Financial Analysis of EasyJet: UK Equity Investment Recommendation

VerifiedAdded on 2023/01/19

|15

|4246

|44

Report

AI Summary

This report provides a detailed financial analysis of EasyJet, evaluating its potential as an investment opportunity. It begins with an introduction to the company, its competitors, and its operational context within the aviation industry. The analysis then delves into the global and UK economic outlook, considering factors like inflation, unemployment, and GDP growth, and assesses their impact on EasyJet's business. Furthermore, the report examines the sector's performance, highlighting challenges such as rising oil prices and competition. A significant portion of the report is dedicated to financial statement analysis, utilizing various ratios to assess profitability, liquidity, efficiency, and investment metrics. Key ratios such as net profit margin, gross profit margin, operating profit margin, ROCE, return on assets, return on equity, current ratio, and accounts receivable turnover ratio are analyzed. The report concludes with an investment recommendation based on the findings from the economic, sector, and financial analysis, providing a comprehensive overview of EasyJet's financial health and future prospects.

FINANCIAL ANALYSIS OF

EASY JET

EASY JET

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

Global economy outlook..................................................................................................................1

Sector performance..........................................................................................................................2

Financial statement analysis............................................................................................................3

CONCLUSION................................................................................................................................5

REFERENCES................................................................................................................................6

APPENDIX....................................................................................................................................................7

Table 1Ratio analysis.......................................................................................................................8

INTRODUCTION...........................................................................................................................1

Global economy outlook..................................................................................................................1

Sector performance..........................................................................................................................2

Financial statement analysis............................................................................................................3

CONCLUSION................................................................................................................................5

REFERENCES................................................................................................................................6

APPENDIX....................................................................................................................................................7

Table 1Ratio analysis.......................................................................................................................8

INTRODUCTION

In the current report analysis of Easy jet is done and opportunity of making profitable investment is explored. Before making

investment in any company it is necessary to gather information about background of the business firm. Easy jet is one of the best

low-cost airlines in the UK. There are number of competitors of Easy jet namely Ryanair which also provide quality of service at

competitive price. In current time period it is operating in 30 nations and operate flights on 1000 routes. It has 14000 employees in its

workforce. In past few months oil prices surged which lead to low profit in the business and due to this reason large number of

business firms shut down. This create a lot of opportunity for Easy jet in its business as more market will be available for it. With

passage of time firm bring lot of changes in its business strategy as it purchases new slots so that more flights can be commenced on

new routes. Easy jet also increases its passenger capacity and innovate its business operations. This reflect that firm do lot of new

things in its business and its management is quite active. Main objective of analysis is to identify whether it will be better to invest in

Easy jet. In this regard economic analysis of UK and world economy will be done so that it can be identified whether in upcoming

time period firm will face more or less challenges in its business. On other hand, sector analysis will be done to find extent to which

sector is performing well and face challenges. Thereafter, company ratio analysis will be done to evaluate firm performance. On basis

of entire analysis finally recommendation section will be prepared.

Global economy outlook

Global economic condition has great impact on the business firms operating in the domestic and international market. Turmoil in

economic conditions at global level lead to high inflation rate, low demand in the market and higher unemployment rate. EasyJet is

operating in aviation sector and provide low cost airline service (UK economic outlook., 2019). Global trends heavily affect its

business. In below section some trends in respect to global economy are explained in detail. Inflation: Global inflation rate is 3.8% which can be considered normal and inevitable for growth. This is because low

inflation rate may convert in deflation which is big hit for any economy. Slight inflation leads to elevation in firm’s

1

In the current report analysis of Easy jet is done and opportunity of making profitable investment is explored. Before making

investment in any company it is necessary to gather information about background of the business firm. Easy jet is one of the best

low-cost airlines in the UK. There are number of competitors of Easy jet namely Ryanair which also provide quality of service at

competitive price. In current time period it is operating in 30 nations and operate flights on 1000 routes. It has 14000 employees in its

workforce. In past few months oil prices surged which lead to low profit in the business and due to this reason large number of

business firms shut down. This create a lot of opportunity for Easy jet in its business as more market will be available for it. With

passage of time firm bring lot of changes in its business strategy as it purchases new slots so that more flights can be commenced on

new routes. Easy jet also increases its passenger capacity and innovate its business operations. This reflect that firm do lot of new

things in its business and its management is quite active. Main objective of analysis is to identify whether it will be better to invest in

Easy jet. In this regard economic analysis of UK and world economy will be done so that it can be identified whether in upcoming

time period firm will face more or less challenges in its business. On other hand, sector analysis will be done to find extent to which

sector is performing well and face challenges. Thereafter, company ratio analysis will be done to evaluate firm performance. On basis

of entire analysis finally recommendation section will be prepared.

