Financial Analysis of Man Group Plc: CAPM, WACC, Dividend Policy

VerifiedAdded on 2021/04/24

|20

|4851

|27

Report

AI Summary

This report presents a financial analysis of Man Group Plc, focusing on key financial aspects such as the Capital Asset Pricing Model (CAPM) for determining the required rate of return and the Weighted Average Cost of Capital (WACC). The analysis reveals the company's financial leverage and its impact on the cost of capital. The report also examines Man Group's dividend policy, including its profit-based approach and its hybrid dividend strategy, and discusses factors influencing dividend distribution decisions. Furthermore, the report explores various valuation models, with a particular emphasis on the dividend valuation model to assess the future share price of the company. The analysis incorporates financial data, including net income, dividend payments, and share price fluctuations, to provide a comprehensive overview of Man Group's financial performance and strategic decisions. The report also discusses the impact of inflation and growth rates on shareholder returns.

RUNNING HEAD: Financial analysis of Man Group Plc 0

Name of the student

Topic- Financial analysis of Man Group Plc

University Name

Name of the student

Topic- Financial analysis of Man Group Plc

University Name

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial analysis of Man Group Plc 1

Table of Contents

Answer to questions no-1................................................................................................................2

Capital assets pricing model........................................................................................................2

1 Answer to question no-2..........................................................................................................5

1.1 Dividend policy of the Man Group plc.............................................................................5

1.2 Valuation Models..............................................................................................................8

1.3 Dividend valuation model.................................................................................................8

2 Answer to question-3.............................................................................................................10

Fisher-Hirshleifer model............................................................................................................10

3 Conclusion.............................................................................................................................11

4 References..............................................................................................................................12

5 Appendix................................................................................................................................14

Income statement...........................................................................................................................16

5.1 Cash flow statement........................................................................................................17

Table of Contents

Answer to questions no-1................................................................................................................2

Capital assets pricing model........................................................................................................2

1 Answer to question no-2..........................................................................................................5

1.1 Dividend policy of the Man Group plc.............................................................................5

1.2 Valuation Models..............................................................................................................8

1.3 Dividend valuation model.................................................................................................8

2 Answer to question-3.............................................................................................................10

Fisher-Hirshleifer model............................................................................................................10

3 Conclusion.............................................................................................................................11

4 References..............................................................................................................................12

5 Appendix................................................................................................................................14

Income statement...........................................................................................................................16

5.1 Cash flow statement........................................................................................................17

Financial analysis of Man Group Plc 2

Answer to questions no-1

Capital assets pricing model

Capital assets pricing model is used to estimate the company's cost of equity, weighted

average cost of capital and its share price After analysing the annual report of company it is

revealed that the capital assets pricing model is the model used to determine the value of the

assets and required rate of return before investing in the particular project. This method assists

Man Group Plc Adr (Mngpy) to determine whether the earned profit should be plugged back into

the business or distributed to shareholders (Prasad, et al, (2015).

In order to compute the required rate of return through the CAPM, firstly beta of

company needs to be computed.

The computed beta of company is taken from the online sites.

The beta value of the company is 1.354 (Financial times, 2017).

After that by using the CAMP method, required rate of return of company will be

computed.

Computation of the required rate of return

CAPM= RF+ (Rm-RF)*B

An RF= Risk-free rate of return

RM= Market Risk

B= Beta of company

Computation of required rate of return

Calculation of Required rate of return

Answer to questions no-1

Capital assets pricing model

Capital assets pricing model is used to estimate the company's cost of equity, weighted

average cost of capital and its share price After analysing the annual report of company it is

revealed that the capital assets pricing model is the model used to determine the value of the

assets and required rate of return before investing in the particular project. This method assists

Man Group Plc Adr (Mngpy) to determine whether the earned profit should be plugged back into

the business or distributed to shareholders (Prasad, et al, (2015).

In order to compute the required rate of return through the CAPM, firstly beta of

company needs to be computed.

The computed beta of company is taken from the online sites.

The beta value of the company is 1.354 (Financial times, 2017).

After that by using the CAMP method, required rate of return of company will be

computed.

Computation of the required rate of return

CAPM= RF+ (Rm-RF)*B

An RF= Risk-free rate of return

RM= Market Risk

B= Beta of company

Computation of required rate of return

Calculation of Required rate of return

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial analysis of Man Group Plc 3

