SD Ltd: Report on Capital Investment Appraisal for Machinery

VerifiedAdded on 2020/05/11

|14

|4051

|32

Report

AI Summary

This report presents a financial analysis of SD Ltd's investment proposals for new machinery, focusing on the selection between G120 and Z125 models. It critically discusses the usefulness of various capital investment appraisal measures, including Accounting Rate of Return (ARR), Payback Period, Net Present Value (NPV), and Internal Rate of Return (IRR). The analysis includes detailed calculations and comparisons of these methods to determine the most appropriate investment option. The report recommends the selection of G120 based on ARR, Payback, and IRR, while NPV favors Z125. It also examines the confidence of the finance director in achieving a certain IRR and the impact of a potential new engine build plant. The conclusion synthesizes the findings and provides a final recommendation for SD Ltd, supported by the analysis of each capital budgeting technique.

Financial analysis and Management

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Introduction................................................................................................................................3

Critical Discussion of Usefulness of the Respective Capital Investment Appraisal Measures

Recommendations for Selection of an Option...........................................................................4

Accounting Rate of Return.....................................................................................................4

Payback period.......................................................................................................................4

Net Present Value (NPV).......................................................................................................5

Internal Rate of return (IRR)..................................................................................................6

Recommendation....................................................................................................................7

Reasons for payback favor to the G120 option and NPV the Z125 option in the given case....8

Analysis of Confidence of Finance Director in the given case about achieving IRR would in

excess of 15% for both options of G120 and Z125....................................................................9

Impact of the Investment Option of a potential purchase of new engine build plant of cost

£2,080,000 with a NPV of £140,800 on the G120 and Z125 investment decision..................10

Conclusion................................................................................................................................11

References................................................................................................................................13

2

Introduction................................................................................................................................3

Critical Discussion of Usefulness of the Respective Capital Investment Appraisal Measures

Recommendations for Selection of an Option...........................................................................4

Accounting Rate of Return.....................................................................................................4

Payback period.......................................................................................................................4

Net Present Value (NPV).......................................................................................................5

Internal Rate of return (IRR)..................................................................................................6

Recommendation....................................................................................................................7

Reasons for payback favor to the G120 option and NPV the Z125 option in the given case....8

Analysis of Confidence of Finance Director in the given case about achieving IRR would in

excess of 15% for both options of G120 and Z125....................................................................9

Impact of the Investment Option of a potential purchase of new engine build plant of cost

£2,080,000 with a NPV of £140,800 on the G120 and Z125 investment decision..................10

Conclusion................................................................................................................................11

References................................................................................................................................13

2

Introduction

The present report aims to present an analysis of the investment proposals that are

considered by SD Ltd for investing in new machinery. The capital budgeting decisions are

very crucial for a business entity in order to select the most profitable investment option that

will improve the business performance in future context. The capital budgeting can be stated

to be a step by step process that a business entity uses for determining the benefits of an

investment project (Bhimani, 2006). The capital budgeting seeks to analyse the risks and

returns of a project and thus help in selecting the most attractive option based on their

accountability. There are various techniques of capital budgeting used by project managers

for analyzing the profitability of a project that are accounting rate of return, payback period,

net present value and internal rate of return. The business entities are able to select the most

appropriate investment option as per their requirements based on the results of the capital

budgeting techniques. The business entities can predict the future cash flows through the help

of capital budgeting decisions for developing their potential growth strategies and objectives

(Huang, 2010).

The selection of a most feasible investment strategy is essential for business entities to

achieving competitive advantage in the market place and thus ensuring their sustainable

growth and development (Peterson and Fabozzi, 2004). The business expansion and

development depends on the capital budgeting decisions and in this context this report

evaluates the investment options presented before SD Ltd. The SD Ltd is considering to

either implementing G120 or Z125 machinery for automating its production and thus

reducing its operational cost. In this context, the report provides an analysis of different

capital investment appraisal measures in order to select the most appropriate option.

