Financial Analysis Report: Comparing KOSE Corp and Shiseido Co Ltd

VerifiedAdded on 2020/07/23

|58

|5288

|34

Report

AI Summary

This report presents a comprehensive financial analysis comparing KOSE Corp and Shiseido Co Ltd, two key players in the personal care products sector. The analysis begins with an industry overview, utilizing Porter's Five Forces to assess the competitive landscape. Company overviews provide background on KOSE Corp and Shiseido Co Ltd, followed by a discussion of the approach and methodology employed, including data gathered from annual reports and market analysis. The report reviews management and director's reports, including disclosures, auditor's reports, and forecasts. A detailed financial statement analysis is conducted, encompassing business analysis, SWOT analysis, and the analysis of key performance indicators such as profitability, efficiency, and liquidity ratios. Trend analysis, common size financial statement analysis, and Altman Z-scores are also included. The report also reviews latest market developments and internal and external factors influencing the companies. Finally, the report concludes with a summary of findings and recommendations, supported by references and appendices including financial statements and ratio calculations.

Financial Analysis

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

1. INTRODUCTION.......................................................................................................................1

1.1 Industry overview..................................................................................................................1

1.2 Company overview................................................................................................................1

1.2.1 KOSE Corp.........................................................................................................................1

1.2.2 Shiseido Co Ltd..................................................................................................................2

1.3 Approach and methodology...................................................................................................2

2. REVIEW ANALYSIS OF MANAGEMENT &DIRECTOR’S REPORT.................................2

2.1 Disclosure and announcement by the companies..................................................................2

2.2 Review of auditor’s report.....................................................................................................2

2.3 Forecasts and potential investment strategies........................................................................3

3. FINANCIAL STATEMENT ANALYSIS..................................................................................4

3.1 Background............................................................................................................................4

3.2 Business analysis...................................................................................................................4

3.3 Analysis of key performance indicators................................................................................5

3.3.5 Trend analysis or share price movement..........................................................................17

3.3.6 Common size financial statement analysis.......................................................................18

3.3.7 Altman Z score.................................................................................................................19

4. REVIEW OF LATEST DEVELOPMENTS............................................................................19

4.1 Market news, trends and developments...............................................................................19

4.2 Internal and external factors................................................................................................20

5. SUMMARY AND RECOMMENDATIONS...........................................................................20

REFERENCES..............................................................................................................................21

APPENDIX....................................................................................................................................23

Income statement of KOSE Corp as at March2015.................................................................23

1. INTRODUCTION.......................................................................................................................1

1.1 Industry overview..................................................................................................................1

1.2 Company overview................................................................................................................1

1.2.1 KOSE Corp.........................................................................................................................1

1.2.2 Shiseido Co Ltd..................................................................................................................2

1.3 Approach and methodology...................................................................................................2

2. REVIEW ANALYSIS OF MANAGEMENT &DIRECTOR’S REPORT.................................2

2.1 Disclosure and announcement by the companies..................................................................2

2.2 Review of auditor’s report.....................................................................................................2

2.3 Forecasts and potential investment strategies........................................................................3

3. FINANCIAL STATEMENT ANALYSIS..................................................................................4

3.1 Background............................................................................................................................4

3.2 Business analysis...................................................................................................................4

3.3 Analysis of key performance indicators................................................................................5

3.3.5 Trend analysis or share price movement..........................................................................17

3.3.6 Common size financial statement analysis.......................................................................18

3.3.7 Altman Z score.................................................................................................................19

4. REVIEW OF LATEST DEVELOPMENTS............................................................................19

4.1 Market news, trends and developments...............................................................................19

4.2 Internal and external factors................................................................................................20

5. SUMMARY AND RECOMMENDATIONS...........................................................................20

REFERENCES..............................................................................................................................21

APPENDIX....................................................................................................................................23

Income statement of KOSE Corp as at March2015.................................................................23

Income statement of KOSE Corp as at March2016 & 2017....................................................25

Balance sheet of KOSE Corp as at March 2015.......................................................................27

Balance sheet of KOSE Corp as at March 2016 & 2017.........................................................29

Income statement of Shiseido Co Ltdas at March 2015...........................................................36

Income statement of Shiseido Co Ltdas at December 2015& 2016.........................................37

Balance sheet of Shiseido Co Ltd as at March 2015................................................................38

Balance sheet of Shiseido Co Ltd as at December 2015& 2016..............................................40

6. Ratio analysis of Shiseido Co Ltd.........................................................................................45

7. Common size financial statement analysis............................................................................47

8. EV/ EBITDA ratio.................................................................................................................47

Balance sheet of KOSE Corp as at March 2015.......................................................................27

Balance sheet of KOSE Corp as at March 2016 & 2017.........................................................29

Income statement of Shiseido Co Ltdas at March 2015...........................................................36

Income statement of Shiseido Co Ltdas at December 2015& 2016.........................................37

Balance sheet of Shiseido Co Ltd as at March 2015................................................................38

Balance sheet of Shiseido Co Ltd as at December 2015& 2016..............................................40

6. Ratio analysis of Shiseido Co Ltd.........................................................................................45

7. Common size financial statement analysis............................................................................47

8. EV/ EBITDA ratio.................................................................................................................47

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1. INTRODUCTION

1.1 Industry overview

Porter five forceanalysis of personal care products sector:

Bargaining power of buyers

From assessment, it has been identified that in the

cosmetic sector customer’s have high bargaining

power. The main reasons behind such high power

arehigh competition and availability of

manufactures which offer beauty products.

