Financial Analysis Report: Reliance Worldwide Corporation Limited

VerifiedAdded on 2021/05/31

|25

|4658

|95

Report

AI Summary

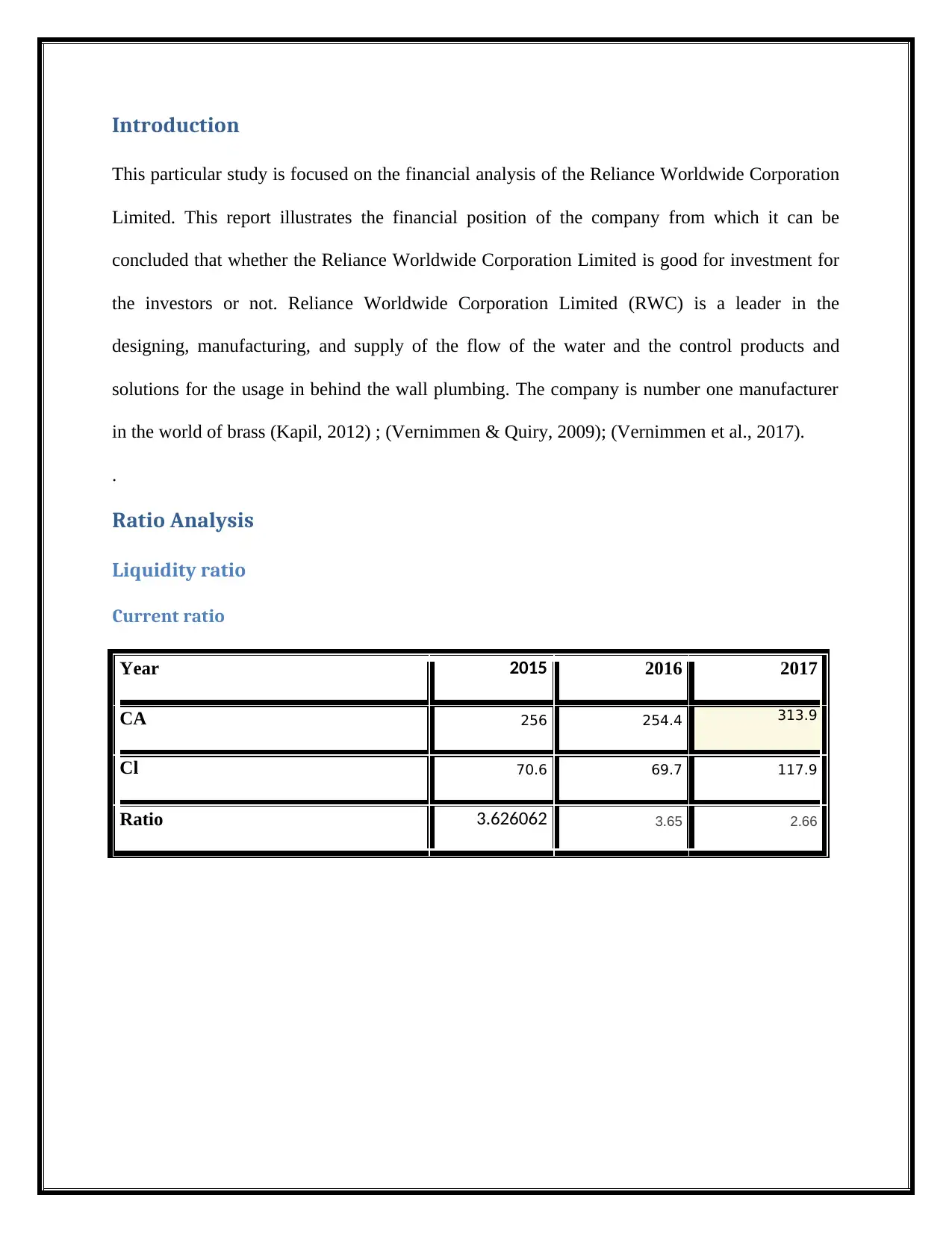

