Detailed Financial Report Analysis of Telstra Corporation (2015-2017)

VerifiedAdded on 2024/05/30

|12

|2690

|471

Report

AI Summary

This report provides a detailed financial analysis of Telstra Corporation from 2015 to 2017, focusing on the cash flow statement, other comprehensive income (OCI), and corporate income tax. The cash flow analysis examines operating, investing, and financing activities, revealing a significant decrease in net cash from 2016 to 2017 due to increased investments and dividend payments. The OCI analysis identifies foreign currency reserves, cash flow hedges, and retained profits as major components, highlighting revenues and expenses not fully realized. The corporate income tax calculation compares the stated income tax with the calculated tax based on a 30% rate, explaining the difference through various factors like different tax rates and non-deductible items. The report concludes with insights into Telstra's tax practices and asset management.

Table of Contents

Executive Summary.....................................................................................................................................2

Analysis of Cash flow statement.................................................................................................................2

Comparison of Other comprehensive income of the company....................................................................6

Calculation of the Corporate income tax.....................................................................................................7

References.................................................................................................................................................10

Executive Summary.....................................................................................................................................2

Analysis of Cash flow statement.................................................................................................................2

Comparison of Other comprehensive income of the company....................................................................6

Calculation of the Corporate income tax.....................................................................................................7

References.................................................................................................................................................10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Executive Summary

The assignment is focused to analyse the various aspects of the fiancial reports which is available

to the public, the students need to understand the annual report of the company for 3 years

between 2015, 2016 and 2017 and present it in detail on three key areas: Cash flow statements,

Other comprehensive income and Income tax. The company which is considered for the analysis

is Telestra Coporation, the company is the major Australian Telecommunication company

involved in offering services like voice, internet, entertainment services, pay TVs etc. The

company was incepted in early 1970 and is in the business for more than 40 years. The company

holds more than 40% market share in the country, this is mainly due to the organic growth and

development. The management is always focused to offer products on fixed line network, mobile

calls, internet data packs and other related services, the business posted a total revenue of more

than $25 billion in 2017 and the net income exceeded $3 billion for the same year.

Analysis of Cash flow statement

The cash flow statement is considered as the statement which intends to show the overall

changes in the income statement and the balance sheet. The focus is mainly on the changes in the

cash and the cash equivalents in all these areas. The cash flow statement is classified into

categories like cash flows which is realised through the operating activities, cash expenditure by

the business due to investment purposes, cash inflows to the business mainly due to the financing

activities and the net cash & cash equivalents for the years. (Telestra, 2017)

The main purpose of the cash flow statement is to offer more data and information on the overall

receipts and the payments for a given period of time, usually a year. This statement will help the

business in understanding the overall liquidity of the company, estimate its solvency from time

The assignment is focused to analyse the various aspects of the fiancial reports which is available

to the public, the students need to understand the annual report of the company for 3 years

between 2015, 2016 and 2017 and present it in detail on three key areas: Cash flow statements,

Other comprehensive income and Income tax. The company which is considered for the analysis

is Telestra Coporation, the company is the major Australian Telecommunication company

involved in offering services like voice, internet, entertainment services, pay TVs etc. The

company was incepted in early 1970 and is in the business for more than 40 years. The company

holds more than 40% market share in the country, this is mainly due to the organic growth and

development. The management is always focused to offer products on fixed line network, mobile

calls, internet data packs and other related services, the business posted a total revenue of more

than $25 billion in 2017 and the net income exceeded $3 billion for the same year.

Analysis of Cash flow statement

The cash flow statement is considered as the statement which intends to show the overall

changes in the income statement and the balance sheet. The focus is mainly on the changes in the

cash and the cash equivalents in all these areas. The cash flow statement is classified into

categories like cash flows which is realised through the operating activities, cash expenditure by

the business due to investment purposes, cash inflows to the business mainly due to the financing

activities and the net cash & cash equivalents for the years. (Telestra, 2017)

The main purpose of the cash flow statement is to offer more data and information on the overall

receipts and the payments for a given period of time, usually a year. This statement will help the

business in understanding the overall liquidity of the company, estimate its solvency from time

to time and forecast the future expected cash outflows and ways to source the funds. The key

aspects of the cash flow statement are mainly based on the accrual basis of the accouting

procedures which needs to be stated by the company so as to compare the revenues and the

expenses. It is noted that cash flow statement holds only the cash and the cash equivalent which

is associated with the inflows and the outflows, these statements tend to exclude any transactions

that does not involve any cash.

The cash flow statement of Telestra corporation shows that the cash and the cash equvalents for

the year 2017 is 936 million, whereas the net cash was at 3,550 million as of 2016 and it stood at

1,396 million in 2015. This shows that the net cash position of the business has significantly

from 2016 to 2017, some of the reason is due to the significant increase in the investments,

payment of dividends and repayment of borrowings by the management. The major categories of

the cash flow statement is analysed in detail:

