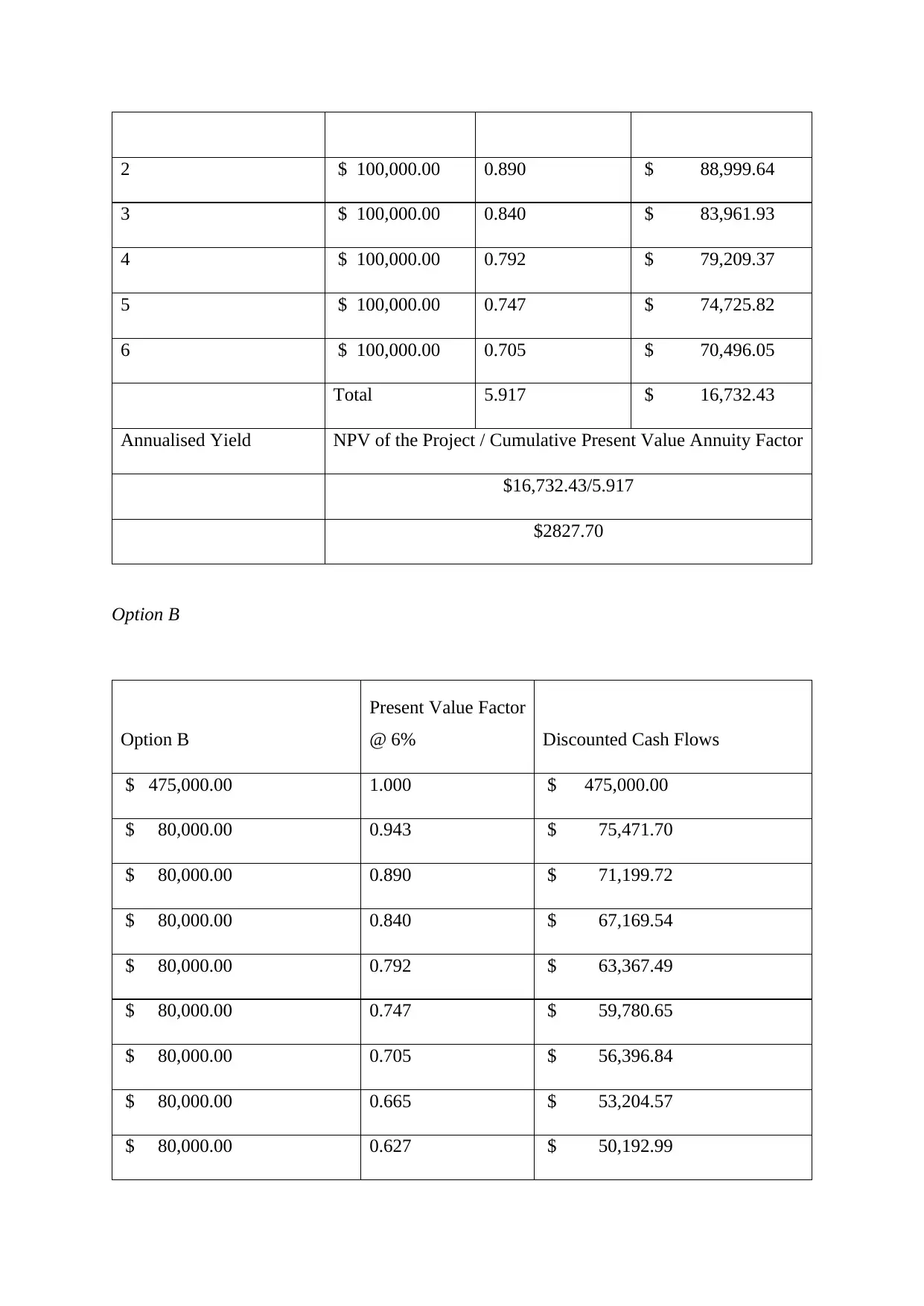

(iii)

In both the investment options, the life of the project is different. Therefore evaluation of

both the projects will be done by considering annualised cost so that NPV of both the projects

can be compared.