Bargaining power of suppliers

Cosmetic sector of is filled up with the low

bargaining power of suppliers. Large number of

market players and supply of diversified products is

one of the main reasons behind the decreasing

power.

Threat of substitutes

In \the concerned sector, high level of threat exists

from the substitute products. Hence, if

manufacturers will charge higher prices and

compromise with the quality aspect then there is a

risk that customers switch on others.

Threat from new entrants

Low threat exists in the personal care products

sector due to high cost, resource requirements s etc.

Besides this, in the cosmetic industry, due to the

aspect of customer loyalty it is not possible for the

new entrant to survive.

Competition intensity: In the cosmetic sector, competitive rivalry is highbecause there are leading

companies which provide customers with high quality personal care products. It includesShiseido Co Ltd,

Kao, Mandom, KOSE, MoltonBrown etc.

1.2 Company overview

For the present report, two companies have been selected namely KOSE Corp and

Shiseido Co Ltd. Brief introduction of such companies are enumerated below:

1.2.1 KOSE Corp

KOSE Corporation is one of the leading Japanese company which operates at global

level. It offers personal care products to the customers such as cosmetic, skin and hair care.

Further, to assess the financial position and performance of KOSE in against to the competitor

Shiseido has been considered.

1.1 Industry overview

Porter five forceanalysis of personal care products sector:

Bargaining power of buyers

From assessment, it has been identified that in the

cosmetic sector customer’s have high bargaining

power. The main reasons behind such high power

arehigh competition and availability of

manufactures which offer beauty products.

Bargaining power of suppliers

Cosmetic sector of is filled up with the low

bargaining power of suppliers. Large number of

market players and supply of diversified products is

one of the main reasons behind the decreasing

power.

Threat of substitutes

In \the concerned sector, high level of threat exists

from the substitute products. Hence, if

manufacturers will charge higher prices and

compromise with the quality aspect then there is a

risk that customers switch on others.

Threat from new entrants

Low threat exists in the personal care products

sector due to high cost, resource requirements s etc.

Besides this, in the cosmetic industry, due to the

aspect of customer loyalty it is not possible for the

new entrant to survive.

Competition intensity: In the cosmetic sector, competitive rivalry is highbecause there are leading

companies which provide customers with high quality personal care products. It includesShiseido Co Ltd,

Kao, Mandom, KOSE, MoltonBrown etc.

1.2 Company overview

For the present report, two companies have been selected namely KOSE Corp and

Shiseido Co Ltd. Brief introduction of such companies are enumerated below:

1.2.1 KOSE Corp

KOSE Corporation is one of the leading Japanese company which operates at global

level. It offers personal care products to the customers such as cosmetic, skin and hair care.

Further, to assess the financial position and performance of KOSE in against to the competitor

Shiseido has been considered.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1.2.2 Shiseido Co Ltd

Shiseido is known as the producer of quality skin and hair care, cosmetic and fragrance

related products. Such Japanese company has secured first position in Japan and fifth in the

world. Both the companies which are undertaken for the study listed on and traded through

Tokyo stock exchange.

1.3 Approach and methodology

With the motive to evaluate financial results of KOSE over the rival firm such as

Shiseido Co Ltddata has been gathered through the annual reports of such companies. Hence, by

accessing incomestatement and balance sheet of KOSE as well as Shiseido, pertaining to 5 years

from 2012 to 2016, data has been gathered. Along with this, to present the better view ofissue

latest economic developments and company’s latest announcements as well as forecasts have

also been evaluated. Hence, main source of information considered for the present study are as

follows:

Annual reports of KOSE and Shiseido

Journals and articles related personal care sector

2. REVIEW ANALYSIS OF MANAGEMENT &DIRECTOR’S REPORT

2.1 Disclosure and announcement by the companies

On 4th March 2014, KOSE announced that it has signed agreement in relation to

acquiring 14856 shares. This aspect shows that KOSE stake in Tarte accounts for 93.5%

respectively whose value is Japan yen135 significantly.

2.2 Review of auditor’s report

Auditor’s report of KOSE Corp shows that financial statements of the concerned

organization are free from errors. Besides this, auditors entailed in their report that company has

made fair distribution of benefits among the shareholders and other stakeholders.

