Financial Analysis Report: Stock Market Analysis and Recommendations

VerifiedAdded on 2022/09/08

|21

|1515

|13

Report

AI Summary

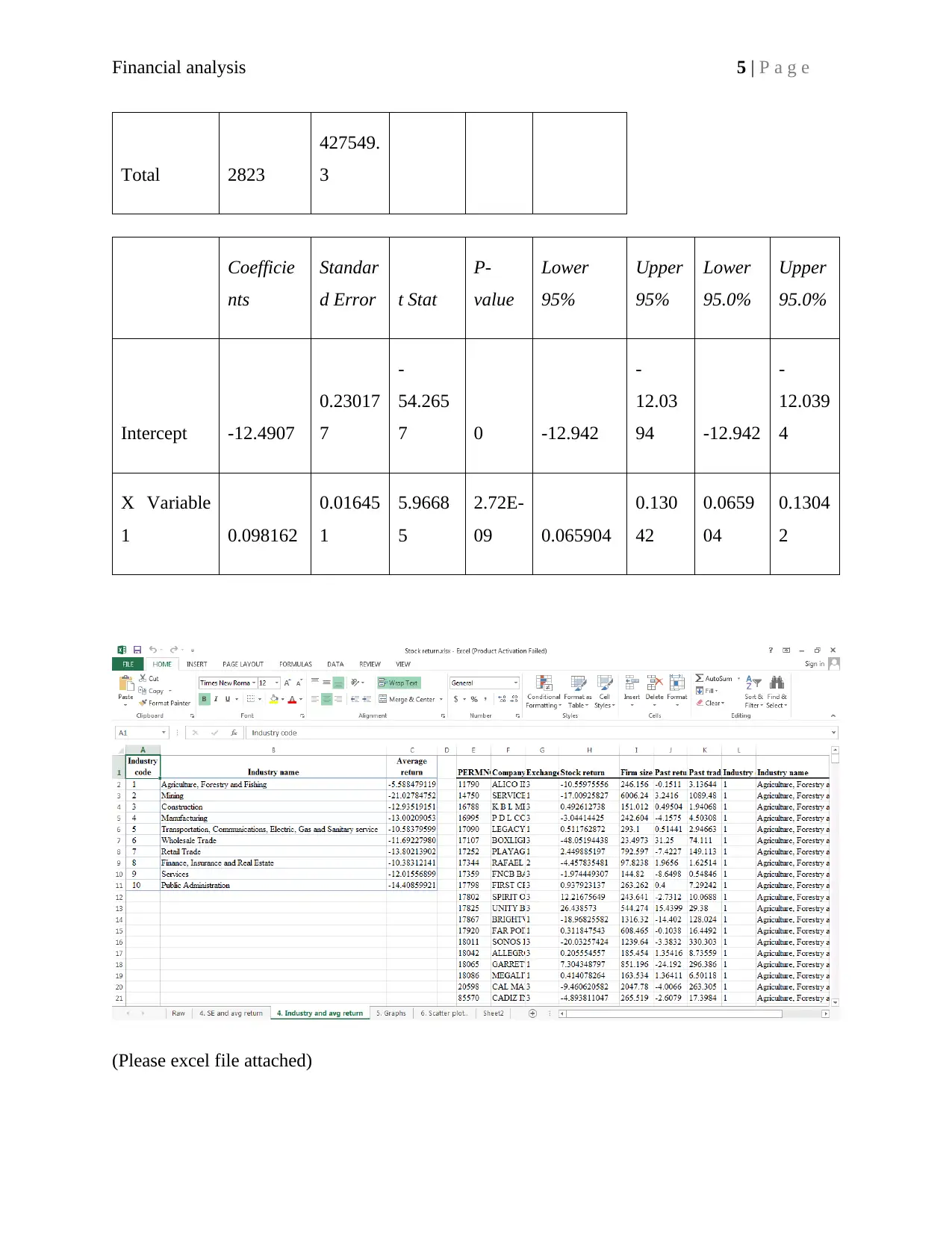

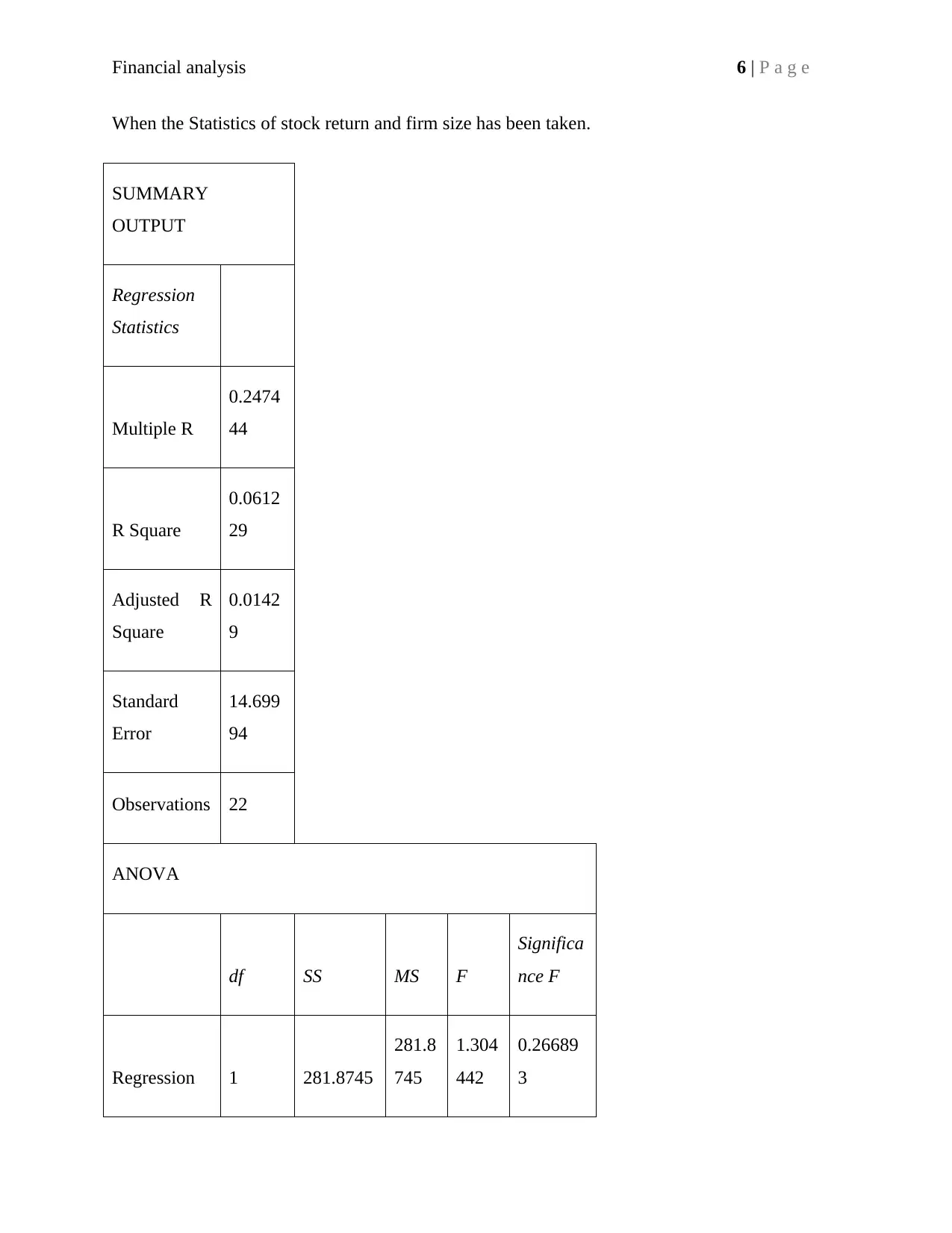

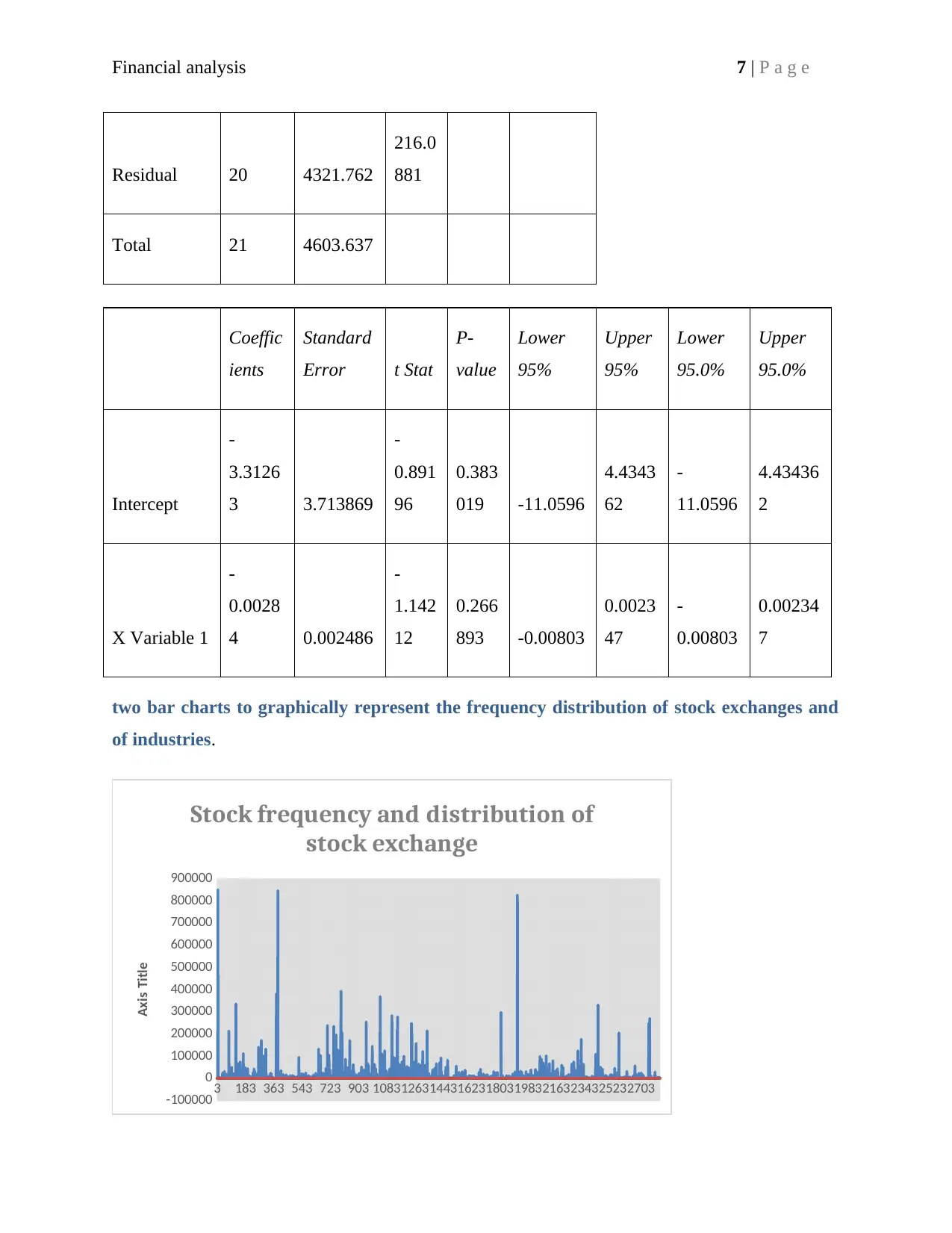