3

The present report aims to present an analysis of the investment proposals that are

considered by SD Ltd for investing in new machinery. The capital budgeting decisions are

very crucial for a business entity in order to select the most profitable investment option that

will improve the business performance in future context. The capital budgeting can be stated

to be a step by step process that a business entity uses for determining the benefits of an

investment project (Bhimani, 2006). The capital budgeting seeks to analyse the risks and

returns of a project and thus help in selecting the most attractive option based on their

accountability. There are various techniques of capital budgeting used by project managers

for analyzing the profitability of a project that are accounting rate of return, payback period,

net present value and internal rate of return. The business entities are able to select the most

appropriate investment option as per their requirements based on the results of the capital

budgeting techniques. The business entities can predict the future cash flows through the help

of capital budgeting decisions for developing their potential growth strategies and objectives

(Huang, 2010).

The selection of a most feasible investment strategy is essential for business entities to

achieving competitive advantage in the market place and thus ensuring their sustainable

growth and development (Peterson and Fabozzi, 2004). The business expansion and

development depends on the capital budgeting decisions and in this context this report

evaluates the investment options presented before SD Ltd. The SD Ltd is considering to

either implementing G120 or Z125 machinery for automating its production and thus

reducing its operational cost. In this context, the report provides an analysis of different

capital investment appraisal measures in order to select the most appropriate option.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Critical Discussion of Usefulness of the Respective Capital Investment Appraisal

Measures Recommendations for Selection of an Option

The different capital investment appraisal measures are analyzed as follows:

Accounting Rate of Return

It is also known as average rate of return (ARR) and is used for selecting the

feasibility of an investment option. It is calculated through dividing the average annual

accounting profit to be realized from a project by initial investment. The project is accepted if

the ARR is greater than required rate of return (Baker and English, 2011). The main

advantage of use of this method is that is easy to implement and to use for analyzing the

feasibility of a project (Besley and Brigham, 2008). The method is not largely used by the

project managers during capital budgeting decisions as it does not take into account the

concept of time value of money that can impact the profit generated from a project with

change in the interest rates. The ARR method is also mainly based on computing the profits

that can be easily manipulated with the change in deprecation methods. Thus, it can provide

misleading results during analysis and selection of different investment options. It does not

take into account the cash flows realized from an investment proposal and therefore do not

provide accurate results (Nwogugu, 2017).

In addition to this, the method also does not take into consideration the increase in

risks of the project over long period of time. The method also is not appropriate for

comparison of different projects as it does not consider other factors that should be evaluated

for comparison of different projects. The accounting rate of return for the two given options

for investment in machinery is different as given in the table. The ARR for G120 is 18% and

for the Z125 is 14.7% and therefore on the basis of ARR the SD Ltd is recommended to

select the investment proposal of investing in G120 machinery (Wilson, 2015).

Payback period

4

Measures Recommendations for Selection of an Option

The different capital investment appraisal measures are analyzed as follows:

Accounting Rate of Return

It is also known as average rate of return (ARR) and is used for selecting the

feasibility of an investment option. It is calculated through dividing the average annual

accounting profit to be realized from a project by initial investment. The project is accepted if

the ARR is greater than required rate of return (Baker and English, 2011). The main

advantage of use of this method is that is easy to implement and to use for analyzing the

feasibility of a project (Besley and Brigham, 2008). The method is not largely used by the

project managers during capital budgeting decisions as it does not take into account the

concept of time value of money that can impact the profit generated from a project with

change in the interest rates. The ARR method is also mainly based on computing the profits

that can be easily manipulated with the change in deprecation methods. Thus, it can provide

misleading results during analysis and selection of different investment options. It does not

take into account the cash flows realized from an investment proposal and therefore do not

provide accurate results (Nwogugu, 2017).

In addition to this, the method also does not take into consideration the increase in

risks of the project over long period of time. The method also is not appropriate for

comparison of different projects as it does not consider other factors that should be evaluated

for comparison of different projects. The accounting rate of return for the two given options

for investment in machinery is different as given in the table. The ARR for G120 is 18% and

for the Z125 is 14.7% and therefore on the basis of ARR the SD Ltd is recommended to

select the investment proposal of investing in G120 machinery (Wilson, 2015).