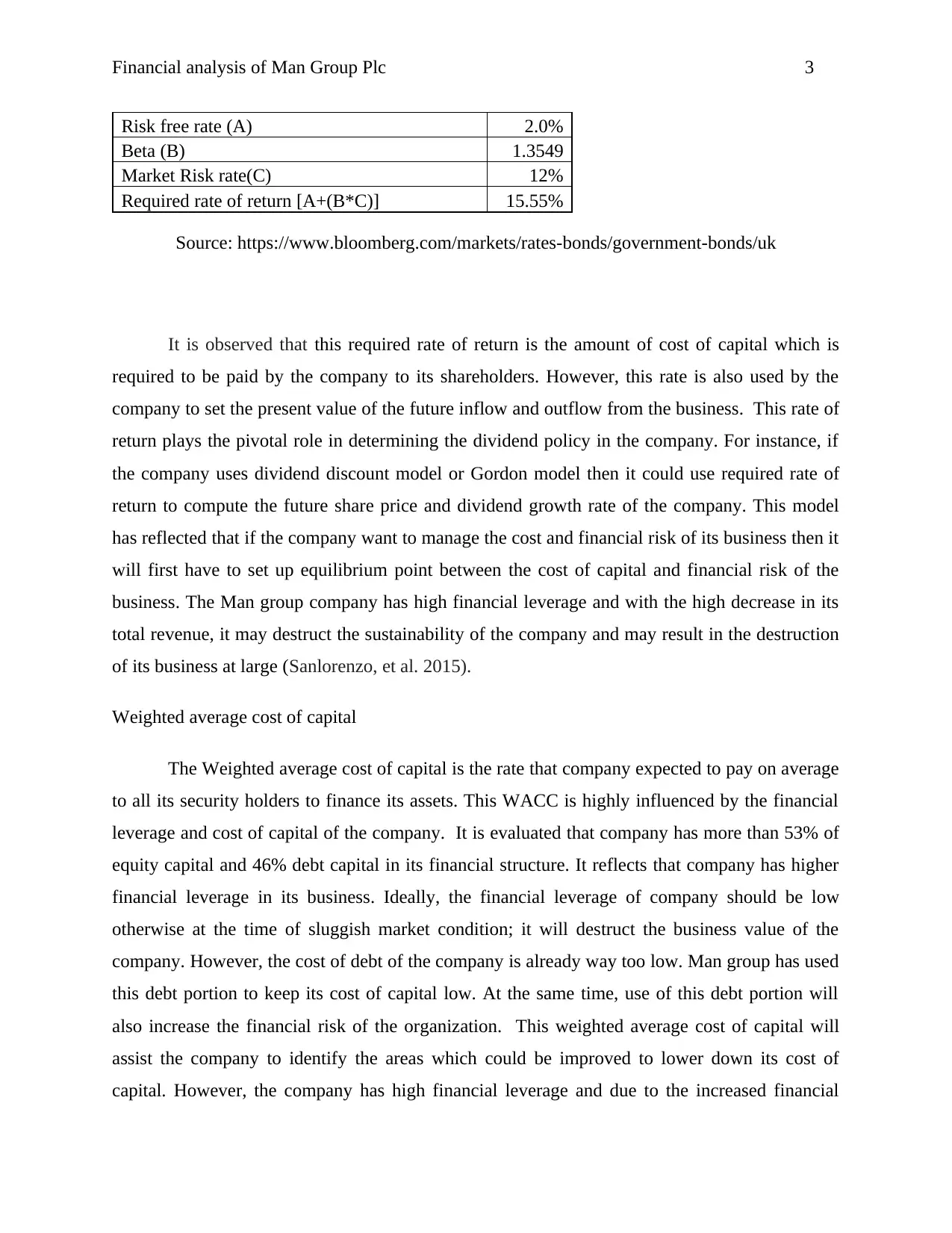

Risk free rate (A) 2.0%

Beta (B) 1.3549

Market Risk rate(C) 12%

Required rate of return [A+(B*C)] 15.55%

Source: https://www.bloomberg.com/markets/rates-bonds/government-bonds/uk

It is observed that this required rate of return is the amount of cost of capital which is

required to be paid by the company to its shareholders. However, this rate is also used by the

company to set the present value of the future inflow and outflow from the business. This rate of

return plays the pivotal role in determining the dividend policy in the company. For instance, if

the company uses dividend discount model or Gordon model then it could use required rate of

return to compute the future share price and dividend growth rate of the company. This model

has reflected that if the company want to manage the cost and financial risk of its business then it

will first have to set up equilibrium point between the cost of capital and financial risk of the

business. The Man group company has high financial leverage and with the high decrease in its

total revenue, it may destruct the sustainability of the company and may result in the destruction

of its business at large (Sanlorenzo, et al. 2015).

Weighted average cost of capital

The Weighted average cost of capital is the rate that company expected to pay on average

to all its security holders to finance its assets. This WACC is highly influenced by the financial

leverage and cost of capital of the company. It is evaluated that company has more than 53% of

equity capital and 46% debt capital in its financial structure. It reflects that company has higher

financial leverage in its business. Ideally, the financial leverage of company should be low

otherwise at the time of sluggish market condition; it will destruct the business value of the

company. However, the cost of debt of the company is already way too low. Man group has used

this debt portion to keep its cost of capital low. At the same time, use of this debt portion will

also increase the financial risk of the organization. This weighted average cost of capital will

assist the company to identify the areas which could be improved to lower down its cost of

capital. However, the company has high financial leverage and due to the increased financial

Risk free rate (A) 2.0%

Beta (B) 1.3549

Market Risk rate(C) 12%

Required rate of return [A+(B*C)] 15.55%

Source: https://www.bloomberg.com/markets/rates-bonds/government-bonds/uk

It is observed that this required rate of return is the amount of cost of capital which is

required to be paid by the company to its shareholders. However, this rate is also used by the

company to set the present value of the future inflow and outflow from the business. This rate of

return plays the pivotal role in determining the dividend policy in the company. For instance, if

the company uses dividend discount model or Gordon model then it could use required rate of

return to compute the future share price and dividend growth rate of the company. This model

has reflected that if the company want to manage the cost and financial risk of its business then it

will first have to set up equilibrium point between the cost of capital and financial risk of the

business. The Man group company has high financial leverage and with the high decrease in its

total revenue, it may destruct the sustainability of the company and may result in the destruction

of its business at large (Sanlorenzo, et al. 2015).