Option A

Years Option A

Present Value

Factor @ 6%

Discounted Cash

Flows

0 $ 475,000.00 1.000 $ (475,000.00)

1 $ 100,000.00 0.943 $ 94,339.62

Cash flow

fromSalva

ge Value

$ - $ - $ - $ - $ - $ - $ - $ - $ - $5.00

Cash

Flows

after Tax

$

4.18 $4.50 $4.82 $5.14 $5.4

8

$5.8

2

$6.1

7

$6.

53 $6.90 $

12.28

Net present value

Particulars/

years 1 2 3 4 5 6 7 8 9 10

Cash Flows

after Tax $4.18 $4.5

0

$4.8

2

$

5.14

$

5.48

$

5.82

$

6.17

$

6.53 $ 6.90 $12.28

Present Value

Factor @

20%

0.833 0.694 0.579 0.482 0.40

2 0.335 0.27

9 0.233 0.194 0.162

Present Value

of Cash Flows $3.49 $3.12 $2.79 $2.48 $2.2

0 $1.95 $1.7

2 $1.52 $1.34 $1.98

Total Present Value of Cash Flows $22.59

Initial Capital Outlay $20.00

Net Present Value $2.59

C

By considering the above calculations, it can be noticed that the project should be accepted as

even by consideration of decline project is generating a positive return, i.e. positive net

present value. Therefore, even if the projection of cash flows are not as per expectations, the

proposed investment will provide benefit to the company.

(iii)

In both the investment options, the life of the project is different. Therefore evaluation of

both the projects will be done by considering annualised cost so that NPV of both the projects

can be compared.

Option A

Years Option A

Present Value

Factor @ 6%

Discounted Cash

Flows

0 $ 475,000.00 1.000 $ (475,000.00)

1 $ 100,000.00 0.943 $ 94,339.62

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2 $ 100,000.00 0.890 $ 88,999.64

