Detailed Financial Analysis Report: Sainsbury and Tesco Comparison

VerifiedAdded on 2021/02/19

|32

|5616

|25

Report

AI Summary

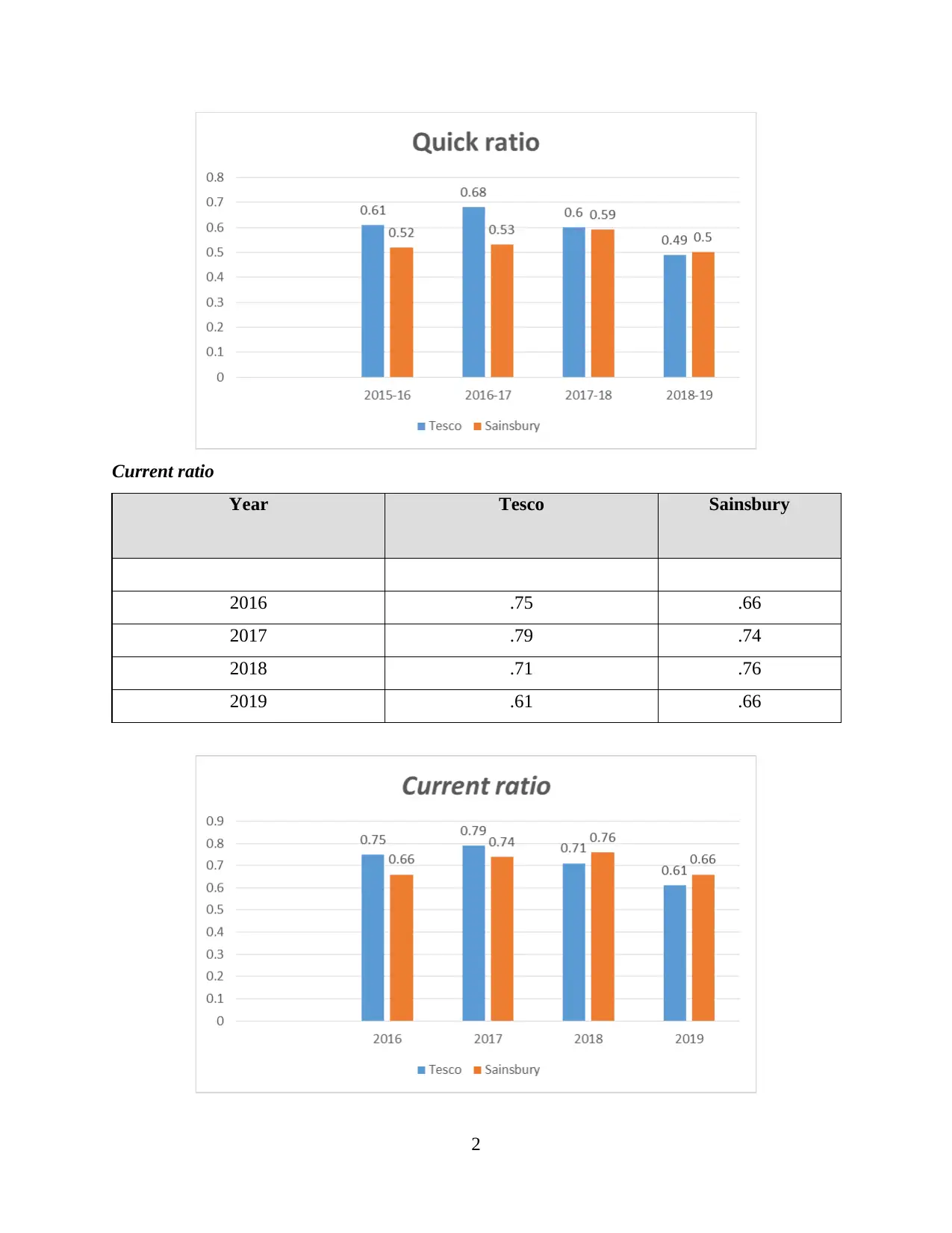

This report presents a detailed financial analysis comparing the performance of Sainsbury and Tesco plc. It begins with an introduction to financial analysis and its importance, followed by an in-depth examination of key financial ratios, including liquidity, investment, efficiency, solvency, and profitability ratios, calculated from the companies' financial statements between 2015 and 2019. The analysis includes a comparison of vertical and horizontal financial statements, providing insights into trends and changes over time. The report also emphasizes the significance of working capital analysis for both companies and offers a critical analysis of their cash flow statements. The findings highlight the financial strengths and weaknesses of each company, offering a comprehensive overview of their financial health and efficiency. The report concludes with a summary of the key findings and references to supporting financial data.

1 out of 32

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.