Global economy outlook

Global economic condition has great impact on the business firms operating in the domestic and international market. Turmoil in

economic conditions at global level lead to high inflation rate, low demand in the market and higher unemployment rate. EasyJet is

operating in aviation sector and provide low cost airline service (UK economic outlook., 2019). Global trends heavily affect its

business. In below section some trends in respect to global economy are explained in detail. Inflation: Global inflation rate is 3.8% which can be considered normal and inevitable for growth. This is because low

inflation rate may convert in deflation which is big hit for any economy. Slight inflation leads to elevation in firm’s

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

profitability. Inflation rate of 3.8% indicate that world economy is on track of progress and in upcoming time period this

growth may multiple. Easy jet is mainly operating in UK and specially in Europe. Inflation rate of mentioned nation is 1.80%

which is very low and will motivate people to take more and more flights of Easy jet to go to destination place. Unemployment: Unemployment rate in UK is 3.8% which can be considered low or moderate. UK GDP is only 1.4% which is

indicating that it is not growing at fast pace. In such situation current unemployment scenario may prevail in upcoming time

period also and with turmoil in economy unemployment rate may rise which will ultimately lead to decline in firm

profitability. Forecasted GDP: Global GDP is expected to grow by 2.8% which reflect that further slowdown will be observed in global

economy. Sharp elevation in demand for low cost airline in not expected in the upcoming time period. Long term GDP growth

of UK economy may be nearby to 2%. It can not be considered as good economic growth. Thus, further problem for low cost

airline may occur. Hence, it can be said that global and domestic economic conditions are not favourable for business and

slowdown in economy may heavily affect aviation sector.

Sector performance

Aviation firms across globe specially in Europe are facing many problems. Oil prices increased in past couple of months which

is mounting pressure on the firms. Companies cannot easily pass impact of oil price on the customers. They have to charge same price

on travellers even ticket price gets increased. Hence, profit get declined and due to such kind of situation many aviation firms in

Europe sold out. Some of these firms are Cyprus Cobalt, Latvia Primera air and Germany small planet etc. Apart from higher fuel

price, compensation pay-out for delay is another reason behind decline in the firm’s profitability (The Airline industry in UK statistics

and facts., 2019). With elimination of few competitor’s face of aviation industry is changing at fast pace. As it can be observed that

because of elimination of few rivals now business firms are able to charge higher fee from the travellers. Overall, it can be said that

low profit is one of major problem firms faced in their business and economic turmoil is the one of the main reason behind this. Low

2

growth may multiple. Easy jet is mainly operating in UK and specially in Europe. Inflation rate of mentioned nation is 1.80%

which is very low and will motivate people to take more and more flights of Easy jet to go to destination place. Unemployment: Unemployment rate in UK is 3.8% which can be considered low or moderate. UK GDP is only 1.4% which is

indicating that it is not growing at fast pace. In such situation current unemployment scenario may prevail in upcoming time

period also and with turmoil in economy unemployment rate may rise which will ultimately lead to decline in firm

profitability. Forecasted GDP: Global GDP is expected to grow by 2.8% which reflect that further slowdown will be observed in global

economy. Sharp elevation in demand for low cost airline in not expected in the upcoming time period. Long term GDP growth

of UK economy may be nearby to 2%. It can not be considered as good economic growth. Thus, further problem for low cost

airline may occur. Hence, it can be said that global and domestic economic conditions are not favourable for business and

slowdown in economy may heavily affect aviation sector.

Sector performance

Aviation firms across globe specially in Europe are facing many problems. Oil prices increased in past couple of months which

is mounting pressure on the firms. Companies cannot easily pass impact of oil price on the customers. They have to charge same price

on travellers even ticket price gets increased. Hence, profit get declined and due to such kind of situation many aviation firms in

Europe sold out. Some of these firms are Cyprus Cobalt, Latvia Primera air and Germany small planet etc. Apart from higher fuel

price, compensation pay-out for delay is another reason behind decline in the firm’s profitability (The Airline industry in UK statistics

and facts., 2019). With elimination of few competitor’s face of aviation industry is changing at fast pace. As it can be observed that

because of elimination of few rivals now business firms are able to charge higher fee from the travellers. Overall, it can be said that

low profit is one of major problem firms faced in their business and economic turmoil is the one of the main reason behind this. Low

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

economic growth and unemployment as well as less economic stability are the three core reasons because of which in future time

period Easy jet and other may face lot of problem in earning profit.