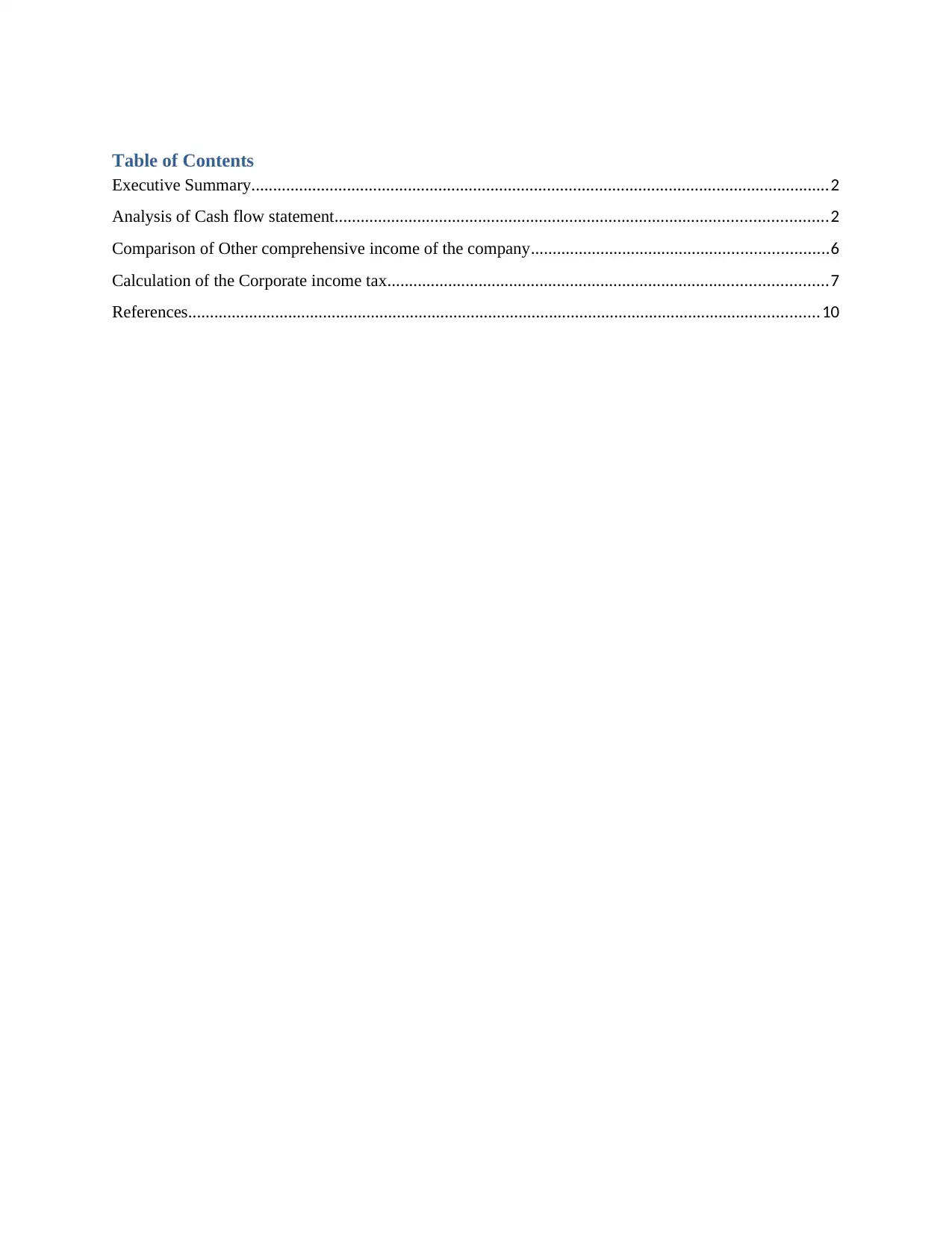

Cash flows from the net operating activities: It is considered as the amount of cash which the

brings in from the normal course of business, which is recurring in nature from the creation and

sales of telecommunication services. The cash flow from the operating services will not include

the long term investments. Based on the critical analysis of the cash flow statement the major

income is from the sale of telecom services to the customers, the income has increased year on

year and it has stood at 31,288 million and the expenses has also increased to -21,997 million.

The cash that was generated from the business was over 9 billion, after paying the income tax,

the net cash from the activities was at 7,775 million in 2017 whereas it was around 8,133 million

in 2016 and 8,311 million in 2015. This shows that the net cash from operating activities has

reduced significantly from 2016 to 2017. (Telestra, 2017)

2017 2016 2015

7500

7600

7700

7800

7900

8000

8100

8200

8300

8400

Net cash provided by operating

activities

Net cash provided by

operating activities

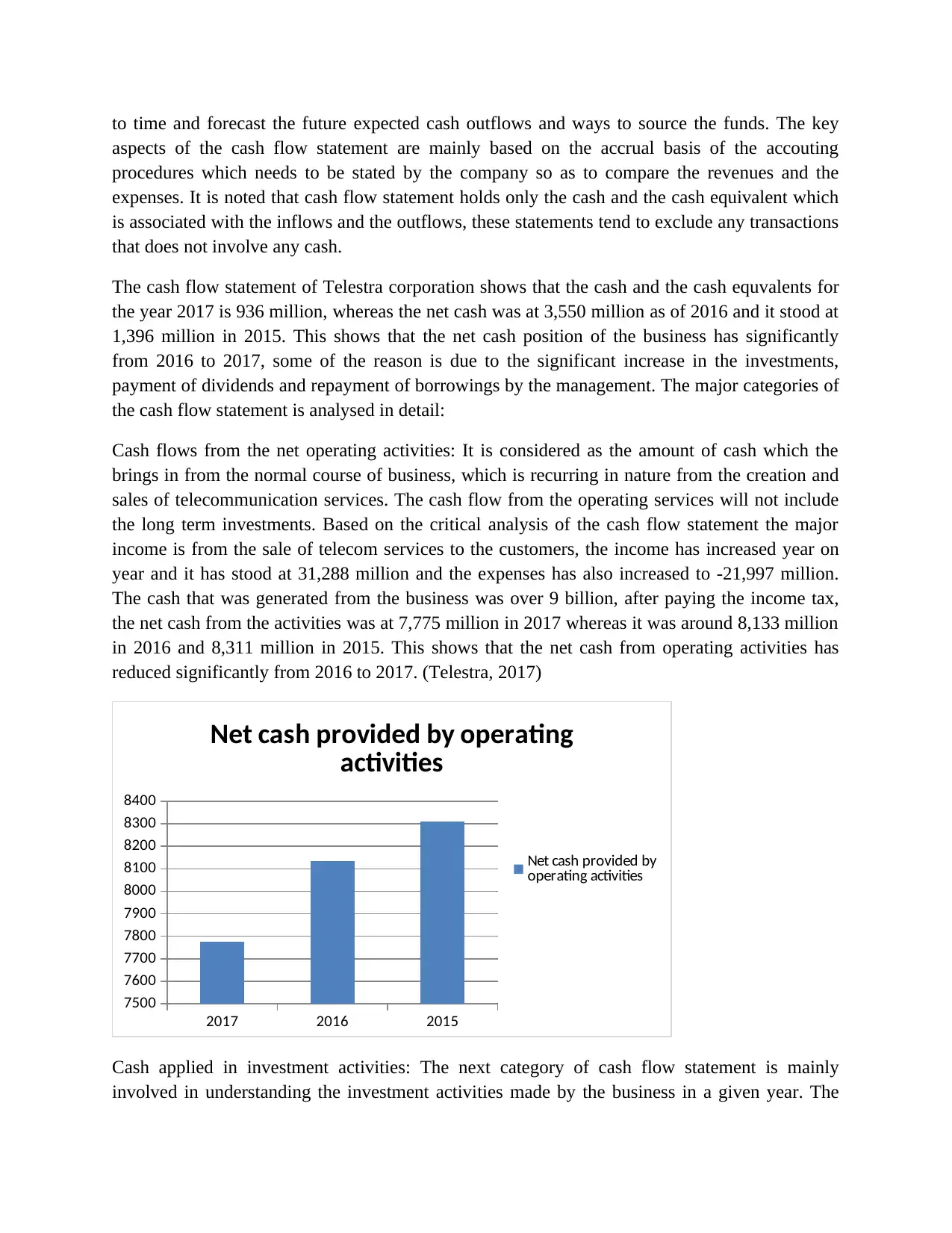

Cash applied in investment activities: The next category of cash flow statement is mainly

involved in understanding the investment activities made by the business in a given year. The

aspects of the cash flow statement are mainly based on the accrual basis of the accouting

procedures which needs to be stated by the company so as to compare the revenues and the

expenses. It is noted that cash flow statement holds only the cash and the cash equivalent which

is associated with the inflows and the outflows, these statements tend to exclude any transactions

that does not involve any cash.

The cash flow statement of Telestra corporation shows that the cash and the cash equvalents for

the year 2017 is 936 million, whereas the net cash was at 3,550 million as of 2016 and it stood at

1,396 million in 2015. This shows that the net cash position of the business has significantly

from 2016 to 2017, some of the reason is due to the significant increase in the investments,

payment of dividends and repayment of borrowings by the management. The major categories of

the cash flow statement is analysed in detail:

Cash flows from the net operating activities: It is considered as the amount of cash which the

brings in from the normal course of business, which is recurring in nature from the creation and

sales of telecommunication services. The cash flow from the operating services will not include

the long term investments. Based on the critical analysis of the cash flow statement the major

income is from the sale of telecom services to the customers, the income has increased year on

year and it has stood at 31,288 million and the expenses has also increased to -21,997 million.