Payback period

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The payback period is referred to as time-period required for recovering the cost of an

investment. The payback period helps in taking decisions regarding to invest in a project or

not. The longer the payback period of a project less it is suitable for investment purpose. The

concept is very simple to be used and also to be understood. It can be calculated even without

the use of a calculator. The method specifically emphasizes on the time required to recover

the cost of a project and as such provides an assessment of its risk. Therefore, it can be used

to compare the risks of different projects on the basis of their payback periods (Holmén and

Pramborg, 2007).

The method also has a drawback of not considering the concept of time value of

money while determining the feasibility of a project. It only focuses on assessing the liquidity

of a project and does not consider its profitability. The method does not take into account the

cash flows that will be received after the payback period. As per this method, it can be said

that SD Ltd should consider the project G120 for investment in comparison to Z125 as it have

less payback period (Mushaho and Mbabazize, 2015).

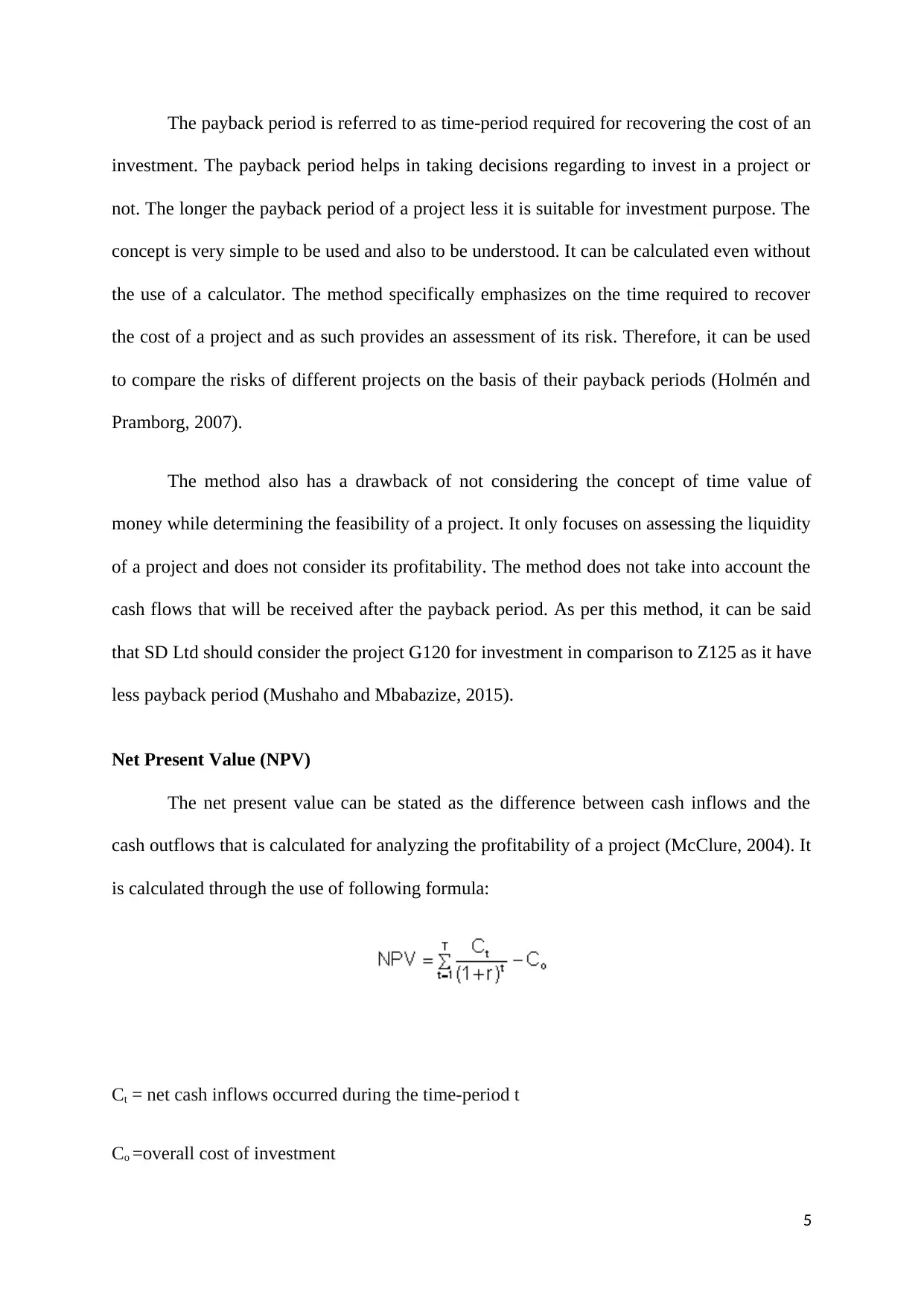

Net Present Value (NPV)

The net present value can be stated as the difference between cash inflows and the

cash outflows that is calculated for analyzing the profitability of a project (McClure, 2004). It

is calculated through the use of following formula:

Ct = net cash inflows occurred during the time-period t

Co =overall cost of investment

5

investment. The payback period helps in taking decisions regarding to invest in a project or

not. The longer the payback period of a project less it is suitable for investment purpose. The

concept is very simple to be used and also to be understood. It can be calculated even without

the use of a calculator. The method specifically emphasizes on the time required to recover

the cost of a project and as such provides an assessment of its risk. Therefore, it can be used

to compare the risks of different projects on the basis of their payback periods (Holmén and

Pramborg, 2007).

The method also has a drawback of not considering the concept of time value of

money while determining the feasibility of a project. It only focuses on assessing the liquidity

of a project and does not consider its profitability. The method does not take into account the

cash flows that will be received after the payback period. As per this method, it can be said

that SD Ltd should consider the project G120 for investment in comparison to Z125 as it have

less payback period (Mushaho and Mbabazize, 2015).

Net Present Value (NPV)

The net present value can be stated as the difference between cash inflows and the