Financial statement analysis

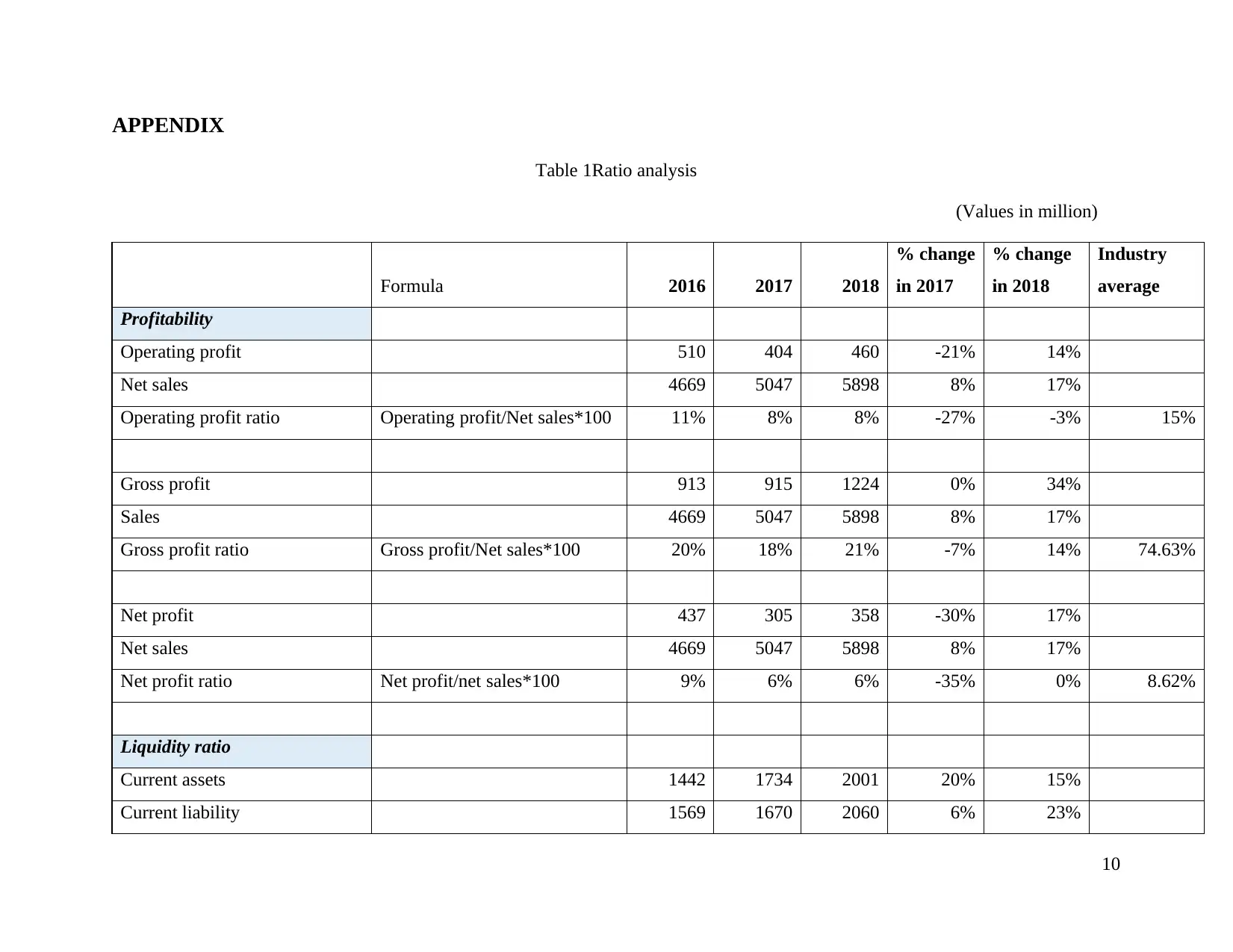

Net profit ratio: It is the ratio which reflect firm capability to control its expenses in the business. Net profit ratio simply

reflects portion of net sales that is covered by the net profit of the business firm. If net profit is increasing consistently then in

that case it can be assumed that strict control is made on expenses in the business (Williams and Dobelman, 2017). Table is

indicating that net profit ratio of the firm declines from 9% to 6% by -35% in year 2017. In 2018 net profit remain same at 6%.

Hence, firm efficiency declines in previous two years and there is stability in that trend. Main reason behind decline in net

profit ratio is higher oil prices in the business. Net profit ratio of the firm is below industry net profit ratio 8.62%. If further oil

price decline in upcoming time period then in that case net profit surely will reduce which is one of the major matter of

concern in respect to Easy jet. Firms normally in order to control such kind of situation can make investment in derivatives.

Loss faced in the crude oil purchase may be offset by the gains made on derivative contracts. Thus, it can be said that by

following such kind of strategy to some extent situation can be bring in control.

Gross profit ratio: Gross profit ratio of the business firm is 21% in 2018 and it decline to 18% in year 2017. In year 2016 gross

profit ratio was 20%. It can be said that gross profit ratio is moving in same direction almost. In 2017 ratio value decline by -

7% but in year 2018 it increased by 14%. Gross profit ratio of industry is 74.63% and same of firm is 21%. On this basis it can

be said that firm give very poor performance relative to industry.

