Comprehensive Financial Analysis Report: Nick Scali Limited

VerifiedAdded on 2022/08/15

|26

|6940

|21

Report

AI Summary

This report presents a comprehensive financial analysis of Nick Scali Limited, a public limited company operating in the furniture retail and import sector. The analysis is divided into two parts: Part A focuses on ratio analysis, including profitability, asset turnover, liquidity, and solvency ratios, examining trends over a five-year period from 2015 to 2019. The report assesses the company's financial health, efficiency, and leverage, providing insights into its performance. Part B delves into the evaluation of future performance using forecasting and valuation models like the dividend discount model, culminating in conclusions and recommendations. The report highlights the company's increasing net profit margin, consistent return on equity, and efficient use of operating assets, while also acknowledging the impact of financial leverage and asset turnover. The analysis aims to guide internal and external stakeholders in understanding the financial figures and trends within the context of the business environment.

FINANCIAL STATEMENT ANALYSIS

NICK SCALI LIMITED

2/9/2020

Student’s Name:

NICK SCALI LIMITED

2/9/2020

Student’s Name:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCIAL ANALYSIS- NICK SCALI LIMITED

1

Contents

Introduction...........................................................................................................................................2

Organisation background and the Outlook............................................................................................2

Ratio Analysis.......................................................................................................................................3

Profitability Ratios.............................................................................................................................3

Asset turnover....................................................................................................................................7

Cash Flow Position................................................................................................................................8

Liquidity Ratios:................................................................................................................................8

Solvency ratio....................................................................................................................................9

Cash debt coverage ratio..................................................................................................................11

Cash flow return on asset.................................................................................................................11

Forecasting..........................................................................................................................................12

Valuation.............................................................................................................................................16

Recommendations...............................................................................................................................19

References...........................................................................................................................................20

Appendix.............................................................................................................................................22

1

Contents

Introduction...........................................................................................................................................2

Organisation background and the Outlook............................................................................................2

Ratio Analysis.......................................................................................................................................3

Profitability Ratios.............................................................................................................................3

Asset turnover....................................................................................................................................7

Cash Flow Position................................................................................................................................8

Liquidity Ratios:................................................................................................................................8

Solvency ratio....................................................................................................................................9

Cash debt coverage ratio..................................................................................................................11

Cash flow return on asset.................................................................................................................11

Forecasting..........................................................................................................................................12

Valuation.............................................................................................................................................16

Recommendations...............................................................................................................................19

References...........................................................................................................................................20

Appendix.............................................................................................................................................22

FINANCIAL ANALYSIS- NICK SCALI LIMITED

2

Introduction

The enhanced globalisation has made the business activities more complex, and a need of

more detailed and efficient presentation of the financial statements to the varied stakeholders.

The process of reviewing the financial statements of an organisation to guide the internal and

external stakeholders is called as the Financial Analysis. The relevancy of the financial

analysis to the external stakeholders is that the same aids in the evaluation of the business

value and value of the investments. In contrast to this, the internal stakeholders use the

financial statement as a monitoring tool, to efficiently manage the varied resources of an

entity. It is imperative to understand the financial figures present in the financial statements

in conjunction with the happenings in the business environment, such as changes in the

political, economic, technological and legal environment and others. Further, the data of

multiple years needs to be analysed to understand the overall trend of the financial

performances. Often the trends are analysed in comparison to the industry benchmarks or the

competitor data.

The following report is prepared with an aim to present a comprehensive financial analysis of

the company Nick Scali Limited. The analysis would be divided into two parts namely the

Part A and the Part B. The Part A would touch the various aspects of the business, and would

be guided by the various financial techniques. In addition to the above, a set of reformatted

financial statements would be provided to guide the detailed analysis of varied items of the

financial statements. The ratio analysis would shed light on the liquidity, solvency,

profitability and overall efficiency of the conduct of the business operations of the entity.

Apart from the above listed; the Part B of the report is inclusive of the evaluation of the

future performances of the entity. This part would include the determination of the forecasted

financial values with the aid of different models such as dividend discount model. An overall

conclusion along with a set of recommendations would be provided at the end to summarise

the key findings and address the issues if any.

Organisation background and the Outlook

The organisation Nick Scali Limited is a public limited company that has been listed on the

Australian Stock Exchange, and the foundation of which was laid down 50 years ago. The

organisation’s chief business is the retailing and the importing of the quality furniture

2

Introduction

The enhanced globalisation has made the business activities more complex, and a need of

more detailed and efficient presentation of the financial statements to the varied stakeholders.

The process of reviewing the financial statements of an organisation to guide the internal and

external stakeholders is called as the Financial Analysis. The relevancy of the financial

analysis to the external stakeholders is that the same aids in the evaluation of the business

value and value of the investments. In contrast to this, the internal stakeholders use the

financial statement as a monitoring tool, to efficiently manage the varied resources of an

entity. It is imperative to understand the financial figures present in the financial statements

in conjunction with the happenings in the business environment, such as changes in the

political, economic, technological and legal environment and others. Further, the data of

multiple years needs to be analysed to understand the overall trend of the financial

performances. Often the trends are analysed in comparison to the industry benchmarks or the

competitor data.

The following report is prepared with an aim to present a comprehensive financial analysis of

the company Nick Scali Limited. The analysis would be divided into two parts namely the

Part A and the Part B. The Part A would touch the various aspects of the business, and would

be guided by the various financial techniques. In addition to the above, a set of reformatted

financial statements would be provided to guide the detailed analysis of varied items of the

financial statements. The ratio analysis would shed light on the liquidity, solvency,

profitability and overall efficiency of the conduct of the business operations of the entity.

Apart from the above listed; the Part B of the report is inclusive of the evaluation of the

future performances of the entity. This part would include the determination of the forecasted

financial values with the aid of different models such as dividend discount model. An overall

conclusion along with a set of recommendations would be provided at the end to summarise

the key findings and address the issues if any.

Organisation background and the Outlook

The organisation Nick Scali Limited is a public limited company that has been listed on the

Australian Stock Exchange, and the foundation of which was laid down 50 years ago. The

organisation’s chief business is the retailing and the importing of the quality furniture

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCIAL ANALYSIS- NICK SCALI LIMITED

3

products, to provide the household furniture and the associated accessories (Nick Scali

Limited, 2020). The headquarters of the company is located at Lidcombe, New South Wales,

and the listing of the company shares is done on ASX under the symbol “NCK.” Some of the

chief products of the company include lounges, dining tables, cabinets, rugs, mirrors and

others. The organisation operates under the two brands namely the Sofas2Go and the Nick

Scali Furniture. Over the years, the company has earned the status of a respected and trusted

brand of furniture in terms of the finest quality and the low prices.