cash outflows that is calculated for analyzing the profitability of a project (McClure, 2004). It

is calculated through the use of following formula:

Ct = net cash inflows occurred during the time-period t

Co =overall cost of investment

5

r=discount-rate

t=number of time-periods

The NPV evaluates the feasibility of a project through calculation and summation of

all the discounted cash flows of a project that is either positive or negative. Thus, it is highly

sensitive to discount rates. The project is accepted if it is expected to generate positive IRR

and rejected if it provides negative IRR. The NPV method estimates the feasibility of a

project on the basis of the cost of capital and the risk involved in estimating the future cash

flows. The NPV method also is very useful for determining the expected value a project will

create for a company (Bierman and Smidt, 2003).

The project managers use the capital budgeting technique of NPV for calculating the

cash flows of different investment options separately. However, its biggest disadvantage is

that it is based on numerous assumptions about the cost of capital of a company. Therefore, if

the cost of capital of an entity is considered to be very low it can result in making sub-optimal

investments and it is very high then it can result in not selection of many appropriate

investment options. As such, based on the NPV of the given two investment options for SD

Ltd, the Z125 machinery investment option should be selected as its NPV is £420,194 and

£284,864 (Bierman and Smidt, 2007).

Internal Rate of return (IRR)

The internal rate of return (IRR) in capital budgeting decisions is used to assess the

profitability of potential investment options. It is said to be a discount rate at which the NPV

of all the cash inflows from a project becomes zero. It is thus used for calculating the

breakeven point of a project. The most significant advantage of the use of this method is that

it considers the concept of time value of money in analyzing the feasibility of a project. Also,

it is simple to understand and so largely used by accounting managers in capital budgeting

6

t=number of time-periods

The NPV evaluates the feasibility of a project through calculation and summation of

all the discounted cash flows of a project that is either positive or negative. Thus, it is highly

sensitive to discount rates. The project is accepted if it is expected to generate positive IRR

and rejected if it provides negative IRR. The NPV method estimates the feasibility of a

project on the basis of the cost of capital and the risk involved in estimating the future cash

flows. The NPV method also is very useful for determining the expected value a project will

create for a company (Bierman and Smidt, 2003).