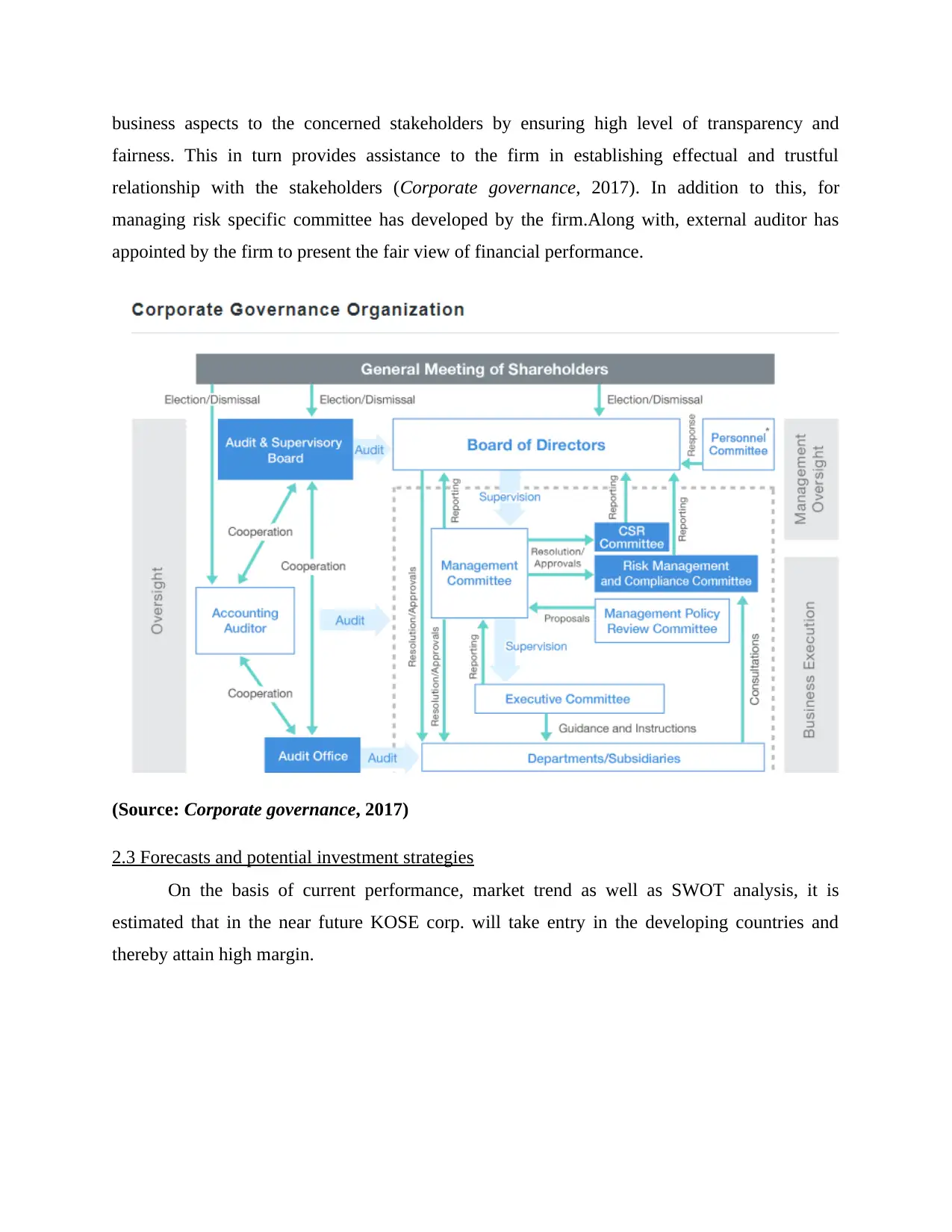

Corporate governance report of KOSE Corp shows that enhancement of the group’s

value is one of the main objectives of the company. Hence, business unit communicates all the

Shiseido is known as the producer of quality skin and hair care, cosmetic and fragrance

related products. Such Japanese company has secured first position in Japan and fifth in the

world. Both the companies which are undertaken for the study listed on and traded through

Tokyo stock exchange.

1.3 Approach and methodology

With the motive to evaluate financial results of KOSE over the rival firm such as

Shiseido Co Ltddata has been gathered through the annual reports of such companies. Hence, by

accessing incomestatement and balance sheet of KOSE as well as Shiseido, pertaining to 5 years

from 2012 to 2016, data has been gathered. Along with this, to present the better view ofissue

latest economic developments and company’s latest announcements as well as forecasts have

also been evaluated. Hence, main source of information considered for the present study are as

follows:

Annual reports of KOSE and Shiseido

Journals and articles related personal care sector

2. REVIEW ANALYSIS OF MANAGEMENT &DIRECTOR’S REPORT

2.1 Disclosure and announcement by the companies

On 4th March 2014, KOSE announced that it has signed agreement in relation to

acquiring 14856 shares. This aspect shows that KOSE stake in Tarte accounts for 93.5%

respectively whose value is Japan yen135 significantly.

2.2 Review of auditor’s report

Auditor’s report of KOSE Corp shows that financial statements of the concerned

organization are free from errors. Besides this, auditors entailed in their report that company has

made fair distribution of benefits among the shareholders and other stakeholders.

Corporate governance report of KOSE Corp shows that enhancement of the group’s

value is one of the main objectives of the company. Hence, business unit communicates all the

business aspects to the concerned stakeholders by ensuring high level of transparency and

fairness. This in turn provides assistance to the firm in establishing effectual and trustful

relationship with the stakeholders (Corporate governance, 2017). In addition to this, for

managing risk specific committee has developed by the firm.Along with, external auditor has

appointed by the firm to present the fair view of financial performance.

(Source: Corporate governance, 2017)

2.3 Forecasts and potential investment strategies

On the basis of current performance, market trend as well as SWOT analysis, it is

estimated that in the near future KOSE corp. will take entry in the developing countries and

thereby attain high margin.

fairness. This in turn provides assistance to the firm in establishing effectual and trustful

relationship with the stakeholders (Corporate governance, 2017). In addition to this, for

managing risk specific committee has developed by the firm.Along with, external auditor has

appointed by the firm to present the fair view of financial performance.

(Source: Corporate governance, 2017)

2.3 Forecasts and potential investment strategies

On the basis of current performance, market trend as well as SWOT analysis, it is

estimated that in the near future KOSE corp. will take entry in the developing countries and

thereby attain high margin.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3. FINANCIAL STATEMENT ANALYSIS

3.1 Background

For the purpose of financial evaluation, ratio analysis technique has been undertaken for

getting deeperinsight or quick indication about thecompany’s performance. In furnishes

informationregarding the several key areas such as profitability, efficiency, investment, liquidity

and solvency. Thus, to summarize the financial position ofKOSE over the years and in

comparison to the competitor such as Shiseido ratio analysis tool has been employed.