PART A

Ratio Analysis

There are various ways to analyse a set of financial statement comprehensively, such as the

trend analysis, vertical analysis and ratio analysis. The technique used in the presented report

is that of the ratio analysis. Computation of ratios is one of most fundamental financial

analysis techniques in which the various ratios give insights about the various aspects of the

financial health. The following report involves the computation of the various ratios for the

period of five financial years, descending from the most recent that is the year 2019. The

analysis of the key ratios is presented as follows.

Profitability Ratios

Determination of the profitability ratios is an important exercise not only for the external

stakeholders such as the regulators and the investors of the company for the decision making

process, but for the internal stakeholders to review the business processes. There are varied

kinds of profitability ratios as computed on the various stages of profitability. The said

earnings are examined against the different elements of the financial statements such as the

assets, revenue, equity and others, and useful insights are gained by comparing and

evaluating the trends (Edmonds, 2013).

Thus, the chief objective of the computation of the said group of ratios is to adjudge the

efficiency of the results of the business operations as against the different items of statement

of financial position and the income statement. The table below is representative of the

various profitability ratios of the organisation Nick Scali Limited.

Financial Ratio Analysis - Nick Scali Limited

Profitabi

lity

Formul

a

2015 2016 2017 2018 2019

3

products, to provide the household furniture and the associated accessories (Nick Scali

Limited, 2020). The headquarters of the company is located at Lidcombe, New South Wales,

and the listing of the company shares is done on ASX under the symbol “NCK.” Some of the

chief products of the company include lounges, dining tables, cabinets, rugs, mirrors and

others. The organisation operates under the two brands namely the Sofas2Go and the Nick

Scali Furniture. Over the years, the company has earned the status of a respected and trusted

brand of furniture in terms of the finest quality and the low prices.

PART A

Ratio Analysis

There are various ways to analyse a set of financial statement comprehensively, such as the

trend analysis, vertical analysis and ratio analysis. The technique used in the presented report

is that of the ratio analysis. Computation of ratios is one of most fundamental financial

analysis techniques in which the various ratios give insights about the various aspects of the

financial health. The following report involves the computation of the various ratios for the

period of five financial years, descending from the most recent that is the year 2019. The

analysis of the key ratios is presented as follows.

Profitability Ratios

Determination of the profitability ratios is an important exercise not only for the external

stakeholders such as the regulators and the investors of the company for the decision making

process, but for the internal stakeholders to review the business processes. There are varied

kinds of profitability ratios as computed on the various stages of profitability. The said

earnings are examined against the different elements of the financial statements such as the

assets, revenue, equity and others, and useful insights are gained by comparing and

evaluating the trends (Edmonds, 2013).

Thus, the chief objective of the computation of the said group of ratios is to adjudge the

efficiency of the results of the business operations as against the different items of statement

of financial position and the income statement. The table below is representative of the

various profitability ratios of the organisation Nick Scali Limited.

Financial Ratio Analysis - Nick Scali Limited

Profitabi

lity

Formul

a

2015 2016 2017 2018 2019

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCIAL ANALYSIS- NICK SCALI LIMITED