The cash that was generated from the business was over 9 billion, after paying the income tax,

the net cash from the activities was at 7,775 million in 2017 whereas it was around 8,133 million

in 2016 and 8,311 million in 2015. This shows that the net cash from operating activities has

reduced significantly from 2016 to 2017. (Telestra, 2017)

2017 2016 2015

7500

7600

7700

7800

7900

8000

8100

8200

8300

8400

Net cash provided by operating

activities

Net cash provided by

operating activities

Cash applied in investment activities: The next category of cash flow statement is mainly

involved in understanding the investment activities made by the business in a given year. The

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

company mainly invest in the area of property, plant and equipment heavily. The investment in

PPE is -3,725 million in 2017, whereas it was -3,051 million in 2016 and -2,845 million in 2015,

this shows that the company need to invest more in order to retain the market share and increase

its revenues and profits. The company has considerabley reduced its investment in intangible

assets like brand name, logos etc. in 2017 the company realised a revenue of 679 million in 2017,

so the net cash in the investment activities were -4,279 million, however in 2016 it was only -

2,207 million. (Brooks, 2012)

2017 2016 2015

-6000

-5000

-4000

-3000

-2000

-1000

0

Net cash used in investing activities

Net cash used in investing

activities

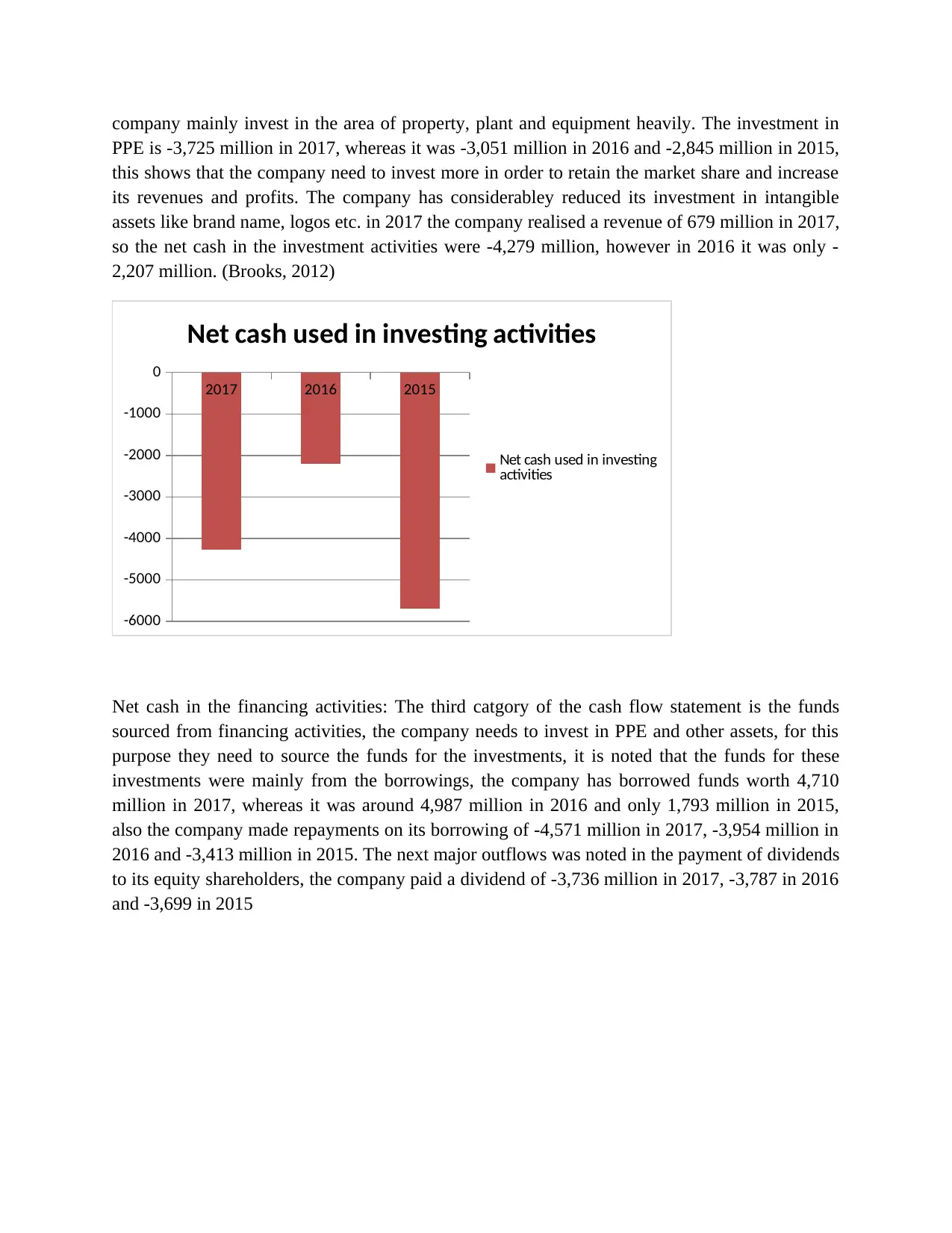

Net cash in the financing activities: The third catgory of the cash flow statement is the funds

sourced from financing activities, the company needs to invest in PPE and other assets, for this

purpose they need to source the funds for the investments, it is noted that the funds for these

investments were mainly from the borrowings, the company has borrowed funds worth 4,710

million in 2017, whereas it was around 4,987 million in 2016 and only 1,793 million in 2015,

also the company made repayments on its borrowing of -4,571 million in 2017, -3,954 million in

2016 and -3,413 million in 2015. The next major outflows was noted in the payment of dividends

to its equity shareholders, the company paid a dividend of -3,736 million in 2017, -3,787 in 2016

and -3,699 in 2015

PPE is -3,725 million in 2017, whereas it was -3,051 million in 2016 and -2,845 million in 2015,

this shows that the company need to invest more in order to retain the market share and increase

its revenues and profits. The company has considerabley reduced its investment in intangible

assets like brand name, logos etc. in 2017 the company realised a revenue of 679 million in 2017,

so the net cash in the investment activities were -4,279 million, however in 2016 it was only -

2,207 million. (Brooks, 2012)

2017 2016 2015

-6000

-5000

-4000

-3000

-2000

-1000

0

Net cash used in investing activities

Net cash used in investing

activities

Net cash in the financing activities: The third catgory of the cash flow statement is the funds

sourced from financing activities, the company needs to invest in PPE and other assets, for this

purpose they need to source the funds for the investments, it is noted that the funds for these

investments were mainly from the borrowings, the company has borrowed funds worth 4,710

million in 2017, whereas it was around 4,987 million in 2016 and only 1,793 million in 2015,

also the company made repayments on its borrowing of -4,571 million in 2017, -3,954 million in

