In-Depth Financial Analysis: Perpetual Limited & Platinum Asset Ltd

VerifiedAdded on 2023/06/03

|18

|3802

|155

Report

AI Summary

This report presents a comprehensive financial analysis of Perpetual Limited and Platinum Asset Limited, two Australian companies, utilizing financial data from their 2016 and 2017 annual reports. It begins with company descriptions, highlighting core activities and competitive advantages. Subsequently, it evaluates financial performance through key ratios, including liquidity, solvency, efficiency, profitability, and market value ratios, to assess their financial positions. The analysis extends to share price movements against market indices like the ASX S&P 200, determining stock volatility and market dependence. The Constant Dividend Growth Rate model is applied to estimate future stock values, comparing them with current prices for informed conclusions. Ultimately, the report provides a recommendation and conclusion, identifying the financially healthier and better-performing company.

RUNNING HEAD: FINANCIAL ANALYSIS

Financial Analysis

Financial Analysis

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial analysis 2

Contents

Introduction.................................................................................................................................................3

Description of the companies......................................................................................................................3

Perpetual Limited....................................................................................................................................3

Platinum Asset Limited...........................................................................................................................4

Calculation and analysis of performance ratios...........................................................................................4

Short term solvency.................................................................................................................................4

Long term solvency.................................................................................................................................6

Asset utilization.......................................................................................................................................8

Profitability ratios....................................................................................................................................9

Market value ratios................................................................................................................................11

Graphs and comparison of share price movements....................................................................................12

Share valuation..........................................................................................................................................14

Recommendation.......................................................................................................................................15

Conclusion.................................................................................................................................................16

References.................................................................................................................................................17

Contents

Introduction.................................................................................................................................................3

Description of the companies......................................................................................................................3

Perpetual Limited....................................................................................................................................3

Platinum Asset Limited...........................................................................................................................4

Calculation and analysis of performance ratios...........................................................................................4

Short term solvency.................................................................................................................................4

Long term solvency.................................................................................................................................6

Asset utilization.......................................................................................................................................8

Profitability ratios....................................................................................................................................9

Market value ratios................................................................................................................................11

Graphs and comparison of share price movements....................................................................................12

Share valuation..........................................................................................................................................14

Recommendation.......................................................................................................................................15

Conclusion.................................................................................................................................................16

References.................................................................................................................................................17

Financial analysis 3

Introduction

The report provides overall financial analysis of the two Australian companies named as

Perpetual Limited and Platinum Asset limited. It measures the performance and position of both

the companies from all the aspects covering the financial data presented in their annual reports

for the past two years. The report commences with a brief introduction about the entities and

their core activities. It also reports about the competitive advantage of both the firms. Further, the

financial performance of both entities has been measured by calculating the performance ratios

including liquidity, solvency, efficiency, profitability and market based ratios. All these are

financial metrics which evaluates the position of the organizations over the past two years that

are 2016 and 2017.

Later on, the fluctuations in the share price movements of both the firms is analysed against the

fluctuations in the market indices. The variations are compared against the changes in ASX S&P

200 and it is observed that whether the stock is volatile or not and highly dependent on market or

not. The report also explains Constant Dividend Growth Rate model which is used to calculate

the future value of stock. The determined value is then compared with the current share price of

the company’s stock and conclusions are been made. In the last, a recommendation and

conclusion is provided suggesting that which company is financially healthy and is performing

better than the other.

Introduction

The report provides overall financial analysis of the two Australian companies named as

Perpetual Limited and Platinum Asset limited. It measures the performance and position of both

the companies from all the aspects covering the financial data presented in their annual reports

for the past two years. The report commences with a brief introduction about the entities and

their core activities. It also reports about the competitive advantage of both the firms. Further, the

financial performance of both entities has been measured by calculating the performance ratios

including liquidity, solvency, efficiency, profitability and market based ratios. All these are

financial metrics which evaluates the position of the organizations over the past two years that

are 2016 and 2017.