Operating profit margin: Operating profit ratio of Easy jet declined consistently from 11% to 7.80% from year 2016 to 2018.

In year 2018 it almost remains same relative to 2017. From year 2016 ratio value declined by 27%. This indicate that firm do

not have control on direct expenses. Industry average is 14.55% and same of the Easy jet is 7.80% in 2018 which means that

firm have poor operating profit margin ratio.

3

period Easy jet and other may face lot of problem in earning profit.

Financial statement analysis

Net profit ratio: It is the ratio which reflect firm capability to control its expenses in the business. Net profit ratio simply

reflects portion of net sales that is covered by the net profit of the business firm. If net profit is increasing consistently then in

that case it can be assumed that strict control is made on expenses in the business (Williams and Dobelman, 2017). Table is

indicating that net profit ratio of the firm declines from 9% to 6% by -35% in year 2017. In 2018 net profit remain same at 6%.

Hence, firm efficiency declines in previous two years and there is stability in that trend. Main reason behind decline in net

profit ratio is higher oil prices in the business. Net profit ratio of the firm is below industry net profit ratio 8.62%. If further oil

price decline in upcoming time period then in that case net profit surely will reduce which is one of the major matter of

concern in respect to Easy jet. Firms normally in order to control such kind of situation can make investment in derivatives.

Loss faced in the crude oil purchase may be offset by the gains made on derivative contracts. Thus, it can be said that by

following such kind of strategy to some extent situation can be bring in control.

Gross profit ratio: Gross profit ratio of the business firm is 21% in 2018 and it decline to 18% in year 2017. In year 2016 gross

profit ratio was 20%. It can be said that gross profit ratio is moving in same direction almost. In 2017 ratio value decline by -

7% but in year 2018 it increased by 14%. Gross profit ratio of industry is 74.63% and same of firm is 21%. On this basis it can

be said that firm give very poor performance relative to industry.

Operating profit margin: Operating profit ratio of Easy jet declined consistently from 11% to 7.80% from year 2016 to 2018.

In year 2018 it almost remains same relative to 2017. From year 2016 ratio value declined by 27%. This indicate that firm do

not have control on direct expenses. Industry average is 14.55% and same of the Easy jet is 7.80% in 2018 which means that

firm have poor operating profit margin ratio.

3

ROCE: ROCE of the firm was 13% in year 2016 and same reduced to 8.10% in 2017 and increased to 8.47% in 2018which

means that ratio declined by 38% in year 2017 and increased by 5% in 2018. Firm failed to make best use of capital in its

business. ROCE of the firm is 8.47% and same of industry is 13.38% which reflect that firm poorly perform on this front.

Return on asset: It indicate gain that is made in business by using asset. Return on asset decline consistently from 8% to 5%

which is matter of concern and indicate that percentage gain is less. Decline of -36% is observed in 2017 and 2018 percentage

remain 0% (The warmest welcome in the sky., 2019). Easy jet failed to make effective use of assets in its business. Easy jet

ratio is slightly lower then industry. Thus, Easy jet must identify assets which are not used effectively in the business and must

either replace them in business or must innovate it to make its best use.

Return on equity: It reflect percentage return that is generated on equity. Easy jet return on equity ratio is half of industry ratio

which indicate that firm is generating less return for its investors (Airline industry., 2019). From table it can be observed that

return on equity decrease from 16% to 11% which means that for shareholders sufficient amount of return is not generated in

the business (Lecy and Searing, 2015). Decline of -33% is observed in 2017 and 2018 percentage remain 0%. This seriously

need to be taken because they run and operate company. It is their strategy and understanding which lead to growth of

company. Hence, cost control must be done in the business to increase profit.

Current ratio: It is the ratio indicating capacity of the business firm to pay current liability or short-term liability on time.

Standard ratio of the current ratio is 2:1 which means that for every unit of current liability there must be 2 units of current

assets. This means that after paying current liability 1 unit of current asset must remain in the business (Robinson. and et.al.,

2015). Thus, it can be said that current ratio to great extent indicate firm capability to make payment of current liability by

using current assets. Current ratio of the firm is above industry ratio value 0.53. Table is indicating that current ratio of Easy jet

was 0.91 in year 2016 and it increase to 1.03 in year 2017. Increase of 13% is observed. Any big change does not come in the

current ratio as it indicates that payment capacity of current liability is almost same in both years. In year 2018 current ratio

value become 0.97 which indicate that slight decline of -6% comes in current ratio but it is slight decline relative to previous

4

means that ratio declined by 38% in year 2017 and increased by 5% in 2018. Firm failed to make best use of capital in its

business. ROCE of the firm is 8.47% and same of industry is 13.38% which reflect that firm poorly perform on this front.