The project managers use the capital budgeting technique of NPV for calculating the

cash flows of different investment options separately. However, its biggest disadvantage is

that it is based on numerous assumptions about the cost of capital of a company. Therefore, if

the cost of capital of an entity is considered to be very low it can result in making sub-optimal

investments and it is very high then it can result in not selection of many appropriate

investment options. As such, based on the NPV of the given two investment options for SD

Ltd, the Z125 machinery investment option should be selected as its NPV is £420,194 and

£284,864 (Bierman and Smidt, 2007).

Internal Rate of return (IRR)

The internal rate of return (IRR) in capital budgeting decisions is used to assess the

profitability of potential investment options. It is said to be a discount rate at which the NPV

of all the cash inflows from a project becomes zero. It is thus used for calculating the

breakeven point of a project. The most significant advantage of the use of this method is that

it considers the concept of time value of money in analyzing the feasibility of a project. Also,

it is simple to understand and so largely used by accounting managers in capital budgeting

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

decisions. The decisions regarding the acceptance or rejection of a project in this technique is

not based on the required rate of return. The major disadvantage of the method is that it does

not consider the economies of scale Also, it does not analyse the profitability of a project on

the basis of the project size. The cash flows are compared with the capital amount and

therefore the projects with different capital investment cannot be compared as higher IRR

will be obtained from a small project. The IRR method only emphasizes on the estimated

cash flows of a project and does not consider the potential costs that can impact its future

profitability. The method also cannot be used when the discount rate of a project is not

known. As per the internal rate of return, the G120 investment option is selected in

comparison to Z125 because it provides larger IRR (Brigham and Ehrhardt, 2007).

Recommendation

On the basis of analysis of all the four capital investment appraisal measures, it can be

said that SD Ltd should select the investment option for investing in G120 machinery because

it has higher IRR, lower payback period and higher ARR. The lower payback period of G120

investment option indicates that it has minimum risk and therefore it will recover its cost of

investment in short period of time. The accounting return of return is also higher which

means that G120 investment option will help in generation of more net income in comparison

to the other option. The IRR of G120 option is higher indicating that the rate of return of this

option is higher in comparison to other. The NPV of Z125 is higher as it evaluates the

attractiveness of a project for inviting on the basis of cost of capital. The Z125 is a highly

capital intensive project and as such its NPV value is higher in comparison to G120 option.

Therefore, the most appropriate investment option for SD Ltd is investing in G120 machinery

for improving its production process (Megginson, Lucey and Smart, 2008).

7

not based on the required rate of return. The major disadvantage of the method is that it does

not consider the economies of scale Also, it does not analyse the profitability of a project on

the basis of the project size. The cash flows are compared with the capital amount and

therefore the projects with different capital investment cannot be compared as higher IRR

will be obtained from a small project. The IRR method only emphasizes on the estimated

cash flows of a project and does not consider the potential costs that can impact its future

profitability. The method also cannot be used when the discount rate of a project is not

known. As per the internal rate of return, the G120 investment option is selected in

comparison to Z125 because it provides larger IRR (Brigham and Ehrhardt, 2007).

Recommendation

On the basis of analysis of all the four capital investment appraisal measures, it can be

said that SD Ltd should select the investment option for investing in G120 machinery because

it has higher IRR, lower payback period and higher ARR. The lower payback period of G120

investment option indicates that it has minimum risk and therefore it will recover its cost of

investment in short period of time. The accounting return of return is also higher which

means that G120 investment option will help in generation of more net income in comparison

to the other option. The IRR of G120 option is higher indicating that the rate of return of this

option is higher in comparison to other. The NPV of Z125 is higher as it evaluates the

attractiveness of a project for inviting on the basis of cost of capital. The Z125 is a highly

capital intensive project and as such its NPV value is higher in comparison to G120 option.

Therefore, the most appropriate investment option for SD Ltd is investing in G120 machinery

for improving its production process (Megginson, Lucey and Smart, 2008).