Weighted average cost of capital

The Weighted average cost of capital is the rate that company expected to pay on average

to all its security holders to finance its assets. This WACC is highly influenced by the financial

leverage and cost of capital of the company. It is evaluated that company has more than 53% of

equity capital and 46% debt capital in its financial structure. It reflects that company has higher

financial leverage in its business. Ideally, the financial leverage of company should be low

otherwise at the time of sluggish market condition; it will destruct the business value of the

company. However, the cost of debt of the company is already way too low. Man group has used

this debt portion to keep its cost of capital low. At the same time, use of this debt portion will

also increase the financial risk of the organization. This weighted average cost of capital will

assist the company to identify the areas which could be improved to lower down its cost of

capital. However, the company has high financial leverage and due to the increased financial

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial analysis of Man Group Plc 4

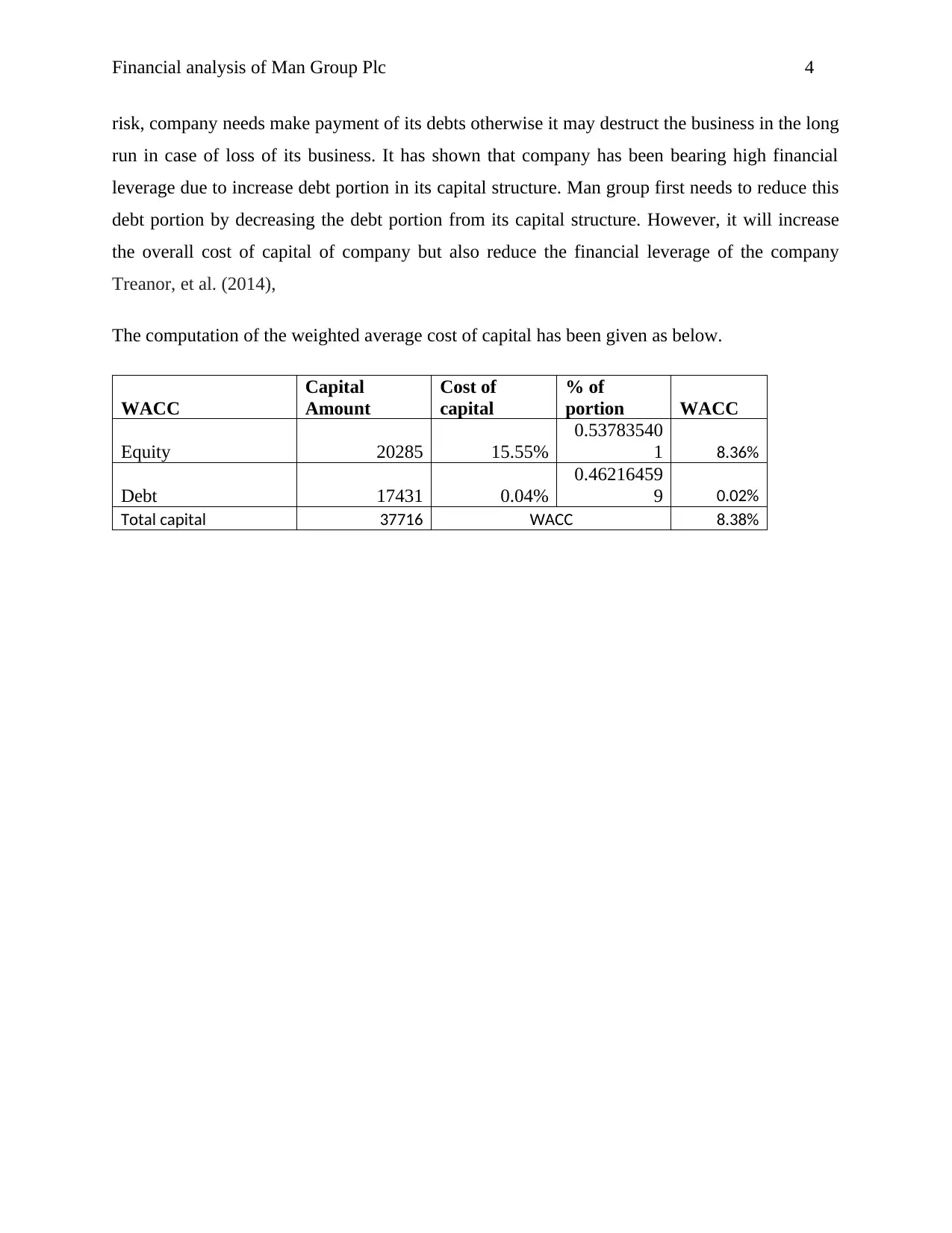

risk, company needs make payment of its debts otherwise it may destruct the business in the long

run in case of loss of its business. It has shown that company has been bearing high financial

leverage due to increase debt portion in its capital structure. Man group first needs to reduce this

debt portion by decreasing the debt portion from its capital structure. However, it will increase

the overall cost of capital of company but also reduce the financial leverage of the company

Treanor, et al. (2014),

The computation of the weighted average cost of capital has been given as below.

WACC

Capital

Amount

Cost of

capital

% of

portion WACC

Equity 20285 15.55%

0.53783540

1 8.36%

Debt 17431 0.04%

0.46216459

9 0.02%

Total capital 37716 WACC 8.38%

risk, company needs make payment of its debts otherwise it may destruct the business in the long

run in case of loss of its business. It has shown that company has been bearing high financial

leverage due to increase debt portion in its capital structure. Man group first needs to reduce this

debt portion by decreasing the debt portion from its capital structure. However, it will increase

the overall cost of capital of company but also reduce the financial leverage of the company

Treanor, et al. (2014),

The computation of the weighted average cost of capital has been given as below.

WACC

Capital

Amount

Cost of

capital

% of

portion WACC

Equity 20285 15.55%

0.53783540

1 8.36%

Debt 17431 0.04%

0.46216459

9 0.02%

Total capital 37716 WACC 8.38%

Financial analysis of Man Group Plc 5

1 Answer to question no-2

There are several factors which may affect the dividend policy and adoption of the same

by the listed companies. It is very difficult to lay down an optimum dividend policy which would

maximize the long-run wealth of the shareholders resulted in increment and decrement of the

firm's value. In this case, Man group Company has been taken which followed profit based

dividend policy to distribute the return of the company to its shareholders.

