Financial Analysis of Portfolio Companies: 2015-2016 Performance

VerifiedAdded on 2020/04/13

Financial Analysis of the Portfolio

Paraphrase This Document

Contents

Introduction......................................................................................................................................3

Portfolio 1........................................................................................................................................3

Calculation of Financial Ratio of both the companies (2015 and 2016) and Analyzing the

Performance, Financial Position and Investment Potential of both Companies..............................4

Different Ratios and their graphs.....................................................................................................5

Further Research on the performance of both companies.............................................................13

Recommendations..........................................................................................................................14

Limitations of Relying on Financial Ratios to Interpret Firm Performance..................................14

Portfolio 2: Capital investment appraisal......................................................................................15

Part A: Payback, Account rate of return and NPV........................................................................15

Payback Period..............................................................................................................................15

Accounting Rate of Return............................................................................................................16

Net Present Value..........................................................................................................................17

Part B: Limitations of using investment appraisal techniques to aid long-term decision-making 18

Conclusion.....................................................................................................................................19

References......................................................................................................................................20

Introduction

The present report is developed for providing an understanding of the accounting and

finance techniques that can be used by the investors for analyzing the financial performance of a

company. In this context, the report aims to construct two portfolios for the investors to aid their

decision-making processes by analyzing the financial performance of the companies. The first

portfolio is developed to present an analysis of the financial information of the two companies,

that are, Sports Direct International PLC and JD Sports Fashion PLC on the perspective of the

financial manger of Madhouse Retail Ltd. The analysis is aimed to assist the financial director of

the company for buying shares of the two companies. The evaluations of the financial position of

both the companies are carried out through the use of ratio analysis technique. The second

portfolio is developed for analyzing the potential worth of the two capital investment projects in

order to recommend the best option for capital investment for a local manufacturing company.

The investment appraisal techniques used to analyze the potential worth of both the projects are

NPV, ARR and payback.

Portfolio 1

The portfolio is developed for analyzing the investment worth of the following two

companies:

Sports Direct International PLC

The company is a recognized retailing group of the UK established in the year 1982. It is

attributed to be the largest sports-goods retailer company of the UK operating about 670 stores

across the world. The company carried out its operations through the four segments that are, UK

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Sports Retail, International Sports Retail, Brands and Premium Lifestyle. In addition to this, the

company is also involved in wholesale distribution and sale of sports, leisure, clothing, footwear

and equipment under its brand name (Sports Direct International PLC, 2016).

JD Sports Fashion PLC

The company is the recognized retailer of the UK involved in retailing and distribution of

branded sports and fashion wear products. The company since its establishment in 1982 is

involved in retailing of branded sports fashion wear, clothing, leisure, footwear and sports

products. The company has about 800 stores across the world involved in providing branded

products in the category of sports and clothing. The company has also acquired First Sport in the

year 2002 that further supported its plans of geographical expansion (JD Sports Fashion PLC,

2016).

Calculation of Financial Ratio of both the companies (2015 and 2016) and Analyzing the

Performance, Financial Position and Investment Potential of both Companies

In this section financial ratios of the Sports Direct International PLC and JD Sports

Fashion PLC have been calculated for years 2015 and 2016. In all about 10 financial have been

calculated. All the detailed calculation is presented below. Financial Data used to interpret the

financial Ratio of both the companies (Kaplan and Atkinson, 2015).

