Financial Analysis of TESCO: Performance and Impact

VerifiedAdded on 2023/06/10

|7

|2297

|418

Report

AI Summary

This report provides a comprehensive financial analysis of TESCO, focusing on its performance in the retail industry and the impact of the COVID-19 pandemic. The report examines the company's financial position through profitability, liquidity, and gearing ratios, calculated using data from the company's annual reports. The analysis includes calculations of gross profit margin, net profit margin, current ratio, quick ratio, debt-equity ratio, and interest earned ratio. The methodology involves a review of secondary data, specifically TESCO's annual reports. The findings reveal trends in TESCO's financial performance over the period, with interpretations of the ratios highlighting strengths and weaknesses, and the impact of COVID-19 on these metrics. The conclusion summarizes the company's market position and sustainability, offering recommendations for continued financial health. References and appendices are included to support the analysis.

Student Name:

Student ID Number:

Programme Title

Module Name Foundation Year Project

Programme Start Date

(e.g. September 2021)

Tutor’s Name

Campus

Table of Contents:

Contents

Introduction (150 – 200)........................................................................................................................2

Literature Review (300 words)..............................................................................................................2

Research Methodology (300 words)......................................................................................................3

Data Analysis and Presentation (400 – 500) words...............................................................................4

Conclusion and Recommendations (200)..............................................................................................5

References.............................................................................................................................................6

Appendixes............................................................................................................................................7

Student ID Number:

Programme Title

Module Name Foundation Year Project

Programme Start Date

(e.g. September 2021)

Tutor’s Name

Campus

Table of Contents:

Contents

Introduction (150 – 200)........................................................................................................................2

Literature Review (300 words)..............................................................................................................2

Research Methodology (300 words)......................................................................................................3

Data Analysis and Presentation (400 – 500) words...............................................................................4

Conclusion and Recommendations (200)..............................................................................................5

References.............................................................................................................................................6

Appendixes............................................................................................................................................7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Introduction (150 – 200).

The following report consists of the analysis of the profitability and the financial

analysis. It is basically deemed to understand about the financial and monetary position of

the company (Allouhi and Amine, 2019). In this research the company chosen is TESCO.

It is listed on the London Stock Exchange and deals in the retail industry. It has many

brands covered under.

Aims: To identify the monetary and sustainable position of TESCO ad the impact of

Covid – 19 on its performance.

Objectives:

To analyse the annual report of the company.

To evaluate the financial performance of the business organisation.

To analyse the impact of Covid – 19 on the performance of the company.

On the whole the report covers the sections such as literature review in which the various

types of data and the research problem will be identified. Further, the directors and the

strategic report of the company published is analyse and some conclusions on the company’s

performance is made accordingly. Further, the research question is framed on the basis of the

aims and objectives. Then the research methodology is preparing on the basis of the type of

data chosen for the research. Moreover, the data collected is analysed and is evaluated on the

basis of the chart and ratios computed for analysing the fiscal performance of the business

entity.

Literature Review (300 words).

Profitability Ratio: These are computed for calculating the profit margin achieved on the

overall sales turnover of the company in a particular year. Some of the ratios which

come under it are: Gross Profit Margin Ratio, Net profit Margin, Operating Profit Margin.

Liquidity Ratio: This ratio helps in determining the liquidity position of the company. It

means that it tells about how much cash the company holds in hand or the assets which

can be converted shortly in cash when needed to the company (Huth, 2020).

Tesco reported the rebuilding of its profit on 4 October 2017, mirroring the

Company's better presentation and the Board's trust in its future possibilities, and

delivered an in-between time profit of 1.0p per normal offer on 24 November 2017. This

follows instalment of no profit in the 52 weeks finished 25 February 2017 and 27

February 2016 and instalment of a profit of 1.16p per normal offer in the 53 weeks

finished 28 February 2015. The Board expects an around 33% to 66% split between the

break and last profits, and means to deliver a last profit of 2.0p per common offer for

the 52 weeks finishing February 24, 2018, with profits projected to increment from

2017.

Explain how and how it underpins your research i.e:

a) Does the COVID-19 have an impact on company’s financial and operating

performance, and you want to find out by conducting this research?

The following report consists of the analysis of the profitability and the financial

analysis. It is basically deemed to understand about the financial and monetary position of

the company (Allouhi and Amine, 2019). In this research the company chosen is TESCO.