Later on, the fluctuations in the share price movements of both the firms is analysed against the

fluctuations in the market indices. The variations are compared against the changes in ASX S&P

200 and it is observed that whether the stock is volatile or not and highly dependent on market or

not. The report also explains Constant Dividend Growth Rate model which is used to calculate

the future value of stock. The determined value is then compared with the current share price of

the company’s stock and conclusions are been made. In the last, a recommendation and

conclusion is provided suggesting that which company is financially healthy and is performing

better than the other.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial analysis 4

Description of the companies

Perpetual Limited

It is an Australian company that offers wide range of financial services and products across the

country. It provides services like portfolio management, financial planning, trustee, funds

management, investment administration and custodian services and others. In addition, the

company offers various investments across the range of asset classes that include cash and fixed

interest, mortgages, Australian and global equities and Australian listed property. Apart from

this, it also provides trust advices and fiduciary advices to its clients. The competitive advantage

of the business is that it has declared high profitability recently and its divisions have reported

high growth in revenue. The company does not pursue any sort of competitive advantage but has

enjoyed success and growth in the business as per the latest annual report (Bloomberg. 2018).

Platinum Asset Limited

Formerly the company is known as Platinum Investment Management Limited engaged in the

business of the funds management. Platinum manages approximately AUD 22 billion with over

7% of this from investors in Europe, America, New Zealand and Asia. It offers investment

management services to its party units named as Platinum Trust Funds and Platinum Global

Fund, its two Australian investment companies listed on ASX and Platinum World Portfolios

Plc. The product range offered by PTM is on global, regional and sector level for the purpose of

investment. The competitive advantage of PTM is that it has expertise in investing in the

international equities. The company deals with all the challenges and threats in a manner that it

can maintain its competitive advantage to a certain extent. It formulates its strategies in a way

that will safeguard its competitive edge (Reuters. 2018).

Description of the companies

Perpetual Limited

It is an Australian company that offers wide range of financial services and products across the

country. It provides services like portfolio management, financial planning, trustee, funds

management, investment administration and custodian services and others. In addition, the

company offers various investments across the range of asset classes that include cash and fixed

interest, mortgages, Australian and global equities and Australian listed property. Apart from

this, it also provides trust advices and fiduciary advices to its clients. The competitive advantage

of the business is that it has declared high profitability recently and its divisions have reported

high growth in revenue. The company does not pursue any sort of competitive advantage but has

enjoyed success and growth in the business as per the latest annual report (Bloomberg. 2018).

Platinum Asset Limited

Formerly the company is known as Platinum Investment Management Limited engaged in the

business of the funds management. Platinum manages approximately AUD 22 billion with over

7% of this from investors in Europe, America, New Zealand and Asia. It offers investment

management services to its party units named as Platinum Trust Funds and Platinum Global

Fund, its two Australian investment companies listed on ASX and Platinum World Portfolios

Plc. The product range offered by PTM is on global, regional and sector level for the purpose of

investment. The competitive advantage of PTM is that it has expertise in investing in the

international equities. The company deals with all the challenges and threats in a manner that it

can maintain its competitive advantage to a certain extent. It formulates its strategies in a way

that will safeguard its competitive edge (Reuters. 2018).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial analysis 5

Calculation and analysis of performance ratios

Short term solvency

Current ratio: It is a financial metric which measures the financial health of the

company by comparing its current assets against the current liabilities. The ideal ratio is

2:1 which is required to be maintained by every company. it reflects that the firm has its

CAs double of its current liabilities (Godwin and Alderman, 2012).

PPT PTM

Current ratio 2016 2017 2016 2017

Current assets (A) 678209.0 716668.0 384695.0 351137.0

Current liabilities

(B) 411,798.0 402,397.0 21,918.0 17,382.0

CR (A/B) 1.65

1.7

8 17.55 20.20

The above table shows the CR of both Perpetual and Platinum Assets for the past two years 2016

and 2017. It can be observed that PPT has maintained the ratio of 1.65 in 2016 and 1.78 in 2017.

On the other side, PTM has the ratio of 17.55 and 20.20 in both the years respectively. The

reason for having such a high ratio was the low current liabilities of PTM. The company does not

report any sort of short term debt borrowings and its payables has also decreased in 2017 as

compare to the prior year. In case of Perpetual Limited, most part of the CLs is covered by firm’s

EMCF Liabilities which reduced from $299971 million to $276954 million which boosted up the

ratio.

Calculation and analysis of performance ratios

Short term solvency

Current ratio: It is a financial metric which measures the financial health of the

company by comparing its current assets against the current liabilities. The ideal ratio is

2:1 which is required to be maintained by every company. it reflects that the firm has its

CAs double of its current liabilities (Godwin and Alderman, 2012).