3.2 Business analysis

SWOT analysis of KOSE Corporation

Strengths

Effectual control on cost (labor)

Highly skilled and efficient workforce

(KOSE Corporation SWOT Analysis

Overview, 2017)

Sound quality management

Weaknesses

Less emphasis on R&D

Lower level of focus on promotional

campaign or aspects

Opportunities

Enhance customer base and profit

margin by taking entry in emerging

economies

Company has opportunity to grab high

market share through innovation and

offering new products as well as

services to the customers.

Threats

Changing rules and regulations

Presence of strong competitors

SWOT analysis of Shiseido Co Ltd

Strengths Weaknesses

3.1 Background

For the purpose of financial evaluation, ratio analysis technique has been undertaken for

getting deeperinsight or quick indication about thecompany’s performance. In furnishes

informationregarding the several key areas such as profitability, efficiency, investment, liquidity

and solvency. Thus, to summarize the financial position ofKOSE over the years and in

comparison to the competitor such as Shiseido ratio analysis tool has been employed.

3.2 Business analysis

SWOT analysis of KOSE Corporation

Strengths

Effectual control on cost (labor)

Highly skilled and efficient workforce

(KOSE Corporation SWOT Analysis

Overview, 2017)

Sound quality management

Weaknesses

Less emphasis on R&D

Lower level of focus on promotional

campaign or aspects

Opportunities

Enhance customer base and profit

margin by taking entry in emerging

economies

Company has opportunity to grab high

market share through innovation and

offering new products as well as

services to the customers.

Threats

Changing rules and regulations

Presence of strong competitors

SWOT analysis of Shiseido Co Ltd

Strengths Weaknesses

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Effective management

Sound customer base

Quality management

Market leader (Shiseido Company,

Limited SWOT Analysis, 2017)

Lack of training & development

session

Lack of R&D program

Opportunities

Expansion of business operations in

global market through mergers and

acquisition

Threats

Government rules and regulations

3.3 Analysis of key performance indicators

3.3.1 Profitability ratios

Return on equity (ROE) Mar

2015

Dec

2015

Dec

2016

Sep2017

Interim

Unaudited

KOSE Corp

Net income / shareholders

equity 10.25% 13.84% 13.16% 10.20%

Shiseido Co

Ltd

9.58% 6.32% 8.19% 9.47%

Sound customer base

Quality management

Market leader (Shiseido Company,

Limited SWOT Analysis, 2017)