Return on asset: It indicate gain that is made in business by using asset. Return on asset decline consistently from 8% to 5%

which is matter of concern and indicate that percentage gain is less. Decline of -36% is observed in 2017 and 2018 percentage

remain 0% (The warmest welcome in the sky., 2019). Easy jet failed to make effective use of assets in its business. Easy jet

ratio is slightly lower then industry. Thus, Easy jet must identify assets which are not used effectively in the business and must

either replace them in business or must innovate it to make its best use.

Return on equity: It reflect percentage return that is generated on equity. Easy jet return on equity ratio is half of industry ratio

which indicate that firm is generating less return for its investors (Airline industry., 2019). From table it can be observed that

return on equity decrease from 16% to 11% which means that for shareholders sufficient amount of return is not generated in

the business (Lecy and Searing, 2015). Decline of -33% is observed in 2017 and 2018 percentage remain 0%. This seriously

need to be taken because they run and operate company. It is their strategy and understanding which lead to growth of

company. Hence, cost control must be done in the business to increase profit.

Current ratio: It is the ratio indicating capacity of the business firm to pay current liability or short-term liability on time.

Standard ratio of the current ratio is 2:1 which means that for every unit of current liability there must be 2 units of current

assets. This means that after paying current liability 1 unit of current asset must remain in the business (Robinson. and et.al.,

2015). Thus, it can be said that current ratio to great extent indicate firm capability to make payment of current liability by

using current assets. Current ratio of the firm is above industry ratio value 0.53. Table is indicating that current ratio of Easy jet

was 0.91 in year 2016 and it increase to 1.03 in year 2017. Increase of 13% is observed. Any big change does not come in the

current ratio as it indicates that payment capacity of current liability is almost same in both years. In year 2018 current ratio

value become 0.97 which indicate that slight decline of -6% comes in current ratio but it is slight decline relative to previous

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

year. This means that payment capacity of the firm almost remains same. Situation is not critical but if firm profitability

decline then in that case current ratio may reduce which may lead to development of problem for the business firm. Currently,

if firm pay all its current liability by using current asset then nothing will remain aside in respect to latter one. In such situation

Easy jet may face problem in meeting its working capital needs. Thus, there is need to improve this ratio.

Account receivable turnover ratio: It is the ratio reflecting Easy jet capability to recover debt amount which it gives to others

in its business. Higher is the number better is considered for the firm. Higher number reflect that in short time period firm is

getting debt amount recovered from its debtors. This also reflect that debtor of the business firm are financially sound (Altman,

E and et.al., 2017). Industry account receivable turnover ratio is greater than firm ratio value. Hence, firm relative to industry is

less capable to convert receivable in to cash. From the table it can be observed that account receivable turnover ratio of the

Easy jet was 22.77 in year 2016 and it decrease to 18.35 in year 2017. Decline of -19% is observed in year 2017. This means

that in year 2016 23 times debt amount was recovered from debtors by Easy jet. On other hand, in year 18 times debt amount

was recovered from debtors. In year 2018 sharp decline is observed in account receivable turnover ratio as it reduces to 14.45

just become half of 2016. Reduction of -21% is observed in 2018 relative to 2017. This reflect that either firm is giving debt is

large amount to those whose financial condition already is not good or because of economic turmoil as part of safe strategy

debtors are making delay in payment even their financial health is good.

Receivable turnover period: Ratio reflect that in year 2016 firm received its trade receivables amount in 16 days which

increased to 20 days in year 2017. In year 2018 ratio increase to 25 days. This means that consistently delay is observed on

receipt of payment. 24% and 27% increase in year 2017 and 2018 is observed relative to previous year. It can be said that firm

need to improve its receivable management. However, value of ratio for industry is 16.38 and same for the firm is 25. It can be

said that relative to industry Easy jet in short time is receiving receivable amount.

5

decline then in that case current ratio may reduce which may lead to development of problem for the business firm. Currently,

if firm pay all its current liability by using current asset then nothing will remain aside in respect to latter one. In such situation

Easy jet may face problem in meeting its working capital needs. Thus, there is need to improve this ratio.

Account receivable turnover ratio: It is the ratio reflecting Easy jet capability to recover debt amount which it gives to others

in its business. Higher is the number better is considered for the firm. Higher number reflect that in short time period firm is

getting debt amount recovered from its debtors. This also reflect that debtor of the business firm are financially sound (Altman,

E and et.al., 2017). Industry account receivable turnover ratio is greater than firm ratio value. Hence, firm relative to industry is

less capable to convert receivable in to cash. From the table it can be observed that account receivable turnover ratio of the

Easy jet was 22.77 in year 2016 and it decrease to 18.35 in year 2017. Decline of -19% is observed in year 2017. This means

that in year 2016 23 times debt amount was recovered from debtors by Easy jet. On other hand, in year 18 times debt amount

was recovered from debtors. In year 2018 sharp decline is observed in account receivable turnover ratio as it reduces to 14.45

just become half of 2016. Reduction of -21% is observed in 2018 relative to 2017. This reflect that either firm is giving debt is

large amount to those whose financial condition already is not good or because of economic turmoil as part of safe strategy

debtors are making delay in payment even their financial health is good.