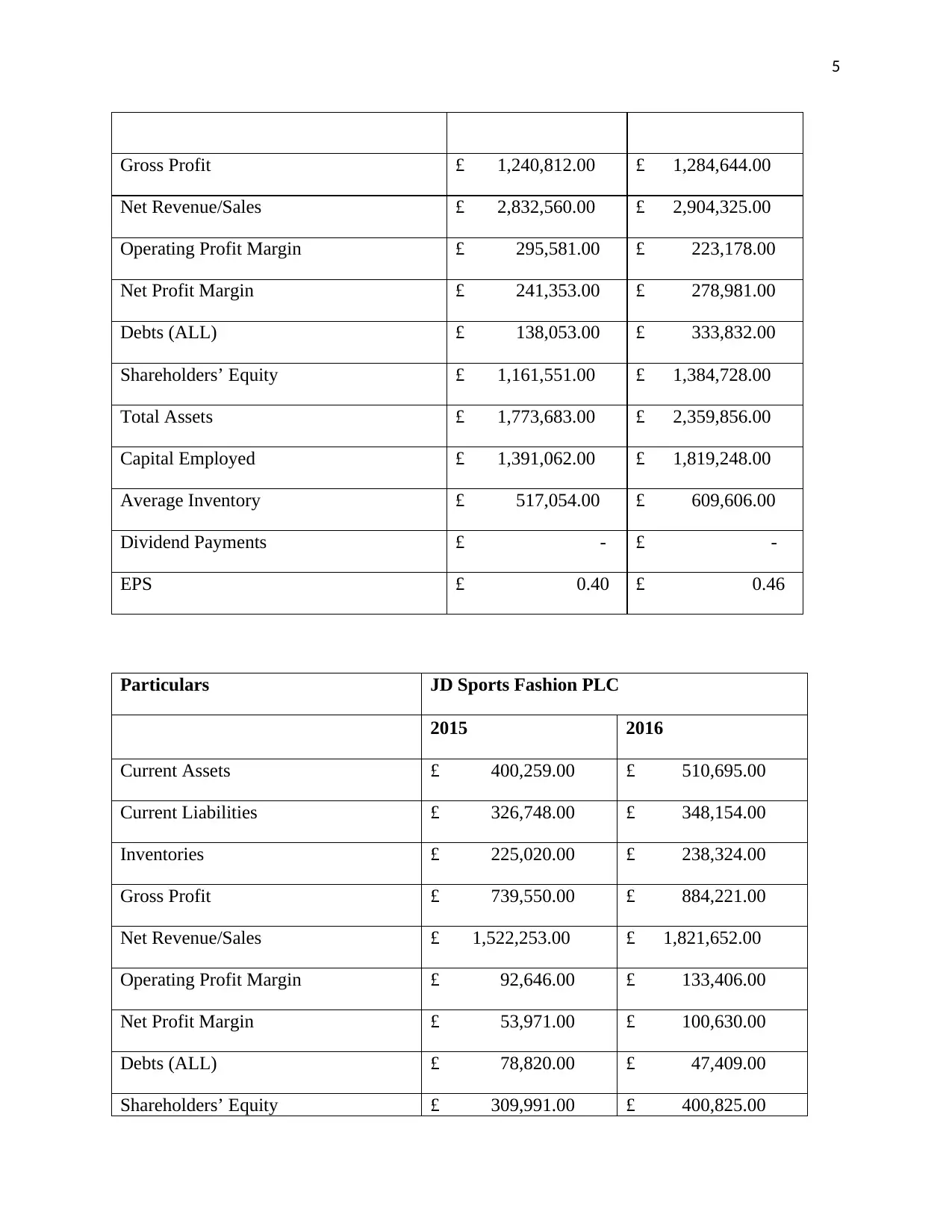

Particulars Sports Direct International PLC

2015 2016

Current Assets £ 878,297.00 £ 1,311,437.00

Current Liabilities £ 382,621.00 £ 540,608.00

Inventories £ 517,054.00 £ 702,158.00

Paraphrase This Document

Gross Profit £ 1,240,812.00 £ 1,284,644.00

Net Revenue/Sales £ 2,832,560.00 £ 2,904,325.00

Operating Profit Margin £ 295,581.00 £ 223,178.00

Net Profit Margin £ 241,353.00 £ 278,981.00

Debts (ALL) £ 138,053.00 £ 333,832.00

Shareholders’ Equity £ 1,161,551.00 £ 1,384,728.00

Total Assets £ 1,773,683.00 £ 2,359,856.00

Capital Employed £ 1,391,062.00 £ 1,819,248.00

Average Inventory £ 517,054.00 £ 609,606.00

Dividend Payments £ - £ -

EPS £ 0.40 £ 0.46

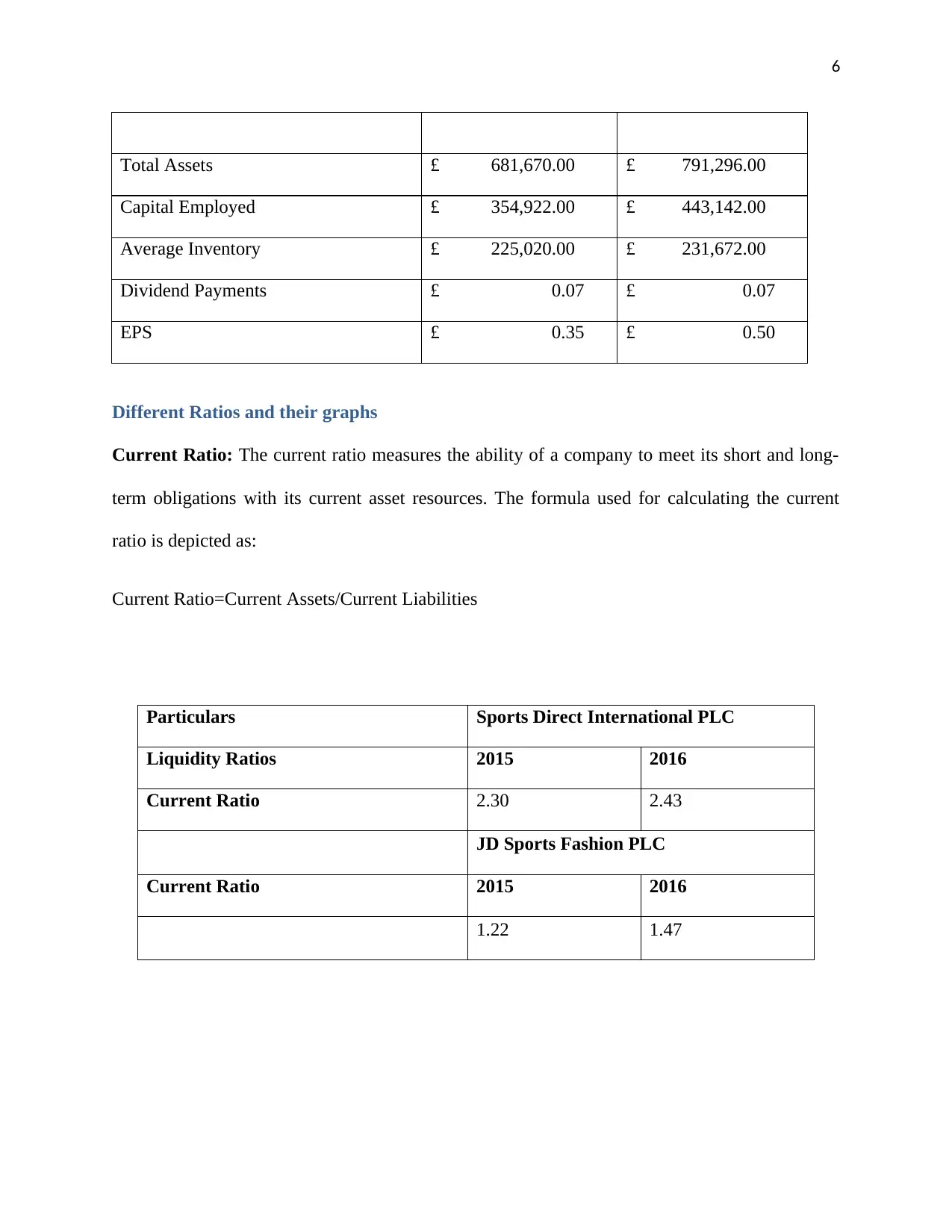

Particulars JD Sports Fashion PLC

2015 2016

Current Assets £ 400,259.00 £ 510,695.00

Current Liabilities £ 326,748.00 £ 348,154.00

Inventories £ 225,020.00 £ 238,324.00

Gross Profit £ 739,550.00 £ 884,221.00

Net Revenue/Sales £ 1,522,253.00 £ 1,821,652.00

Operating Profit Margin £ 92,646.00 £ 133,406.00

Net Profit Margin £ 53,971.00 £ 100,630.00

Debts (ALL) £ 78,820.00 £ 47,409.00

Shareholders’ Equity £ 309,991.00 £ 400,825.00

Total Assets £ 681,670.00 £ 791,296.00

Capital Employed £ 354,922.00 £ 443,142.00

Average Inventory £ 225,020.00 £ 231,672.00

Dividend Payments £ 0.07 £ 0.07

EPS £ 0.35 £ 0.50

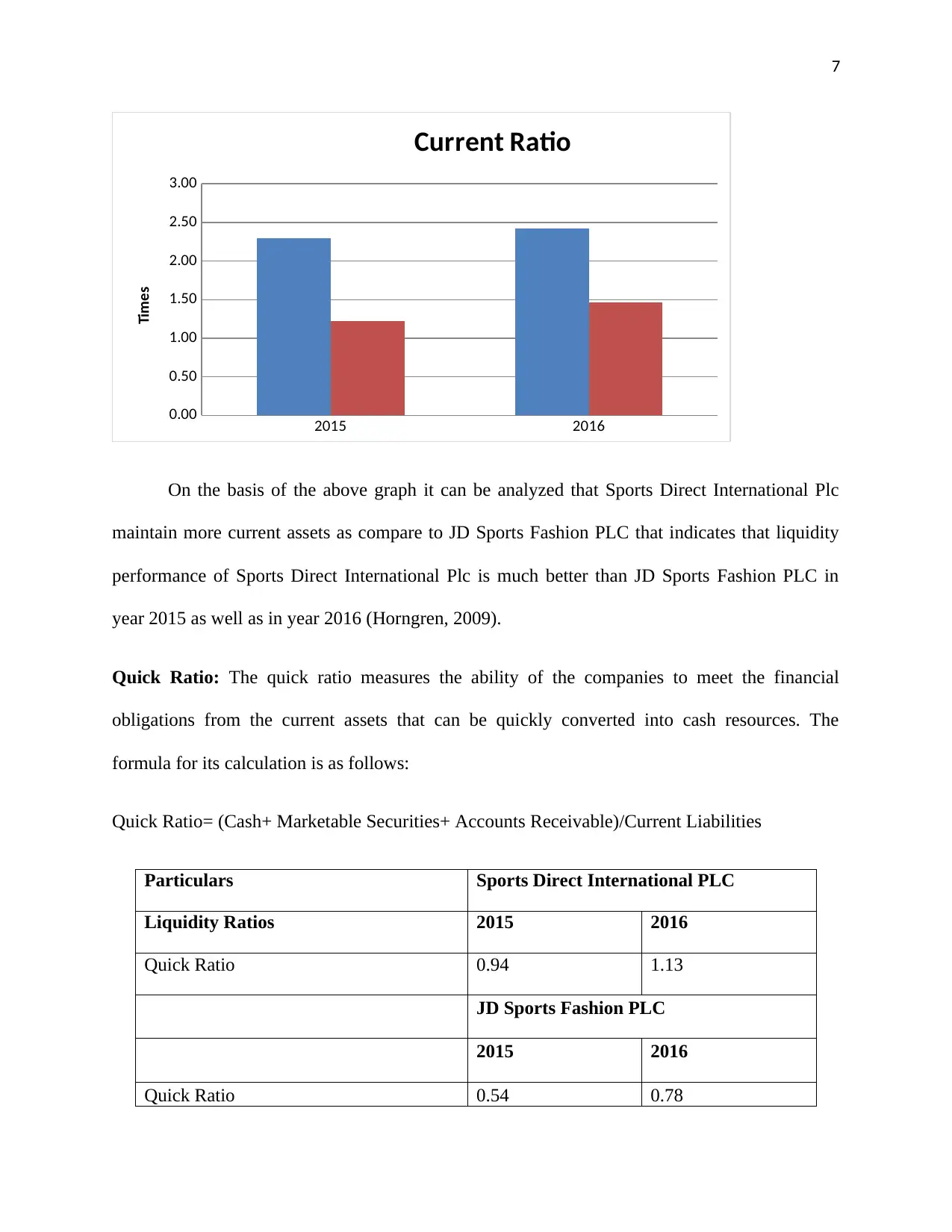

Different Ratios and their graphs

Current Ratio: The current ratio measures the ability of a company to meet its short and long-

term obligations with its current asset resources. The formula used for calculating the current

ratio is depicted as:

Current Ratio=Current Assets/Current Liabilities

Particulars Sports Direct International PLC

Liquidity Ratios 2015 2016

Current Ratio 2.30 2.43

JD Sports Fashion PLC

Current Ratio 2015 2016

1.22 1.47

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2015 2016

0.00

0.50

1.00

1.50

2.00

2.50

3.00

Current Ratio

Times

On the basis of the above graph it can be analyzed that Sports Direct International Plc

maintain more current assets as compare to JD Sports Fashion PLC that indicates that liquidity

performance of Sports Direct International Plc is much better than JD Sports Fashion PLC in

year 2015 as well as in year 2016 (Horngren, 2009).

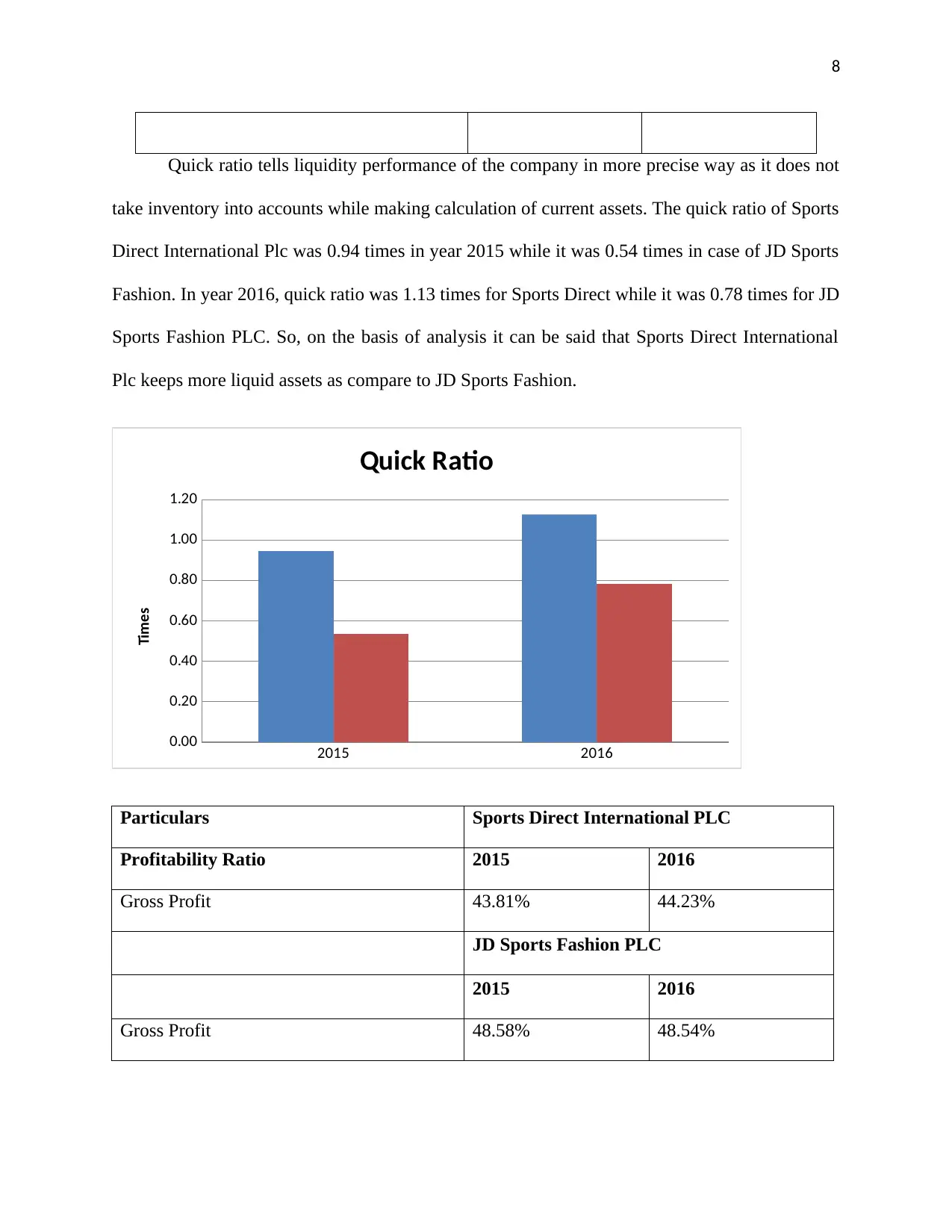

Quick Ratio: The quick ratio measures the ability of the companies to meet the financial

obligations from the current assets that can be quickly converted into cash resources. The

formula for its calculation is as follows:

Quick Ratio= (Cash+ Marketable Securities+ Accounts Receivable)/Current Liabilities

Particulars Sports Direct International PLC

Liquidity Ratios 2015 2016

Quick Ratio 0.94 1.13

JD Sports Fashion PLC

2015 2016

Quick Ratio 0.54 0.78

Paraphrase This Document

Quick ratio tells liquidity performance of the company in more precise way as it does not

take inventory into accounts while making calculation of current assets. The quick ratio of Sports

Direct International Plc was 0.94 times in year 2015 while it was 0.54 times in case of JD Sports

Fashion. In year 2016, quick ratio was 1.13 times for Sports Direct while it was 0.78 times for JD

Sports Fashion PLC. So, on the basis of analysis it can be said that Sports Direct International

Plc keeps more liquid assets as compare to JD Sports Fashion.

