MBA Financial Analysis Report: Dutch Lady Milk Industries Berhad

VerifiedAdded on 2022/08/12

|25

|4270

|32

Report

AI Summary

This report presents a comprehensive financial analysis of Dutch Lady Milk Industries Berhad, a prominent dairy company in Malaysia. It begins with an introduction to financial analysis and its significance in business decision-making, followed by a detailed profile of Dutch Lady, including its history, product offerings, and strategic analysis based on internal and external factors. The report then assesses industry attractiveness and conducts a PEST analysis to understand the political, economic, social, and technological factors influencing the company. A crucial part of the report involves a four-year financial performance analysis, utilizing profitability, liquidity, and efficiency ratios to evaluate the company's financial health and trends. The report also includes a cash flow analysis and concludes with suggestions for further research and improvements, providing valuable insights for understanding the company's financial performance and strategic positioning in the market. This report follows the assignment brief from an MBA module in Financial Analysis and Management.

Running Head: ACCOUNTING FINNACIAL ANALYSIS REPORT

ACCOUNTING FINANCIAL ANALYSIS REPORT

Name of the Student

Name of the University

Author Note

ACCOUNTING FINANCIAL ANALYSIS REPORT

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ACCOUNTING FINANCIAL ANALYSIS REPORT

Table of Contents

Introduction................................................................................................................................2

Profiling Information.................................................................................................................2

Industry Attractiveness...............................................................................................................4

PEST Analysis...........................................................................................................................5

Financial Performance Analysis................................................................................................6

Cash Flow Analysis..................................................................................................................17

Scope for Further Research......................................................................................................20

Reference..................................................................................................................................22

Table of Contents

Introduction................................................................................................................................2

Profiling Information.................................................................................................................2

Industry Attractiveness...............................................................................................................4

PEST Analysis...........................................................................................................................5

Financial Performance Analysis................................................................................................6

Cash Flow Analysis..................................................................................................................17

Scope for Further Research......................................................................................................20

Reference..................................................................................................................................22

2ACCOUNTING FINANCIAL ANALYSIS REPORT

Introduction

Financial analysis examines the financial information for reaching the decisions of

business. It involves using the financial data for assessing performance of company and

making recommendations regarding the way it can be improved. Financial health of company

is the best indicator of analyzing potential of business for the long-term growth (AMOAH

2016). Hence, this report aims to evaluate key drivers, which have affected group and

industry as whole. Further, financial analysis of “Dutch Lady Milk Industries Berhad” for

four consecutive year will be done and suggestions will be given based on prevailing trends.

Lastly, analysis of the cash flow statements will be done and suggestions will be given on

possible impacts of changing environment.

Profiling Information

“Dutch Lady Milk Industries Berhad” is the dairy company based in Malaysia. This

company operates through manufacturing as well as distribution of ranges of the dairy

products segments. The company manufacturers milk powder, sweetened condensed milk,

fruit juice drinks and dairy products. It established first as manufacturer of the sweetened

condensed milk in year 1960 in their own factory in Petaling Jaya and still when more than

fifty years have passed, it operates in same plant of production. The products of this entity

include “Friso Gold”, “Dutch Lady Purefarm UHT milk” and formulated milk powder for the

children “Dutch Lady Nutriplan with 5X DHA”. The distribution of these products are in

East Malaysia as well as Peninsular (Disclosure.bursamalaysia.com. 2020).

Strategic Analysis

Introduction

Financial analysis examines the financial information for reaching the decisions of

business. It involves using the financial data for assessing performance of company and

making recommendations regarding the way it can be improved. Financial health of company

is the best indicator of analyzing potential of business for the long-term growth (AMOAH

2016). Hence, this report aims to evaluate key drivers, which have affected group and

industry as whole. Further, financial analysis of “Dutch Lady Milk Industries Berhad” for

four consecutive year will be done and suggestions will be given based on prevailing trends.

Lastly, analysis of the cash flow statements will be done and suggestions will be given on

possible impacts of changing environment.

Profiling Information

“Dutch Lady Milk Industries Berhad” is the dairy company based in Malaysia. This

company operates through manufacturing as well as distribution of ranges of the dairy

products segments. The company manufacturers milk powder, sweetened condensed milk,

fruit juice drinks and dairy products. It established first as manufacturer of the sweetened

condensed milk in year 1960 in their own factory in Petaling Jaya and still when more than

fifty years have passed, it operates in same plant of production. The products of this entity

include “Friso Gold”, “Dutch Lady Purefarm UHT milk” and formulated milk powder for the

children “Dutch Lady Nutriplan with 5X DHA”. The distribution of these products are in

East Malaysia as well as Peninsular (Disclosure.bursamalaysia.com. 2020).

Strategic Analysis

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ACCOUNTING FINANCIAL ANALYSIS REPORT