2016 and -3,413 million in 2015. The next major outflows was noted in the payment of dividends

to its equity shareholders, the company paid a dividend of -3,736 million in 2017, -3,787 in 2016

and -3,699 in 2015

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2017 2016 2015

-8000

-7000

-6000

-5000

-4000

-3000

-2000

-1000

0

Net cash used in financing activities

Net cash used in financing

activities

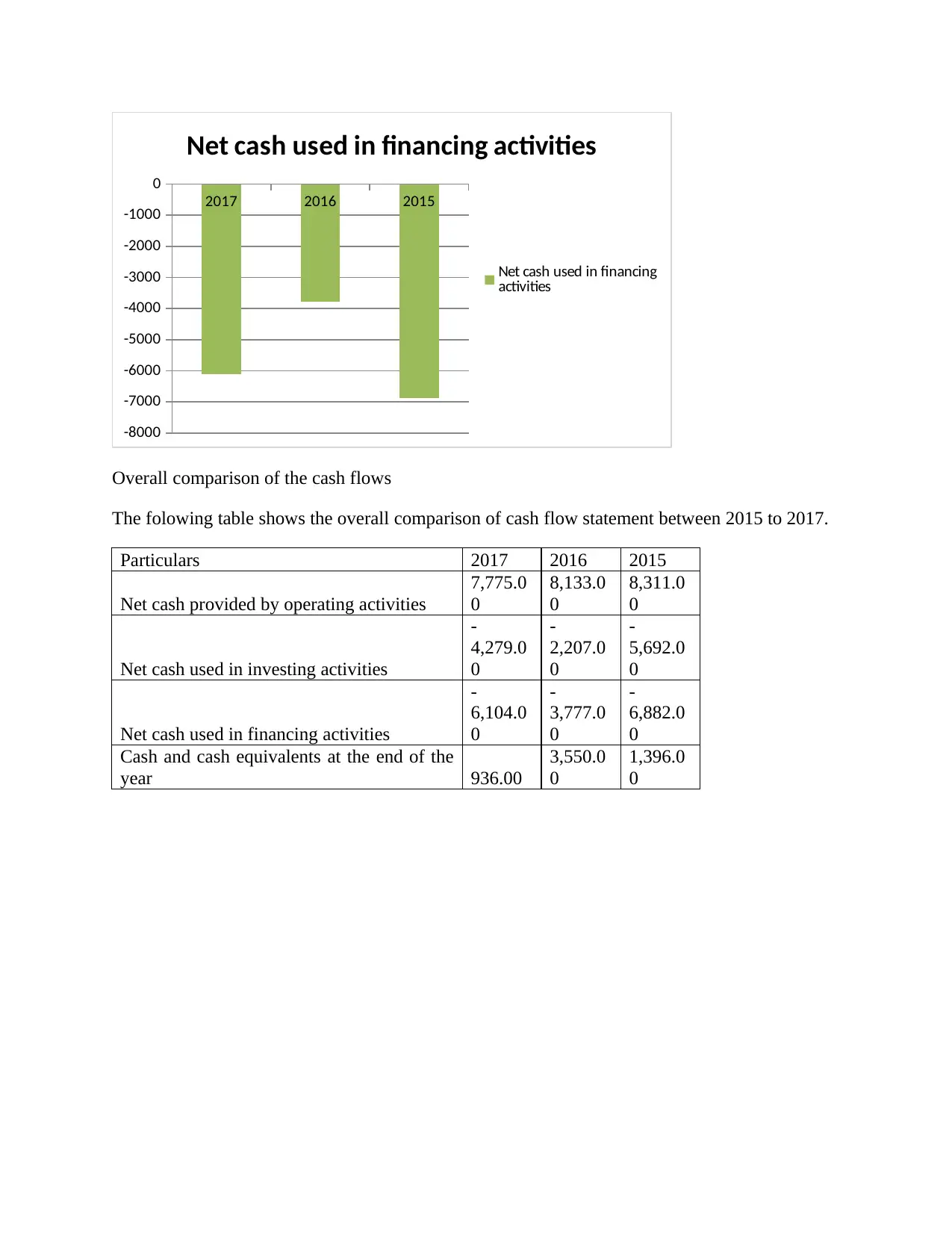

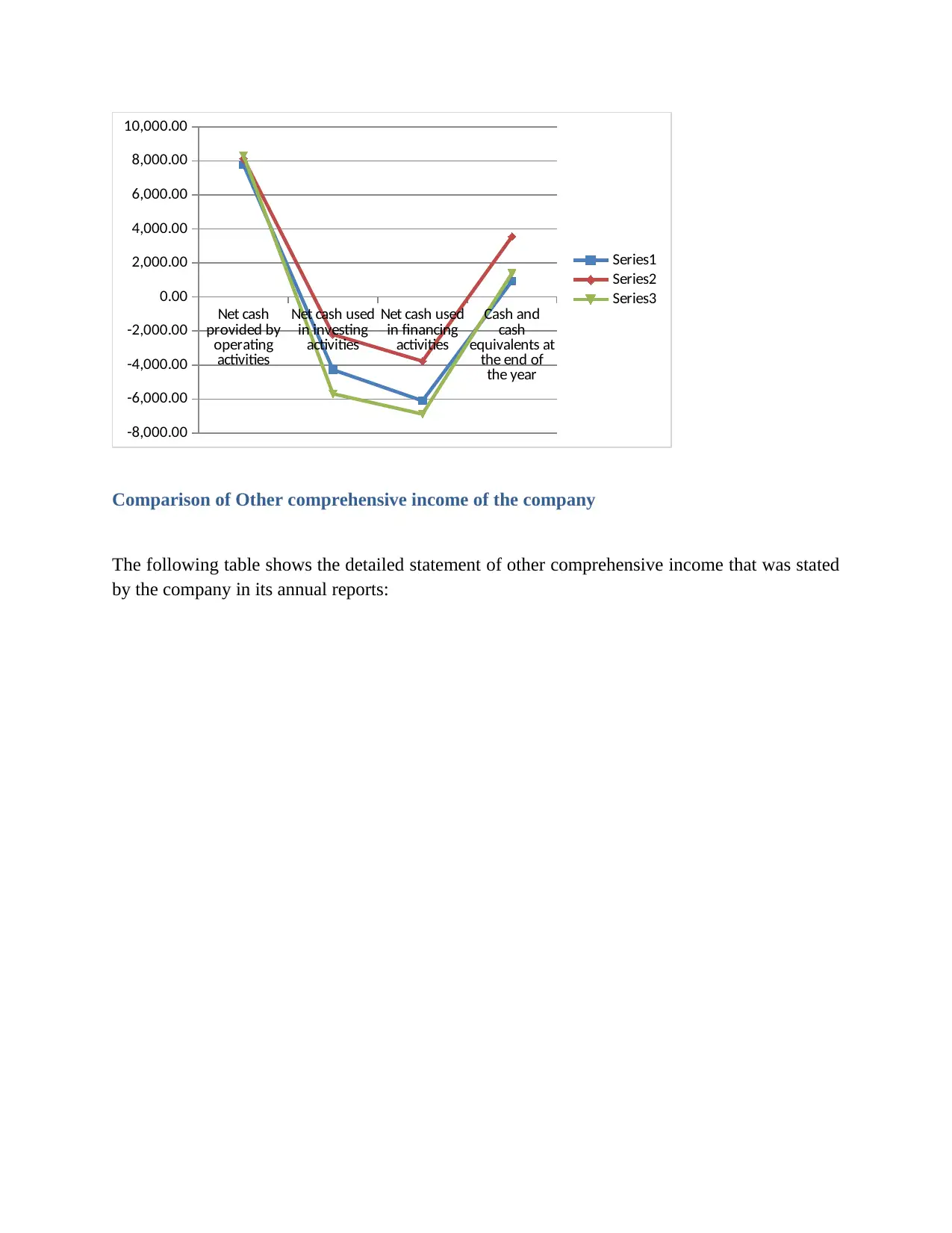

Overall comparison of the cash flows

The folowing table shows the overall comparison of cash flow statement between 2015 to 2017.

Particulars 2017 2016 2015

Net cash provided by operating activities

7,775.0

0

8,133.0

0

8,311.0

0

Net cash used in investing activities

-

4,279.0

0

-

2,207.0

0

-

5,692.0

0

Net cash used in financing activities

-

6,104.0

0

-

3,777.0

0

-

6,882.0

0

Cash and cash equivalents at the end of the

year 936.00

3,550.0

0

1,396.0

0

-8000

-7000

-6000

-5000

-4000

-3000

-2000

-1000

0

Net cash used in financing activities

Net cash used in financing

activities

Overall comparison of the cash flows

The folowing table shows the overall comparison of cash flow statement between 2015 to 2017.