3 $ 100,000.00 0.840 $ 83,961.93

4 $ 100,000.00 0.792 $ 79,209.37

5 $ 100,000.00 0.747 $ 74,725.82

6 $ 100,000.00 0.705 $ 70,496.05

Total 5.917 $ 16,732.43

Annualised Yield NPV of the Project / Cumulative Present Value Annuity Factor

$16,732.43/5.917

$2827.70

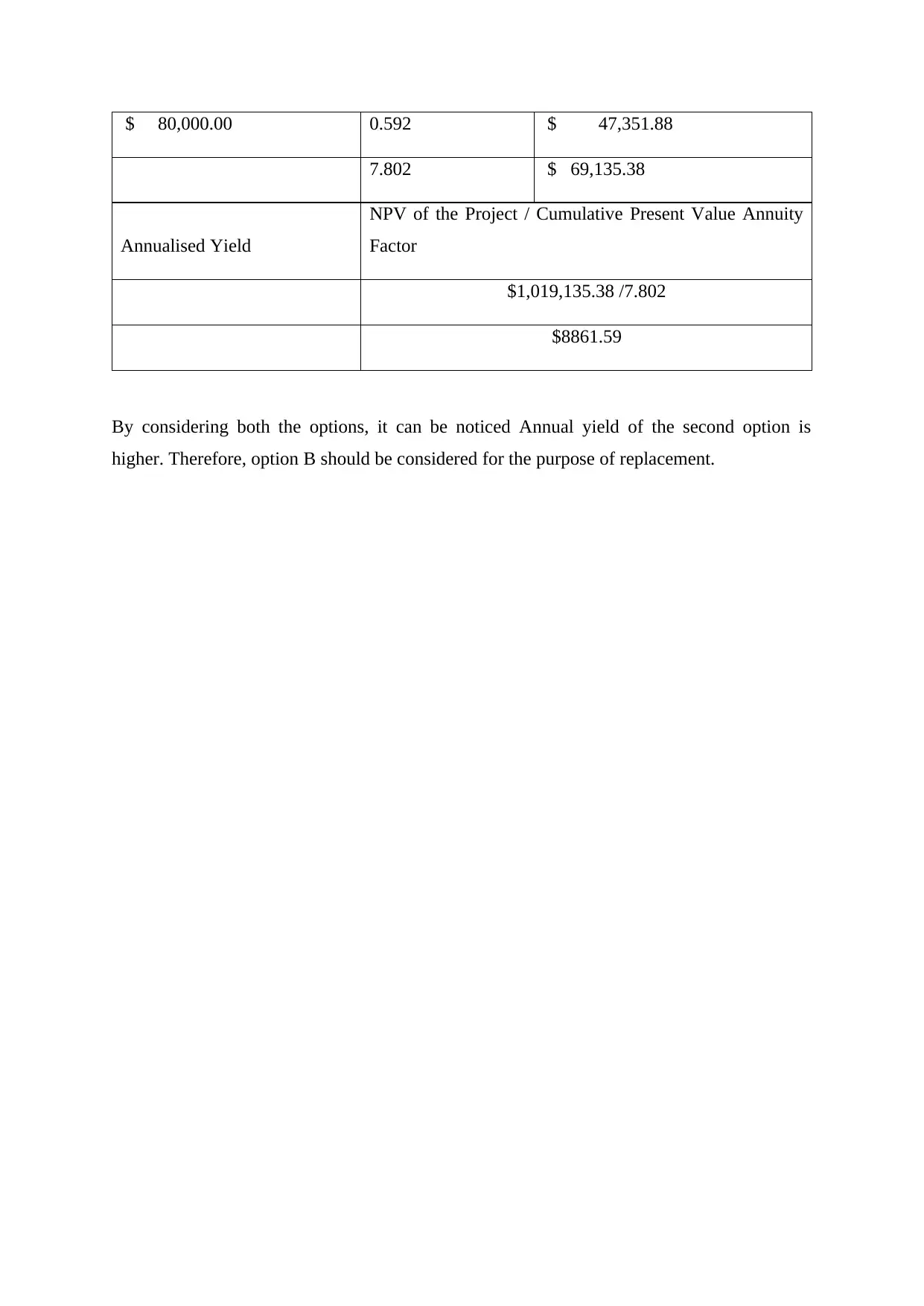

Option B

Option B

Present Value Factor

@ 6% Discounted Cash Flows

$ 475,000.00 1.000 $ 475,000.00

$ 80,000.00 0.943 $ 75,471.70

$ 80,000.00 0.890 $ 71,199.72

$ 80,000.00 0.840 $ 67,169.54

$ 80,000.00 0.792 $ 63,367.49

$ 80,000.00 0.747 $ 59,780.65

$ 80,000.00 0.705 $ 56,396.84

$ 80,000.00 0.665 $ 53,204.57

$ 80,000.00 0.627 $ 50,192.99

3 $ 100,000.00 0.840 $ 83,961.93

4 $ 100,000.00 0.792 $ 79,209.37

5 $ 100,000.00 0.747 $ 74,725.82

6 $ 100,000.00 0.705 $ 70,496.05

Total 5.917 $ 16,732.43

Annualised Yield NPV of the Project / Cumulative Present Value Annuity Factor

$16,732.43/5.917

$2827.70

Option B

Option B

Present Value Factor

@ 6% Discounted Cash Flows

$ 475,000.00 1.000 $ 475,000.00

$ 80,000.00 0.943 $ 75,471.70

$ 80,000.00 0.890 $ 71,199.72

$ 80,000.00 0.840 $ 67,169.54

$ 80,000.00 0.792 $ 63,367.49

$ 80,000.00 0.747 $ 59,780.65

$ 80,000.00 0.705 $ 56,396.84

$ 80,000.00 0.665 $ 53,204.57

$ 80,000.00 0.627 $ 50,192.99

$ 80,000.00 0.592 $ 47,351.88

7.802 $ 69,135.38

Annualised Yield

NPV of the Project / Cumulative Present Value Annuity

Factor

$1,019,135.38 /7.802

$8861.59

By considering both the options, it can be noticed Annual yield of the second option is

higher. Therefore, option B should be considered for the purpose of replacement.