4

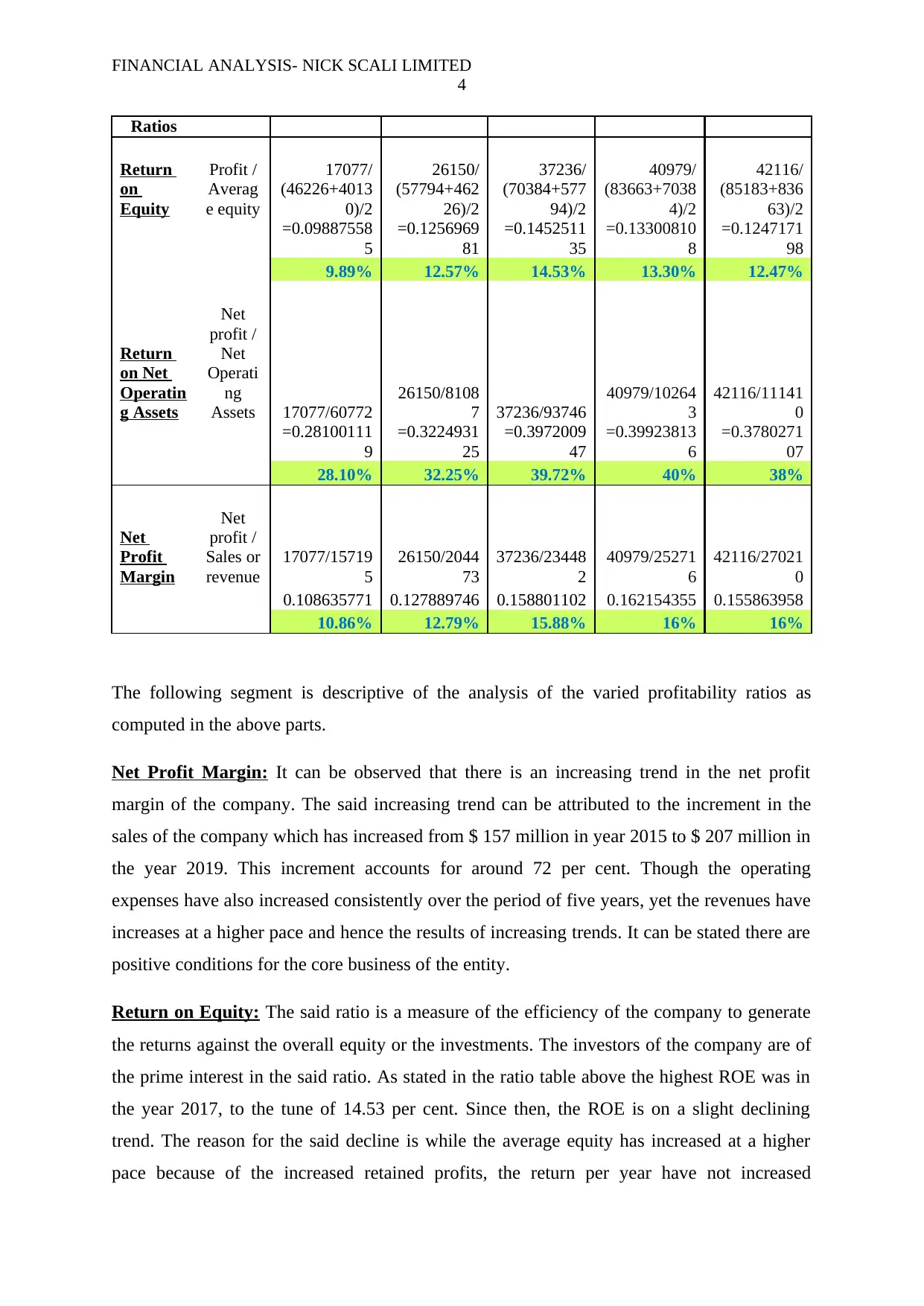

Ratios

Return

on

Equity

Profit /

Averag

e equity

17077/

(46226+4013

0)/2

26150/

(57794+462

26)/2

37236/

(70384+577

94)/2

40979/

(83663+7038

4)/2

42116/

(85183+836

63)/2

=0.09887558

5

=0.1256969

81

=0.1452511

35

=0.13300810

8

=0.1247171

98

9.89% 12.57% 14.53% 13.30% 12.47%

Return

on Net

Operatin

g Assets

Net

profit /

Net

Operati

ng

Assets 17077/60772

26150/8108

7 37236/93746

40979/10264

3

42116/11141

0

=0.28100111

9

=0.3224931

25

=0.3972009

47

=0.39923813

6

=0.3780271

07

28.10% 32.25% 39.72% 40% 38%

Net

Profit

Margin

Net

profit /

Sales or

revenue

17077/15719

5

26150/2044

73

37236/23448

2

40979/25271

6

42116/27021

0

0.108635771 0.127889746 0.158801102 0.162154355 0.155863958

10.86% 12.79% 15.88% 16% 16%

The following segment is descriptive of the analysis of the varied profitability ratios as

computed in the above parts.

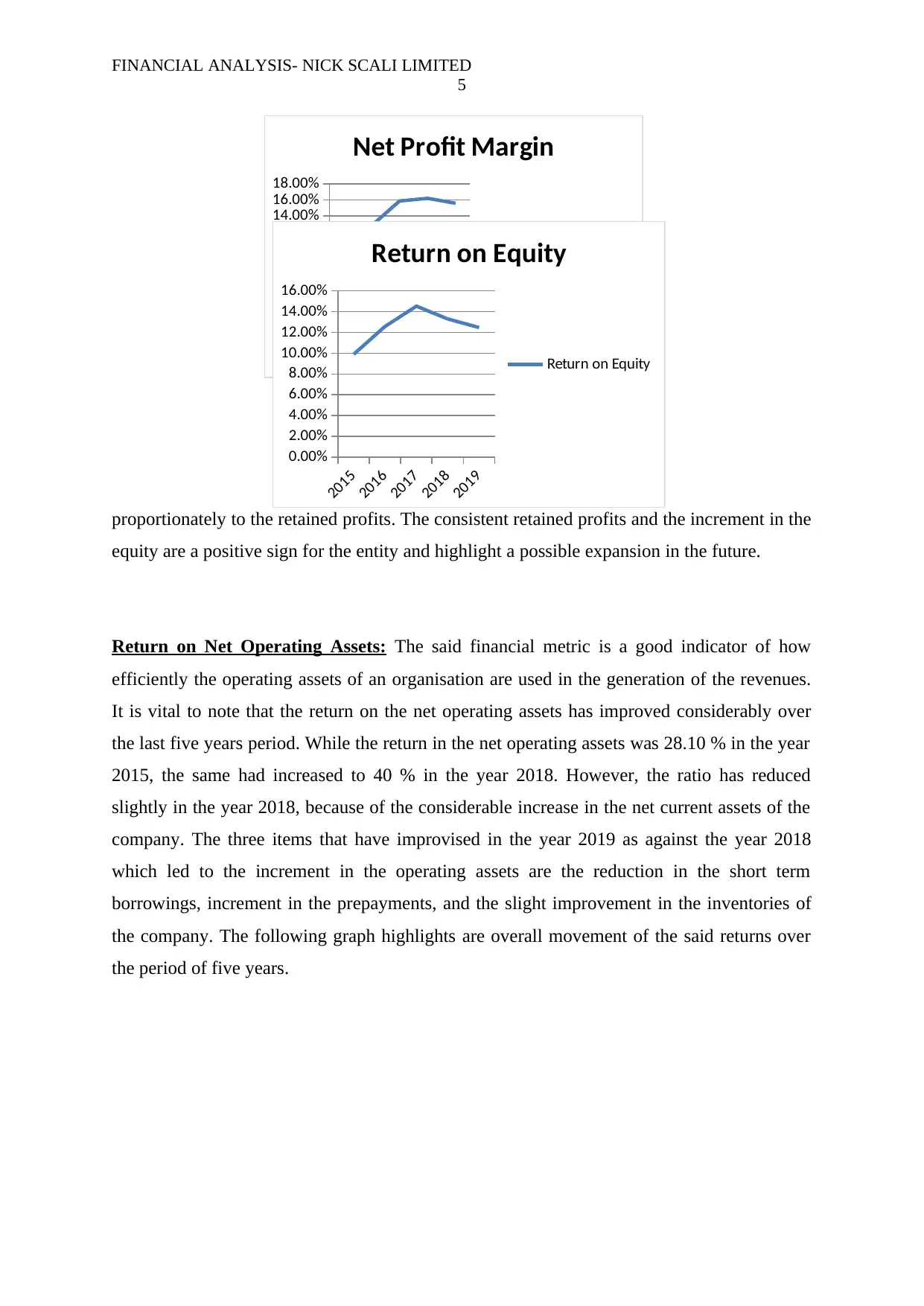

Net Profit Margin: It can be observed that there is an increasing trend in the net profit

margin of the company. The said increasing trend can be attributed to the increment in the

sales of the company which has increased from $ 157 million in year 2015 to $ 207 million in

the year 2019. This increment accounts for around 72 per cent. Though the operating

expenses have also increased consistently over the period of five years, yet the revenues have

increases at a higher pace and hence the results of increasing trends. It can be stated there are

positive conditions for the core business of the entity.

Return on Equity: The said ratio is a measure of the efficiency of the company to generate

the returns against the overall equity or the investments. The investors of the company are of

the prime interest in the said ratio. As stated in the ratio table above the highest ROE was in

the year 2017, to the tune of 14.53 per cent. Since then, the ROE is on a slight declining

trend. The reason for the said decline is while the average equity has increased at a higher

pace because of the increased retained profits, the return per year have not increased

4

Ratios

Return

on

Equity

Profit /

Averag

e equity

17077/

(46226+4013

0)/2

26150/

(57794+462

26)/2

37236/

(70384+577

94)/2

40979/

(83663+7038

4)/2

42116/

(85183+836

63)/2

=0.09887558

5

=0.1256969

81

=0.1452511

35

=0.13300810

8

=0.1247171

98

9.89% 12.57% 14.53% 13.30% 12.47%

Return

on Net

Operatin

g Assets

Net

profit /

Net

Operati

ng

Assets 17077/60772

26150/8108

7 37236/93746

40979/10264

3

42116/11141

0

=0.28100111

9

=0.3224931

25

=0.3972009

47

=0.39923813

6

=0.3780271

07

28.10% 32.25% 39.72% 40% 38%

Net

Profit

Margin

Net

profit /

Sales or

revenue

17077/15719

5

26150/2044

73

37236/23448

2

40979/25271

6

42116/27021

0

0.108635771 0.127889746 0.158801102 0.162154355 0.155863958

10.86% 12.79% 15.88% 16% 16%

The following segment is descriptive of the analysis of the varied profitability ratios as

computed in the above parts.