PPT PTM

Current ratio 2016 2017 2016 2017

Current assets (A) 678209.0 716668.0 384695.0 351137.0

Current liabilities

(B) 411,798.0 402,397.0 21,918.0 17,382.0

CR (A/B) 1.65

1.7

8 17.55 20.20

The above table shows the CR of both Perpetual and Platinum Assets for the past two years 2016

and 2017. It can be observed that PPT has maintained the ratio of 1.65 in 2016 and 1.78 in 2017.

On the other side, PTM has the ratio of 17.55 and 20.20 in both the years respectively. The

reason for having such a high ratio was the low current liabilities of PTM. The company does not

report any sort of short term debt borrowings and its payables has also decreased in 2017 as

compare to the prior year. In case of Perpetual Limited, most part of the CLs is covered by firm’s

EMCF Liabilities which reduced from $299971 million to $276954 million which boosted up the

ratio.

Financial analysis 6

Quick ratio: it also measures the liquidity position of the firm by taking into account the

quick assets of the firm. The ideal ratio is 1:1 which means the most liquid assets of the

firm should be equal to its current liabilities (Saleem and Rehman, 2011).

PPT PTM

Quick ratio 2016 2017 2016 2017

Quick Assets (A) 678209.0 716668.0

384695.

0 351137.0

Current Liabilities

(B) 411,798.0 402,397.0 21918.0 17382.0

QR (A/B) 1.65 1.78 17.6 20.2

The QR of both the companies is same as their current ratio because they do not have any sort of

inventories due to the nature of business they undertake. Being a financial service provider

company, the annual reports of both the firms did not report any inventory amount in the last two

years.

Long term solvency

Debt/Equity ratio: it is financial metric which measures the long term solvency position

of the company by comparing its debt and equity portion against each other. The ratio

reflected the amount of firm’s resources funded by debt against the portion of assets

which is funded by equity. A high D/E ratio is not favourable for the company as it shows

that the company relies more on outside borrowings and have high financial risk

(Higgins, 2012).

PPT PTM

Quick ratio: it also measures the liquidity position of the firm by taking into account the

quick assets of the firm. The ideal ratio is 1:1 which means the most liquid assets of the

firm should be equal to its current liabilities (Saleem and Rehman, 2011).

PPT PTM

Quick ratio 2016 2017 2016 2017

Quick Assets (A) 678209.0 716668.0

384695.

0 351137.0

Current Liabilities

(B) 411,798.0 402,397.0 21918.0 17382.0

QR (A/B) 1.65 1.78 17.6 20.2

The QR of both the companies is same as their current ratio because they do not have any sort of

inventories due to the nature of business they undertake. Being a financial service provider

company, the annual reports of both the firms did not report any inventory amount in the last two

years.

Long term solvency

Debt/Equity ratio: it is financial metric which measures the long term solvency position

of the company by comparing its debt and equity portion against each other. The ratio

reflected the amount of firm’s resources funded by debt against the portion of assets

which is funded by equity. A high D/E ratio is not favourable for the company as it shows

that the company relies more on outside borrowings and have high financial risk

(Higgins, 2012).

PPT PTM

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial analysis 7

Debt to equity 2016 2017 2016 2017

Total debt (A) 87000.0 87000.0 23112.0 18892.0

Shareholder's equity (B) 605519.0 634381.0 364211.0 335074.0

D/E (A/B) 14.37% 13.71% 6.35% 5.64%

Perpetual Limited has reported a decreased D/E ratio but higher than PTM. Its ratio was 14.37%

in 2016 which declined to 13.71% in 2017. The reason for such reduction was that company’s

long term borrowing remain same in the both the years at $87000 million. In relation to that its

shareholder’s equity increases during the year which eventually brings down the ratio. In case of

PTM, the ratio reduces from 6.35% to 5.64% due to the overall reduction in its liabilities.

Moreover, the company does not have any sort of long term borrowings in past years. This

ultimately reduces the content of its financial leverage.

Debt ratio: it is a solvency ratio which measures the total liabilities and total assets of the

firm against each other. It shows the degree of financial leverage taken by the company

during a particular financial year. In other words, it reflects the amount of firm’s assets

which are financed through debt (Jenter and Lewellen, 2015).