Lack of training & development

session

Lack of R&D program

Opportunities

Expansion of business operations in

global market through mergers and

acquisition

Threats

Government rules and regulations

3.3 Analysis of key performance indicators

3.3.1 Profitability ratios

Return on equity (ROE) Mar

2015

Dec

2015

Dec

2016

Sep2017

Interim

Unaudited

KOSE Corp

Net income / shareholders

equity 10.25% 13.84% 13.16% 10.20%

Shiseido Co

Ltd

9.58% 6.32% 8.19% 9.47%

Interim

Unaudited

Mar-15 Dec-15 Dec-16 Sep-17

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

14.00%

KOSE Corp

Shiseido Co Ltd

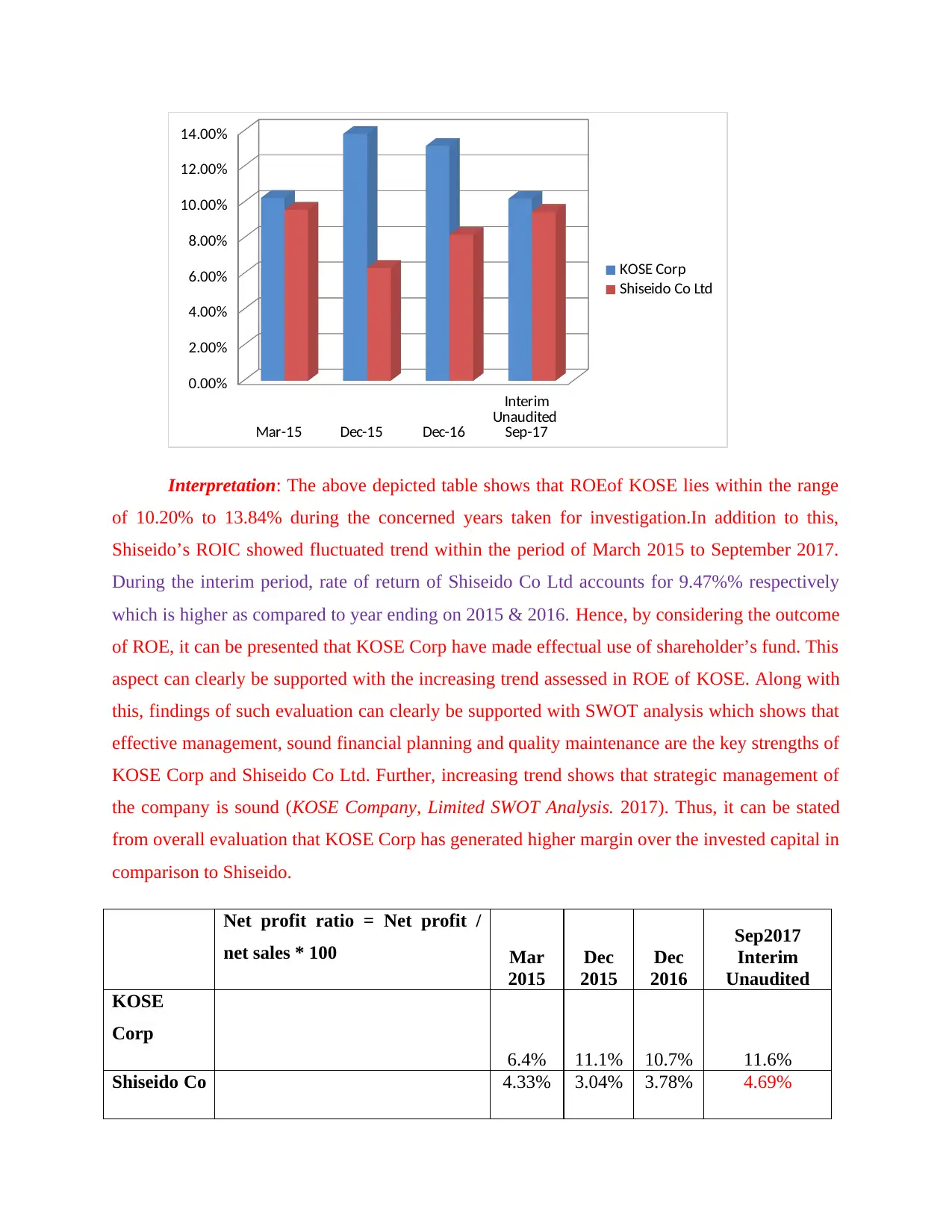

Interpretation: The above depicted table shows that ROEof KOSE lies within the range

of 10.20% to 13.84% during the concerned years taken for investigation.In addition to this,

Shiseido’s ROIC showed fluctuated trend within the period of March 2015 to September 2017.

During the interim period, rate of return of Shiseido Co Ltd accounts for 9.47%% respectively

which is higher as compared to year ending on 2015 & 2016. Hence, by considering the outcome

of ROE, it can be presented that KOSE Corp have made effectual use of shareholder’s fund. This

aspect can clearly be supported with the increasing trend assessed in ROE of KOSE. Along with

this, findings of such evaluation can clearly be supported with SWOT analysis which shows that

effective management, sound financial planning and quality maintenance are the key strengths of

KOSE Corp and Shiseido Co Ltd. Further, increasing trend shows that strategic management of

the company is sound (KOSE Company, Limited SWOT Analysis. 2017). Thus, it can be stated

from overall evaluation that KOSE Corp has generated higher margin over the invested capital in

comparison to Shiseido.

Net profit ratio = Net profit /

net sales * 100 Mar

2015

Dec

2015

Dec

2016

Sep2017

Interim

Unaudited

KOSE

Corp

6.4% 11.1% 10.7% 11.6%

Shiseido Co 4.33% 3.04% 3.78% 4.69%

Unaudited

Mar-15 Dec-15 Dec-16 Sep-17

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

14.00%

KOSE Corp

Shiseido Co Ltd

Interpretation: The above depicted table shows that ROEof KOSE lies within the range

of 10.20% to 13.84% during the concerned years taken for investigation.In addition to this,

Shiseido’s ROIC showed fluctuated trend within the period of March 2015 to September 2017.

During the interim period, rate of return of Shiseido Co Ltd accounts for 9.47%% respectively

which is higher as compared to year ending on 2015 & 2016. Hence, by considering the outcome

of ROE, it can be presented that KOSE Corp have made effectual use of shareholder’s fund. This

aspect can clearly be supported with the increasing trend assessed in ROE of KOSE. Along with

this, findings of such evaluation can clearly be supported with SWOT analysis which shows that

effective management, sound financial planning and quality maintenance are the key strengths of

KOSE Corp and Shiseido Co Ltd. Further, increasing trend shows that strategic management of

the company is sound (KOSE Company, Limited SWOT Analysis. 2017). Thus, it can be stated

from overall evaluation that KOSE Corp has generated higher margin over the invested capital in

comparison to Shiseido.

Net profit ratio = Net profit /

net sales * 100 Mar

2015

Dec

2015

Dec

2016

Sep2017

Interim

Unaudited

KOSE

Corp

6.4% 11.1% 10.7% 11.6%

Shiseido Co 4.33% 3.04% 3.78% 4.69%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Ltd