The dividend policy is an important component of the corporate financial management

policy. It could be defined as the amount of profit or return earned by company distributed to

shareholders on their shareholding proportioned basis. For a long-term, the subject of dividend

policy has captivated the interest of many investors and researchers (Zhu, 2014). It is evaluated

that the dividend policy of the company is highly based on the profit earning capacity and the

future growth of the company. There are several factors which have been affecting the dividend

distribution decision of company such as nature of the business, the profitability of the company,

future growth, market share price and return on capital employed by the company and the

inflation rate the Inflation rate of UK is 2.7%. It is observed that the growth rate of the company

is 3% which is higher than the inflation rate. Inflation is generally defined as increase price of

goods and services over certain period. It divulges that if shareholders invest their capital in JB

Hi-Fi Company then it will increase the value of their capital investment and save them from the

time value present factors risk. Company should have higher growth rate as compared to

inflation rate if it wants to offer high return on capital value to its shareholder. As per the point of

views of the general investors, dividend serves an important indicator of the strength and future

perspective of the business (Brigham and Ehrhardt, (2013), if company reduce its dividend

offered rate then it has been decreasing its earning capabilities and vice-versa. Ideally, the big

organization such as GE capital, Wesfarmers, JB Hi-Fi Company are following stable dividend

policy to maintain an effective brand image in the mind of investors irrespective of their earning

capacity. However, in case of loss of its business, it keeps its dividend payout zero. Nonetheless,

extensive level of literature reviews and research papers have been formulated on determining

the optimum level of dividend policy for an organization but nothing such qualitative

1 Answer to question no-2

There are several factors which may affect the dividend policy and adoption of the same

by the listed companies. It is very difficult to lay down an optimum dividend policy which would

maximize the long-run wealth of the shareholders resulted in increment and decrement of the

firm's value. In this case, Man group Company has been taken which followed profit based

dividend policy to distribute the return of the company to its shareholders.

The dividend policy is an important component of the corporate financial management

policy. It could be defined as the amount of profit or return earned by company distributed to

shareholders on their shareholding proportioned basis. For a long-term, the subject of dividend

policy has captivated the interest of many investors and researchers (Zhu, 2014). It is evaluated

that the dividend policy of the company is highly based on the profit earning capacity and the

future growth of the company. There are several factors which have been affecting the dividend

distribution decision of company such as nature of the business, the profitability of the company,

future growth, market share price and return on capital employed by the company and the

inflation rate the Inflation rate of UK is 2.7%. It is observed that the growth rate of the company

is 3% which is higher than the inflation rate. Inflation is generally defined as increase price of

goods and services over certain period. It divulges that if shareholders invest their capital in JB

Hi-Fi Company then it will increase the value of their capital investment and save them from the

time value present factors risk. Company should have higher growth rate as compared to

inflation rate if it wants to offer high return on capital value to its shareholder. As per the point of

views of the general investors, dividend serves an important indicator of the strength and future

perspective of the business (Brigham and Ehrhardt, (2013), if company reduce its dividend

offered rate then it has been decreasing its earning capabilities and vice-versa. Ideally, the big

organization such as GE capital, Wesfarmers, JB Hi-Fi Company are following stable dividend

policy to maintain an effective brand image in the mind of investors irrespective of their earning

capacity. However, in case of loss of its business, it keeps its dividend payout zero. Nonetheless,

extensive level of literature reviews and research papers have been formulated on determining

the optimum level of dividend policy for an organization but nothing such qualitative

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial analysis of Man Group Plc 6

information has been collected which could be used to evaluate the best dividend policy of

company (Man Group, 2017).

1.1 Dividend policy of the Man Group plc

There are several factors which may influence the dividend policy and dividend payout

decisions such as cost of the equity, debt interest rate, inflation rate of market, growth available

in business, shareholders return, capital employed by company and financial leverage of

company. The share price fluctuation is based on the earning and market situation of the

company. However, the share price of the company has increased by 20% since last five years

(Duchin, and Sosyura, (2014)