Net Profit Margin: It can be observed that there is an increasing trend in the net profit

margin of the company. The said increasing trend can be attributed to the increment in the

sales of the company which has increased from $ 157 million in year 2015 to $ 207 million in

the year 2019. This increment accounts for around 72 per cent. Though the operating

expenses have also increased consistently over the period of five years, yet the revenues have

increases at a higher pace and hence the results of increasing trends. It can be stated there are

positive conditions for the core business of the entity.

Return on Equity: The said ratio is a measure of the efficiency of the company to generate

the returns against the overall equity or the investments. The investors of the company are of

the prime interest in the said ratio. As stated in the ratio table above the highest ROE was in

the year 2017, to the tune of 14.53 per cent. Since then, the ROE is on a slight declining

trend. The reason for the said decline is while the average equity has increased at a higher

pace because of the increased retained profits, the return per year have not increased

FINANCIAL ANALYSIS- NICK SCALI LIMITED

5

proportionately to the retained profits. The consistent retained profits and the increment in the

equity are a positive sign for the entity and highlight a possible expansion in the future.

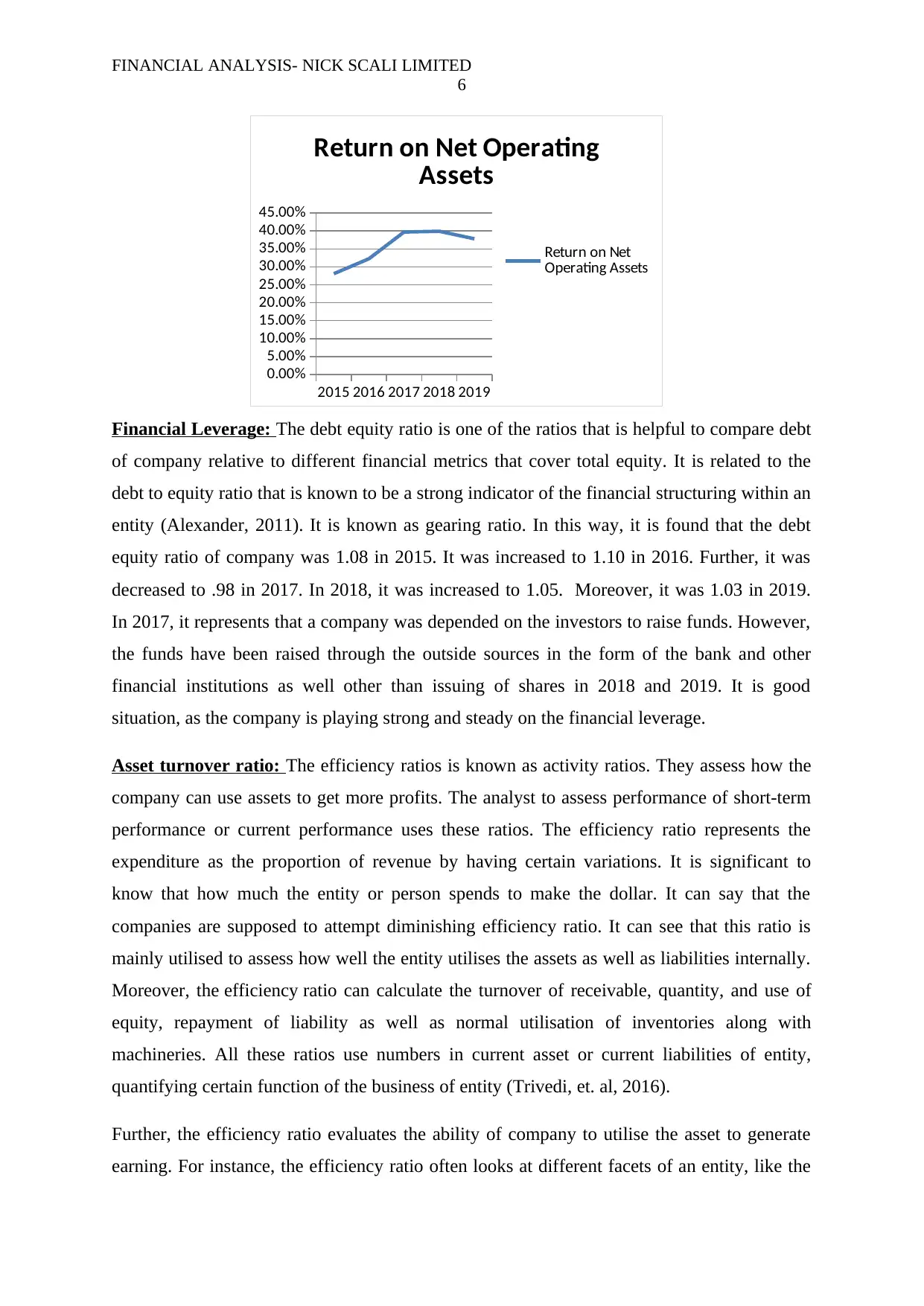

Return on Net Operating Assets: The said financial metric is a good indicator of how

efficiently the operating assets of an organisation are used in the generation of the revenues.

It is vital to note that the return on the net operating assets has improved considerably over

the last five years period. While the return in the net operating assets was 28.10 % in the year

2015, the same had increased to 40 % in the year 2018. However, the ratio has reduced

slightly in the year 2018, because of the considerable increase in the net current assets of the

company. The three items that have improvised in the year 2019 as against the year 2018

which led to the increment in the operating assets are the reduction in the short term

borrowings, increment in the prepayments, and the slight improvement in the inventories of

the company. The following graph highlights are overall movement of the said returns over

the period of five years.

2015

2016

2017

2018

2019

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

14.00%

16.00%

18.00%

Net Profit Margin

Net Profit Margin

2015

2016

2017

2018

2019

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

14.00%

16.00%

Return on Equity

Return on Equity

5

proportionately to the retained profits. The consistent retained profits and the increment in the

equity are a positive sign for the entity and highlight a possible expansion in the future.

