JB HI-FI & Harvey Norman: Owner's Equity, Cash Flow, and Tax Rates

VerifiedAdded on 2023/06/05

|9

|404

|337

Report

AI Summary

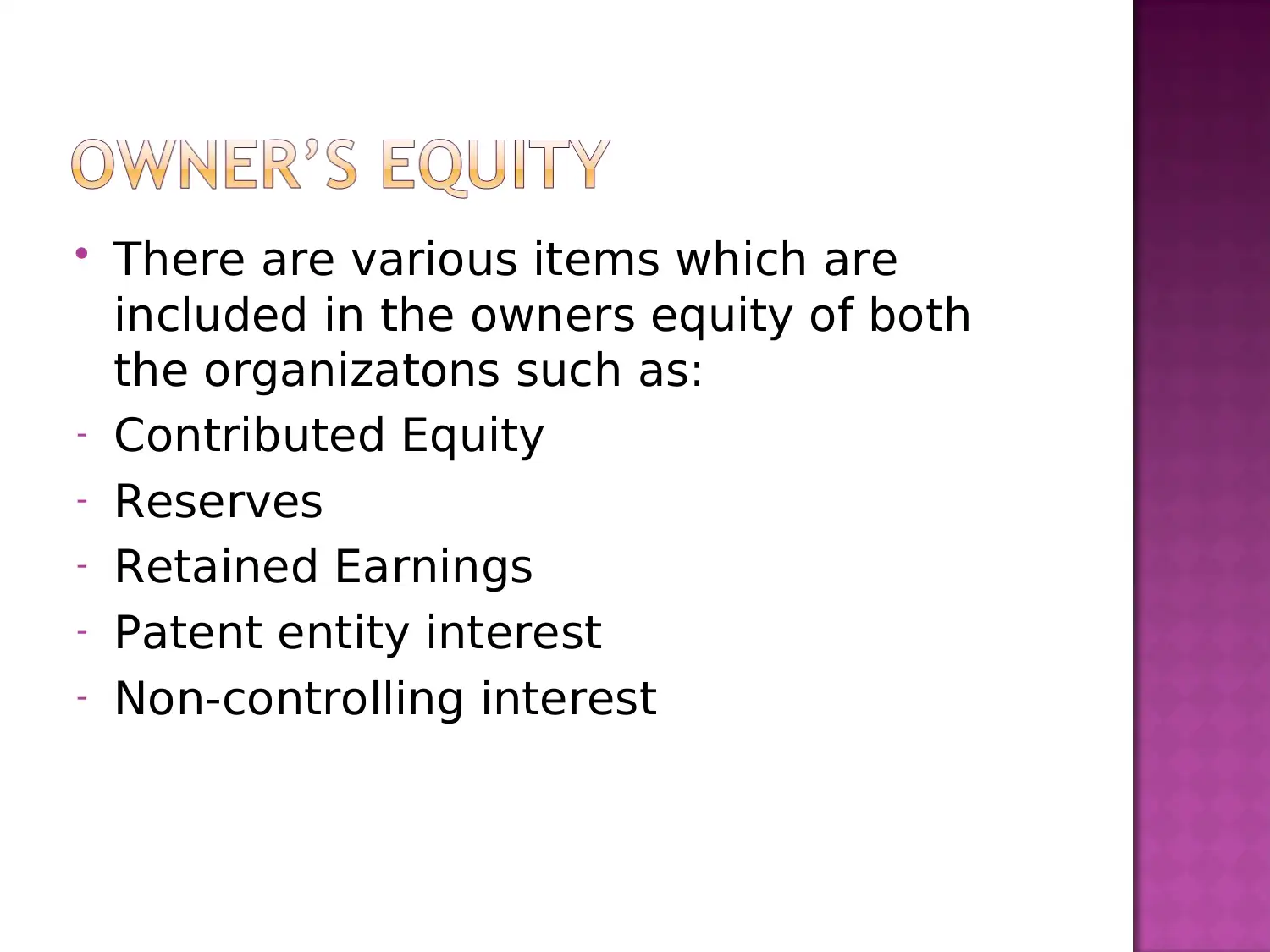

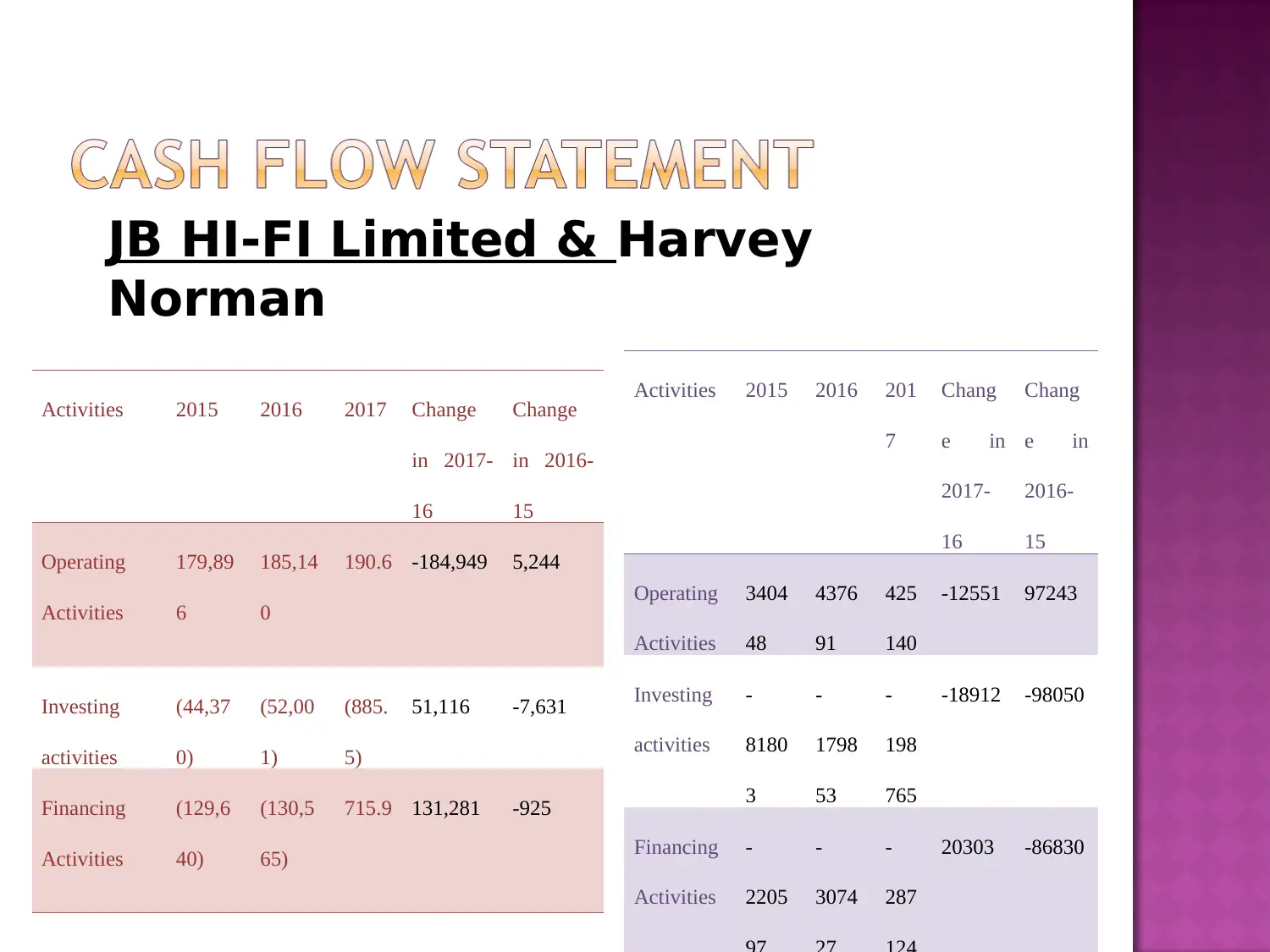

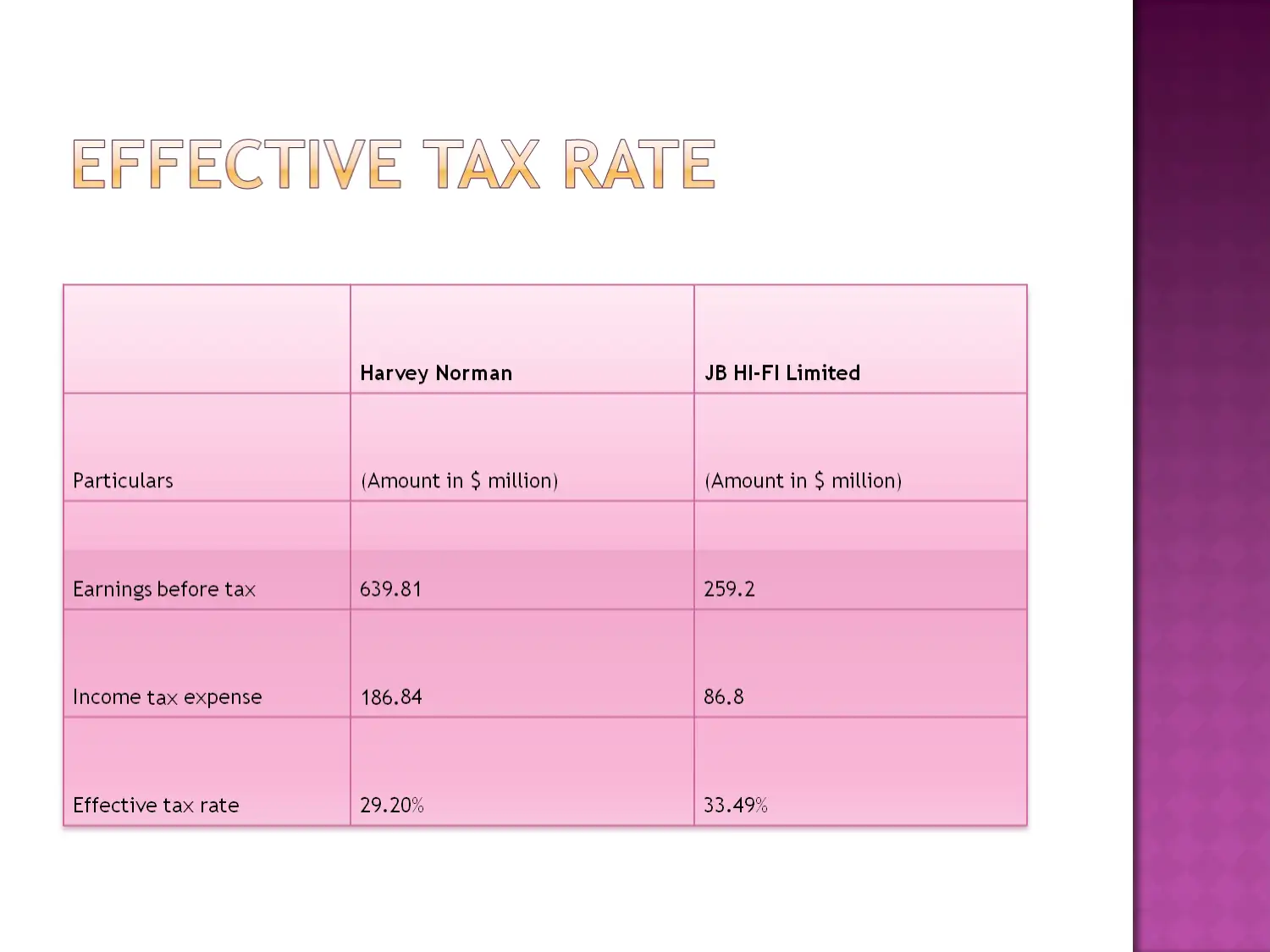