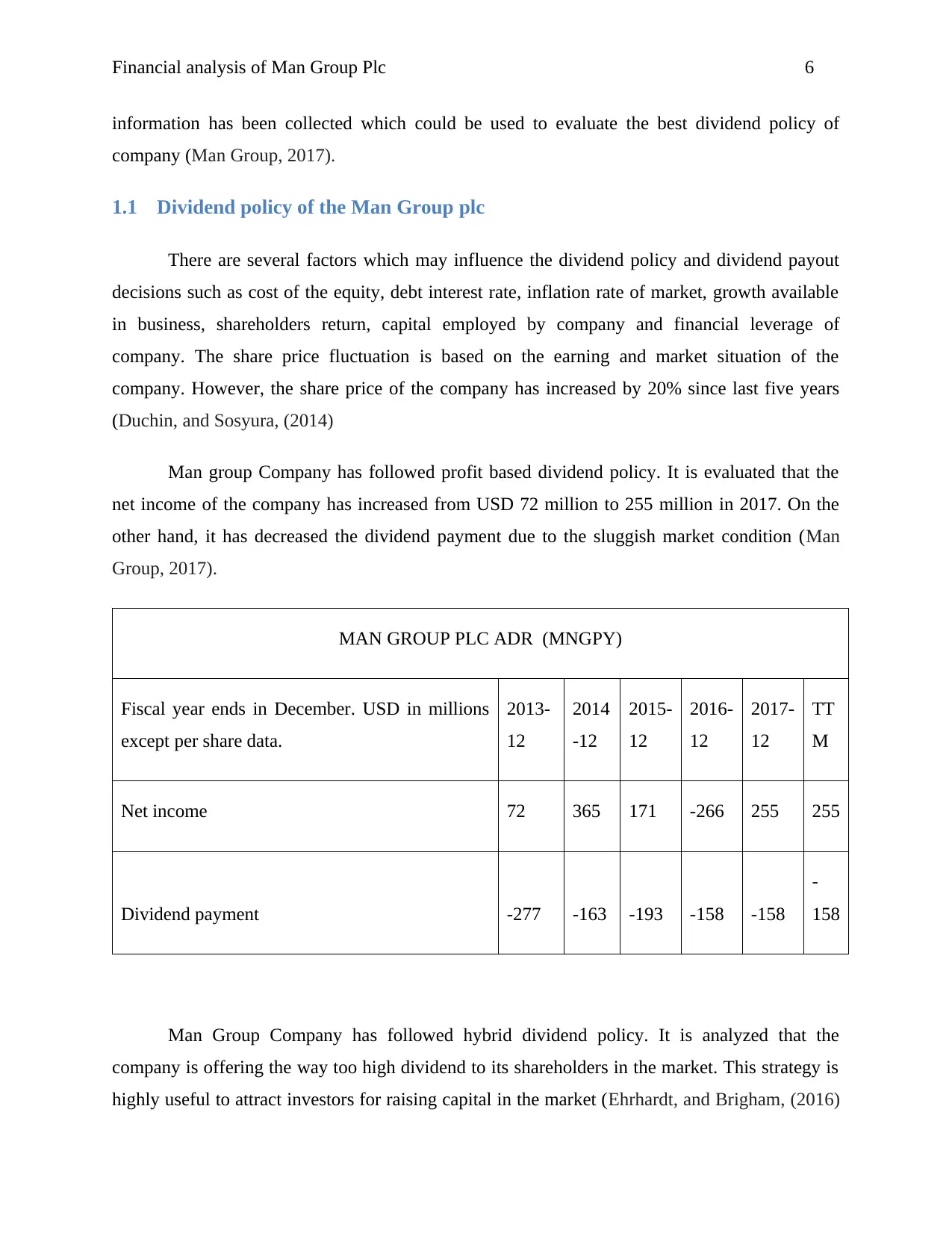

Man group Company has followed profit based dividend policy. It is evaluated that the

net income of the company has increased from USD 72 million to 255 million in 2017. On the

other hand, it has decreased the dividend payment due to the sluggish market condition (Man

Group, 2017).

MAN GROUP PLC ADR (MNGPY)

Fiscal year ends in December. USD in millions

except per share data.

2013-

12

2014

-12

2015-

12

2016-

12

2017-

12

TT

M

Net income 72 365 171 -266 255 255

Dividend payment -277 -163 -193 -158 -158

-

158

Man Group Company has followed hybrid dividend policy. It is analyzed that the

company is offering the way too high dividend to its shareholders in the market. This strategy is

highly useful to attract investors for raising capital in the market (Ehrhardt, and Brigham, (2016)

information has been collected which could be used to evaluate the best dividend policy of

company (Man Group, 2017).

1.1 Dividend policy of the Man Group plc

There are several factors which may influence the dividend policy and dividend payout

decisions such as cost of the equity, debt interest rate, inflation rate of market, growth available

in business, shareholders return, capital employed by company and financial leverage of

company. The share price fluctuation is based on the earning and market situation of the

company. However, the share price of the company has increased by 20% since last five years

(Duchin, and Sosyura, (2014)

Man group Company has followed profit based dividend policy. It is evaluated that the

net income of the company has increased from USD 72 million to 255 million in 2017. On the

other hand, it has decreased the dividend payment due to the sluggish market condition (Man

Group, 2017).

MAN GROUP PLC ADR (MNGPY)

Fiscal year ends in December. USD in millions

except per share data.

2013-

12

2014

-12

2015-

12

2016-

12

2017-

12

TT

M

Net income 72 365 171 -266 255 255

Dividend payment -277 -163 -193 -158 -158

-

158

Man Group Company has followed hybrid dividend policy. It is analyzed that the

company is offering the way too high dividend to its shareholders in the market. This strategy is

highly useful to attract investors for raising capital in the market (Ehrhardt, and Brigham, (2016)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial analysis of Man Group Plc 7

However, in 2016 and 2015 company followed dividend policy and kept its dividend payment

stable. It reflects that company has been following stable divided policy since last three year. On

the contrary to that, the company has been increasing its profit throughout the time.

There is below share price of Man group and LSE have been given.

Date Average return-Man Group Average Return LSE

Average

Return

01-03-2017 null

01-01-1900 215.9657

217.965

7

01-05-2017 234.2261 8.5%

240.226

1 10.2%

01-06-2017 227.9371 -2.7%

237.937

1 -1.0%

01-07-2017 242.2759 6.3%

245.275

9 3.1%

01-08-2017 247.5898 2.2%

255.261

7 4.1%

01-09-2017 238.2291 -3.8%

263.225

8 3.1%

01-10-2017 260.2789 9.3%

271.190

0 3.0%

01-11-2017 274.1159 5.3%

279.154

2 2.9%

01-12-2017 253.3654 -7.6%

245.275

9 -12.1%

01-01-2018 246.2391 -2.8%

255.261

7 4.1%

01-02-2018 244.6804 -0.6%

263.225

8 3.1%

01-03-2018 240.7291 -1.6%

245.275

9 -6.8%

23-03-2018 242.4800 0.7%

255.261

7 4.1%

The main important point is related to the fact that in spite of having lost in its business,

company consistently offered dividend to its shareholders. This reflects that company is more

inclined towards attracting the shareholders and keep them attracted toward its business (Garrett,

Hoitash, and Prawitt, (2014) It is analyzed that if the company is having high growth in its

business then it should instead of offering its dividend amount to its shareholders, put more

efforts to plug back its profit in its business. It will not only help the organization to provide

However, in 2016 and 2015 company followed dividend policy and kept its dividend payment

stable. It reflects that company has been following stable divided policy since last three year. On

the contrary to that, the company has been increasing its profit throughout the time.

There is below share price of Man group and LSE have been given.