It is listed on the London Stock Exchange and deals in the retail industry. It has many

brands covered under.

Aims: To identify the monetary and sustainable position of TESCO ad the impact of

Covid – 19 on its performance.

Objectives:

To analyse the annual report of the company.

To evaluate the financial performance of the business organisation.

To analyse the impact of Covid – 19 on the performance of the company.

On the whole the report covers the sections such as literature review in which the various

types of data and the research problem will be identified. Further, the directors and the

strategic report of the company published is analyse and some conclusions on the company’s

performance is made accordingly. Further, the research question is framed on the basis of the

aims and objectives. Then the research methodology is preparing on the basis of the type of

data chosen for the research. Moreover, the data collected is analysed and is evaluated on the

basis of the chart and ratios computed for analysing the fiscal performance of the business

entity.

Literature Review (300 words).

Profitability Ratio: These are computed for calculating the profit margin achieved on the

overall sales turnover of the company in a particular year. Some of the ratios which

come under it are: Gross Profit Margin Ratio, Net profit Margin, Operating Profit Margin.

Liquidity Ratio: This ratio helps in determining the liquidity position of the company. It

means that it tells about how much cash the company holds in hand or the assets which

can be converted shortly in cash when needed to the company (Huth, 2020).

Tesco reported the rebuilding of its profit on 4 October 2017, mirroring the

Company's better presentation and the Board's trust in its future possibilities, and

delivered an in-between time profit of 1.0p per normal offer on 24 November 2017. This

follows instalment of no profit in the 52 weeks finished 25 February 2017 and 27

February 2016 and instalment of a profit of 1.16p per normal offer in the 53 weeks

finished 28 February 2015. The Board expects an around 33% to 66% split between the

break and last profits, and means to deliver a last profit of 2.0p per common offer for

the 52 weeks finishing February 24, 2018, with profits projected to increment from

2017.

Explain how and how it underpins your research i.e:

a) Does the COVID-19 have an impact on company’s financial and operating

performance, and you want to find out by conducting this research?

Yes, the company’s financial and operating performance is impacted by the

situation of Covid – 19. The operating profit of the company has declined

along with the diminishment in the sales turnover.

b) Is it the government policies and its impact on business performance that

made you conduct this research?

No, the research is conducted for carrying out the monetary performance of

the business for finding out its own standout position in the market.

Research Methodology (300 words).

Primary research: The sole objective of primary based researches is to assemble data

and information which would help to answer questions which a user has never come

across before. It is considered as a time-consuming method and incurs higher level of

expenses when compared with secondary researches. In case of primary researches

team is in charge of every action which includes from selecting best method till reaching

desired audience as well. Primary data is collected and served fresh and has no chance

of repetition of data (Liu and Shang, 2018).

Secondary research: It is sort of research which is already available and which is

developed by professionals without committing any mistake the reason being the data

collected is used by many people and investors for reaching a decision as whether to

invest in a certain company for that time period or not. It is suggested on a larger scale

because it is more cost effective and helps to recommend from past studies and material

collected so far by them. It is quicker and counted as better medium for large scale

companies when compared with other research related methods and tools (Ong and

Sato, 2018).

Financial performance of TESCO company assessed with the help of Annual reports

published by the company:

It is clear and evident that performance rendered by a company can only be

evaluated as well as examined with the help of data collected. It is further necessary for

a investigator to go through records being provided by the business related entities in

market for predicting the work being served by them and the results being recorded

keeping past performances in mind. It further serves as a guide to perform comparison

between results. Secondary data is chosen and considered more relevant the reason

being that it is published by the company itself for attracting more clients and customers

from marketplaces to increase expansion and growth of firm over a period of time in

competitive environment. It provides insights into competitors, trend that exist in

current situation and size of the market as well, the information collected so far can be

used for serving as a guide in decision making and better positioning of product in

market which would help to get an advantage over competitors. One more reason

behind choosing secondary method is that it is typically free and less expensive as well

for obtaining and acting as a stronger foundation for any research plan. It also helps to

save time and money also it is useful in making primary based data collection more

relevant and specific as well. It is also beneficial because it has already been used in

previous carried out researches which makes it simple and easier for carrying out further

situation of Covid – 19. The operating profit of the company has declined

along with the diminishment in the sales turnover.

b) Is it the government policies and its impact on business performance that

made you conduct this research?