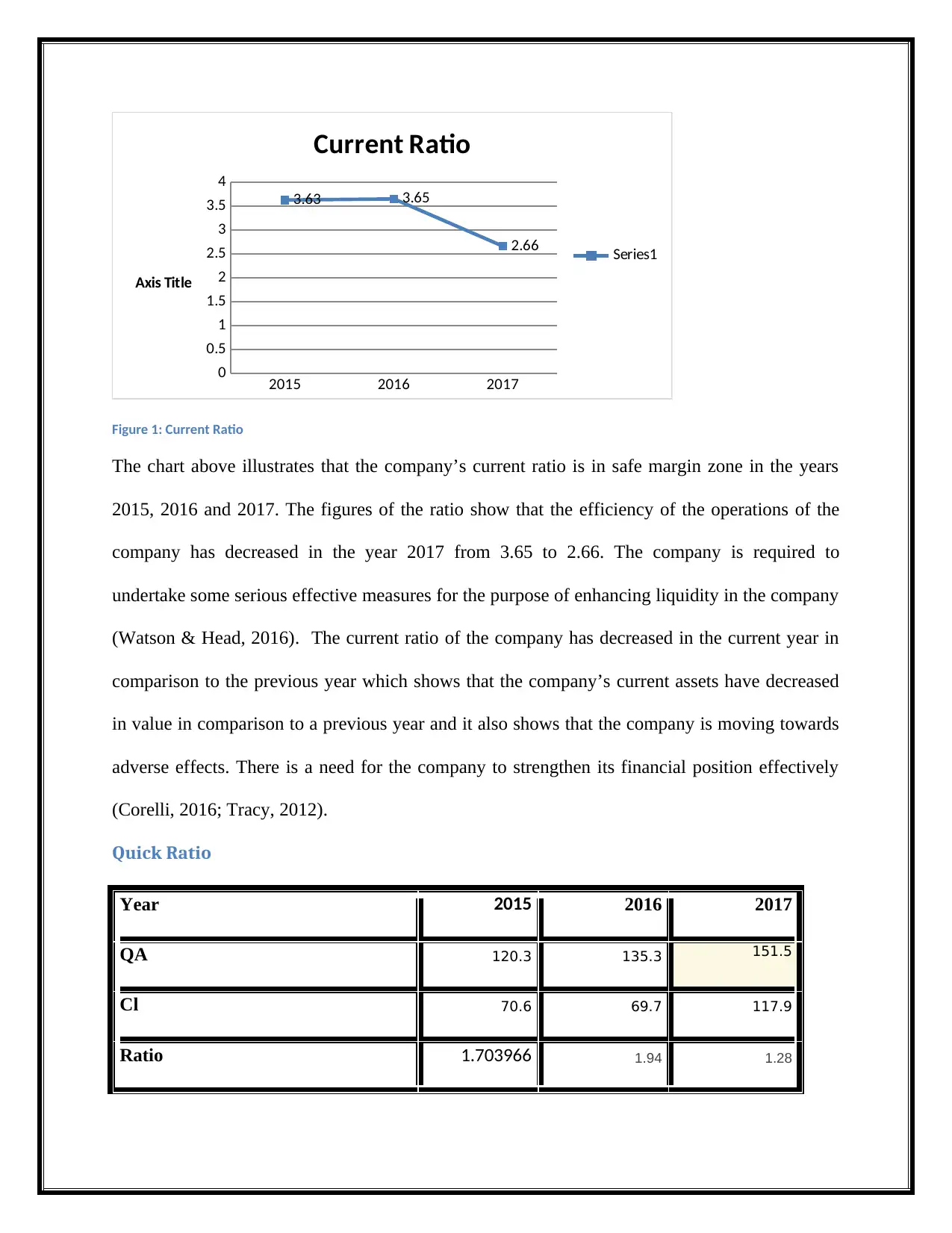

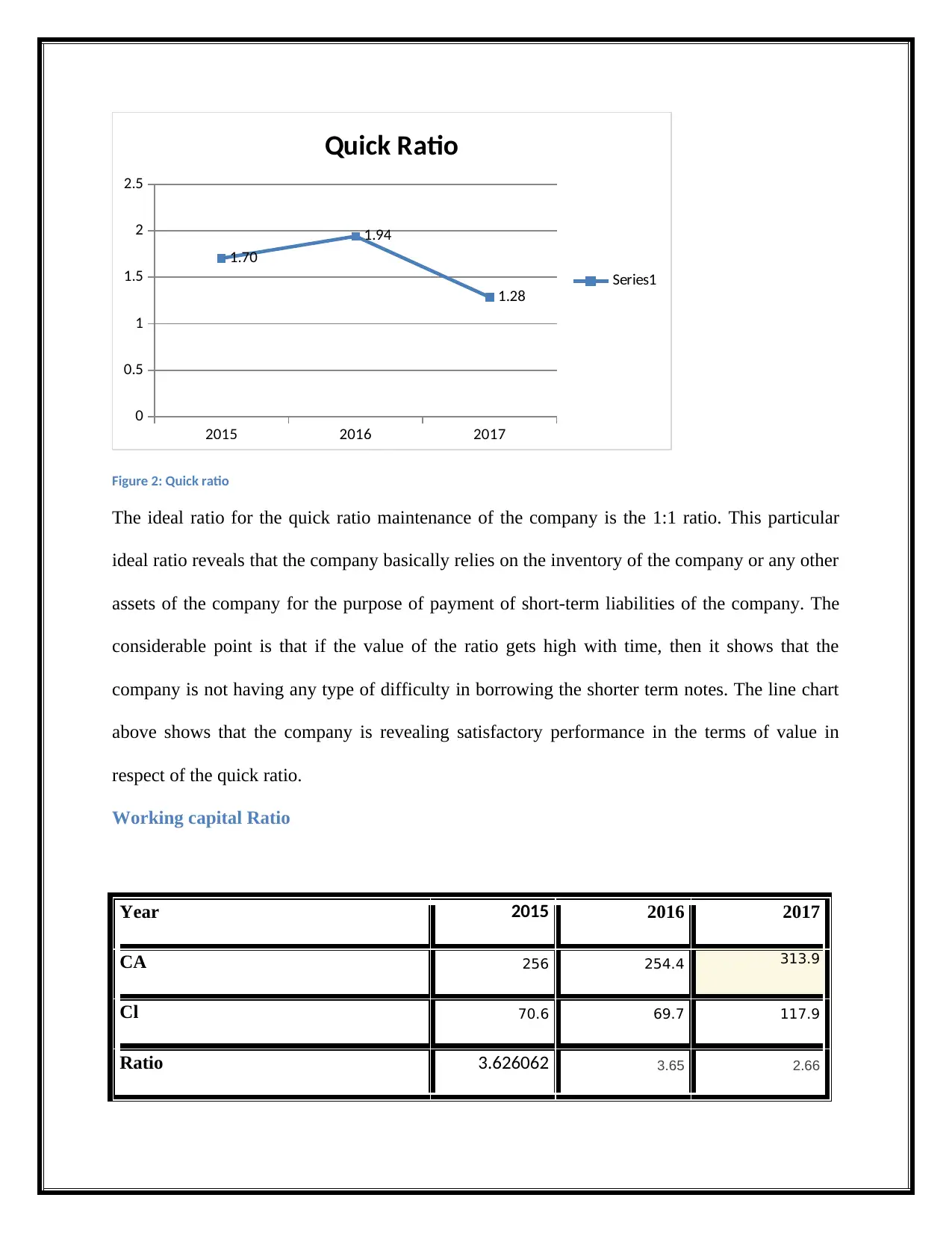

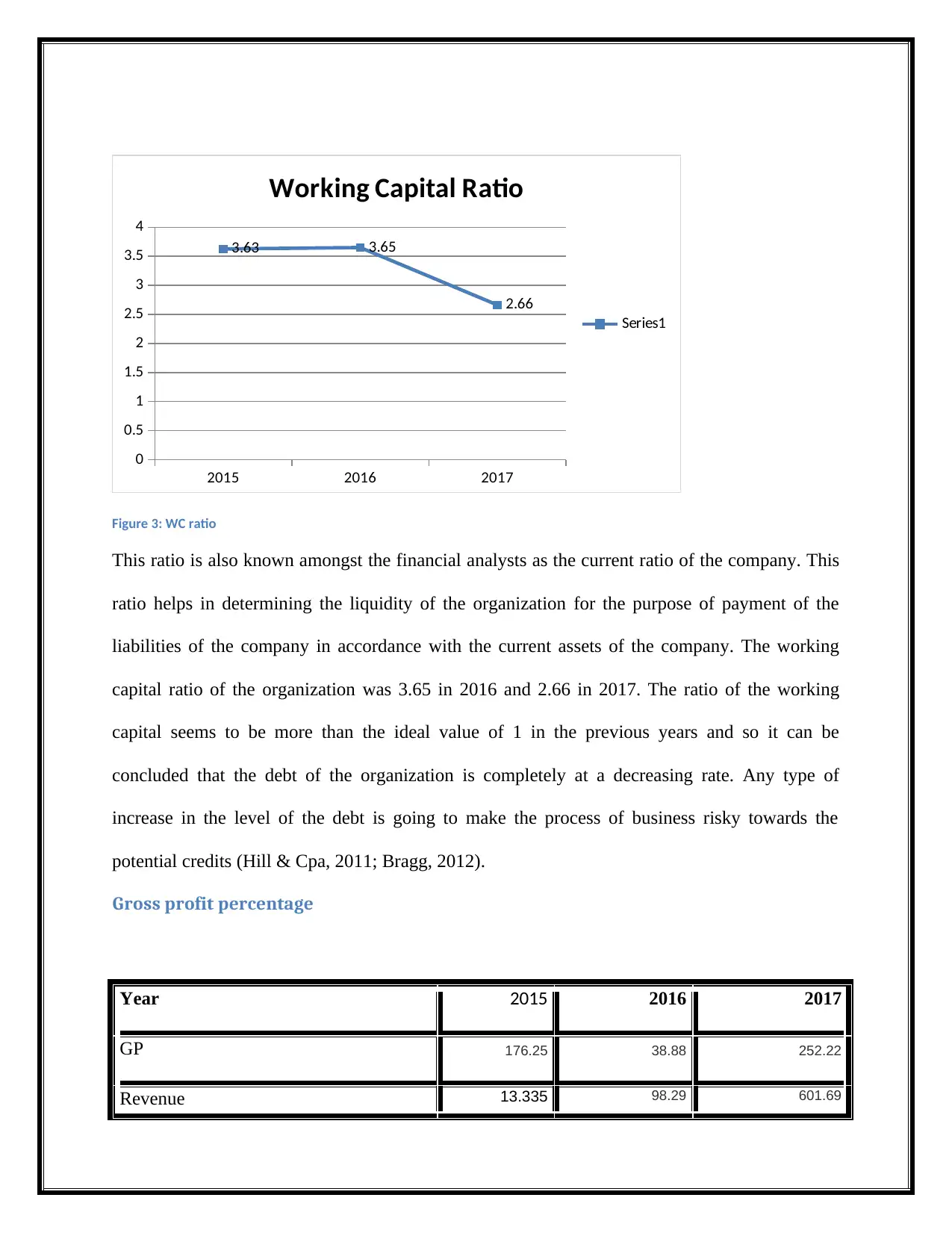

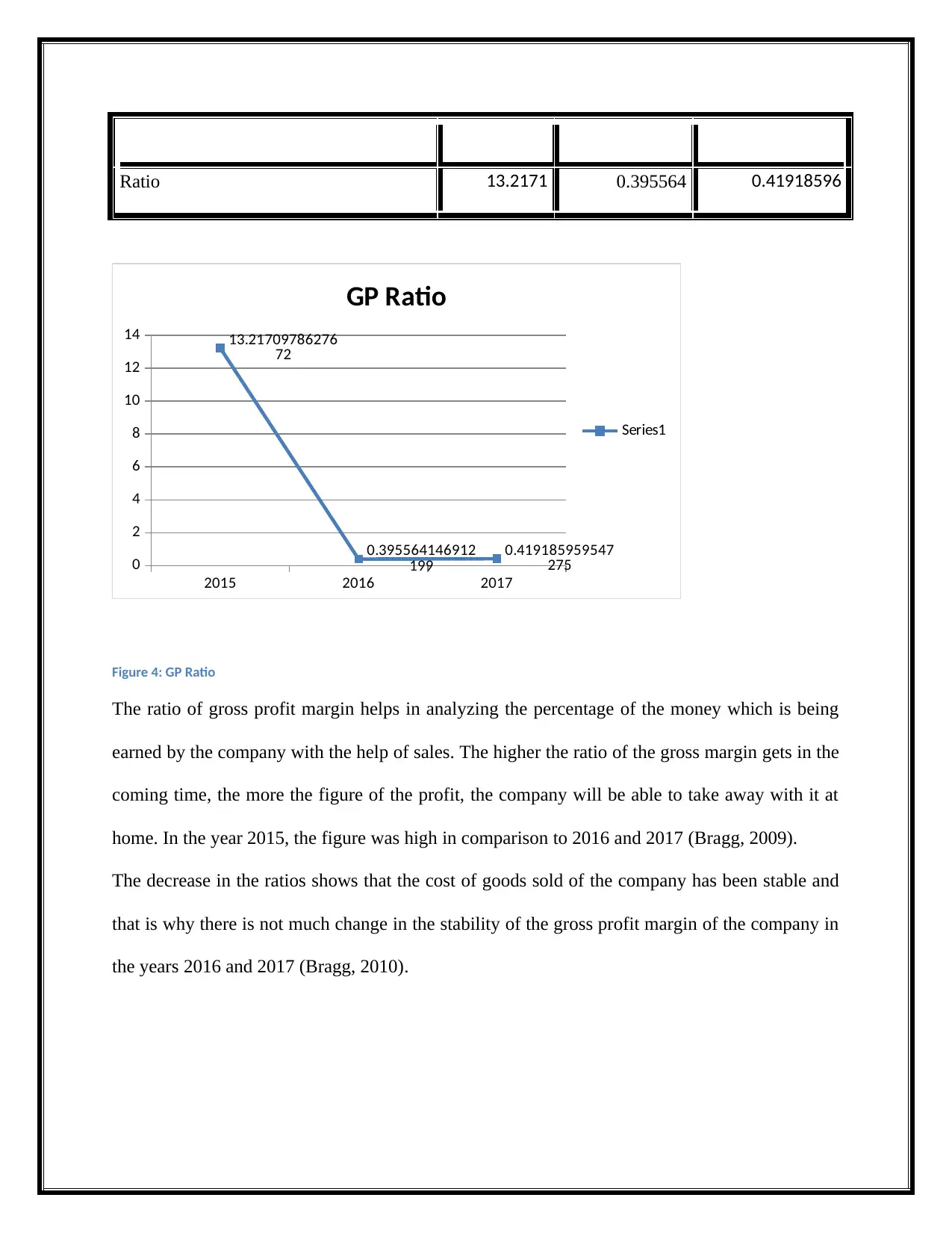

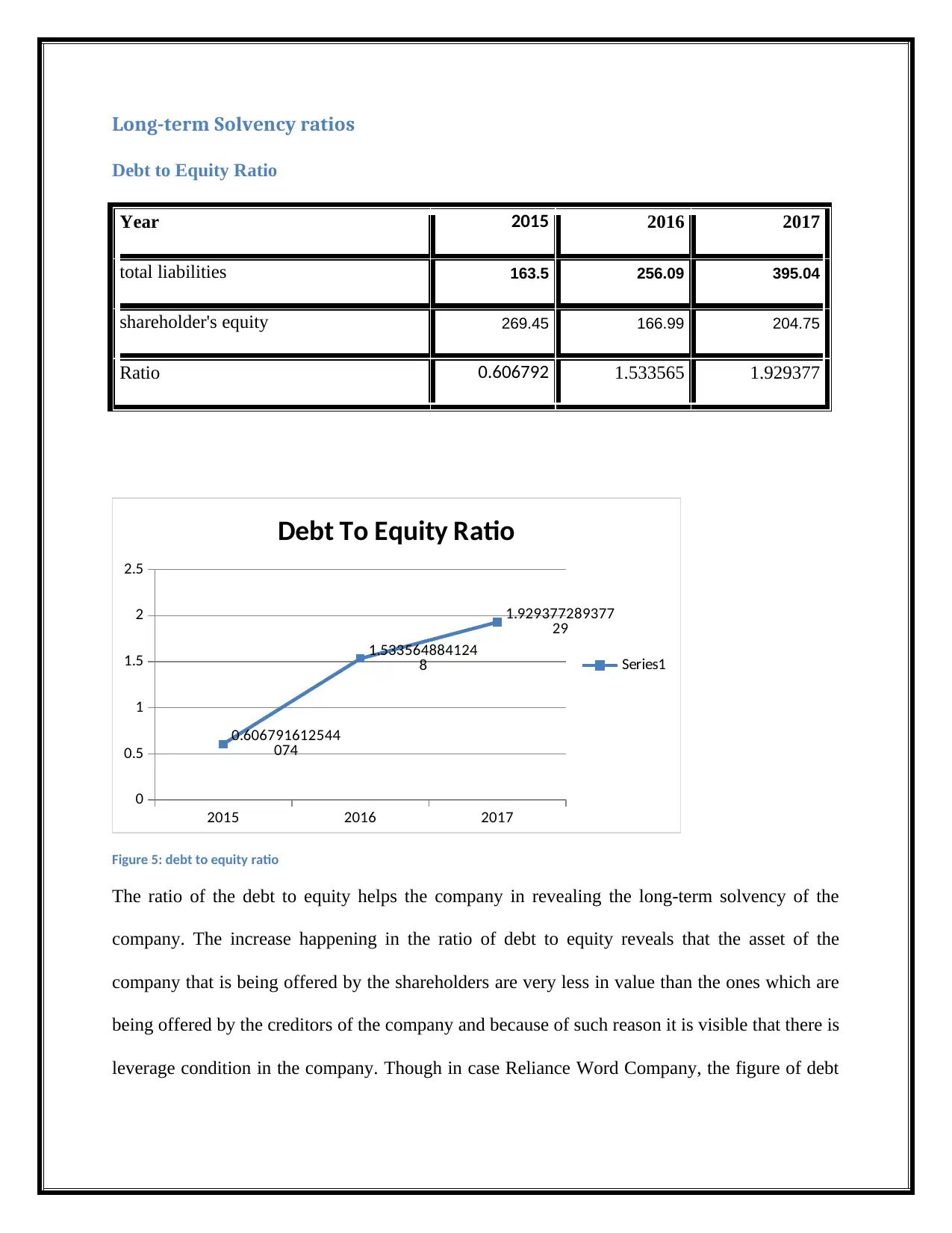