Date Average return-Man Group Average Return LSE

Average

Return

01-03-2017 null

01-01-1900 215.9657

217.965

7

01-05-2017 234.2261 8.5%

240.226

1 10.2%

01-06-2017 227.9371 -2.7%

237.937

1 -1.0%

01-07-2017 242.2759 6.3%

245.275

9 3.1%

01-08-2017 247.5898 2.2%

255.261

7 4.1%

01-09-2017 238.2291 -3.8%

263.225

8 3.1%

01-10-2017 260.2789 9.3%

271.190

0 3.0%

01-11-2017 274.1159 5.3%

279.154

2 2.9%

01-12-2017 253.3654 -7.6%

245.275

9 -12.1%

01-01-2018 246.2391 -2.8%

255.261

7 4.1%

01-02-2018 244.6804 -0.6%

263.225

8 3.1%

01-03-2018 240.7291 -1.6%

245.275

9 -6.8%

23-03-2018 242.4800 0.7%

255.261

7 4.1%

The main important point is related to the fact that in spite of having lost in its business,

company consistently offered dividend to its shareholders. This reflects that company is more

inclined towards attracting the shareholders and keep them attracted toward its business (Garrett,

Hoitash, and Prawitt, (2014) It is analyzed that if the company is having high growth in its

business then it should instead of offering its dividend amount to its shareholders, put more

efforts to plug back its profit in its business. It will not only help the organization to provide

Financial analysis of Man Group Plc 8

capital for the business growth but also establish the proper linkage between organization

development and economic growth. After evaluating the annual report of Man group Company,

it is analyzed that company has been following hybrid dividend policy to distribute its dividend

to its shareholders. This policy reveals that company keeps its dividend payment stable in some

years and at the point of time it follows residual dividend policy. This strategy is highly

attractive towards investors. It is used by the company to maintain an effective brand image to

attract more investors. The cash flow statement of Man group Company has shown that company

has increased its dividend payout amount with the increase in its profitability. Nonetheless, in

several years, the company has increased its retained earning with a view to plug back its profit

for the future growth of the company. Company is having high profitability and will give offer

high dividend to its shareholders.

1.2 Valuation Models

There are several valuation models. However, these models could be used by company to

value the shares of Man Group Plc. There are several valuation models such as dividend

valuation model, free cash flow to equity model, price earnings ratio model and value ratio

model. This valuation model reflects that company has issued good amount of dividend to its

shareholders. However, there are several valuation modes which could be used by the company

to assess the value of its company. Nonetheless, the dividend valuation model is the most

suitable method to analyse the future value of the company.

1.3 Dividend valuation model

The market share, profit, dividend, share price index, and current inflation rate have been

used to determine the future share price of the company by using dividend growth model. This

model is used to identify the true value of the company based on the stock price and sum of all

the future dividend payments. This model is used to evaluate the net present value of the future

dividend available to shareholders (Kundakchyan, and Zulfakarova, 2014).

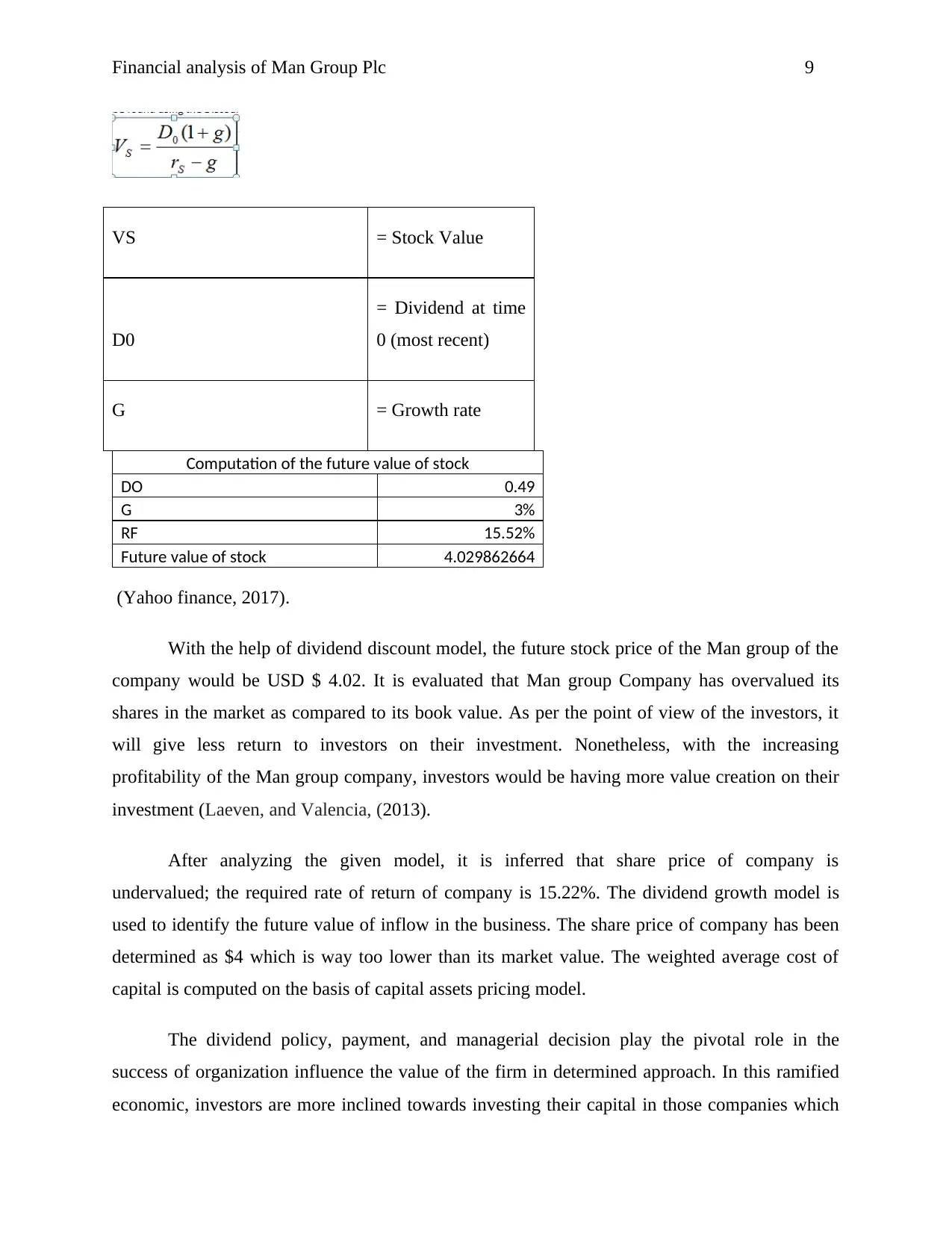

Future value of stock =

capital for the business growth but also establish the proper linkage between organization