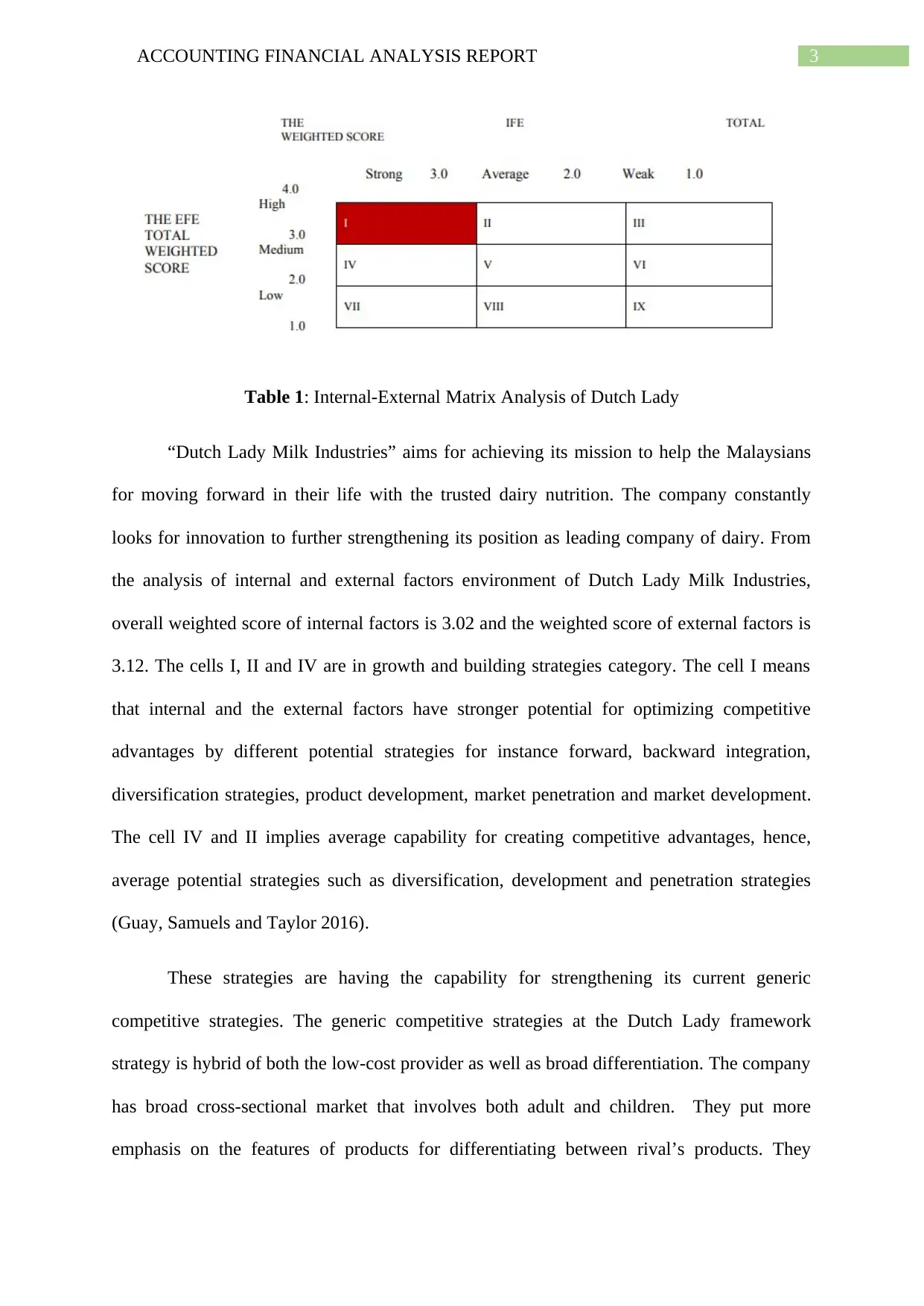

Table 1: Internal-External Matrix Analysis of Dutch Lady

“Dutch Lady Milk Industries” aims for achieving its mission to help the Malaysians

for moving forward in their life with the trusted dairy nutrition. The company constantly

looks for innovation to further strengthening its position as leading company of dairy. From

the analysis of internal and external factors environment of Dutch Lady Milk Industries,

overall weighted score of internal factors is 3.02 and the weighted score of external factors is

3.12. The cells I, II and IV are in growth and building strategies category. The cell I means

that internal and the external factors have stronger potential for optimizing competitive

advantages by different potential strategies for instance forward, backward integration,

diversification strategies, product development, market penetration and market development.

The cell IV and II implies average capability for creating competitive advantages, hence,

average potential strategies such as diversification, development and penetration strategies

(Guay, Samuels and Taylor 2016).

These strategies are having the capability for strengthening its current generic

competitive strategies. The generic competitive strategies at the Dutch Lady framework

strategy is hybrid of both the low-cost provider as well as broad differentiation. The company

has broad cross-sectional market that involves both adult and children. They put more

emphasis on the features of products for differentiating between rival’s products. They

Table 1: Internal-External Matrix Analysis of Dutch Lady

“Dutch Lady Milk Industries” aims for achieving its mission to help the Malaysians

for moving forward in their life with the trusted dairy nutrition. The company constantly

looks for innovation to further strengthening its position as leading company of dairy. From

the analysis of internal and external factors environment of Dutch Lady Milk Industries,

overall weighted score of internal factors is 3.02 and the weighted score of external factors is

3.12. The cells I, II and IV are in growth and building strategies category. The cell I means

that internal and the external factors have stronger potential for optimizing competitive

advantages by different potential strategies for instance forward, backward integration,

diversification strategies, product development, market penetration and market development.

The cell IV and II implies average capability for creating competitive advantages, hence,

average potential strategies such as diversification, development and penetration strategies

(Guay, Samuels and Taylor 2016).

These strategies are having the capability for strengthening its current generic

competitive strategies. The generic competitive strategies at the Dutch Lady framework

strategy is hybrid of both the low-cost provider as well as broad differentiation. The company

has broad cross-sectional market that involves both adult and children. They put more

emphasis on the features of products for differentiating between rival’s products. They

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ACCOUNTING FINANCIAL ANALYSIS REPORT

continuously strives for reducing cost that help them in upgradation to robotic and automatic

line in power plant as well as relaunching of products with the new formulation. The

company have also customized packaging and the promotion for various target group for

instance, iconic animation for attracting kinds, smaller six for the school children and

economic pack for the families and many more (Disclosure.bursamalaysia.com. 2020).

