Financial Analysis Project: Cash Conversion Cycle, NPV, IRR Analysis

VerifiedAdded on 2023/01/13

|17

|3971

|96

Project

AI Summary

This project delves into the core aspects of financial analysis, encompassing the evaluation of a company's financial data through various analytical techniques. The project begins with an introduction to financial analysis, emphasizing its role in assessing past and projected performance, cash flow, and risk, and its importance for both internal and external stakeholders. The main body of the project is divided into seven tasks. The first three tasks focus on the cash conversion cycle (CCC), its components (days inventory outstanding, days sales outstanding, and days payable outstanding), and methods to improve cash flow. Tasks four, five, and six involve the calculation of Net Present Value (NPV) and Internal Rate of Return (IRR) for investment projects. The final task discusses the limitations of the IRR technique. The project provides detailed calculations, interpretations, and analyses to demonstrate the application of financial analysis principles in real-world scenarios. The project underscores the importance of financial analysis in making informed strategic decisions and managing a company's financial health.

FINANCIAL ANALYSIS

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION

Financial analysis is characterised as a procedure of assessing financial information of

companies and evaluating each aspect by help of different techniques. In other words, this

can be defined as review of financial material to make strategic decisions. Usually this study

includes a summary of both past and expected productivity, cash flow, and risk. It can result

in the redistribution of personnel to or from an entity or a particular internal process

(Antonopoulos and Hall, 2018). This is crucial for corporations to do proper financial

analyse so that their stakeholders can aware from actual financial condition. This analysis is

useful for both to the internal and external stakeholders. As well as it also contributes in

analysing market trends, develop financial policies, construct long-term economic activity

strategies and classify projects or businesses. In order to do financial analysis of companies,

there are range of plans and methods that are applied by them. Eventually, without proper

financial analysis, this can be difficult for managers to take corrective actions (Tang and

Baker, 2016). It is so because if there will lack of financial information then this will be

difficult for managers to find a suitable framework to take appropriate actions.

The project report is based on different task which covers information about various

aspects. Basically, the report can be categorised into seven tasks in which first, second and

third task consists information about cash conversion cycle, methods to cash flow condition.

As well as in task four, five and six information about calculation of NPV, IRRetc. is done.

In the end of report, limitation of IRR technique is mentioned.

MAIN BODY

Task 1.

(a) What is cash conversion cycle (CCC)?

The term CCC can be defined as a type of matrix which is expressed in terms of time (Banerjee

and et.al., 2016). It calculates time period which is taken by a company in order to convert their

investments in stock and other sources in cash from sales. It is being calculated by including

different aspects such as inventory days, receivable days etc. Mainly it is computed by the

specific formula that is:

Days inventory outstanding + Days sales Outstanding – Days Payables outstanding

Financial analysis is characterised as a procedure of assessing financial information of

companies and evaluating each aspect by help of different techniques. In other words, this

can be defined as review of financial material to make strategic decisions. Usually this study

includes a summary of both past and expected productivity, cash flow, and risk. It can result

in the redistribution of personnel to or from an entity or a particular internal process

(Antonopoulos and Hall, 2018). This is crucial for corporations to do proper financial

analyse so that their stakeholders can aware from actual financial condition. This analysis is

useful for both to the internal and external stakeholders. As well as it also contributes in

analysing market trends, develop financial policies, construct long-term economic activity

strategies and classify projects or businesses. In order to do financial analysis of companies,

there are range of plans and methods that are applied by them. Eventually, without proper

financial analysis, this can be difficult for managers to take corrective actions (Tang and

Baker, 2016). It is so because if there will lack of financial information then this will be

difficult for managers to find a suitable framework to take appropriate actions.

The project report is based on different task which covers information about various

aspects. Basically, the report can be categorised into seven tasks in which first, second and

third task consists information about cash conversion cycle, methods to cash flow condition.

As well as in task four, five and six information about calculation of NPV, IRRetc. is done.

In the end of report, limitation of IRR technique is mentioned.

MAIN BODY

Task 1.

(a) What is cash conversion cycle (CCC)?

The term CCC can be defined as a type of matrix which is expressed in terms of time (Banerjee

and et.al., 2016). It calculates time period which is taken by a company in order to convert their

investments in stock and other sources in cash from sales. It is being calculated by including

different aspects such as inventory days, receivable days etc. Mainly it is computed by the

specific formula that is:

Days inventory outstanding + Days sales Outstanding – Days Payables outstanding

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

A smaller CCC is an indication of a period of better stock-to-sales. A smoother method is

suggested by a higher Cash conversion cycle. A low CCC is generally considered more

favourable, even if it focuses on the respective sector, market and abilities. Thus, it is stated that

CCC provide a valuable information which is helpful in comparing the performance of operation

and activities from the past performances.

(b) Analysis of three components of CCC?

It is based on three key components by which it is being calculated. Herein, underneath analysis

of these components is done in such manner:

Days inventory outstanding: This is also known as days’ sales of inventory which is

being used by companies to find out days in which a company holds stock before selling

(Brusca, Gómez‐villegas and Montesinos, 2016). In order to calculate the value of DIO

specific formula is used such as:

DIO = (Average Inventory ÷ Cost of Goods Sold) x 365

Average Stock = (Opening stock + closing stock) ÷ 2

Cost of goods sold = Opening stock + Purchases –closing stock.

Days sales outstanding: DSO is really the total number of hours between days the

receivable balances (the money owed to your business) are expected to be received.