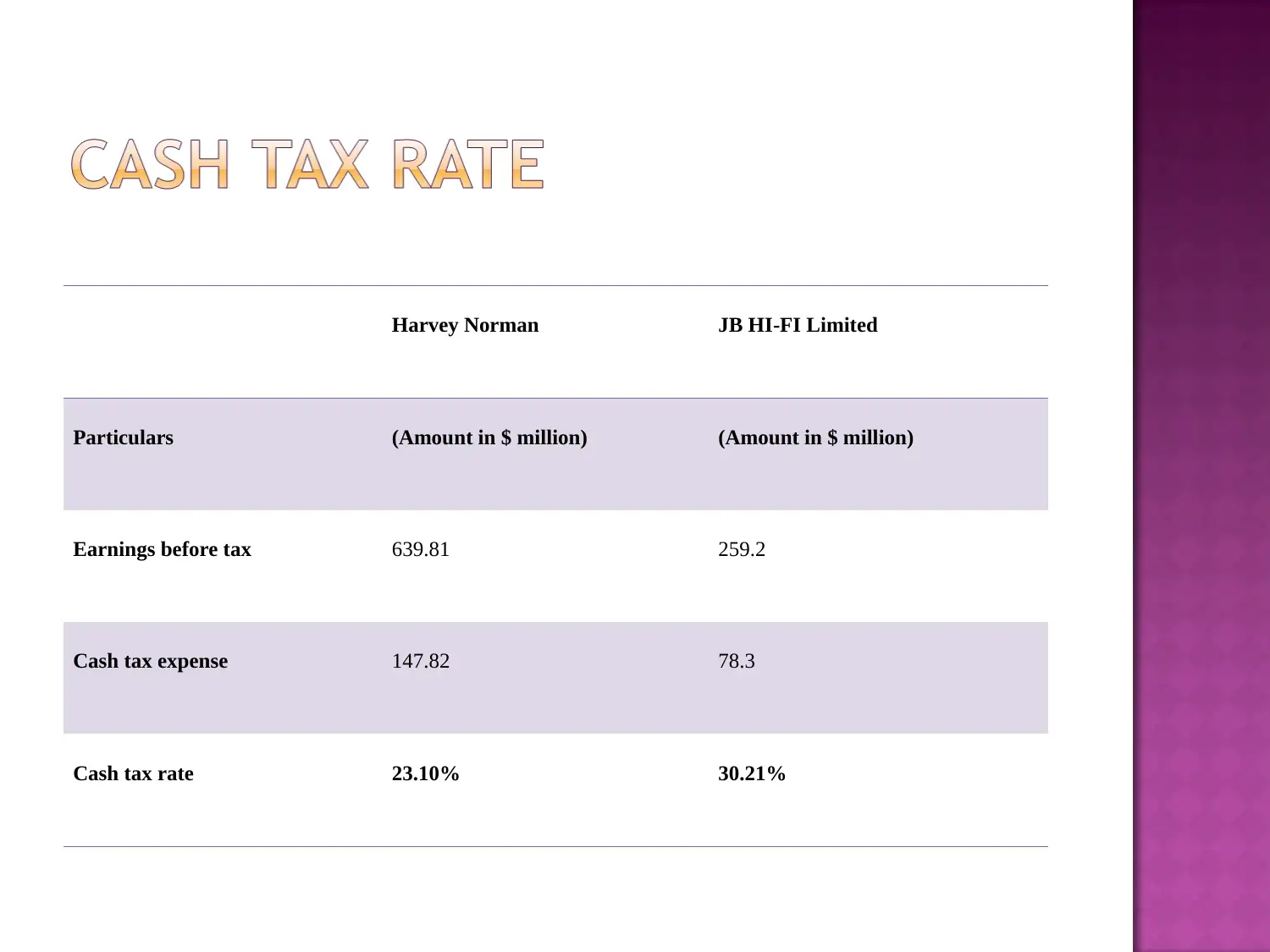

This report provides a financial analysis of JB HI-FI Limited and Harvey Norman, focusing on owner's equity, cash flow statements, and effective tax rates. The analysis includes a comparative look at contributed equity, reserves, retained earnings, and non-controlling interests for both organizations. Cash flow activities are detailed for the years 2015, 2016, and 2017, highlighting changes in operating, investing, and financing activities. The report also presents earnings before tax, cash tax expense, and cash tax rates for both companies. The conclusion emphasizes the importance of maintaining accurate financial records for effective decision-making. Desklib provides access to this report and other solved assignments to aid students in their studies.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.