Return on Net Operating Assets: The said financial metric is a good indicator of how

efficiently the operating assets of an organisation are used in the generation of the revenues.

It is vital to note that the return on the net operating assets has improved considerably over

the last five years period. While the return in the net operating assets was 28.10 % in the year

2015, the same had increased to 40 % in the year 2018. However, the ratio has reduced

slightly in the year 2018, because of the considerable increase in the net current assets of the

company. The three items that have improvised in the year 2019 as against the year 2018

which led to the increment in the operating assets are the reduction in the short term

borrowings, increment in the prepayments, and the slight improvement in the inventories of

the company. The following graph highlights are overall movement of the said returns over

the period of five years.

2015

2016

2017

2018

2019

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

14.00%

16.00%

18.00%

Net Profit Margin

Net Profit Margin

2015

2016

2017

2018

2019

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

14.00%

16.00%

Return on Equity

Return on Equity

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCIAL ANALYSIS- NICK SCALI LIMITED

6

Financial Leverage: The debt equity ratio is one of the ratios that is helpful to compare debt

of company relative to different financial metrics that cover total equity. It is related to the

debt to equity ratio that is known to be a strong indicator of the financial structuring within an

entity (Alexander, 2011). It is known as gearing ratio. In this way, it is found that the debt

equity ratio of company was 1.08 in 2015. It was increased to 1.10 in 2016. Further, it was

decreased to .98 in 2017. In 2018, it was increased to 1.05. Moreover, it was 1.03 in 2019.

In 2017, it represents that a company was depended on the investors to raise funds. However,

the funds have been raised through the outside sources in the form of the bank and other

financial institutions as well other than issuing of shares in 2018 and 2019. It is good

situation, as the company is playing strong and steady on the financial leverage.

Asset turnover ratio: The efficiency ratios is known as activity ratios. They assess how the

company can use assets to get more profits. The analyst to assess performance of short-term

performance or current performance uses these ratios. The efficiency ratio represents the

expenditure as the proportion of revenue by having certain variations. It is significant to

know that how much the entity or person spends to make the dollar. It can say that the

companies are supposed to attempt diminishing efficiency ratio. It can see that this ratio is

mainly utilised to assess how well the entity utilises the assets as well as liabilities internally.

Moreover, the efficiency ratio can calculate the turnover of receivable, quantity, and use of

equity, repayment of liability as well as normal utilisation of inventories along with

machineries. All these ratios use numbers in current asset or current liabilities of entity,

quantifying certain function of the business of entity (Trivedi, et. al, 2016).

Further, the efficiency ratio evaluates the ability of company to utilise the asset to generate

earning. For instance, the efficiency ratio often looks at different facets of an entity, like the

2015 2016 2017 2018 2019

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

35.00%

40.00%

45.00%

Return on Net Operating

Assets

Return on Net

Operating Assets

6

Financial Leverage: The debt equity ratio is one of the ratios that is helpful to compare debt

of company relative to different financial metrics that cover total equity. It is related to the

debt to equity ratio that is known to be a strong indicator of the financial structuring within an

entity (Alexander, 2011). It is known as gearing ratio. In this way, it is found that the debt

equity ratio of company was 1.08 in 2015. It was increased to 1.10 in 2016. Further, it was

decreased to .98 in 2017. In 2018, it was increased to 1.05. Moreover, it was 1.03 in 2019.

In 2017, it represents that a company was depended on the investors to raise funds. However,

the funds have been raised through the outside sources in the form of the bank and other

financial institutions as well other than issuing of shares in 2018 and 2019. It is good

situation, as the company is playing strong and steady on the financial leverage.

Asset turnover ratio: The efficiency ratios is known as activity ratios. They assess how the

company can use assets to get more profits. The analyst to assess performance of short-term

performance or current performance uses these ratios. The efficiency ratio represents the

expenditure as the proportion of revenue by having certain variations. It is significant to

know that how much the entity or person spends to make the dollar. It can say that the

companies are supposed to attempt diminishing efficiency ratio. It can see that this ratio is

mainly utilised to assess how well the entity utilises the assets as well as liabilities internally.

Moreover, the efficiency ratio can calculate the turnover of receivable, quantity, and use of

equity, repayment of liability as well as normal utilisation of inventories along with

machineries. All these ratios use numbers in current asset or current liabilities of entity,

quantifying certain function of the business of entity (Trivedi, et. al, 2016).

Further, the efficiency ratio evaluates the ability of company to utilise the asset to generate

earning. For instance, the efficiency ratio often looks at different facets of an entity, like the

2015 2016 2017 2018 2019

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

35.00%

40.00%

45.00%

Return on Net Operating

Assets

Return on Net

Operating Assets

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCIAL ANALYSIS- NICK SCALI LIMITED

7

time to take cash from customer or the amount of time to change inventory into cash. In this

way, it creates the efficiency ratios significant. The main reason is that the improvement in

efficiency ratio generally transforms to developed profitability (West, 2018). In this way, the

efficiency ratios are best to be used to know how to reduce expenses as well as increase

earnings. It can that the efficiency of company can be assessed from different ratios. These

efficiency ratios are accounts receivable turnover, sale to inventory, asset turnover, accounts

payable to sales, sales to net working capital, cash flow return on asset, stock turnover ratio

as well as asset turnover ratios. The asset turnover ratio as well as cash flow return on asset

are significant to measure company’s efficiency (Williams and Dobelman, 2017). These two

ratios are discussed below -

Asset turnover

The asset turnover ratio is helpful in measuring the value of sales or revenue of company

relative to value of company’s assets. The asset turnover ratio is assessed annually. The

company uses this ratio as the indicator of the efficiency with which the entity is utilising

the assets to get income. The higher the asset turnover ratio, the more efficient a company. It

can say that high asset turnover ratio states that company is doing well. The high ratios states

that the company is making revenue per dollar of the asset. On the other hand, if the entity

has lower asset turnover ratio, it means that company is not using assets effectively to

generate revenue. It is assessed that the asset turnover ratio was 1.78 in 2015. It was slightly

increased to 1.88 in 2016. Further, it was slightly decreased to 1.83 in 2017 and 1.63 in 2018.

It was 1.57 in 2019. It means company is not doing well. In this way, the entity can improve

the low asset turnover ratio by constantly utilising assets restraining purchase of inventories,

as well as make sales without buying new assets (Satryo, Rokhmania and Diptyana, 2017).