Although cash-only transactions have a zero DSO, customers use company-extended

credit, so that this figure will be good. Thus in case of lower number of DSWO it is

consider to be more favourable. In context to determine the value of DSO specific

formula is used that is:

DSO = (Accounts Receivable ÷ Net Credit Sales) x 365

(Opening Receivables + closing Receivables) ÷ 2

Days Payable Outstanding: DPO is really the total time frame a corporation takes to

produce its payables from its providers to the companies owes money and to make proper

compensate for them (Siminica, Motoi and Dumitru, 2017). If this could be greatly

increased, the business can keep on to money longer, increasing the investment value;

thus, it is easier to have a longer DPO. Formula for determining the DPO is:

DPO = Closing Accounts Payable ÷ (COGS ÷ 365)

suggested by a higher Cash conversion cycle. A low CCC is generally considered more

favourable, even if it focuses on the respective sector, market and abilities. Thus, it is stated that

CCC provide a valuable information which is helpful in comparing the performance of operation

and activities from the past performances.

(b) Analysis of three components of CCC?

It is based on three key components by which it is being calculated. Herein, underneath analysis

of these components is done in such manner:

Days inventory outstanding: This is also known as days’ sales of inventory which is

being used by companies to find out days in which a company holds stock before selling

(Brusca, Gómez‐villegas and Montesinos, 2016). In order to calculate the value of DIO

specific formula is used such as:

DIO = (Average Inventory ÷ Cost of Goods Sold) x 365

Average Stock = (Opening stock + closing stock) ÷ 2

Cost of goods sold = Opening stock + Purchases –closing stock.

Days sales outstanding: DSO is really the total number of hours between days the

receivable balances (the money owed to your business) are expected to be received.

Although cash-only transactions have a zero DSO, customers use company-extended

credit, so that this figure will be good. Thus in case of lower number of DSWO it is

consider to be more favourable. In context to determine the value of DSO specific

formula is used that is:

DSO = (Accounts Receivable ÷ Net Credit Sales) x 365

(Opening Receivables + closing Receivables) ÷ 2

Days Payable Outstanding: DPO is really the total time frame a corporation takes to

produce its payables from its providers to the companies owes money and to make proper

compensate for them (Siminica, Motoi and Dumitru, 2017). If this could be greatly

increased, the business can keep on to money longer, increasing the investment value;

thus, it is easier to have a longer DPO. Formula for determining the DPO is:

DPO = Closing Accounts Payable ÷ (COGS ÷ 365)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

(Beginning Payable + Ending Payable) ÷ 2.

Task 2.

(a) Calculation of days’ inventory outstanding= Average inventory / COGS * 365 days

= 6500/40000*365 days

= 59 days

Analysis: On the basis of above calculation this can be find out that company is taking time

of 59 days in order to transfer their raw material into finished goods. As well as for selling

available amount of inventories to customers.

Working Note:

Average inventory= (Opening stock + closing stock)/2

= (1000+3000)/2

= 13000/2

= 6500

(b) Calculation of days’ sales outstanding= AR/ credit sales* 365 days

= 5000/120000*365 days

= 15.20 or 15 days

Analysis- As per above computed value of days’ sales outstanding, this may be assessed

that company taking time period of 15 days in order to receive debt amount from

different customers. This time period is effective.

Working Note:

Average AR= (Opening AR + closing AR) / 2

= (4000 + 6000)/2

= 5000

Task 2.

(a) Calculation of days’ inventory outstanding= Average inventory / COGS * 365 days

= 6500/40000*365 days

= 59 days

Analysis: On the basis of above calculation this can be find out that company is taking time

of 59 days in order to transfer their raw material into finished goods. As well as for selling

available amount of inventories to customers.

Working Note:

Average inventory= (Opening stock + closing stock)/2

= (1000+3000)/2

= 13000/2

= 6500

(b) Calculation of days’ sales outstanding= AR/ credit sales* 365 days

= 5000/120000*365 days

= 15.20 or 15 days

Analysis- As per above computed value of days’ sales outstanding, this may be assessed

that company taking time period of 15 days in order to receive debt amount from

different customers. This time period is effective.

Working Note:

Average AR= (Opening AR + closing AR) / 2

= (4000 + 6000)/2

= 5000

(c) Calculation of days payable outstanding= Accounts payable / cost of goods sold*365

days

= 1500/40000*365 days

= 13.68 or 14 days

Analysis- As per the above calculated value of days payable outstanding, this can be find

out that its value is of 14 days. It means company is taking this time period in order to

make payment to their creditors.

(d) Calculation of cash conversion cycle= Day inventory outstanding + Days sales

outstanding – Day payable outstanding

= (59 + 15 – 14) days

= 60 days

Analysis- The CCC is of 60 days, that is prepared by making addition of days’ inventory

outstanding and days sales outstanding.

Task 3.

Ways to improve cash flow condition of company in accordance of above scenario.

The term cash flow can be defined as flow of cash during a particular time frame. It is

beneficial for companies if there is inflow of cash and higher outflow shows negative condition

of a company. Due to which, it becomes essential for corporations to enhance cash flow in a

better manner. Herein, underneath way to improve cash flow are mentioned in such manner:

By improving inventory- This is an effective way to improve cash flow condition for a

company. It is so because if inventory will have managed in an efficient way then it

becomes easier to companies to minimise cost of storage (Cantillon, Maître and Watson,

2016). Such as in the aspect of above calculated value of days’ inventory, it can be find

out that it is of 59 days. It is indicating that this is too higher. Hence, this is essential for

above company that they should minimise it as soon as possible.

Send out invoices immediately- In addition, sending invoices immediately to customers

so that company can recover payment on time is also important. It is so because if

companies will send invoices on right time then customers will be liable to pay before

days

= 1500/40000*365 days

= 13.68 or 14 days

Analysis- As per the above calculated value of days payable outstanding, this can be find

out that its value is of 14 days. It means company is taking this time period in order to

make payment to their creditors.