development and economic growth. After evaluating the annual report of Man group Company,

it is analyzed that company has been following hybrid dividend policy to distribute its dividend

to its shareholders. This policy reveals that company keeps its dividend payment stable in some

years and at the point of time it follows residual dividend policy. This strategy is highly

attractive towards investors. It is used by the company to maintain an effective brand image to

attract more investors. The cash flow statement of Man group Company has shown that company

has increased its dividend payout amount with the increase in its profitability. Nonetheless, in

several years, the company has increased its retained earning with a view to plug back its profit

for the future growth of the company. Company is having high profitability and will give offer

high dividend to its shareholders.

1.2 Valuation Models

There are several valuation models. However, these models could be used by company to

value the shares of Man Group Plc. There are several valuation models such as dividend

valuation model, free cash flow to equity model, price earnings ratio model and value ratio

model. This valuation model reflects that company has issued good amount of dividend to its

shareholders. However, there are several valuation modes which could be used by the company

to assess the value of its company. Nonetheless, the dividend valuation model is the most

suitable method to analyse the future value of the company.

1.3 Dividend valuation model

The market share, profit, dividend, share price index, and current inflation rate have been

used to determine the future share price of the company by using dividend growth model. This

model is used to identify the true value of the company based on the stock price and sum of all

the future dividend payments. This model is used to evaluate the net present value of the future

dividend available to shareholders (Kundakchyan, and Zulfakarova, 2014).

Future value of stock =

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial analysis of Man Group Plc 9

VS = Stock Value

D0

= Dividend at time

0 (most recent)

G = Growth rate

Computation of the future value of stock

DO 0.49

G 3%

RF 15.52%

Future value of stock 4.029862664

(Yahoo finance, 2017).

With the help of dividend discount model, the future stock price of the Man group of the

company would be USD $ 4.02. It is evaluated that Man group Company has overvalued its

shares in the market as compared to its book value. As per the point of view of the investors, it

will give less return to investors on their investment. Nonetheless, with the increasing

profitability of the Man group company, investors would be having more value creation on their

investment (Laeven, and Valencia, (2013).

After analyzing the given model, it is inferred that share price of company is

undervalued; the required rate of return of company is 15.22%. The dividend growth model is

used to identify the future value of inflow in the business. The share price of company has been

determined as $4 which is way too lower than its market value. The weighted average cost of

capital is computed on the basis of capital assets pricing model.

The dividend policy, payment, and managerial decision play the pivotal role in the

success of organization influence the value of the firm in determined approach. In this ramified

economic, investors are more inclined towards investing their capital in those companies which

VS = Stock Value

D0

= Dividend at time

0 (most recent)

G = Growth rate

Computation of the future value of stock

DO 0.49

G 3%

RF 15.52%

Future value of stock 4.029862664

(Yahoo finance, 2017).

With the help of dividend discount model, the future stock price of the Man group of the

company would be USD $ 4.02. It is evaluated that Man group Company has overvalued its

shares in the market as compared to its book value. As per the point of view of the investors, it

will give less return to investors on their investment. Nonetheless, with the increasing

profitability of the Man group company, investors would be having more value creation on their

investment (Laeven, and Valencia, (2013).

After analyzing the given model, it is inferred that share price of company is

undervalued; the required rate of return of company is 15.22%. The dividend growth model is

used to identify the future value of inflow in the business. The share price of company has been

determined as $4 which is way too lower than its market value. The weighted average cost of

capital is computed on the basis of capital assets pricing model.

The dividend policy, payment, and managerial decision play the pivotal role in the

success of organization influence the value of the firm in determined approach. In this ramified

economic, investors are more inclined towards investing their capital in those companies which

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial analysis of Man Group Plc 10

are offering the high dividend to shareholders. However, long-term shareholders are more

inclined towards the long-term value creation of the company.

In simple words, dividend policy could be described as the set of guidelines which

company uses to decide how much of its earning and amount of profit it will pay out to its

shareholders. However, some of the researchers are of the view that investors are not concerned

with the dividend policy of company since they could sell a portion of their portfolio of equities

if they want to earn money.

The Man Group Plc Adr (Mngpy) has been paying the dividend since last five years.

However, there is no such detail which could be used to determine as the basis on which this

dividend payment was done. However, Capital assets pricing model could be used to analyze the

dividend policy and true value firm in the market.

2 Answer to question-3

Fisher-Hirshleifer model

Fisher-Hirshleifer model has been used to examine the firm's investment decision and role

of the capital market The Fisher-Hirshleifer model, stipulates that the goal of any firm is to

increase the future value of the company and increase the overall return on capital employed.