PPT PTM

Debt ratio 2016 2017 2016 2017

Total Liabilities

(A) 547790.0 537164.0 23112.0 18892.0

Total Assets (B) 1,153,309.0 1,171,545.0 387,323.0 353,966.0

DR (A/B) 47.5% 45.9% 5.97% 5.34%

Debt to equity 2016 2017 2016 2017

Total debt (A) 87000.0 87000.0 23112.0 18892.0

Shareholder's equity (B) 605519.0 634381.0 364211.0 335074.0

D/E (A/B) 14.37% 13.71% 6.35% 5.64%

Perpetual Limited has reported a decreased D/E ratio but higher than PTM. Its ratio was 14.37%

in 2016 which declined to 13.71% in 2017. The reason for such reduction was that company’s

long term borrowing remain same in the both the years at $87000 million. In relation to that its

shareholder’s equity increases during the year which eventually brings down the ratio. In case of

PTM, the ratio reduces from 6.35% to 5.64% due to the overall reduction in its liabilities.

Moreover, the company does not have any sort of long term borrowings in past years. This

ultimately reduces the content of its financial leverage.

Debt ratio: it is a solvency ratio which measures the total liabilities and total assets of the

firm against each other. It shows the degree of financial leverage taken by the company

during a particular financial year. In other words, it reflects the amount of firm’s assets

which are financed through debt (Jenter and Lewellen, 2015).

PPT PTM

Debt ratio 2016 2017 2016 2017

Total Liabilities

(A) 547790.0 537164.0 23112.0 18892.0

Total Assets (B) 1,153,309.0 1,171,545.0 387,323.0 353,966.0

DR (A/B) 47.5% 45.9% 5.97% 5.34%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial analysis 8

Similar trends have been noticed in the debt ratio of both the companies as they reported an

overall decline in the same. In case of PPT, the DR reduced from 47.5% to 45.9% due to the

proportionate decrease in company’s liabilities and increase in its total assets. Comparatively,

PTM’s Dr is less than that of PPT because of the low liabilities. The major part of company’s

total obligations is covered by its accounts payable and income tax payable which has been

significantly reduced in 2017 as compare to 2016.

Asset utilization

Debtor turnover ratio: It is an efficiency ratio which shows determines the capability of

the company in collecting its debtors effectively and on time in order to generate high

turnover. A high DTR shows that company is converting its receivables into cash quickly

and is contributing ti high turnover (Kimmel, Weygandt and Kieso, 2010).

PPT PTM

Receivable turnover ratio 2016 2017 2016 2017

Total revenue (A) 507729.0 520881.0 337894.0 312468.0

Average receivables (B) 88,156.0 92,232.0 29,900.0 30,049.5

DTR (A/B) 5.76 5.65 11.30 10.40

The DTR of PPT has reduced from 5.76 times to 5.65 times which reflects that company is not

efficient enough to generate revenue from its receivables. Moreover, the increase in amount of its

debtors has reduced the ratio in last year. On the other hand, PTM has high DTR but it has also

been reduced in 2017 to 10.40 times from 11.30 times. Comparatively, fewer amounts of cash is

hold by PTM’s debtors.

Similar trends have been noticed in the debt ratio of both the companies as they reported an

overall decline in the same. In case of PPT, the DR reduced from 47.5% to 45.9% due to the

proportionate decrease in company’s liabilities and increase in its total assets. Comparatively,

PTM’s Dr is less than that of PPT because of the low liabilities. The major part of company’s

total obligations is covered by its accounts payable and income tax payable which has been

significantly reduced in 2017 as compare to 2016.

Asset utilization

Debtor turnover ratio: It is an efficiency ratio which shows determines the capability of

the company in collecting its debtors effectively and on time in order to generate high

turnover. A high DTR shows that company is converting its receivables into cash quickly

and is contributing ti high turnover (Kimmel, Weygandt and Kieso, 2010).

PPT PTM

Receivable turnover ratio 2016 2017 2016 2017

Total revenue (A) 507729.0 520881.0 337894.0 312468.0

Average receivables (B) 88,156.0 92,232.0 29,900.0 30,049.5

DTR (A/B) 5.76 5.65 11.30 10.40

The DTR of PPT has reduced from 5.76 times to 5.65 times which reflects that company is not

efficient enough to generate revenue from its receivables. Moreover, the increase in amount of its

debtors has reduced the ratio in last year. On the other hand, PTM has high DTR but it has also

been reduced in 2017 to 10.40 times from 11.30 times. Comparatively, fewer amounts of cash is

hold by PTM’s debtors.