Particulars 2017 2016 2015

Net cash provided by operating activities

7,775.0

0

8,133.0

0

8,311.0

0

Net cash used in investing activities

-

4,279.0

0

-

2,207.0

0

-

5,692.0

0

Net cash used in financing activities

-

6,104.0

0

-

3,777.0

0

-

6,882.0

0

Cash and cash equivalents at the end of the

year 936.00

3,550.0

0

1,396.0

0

Net cash

provided by

operating

activities

Net cash used

in investing

activities

Net cash used

in financing

activities

Cash and

cash

equivalents at

the end of

the year

-8,000.00

-6,000.00

-4,000.00

-2,000.00

0.00

2,000.00

4,000.00

6,000.00

8,000.00

10,000.00

Series1

Series2

Series3

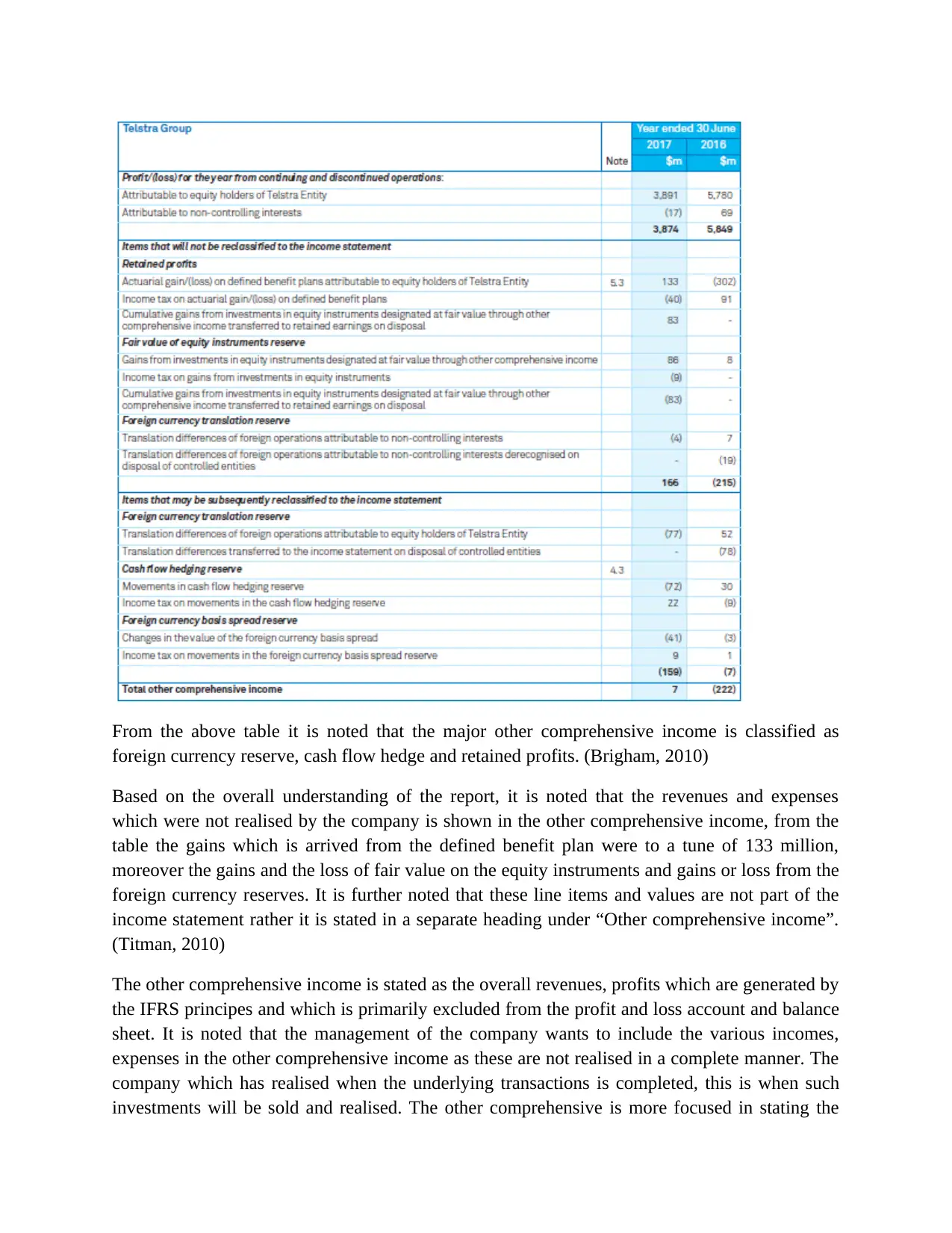

Comparison of Other comprehensive income of the company

The following table shows the detailed statement of other comprehensive income that was stated

by the company in its annual reports:

provided by

operating

activities

Net cash used

in investing

activities

Net cash used

in financing

activities

Cash and

cash

equivalents at

the end of

the year

-8,000.00

-6,000.00

-4,000.00

-2,000.00

0.00

2,000.00

4,000.00

6,000.00

8,000.00

10,000.00

Series1

Series2

Series3

Comparison of Other comprehensive income of the company

The following table shows the detailed statement of other comprehensive income that was stated

by the company in its annual reports:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

From the above table it is noted that the major other comprehensive income is classified as

foreign currency reserve, cash flow hedge and retained profits. (Brigham, 2010)

Based on the overall understanding of the report, it is noted that the revenues and expenses

which were not realised by the company is shown in the other comprehensive income, from the

table the gains which is arrived from the defined benefit plan were to a tune of 133 million,

moreover the gains and the loss of fair value on the equity instruments and gains or loss from the

foreign currency reserves. It is further noted that these line items and values are not part of the

income statement rather it is stated in a separate heading under “Other comprehensive income”.

(Titman, 2010)

The other comprehensive income is stated as the overall revenues, profits which are generated by

the IFRS principes and which is primarily excluded from the profit and loss account and balance

sheet. It is noted that the management of the company wants to include the various incomes,

expenses in the other comprehensive income as these are not realised in a complete manner. The

company which has realised when the underlying transactions is completed, this is when such

investments will be sold and realised. The other comprehensive is more focused in stating the

foreign currency reserve, cash flow hedge and retained profits. (Brigham, 2010)

Based on the overall understanding of the report, it is noted that the revenues and expenses

which were not realised by the company is shown in the other comprehensive income, from the

table the gains which is arrived from the defined benefit plan were to a tune of 133 million,

moreover the gains and the loss of fair value on the equity instruments and gains or loss from the

foreign currency reserves. It is further noted that these line items and values are not part of the

income statement rather it is stated in a separate heading under “Other comprehensive income”.

(Titman, 2010)

The other comprehensive income is stated as the overall revenues, profits which are generated by

the IFRS principes and which is primarily excluded from the profit and loss account and balance

sheet. It is noted that the management of the company wants to include the various incomes,

expenses in the other comprehensive income as these are not realised in a complete manner. The

company which has realised when the underlying transactions is completed, this is when such

investments will be sold and realised. The other comprehensive is more focused in stating the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

unreserved aspect on the net income, previously the changes to the profits of the business which

are outside the core operations were been included in the equity. (Ray, 2011). The OCI intends to

state in detail the values, which are non core in nature and it is not realised by the company. It

provides detailed and more holistic aspects on the company operations and other aspects of the

business.