This Fisher-Hirshleifer model could be broken down into three key assentation such as firm’s

investment decisions are separate from the preference of firm’s owners. As per the Fisher-

Hirshleifer model, it is considered that consumption and investment decisions of an individual

are examined in the presence of frictionless of the capital market Vogel, (2014) in the simple

words, Fisher-Hirshleifer model revealed that total investment of the investors should be

equivalent to his saving. However, the interest rate should be more than saving interest rate when

investors want to invest his funds in the market. The Fisher-Hirshleifer model provides the

conceptual frameworks for the Net present value model. As per this model, the only way to

increase the value of its investment is to invest in the market so that it could compensate the time

value of money. In context with the dividend case, it is inferred that investors would be inclined

towards investing money only in those firms which offer the good amount of return to its

are offering the high dividend to shareholders. However, long-term shareholders are more

inclined towards the long-term value creation of the company.

In simple words, dividend policy could be described as the set of guidelines which

company uses to decide how much of its earning and amount of profit it will pay out to its

shareholders. However, some of the researchers are of the view that investors are not concerned

with the dividend policy of company since they could sell a portion of their portfolio of equities

if they want to earn money.

The Man Group Plc Adr (Mngpy) has been paying the dividend since last five years.

However, there is no such detail which could be used to determine as the basis on which this

dividend payment was done. However, Capital assets pricing model could be used to analyze the

dividend policy and true value firm in the market.

2 Answer to question-3

Fisher-Hirshleifer model

Fisher-Hirshleifer model has been used to examine the firm's investment decision and role

of the capital market The Fisher-Hirshleifer model, stipulates that the goal of any firm is to

increase the future value of the company and increase the overall return on capital employed.

This Fisher-Hirshleifer model could be broken down into three key assentation such as firm’s

investment decisions are separate from the preference of firm’s owners. As per the Fisher-

Hirshleifer model, it is considered that consumption and investment decisions of an individual

are examined in the presence of frictionless of the capital market Vogel, (2014) in the simple

words, Fisher-Hirshleifer model revealed that total investment of the investors should be

equivalent to his saving. However, the interest rate should be more than saving interest rate when

investors want to invest his funds in the market. The Fisher-Hirshleifer model provides the

conceptual frameworks for the Net present value model. As per this model, the only way to

increase the value of its investment is to invest in the market so that it could compensate the time

value of money. In context with the dividend case, it is inferred that investors would be inclined

towards investing money only in those firms which offer the good amount of return to its

Financial analysis of Man Group Plc 11

investors. On the other part, if the company is having the good option to create value on its

investment then instead of distributing the dividend to shareholders, it would plug back its funds

in its business. The Fisher-Hirshleifer model clarifies all the possibilities and issues of the capital

market. It also helps investors to assume that the capital market is offering the good amount of

return and less fluctuated.

The investment decision of Man's Group is aggressive. It has been plugging back most of its

funds in its business to expand the business chains in the market. Nonetheless, the role of capital

market in the investment decision is very pivotal. The capital market is highly unstable and as

per the Fisher-Hirshleifer model if investment made in the capital market in the particular time

period then the yield output would be received only in the next period (Weygandt, Kimmel, and

Kieso, 2015). The investment decisions of the Man’s group is highly based on the present value,

discounting factors and return available in the capital market. It has invested most of its capital

market with a view to increasing the overall return on this investment. However, hedging process

has also been used as per the Fisher-Hirshleifer model with a view to mitigating the market

transactional risk factors. Fisher only focuses on the consumption of the value and investment. If

the company keeps its capital idol in it a business then it will destruct the value of the

investment. Nonetheless, the capital market offers the good amount of return. The company

needs to opt best option to save its capital from the capital market loss and risk arise from the

inflation rate.

After evaluating all the details and theory given by the Fisher-Hirshleifer model, it is clear that

Man group needs to keep its capital investment decision active. It needs to assess all the

available profits and competitor’s offering in the market.

3 Conclusion

The dividend policy of company should be based on the profit, inflation rate, interest rate and

external factors of the business. The Man group company has followed hybrid dividend policy to

offer the dividend to its shareholders. This dividend policy is used to attract the investors. The

Man group has used this dividend policy to attract more investors in the market. Now, in the end,

it could be inferred that Man group plc should lower down its dividend payment otherwise it

would have to face the high amount of loss in its business. The company should plug back its

investors. On the other part, if the company is having the good option to create value on its

investment then instead of distributing the dividend to shareholders, it would plug back its funds

in its business. The Fisher-Hirshleifer model clarifies all the possibilities and issues of the capital

market. It also helps investors to assume that the capital market is offering the good amount of

return and less fluctuated.

The investment decision of Man's Group is aggressive. It has been plugging back most of its

funds in its business to expand the business chains in the market. Nonetheless, the role of capital

market in the investment decision is very pivotal. The capital market is highly unstable and as

per the Fisher-Hirshleifer model if investment made in the capital market in the particular time

period then the yield output would be received only in the next period (Weygandt, Kimmel, and

Kieso, 2015). The investment decisions of the Man’s group is highly based on the present value,

discounting factors and return available in the capital market. It has invested most of its capital

market with a view to increasing the overall return on this investment. However, hedging process

has also been used as per the Fisher-Hirshleifer model with a view to mitigating the market

transactional risk factors. Fisher only focuses on the consumption of the value and investment. If

the company keeps its capital idol in it a business then it will destruct the value of the

investment. Nonetheless, the capital market offers the good amount of return. The company

needs to opt best option to save its capital from the capital market loss and risk arise from the

inflation rate.

After evaluating all the details and theory given by the Fisher-Hirshleifer model, it is clear that

Man group needs to keep its capital investment decision active. It needs to assess all the

available profits and competitor’s offering in the market.

3 Conclusion

The dividend policy of company should be based on the profit, inflation rate, interest rate and

external factors of the business. The Man group company has followed hybrid dividend policy to

offer the dividend to its shareholders. This dividend policy is used to attract the investors. The

Man group has used this dividend policy to attract more investors in the market. Now, in the end,

it could be inferred that Man group plc should lower down its dividend payment otherwise it

would have to face the high amount of loss in its business. The company should plug back its

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.