7

time to take cash from customer or the amount of time to change inventory into cash. In this

way, it creates the efficiency ratios significant. The main reason is that the improvement in

efficiency ratio generally transforms to developed profitability (West, 2018). In this way, the

efficiency ratios are best to be used to know how to reduce expenses as well as increase

earnings. It can that the efficiency of company can be assessed from different ratios. These

efficiency ratios are accounts receivable turnover, sale to inventory, asset turnover, accounts

payable to sales, sales to net working capital, cash flow return on asset, stock turnover ratio

as well as asset turnover ratios. The asset turnover ratio as well as cash flow return on asset

are significant to measure company’s efficiency (Williams and Dobelman, 2017). These two

ratios are discussed below -

Asset turnover

The asset turnover ratio is helpful in measuring the value of sales or revenue of company

relative to value of company’s assets. The asset turnover ratio is assessed annually. The

company uses this ratio as the indicator of the efficiency with which the entity is utilising

the assets to get income. The higher the asset turnover ratio, the more efficient a company. It

can say that high asset turnover ratio states that company is doing well. The high ratios states

that the company is making revenue per dollar of the asset. On the other hand, if the entity

has lower asset turnover ratio, it means that company is not using assets effectively to

generate revenue. It is assessed that the asset turnover ratio was 1.78 in 2015. It was slightly

increased to 1.88 in 2016. Further, it was slightly decreased to 1.83 in 2017 and 1.63 in 2018.

It was 1.57 in 2019. It means company is not doing well. In this way, the entity can improve

the low asset turnover ratio by constantly utilising assets restraining purchase of inventories,

as well as make sales without buying new assets (Satryo, Rokhmania and Diptyana, 2017).

FINANCIAL ANALYSIS- NICK SCALI LIMITED

8

Cash Flow Position

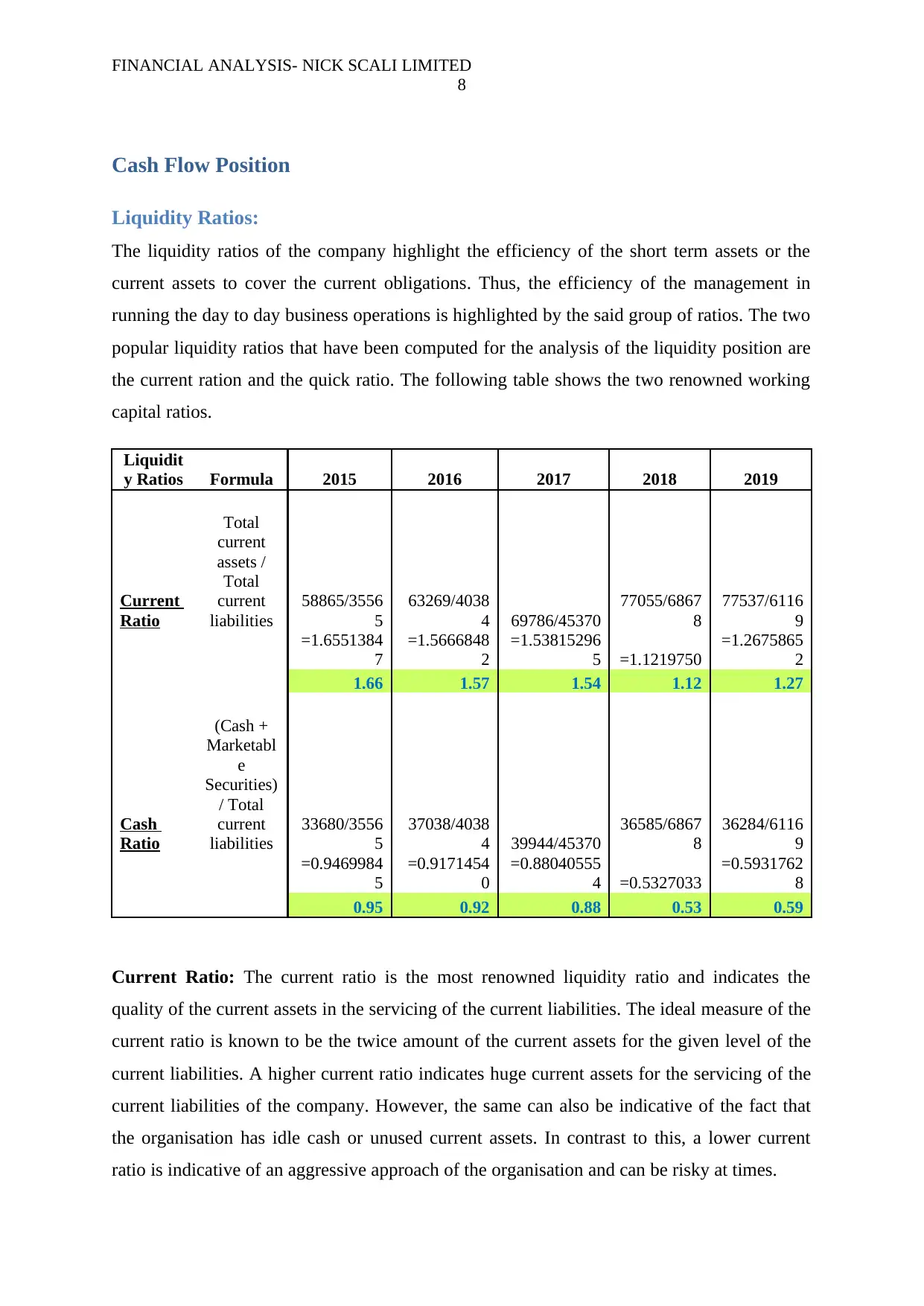

Liquidity Ratios:

The liquidity ratios of the company highlight the efficiency of the short term assets or the

current assets to cover the current obligations. Thus, the efficiency of the management in

running the day to day business operations is highlighted by the said group of ratios. The two

popular liquidity ratios that have been computed for the analysis of the liquidity position are

the current ration and the quick ratio. The following table shows the two renowned working

capital ratios.

Liquidit

y Ratios Formula 2015 2016 2017 2018 2019

Current

Ratio

Total

current

assets /

Total

current

liabilities

58865/3556

5

63269/4038

4 69786/45370

77055/6867

8

77537/6116

9

=1.6551384

7

=1.5666848

2

=1.53815296

5 =1.1219750

=1.2675865

2

1.66 1.57 1.54 1.12 1.27

Cash

Ratio

(Cash +

Marketabl

e

Securities)

/ Total

current

liabilities

33680/3556

5

37038/4038

4 39944/45370

36585/6867

8

36284/6116

9

=0.9469984

5

=0.9171454

0

=0.88040555

4 =0.5327033

=0.5931762

8

0.95 0.92 0.88 0.53 0.59

Current Ratio: The current ratio is the most renowned liquidity ratio and indicates the

quality of the current assets in the servicing of the current liabilities. The ideal measure of the

current ratio is known to be the twice amount of the current assets for the given level of the

current liabilities. A higher current ratio indicates huge current assets for the servicing of the

current liabilities of the company. However, the same can also be indicative of the fact that

the organisation has idle cash or unused current assets. In contrast to this, a lower current

ratio is indicative of an aggressive approach of the organisation and can be risky at times.