Financial analysis 9

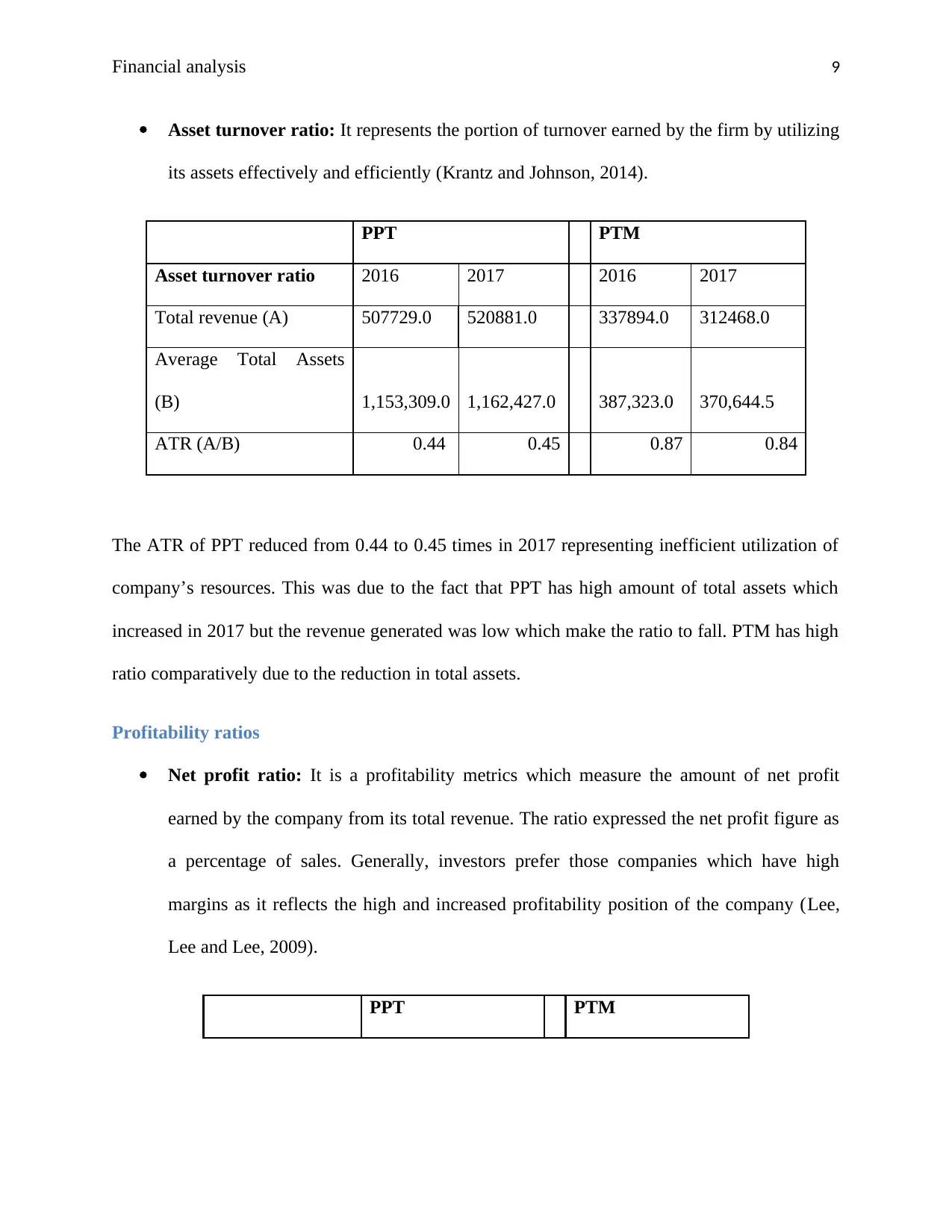

Asset turnover ratio: It represents the portion of turnover earned by the firm by utilizing

its assets effectively and efficiently (Krantz and Johnson, 2014).

PPT PTM

Asset turnover ratio 2016 2017 2016 2017

Total revenue (A) 507729.0 520881.0 337894.0 312468.0

Average Total Assets

(B) 1,153,309.0 1,162,427.0 387,323.0 370,644.5

ATR (A/B) 0.44 0.45 0.87 0.84

The ATR of PPT reduced from 0.44 to 0.45 times in 2017 representing inefficient utilization of

company’s resources. This was due to the fact that PPT has high amount of total assets which

increased in 2017 but the revenue generated was low which make the ratio to fall. PTM has high

ratio comparatively due to the reduction in total assets.