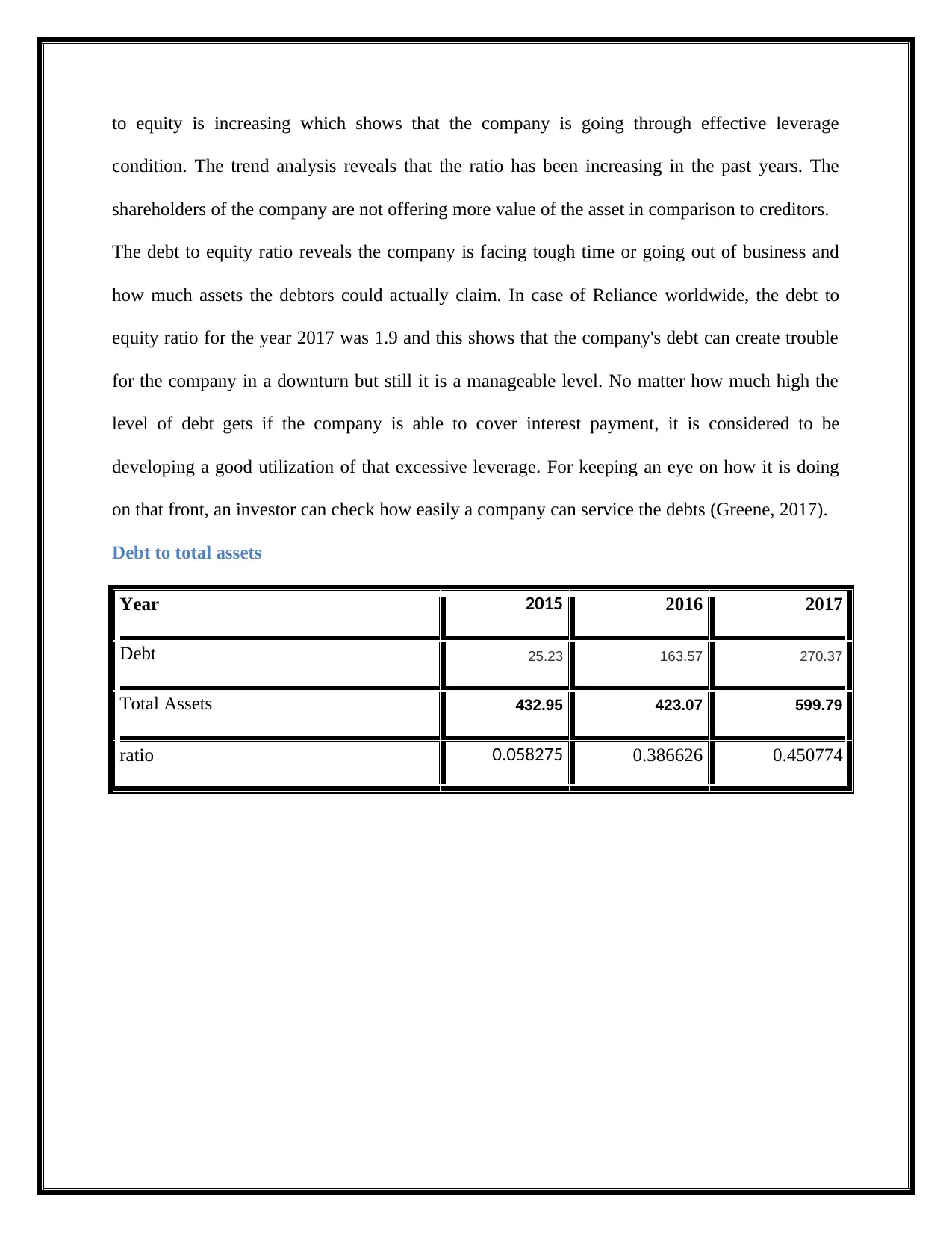

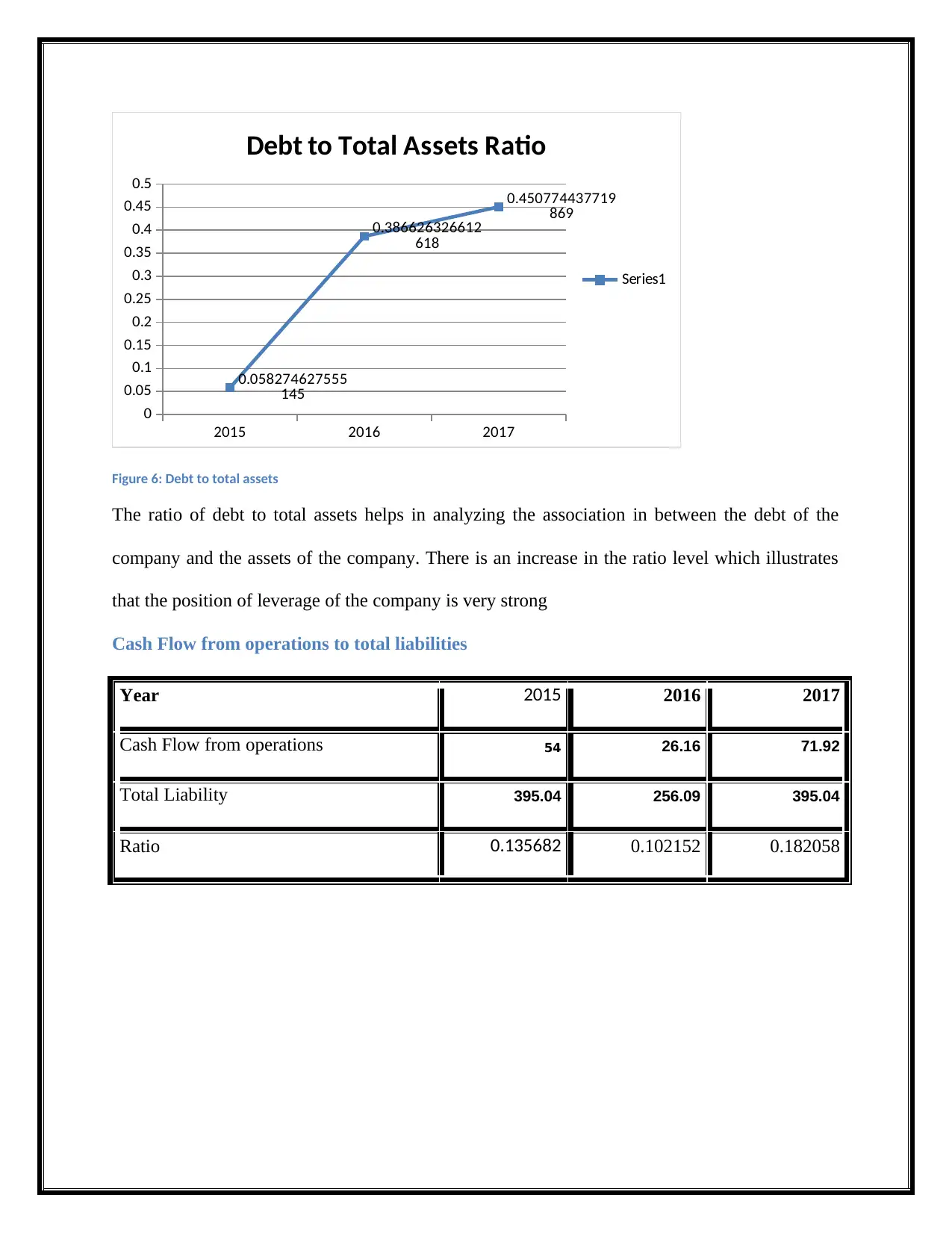

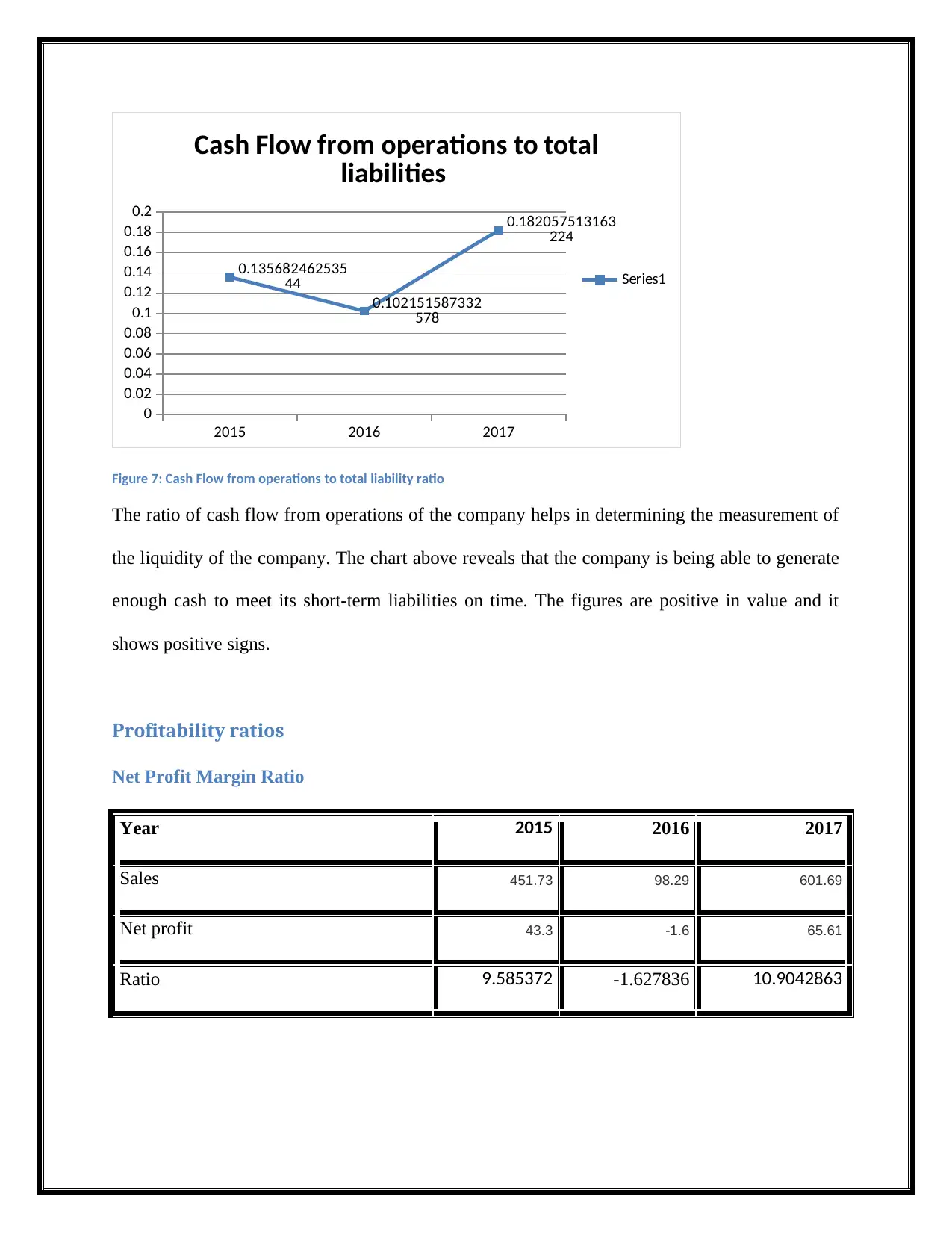

This report offers a detailed financial analysis of Reliance Worldwide Corporation Limited (RWC), evaluating its performance from 2015 to 2017. The analysis encompasses a range of financial ratios, including liquidity (current, quick, and working capital ratios), long-term solvency (debt-to-equity, debt-to-total assets), profitability (net profit margin, total asset turnover, return on assets, and return on equity), and cash flow ratios. The report examines trends in these ratios to assess RWC's financial health, highlighting areas of strength and weakness. Key findings include observations on liquidity, solvency, and profitability trends, and the report also discusses the risks faced by the company. The analysis provides insights into RWC's financial position and potential investment considerations, making it a valuable resource for understanding the company's financial performance.

1 out of 25

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.