(d) Calculation of cash conversion cycle= Day inventory outstanding + Days sales

outstanding – Day payable outstanding

= (59 + 15 – 14) days

= 60 days

Analysis- The CCC is of 60 days, that is prepared by making addition of days’ inventory

outstanding and days sales outstanding.

Task 3.

Ways to improve cash flow condition of company in accordance of above scenario.

The term cash flow can be defined as flow of cash during a particular time frame. It is

beneficial for companies if there is inflow of cash and higher outflow shows negative condition

of a company. Due to which, it becomes essential for corporations to enhance cash flow in a

better manner. Herein, underneath way to improve cash flow are mentioned in such manner:

By improving inventory- This is an effective way to improve cash flow condition for a

company. It is so because if inventory will have managed in an efficient way then it

becomes easier to companies to minimise cost of storage (Cantillon, Maître and Watson,

2016). Such as in the aspect of above calculated value of days’ inventory, it can be find

out that it is of 59 days. It is indicating that this is too higher. Hence, this is essential for

above company that they should minimise it as soon as possible.

Send out invoices immediately- In addition, sending invoices immediately to customers

so that company can recover payment on time is also important. It is so because if

companies will send invoices on right time then customers will be liable to pay before

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

due date. By doing so, companies will get cash on time and before due date. Such as in

the aspect of above calculation, it can be find out that days’ outstanding sales is of 15

days which is impressive. Hence, companies should try to minimise days of outstanding

sales so that they can recover fund from creditors on time.

Paying less to suppliers- The suppliers are those who sell raw material and other form of

goods to companies on debt or cash. In order to enhance cash flow of companies, this is

essential to pay less to suppliers. It means company should buy raw materials from those

suppliers who are providing discount as well as ready to get payment in instalments. By

doing so, this will be easier for companies to protect funds as reserve. So this is also an

effective way to improve cash flow position of companies (Engel and et.al., 2016).

Liquidate old inventory- In the business firms purchasing of inventories is a huge

expense. Herein, it is important to know that all types of inventories are not used in

operations. Thus, companies should try to sell out those inventories which are old and

cannot be used. By doing so, level of cash flow will enhance and because selling of old

assets will produce cash and as a result cash flow condition will be better.

So, these are the ways which can be helpful for companies in order to enhance their cash flow as

well as the above mentioned methods can contribute to increasing efficiency in other operations.

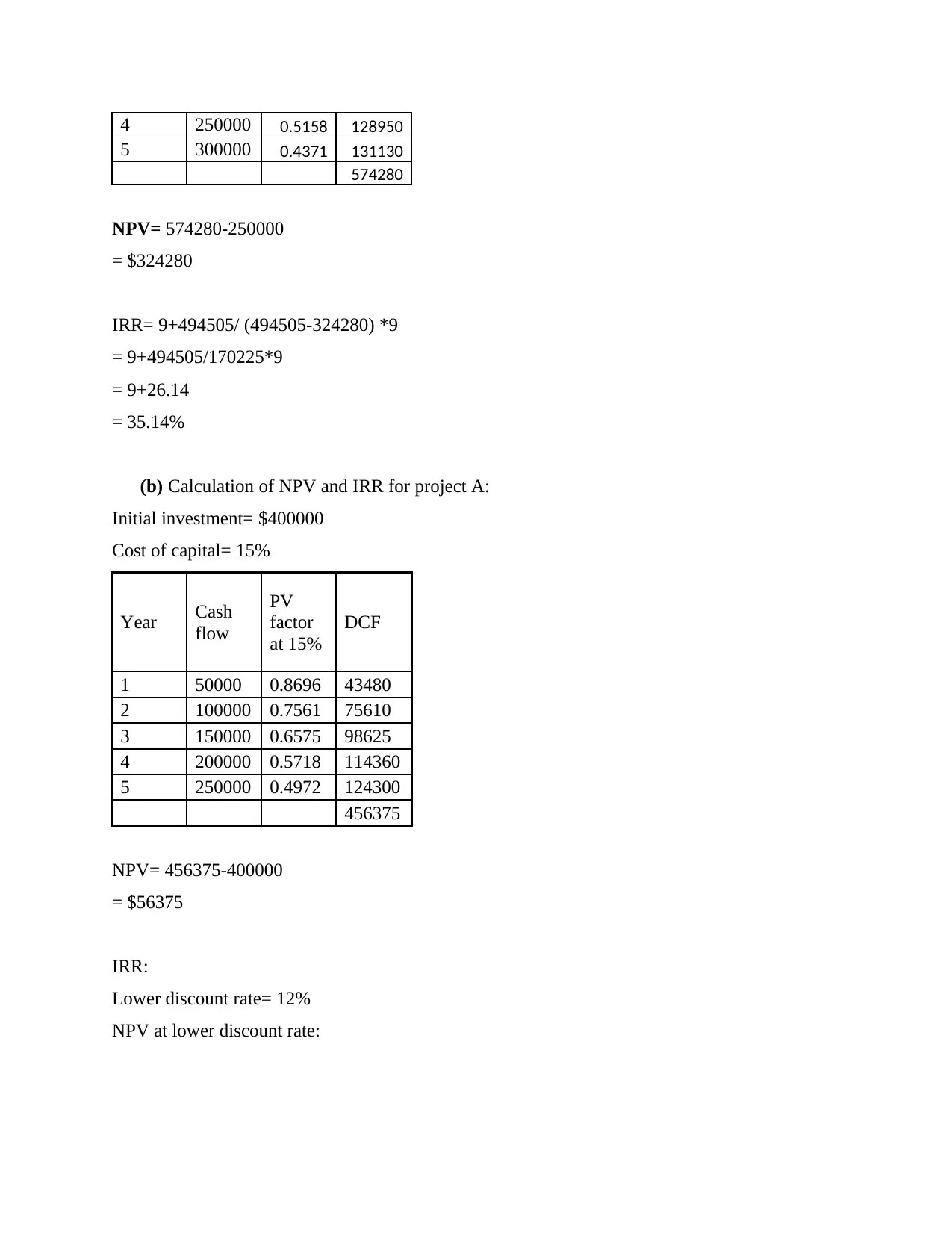

Task 4.