7.802 $ 69,135.38

Annualised Yield

NPV of the Project / Cumulative Present Value Annuity

Factor

$1,019,135.38 /7.802

$8861.59

By considering both the options, it can be noticed Annual yield of the second option is

higher. Therefore, option B should be considered for the purpose of replacement.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

PART B

Executive summary

Financial analysis is considered as the procedure of assessing business, budgets, projects and

another financial related business enterprise to identify the validity and performance. It is

employed to evaluate if or if not the business entity has enough profitability, solvency,

stability and liquidity to ensure a monetary investment. The prevailing study is based on the

financial analysis of the AMP limited to assess the involved risks and estimate the

performance of the company. The present study shows that the company has maintained an

effective financial structure, by raising balanced equity and debt and fixing the returns of

shareholders.

Introduction

The present study aims to evaluate and analyze the Annual Report of AMP Limited critically;

so as to conduct the comparative analysis of WAACC and capital structure, as well as the

study also covers the evaluation of key financial ratios of the AMP limited, to assess the

financial performance of the company. Following to this, the study also intends to consider

the major changes held in the capital structure of AMP limited in the past three years, with

the consideration towards the material risks identified in the annual report supported by the

appropriate mitigation strategies adopted by the company.

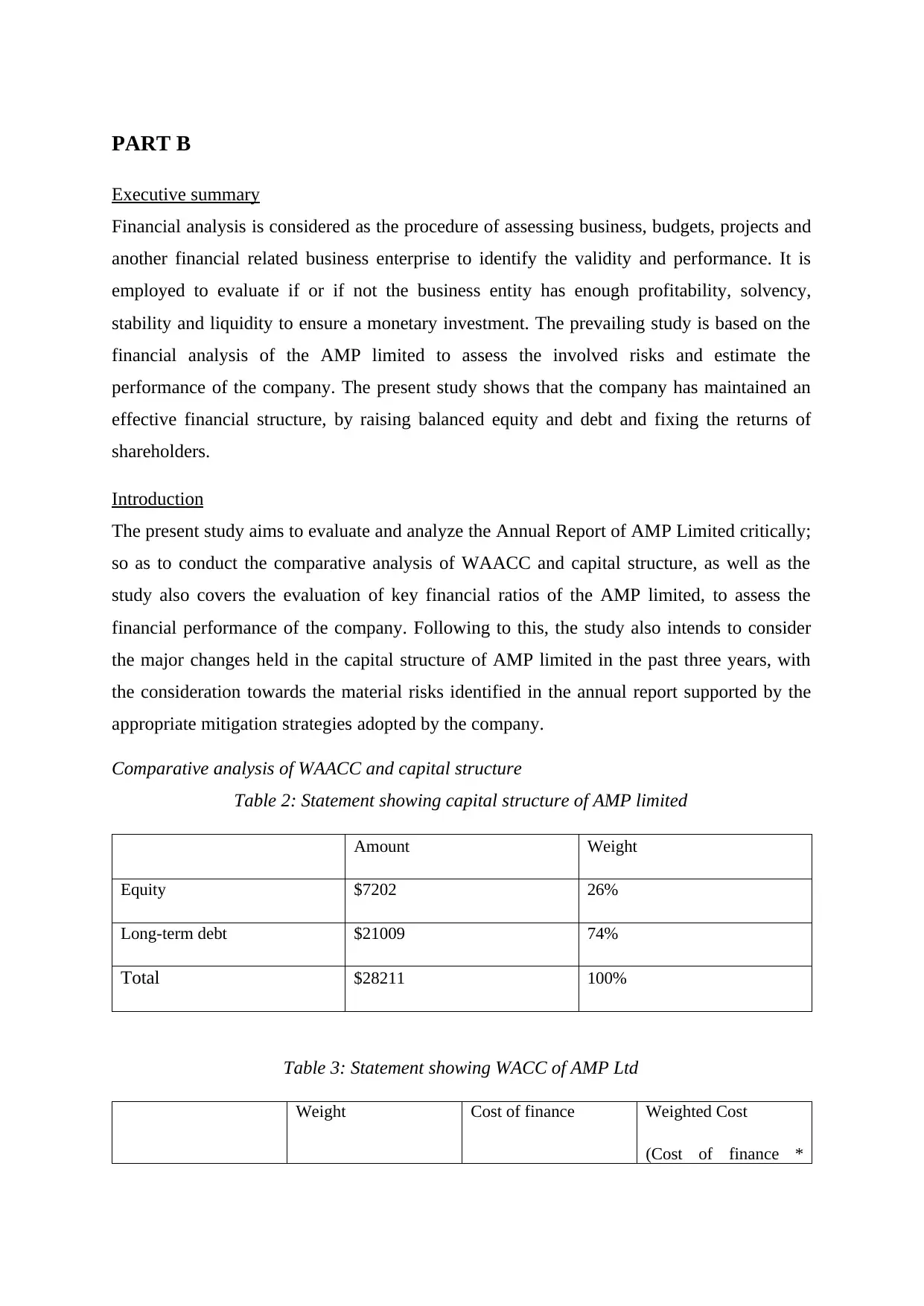

Comparative analysis of WAACC and capital structure

Table 2: Statement showing capital structure of AMP limited

Amount Weight

Equity $7202 26%

Long-term debt $21009 74%

Total $28211 100%

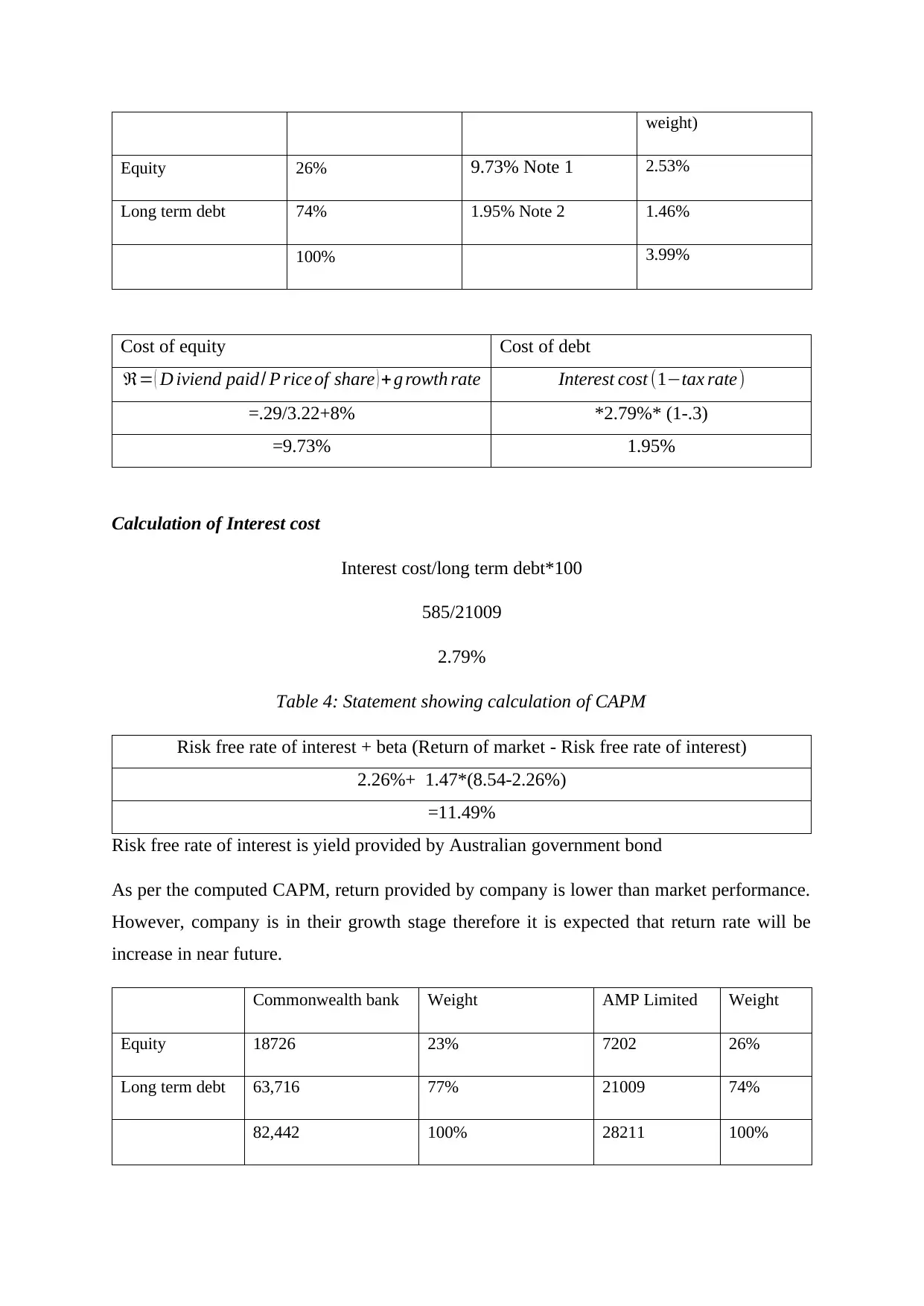

Table 3: Statement showing WACC of AMP Ltd

Weight Cost of finance Weighted Cost

(Cost of finance *

Executive summary

Financial analysis is considered as the procedure of assessing business, budgets, projects and

another financial related business enterprise to identify the validity and performance. It is

employed to evaluate if or if not the business entity has enough profitability, solvency,

stability and liquidity to ensure a monetary investment. The prevailing study is based on the

financial analysis of the AMP limited to assess the involved risks and estimate the

performance of the company. The present study shows that the company has maintained an

effective financial structure, by raising balanced equity and debt and fixing the returns of

shareholders.

Introduction

The present study aims to evaluate and analyze the Annual Report of AMP Limited critically;

so as to conduct the comparative analysis of WAACC and capital structure, as well as the