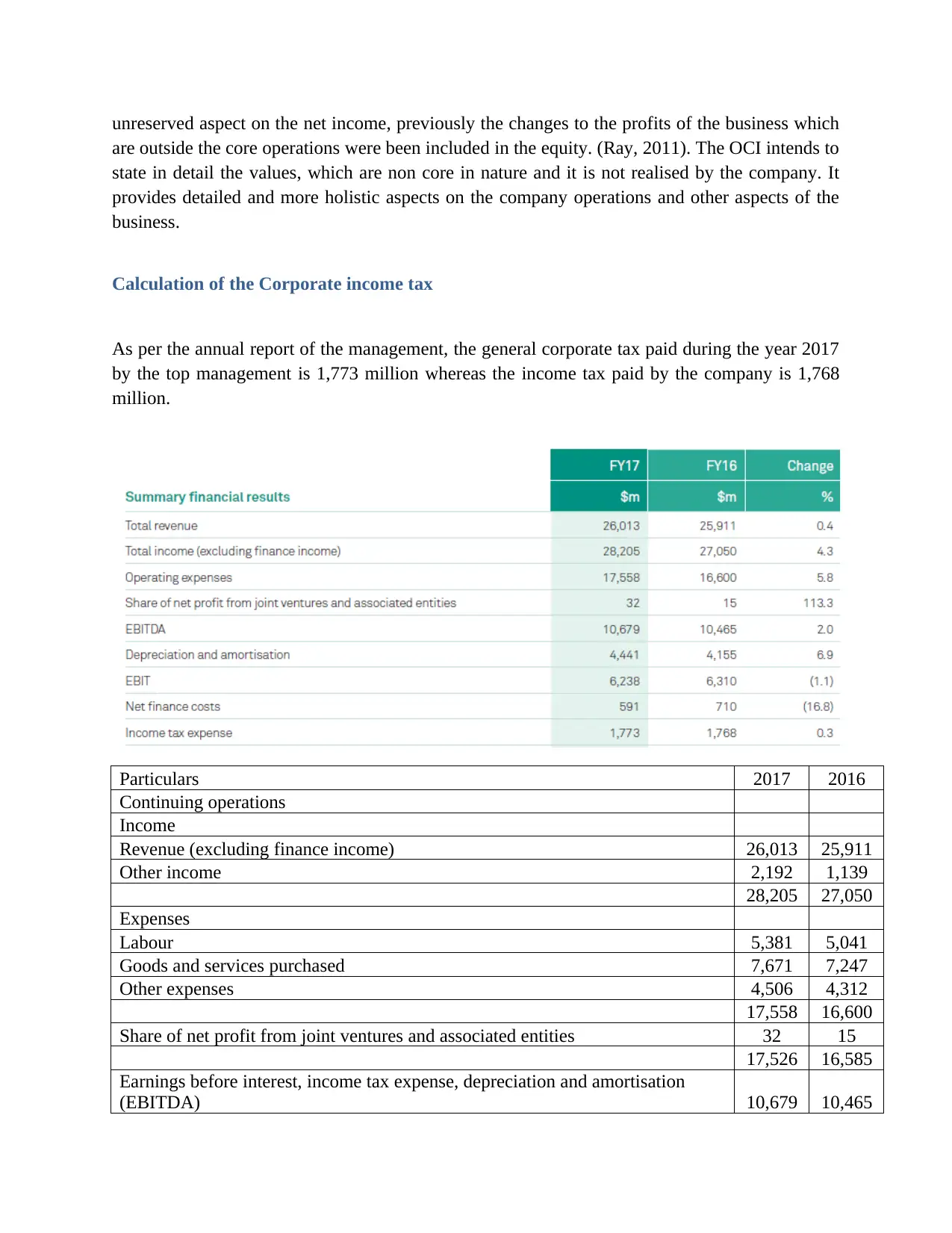

Calculation of the Corporate income tax

As per the annual report of the management, the general corporate tax paid during the year 2017

by the top management is 1,773 million whereas the income tax paid by the company is 1,768

million.

Particulars 2017 2016

Continuing operations

Income

Revenue (excluding finance income) 26,013 25,911

Other income 2,192 1,139

28,205 27,050

Expenses

Labour 5,381 5,041

Goods and services purchased 7,671 7,247

Other expenses 4,506 4,312

17,558 16,600

Share of net profit from joint ventures and associated entities 32 15

17,526 16,585

Earnings before interest, income tax expense, depreciation and amortisation

(EBITDA) 10,679 10,465

are outside the core operations were been included in the equity. (Ray, 2011). The OCI intends to

state in detail the values, which are non core in nature and it is not realised by the company. It

provides detailed and more holistic aspects on the company operations and other aspects of the

business.

Calculation of the Corporate income tax

As per the annual report of the management, the general corporate tax paid during the year 2017

by the top management is 1,773 million whereas the income tax paid by the company is 1,768

million.