Industry Attractiveness

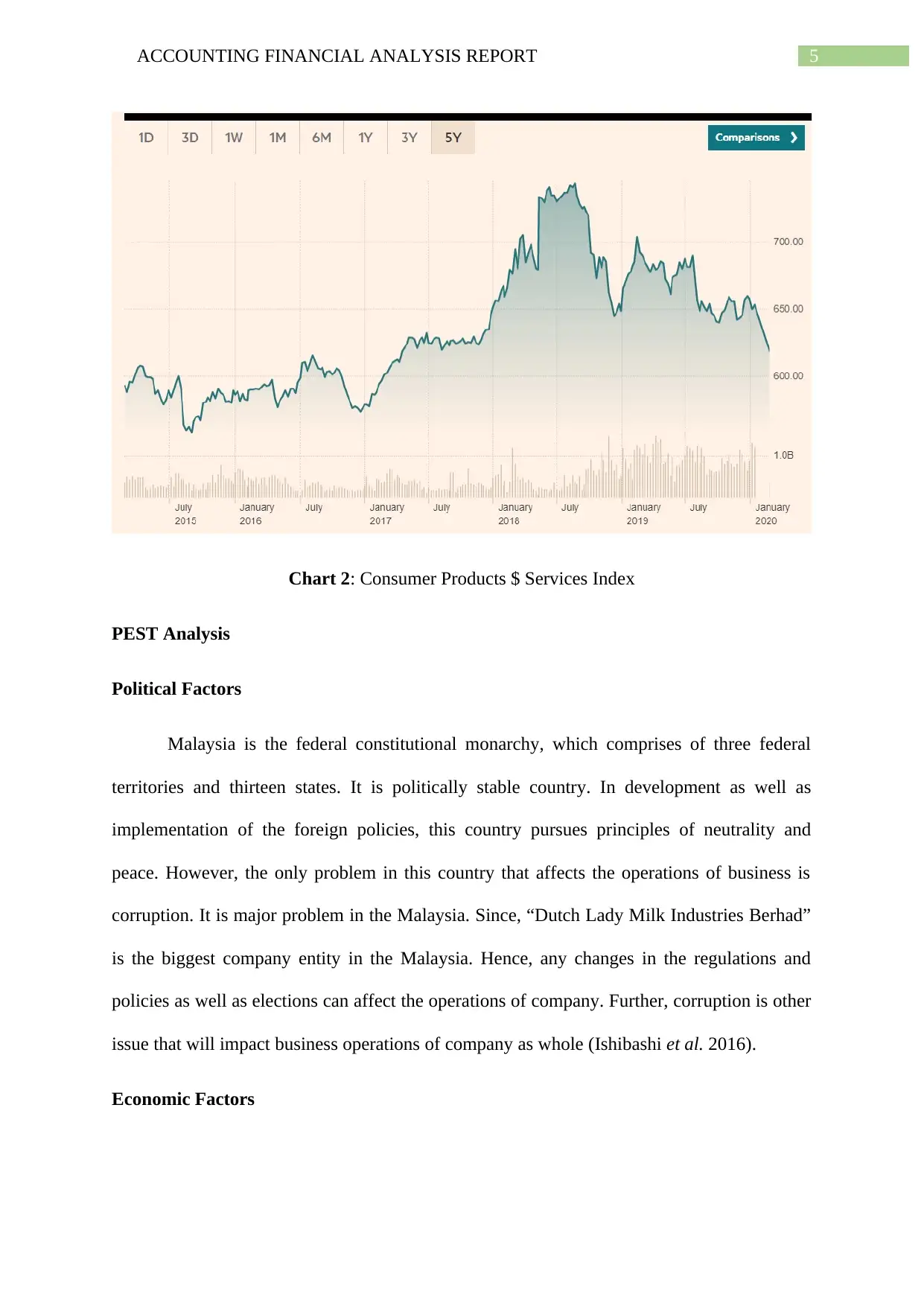

The company operates in the industry of consumer products & services. The

improvement in economic outlook and the growth data of job are expected to fuel the

spending of consumer globally. Further, several stocks of consumer on local bourse have

witnessed high valuations over past years, while consumer index of Bursa Malaysia has

outperformed FBM KLCI, right since start of year. The consumer index has PER of 29.8

times. The country’s recent performance of the consumer stocks has been influenced largely

by uncertainties in run-up to 14th general elections and post-election policies. Hence, in run-

up to election, the index of consumer rose 5.1% in comparison to FBM KLCI’s 2.8%.

However, after election, this index rose to 14.5%, while FBM KLCI fell by 2%. Moreover,

the five-year trend of consumer staples industry indicates high growth rate of industry over

the years (Popoola et al. 2014).

continuously strives for reducing cost that help them in upgradation to robotic and automatic

line in power plant as well as relaunching of products with the new formulation. The

company have also customized packaging and the promotion for various target group for

instance, iconic animation for attracting kinds, smaller six for the school children and

economic pack for the families and many more (Disclosure.bursamalaysia.com. 2020).

Industry Attractiveness

The company operates in the industry of consumer products & services. The

improvement in economic outlook and the growth data of job are expected to fuel the

spending of consumer globally. Further, several stocks of consumer on local bourse have

witnessed high valuations over past years, while consumer index of Bursa Malaysia has

outperformed FBM KLCI, right since start of year. The consumer index has PER of 29.8

times. The country’s recent performance of the consumer stocks has been influenced largely

by uncertainties in run-up to 14th general elections and post-election policies. Hence, in run-

up to election, the index of consumer rose 5.1% in comparison to FBM KLCI’s 2.8%.

However, after election, this index rose to 14.5%, while FBM KLCI fell by 2%. Moreover,

the five-year trend of consumer staples industry indicates high growth rate of industry over

the years (Popoola et al. 2014).

5ACCOUNTING FINANCIAL ANALYSIS REPORT

Chart 2: Consumer Products $ Services Index

PEST Analysis

Political Factors

Malaysia is the federal constitutional monarchy, which comprises of three federal

territories and thirteen states. It is politically stable country. In development as well as

implementation of the foreign policies, this country pursues principles of neutrality and

peace. However, the only problem in this country that affects the operations of business is

corruption. It is major problem in the Malaysia. Since, “Dutch Lady Milk Industries Berhad”

is the biggest company entity in the Malaysia. Hence, any changes in the regulations and

policies as well as elections can affect the operations of company. Further, corruption is other

issue that will impact business operations of company as whole (Ishibashi et al. 2016).

Economic Factors

Chart 2: Consumer Products $ Services Index

PEST Analysis

Political Factors

Malaysia is the federal constitutional monarchy, which comprises of three federal

territories and thirteen states. It is politically stable country. In development as well as

implementation of the foreign policies, this country pursues principles of neutrality and

peace. However, the only problem in this country that affects the operations of business is

corruption. It is major problem in the Malaysia. Since, “Dutch Lady Milk Industries Berhad”

is the biggest company entity in the Malaysia. Hence, any changes in the regulations and

policies as well as elections can affect the operations of company. Further, corruption is other

issue that will impact business operations of company as whole (Ishibashi et al. 2016).

Economic Factors

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ACCOUNTING FINANCIAL ANALYSIS REPORT

The projections by IMF states that Malaysia is ranks 37 in global GDP ranking. The

GDP of Malaysia is $358,579 million in 2018 and GDP per capital in same year was around

$11,072 that was quite higher than the previous years. Malaysia is having robust, healthy and

industrialized economy. The rate of unemployment in this country has benefitted from the

adoption of the cutting-edge technology. This economy growth rate of country has helped the

company to operate with greater efficiency and expand their operations. This company

influenced purchasing power of the potential customers.