No, the research is conducted for carrying out the monetary performance of

the business for finding out its own standout position in the market.

Research Methodology (300 words).

Primary research: The sole objective of primary based researches is to assemble data

and information which would help to answer questions which a user has never come

across before. It is considered as a time-consuming method and incurs higher level of

expenses when compared with secondary researches. In case of primary researches

team is in charge of every action which includes from selecting best method till reaching

desired audience as well. Primary data is collected and served fresh and has no chance

of repetition of data (Liu and Shang, 2018).

Secondary research: It is sort of research which is already available and which is

developed by professionals without committing any mistake the reason being the data

collected is used by many people and investors for reaching a decision as whether to

invest in a certain company for that time period or not. It is suggested on a larger scale

because it is more cost effective and helps to recommend from past studies and material

collected so far by them. It is quicker and counted as better medium for large scale

companies when compared with other research related methods and tools (Ong and

Sato, 2018).

Financial performance of TESCO company assessed with the help of Annual reports

published by the company:

It is clear and evident that performance rendered by a company can only be

evaluated as well as examined with the help of data collected. It is further necessary for

a investigator to go through records being provided by the business related entities in

market for predicting the work being served by them and the results being recorded

keeping past performances in mind. It further serves as a guide to perform comparison

between results. Secondary data is chosen and considered more relevant the reason

being that it is published by the company itself for attracting more clients and customers

from marketplaces to increase expansion and growth of firm over a period of time in

competitive environment. It provides insights into competitors, trend that exist in

current situation and size of the market as well, the information collected so far can be

used for serving as a guide in decision making and better positioning of product in

market which would help to get an advantage over competitors. One more reason

behind choosing secondary method is that it is typically free and less expensive as well

for obtaining and acting as a stronger foundation for any research plan. It also helps to

save time and money also it is useful in making primary based data collection more

relevant and specific as well. It is also beneficial because it has already been used in

previous carried out researches which makes it simple and easier for carrying out further

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

researches. It also provides an internal analysis as well which helps it easier to find what

is going in marketplaces and where the company is standing in the market, customer

views about your company and plan in advance what can be done, how can be done and

in what ways company would be able to improve the performance rendered by them

over a point of time.