2015 2016

0.00

0.20

0.40

0.60

0.80

1.00

1.20

Quick Ratio

Times

Particulars Sports Direct International PLC

Profitability Ratio 2015 2016

Gross Profit 43.81% 44.23%

JD Sports Fashion PLC

2015 2016

Gross Profit 48.58% 48.54%

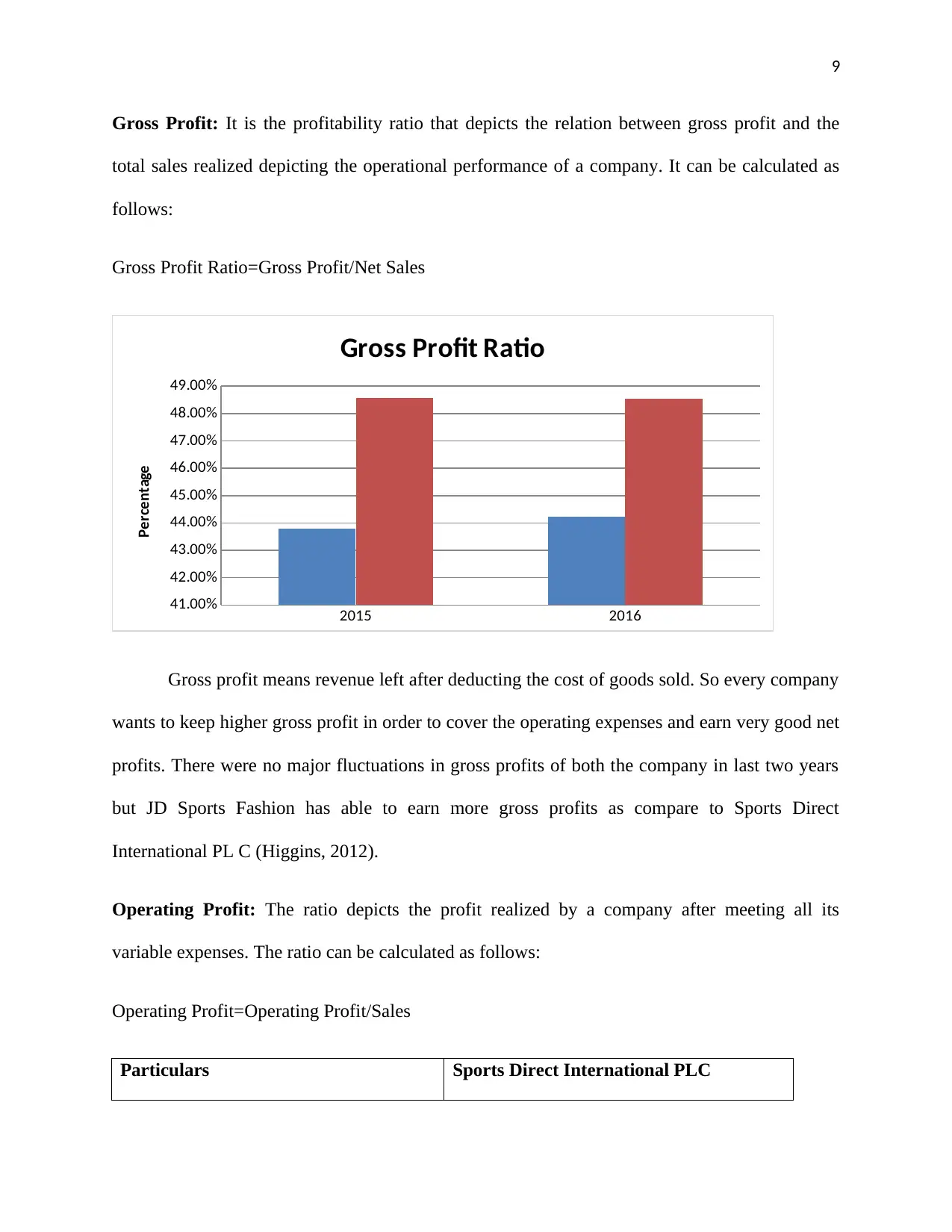

Gross Profit: It is the profitability ratio that depicts the relation between gross profit and the

total sales realized depicting the operational performance of a company. It can be calculated as

follows:

Gross Profit Ratio=Gross Profit/Net Sales

2015 2016

41.00%

42.00%

43.00%

44.00%

45.00%

46.00%

47.00%

48.00%

49.00%

Gross Profit Ratio

Percentage

Gross profit means revenue left after deducting the cost of goods sold. So every company

wants to keep higher gross profit in order to cover the operating expenses and earn very good net

profits. There were no major fluctuations in gross profits of both the company in last two years

but JD Sports Fashion has able to earn more gross profits as compare to Sports Direct

International PL C (Higgins, 2012).

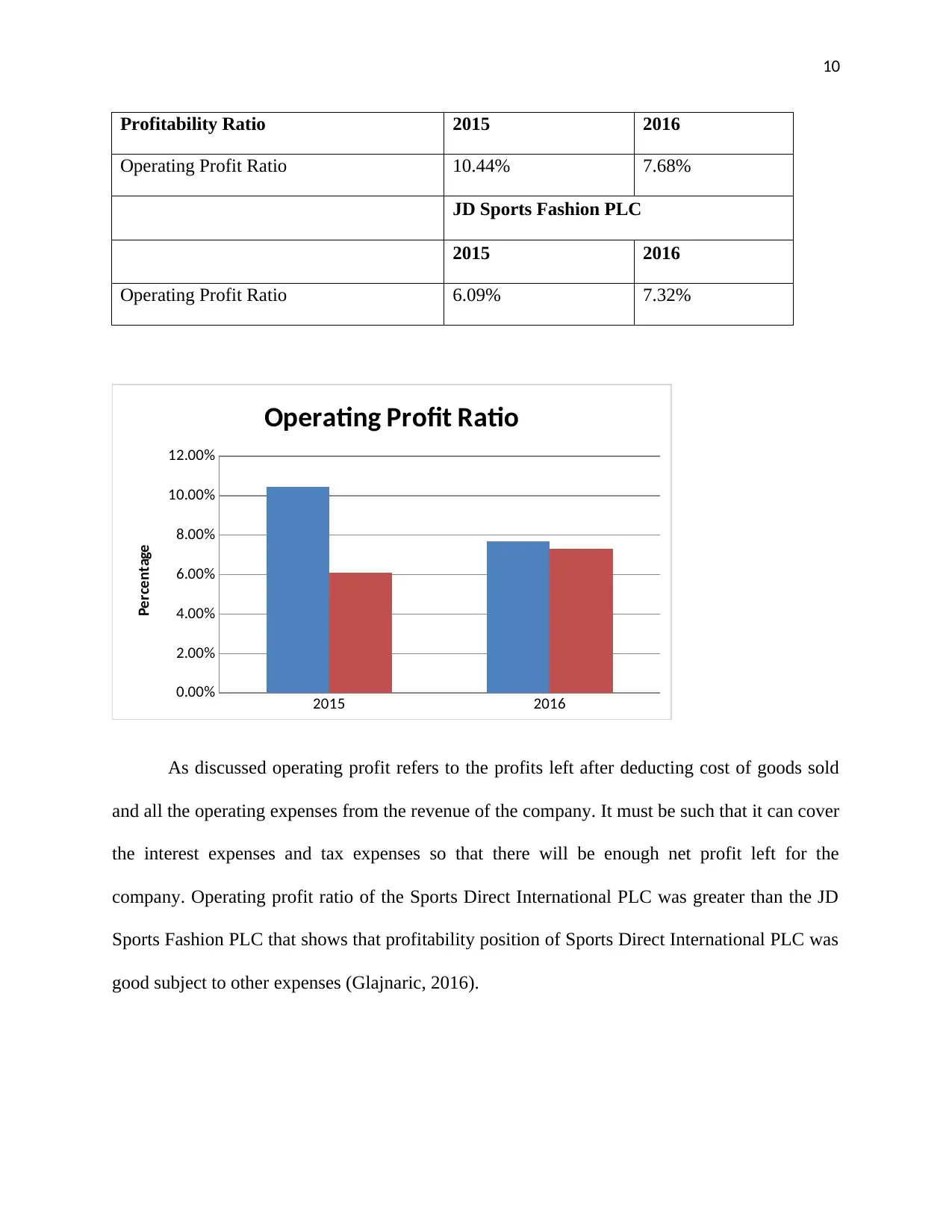

Operating Profit: The ratio depicts the profit realized by a company after meeting all its

variable expenses. The ratio can be calculated as follows:

Operating Profit=Operating Profit/Sales

Particulars Sports Direct International PLC

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Profitability Ratio 2015 2016

Operating Profit Ratio 10.44% 7.68%

JD Sports Fashion PLC

2015 2016

Operating Profit Ratio 6.09% 7.32%

2015 2016

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

Operating Profit Ratio

Percentage

As discussed operating profit refers to the profits left after deducting cost of goods sold

and all the operating expenses from the revenue of the company. It must be such that it can cover

the interest expenses and tax expenses so that there will be enough net profit left for the

company. Operating profit ratio of the Sports Direct International PLC was greater than the JD

Sports Fashion PLC that shows that profitability position of Sports Direct International PLC was

good subject to other expenses (Glajnaric, 2016).