8

Cash Flow Position

Liquidity Ratios:

The liquidity ratios of the company highlight the efficiency of the short term assets or the

current assets to cover the current obligations. Thus, the efficiency of the management in

running the day to day business operations is highlighted by the said group of ratios. The two

popular liquidity ratios that have been computed for the analysis of the liquidity position are

the current ration and the quick ratio. The following table shows the two renowned working

capital ratios.

Liquidit

y Ratios Formula 2015 2016 2017 2018 2019

Current

Ratio

Total

current

assets /

Total

current

liabilities

58865/3556

5

63269/4038

4 69786/45370

77055/6867

8

77537/6116

9

=1.6551384

7

=1.5666848

2

=1.53815296

5 =1.1219750

=1.2675865

2

1.66 1.57 1.54 1.12 1.27

Cash

Ratio

(Cash +

Marketabl

e

Securities)

/ Total

current

liabilities

33680/3556

5

37038/4038

4 39944/45370

36585/6867

8

36284/6116

9

=0.9469984

5

=0.9171454

0

=0.88040555

4 =0.5327033

=0.5931762

8

0.95 0.92 0.88 0.53 0.59

Current Ratio: The current ratio is the most renowned liquidity ratio and indicates the

quality of the current assets in the servicing of the current liabilities. The ideal measure of the

current ratio is known to be the twice amount of the current assets for the given level of the

current liabilities. A higher current ratio indicates huge current assets for the servicing of the

current liabilities of the company. However, the same can also be indicative of the fact that

the organisation has idle cash or unused current assets. In contrast to this, a lower current

ratio is indicative of an aggressive approach of the organisation and can be risky at times.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCIAL ANALYSIS- NICK SCALI LIMITED

9

9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCIAL ANALYSIS- NICK SCALI LIMITED

10

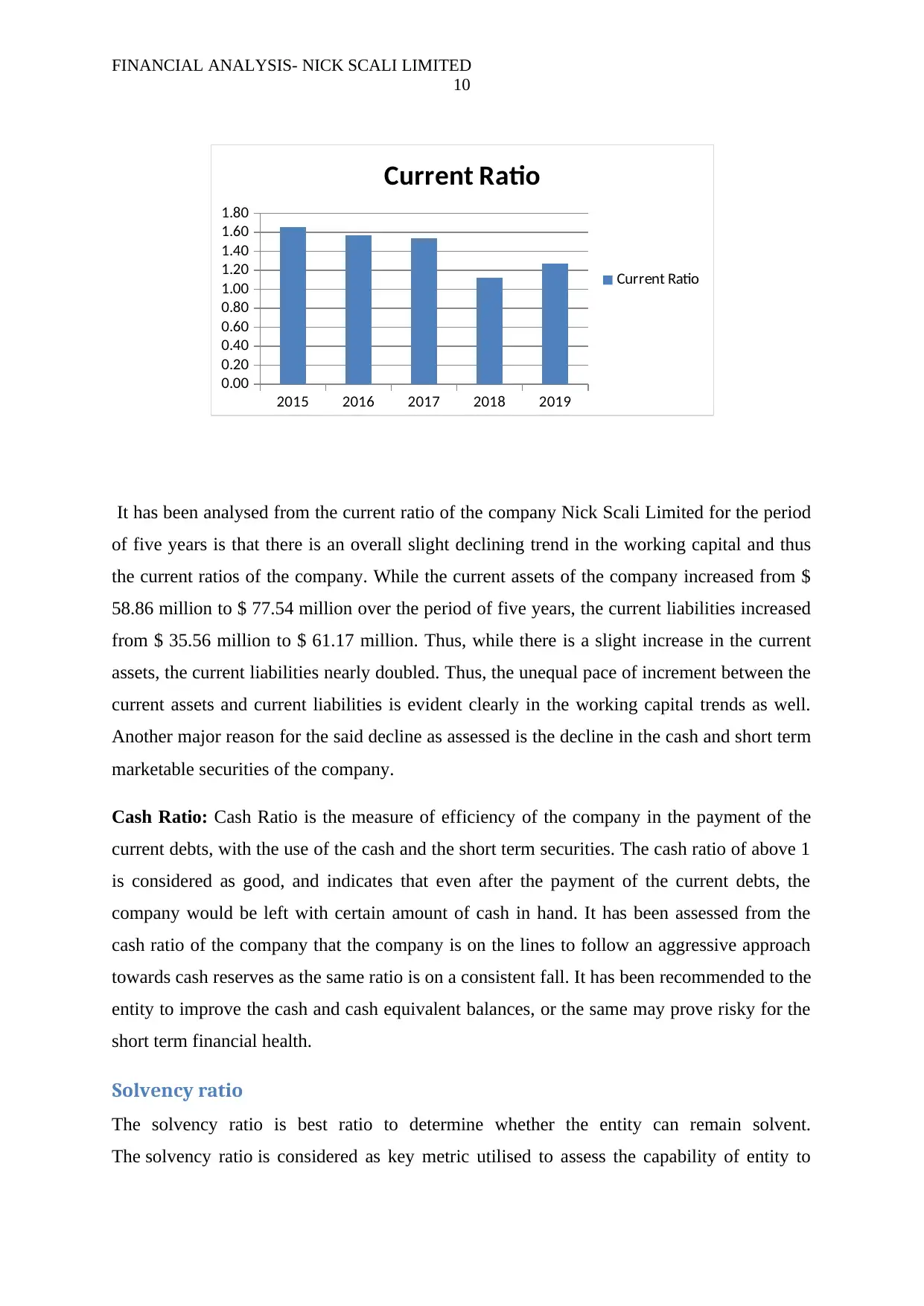

It has been analysed from the current ratio of the company Nick Scali Limited for the period

of five years is that there is an overall slight declining trend in the working capital and thus

the current ratios of the company. While the current assets of the company increased from $

58.86 million to $ 77.54 million over the period of five years, the current liabilities increased

from $ 35.56 million to $ 61.17 million. Thus, while there is a slight increase in the current

assets, the current liabilities nearly doubled. Thus, the unequal pace of increment between the

current assets and current liabilities is evident clearly in the working capital trends as well.

Another major reason for the said decline as assessed is the decline in the cash and short term

marketable securities of the company.