Interim

Unaudited

Mar-15 Dec-15 Dec-16 Sep-17

0.00%

100.00%

200.00%

300.00%

400.00%

500.00%

600.00%

700.00%

800.00%

900.00%

Shiseido Co Ltd

KOSE Corp

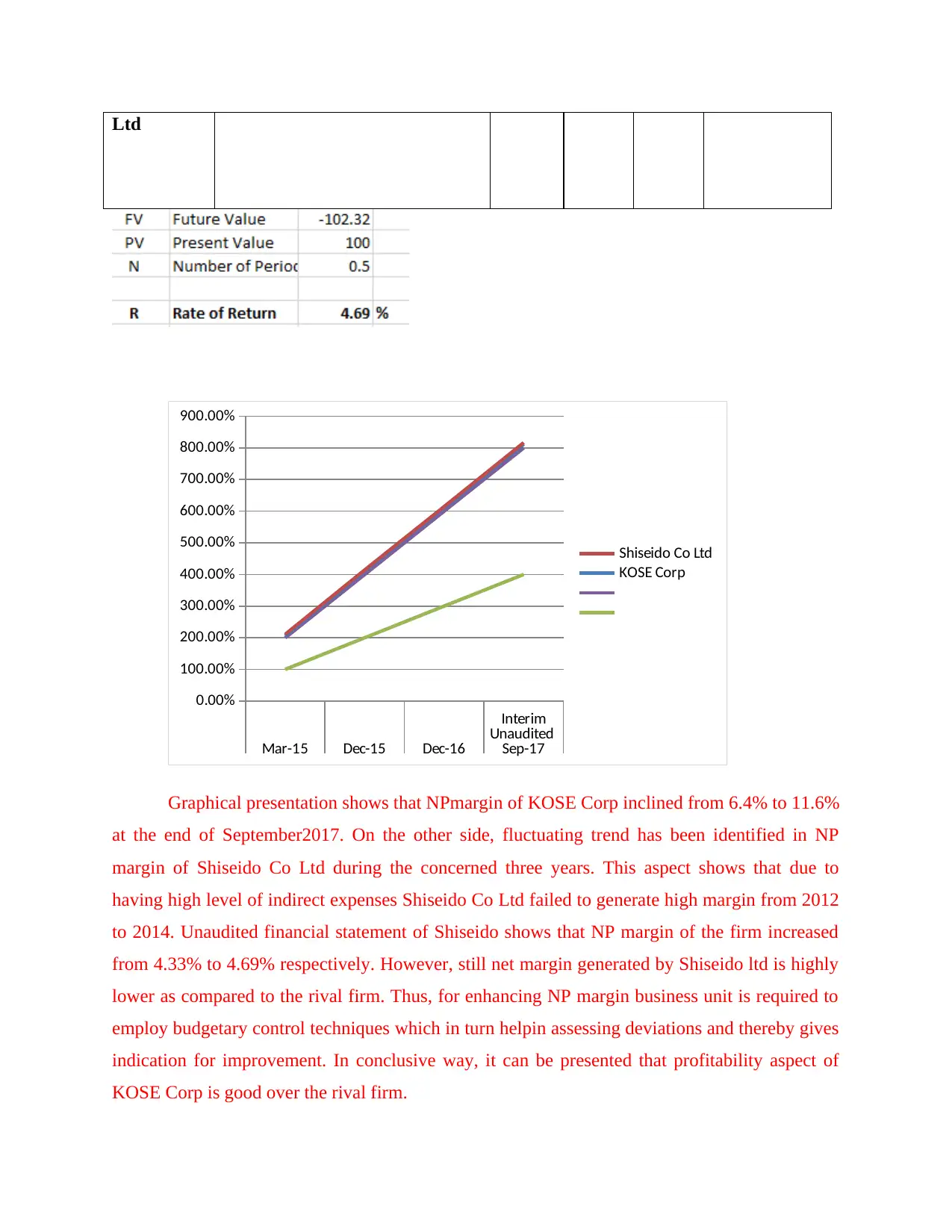

Graphical presentation shows that NPmargin of KOSE Corp inclined from 6.4% to 11.6%

at the end of September2017. On the other side, fluctuating trend has been identified in NP

margin of Shiseido Co Ltd during the concerned three years. This aspect shows that due to

having high level of indirect expenses Shiseido Co Ltd failed to generate high margin from 2012

to 2014. Unaudited financial statement of Shiseido shows that NP margin of the firm increased

from 4.33% to 4.69% respectively. However, still net margin generated by Shiseido ltd is highly

lower as compared to the rival firm. Thus, for enhancing NP margin business unit is required to

employ budgetary control techniques which in turn helpin assessing deviations and thereby gives

indication for improvement. In conclusive way, it can be presented that profitability aspect of

KOSE Corp is good over the rival firm.

Interim

Unaudited

Mar-15 Dec-15 Dec-16 Sep-17

0.00%

100.00%

200.00%

300.00%

400.00%

500.00%

600.00%

700.00%

800.00%

900.00%

Shiseido Co Ltd

KOSE Corp

Graphical presentation shows that NPmargin of KOSE Corp inclined from 6.4% to 11.6%

at the end of September2017. On the other side, fluctuating trend has been identified in NP

margin of Shiseido Co Ltd during the concerned three years. This aspect shows that due to

having high level of indirect expenses Shiseido Co Ltd failed to generate high margin from 2012

to 2014. Unaudited financial statement of Shiseido shows that NP margin of the firm increased

from 4.33% to 4.69% respectively. However, still net margin generated by Shiseido ltd is highly

lower as compared to the rival firm. Thus, for enhancing NP margin business unit is required to

employ budgetary control techniques which in turn helpin assessing deviations and thereby gives

indication for improvement. In conclusive way, it can be presented that profitability aspect of

KOSE Corp is good over the rival firm.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