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Reasons for payback favor to the G120 option and NPV the Z125 option in the given

case

As depicted from the given table, the payback and NPV method of capital budgeting

used for analyzing the feasibility of the two given investment options have shown different

results. The payback capital budgeting technique favors G120 option as it has lower payback

time therefore it will recover its cost in small period of time in comparison to other

investment option. On the basis of pay-back method, it can be said that G120 investment

option is less risky as it recover its cost of investment quickly. The NPV method favors Z125

option because it provides maximise wealth to the shareholders as it has larger NPV than

G120 option. The NPV methods calculate the present value of cash flows and derive the

value of a project that will be added to the shareholders wealth. The overall analysis provided

by NPV is based o the cost of capital (Peterson and Fabozzi, 2004). The assessment provided

by the NPV method can be said to be more reliable and therefore the company can consider

the selection of investment option for Z125 machinery. The NPV value can be said to more

reliable as it analyses the profitability of a project o the basis of the concept of time value of

money and also provides results by considering the cash flows to be realized at the end of a

project. Thus, it predicts the best investment option for a company by considering the future

changes in the market place (Pogue, 2010).

However, the payback period method is considered to be less reliable than NPV

method because the results provided by it have not considered the factor of time value of

money. Therefore, the company can select the Z125 machinery investment option as NOV

method is more reliable capital budgeting technique in comparison to payback method.

However, as per my opinion in the given case the G120 option is less risky because the

projects that have payback period less than 3 years are accepted on the basis of their less risk.

The Z125 option has more risk as its payback period is more than 3 years. Therefore, the

company by selecting the G120 option can reduce its risk and by realizing the breakeven

8

case

As depicted from the given table, the payback and NPV method of capital budgeting

used for analyzing the feasibility of the two given investment options have shown different

results. The payback capital budgeting technique favors G120 option as it has lower payback

time therefore it will recover its cost in small period of time in comparison to other

investment option. On the basis of pay-back method, it can be said that G120 investment

option is less risky as it recover its cost of investment quickly. The NPV method favors Z125

option because it provides maximise wealth to the shareholders as it has larger NPV than

G120 option. The NPV methods calculate the present value of cash flows and derive the

value of a project that will be added to the shareholders wealth. The overall analysis provided

by NPV is based o the cost of capital (Peterson and Fabozzi, 2004). The assessment provided

by the NPV method can be said to be more reliable and therefore the company can consider

the selection of investment option for Z125 machinery. The NPV value can be said to more

reliable as it analyses the profitability of a project o the basis of the concept of time value of

money and also provides results by considering the cash flows to be realized at the end of a

project. Thus, it predicts the best investment option for a company by considering the future

changes in the market place (Pogue, 2010).

However, the payback period method is considered to be less reliable than NPV

method because the results provided by it have not considered the factor of time value of

money. Therefore, the company can select the Z125 machinery investment option as NOV

method is more reliable capital budgeting technique in comparison to payback method.

However, as per my opinion in the given case the G120 option is less risky because the

projects that have payback period less than 3 years are accepted on the basis of their less risk.

The Z125 option has more risk as its payback period is more than 3 years. Therefore, the

company by selecting the G120 option can reduce its risk and by realizing the breakeven

8

point earlier can re-invest the funds for earning greater profits. Also, the investing in Z125

would require the company to invest its entire capital budget as it requires more capital (Pratt,

2003). Therefore, the company should play safe and is recommended to invest in the projects

that have less risk that is in G120 option. Both the option does not consider the project size

and therefore on the basis of results of payback period and NPV value, it is suggested that SD

Ltd should select the investment option of G120 because it have less risk. The company is not

in position of taking higher risk due to capital budget constraints and therefore recommended

to select the results obtained from payback period method (Shapiro, 2005).

Analysis of Confidence of Finance Director in the given case about achieving IRR would

in excess of 15% for both options of G120 and Z125

The IRR (Internal Rate of Return) is regarded as the discount rate at which the net

present value of cash flows becomes zero. The internal rate of return is often selected as the

best option to accept or reject a project if the other factors are considered to be constant. On

the other hand, the net present value is said to be the difference between the present value of

cash inflows and outflows. It evaluates the profitability by taking into consideration the value

of a dollar in present with that in the future (Hsu, 2005). The NPV and IRR both evaluates the

profitability of a project by considering the time value of money and are used in combination

by the project managers for analyzing and comparing the investment options. The relation

between NPV and IRR can be used to describe the reason for the confidence of finance

director that IRR would be greater than 15% for both the investment options. The NPV of a

project if is less than zero then IRR is also less than the cost of capital and the project will be

rejected (Griff, 2014).