Particulars 2017 2016

Continuing operations

Income

Revenue (excluding finance income) 26,013 25,911

Other income 2,192 1,139

28,205 27,050

Expenses

Labour 5,381 5,041

Goods and services purchased 7,671 7,247

Other expenses 4,506 4,312

17,558 16,600

Share of net profit from joint ventures and associated entities 32 15

17,526 16,585

Earnings before interest, income tax expense, depreciation and amortisation

(EBITDA) 10,679 10,465

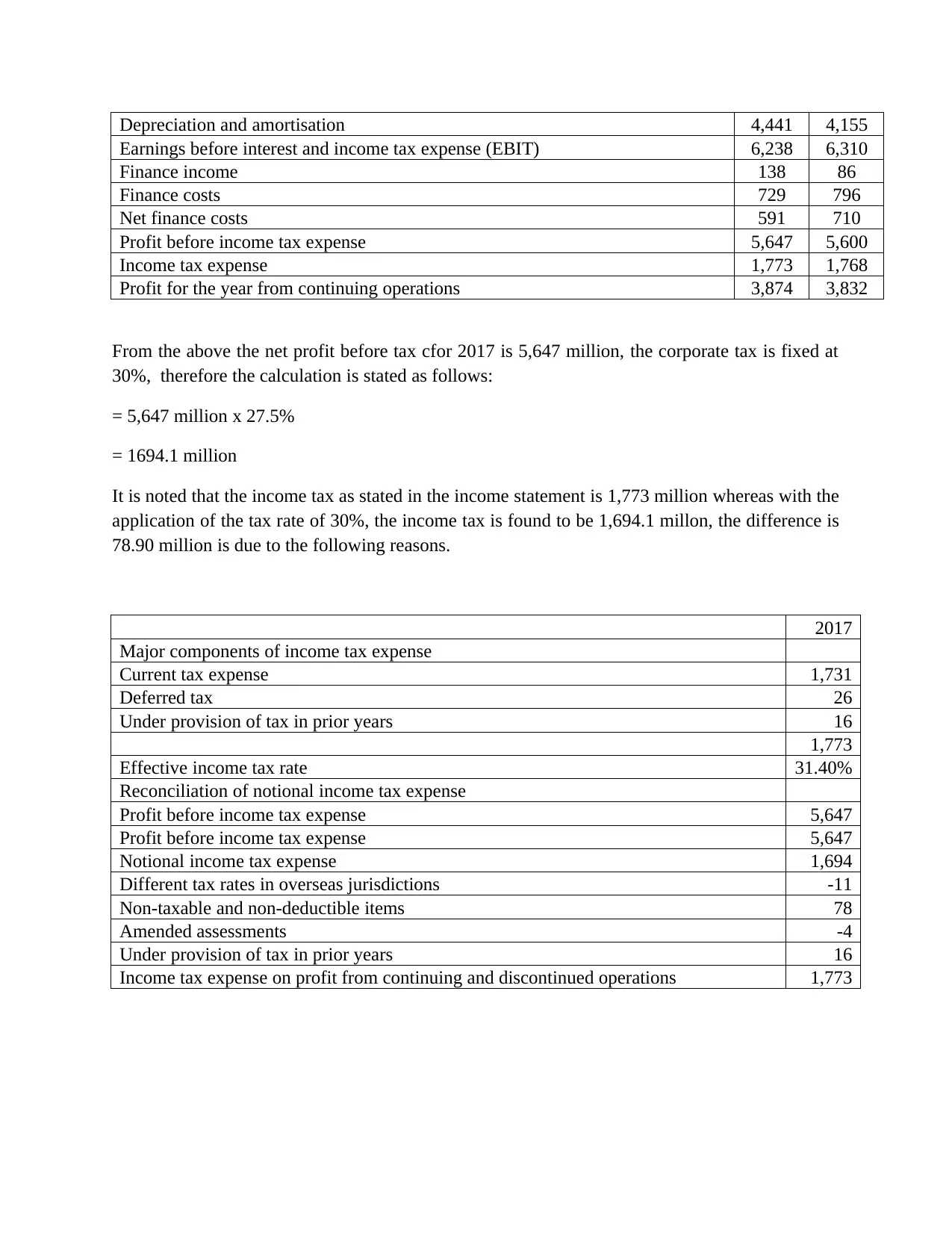

Depreciation and amortisation 4,441 4,155

Earnings before interest and income tax expense (EBIT) 6,238 6,310

Finance income 138 86

Finance costs 729 796

Net finance costs 591 710

Profit before income tax expense 5,647 5,600

Income tax expense 1,773 1,768

Profit for the year from continuing operations 3,874 3,832

From the above the net profit before tax cfor 2017 is 5,647 million, the corporate tax is fixed at

30%, therefore the calculation is stated as follows:

= 5,647 million x 27.5%

= 1694.1 million

It is noted that the income tax as stated in the income statement is 1,773 million whereas with the

application of the tax rate of 30%, the income tax is found to be 1,694.1 millon, the difference is

78.90 million is due to the following reasons.

2017

Major components of income tax expense

Current tax expense 1,731

Deferred tax 26

Under provision of tax in prior years 16

1,773

Effective income tax rate 31.40%

Reconciliation of notional income tax expense

Profit before income tax expense 5,647

Profit before income tax expense 5,647

Notional income tax expense 1,694

Different tax rates in overseas jurisdictions -11

Non-taxable and non-deductible items 78

Amended assessments -4

Under provision of tax in prior years 16

Income tax expense on profit from continuing and discontinued operations 1,773

Earnings before interest and income tax expense (EBIT) 6,238 6,310

Finance income 138 86

Finance costs 729 796

Net finance costs 591 710

Profit before income tax expense 5,647 5,600

Income tax expense 1,773 1,768

Profit for the year from continuing operations 3,874 3,832

From the above the net profit before tax cfor 2017 is 5,647 million, the corporate tax is fixed at

30%, therefore the calculation is stated as follows:

= 5,647 million x 27.5%

= 1694.1 million

It is noted that the income tax as stated in the income statement is 1,773 million whereas with the

application of the tax rate of 30%, the income tax is found to be 1,694.1 millon, the difference is

78.90 million is due to the following reasons.

2017

Major components of income tax expense

Current tax expense 1,731

Deferred tax 26

Under provision of tax in prior years 16

1,773

Effective income tax rate 31.40%

Reconciliation of notional income tax expense

Profit before income tax expense 5,647

Profit before income tax expense 5,647

Notional income tax expense 1,694

Different tax rates in overseas jurisdictions -11

Non-taxable and non-deductible items 78

Amended assessments -4

Under provision of tax in prior years 16

Income tax expense on profit from continuing and discontinued operations 1,773

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

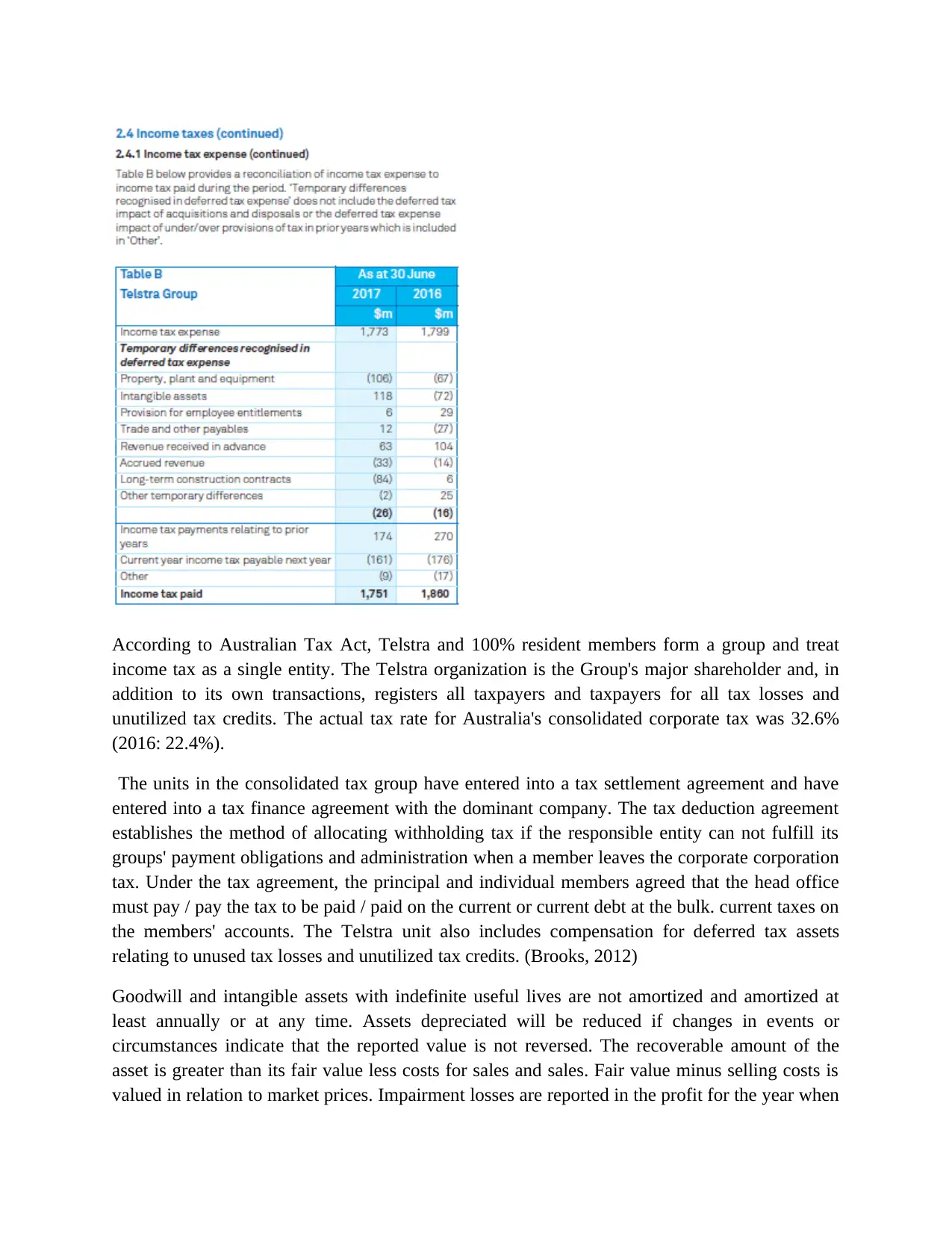

According to Australian Tax Act, Telstra and 100% resident members form a group and treat

income tax as a single entity. The Telstra organization is the Group's major shareholder and, in

addition to its own transactions, registers all taxpayers and taxpayers for all tax losses and

unutilized tax credits. The actual tax rate for Australia's consolidated corporate tax was 32.6%

(2016: 22.4%).