Receivable turnover period: Ratio reflect that in year 2016 firm received its trade receivables amount in 16 days which

increased to 20 days in year 2017. In year 2018 ratio increase to 25 days. This means that consistently delay is observed on

receipt of payment. 24% and 27% increase in year 2017 and 2018 is observed relative to previous year. It can be said that firm

need to improve its receivable management. However, value of ratio for industry is 16.38 and same for the firm is 25. It can be

said that relative to industry Easy jet in short time is receiving receivable amount.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Total asset turnover ratio: Asset turnover ratio of the firm is almost same from year 2016 to 2018. It can be observed that 0.85

was in year 2016 and same decreased to 0.84. Industry asset turnover ratio is 0.78 and relative to it firm is performing better.

Hence, it can be said that firm perform better on this front.

Price earnings ratio: It is the ratio which is used for equity valuation as its value is compared to industry PE ratio to identify

whether firm shares are overvalued or undervalued (Parson and et.al., 2015). Relative to industry firm shares are overvalued. It

can be observed from the table that PE ratio of Easy jet was 914.82 in year 2016 and same increased to 1705 in year 2017 by

86%. This further decline to 1184 in year 2018 relative to 2017 by -31%. Thus, it can be said that firm shares value decline

because of low profit. Thus, Easy jet must focus on increasing its business profit.

Earnings per share: This ratio reflect the earning that shareholder receive on each unit of shares they hold (Caserio, Panaro.

and Trucco, 2016). EPS of EasyJet is lower than industry ratio. Table reflect that EPS of the firm in the year 2016 was 1.10

and same decreased to 0.76 in year 2017 by -30%. Further, it increased to 0.90 in 2018 relative to 2017 by 17% which reflect

that due to loss in business or low profit investors are earning less amount on each share they hold in their business in year

2017 but firm perform better in 2018 which lead to high EPS. Dividend pay-out ratio: It is the ratio which reflect portion of net income used to pay dividend to the shareholders. DPOR was

140.81% in year 2016. In FY 2017 and 2018 value was zero and this indicate that firm in single year pay dividend and of

higher percentage to its shareholders. Dividend pay-out ratio of industry is 8.85% and same is much higher then Easy jet. Firm

need to do work on this front. Dividend per share: Dividend on each share in year 2016 was 1.55 and in next two years no dividend is paid to the

shareholders. Hence, value of ratio is zero. Dividend per share of the firm is also low relative to industry and performance is

poor.

6

was in year 2016 and same decreased to 0.84. Industry asset turnover ratio is 0.78 and relative to it firm is performing better.

Hence, it can be said that firm perform better on this front.

Price earnings ratio: It is the ratio which is used for equity valuation as its value is compared to industry PE ratio to identify

whether firm shares are overvalued or undervalued (Parson and et.al., 2015). Relative to industry firm shares are overvalued. It

can be observed from the table that PE ratio of Easy jet was 914.82 in year 2016 and same increased to 1705 in year 2017 by

86%. This further decline to 1184 in year 2018 relative to 2017 by -31%. Thus, it can be said that firm shares value decline

because of low profit. Thus, Easy jet must focus on increasing its business profit.

Earnings per share: This ratio reflect the earning that shareholder receive on each unit of shares they hold (Caserio, Panaro.

and Trucco, 2016). EPS of EasyJet is lower than industry ratio. Table reflect that EPS of the firm in the year 2016 was 1.10

and same decreased to 0.76 in year 2017 by -30%. Further, it increased to 0.90 in 2018 relative to 2017 by 17% which reflect

that due to loss in business or low profit investors are earning less amount on each share they hold in their business in year

2017 but firm perform better in 2018 which lead to high EPS. Dividend pay-out ratio: It is the ratio which reflect portion of net income used to pay dividend to the shareholders. DPOR was

140.81% in year 2016. In FY 2017 and 2018 value was zero and this indicate that firm in single year pay dividend and of

higher percentage to its shareholders. Dividend pay-out ratio of industry is 8.85% and same is much higher then Easy jet. Firm

need to do work on this front. Dividend per share: Dividend on each share in year 2016 was 1.55 and in next two years no dividend is paid to the

shareholders. Hence, value of ratio is zero. Dividend per share of the firm is also low relative to industry and performance is

poor.