3.3.2 Efficiency ratios

31/3/2015 31/12/2015 31/12/2016 30/8/2017

0

1

2

3

4

5

6

Fixed assets turnover ratio

in times

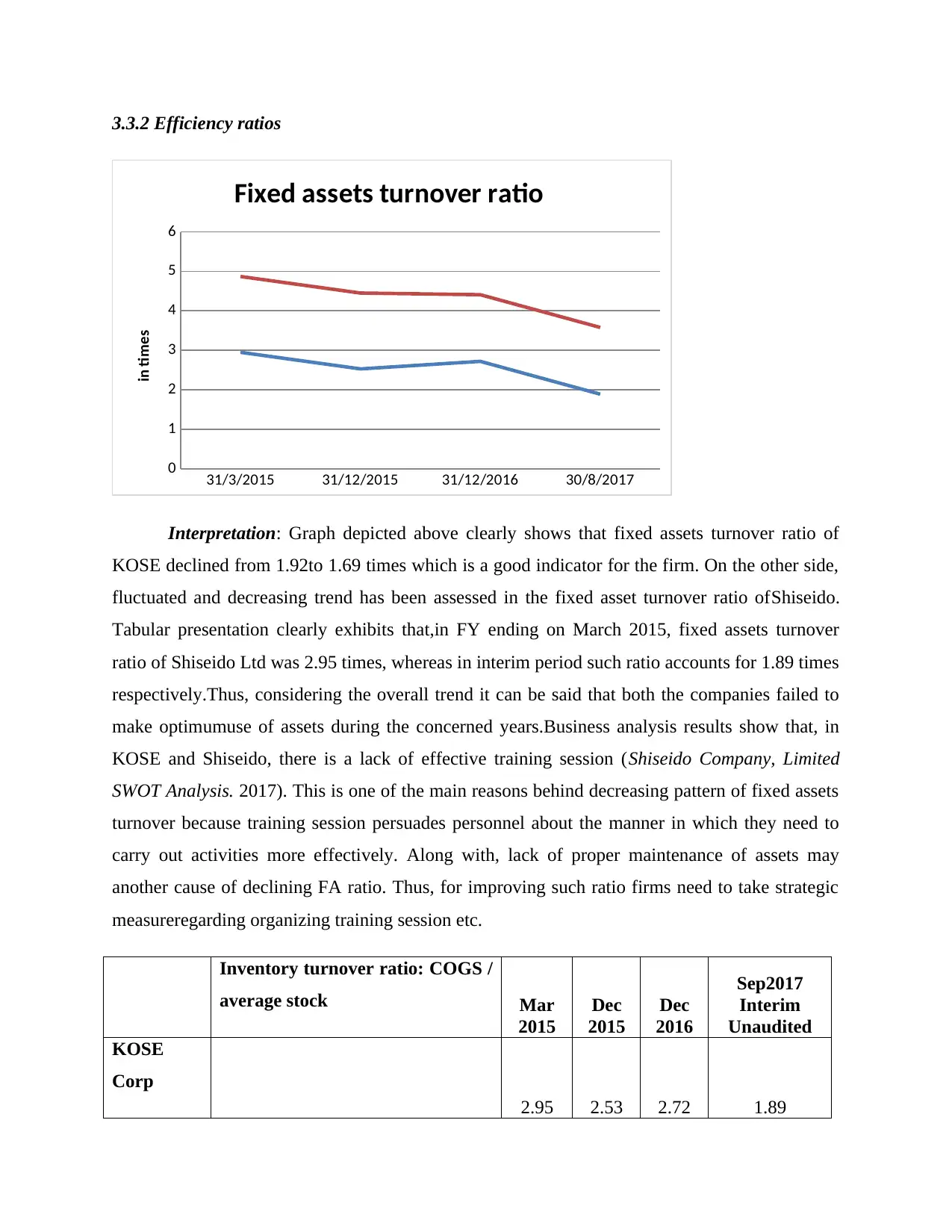

Interpretation: Graph depicted above clearly shows that fixed assets turnover ratio of

KOSE declined from 1.92to 1.69 times which is a good indicator for the firm. On the other side,

fluctuated and decreasing trend has been assessed in the fixed asset turnover ratio ofShiseido.

Tabular presentation clearly exhibits that,in FY ending on March 2015, fixed assets turnover

ratio of Shiseido Ltd was 2.95 times, whereas in interim period such ratio accounts for 1.89 times

respectively.Thus, considering the overall trend it can be said that both the companies failed to

make optimumuse of assets during the concerned years.Business analysis results show that, in

KOSE and Shiseido, there is a lack of effective training session (Shiseido Company, Limited

SWOT Analysis. 2017). This is one of the main reasons behind decreasing pattern of fixed assets

turnover because training session persuades personnel about the manner in which they need to

carry out activities more effectively. Along with, lack of proper maintenance of assets may

another cause of declining FA ratio. Thus, for improving such ratio firms need to take strategic

measureregarding organizing training session etc.

Inventory turnover ratio: COGS /

average stock Mar

2015

Dec

2015

Dec

2016

Sep2017

Interim

Unaudited

KOSE

Corp

2.95 2.53 2.72 1.89

31/3/2015 31/12/2015 31/12/2016 30/8/2017

0

1

2

3

4

5

6

Fixed assets turnover ratio

in times

Interpretation: Graph depicted above clearly shows that fixed assets turnover ratio of

KOSE declined from 1.92to 1.69 times which is a good indicator for the firm. On the other side,

fluctuated and decreasing trend has been assessed in the fixed asset turnover ratio ofShiseido.

Tabular presentation clearly exhibits that,in FY ending on March 2015, fixed assets turnover

ratio of Shiseido Ltd was 2.95 times, whereas in interim period such ratio accounts for 1.89 times

respectively.Thus, considering the overall trend it can be said that both the companies failed to

make optimumuse of assets during the concerned years.Business analysis results show that, in

KOSE and Shiseido, there is a lack of effective training session (Shiseido Company, Limited

SWOT Analysis. 2017). This is one of the main reasons behind decreasing pattern of fixed assets

turnover because training session persuades personnel about the manner in which they need to

carry out activities more effectively. Along with, lack of proper maintenance of assets may

another cause of declining FA ratio. Thus, for improving such ratio firms need to take strategic

measureregarding organizing training session etc.