Paraphrase This Document

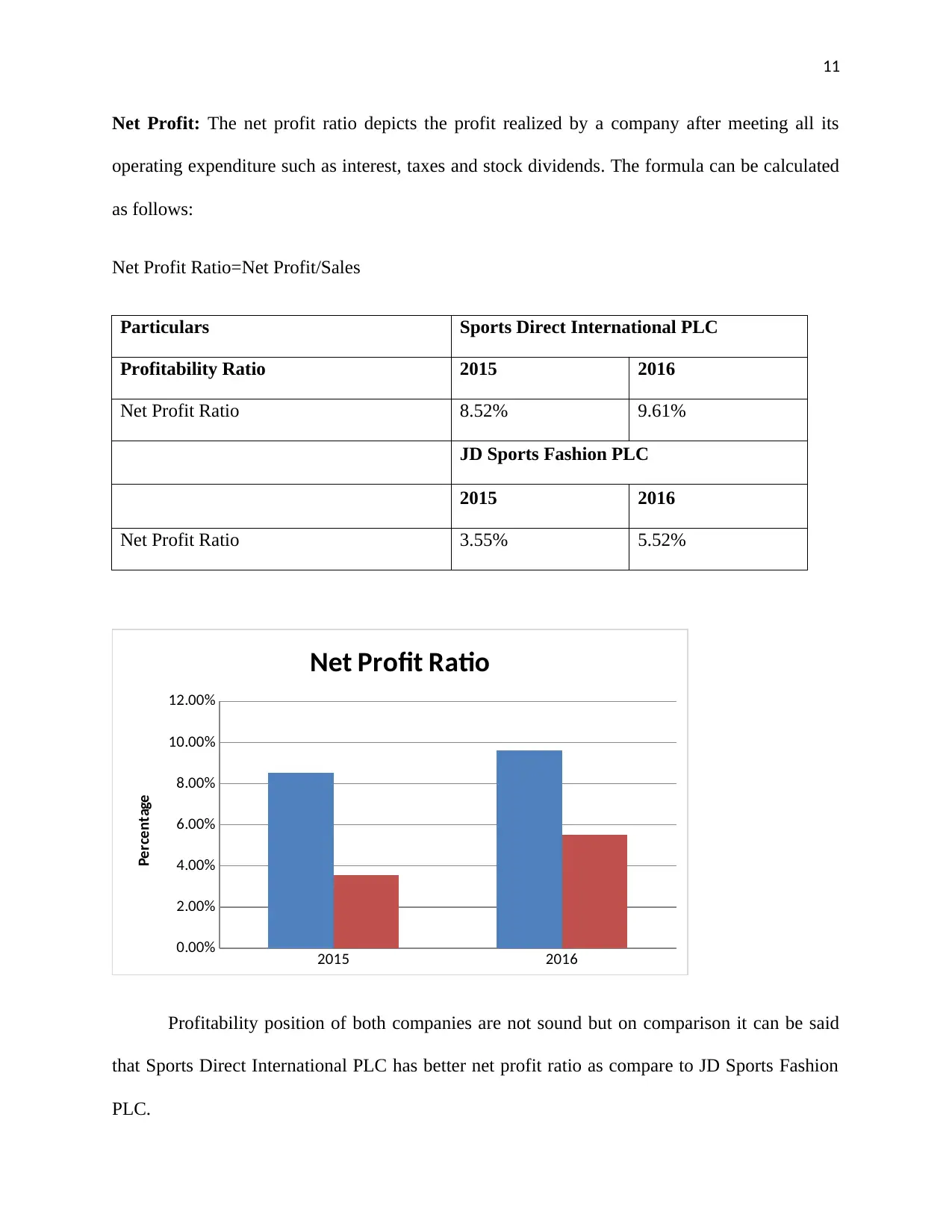

Net Profit: The net profit ratio depicts the profit realized by a company after meeting all its

operating expenditure such as interest, taxes and stock dividends. The formula can be calculated

as follows:

Net Profit Ratio=Net Profit/Sales

Particulars Sports Direct International PLC

Profitability Ratio 2015 2016

Net Profit Ratio 8.52% 9.61%

JD Sports Fashion PLC

2015 2016

Net Profit Ratio 3.55% 5.52%

2015 2016

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

Net Profit Ratio

Percentage

Profitability position of both companies are not sound but on comparison it can be said

that Sports Direct International PLC has better net profit ratio as compare to JD Sports Fashion

PLC.

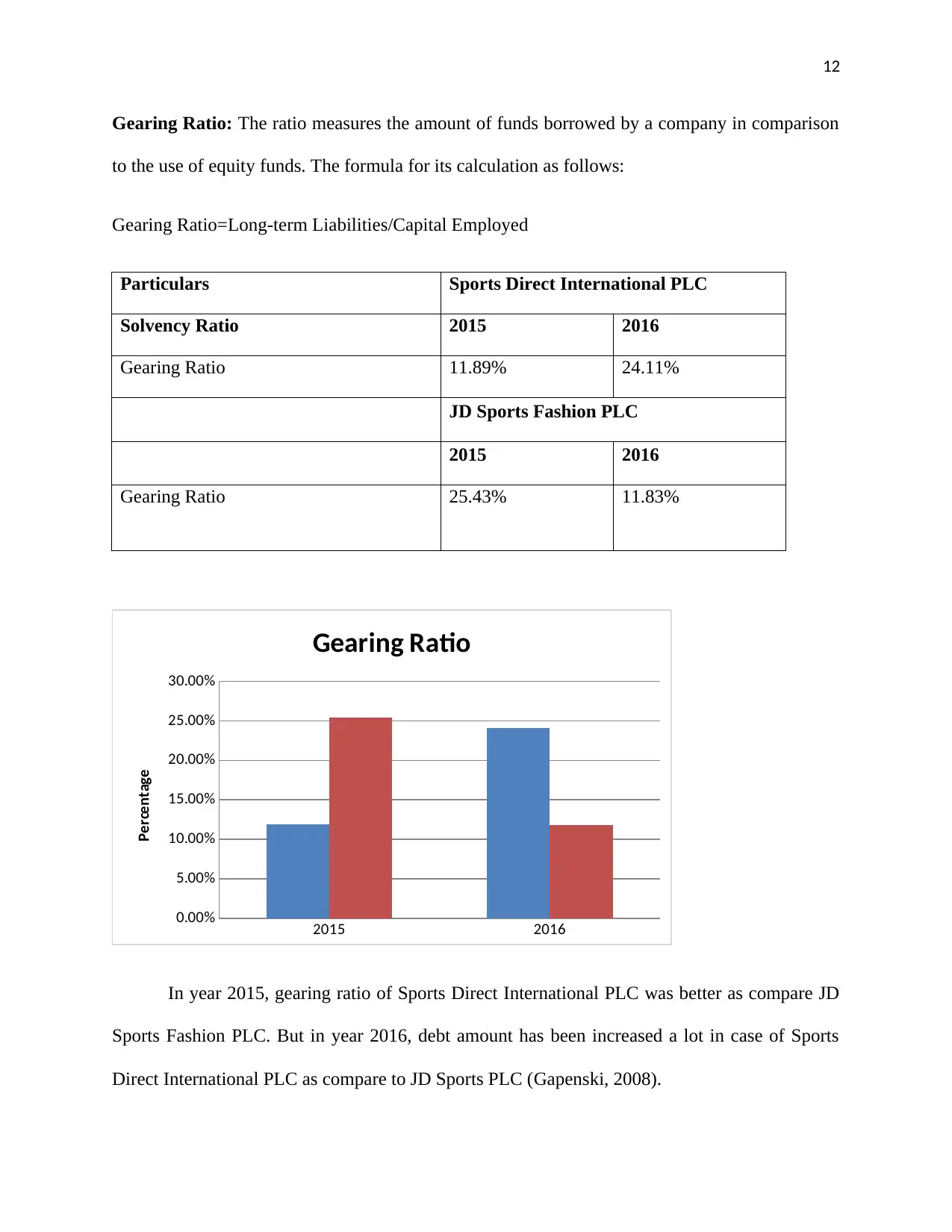

Gearing Ratio: The ratio measures the amount of funds borrowed by a company in comparison

to the use of equity funds. The formula for its calculation as follows:

Gearing Ratio=Long-term Liabilities/Capital Employed

Particulars Sports Direct International PLC

Solvency Ratio 2015 2016

Gearing Ratio 11.89% 24.11%

JD Sports Fashion PLC

2015 2016

Gearing Ratio 25.43% 11.83%

2015 2016

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

Gearing Ratio

Percentage

In year 2015, gearing ratio of Sports Direct International PLC was better as compare JD

Sports Fashion PLC. But in year 2016, debt amount has been increased a lot in case of Sports

Direct International PLC as compare to JD Sports PLC (Gapenski, 2008).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