6

Dividend coverage ratio: It is the ratio of company earning over dividend on each share. Value of ratio is 0.71 which indicate

that dividend is paid more than income earned. Firm may have play to not pay dividend in upcoming years and due to this

reason perhaps firm pay higher amount of dividend to its shareholders. On this front both industry and firm perform equally. Dividend yield ratio: It indicate dividend received on each dollar spend on purchase of share. Dividend yield ratio was high in

year 0.61 which can be considered good. Thereafter, in year 2017 and 2018 no dividend issued and due to this reason value is

zero. Dividend yield ratio of the firm is low then industry and work is needed by the management on this front.

Debt equity ratio: It reflect the capital structure of the business firm (Edwards, Schwab. and Shevlin, 2015). In comparison to

industry Easy jet capital structure is balanced as it has less debt in the capital structure. Value of debt equity ratio in year 2016

was 0.24 which increase to 0.34 in year 2017. Increase of 39% is observed in the ratio. In year 2018 debt equity ratio was 0.29

and it declined by -14% from 2017 (Purposeful and disciplined growth., 2018). Proportion of debt in capital structure is low

and this means that interest payment liability will also be less on business firm. On this front, firm is in good position.

Interest coverage ratio: This reflect firm capability to pay debt on time. Interest coverage ratio was 39.23 in year 2016 and

same decreased to 13.93 in year 2017. In year 2018 ratio value slightly increased to 15.33. It can be said that in year 2016 ratio

value decline sharply by -64% and in year 2018 it increased to 10%. Hence, Easy jet capability to pay interest on time decline

sharply. Industry coverage ratio is 727 and same of the firm is 15. Thus, Easy jet give very poor performance on this front.

CONCLUSION

On basis of above discussion, it is concluded that firm and economy condition is not good whether it is domestic or international.

GDP growth rate is low and unemployment is moderate. Moreover, oil price increase demotivates people to take flight service.

Further, profit is consistently low and decreasing in the business. It is recommended that investment must not be made in Easy jet as

economic conditions are not supportive to its business.

7

that dividend is paid more than income earned. Firm may have play to not pay dividend in upcoming years and due to this

reason perhaps firm pay higher amount of dividend to its shareholders. On this front both industry and firm perform equally. Dividend yield ratio: It indicate dividend received on each dollar spend on purchase of share. Dividend yield ratio was high in

year 0.61 which can be considered good. Thereafter, in year 2017 and 2018 no dividend issued and due to this reason value is

zero. Dividend yield ratio of the firm is low then industry and work is needed by the management on this front.

Debt equity ratio: It reflect the capital structure of the business firm (Edwards, Schwab. and Shevlin, 2015). In comparison to

industry Easy jet capital structure is balanced as it has less debt in the capital structure. Value of debt equity ratio in year 2016

was 0.24 which increase to 0.34 in year 2017. Increase of 39% is observed in the ratio. In year 2018 debt equity ratio was 0.29

and it declined by -14% from 2017 (Purposeful and disciplined growth., 2018). Proportion of debt in capital structure is low

and this means that interest payment liability will also be less on business firm. On this front, firm is in good position.

Interest coverage ratio: This reflect firm capability to pay debt on time. Interest coverage ratio was 39.23 in year 2016 and

same decreased to 13.93 in year 2017. In year 2018 ratio value slightly increased to 15.33. It can be said that in year 2016 ratio

value decline sharply by -64% and in year 2018 it increased to 10%. Hence, Easy jet capability to pay interest on time decline

sharply. Industry coverage ratio is 727 and same of the firm is 15. Thus, Easy jet give very poor performance on this front.

CONCLUSION

On basis of above discussion, it is concluded that firm and economy condition is not good whether it is domestic or international.

GDP growth rate is low and unemployment is moderate. Moreover, oil price increase demotivates people to take flight service.

Further, profit is consistently low and decreasing in the business. It is recommended that investment must not be made in Easy jet as

economic conditions are not supportive to its business.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books and Journals

Altman, E.I. and et.al., 2017. Financial distress prediction in an international context: A review and empirical analysis of Altman's Z‐

score model. Journal of International Financial Management & Accounting. 28(2). pp.131-171.

Caserio, C., Panaro, D. and Trucco, S., 2016. Management Discussion and Analysis in the US Financial Companies: A Data Mining

Analysis. In Strengthening Information and Control Systems (pp. 43-57). Springer, Cham.

Edwards, A., Schwab, C. and Shevlin, T., 2015. Financial constraints and cash tax savings. The Accounting Review, 91(3), pp.859-

881.

Lecy, J.D. and Searing, E.A., 2015. Anatomy of the nonprofit starvation cycle: An analysis of falling overhead ratios in the nonprofit

sector. Nonprofit and Voluntary Sector Quarterly. 44(3). pp.539-563.

Parson, R. and et.al., 2015. Methods and apparatus for analysing and/or pre-processing financial accounting data. U.S. Patent

9,031,873.