Social Factors

Malaysia is the diverse ethically and it has rich cultural life. In this county, people live

their life much more affluent lifestyle in comparison to its various other upper-middle income

countries. Further, factors that contributes to this includes system of social welfare, low cost

of household, food and fuel products, almost free system of health care. “Dutch Lady Milk

Industries Berhad” is leading and oldest brand in the Malaysia and people of this country

stick to this brand, since its establishment because of the faith in brand.

Technological factors

Malaysia is the most digitally connected country around the world. Approx. eighty

percent of the residents of this country have access to the internet, especially through the

mobile networks. This country has been great place for the international technology-oriented

entities. Malaysia aims to become favorite destination for the high-tech investment by the end

of 2025. “Dutch Lady Milk Industries Berhad” is adaptive to technology. The company is up-

to-date with the change in technology. Hence, change in technology will not affect the

operations of company (Kulikova and Satdarova 2016).

Financial Performance Analysis

Profitability Ratio

The projections by IMF states that Malaysia is ranks 37 in global GDP ranking. The

GDP of Malaysia is $358,579 million in 2018 and GDP per capital in same year was around

$11,072 that was quite higher than the previous years. Malaysia is having robust, healthy and

industrialized economy. The rate of unemployment in this country has benefitted from the

adoption of the cutting-edge technology. This economy growth rate of country has helped the

company to operate with greater efficiency and expand their operations. This company

influenced purchasing power of the potential customers.

Social Factors

Malaysia is the diverse ethically and it has rich cultural life. In this county, people live

their life much more affluent lifestyle in comparison to its various other upper-middle income

countries. Further, factors that contributes to this includes system of social welfare, low cost

of household, food and fuel products, almost free system of health care. “Dutch Lady Milk

Industries Berhad” is leading and oldest brand in the Malaysia and people of this country

stick to this brand, since its establishment because of the faith in brand.

Technological factors

Malaysia is the most digitally connected country around the world. Approx. eighty

percent of the residents of this country have access to the internet, especially through the

mobile networks. This country has been great place for the international technology-oriented

entities. Malaysia aims to become favorite destination for the high-tech investment by the end

of 2025. “Dutch Lady Milk Industries Berhad” is adaptive to technology. The company is up-

to-date with the change in technology. Hence, change in technology will not affect the

operations of company (Kulikova and Satdarova 2016).

Financial Performance Analysis

Profitability Ratio

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ACCOUNTING FINANCIAL ANALYSIS REPORT

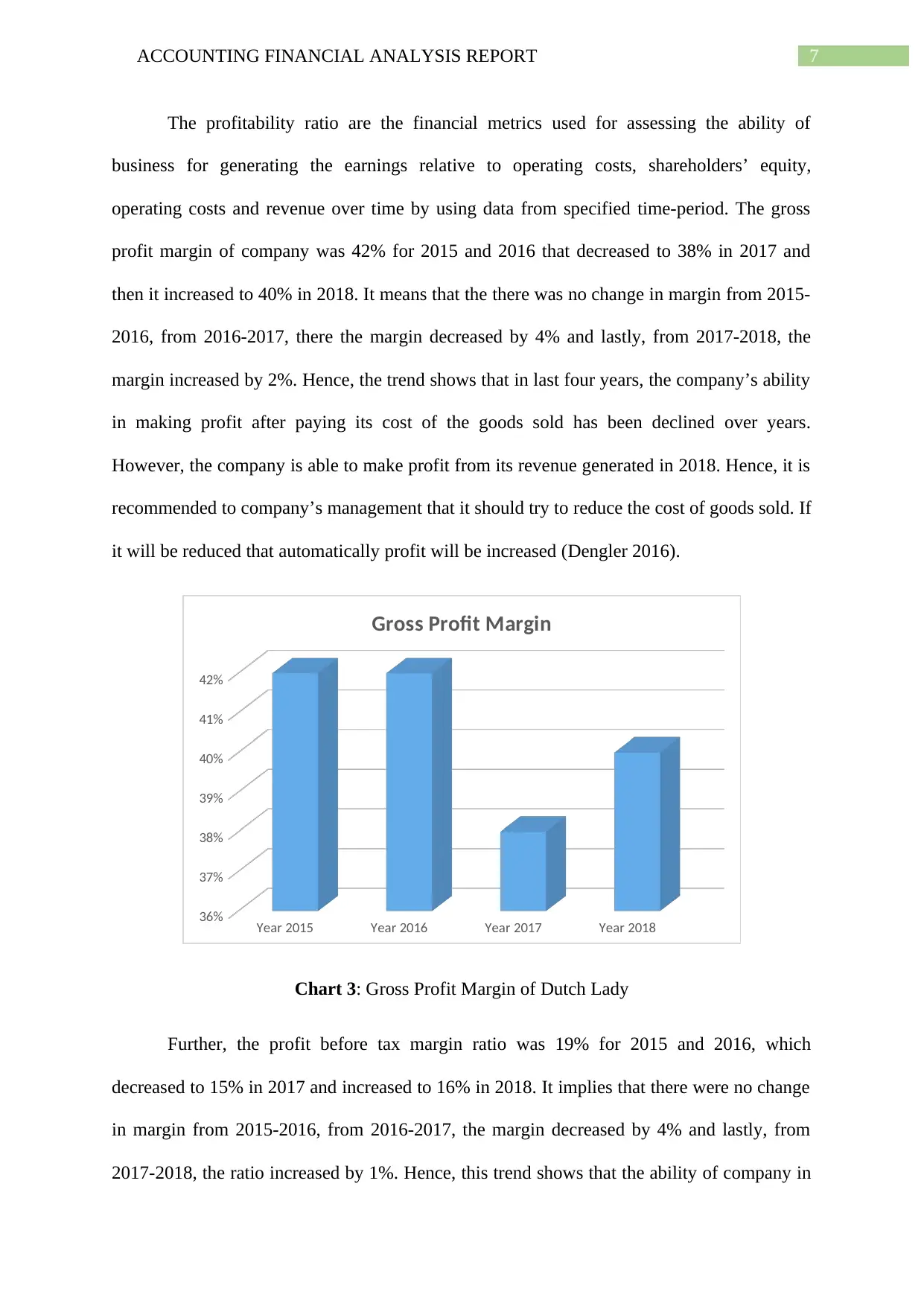

The profitability ratio are the financial metrics used for assessing the ability of

business for generating the earnings relative to operating costs, shareholders’ equity,

operating costs and revenue over time by using data from specified time-period. The gross

profit margin of company was 42% for 2015 and 2016 that decreased to 38% in 2017 and

then it increased to 40% in 2018. It means that the there was no change in margin from 2015-

2016, from 2016-2017, there the margin decreased by 4% and lastly, from 2017-2018, the

margin increased by 2%. Hence, the trend shows that in last four years, the company’s ability

in making profit after paying its cost of the goods sold has been declined over years.