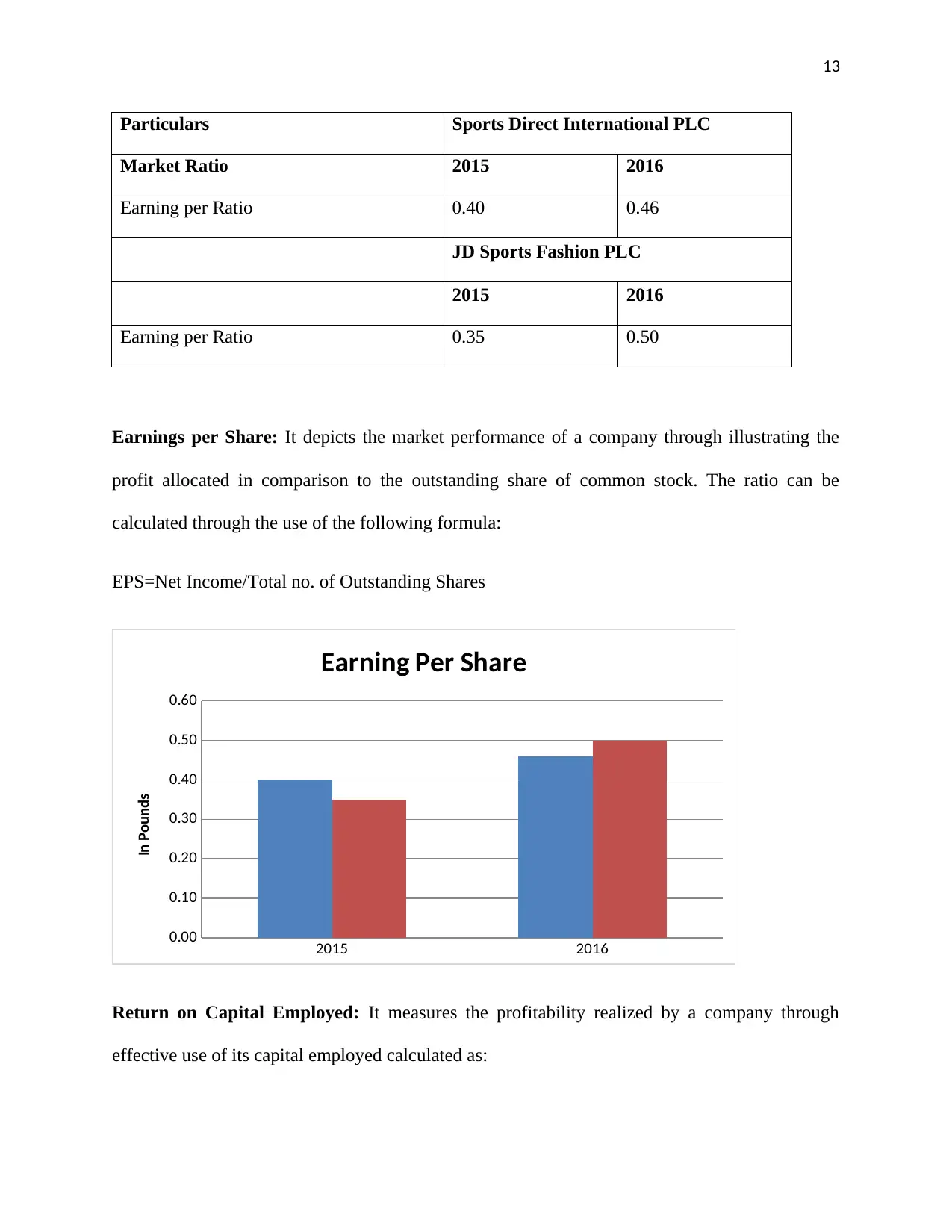

Particulars Sports Direct International PLC

Market Ratio 2015 2016

Earning per Ratio 0.40 0.46

JD Sports Fashion PLC

2015 2016

Earning per Ratio 0.35 0.50

Earnings per Share: It depicts the market performance of a company through illustrating the

profit allocated in comparison to the outstanding share of common stock. The ratio can be

calculated through the use of the following formula:

EPS=Net Income/Total no. of Outstanding Shares

2015 2016

0.00

0.10

0.20

0.30

0.40

0.50

0.60

Earning Per Share

In Pounds

Return on Capital Employed: It measures the profitability realized by a company through

effective use of its capital employed calculated as:

Paraphrase This Document

ROCE=Earnings before Interest and Tax/Capital Employed

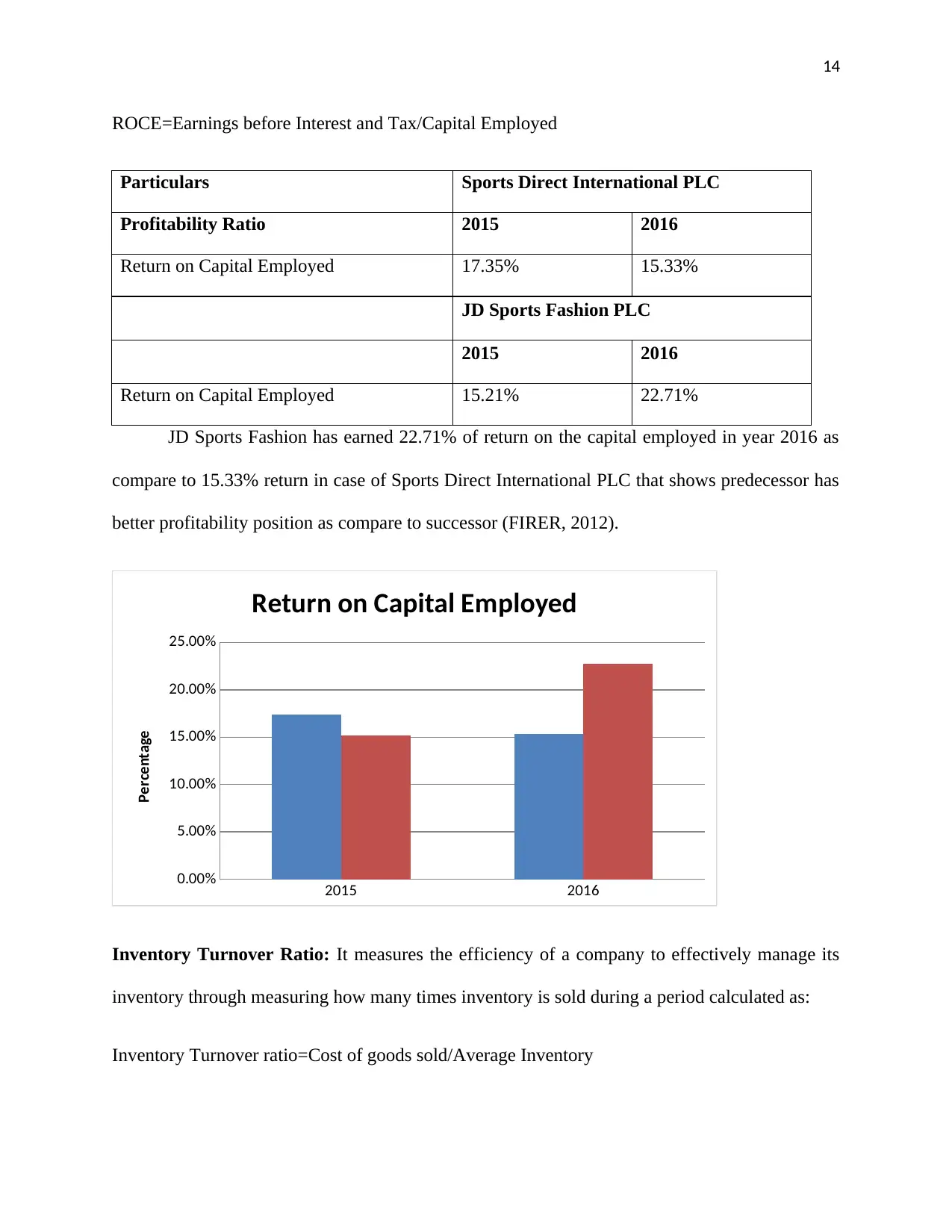

Particulars Sports Direct International PLC

Profitability Ratio 2015 2016

Return on Capital Employed 17.35% 15.33%

JD Sports Fashion PLC

2015 2016

Return on Capital Employed 15.21% 22.71%

JD Sports Fashion has earned 22.71% of return on the capital employed in year 2016 as

compare to 15.33% return in case of Sports Direct International PLC that shows predecessor has

better profitability position as compare to successor (FIRER, 2012).

2015 2016

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

Return on Capital Employed

Percentage

Inventory Turnover Ratio: It measures the efficiency of a company to effectively manage its

inventory through measuring how many times inventory is sold during a period calculated as:

Inventory Turnover ratio=Cost of goods sold/Average Inventory

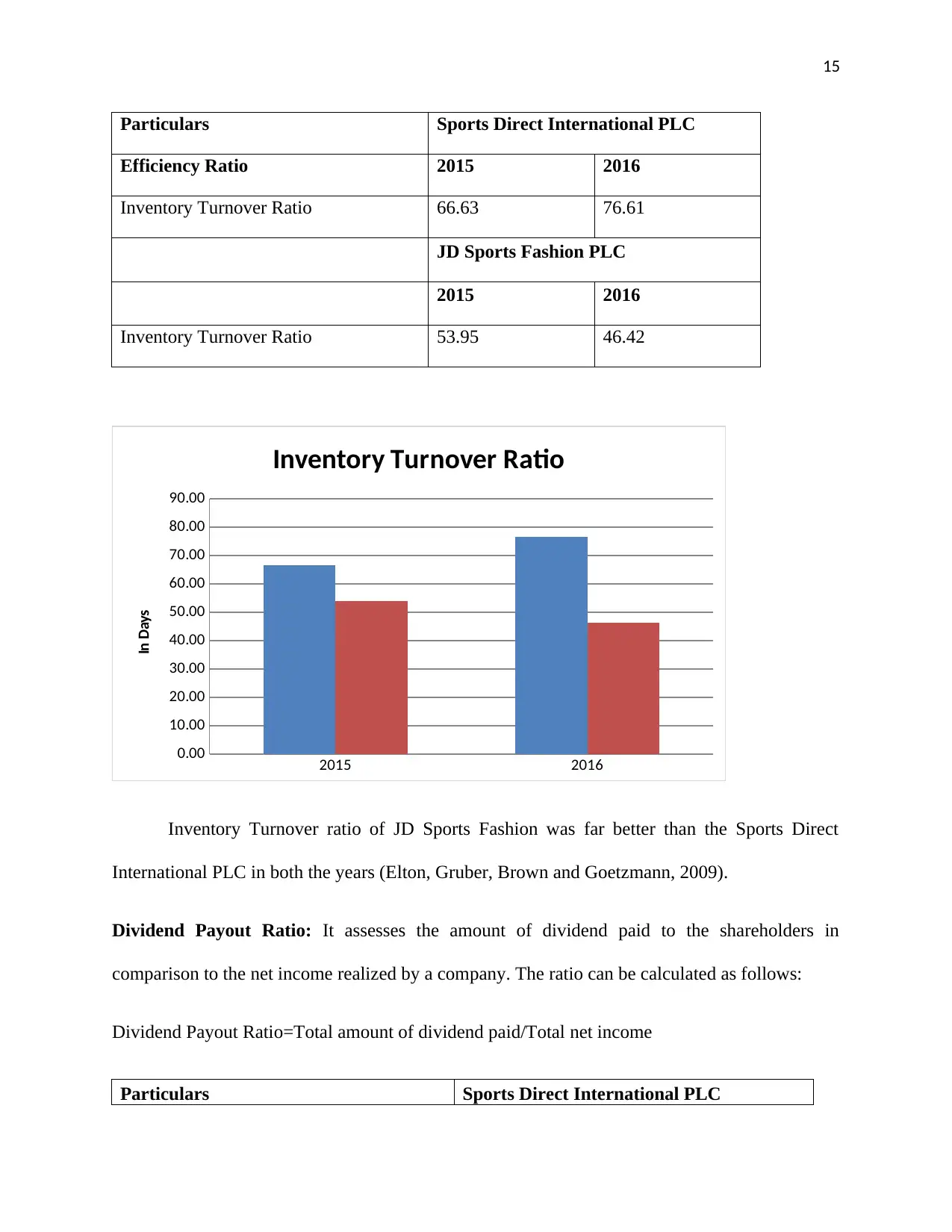

Particulars Sports Direct International PLC

Efficiency Ratio 2015 2016

Inventory Turnover Ratio 66.63 76.61

JD Sports Fashion PLC

2015 2016

Inventory Turnover Ratio 53.95 46.42

2015 2016

0.00

10.00

20.00

30.00

40.00

50.00

60.00

70.00

80.00

90.00

Inventory Turnover Ratio

In Days

Inventory Turnover ratio of JD Sports Fashion was far better than the Sports Direct

International PLC in both the years (Elton, Gruber, Brown and Goetzmann, 2009).