The units in the consolidated tax group have entered into a tax settlement agreement and have

entered into a tax finance agreement with the dominant company. The tax deduction agreement

establishes the method of allocating withholding tax if the responsible entity can not fulfill its

groups' payment obligations and administration when a member leaves the corporate corporation

tax. Under the tax agreement, the principal and individual members agreed that the head office

must pay / pay the tax to be paid / paid on the current or current debt at the bulk. current taxes on

the members' accounts. The Telstra unit also includes compensation for deferred tax assets

relating to unused tax losses and unutilized tax credits. (Brooks, 2012)

Goodwill and intangible assets with indefinite useful lives are not amortized and amortized at

least annually or at any time. Assets depreciated will be reduced if changes in events or

circumstances indicate that the reported value is not reversed. The recoverable amount of the

asset is greater than its fair value less costs for sales and sales. Fair value minus selling costs is

valued in relation to market prices. Impairment losses are reported in the profit for the year when

income tax as a single entity. The Telstra organization is the Group's major shareholder and, in

addition to its own transactions, registers all taxpayers and taxpayers for all tax losses and

unutilized tax credits. The actual tax rate for Australia's consolidated corporate tax was 32.6%

(2016: 22.4%).

The units in the consolidated tax group have entered into a tax settlement agreement and have

entered into a tax finance agreement with the dominant company. The tax deduction agreement

establishes the method of allocating withholding tax if the responsible entity can not fulfill its

groups' payment obligations and administration when a member leaves the corporate corporation

tax. Under the tax agreement, the principal and individual members agreed that the head office

must pay / pay the tax to be paid / paid on the current or current debt at the bulk. current taxes on

the members' accounts. The Telstra unit also includes compensation for deferred tax assets

relating to unused tax losses and unutilized tax credits. (Brooks, 2012)

Goodwill and intangible assets with indefinite useful lives are not amortized and amortized at

least annually or at any time. Assets depreciated will be reduced if changes in events or

circumstances indicate that the reported value is not reversed. The recoverable amount of the

asset is greater than its fair value less costs for sales and sales. Fair value minus selling costs is

valued in relation to market prices. Impairment losses are reported in the profit for the year when

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

the asset's carrying amount exceeds the recoverable amount. As of June 30, 2017, the book value

of FRED IT and HealthConnex deteriorated. The recoverable value of these UGCs was

determined using a "usage value" and lower than their carrying amount. As a result, we lost $ 21

million in write-downs and $ 17 million in write-downs due to the relevant UCI's goodwill.

(Weygandt, 2011)

Impairments are the result of changed industrial conditions and competitive pressure in the older

pharmaceutical and healthcare industries, resulting in a lower cash flow forecast. Calculation of

the value of treatment during use takes into account the above factors. In addition, depreciation

of $ 26 million was reported against goodwill, which is similar to individually qualified

intellectual property UGC. The aging analysis in the table above is based on the customer's

original maturity, including renegotiation of the payment terms for certain postponements. As of

June 30, 2017, the book value of $ 950 million (USD 996 million in 2016) was calculated but not

decreased. We provide a number of complaints, including late or doubtful claims, warranties,

credit letters and deposits. During the fiscal year 2017 the titles were insignificant. These

business requirements, together with our claims from non-paying and troubled customers,

include good customer history customers and can be refunded. The terms of the derivative

contract are initially determined and therefore the change in the underlying asset's exchange rate

will result in a continuous fluctuation in the contract value, which is reflected in the fair value of

the derivative trade. All derivative instruments are initially recognized at fair value and

subsequently valued at fair value at each balance sheet date. If the fair value of a derivative is

positive, it is reported as an asset and, if negative, a liability.

References

Bragg, Steven. (2007). Throughput Accounting: A Guide to Constraint Management. 1st edition.

Wiley & Sons

Brigham, E. F. (2010). Financial Management: Theory & Practice. 5th edition. Cengage

Learning.

Brooks, R. M. (2012). Financial Management. 4th edition. Prentice Hall.

Kaplan, R. S., & Young, M. S. (2011). Management Accounting. 3rd edition. Prentice Hall.

Ray, G., & Eric, N. (2011). Managerial Accounting. McGraw-Hill/Irwin.

Telestra Corporation (2017). Annual report of Telestra

Titman, S. J. (2010). Financial Management. Prentice Hall.

of FRED IT and HealthConnex deteriorated. The recoverable value of these UGCs was

determined using a "usage value" and lower than their carrying amount. As a result, we lost $ 21

million in write-downs and $ 17 million in write-downs due to the relevant UCI's goodwill.

(Weygandt, 2011)

Impairments are the result of changed industrial conditions and competitive pressure in the older

pharmaceutical and healthcare industries, resulting in a lower cash flow forecast. Calculation of

the value of treatment during use takes into account the above factors. In addition, depreciation

of $ 26 million was reported against goodwill, which is similar to individually qualified

intellectual property UGC. The aging analysis in the table above is based on the customer's

original maturity, including renegotiation of the payment terms for certain postponements. As of

June 30, 2017, the book value of $ 950 million (USD 996 million in 2016) was calculated but not

decreased. We provide a number of complaints, including late or doubtful claims, warranties,

credit letters and deposits. During the fiscal year 2017 the titles were insignificant. These

business requirements, together with our claims from non-paying and troubled customers,

include good customer history customers and can be refunded. The terms of the derivative

contract are initially determined and therefore the change in the underlying asset's exchange rate

will result in a continuous fluctuation in the contract value, which is reflected in the fair value of

the derivative trade. All derivative instruments are initially recognized at fair value and

subsequently valued at fair value at each balance sheet date. If the fair value of a derivative is

positive, it is reported as an asset and, if negative, a liability.

References

Bragg, Steven. (2007). Throughput Accounting: A Guide to Constraint Management. 1st edition.

Wiley & Sons

Brigham, E. F. (2010). Financial Management: Theory & Practice. 5th edition. Cengage

Learning.

Brooks, R. M. (2012). Financial Management. 4th edition. Prentice Hall.

Kaplan, R. S., & Young, M. S. (2011). Management Accounting. 3rd edition. Prentice Hall.

Ray, G., & Eric, N. (2011). Managerial Accounting. McGraw-Hill/Irwin.

Telestra Corporation (2017). Annual report of Telestra

Titman, S. J. (2010). Financial Management. Prentice Hall.

Weygandt. (2011). Managerial Accounting: Tools for Business Decision Making (6th ed.).

Wiley.

Wiley.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.