This is because the rate of return of a project is less than the expenditure incurred

during carrying the project and therefore it is not able to realize its breakeven point.

However, if NPV is equal to zero, then IRR is equal to the cost of capital and the project will

9

would require the company to invest its entire capital budget as it requires more capital (Pratt,

2003). Therefore, the company should play safe and is recommended to invest in the projects

that have less risk that is in G120 option. Both the option does not consider the project size

and therefore on the basis of results of payback period and NPV value, it is suggested that SD

Ltd should select the investment option of G120 because it have less risk. The company is not

in position of taking higher risk due to capital budget constraints and therefore recommended

to select the results obtained from payback period method (Shapiro, 2005).

Analysis of Confidence of Finance Director in the given case about achieving IRR would

in excess of 15% for both options of G120 and Z125

The IRR (Internal Rate of Return) is regarded as the discount rate at which the net

present value of cash flows becomes zero. The internal rate of return is often selected as the

best option to accept or reject a project if the other factors are considered to be constant. On

the other hand, the net present value is said to be the difference between the present value of

cash inflows and outflows. It evaluates the profitability by taking into consideration the value

of a dollar in present with that in the future (Hsu, 2005). The NPV and IRR both evaluates the

profitability of a project by considering the time value of money and are used in combination

by the project managers for analyzing and comparing the investment options. The relation

between NPV and IRR can be used to describe the reason for the confidence of finance

director that IRR would be greater than 15% for both the investment options. The NPV of a

project if is less than zero then IRR is also less than the cost of capital and the project will be

rejected (Griff, 2014).

This is because the rate of return of a project is less than the expenditure incurred

during carrying the project and therefore it is not able to realize its breakeven point.

However, if NPV is equal to zero, then IRR is equal to the cost of capital and the project will

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

be probably rejected as it will provides less return (Al-Ani, 2015). However, if NPV is

greater than zero, then IRR is also greater than cost of capital and the project is accepted on

the basis of providing it large profitability. As such, in the given scenario, the NPV is

calculated through applying the cost of capital to be 15%. The NPV of both the projects as

evaluated are positive and therefore it can be said that IRR of both the projects will be above

15%. This is because the IRR is calculated at the discount rate when NPV becomes zero.

Therefore, the discount rate of both the projects would be above 15% to arrive at NPV to be

zero which is calculated at the cost of capital rate of 15% (Lunkes et al., 2015).

Impact of the Investment Option of a potential purchase of new engine plant

The evaluation of the third investment option of new machinery with cost of

£2,080,000 and NPV of £140,800 for SD Ltd can be done through considering the following

two assumptions:

Assumption 1: This option assumes that only one investment cession will be

considered by SD Ltd out of the total three options. In this case, there will be no

impact of the given option as its NPV is less than the NPV’s of both G120 and Z125.

Hence, it can be said that in the case of company only selecting one investment option

it will either choose G120 and Z125 (Venkatesh and Gugloth, 2017).

Assumption 2: This assumption assumes that two investment options from the three

can be selected. In this case, the two investment options that can be selected by SD

Ltd in combination are G120 and the new investment option. This is because the total

capital budget of the company for investment purpose in the new machinery is equal

to the overall initial investment that is to be made in investing the machinery option of

Z125, that is, £3,232,000. As such, the total capital budget that will be required for

undertaking both the investment options of G120 and the given new investment

10

greater than zero, then IRR is also greater than cost of capital and the project is accepted on

the basis of providing it large profitability. As such, in the given scenario, the NPV is

calculated through applying the cost of capital to be 15%. The NPV of both the projects as

evaluated are positive and therefore it can be said that IRR of both the projects will be above

15%. This is because the IRR is calculated at the discount rate when NPV becomes zero.