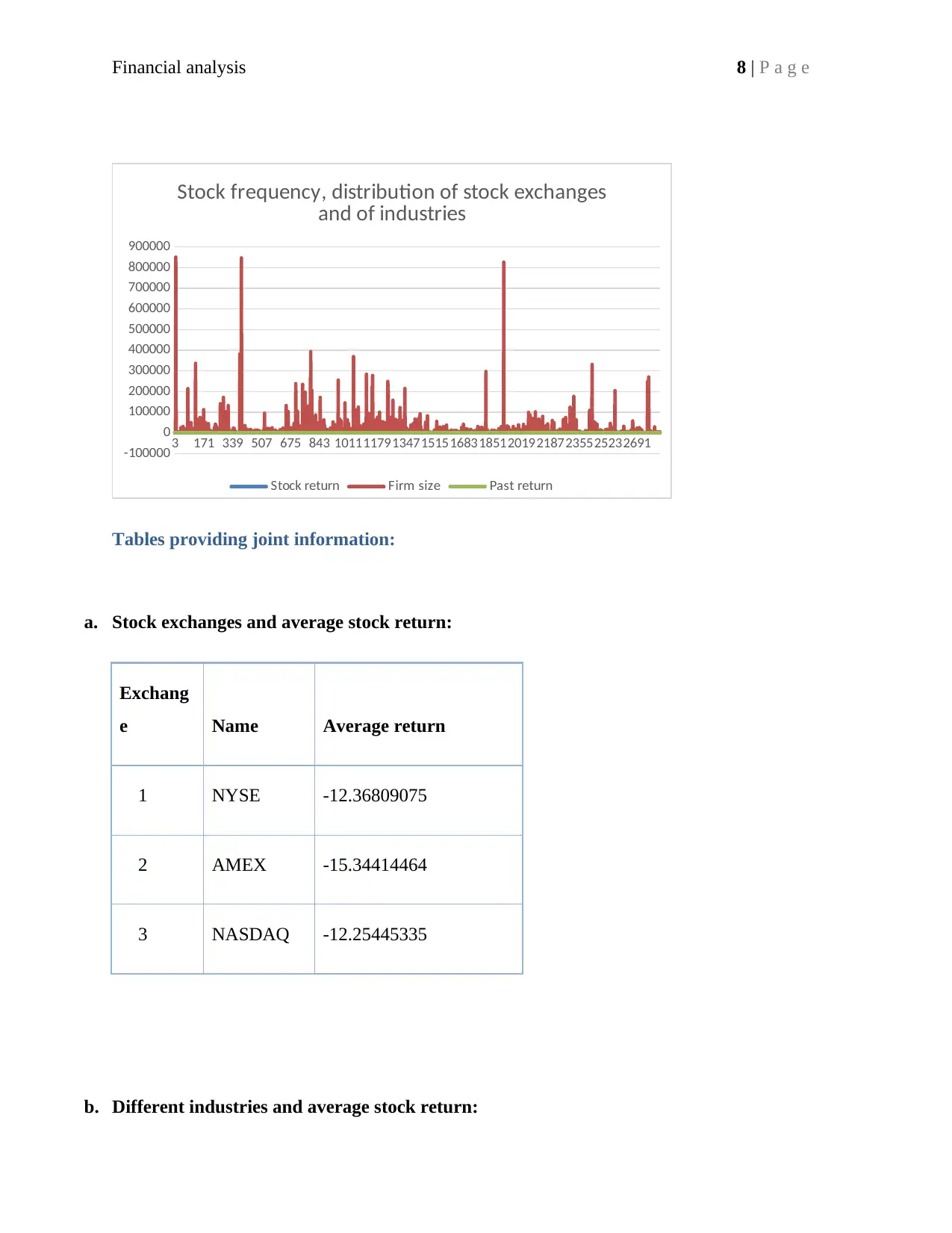

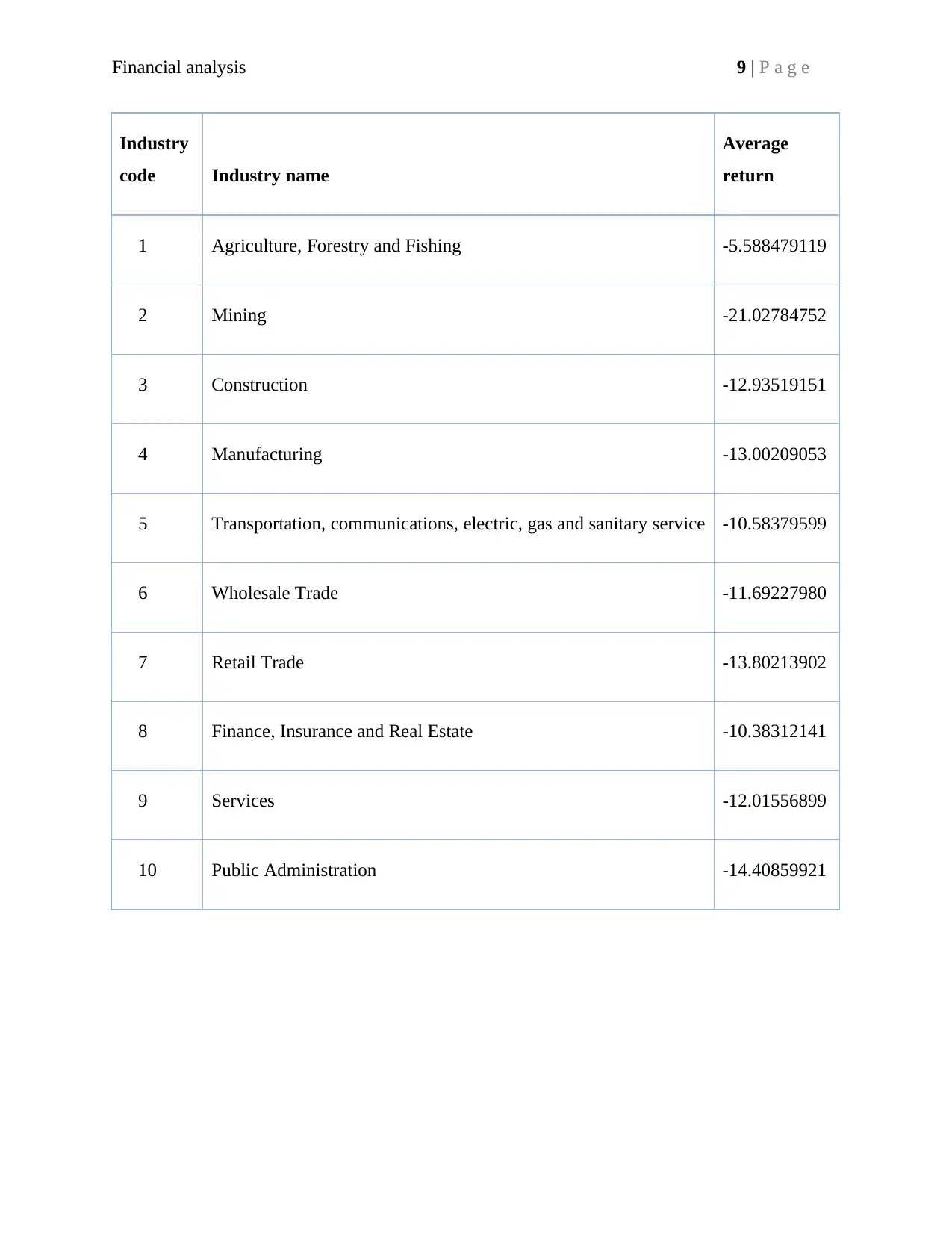

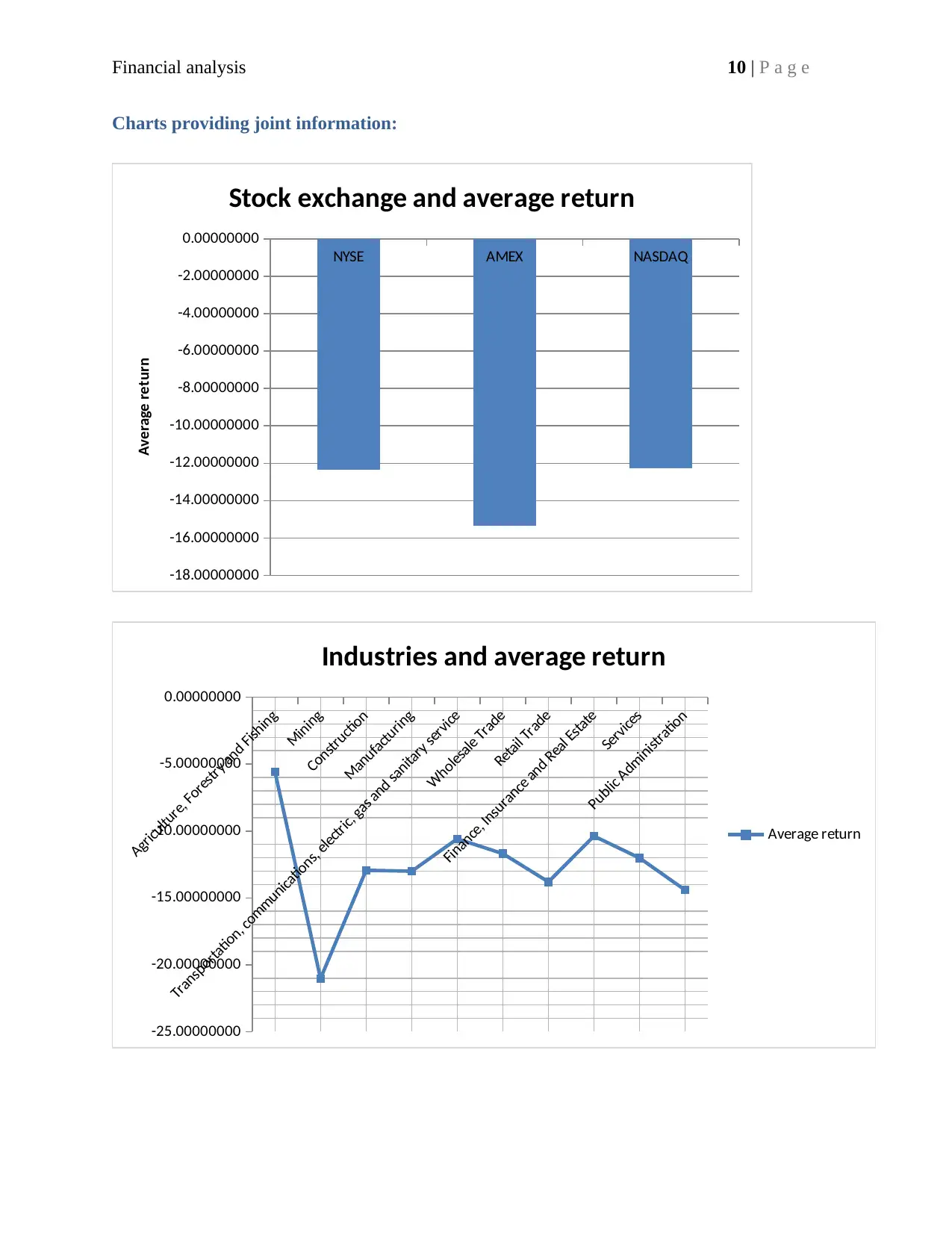

This report presents a financial analysis of U.S. stock market data, focusing on the identification of variables and their types, descriptive statistics of stock returns and firm size, and graphical representations of frequency distributions. It examines the correlation between stock returns and firm size, past returns, and trading value. The analysis includes tables providing joint information on stock exchanges and average stock returns across different industries. Based on these findings, the report offers recommendations to investors in the U.S. stock market, emphasizing the volatility observed and the importance of considering risk and return profiles. The report utilizes statistical tools such as regression analysis and correlation coefficients to provide a comprehensive overview of the data and its implications for investment decisions. The findings suggest that investors should carefully assess the risk and return associated with each investment option before making any investment decisions.

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.