Cash Ratio: Cash Ratio is the measure of efficiency of the company in the payment of the

current debts, with the use of the cash and the short term securities. The cash ratio of above 1

is considered as good, and indicates that even after the payment of the current debts, the

company would be left with certain amount of cash in hand. It has been assessed from the

cash ratio of the company that the company is on the lines to follow an aggressive approach

towards cash reserves as the same ratio is on a consistent fall. It has been recommended to the

entity to improve the cash and cash equivalent balances, or the same may prove risky for the

short term financial health.

Solvency ratio

The solvency ratio is best ratio to determine whether the entity can remain solvent.

The solvency ratio is considered as key metric utilised to assess the capability of entity to

2015 2016 2017 2018 2019

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

1.80

Current Ratio

Current Ratio

10

It has been analysed from the current ratio of the company Nick Scali Limited for the period

of five years is that there is an overall slight declining trend in the working capital and thus

the current ratios of the company. While the current assets of the company increased from $

58.86 million to $ 77.54 million over the period of five years, the current liabilities increased

from $ 35.56 million to $ 61.17 million. Thus, while there is a slight increase in the current

assets, the current liabilities nearly doubled. Thus, the unequal pace of increment between the

current assets and current liabilities is evident clearly in the working capital trends as well.

Another major reason for the said decline as assessed is the decline in the cash and short term

marketable securities of the company.

Cash Ratio: Cash Ratio is the measure of efficiency of the company in the payment of the

current debts, with the use of the cash and the short term securities. The cash ratio of above 1

is considered as good, and indicates that even after the payment of the current debts, the

company would be left with certain amount of cash in hand. It has been assessed from the

cash ratio of the company that the company is on the lines to follow an aggressive approach

towards cash reserves as the same ratio is on a consistent fall. It has been recommended to the

entity to improve the cash and cash equivalent balances, or the same may prove risky for the

short term financial health.

Solvency ratio

The solvency ratio is best ratio to determine whether the entity can remain solvent.

The solvency ratio is considered as key metric utilised to assess the capability of entity to

2015 2016 2017 2018 2019

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

1.80

Current Ratio

Current Ratio

FINANCIAL ANALYSIS- NICK SCALI LIMITED

11

fulfil the obligation related to debts. This ratio is helpful in measuring the extent to which

asset covers commitment for the payment in upcoming period. Solvency ratio of the entity is

considered as size of the capital relative to risk taken by it. It can say that the future business

lender uses this ratio. It is indicated by the solvency ratio that whether the cash flow of

company is sufficient to fulfil the short-term liabilities as well as long-term liabilities. It is

evident that the lower solvency ratio of company leads the great possibility that this would

default on the debts obligation (Salawau, 2017).

Further, the solvency ratio is considered as wide-ranging measure of solvency. The main

reason is that it is helpful in assessing the actual cash flow of company in place of net income

by including depreciation again and non-cash expenditure to measure the ability of company

to stay afloat. It is evident that the solvency ratio assesses the cash flow ability regarding the

liabilities in place of only short-term debts. Therefore, one can use the solvency ratio to

assess long-term health of company by assessing the capability of repayment for the long-

term debts as well as interest on long-term debt. In general, the solvency ratio more than

twenty per cent is considered fiscally sound. However, this ratio can differ from industry to

industry. In this way, the entity is capable to close out the long-term debt obligation when

they become due utilising operating revenue. Henceforth, the lenders will usually use the

solvency ratio as a factor for soundness by assessing the financial statement of company. The

solvency ratio examines a company's ability to meet its long-term obligations. This ratio is

utilised by potential lenders at the time of assessing creditworthiness of company. A higher

ratio percentage result indicates a company's increased ability to cover its liabilities over the

long term. There are different solvency ratios to assess the solvency of company. These are

debt to equity as well as equity ratio. These are discussed as below-

The equity ratio is solvency ratio. It is helpful in measuring the amount of asset that is funded

by owners' investment by making comparison with total equity in organisation to total assets.

This ratio puts focus on the two significant financial concepts of solvent operations of

company. The low equity ratio shows that the company has used more debt to pay for the

assets. This ratio also states that how much shareholder will get at the time of liquidation

(Singh, 2017). The ratio states the dependency of company on debt. It also shows stability of

company. The equity ratio of company was 0.48 in 2015 and 2016. It was increased to .51 in

2017. Further, it was decreased to .49 in 2018 and 2019. It means company is doing well. The

11

fulfil the obligation related to debts. This ratio is helpful in measuring the extent to which

asset covers commitment for the payment in upcoming period. Solvency ratio of the entity is

considered as size of the capital relative to risk taken by it. It can say that the future business

lender uses this ratio. It is indicated by the solvency ratio that whether the cash flow of

company is sufficient to fulfil the short-term liabilities as well as long-term liabilities. It is

evident that the lower solvency ratio of company leads the great possibility that this would

default on the debts obligation (Salawau, 2017).

Further, the solvency ratio is considered as wide-ranging measure of solvency. The main

reason is that it is helpful in assessing the actual cash flow of company in place of net income

by including depreciation again and non-cash expenditure to measure the ability of company

to stay afloat. It is evident that the solvency ratio assesses the cash flow ability regarding the

liabilities in place of only short-term debts. Therefore, one can use the solvency ratio to

assess long-term health of company by assessing the capability of repayment for the long-

term debts as well as interest on long-term debt. In general, the solvency ratio more than

twenty per cent is considered fiscally sound. However, this ratio can differ from industry to

industry. In this way, the entity is capable to close out the long-term debt obligation when

they become due utilising operating revenue. Henceforth, the lenders will usually use the

solvency ratio as a factor for soundness by assessing the financial statement of company. The

solvency ratio examines a company's ability to meet its long-term obligations. This ratio is

utilised by potential lenders at the time of assessing creditworthiness of company. A higher

ratio percentage result indicates a company's increased ability to cover its liabilities over the

long term. There are different solvency ratios to assess the solvency of company. These are

debt to equity as well as equity ratio. These are discussed as below-

The equity ratio is solvency ratio. It is helpful in measuring the amount of asset that is funded

by owners' investment by making comparison with total equity in organisation to total assets.

This ratio puts focus on the two significant financial concepts of solvent operations of

company. The low equity ratio shows that the company has used more debt to pay for the

assets. This ratio also states that how much shareholder will get at the time of liquidation

(Singh, 2017). The ratio states the dependency of company on debt. It also shows stability of

company. The equity ratio of company was 0.48 in 2015 and 2016. It was increased to .51 in

2017. Further, it was decreased to .49 in 2018 and 2019. It means company is doing well. The

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 26

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.