Therefore, the discount rate of both the projects would be above 15% to arrive at NPV to be

zero which is calculated at the cost of capital rate of 15% (Lunkes et al., 2015).

Impact of the Investment Option of a potential purchase of new engine plant

The evaluation of the third investment option of new machinery with cost of

£2,080,000 and NPV of £140,800 for SD Ltd can be done through considering the following

two assumptions:

Assumption 1: This option assumes that only one investment cession will be

considered by SD Ltd out of the total three options. In this case, there will be no

impact of the given option as its NPV is less than the NPV’s of both G120 and Z125.

Hence, it can be said that in the case of company only selecting one investment option

it will either choose G120 and Z125 (Venkatesh and Gugloth, 2017).

Assumption 2: This assumption assumes that two investment options from the three

can be selected. In this case, the two investment options that can be selected by SD

Ltd in combination are G120 and the new investment option. This is because the total

capital budget of the company for investment purpose in the new machinery is equal

to the overall initial investment that is to be made in investing the machinery option of

Z125, that is, £3,232,000. As such, the total capital budget that will be required for

undertaking both the investment options of G120 and the given new investment

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

option will be £ 3,19,2000. This is the summation of the initial investment for G120

and the new investment option. Also, the combined NPV of both the projects will be

£425,664 that is greater than the NPV of Z125 machinery investment option of

£420,194. However, the company cannot take the investment decision to invest in the

given new investment option and the Z125 option. This is due to the fact that SD Ltd

only has a maximum capital budget that is equal to the initial investment required for

investing in the Z125 machinery (Bierman and Smidt, 2007). Therefore, it is not

feasible for the company to undertake any other investment option in addition of the

Z125 option. As such, it can be said that the company if want to select the two

investment options then it should decide to invest in the new machinery of the given

investment option and the G120. This will help the company to achieve higher NPV

in comparison to investing only in the investment option of Z125 within its capital

budget constraints (Kengatharan, 2016).

Conclusion

Thus, it can be said from the overall discussion held in the report that capital

budgeting decisions plays a critical role for achieving success from a capital project. The

capital budgeting techniques analyzed in the report, that are, accounting rate of return,

internal rate of return, net present value and the payback period are very important for

evaluating the potential worth of a project, These techniques provides a base for accepting or

rejecting a project under consideration based on its potential profitability and returns. The SD

Ltd should select the investment option from the given tow machinery of G120 and Z125

after thorough analysis of the results obtained from the use of capital budgeting techniques.

This is essential so that the company can achieve its strategic goals and objectives which it

wants to achieve through installation of new machinery. The results obtained from the capital

11

and the new investment option. Also, the combined NPV of both the projects will be

£425,664 that is greater than the NPV of Z125 machinery investment option of

£420,194. However, the company cannot take the investment decision to invest in the

given new investment option and the Z125 option. This is due to the fact that SD Ltd

only has a maximum capital budget that is equal to the initial investment required for

investing in the Z125 machinery (Bierman and Smidt, 2007). Therefore, it is not

feasible for the company to undertake any other investment option in addition of the

Z125 option. As such, it can be said that the company if want to select the two

investment options then it should decide to invest in the new machinery of the given

investment option and the G120. This will help the company to achieve higher NPV

in comparison to investing only in the investment option of Z125 within its capital

budget constraints (Kengatharan, 2016).

Conclusion

Thus, it can be said from the overall discussion held in the report that capital

budgeting decisions plays a critical role for achieving success from a capital project. The

capital budgeting techniques analyzed in the report, that are, accounting rate of return,

internal rate of return, net present value and the payback period are very important for

evaluating the potential worth of a project, These techniques provides a base for accepting or

rejecting a project under consideration based on its potential profitability and returns. The SD

Ltd should select the investment option from the given tow machinery of G120 and Z125

after thorough analysis of the results obtained from the use of capital budgeting techniques.

This is essential so that the company can achieve its strategic goals and objectives which it

wants to achieve through installation of new machinery. The results obtained from the capital

11

budgeting techniques in combination with the business requirements would decide the

selection of the most appropriate investment option.

12

selection of the most appropriate investment option.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.