(a) Calculation of NPV and IRR:

NPV- The net present value method is a process of computing PV of a project. Under this,

variation between DCF and initial investment is calculated (Ferguson and Morton-

Huddleston, 2016). The value of discounted cash flow is calculated by help of present value

factor. Herein, below calculation of NPV is done of project X in such manner:

Year Cash

flow

PV

factor

at 10%

DCF

1 100000 0.9091 90910

2 150000 0.8264 123960

3 200000 0.7513 150260

the aspect of above calculation, it can be find out that days’ outstanding sales is of 15

days which is impressive. Hence, companies should try to minimise days of outstanding

sales so that they can recover fund from creditors on time.

Paying less to suppliers- The suppliers are those who sell raw material and other form of

goods to companies on debt or cash. In order to enhance cash flow of companies, this is

essential to pay less to suppliers. It means company should buy raw materials from those

suppliers who are providing discount as well as ready to get payment in instalments. By

doing so, this will be easier for companies to protect funds as reserve. So this is also an

effective way to improve cash flow position of companies (Engel and et.al., 2016).

Liquidate old inventory- In the business firms purchasing of inventories is a huge

expense. Herein, it is important to know that all types of inventories are not used in

operations. Thus, companies should try to sell out those inventories which are old and

cannot be used. By doing so, level of cash flow will enhance and because selling of old

assets will produce cash and as a result cash flow condition will be better.

So, these are the ways which can be helpful for companies in order to enhance their cash flow as

well as the above mentioned methods can contribute to increasing efficiency in other operations.

Task 4.

(a) Calculation of NPV and IRR:

NPV- The net present value method is a process of computing PV of a project. Under this,

variation between DCF and initial investment is calculated (Ferguson and Morton-

Huddleston, 2016). The value of discounted cash flow is calculated by help of present value

factor. Herein, below calculation of NPV is done of project X in such manner:

Year Cash

flow

PV

factor

at 10%

DCF

1 100000 0.9091 90910

2 150000 0.8264 123960

3 200000 0.7513 150260

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

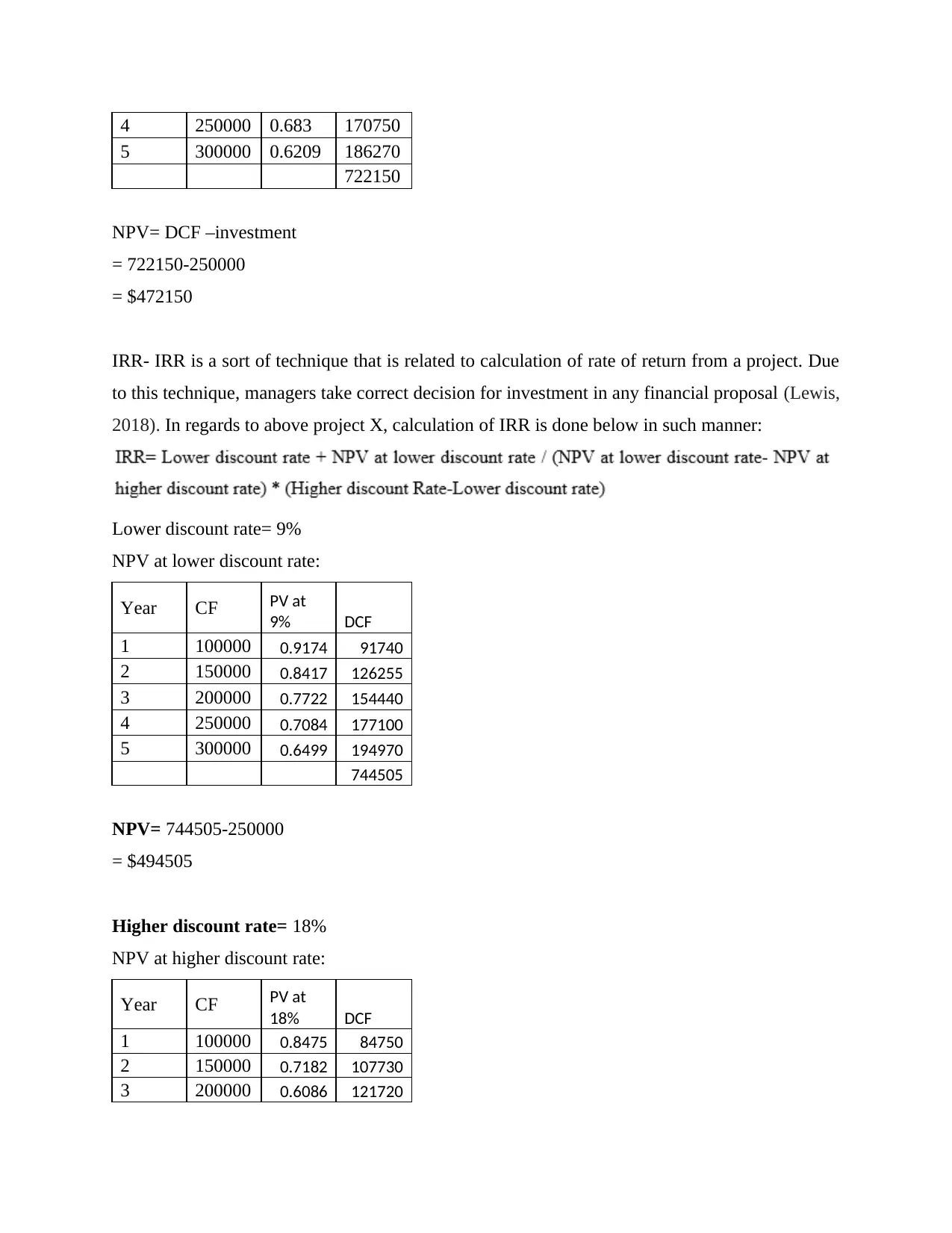

4 250000 0.683 170750

5 300000 0.6209 186270

722150

NPV= DCF –investment

= 722150-250000

= $472150

IRR- IRR is a sort of technique that is related to calculation of rate of return from a project. Due

to this technique, managers take correct decision for investment in any financial proposal (Lewis,

2018). In regards to above project X, calculation of IRR is done below in such manner:

Lower discount rate= 9%

NPV at lower discount rate:

Year CF PV at

9% DCF

1 100000 0.9174 91740

2 150000 0.8417 126255

3 200000 0.7722 154440

4 250000 0.7084 177100

5 300000 0.6499 194970

744505

NPV= 744505-250000

= $494505

Higher discount rate= 18%

NPV at higher discount rate:

Year CF PV at

18% DCF

1 100000 0.8475 84750

2 150000 0.7182 107730

3 200000 0.6086 121720

5 300000 0.6209 186270

722150

NPV= DCF –investment

= 722150-250000

= $472150

IRR- IRR is a sort of technique that is related to calculation of rate of return from a project. Due

to this technique, managers take correct decision for investment in any financial proposal (Lewis,

2018). In regards to above project X, calculation of IRR is done below in such manner:

Lower discount rate= 9%

NPV at lower discount rate:

Year CF PV at

9% DCF

1 100000 0.9174 91740

2 150000 0.8417 126255

3 200000 0.7722 154440

4 250000 0.7084 177100

5 300000 0.6499 194970

744505

NPV= 744505-250000

= $494505

Higher discount rate= 18%

NPV at higher discount rate:

Year CF PV at

18% DCF

1 100000 0.8475 84750

2 150000 0.7182 107730

3 200000 0.6086 121720

4 250000 0.5158 128950

5 300000 0.4371 131130

574280

NPV= 574280-250000

= $324280

IRR= 9+494505/ (494505-324280) *9

= 9+494505/170225*9

= 9+26.14

= 35.14%

(b) Calculation of NPV and IRR for project A:

Initial investment= $400000

Cost of capital= 15%

Year Cash

flow

PV

factor

at 15%

DCF

1 50000 0.8696 43480

2 100000 0.7561 75610

3 150000 0.6575 98625

4 200000 0.5718 114360

5 250000 0.4972 124300

456375

NPV= 456375-400000

= $56375

IRR:

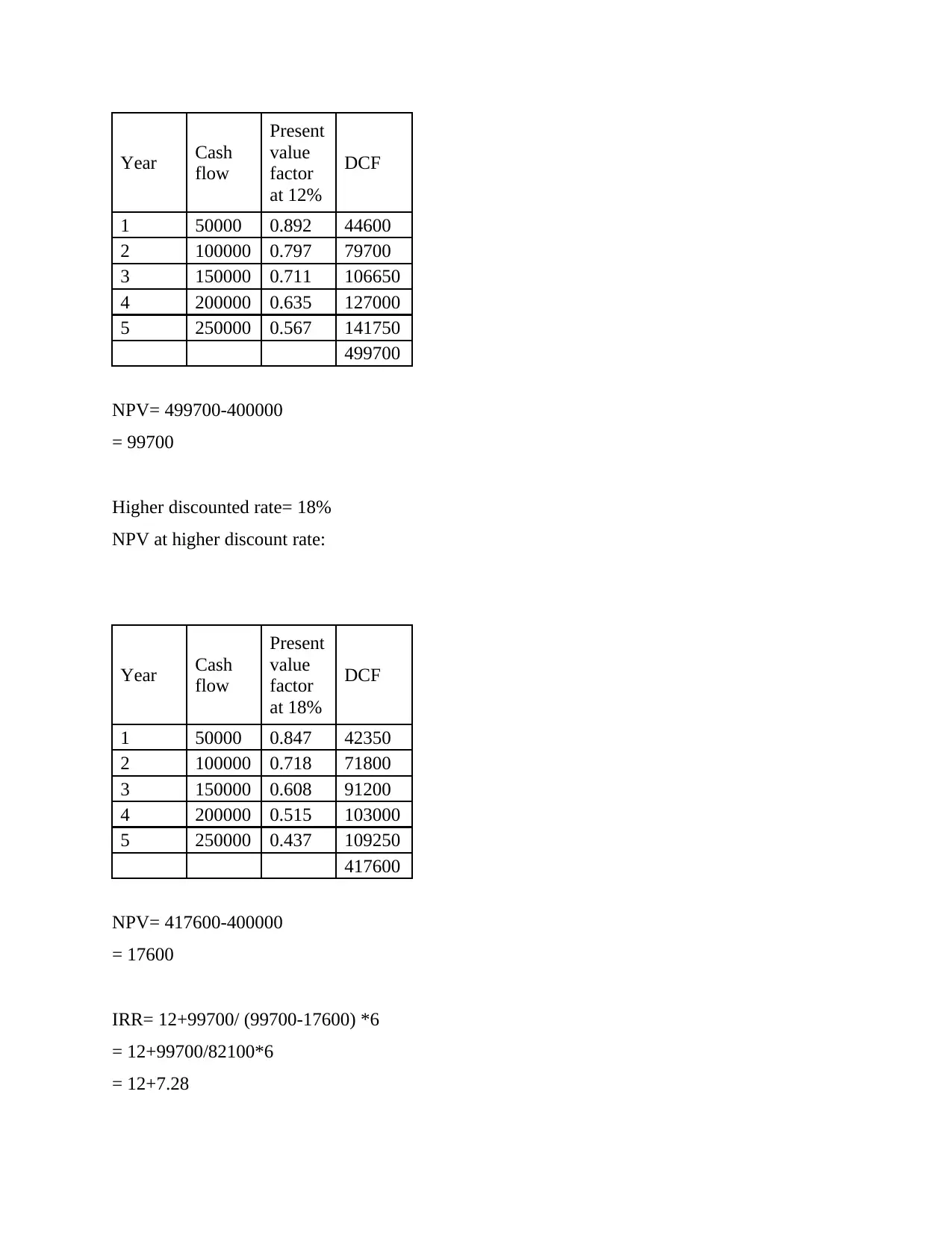

Lower discount rate= 12%

NPV at lower discount rate:

5 300000 0.4371 131130

574280

NPV= 574280-250000

= $324280

IRR= 9+494505/ (494505-324280) *9

= 9+494505/170225*9

= 9+26.14

= 35.14%

(b) Calculation of NPV and IRR for project A:

Initial investment= $400000

Cost of capital= 15%

Year Cash

flow

PV

factor

at 15%

DCF

1 50000 0.8696 43480

2 100000 0.7561 75610

3 150000 0.6575 98625

4 200000 0.5718 114360

5 250000 0.4972 124300

456375

NPV= 456375-400000

= $56375

IRR:

Lower discount rate= 12%

NPV at lower discount rate:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Year Cash

flow

Present

value

factor

at 12%

DCF

1 50000 0.892 44600

2 100000 0.797 79700

3 150000 0.711 106650

4 200000 0.635 127000

5 250000 0.567 141750

499700

NPV= 499700-400000

= 99700

Higher discounted rate= 18%

NPV at higher discount rate:

Year Cash

flow

Present

value

factor

at 18%

DCF

1 50000 0.847 42350

2 100000 0.718 71800

3 150000 0.608 91200

4 200000 0.515 103000

5 250000 0.437 109250

417600

NPV= 417600-400000

= 17600

IRR= 12+99700/ (99700-17600) *6

= 12+99700/82100*6

= 12+7.28

flow

Present

value

factor

at 12%

DCF

1 50000 0.892 44600

2 100000 0.797 79700

3 150000 0.711 106650

4 200000 0.635 127000

5 250000 0.567 141750

499700

NPV= 499700-400000

= 99700

Higher discounted rate= 18%

NPV at higher discount rate:

Year Cash

flow

Present

value

factor

at 18%

DCF

1 50000 0.847 42350

2 100000 0.718 71800

3 150000 0.608 91200

4 200000 0.515 103000

5 250000 0.437 109250

417600

NPV= 417600-400000

= 17600

IRR= 12+99700/ (99700-17600) *6

= 12+99700/82100*6

= 12+7.28

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

= 19.28%

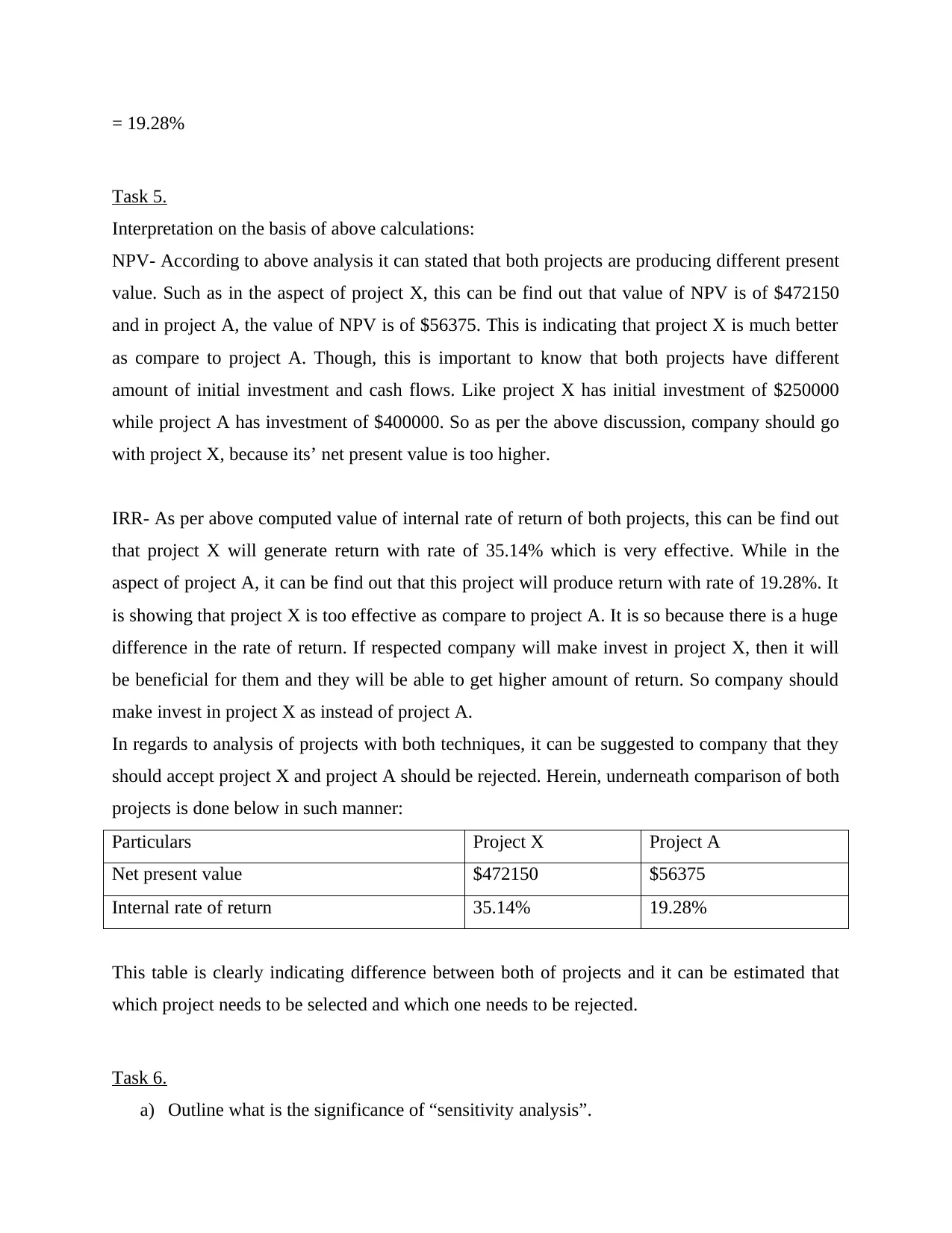

Task 5.

Interpretation on the basis of above calculations:

NPV- According to above analysis it can stated that both projects are producing different present

value. Such as in the aspect of project X, this can be find out that value of NPV is of $472150

and in project A, the value of NPV is of $56375. This is indicating that project X is much better

as compare to project A. Though, this is important to know that both projects have different

amount of initial investment and cash flows. Like project X has initial investment of $250000

while project A has investment of $400000. So as per the above discussion, company should go

with project X, because its’ net present value is too higher.

IRR- As per above computed value of internal rate of return of both projects, this can be find out

that project X will generate return with rate of 35.14% which is very effective. While in the

aspect of project A, it can be find out that this project will produce return with rate of 19.28%. It

is showing that project X is too effective as compare to project A. It is so because there is a huge

difference in the rate of return. If respected company will make invest in project X, then it will

be beneficial for them and they will be able to get higher amount of return. So company should

make invest in project X as instead of project A.

In regards to analysis of projects with both techniques, it can be suggested to company that they

should accept project X and project A should be rejected. Herein, underneath comparison of both

projects is done below in such manner:

Particulars Project X Project A

Net present value $472150 $56375

Internal rate of return 35.14% 19.28%

This table is clearly indicating difference between both of projects and it can be estimated that

which project needs to be selected and which one needs to be rejected.

Task 6.

a) Outline what is the significance of “sensitivity analysis”.

Task 5.

Interpretation on the basis of above calculations:

NPV- According to above analysis it can stated that both projects are producing different present

value. Such as in the aspect of project X, this can be find out that value of NPV is of $472150

and in project A, the value of NPV is of $56375. This is indicating that project X is much better

as compare to project A. Though, this is important to know that both projects have different

amount of initial investment and cash flows. Like project X has initial investment of $250000

while project A has investment of $400000. So as per the above discussion, company should go

with project X, because its’ net present value is too higher.

IRR- As per above computed value of internal rate of return of both projects, this can be find out

that project X will generate return with rate of 35.14% which is very effective. While in the

aspect of project A, it can be find out that this project will produce return with rate of 19.28%. It

is showing that project X is too effective as compare to project A. It is so because there is a huge

difference in the rate of return. If respected company will make invest in project X, then it will

be beneficial for them and they will be able to get higher amount of return. So company should

make invest in project X as instead of project A.

In regards to analysis of projects with both techniques, it can be suggested to company that they

should accept project X and project A should be rejected. Herein, underneath comparison of both

projects is done below in such manner:

Particulars Project X Project A

Net present value $472150 $56375

Internal rate of return 35.14% 19.28%

This table is clearly indicating difference between both of projects and it can be estimated that

which project needs to be selected and which one needs to be rejected.

Task 6.

a) Outline what is the significance of “sensitivity analysis”.