Profitability ratios

Net profit ratio: It is a profitability metrics which measure the amount of net profit

earned by the company from its total revenue. The ratio expressed the net profit figure as

a percentage of sales. Generally, investors prefer those companies which have high

margins as it reflects the high and increased profitability position of the company (Lee,

Lee and Lee, 2009).

PPT PTM

Asset turnover ratio: It represents the portion of turnover earned by the firm by utilizing

its assets effectively and efficiently (Krantz and Johnson, 2014).

PPT PTM

Asset turnover ratio 2016 2017 2016 2017

Total revenue (A) 507729.0 520881.0 337894.0 312468.0

Average Total Assets

(B) 1,153,309.0 1,162,427.0 387,323.0 370,644.5

ATR (A/B) 0.44 0.45 0.87 0.84

The ATR of PPT reduced from 0.44 to 0.45 times in 2017 representing inefficient utilization of

company’s resources. This was due to the fact that PPT has high amount of total assets which

increased in 2017 but the revenue generated was low which make the ratio to fall. PTM has high

ratio comparatively due to the reduction in total assets.

Profitability ratios

Net profit ratio: It is a profitability metrics which measure the amount of net profit

earned by the company from its total revenue. The ratio expressed the net profit figure as

a percentage of sales. Generally, investors prefer those companies which have high

margins as it reflects the high and increased profitability position of the company (Lee,

Lee and Lee, 2009).

PPT PTM

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial analysis 10

Net profit

margin 2016 2017 2016 2017

Net profit (A) 132005.0 137293.0 199870.0 192647.0

Total revenue (B) 507,729.0 520,881.0 337,894.0 312,468.0

NPR (A/B) 26.00% 26.36% 59.15% 61.65%

The above table shows that PPT has net margin of 26% in 2016 which slightly increased to

26.36% in 2017. Such upsurge was due to the slightest increase in the net profit of the company

as compare to the upsurge in its total revenue. On the other hand, PPT reported high and

increased NPR of 59.15% and 61.65% in last two years respectively. This was due to the

proportionate reduction in both the turnover and profit of PTM which eventually increased its

NPR.

Return on Assets: It shows the amount of returns made by the company on its total

assets. a high ROA reflects that high amount of profit is generated by utilizing its assets

(Nikolai, Bazley and Jones, 2009)..

PPT PTM

Return on Assets 2016 2017 2016 2017

Net profit (A) 132005.0 137293.0 199870.0 192647.0

Total Assets (B) 1,153,309.0

1,171,545.

0 387,323.0 353,966.0

ROA (A/B) 11.45% 11.72% 51.60% 54.43%

Net profit

margin 2016 2017 2016 2017

Net profit (A) 132005.0 137293.0 199870.0 192647.0

Total revenue (B) 507,729.0 520,881.0 337,894.0 312,468.0

NPR (A/B) 26.00% 26.36% 59.15% 61.65%

The above table shows that PPT has net margin of 26% in 2016 which slightly increased to

26.36% in 2017. Such upsurge was due to the slightest increase in the net profit of the company

as compare to the upsurge in its total revenue. On the other hand, PPT reported high and

increased NPR of 59.15% and 61.65% in last two years respectively. This was due to the

proportionate reduction in both the turnover and profit of PTM which eventually increased its

NPR.

Return on Assets: It shows the amount of returns made by the company on its total

assets. a high ROA reflects that high amount of profit is generated by utilizing its assets

(Nikolai, Bazley and Jones, 2009)..

PPT PTM

Return on Assets 2016 2017 2016 2017

Net profit (A) 132005.0 137293.0 199870.0 192647.0

Total Assets (B) 1,153,309.0

1,171,545.

0 387,323.0 353,966.0

ROA (A/B) 11.45% 11.72% 51.60% 54.43%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial analysis 11

The ROA of PPT has increased from 11.45% to 11.72% due to the significant increase in

company’s profit. However, the ratio was less than the ROA of PTM as it is has low total assets

as compare to the PPT. Reduction in company’s assets boosted up the ratio from 51.60% to

54.43%. The proportionate decrease in PTM assets and profit eventually boosted up the ratio.