Dividend Payout Ratio: It assesses the amount of dividend paid to the shareholders in

comparison to the net income realized by a company. The ratio can be calculated as follows:

Dividend Payout Ratio=Total amount of dividend paid/Total net income

Particulars Sports Direct International PLC

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

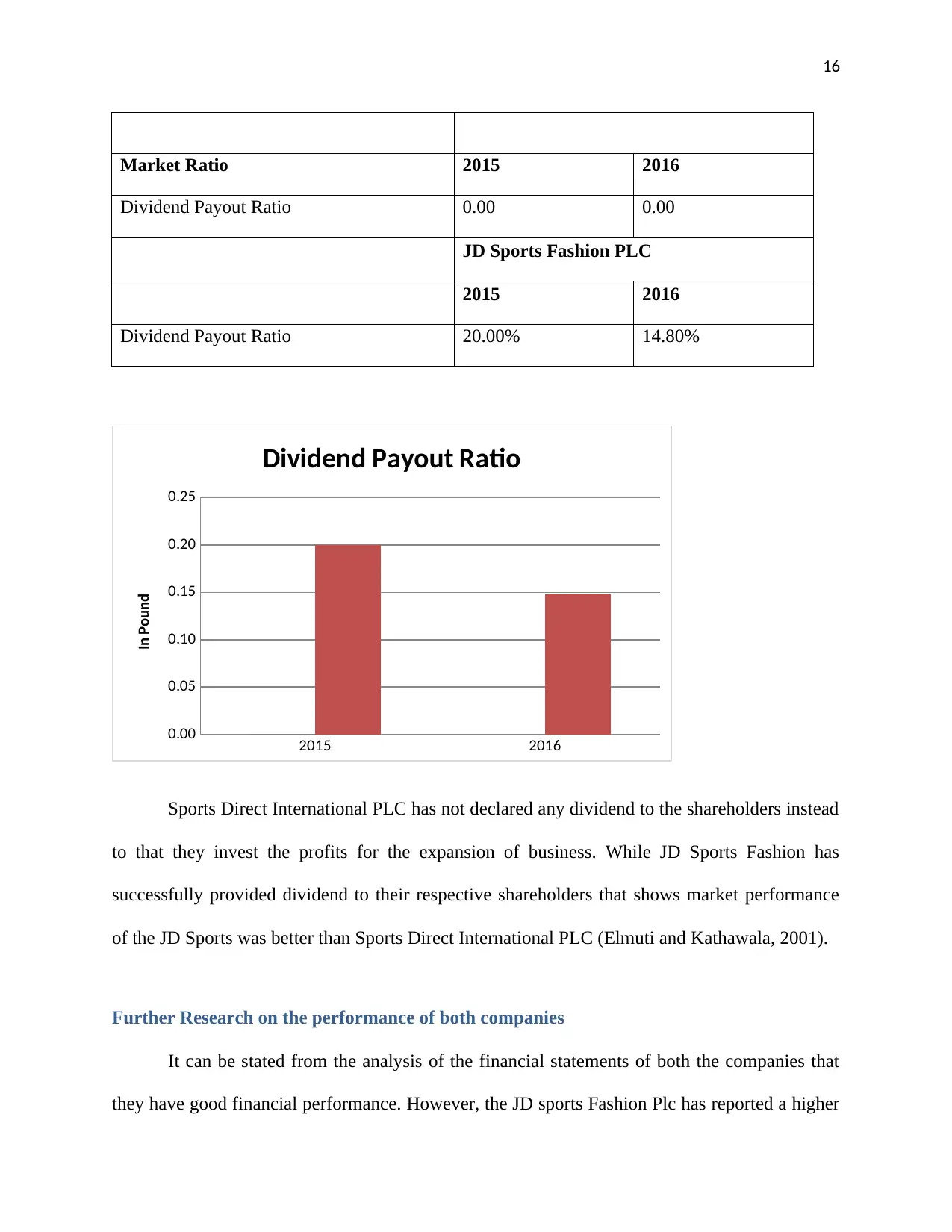

Market Ratio 2015 2016

Dividend Payout Ratio 0.00 0.00

JD Sports Fashion PLC

2015 2016

Dividend Payout Ratio 20.00% 14.80%

2015 2016

0.00

0.05

0.10

0.15

0.20

0.25

Dividend Payout Ratio

In Pound

Sports Direct International PLC has not declared any dividend to the shareholders instead

to that they invest the profits for the expansion of business. While JD Sports Fashion has

successfully provided dividend to their respective shareholders that shows market performance

of the JD Sports was better than Sports Direct International PLC (Elmuti and Kathawala, 2001).

Further Research on the performance of both companies

It can be stated from the analysis of the financial statements of both the companies that

they have good financial performance. However, the JD sports Fashion Plc has reported a higher

Paraphrase This Document

profitability with recording in dividend growth from 6.20p to 7.40p from the financial year of

2015 to 2016 (Sports Direct International PLC, 2016). On the other hand, the dividend payout

ratio of Sports Retail is not good for the respective financial period also its earnings per share

and profit before tax has shown a decreasing trend (JD Sports Fashion PLC, 2016). On the

contrary, the profit before tax for JD Sports has recorded high financial figures of £157.1 million.

Therefore, it can be stated from the financial analysis of both the companies that Madhouse

Retail Ltd should buy out the shares of JD Sports Fashion PLC.

Recommendations

On the basis of the financial analysis carried out for both the companies of JD Sports

Fashion and Sports Retail, it is recommend that the investors should invest in the JD sports as its

financial position is much better than Sports Retail. The profit before tax, earnings per share and

dividends per share of the company has decreased to a large extent indicating that the company

financial position is not stable. AS such, the company is recommended to implement effective

strategies for improving its financial performance. It needs to improve its profit before tax by

reducing its operational expenses and variable costs of production. The earnings per share and

dividend payout ratio of the company can be improved through enhancing its net sales

realization.

Limitations of Relying on Financial Ratios to Interpret Firm Performance

The major limitation of the ratio analysis is that it uses historical financial data for

analyzing the financial performance of the companies. The ratio analysis technique is not useful

for estimating the future performance of the companies as the historical data used cannot predict

the future market trends. The ratio analysis is also not regarded to be a useful technique for

generating consistent results as different companies uses varied accounting policies for

developing the financial statements (Dixon and Monk, 2009). Therefore, the results obtained

through the use of financial ratio analysis technique are not regarded to be accurate and reliable

for comparing the financial performance of the companies. Also, the technique cannot carry out

financial analysis of the companies having different sizes and belonging to different industries

due to large difference in the preparation of the financial statements. The ratio analysis has also a

drawback of not carrying out financial analysis of a company on stand-alone basis. It can only be

used to carry out comparative analysis of financial performance of the two companies. The

impact of inflation can also distort the financial data used for evaluating the financial

performance of the companies in the ratio analysis method. Therefore, the use of the technique

can sometimes lead to manipulates results in the event of distortion of the financial data due to

certain economic conditions (Deegan, 2013).