However, the company is able to make profit from its revenue generated in 2018. Hence, it is

recommended to company’s management that it should try to reduce the cost of goods sold. If

it will be reduced that automatically profit will be increased (Dengler 2016).

Year 2015 Year 2016 Year 2017 Year 2018

36%

37%

38%

39%

40%

41%

42%

Gross Profit Margin

Chart 3: Gross Profit Margin of Dutch Lady

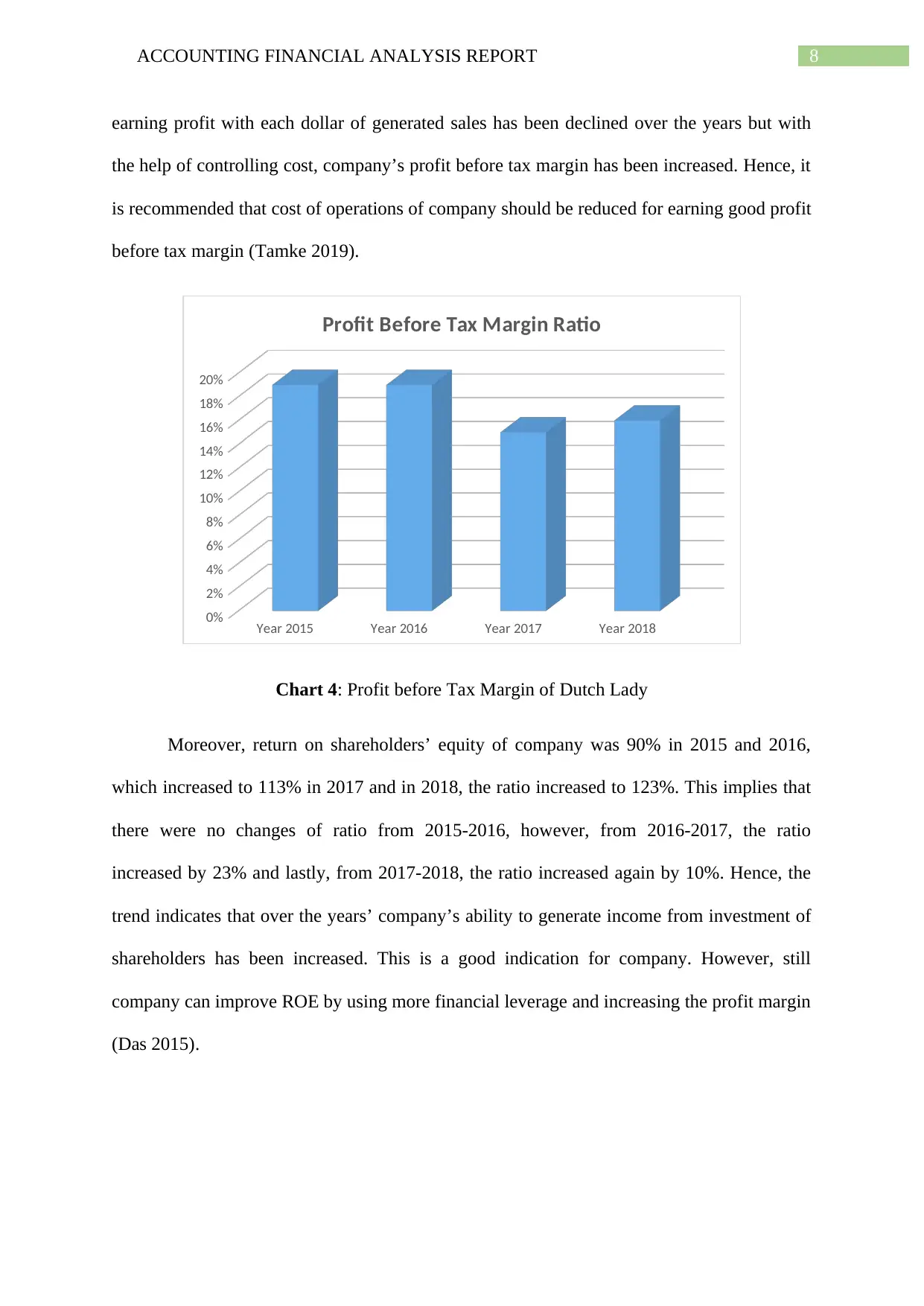

Further, the profit before tax margin ratio was 19% for 2015 and 2016, which

decreased to 15% in 2017 and increased to 16% in 2018. It implies that there were no change

in margin from 2015-2016, from 2016-2017, the margin decreased by 4% and lastly, from

2017-2018, the ratio increased by 1%. Hence, this trend shows that the ability of company in

The profitability ratio are the financial metrics used for assessing the ability of

business for generating the earnings relative to operating costs, shareholders’ equity,

operating costs and revenue over time by using data from specified time-period. The gross

profit margin of company was 42% for 2015 and 2016 that decreased to 38% in 2017 and

then it increased to 40% in 2018. It means that the there was no change in margin from 2015-

2016, from 2016-2017, there the margin decreased by 4% and lastly, from 2017-2018, the

margin increased by 2%. Hence, the trend shows that in last four years, the company’s ability

in making profit after paying its cost of the goods sold has been declined over years.

However, the company is able to make profit from its revenue generated in 2018. Hence, it is

recommended to company’s management that it should try to reduce the cost of goods sold. If

it will be reduced that automatically profit will be increased (Dengler 2016).