Return on Equity: The ratio determines the amount of return offered by the company to

its investors on the portion of their share capital invested in the firm.

PPT PTM

Return on Equity 2016 2017 2016 2017

Net income available to shareholders (A) 132005.0 137293.0 199870.0 192647.0

Shareholder's equity (B) 605,519.0 634,381.0 364,211.0 335,074.0

ROE (A/B) 21.80% 21.64% 54.88% 57.49%

The ROE of PPT has reduced from 21.80% to 21.64% due to the increase in its equity and profits

at the same time. This reflects that company is not able to offer high returns to its investors as its

shareholders have also increased at the same time. On the other hand, the ROE of PTM was

54.88% to 57.49%. The reduction was due to the overall fall in company’s net income which

ultimately reduced its shareholders’ equity.

Market value ratios

Earnings per share: It shows the amount of earnings earned by each outstanding share

of the company. It is an indicator of company’s profitability (Vogel, 2014).

PPT PTM

Earnings per share 2016 2017 2016 2017

The ROA of PPT has increased from 11.45% to 11.72% due to the significant increase in

company’s profit. However, the ratio was less than the ROA of PTM as it is has low total assets

as compare to the PPT. Reduction in company’s assets boosted up the ratio from 51.60% to

54.43%. The proportionate decrease in PTM assets and profit eventually boosted up the ratio.

Return on Equity: The ratio determines the amount of return offered by the company to

its investors on the portion of their share capital invested in the firm.

PPT PTM

Return on Equity 2016 2017 2016 2017

Net income available to shareholders (A) 132005.0 137293.0 199870.0 192647.0

Shareholder's equity (B) 605,519.0 634,381.0 364,211.0 335,074.0

ROE (A/B) 21.80% 21.64% 54.88% 57.49%

The ROE of PPT has reduced from 21.80% to 21.64% due to the increase in its equity and profits

at the same time. This reflects that company is not able to offer high returns to its investors as its

shareholders have also increased at the same time. On the other hand, the ROE of PTM was

54.88% to 57.49%. The reduction was due to the overall fall in company’s net income which

ultimately reduced its shareholders’ equity.

Market value ratios

Earnings per share: It shows the amount of earnings earned by each outstanding share

of the company. It is an indicator of company’s profitability (Vogel, 2014).

PPT PTM

Earnings per share 2016 2017 2016 2017

Financial analysis 12

Net income available to shareholders

(A) 132005.0 137293.0 199870.0 192647.0

Number of outstanding shares (A) 46,431.0 46,706.0 58,610.0 58,712.0

EPS (A/B)

2.84

3

2.9

4

3.4

1

3.2

8

The EPS of PTM was higher than the EPS of PPT due to the high number of shares issued by the

company. This shows that the firm is focused on increasing its profitability and its stocks are

performing well in the market.

Price earnings ratio: It is also known as price multiple and shows the willingness of the

investors in paying for each dollar of earnings.

PPT PTM

Price earning ratio 2016 2017 2016 2017

Market value per share (A) 41.12 55.87 17.4 24.2

Earnings per share (B) 2.843 2.9 3.41 3.28

P/E (A/B)

14.463

4 19.0065 5.10 7.37

The P/E ratio of PPT was more than the ratio of PTM which reflects that investors will

expect growth in company’s share in future and it will be considered as more desirable.

Net income available to shareholders

(A) 132005.0 137293.0 199870.0 192647.0

Number of outstanding shares (A) 46,431.0 46,706.0 58,610.0 58,712.0

EPS (A/B)

2.84

3

2.9

4

3.4

1

3.2

8

The EPS of PTM was higher than the EPS of PPT due to the high number of shares issued by the

company. This shows that the firm is focused on increasing its profitability and its stocks are

performing well in the market.

Price earnings ratio: It is also known as price multiple and shows the willingness of the

investors in paying for each dollar of earnings.

PPT PTM

Price earning ratio 2016 2017 2016 2017

Market value per share (A) 41.12 55.87 17.4 24.2

Earnings per share (B) 2.843 2.9 3.41 3.28

P/E (A/B)

14.463

4 19.0065 5.10 7.37

The P/E ratio of PPT was more than the ratio of PTM which reflects that investors will

expect growth in company’s share in future and it will be considered as more desirable.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.