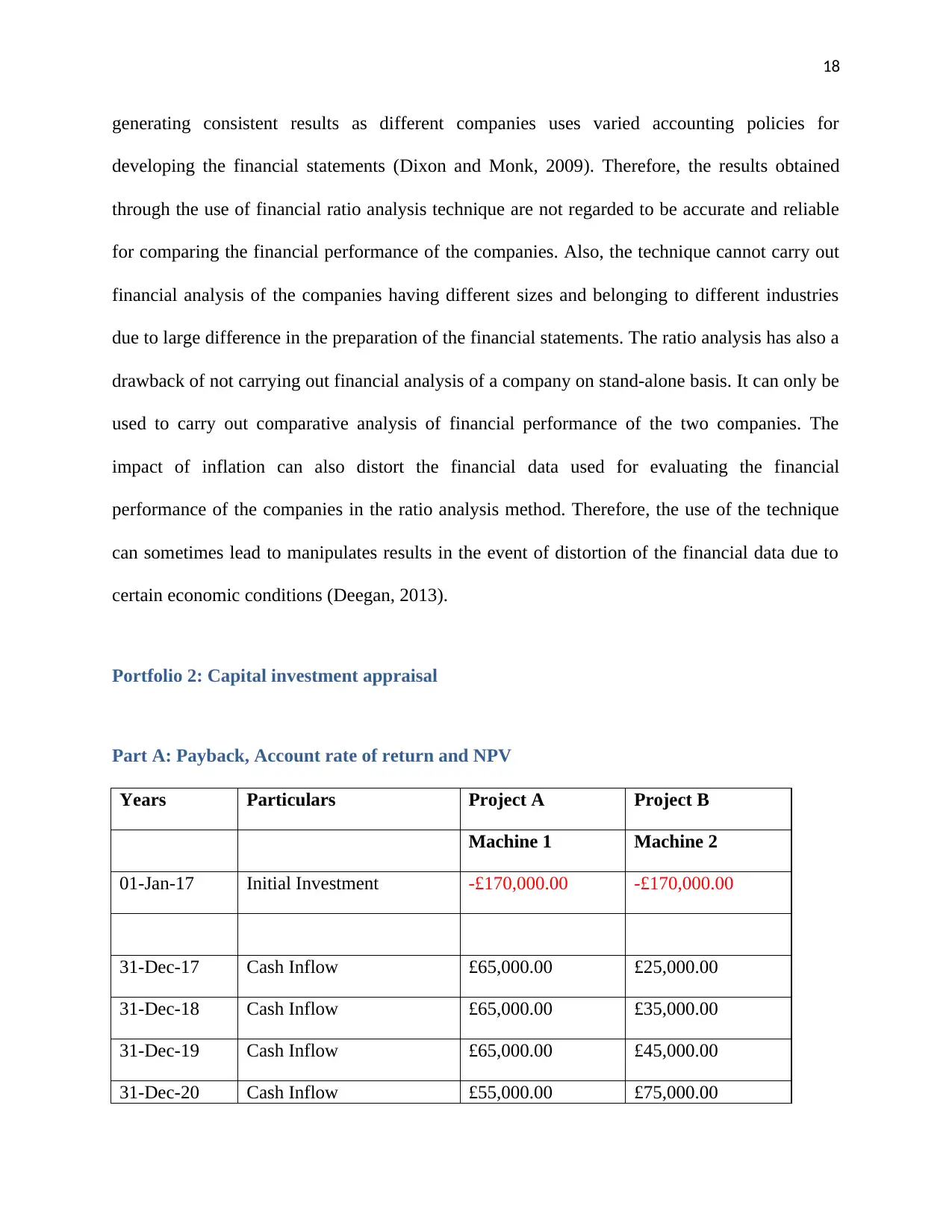

Portfolio 2: Capital investment appraisal

Part A: Payback, Account rate of return and NPV

Years Particulars Project A Project B

Machine 1 Machine 2

01-Jan-17 Initial Investment -£170,000.00 -£170,000.00

31-Dec-17 Cash Inflow £65,000.00 £25,000.00

31-Dec-18 Cash Inflow £65,000.00 £35,000.00

31-Dec-19 Cash Inflow £65,000.00 £45,000.00

31-Dec-20 Cash Inflow £55,000.00 £75,000.00

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

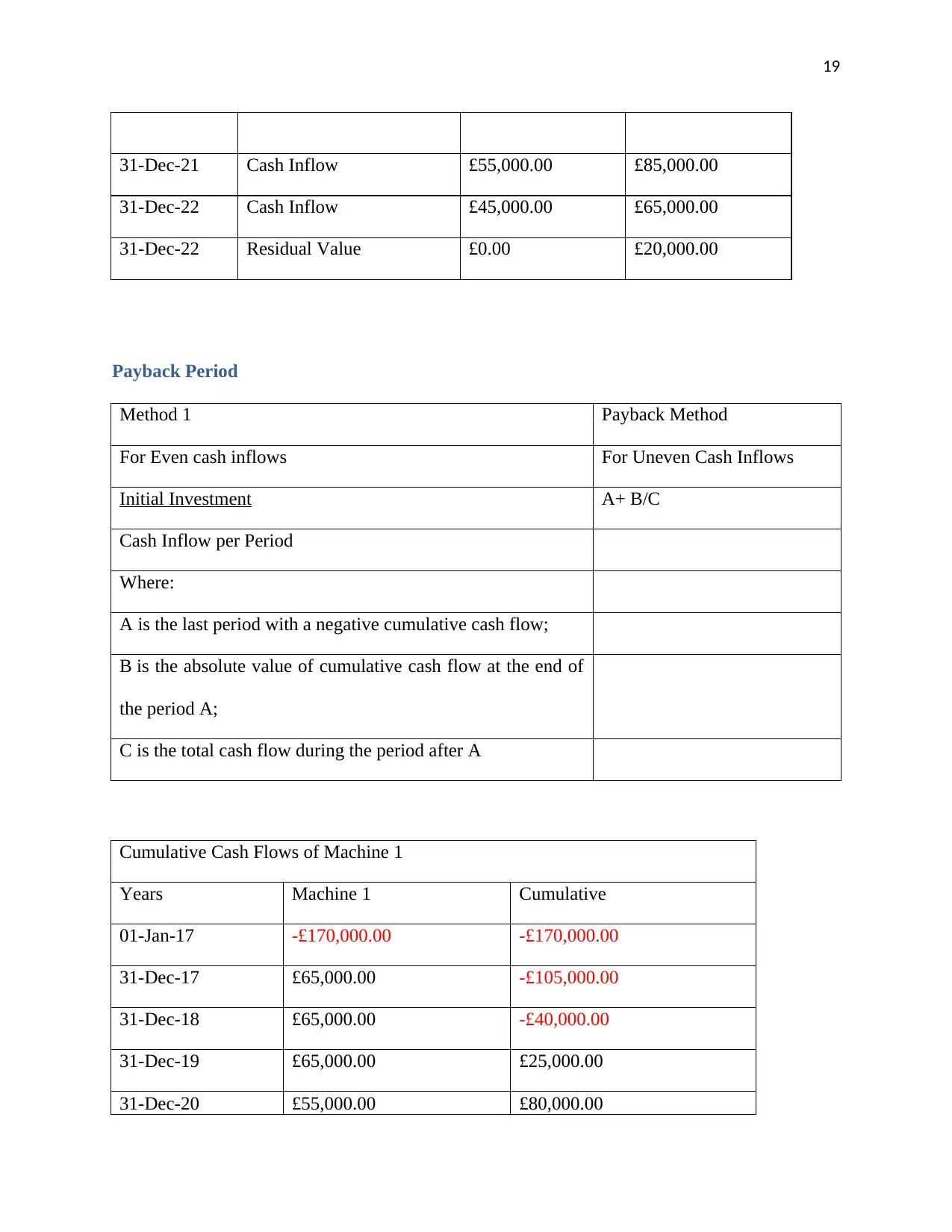

31-Dec-21 Cash Inflow £55,000.00 £85,000.00

31-Dec-22 Cash Inflow £45,000.00 £65,000.00

31-Dec-22 Residual Value £0.00 £20,000.00

Payback Period

Method 1 Payback Method

For Even cash inflows For Uneven Cash Inflows

Initial Investment A+ B/C

Cash Inflow per Period

Where:

A is the last period with a negative cumulative cash flow;

B is the absolute value of cumulative cash flow at the end of

the period A;

C is the total cash flow during the period after A

Cumulative Cash Flows of Machine 1

Years Machine 1 Cumulative

01-Jan-17 -£170,000.00 -£170,000.00

31-Dec-17 £65,000.00 -£105,000.00

31-Dec-18 £65,000.00 -£40,000.00

31-Dec-19 £65,000.00 £25,000.00

31-Dec-20 £55,000.00 £80,000.00

Paraphrase This Document

31-Dec-21 £55,000.00 £135,000.00

31-Dec-22 £45,000.00 £180,000.00

Cumulative Cash Flows of Machine 2

Years Machine 2 Cumulative

01-Jan-17 -£170,000.00 -£170,000.00

31-Dec-17 £25,000.00 -£145,000.00

31-Dec-18 £35,000.00 -£110,000.00

31-Dec-19 £45,000.00 -£65,000.00

31-Dec-20 £75,000.00 £10,000.00

31-Dec-21 £85,000.00 £95,000.00

31-Dec-22 £65,000.00 £160,000.00

Machine 1 Machine 2

Payback 3.62 4.87

3.62 years 4.87 years

Decision: On the basis of above calculation, senior management should select Machine 1 as it

has lower payback period as compare to Machine 2.

(Brigham and Houston, 2012)