study also covers the evaluation of key financial ratios of the AMP limited, to assess the

financial performance of the company. Following to this, the study also intends to consider

the major changes held in the capital structure of AMP limited in the past three years, with

the consideration towards the material risks identified in the annual report supported by the

appropriate mitigation strategies adopted by the company.

Comparative analysis of WAACC and capital structure

Table 2: Statement showing capital structure of AMP limited

Amount Weight

Equity $7202 26%

Long-term debt $21009 74%

Total $28211 100%

Table 3: Statement showing WACC of AMP Ltd

Weight Cost of finance Weighted Cost

(Cost of finance *

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

weight)

Equity 26% 9.73% Note 1 2.53%

Long term debt 74% 1.95% Note 2 1.46%

100% 3.99%

Cost of equity Cost of debt

ℜ= ( D iviend paid/ P rice of share ) + g rowth rate Interest cost (1−tax rate)

=.29/3.22+8% *2.79%* (1-.3)

=9.73% 1.95%

Calculation of Interest cost

Interest cost/long term debt*100

585/21009

2.79%

Table 4: Statement showing calculation of CAPM

Risk free rate of interest + beta (Return of market - Risk free rate of interest)

2.26%+ 1.47*(8.54-2.26%)

=11.49%

Risk free rate of interest is yield provided by Australian government bond

As per the computed CAPM, return provided by company is lower than market performance.