Year 2015 Year 2016 Year 2017 Year 2018

36%

37%

38%

39%

40%

41%

42%

Gross Profit Margin

Chart 3: Gross Profit Margin of Dutch Lady

Further, the profit before tax margin ratio was 19% for 2015 and 2016, which

decreased to 15% in 2017 and increased to 16% in 2018. It implies that there were no change

in margin from 2015-2016, from 2016-2017, the margin decreased by 4% and lastly, from

2017-2018, the ratio increased by 1%. Hence, this trend shows that the ability of company in

8ACCOUNTING FINANCIAL ANALYSIS REPORT

earning profit with each dollar of generated sales has been declined over the years but with

the help of controlling cost, company’s profit before tax margin has been increased. Hence, it

is recommended that cost of operations of company should be reduced for earning good profit

before tax margin (Tamke 2019).

Year 2015 Year 2016 Year 2017 Year 2018

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

Profit Before Tax Margin Ratio

Chart 4: Profit before Tax Margin of Dutch Lady

Moreover, return on shareholders’ equity of company was 90% in 2015 and 2016,

which increased to 113% in 2017 and in 2018, the ratio increased to 123%. This implies that

there were no changes of ratio from 2015-2016, however, from 2016-2017, the ratio

increased by 23% and lastly, from 2017-2018, the ratio increased again by 10%. Hence, the

trend indicates that over the years’ company’s ability to generate income from investment of

shareholders has been increased. This is a good indication for company. However, still

company can improve ROE by using more financial leverage and increasing the profit margin

(Das 2015).

earning profit with each dollar of generated sales has been declined over the years but with

the help of controlling cost, company’s profit before tax margin has been increased. Hence, it

is recommended that cost of operations of company should be reduced for earning good profit

before tax margin (Tamke 2019).

Year 2015 Year 2016 Year 2017 Year 2018

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

Profit Before Tax Margin Ratio

Chart 4: Profit before Tax Margin of Dutch Lady

Moreover, return on shareholders’ equity of company was 90% in 2015 and 2016,

which increased to 113% in 2017 and in 2018, the ratio increased to 123%. This implies that

there were no changes of ratio from 2015-2016, however, from 2016-2017, the ratio

increased by 23% and lastly, from 2017-2018, the ratio increased again by 10%. Hence, the

trend indicates that over the years’ company’s ability to generate income from investment of

shareholders has been increased. This is a good indication for company. However, still

company can improve ROE by using more financial leverage and increasing the profit margin

(Das 2015).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ACCOUNTING FINANCIAL ANALYSIS REPORT