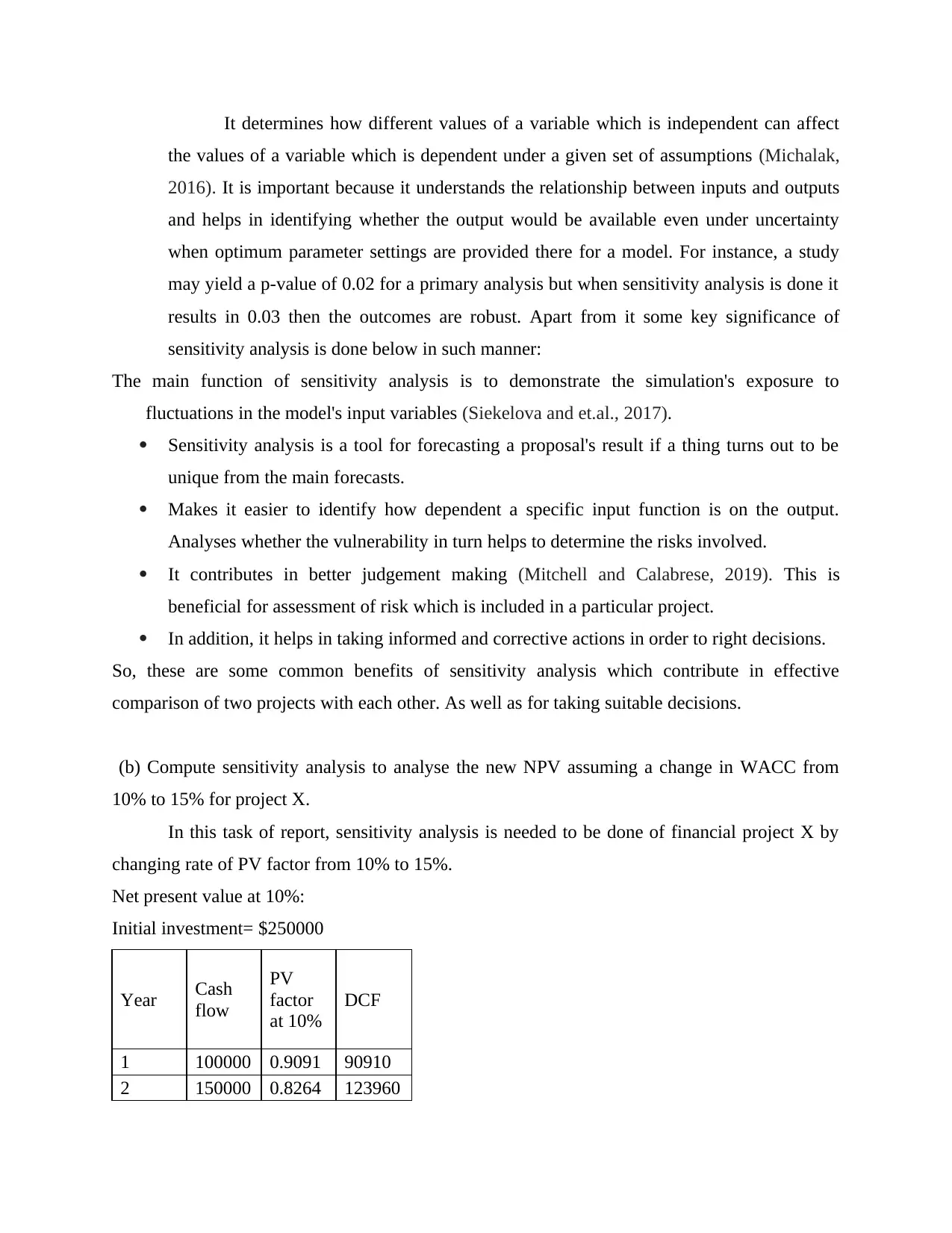

It determines how different values of a variable which is independent can affect

the values of a variable which is dependent under a given set of assumptions (Michalak,

2016). It is important because it understands the relationship between inputs and outputs

and helps in identifying whether the output would be available even under uncertainty

when optimum parameter settings are provided there for a model. For instance, a study

may yield a p-value of 0.02 for a primary analysis but when sensitivity analysis is done it

results in 0.03 then the outcomes are robust. Apart from it some key significance of

sensitivity analysis is done below in such manner:

The main function of sensitivity analysis is to demonstrate the simulation's exposure to

fluctuations in the model's input variables (Siekelova and et.al., 2017).

Sensitivity analysis is a tool for forecasting a proposal's result if a thing turns out to be

unique from the main forecasts.

Makes it easier to identify how dependent a specific input function is on the output.

Analyses whether the vulnerability in turn helps to determine the risks involved.

It contributes in better judgement making (Mitchell and Calabrese, 2019). This is

beneficial for assessment of risk which is included in a particular project.

In addition, it helps in taking informed and corrective actions in order to right decisions.

So, these are some common benefits of sensitivity analysis which contribute in effective

comparison of two projects with each other. As well as for taking suitable decisions.

(b) Compute sensitivity analysis to analyse the new NPV assuming a change in WACC from

10% to 15% for project X.

In this task of report, sensitivity analysis is needed to be done of financial project X by

changing rate of PV factor from 10% to 15%.

Net present value at 10%:

Initial investment= $250000

Year Cash

flow

PV

factor

at 10%

DCF

1 100000 0.9091 90910

2 150000 0.8264 123960

the values of a variable which is dependent under a given set of assumptions (Michalak,

2016). It is important because it understands the relationship between inputs and outputs

and helps in identifying whether the output would be available even under uncertainty

when optimum parameter settings are provided there for a model. For instance, a study

may yield a p-value of 0.02 for a primary analysis but when sensitivity analysis is done it

results in 0.03 then the outcomes are robust. Apart from it some key significance of

sensitivity analysis is done below in such manner:

The main function of sensitivity analysis is to demonstrate the simulation's exposure to

fluctuations in the model's input variables (Siekelova and et.al., 2017).

Sensitivity analysis is a tool for forecasting a proposal's result if a thing turns out to be

unique from the main forecasts.

Makes it easier to identify how dependent a specific input function is on the output.

Analyses whether the vulnerability in turn helps to determine the risks involved.

It contributes in better judgement making (Mitchell and Calabrese, 2019). This is

beneficial for assessment of risk which is included in a particular project.

In addition, it helps in taking informed and corrective actions in order to right decisions.

So, these are some common benefits of sensitivity analysis which contribute in effective

comparison of two projects with each other. As well as for taking suitable decisions.

(b) Compute sensitivity analysis to analyse the new NPV assuming a change in WACC from

10% to 15% for project X.

In this task of report, sensitivity analysis is needed to be done of financial project X by

changing rate of PV factor from 10% to 15%.

Net present value at 10%:

Initial investment= $250000

Year Cash

flow

PV

factor

at 10%

DCF

1 100000 0.9091 90910

2 150000 0.8264 123960

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.