However, company is in their growth stage therefore it is expected that return rate will be

increase in near future.

Commonwealth bank Weight AMP Limited Weight

Equity 18726 23% 7202 26%

Long term debt 63,716 77% 21009 74%

82,442 100% 28211 100%

Equity 26% 9.73% Note 1 2.53%

Long term debt 74% 1.95% Note 2 1.46%

100% 3.99%

Cost of equity Cost of debt

ℜ= ( D iviend paid/ P rice of share ) + g rowth rate Interest cost (1−tax rate)

=.29/3.22+8% *2.79%* (1-.3)

=9.73% 1.95%

Calculation of Interest cost

Interest cost/long term debt*100

585/21009

2.79%

Table 4: Statement showing calculation of CAPM

Risk free rate of interest + beta (Return of market - Risk free rate of interest)

2.26%+ 1.47*(8.54-2.26%)

=11.49%

Risk free rate of interest is yield provided by Australian government bond

As per the computed CAPM, return provided by company is lower than market performance.

However, company is in their growth stage therefore it is expected that return rate will be

increase in near future.

Commonwealth bank Weight AMP Limited Weight

Equity 18726 23% 7202 26%

Long term debt 63,716 77% 21009 74%

82,442 100% 28211 100%

By considering capital structure of both the companies it can be noticed that both the

companies had considered similar strategy for maintaining capital structure. It is because;

both the banking organisations are profit making entities therefore to ensure optimum capital

cost it is viable to keep the portion of debt higher than equity.