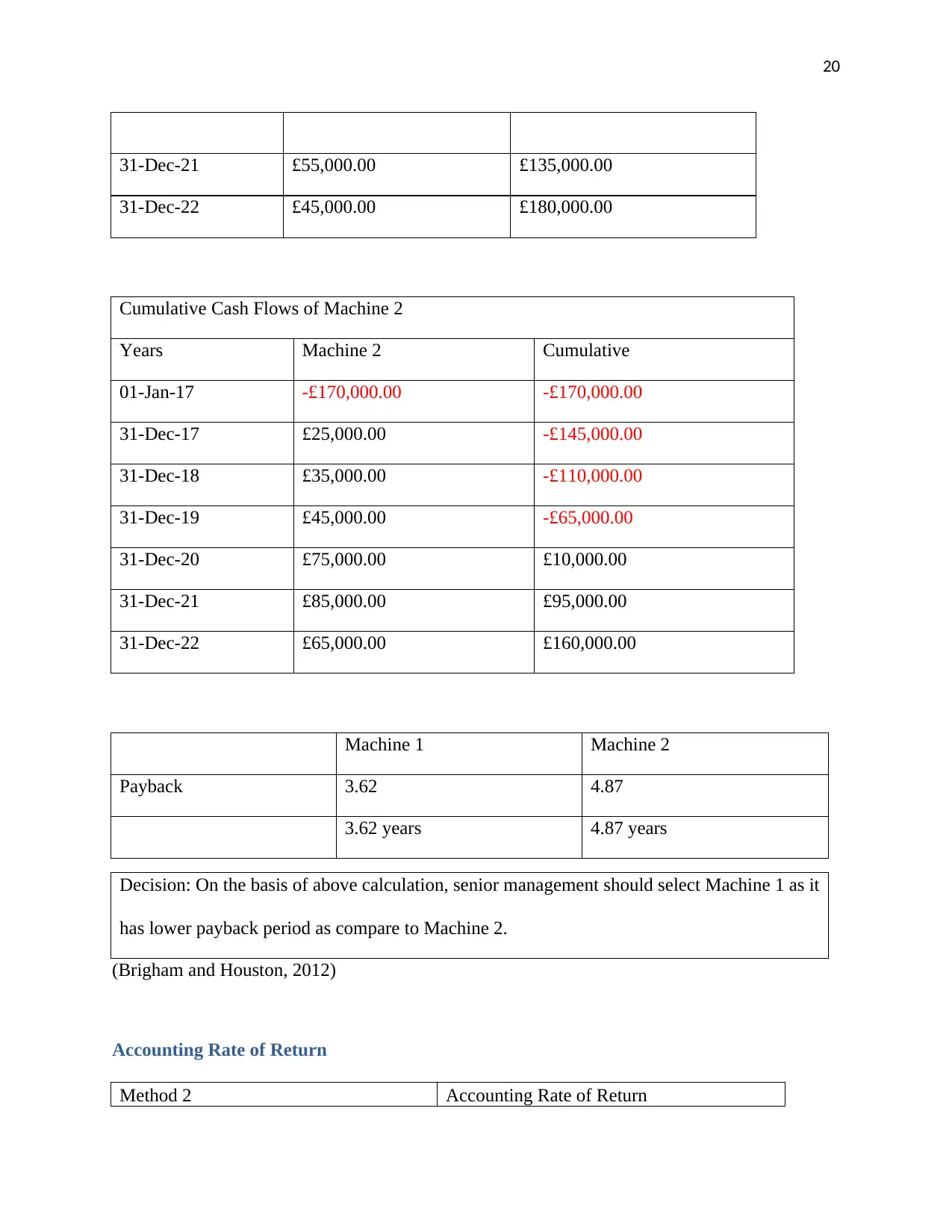

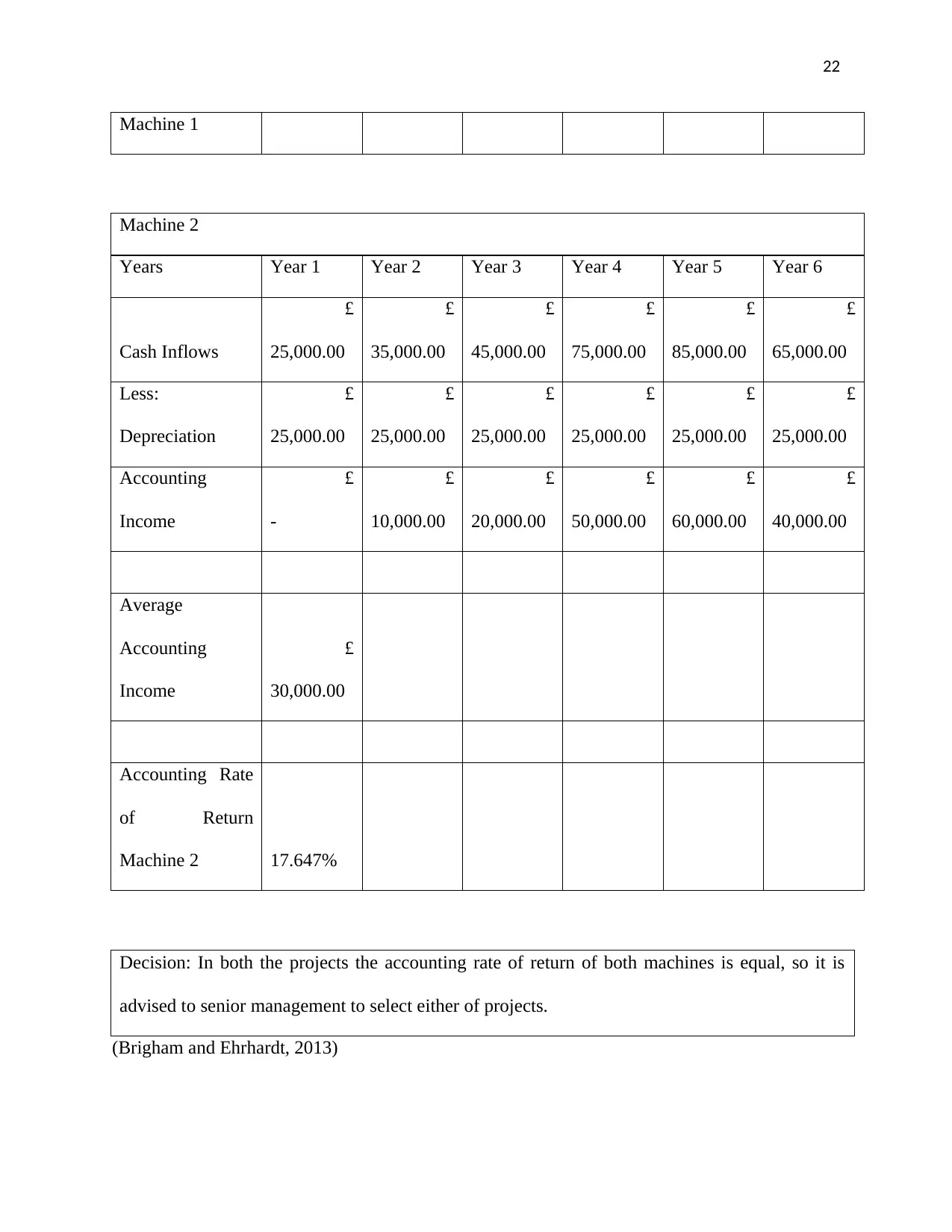

Accounting Rate of Return

Method 2 Accounting Rate of Return

Formula Average Accounting Profit

Average Investment

Particulars Machine 1 Machine 2

Annual Depreciation £28,333.33 £25,000.00

Calculation of Average Accounting Profit/Income

Machine 1

Years Year 1 Year 2 Year 3 Year 4 Year 5 Year 6

Cash Inflows

£

65,000.00

£

65,000.00

£

65,000.00

£

55,000.00

£

55,000.00

£

45,000.00

Less:

Depreciation

£

28,333.33

£

28,333.33

£

28,333.33

£

28,333.33

£

28,333.33

£

28,333.33

Accounting

Income

£

36,666.67

£

36,666.67

£

36,666.67

£

26,666.67

£

26,666.67

£

16,666.67

Average

Accounting

Income

£

30,000.00

Accounting Rate

of Return

17.647%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Machine 1

Machine 2

Years Year 1 Year 2 Year 3 Year 4 Year 5 Year 6

Cash Inflows

£

25,000.00

£

35,000.00

£

45,000.00

£

75,000.00

£

85,000.00

£

65,000.00

Less:

Depreciation

£

25,000.00

£

25,000.00

£

25,000.00

£

25,000.00

£

25,000.00

£

25,000.00

Accounting

Income

£

-

£

10,000.00

£

20,000.00

£

50,000.00

£

60,000.00

£

40,000.00

Average

Accounting

Income

£

30,000.00

Accounting Rate

of Return

Machine 2 17.647%

Decision: In both the projects the accounting rate of return of both machines is equal, so it is

advised to senior management to select either of projects.

(Brigham and Ehrhardt, 2013)

Paraphrase This Document

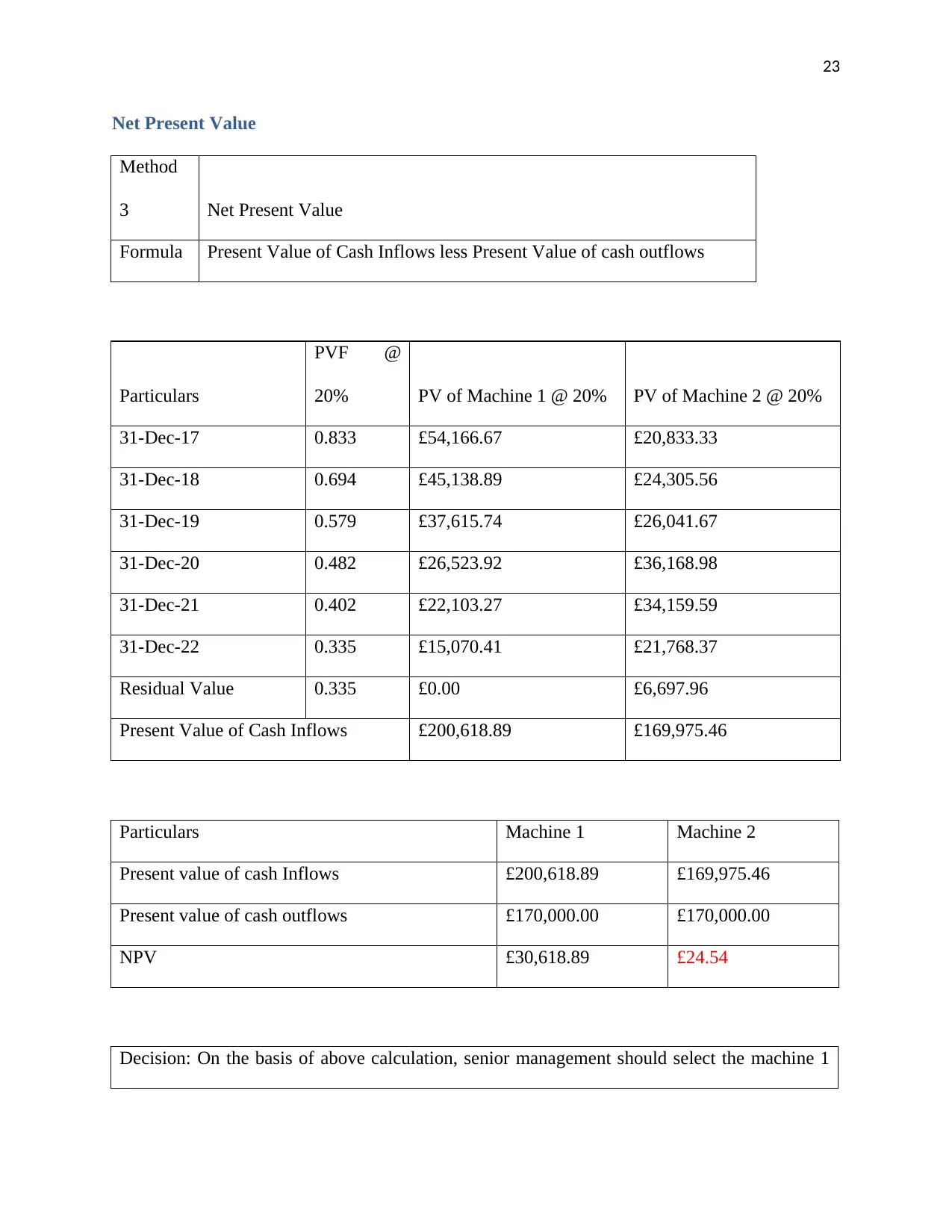

Net Present Value

Method

3 Net Present Value

Formula Present Value of Cash Inflows less Present Value of cash outflows

Particulars

PVF @

20% PV of Machine 1 @ 20% PV of Machine 2 @ 20%

31-Dec-17 0.833 £54,166.67 £20,833.33

31-Dec-18 0.694 £45,138.89 £24,305.56

31-Dec-19 0.579 £37,615.74 £26,041.67

31-Dec-20 0.482 £26,523.92 £36,168.98

31-Dec-21 0.402 £22,103.27 £34,159.59

31-Dec-22 0.335 £15,070.41 £21,768.37

Residual Value 0.335 £0.00 £6,697.96

Present Value of Cash Inflows £200,618.89 £169,975.46

Particulars Machine 1 Machine 2

Present value of cash Inflows £200,618.89 £169,975.46

Present value of cash outflows £170,000.00 £170,000.00

NPV £30,618.89 £24.54

Decision: On the basis of above calculation, senior management should select the machine 1

due to higher NPV as compare to machine 2.

Part B: Limitations of using investment appraisal techniques to aid long-term decision-

making

NPV

The cost of capital assed by the method is based on estimation and therefore not reliable

It is not a useful method for comparing the projects of two different sizes

The results obtained from the method are also highly sensitive to the discount rates as it

incorporates the use of summation of multiple discounted cash flows for estimating the

present value of an investment

The method is also difficult to understand and implement by the project managers

(Brealey, Myers and Marcus, 2007)

ARR

The method does not take into account the concept of time value of money and thus not

effective method for estimating the future worth of an investment

The method also does not include the external factors that can impact the profitability of

a project

The method also does not determine the present value of cash flows that are more

important than the accounting profits

It is also not an effective method to be used for calculating the worth of a project in

which investment is to be made in parts (Batra and Verma, 2014)

Payback

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

© 2024 | Zucol Services PVT LTD | All rights reserved.