Year 2015 Year 2016 Year 2017 Year 2018

0%

20%

40%

60%

80%

100%

120%

140%

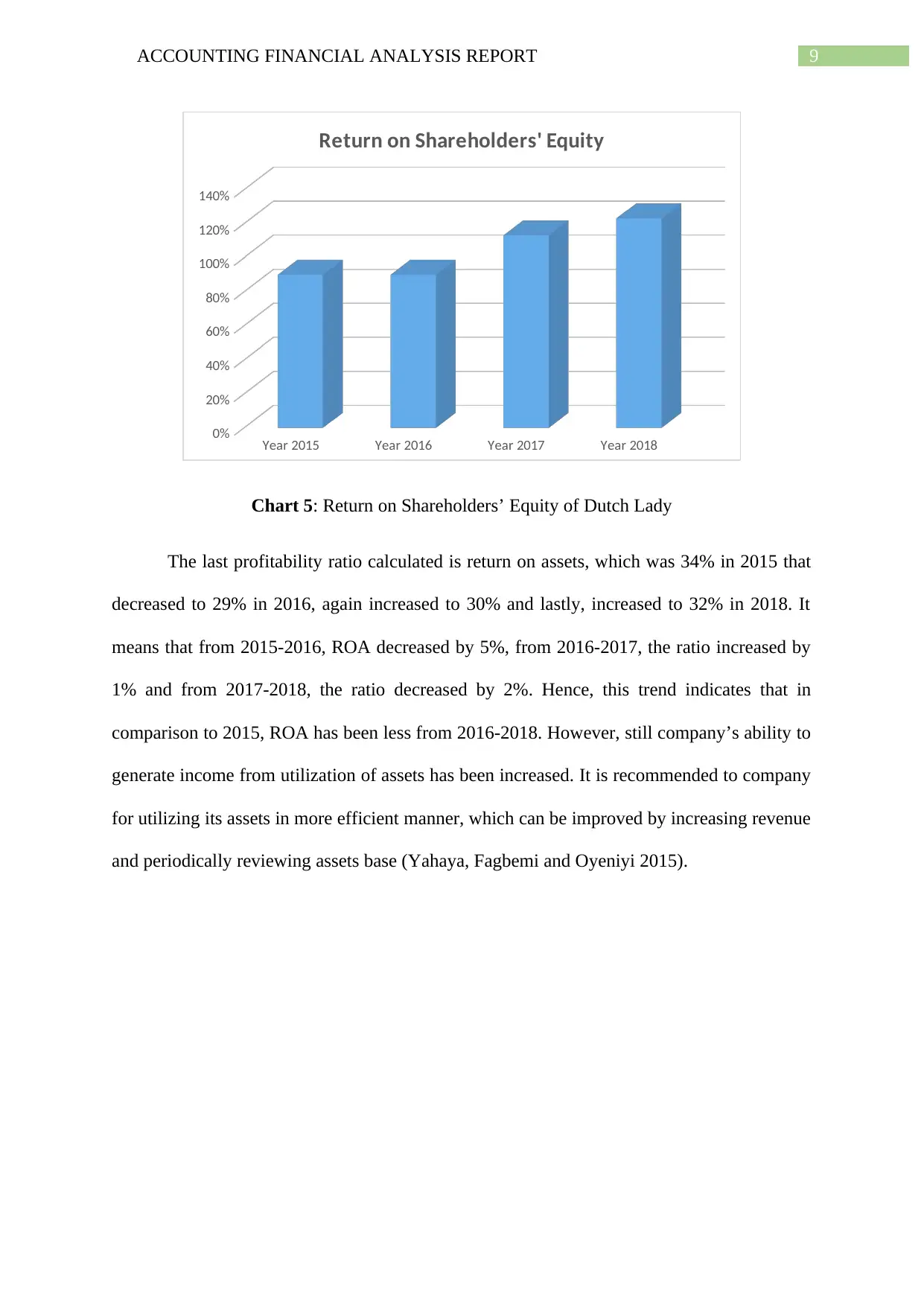

Return on Shareholders' Equity

Chart 5: Return on Shareholders’ Equity of Dutch Lady

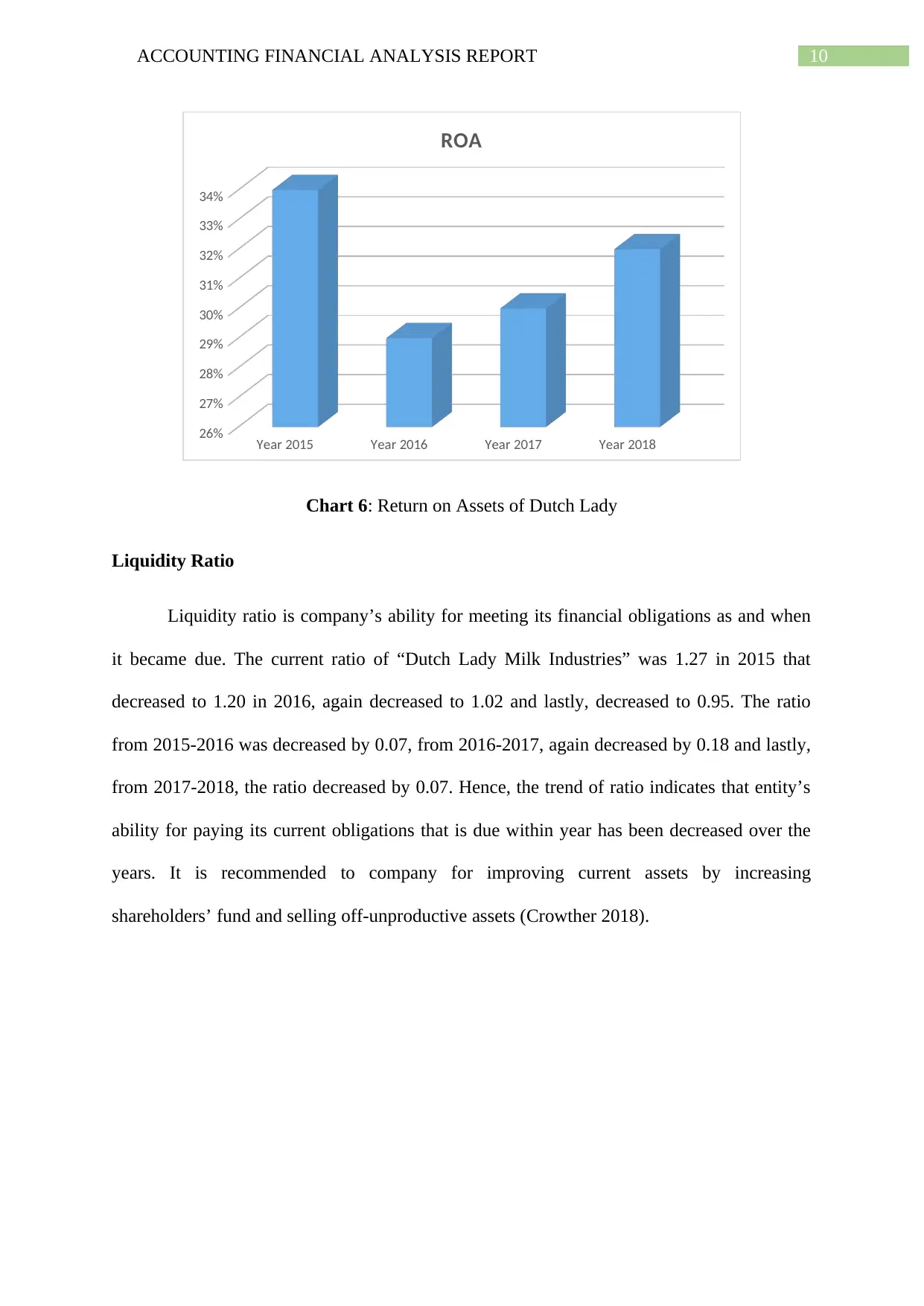

The last profitability ratio calculated is return on assets, which was 34% in 2015 that

decreased to 29% in 2016, again increased to 30% and lastly, increased to 32% in 2018. It

means that from 2015-2016, ROA decreased by 5%, from 2016-2017, the ratio increased by

1% and from 2017-2018, the ratio decreased by 2%. Hence, this trend indicates that in

comparison to 2015, ROA has been less from 2016-2018. However, still company’s ability to

generate income from utilization of assets has been increased. It is recommended to company

for utilizing its assets in more efficient manner, which can be improved by increasing revenue

and periodically reviewing assets base (Yahaya, Fagbemi and Oyeniyi 2015).

Year 2015 Year 2016 Year 2017 Year 2018

0%

20%

40%

60%

80%

100%

120%

140%

Return on Shareholders' Equity

Chart 5: Return on Shareholders’ Equity of Dutch Lady

The last profitability ratio calculated is return on assets, which was 34% in 2015 that

decreased to 29% in 2016, again increased to 30% and lastly, increased to 32% in 2018. It

means that from 2015-2016, ROA decreased by 5%, from 2016-2017, the ratio increased by

1% and from 2017-2018, the ratio decreased by 2%. Hence, this trend indicates that in

comparison to 2015, ROA has been less from 2016-2018. However, still company’s ability to

generate income from utilization of assets has been increased. It is recommended to company

for utilizing its assets in more efficient manner, which can be improved by increasing revenue

and periodically reviewing assets base (Yahaya, Fagbemi and Oyeniyi 2015).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10ACCOUNTING FINANCIAL ANALYSIS REPORT