Inventory turnover ratio: COGS /

average stock Mar

2015

Dec

2015

Dec

2016

Sep2017

Interim

Unaudited

KOSE

Corp

2.95 2.53 2.72 1.89

Shiseido

Co Ltd

1.84 1.85 1.79 1.23

31/3/2015 31/12/2015 31/12/2016 30/8/2017

2.95

2.53 2.72

1.891.84 1.85 1.79

1.23

Inventory turnover ratio

KOSE Corp Shiseido Co Ltd

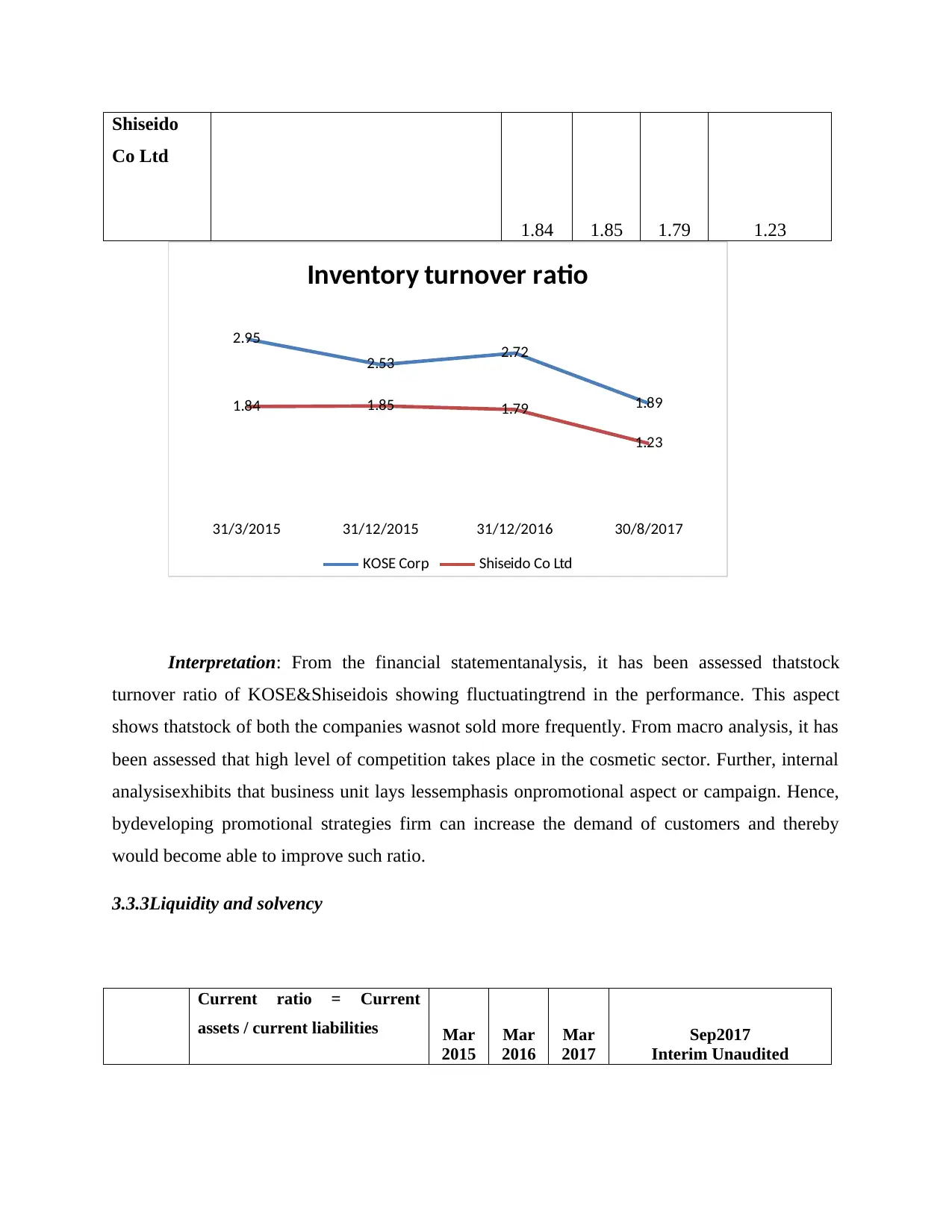

Interpretation: From the financial statementanalysis, it has been assessed thatstock

turnover ratio of KOSE&Shiseidois showing fluctuatingtrend in the performance. This aspect

shows thatstock of both the companies wasnot sold more frequently. From macro analysis, it has

been assessed that high level of competition takes place in the cosmetic sector. Further, internal

analysisexhibits that business unit lays lessemphasis onpromotional aspect or campaign. Hence,

bydeveloping promotional strategies firm can increase the demand of customers and thereby

would become able to improve such ratio.

3.3.3Liquidity and solvency

Current ratio = Current

assets / current liabilities Mar

2015

Mar

2016

Mar

2017

Sep2017

Interim Unaudited

Co Ltd

1.84 1.85 1.79 1.23

31/3/2015 31/12/2015 31/12/2016 30/8/2017

2.95

2.53 2.72

1.891.84 1.85 1.79

1.23

Inventory turnover ratio

KOSE Corp Shiseido Co Ltd

Interpretation: From the financial statementanalysis, it has been assessed thatstock

turnover ratio of KOSE&Shiseidois showing fluctuatingtrend in the performance. This aspect

shows thatstock of both the companies wasnot sold more frequently. From macro analysis, it has

been assessed that high level of competition takes place in the cosmetic sector. Further, internal

analysisexhibits that business unit lays lessemphasis onpromotional aspect or campaign. Hence,

bydeveloping promotional strategies firm can increase the demand of customers and thereby

would become able to improve such ratio.

3.3.3Liquidity and solvency

Current ratio = Current

assets / current liabilities Mar

2015

Mar

2016

Mar

2017

Sep2017

Interim Unaudited

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 58

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.