Robinson, T.R. and et.al., 2015. International financial statement analysis. John Wiley & Sons.

Williams, E.E. and Dobelman, J.A., 2017. Financial statement analysis. World Scientific Book Chapters. pp.109-169.

Online

Airline industry., 2019. [Online]. Available through:< https://csimarket.com/Industry/industry_ManagementEffectiveness.php?

ind=1102>.

Purposeful and disciplined growth., 2018. [PDF]. Available through:<

http://www.annualreports.com/HostedData/AnnualReportArchive/e/LSE_EZJ_2017.pdf>.

8

Books and Journals

Altman, E.I. and et.al., 2017. Financial distress prediction in an international context: A review and empirical analysis of Altman's Z‐

score model. Journal of International Financial Management & Accounting. 28(2). pp.131-171.

Caserio, C., Panaro, D. and Trucco, S., 2016. Management Discussion and Analysis in the US Financial Companies: A Data Mining

Analysis. In Strengthening Information and Control Systems (pp. 43-57). Springer, Cham.

Edwards, A., Schwab, C. and Shevlin, T., 2015. Financial constraints and cash tax savings. The Accounting Review, 91(3), pp.859-

881.

Lecy, J.D. and Searing, E.A., 2015. Anatomy of the nonprofit starvation cycle: An analysis of falling overhead ratios in the nonprofit

sector. Nonprofit and Voluntary Sector Quarterly. 44(3). pp.539-563.

Parson, R. and et.al., 2015. Methods and apparatus for analysing and/or pre-processing financial accounting data. U.S. Patent

9,031,873.

Robinson, T.R. and et.al., 2015. International financial statement analysis. John Wiley & Sons.

Williams, E.E. and Dobelman, J.A., 2017. Financial statement analysis. World Scientific Book Chapters. pp.109-169.

Online

Airline industry., 2019. [Online]. Available through:< https://csimarket.com/Industry/industry_ManagementEffectiveness.php?

ind=1102>.

Purposeful and disciplined growth., 2018. [PDF]. Available through:<

http://www.annualreports.com/HostedData/AnnualReportArchive/e/LSE_EZJ_2017.pdf>.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The Airline industry in UK statistics and facts., 2019. [Online]. Available through:< https://www.statista.com/topics/3670/airline-

industry-uk/>.

The warmest welcome in the sky., 2019. [PDF]. Available through:<

http://www.annualreports.com/HostedData/AnnualReports/PDF/LSE_EZJ_2018.pdf.>.

UK economic outlook., 2019. [Online]. Available through:< https://www.pwc.co.uk/services/economics-policy/insights/uk-economic-

outlook.html>.

9

industry-uk/>.

The warmest welcome in the sky., 2019. [PDF]. Available through:<

http://www.annualreports.com/HostedData/AnnualReports/PDF/LSE_EZJ_2018.pdf.>.

UK economic outlook., 2019. [Online]. Available through:< https://www.pwc.co.uk/services/economics-policy/insights/uk-economic-

outlook.html>.

9

APPENDIX

Table 1Ratio analysis

(Values in million)

Formula 2016 2017 2018

% change

in 2017

% change

in 2018

Industry

average

Profitability

Operating profit 510 404 460 -21% 14%

Net sales 4669 5047 5898 8% 17%

Operating profit ratio Operating profit/Net sales*100 11% 8% 8% -27% -3% 15%

Gross profit 913 915 1224 0% 34%

Sales 4669 5047 5898 8% 17%

Gross profit ratio Gross profit/Net sales*100 20% 18% 21% -7% 14% 74.63%

Net profit 437 305 358 -30% 17%

Net sales 4669 5047 5898 8% 17%

Net profit ratio Net profit/net sales*100 9% 6% 6% -35% 0% 8.62%

Liquidity ratio

Current assets 1442 1734 2001 20% 15%

Current liability 1569 1670 2060 6% 23%

10

Table 1Ratio analysis

(Values in million)

Formula 2016 2017 2018

% change

in 2017

% change

in 2018

Industry

average

Profitability

Operating profit 510 404 460 -21% 14%

Net sales 4669 5047 5898 8% 17%

Operating profit ratio Operating profit/Net sales*100 11% 8% 8% -27% -3% 15%

Gross profit 913 915 1224 0% 34%

Sales 4669 5047 5898 8% 17%

Gross profit ratio Gross profit/Net sales*100 20% 18% 21% -7% 14% 74.63%

Net profit 437 305 358 -30% 17%

Net sales 4669 5047 5898 8% 17%

Net profit ratio Net profit/net sales*100 9% 6% 6% -35% 0% 8.62%

Liquidity ratio

Current assets 1442 1734 2001 20% 15%

Current liability 1569 1670 2060 6% 23%

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.