Year 2015 Year 2016 Year 2017 Year 2018

26%

27%

28%

29%

30%

31%

32%

33%

34%

ROA

Chart 6: Return on Assets of Dutch Lady

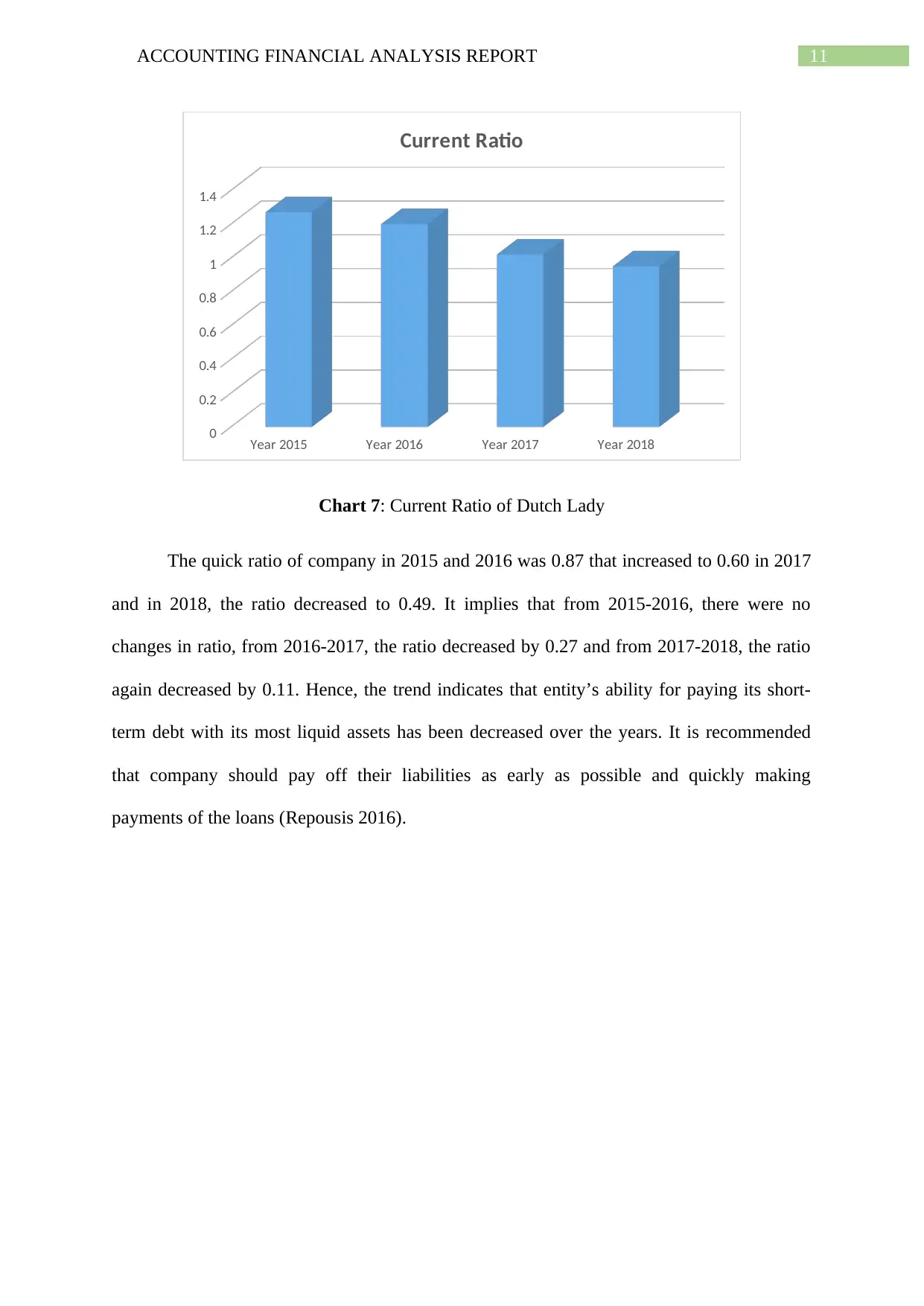

Liquidity Ratio

Liquidity ratio is company’s ability for meeting its financial obligations as and when

it became due. The current ratio of “Dutch Lady Milk Industries” was 1.27 in 2015 that

decreased to 1.20 in 2016, again decreased to 1.02 and lastly, decreased to 0.95. The ratio

from 2015-2016 was decreased by 0.07, from 2016-2017, again decreased by 0.18 and lastly,

from 2017-2018, the ratio decreased by 0.07. Hence, the trend of ratio indicates that entity’s

ability for paying its current obligations that is due within year has been decreased over the

years. It is recommended to company for improving current assets by increasing

shareholders’ fund and selling off-unproductive assets (Crowther 2018).

Year 2015 Year 2016 Year 2017 Year 2018

26%

27%

28%

29%

30%

31%

32%

33%

34%

ROA

Chart 6: Return on Assets of Dutch Lady

Liquidity Ratio

Liquidity ratio is company’s ability for meeting its financial obligations as and when

it became due. The current ratio of “Dutch Lady Milk Industries” was 1.27 in 2015 that

decreased to 1.20 in 2016, again decreased to 1.02 and lastly, decreased to 0.95. The ratio

from 2015-2016 was decreased by 0.07, from 2016-2017, again decreased by 0.18 and lastly,

from 2017-2018, the ratio decreased by 0.07. Hence, the trend of ratio indicates that entity’s

ability for paying its current obligations that is due within year has been decreased over the

years. It is recommended to company for improving current assets by increasing

shareholders’ fund and selling off-unproductive assets (Crowther 2018).

11ACCOUNTING FINANCIAL ANALYSIS REPORT

Year 2015 Year 2016 Year 2017 Year 2018

0

0.2

0.4

0.6

0.8

1

1.2

1.4

Current Ratio

Chart 7: Current Ratio of Dutch Lady

The quick ratio of company in 2015 and 2016 was 0.87 that increased to 0.60 in 2017

and in 2018, the ratio decreased to 0.49. It implies that from 2015-2016, there were no

changes in ratio, from 2016-2017, the ratio decreased by 0.27 and from 2017-2018, the ratio

again decreased by 0.11. Hence, the trend indicates that entity’s ability for paying its short-

term debt with its most liquid assets has been decreased over the years. It is recommended

that company should pay off their liabilities as early as possible and quickly making

payments of the loans (Repousis 2016).

Year 2015 Year 2016 Year 2017 Year 2018

0

0.2

0.4

0.6

0.8

1

1.2

1.4

Current Ratio

Chart 7: Current Ratio of Dutch Lady

The quick ratio of company in 2015 and 2016 was 0.87 that increased to 0.60 in 2017

and in 2018, the ratio decreased to 0.49. It implies that from 2015-2016, there were no

changes in ratio, from 2016-2017, the ratio decreased by 0.27 and from 2017-2018, the ratio

again decreased by 0.11. Hence, the trend indicates that entity’s ability for paying its short-

term debt with its most liquid assets has been decreased over the years. It is recommended

that company should pay off their liabilities as early as possible and quickly making

payments of the loans (Repousis 2016).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 25

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.