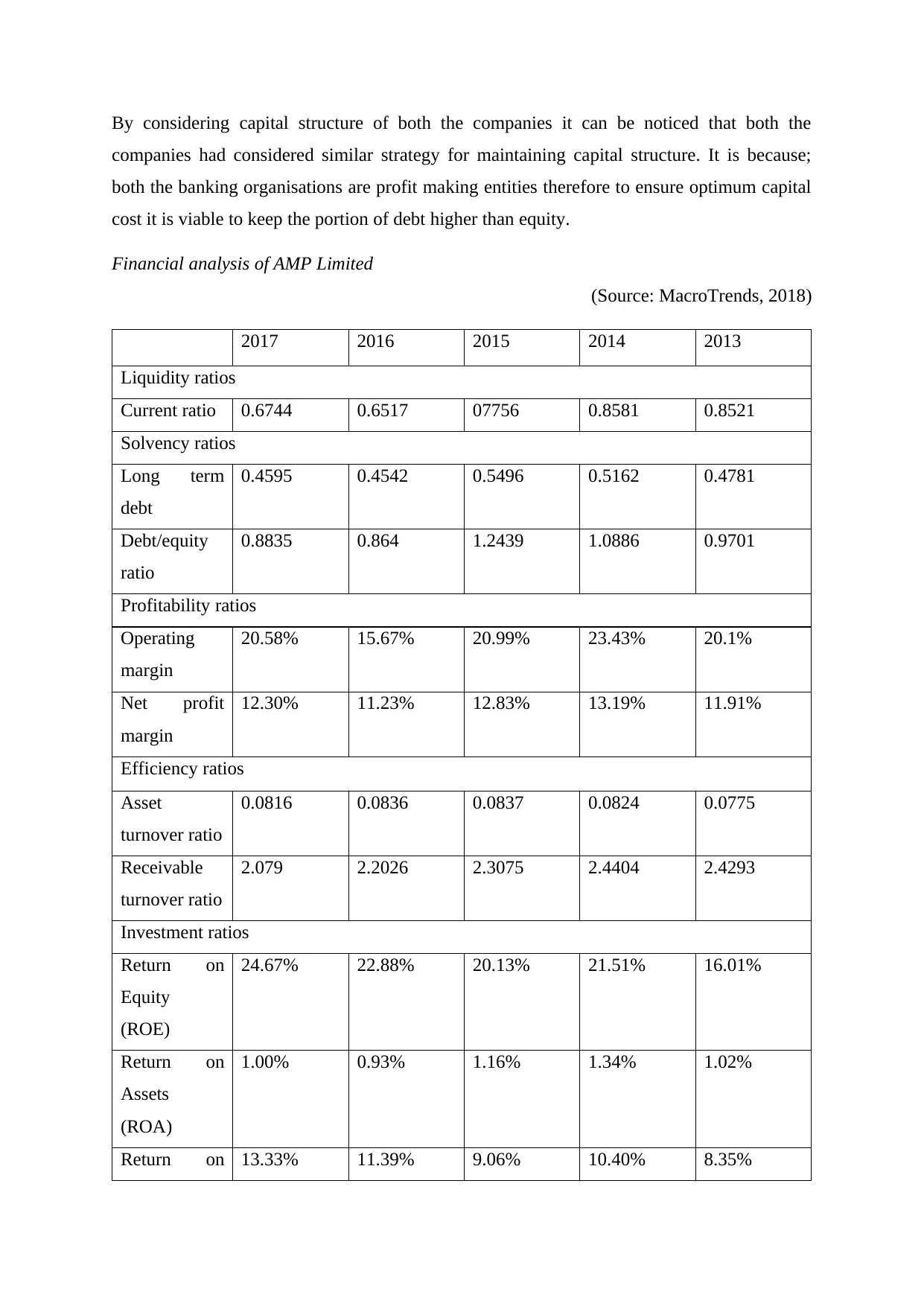

Financial analysis of AMP Limited

(Source: MacroTrends, 2018)

2017 2016 2015 2014 2013

Liquidity ratios

Current ratio 0.6744 0.6517 07756 0.8581 0.8521

Solvency ratios

Long term

debt

0.4595 0.4542 0.5496 0.5162 0.4781

Debt/equity

ratio

0.8835 0.864 1.2439 1.0886 0.9701

Profitability ratios

Operating

margin

20.58% 15.67% 20.99% 23.43% 20.1%

Net profit

margin

12.30% 11.23% 12.83% 13.19% 11.91%

Efficiency ratios

Asset

turnover ratio

0.0816 0.0836 0.0837 0.0824 0.0775

Receivable

turnover ratio

2.079 2.2026 2.3075 2.4404 2.4293

Investment ratios

Return on

Equity

(ROE)

24.67% 22.88% 20.13% 21.51% 16.01%

Return on

Assets

(ROA)

1.00% 0.93% 1.16% 1.34% 1.02%

Return on 13.33% 11.39% 9.06% 10.40% 8.35%

companies had considered similar strategy for maintaining capital structure. It is because;

both the banking organisations are profit making entities therefore to ensure optimum capital

cost it is viable to keep the portion of debt higher than equity.

Financial analysis of AMP Limited

(Source: MacroTrends, 2018)

2017 2016 2015 2014 2013

Liquidity ratios

Current ratio 0.6744 0.6517 07756 0.8581 0.8521

Solvency ratios

Long term

debt

0.4595 0.4542 0.5496 0.5162 0.4781

Debt/equity

ratio

0.8835 0.864 1.2439 1.0886 0.9701

Profitability ratios

Operating

margin

20.58% 15.67% 20.99% 23.43% 20.1%

Net profit

margin

12.30% 11.23% 12.83% 13.19% 11.91%

Efficiency ratios

Asset

turnover ratio

0.0816 0.0836 0.0837 0.0824 0.0775

Receivable

turnover ratio

2.079 2.2026 2.3075 2.4404 2.4293

Investment ratios

Return on

Equity

(ROE)

24.67% 22.88% 20.13% 21.51% 16.01%

Return on

Assets

(ROA)

1.00% 0.93% 1.16% 1.34% 1.02%

Return on 13.33% 11.39% 9.06% 10.40% 8.35%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.