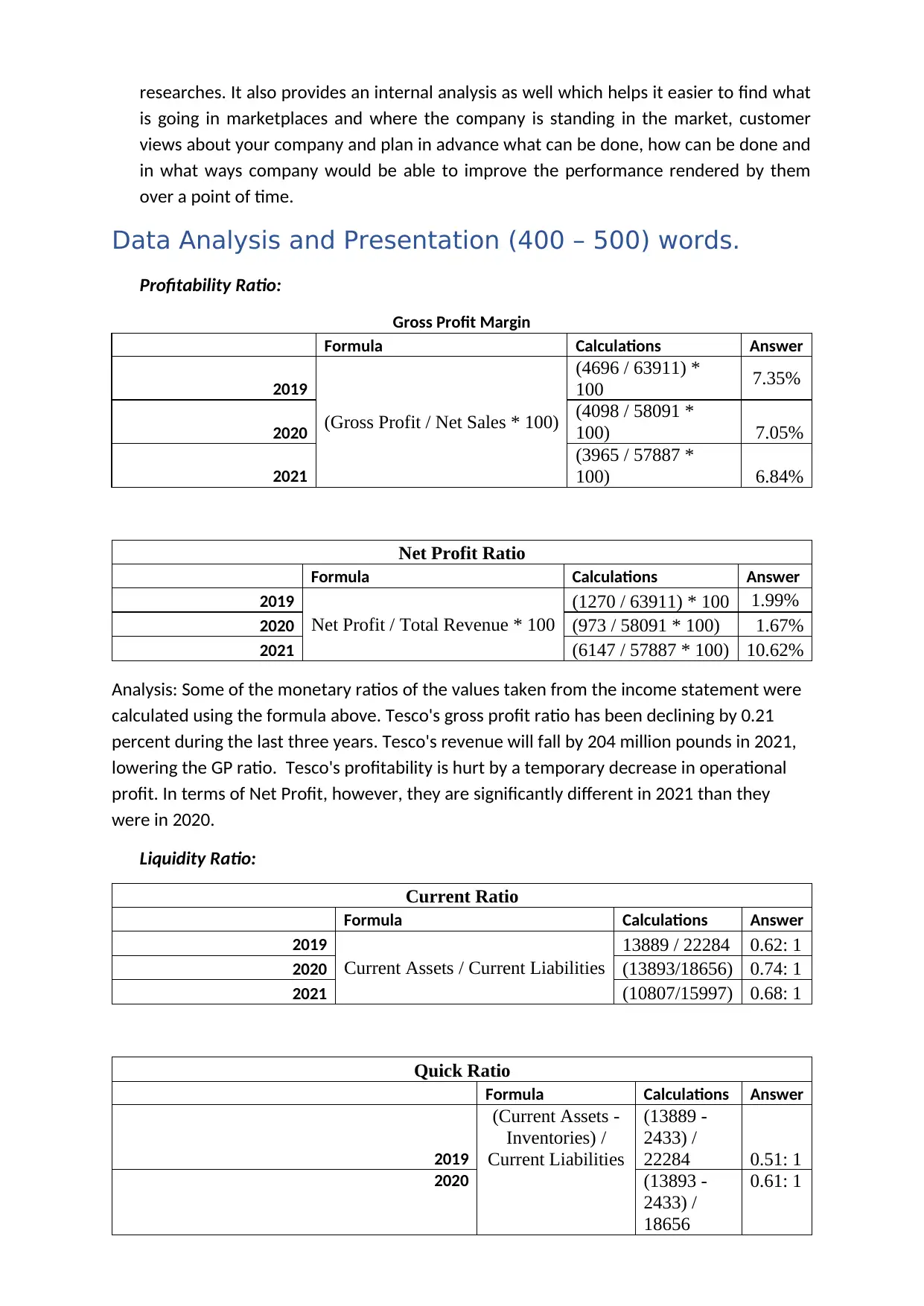

Data Analysis and Presentation (400 – 500) words.

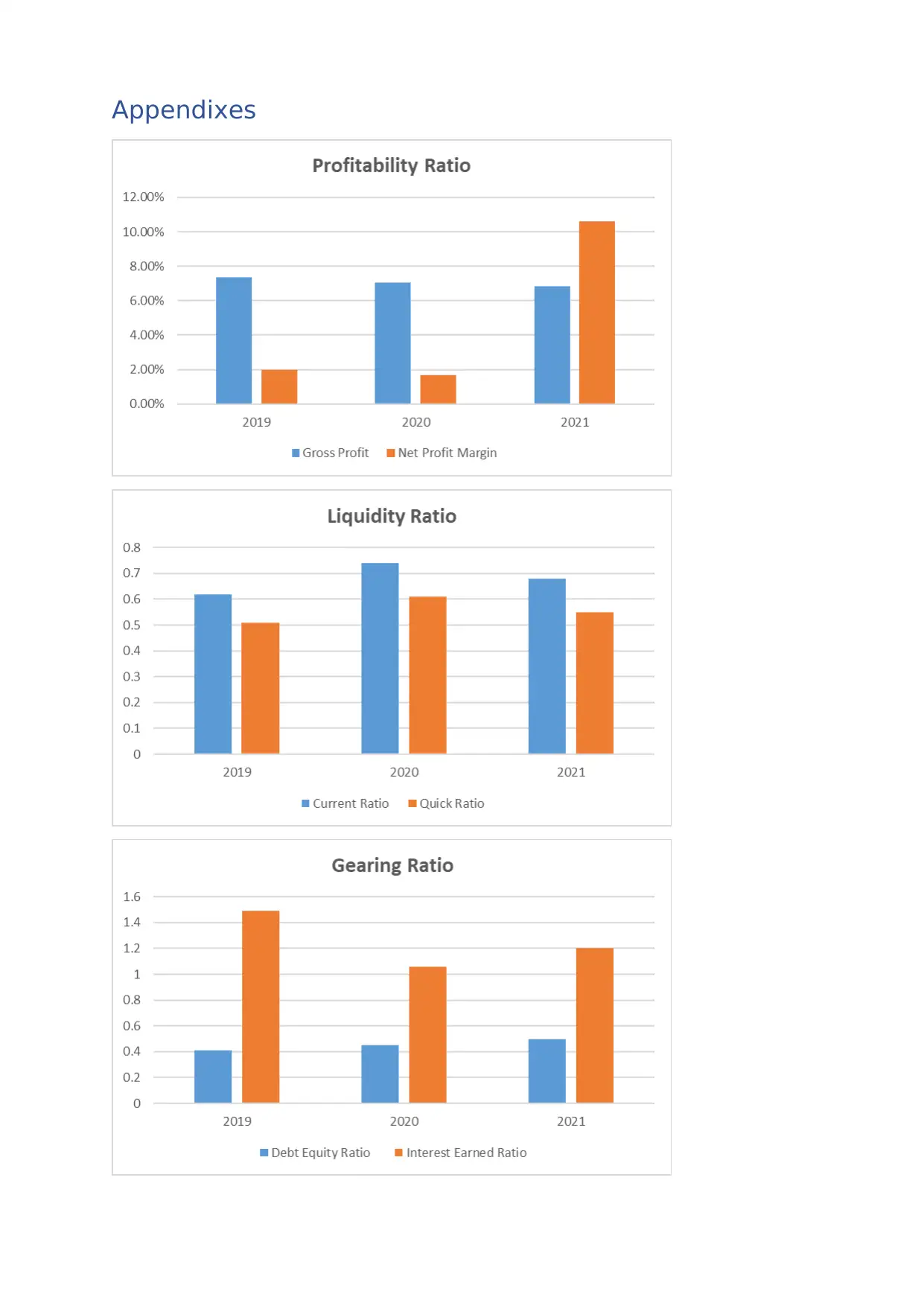

Profitability Ratio:

Gross Profit Margin

Formula Calculations Answer

2019

(Gross Profit / Net Sales * 100)

(4696 / 63911) *

100 7.35%

2020

(4098 / 58091 *

100) 7.05%

2021

(3965 / 57887 *

100) 6.84%

Net Profit Ratio

Formula Calculations Answer

2019

Net Profit / Total Revenue * 100

(1270 / 63911) * 100 1.99%

2020 (973 / 58091 * 100) 1.67%

2021 (6147 / 57887 * 100) 10.62%

Analysis: Some of the monetary ratios of the values taken from the income statement were

calculated using the formula above. Tesco's gross profit ratio has been declining by 0.21

percent during the last three years. Tesco's revenue will fall by 204 million pounds in 2021,

lowering the GP ratio. Tesco's profitability is hurt by a temporary decrease in operational

profit. In terms of Net Profit, however, they are significantly different in 2021 than they

were in 2020.

Liquidity Ratio:

Current Ratio

Formula Calculations Answer

2019

Current Assets / Current Liabilities

13889 / 22284 0.62: 1

2020 (13893/18656) 0.74: 1

2021 (10807/15997) 0.68: 1

Quick Ratio

Formula Calculations Answer

2019

(Current Assets -

Inventories) /

Current Liabilities

(13889 -

2433) /

22284 0.51: 1

2020 (13893 -

2433) /

18656

0.61: 1

is going in marketplaces and where the company is standing in the market, customer

views about your company and plan in advance what can be done, how can be done and

in what ways company would be able to improve the performance rendered by them

over a point of time.

Data Analysis and Presentation (400 – 500) words.

Profitability Ratio:

Gross Profit Margin

Formula Calculations Answer

2019

(Gross Profit / Net Sales * 100)

(4696 / 63911) *

100 7.35%

2020

(4098 / 58091 *

100) 7.05%

2021

(3965 / 57887 *

100) 6.84%

Net Profit Ratio

Formula Calculations Answer

2019

Net Profit / Total Revenue * 100

(1270 / 63911) * 100 1.99%

2020 (973 / 58091 * 100) 1.67%

2021 (6147 / 57887 * 100) 10.62%

Analysis: Some of the monetary ratios of the values taken from the income statement were

calculated using the formula above. Tesco's gross profit ratio has been declining by 0.21

percent during the last three years. Tesco's revenue will fall by 204 million pounds in 2021,

lowering the GP ratio. Tesco's profitability is hurt by a temporary decrease in operational

profit. In terms of Net Profit, however, they are significantly different in 2021 than they

were in 2020.

Liquidity Ratio:

Current Ratio

Formula Calculations Answer

2019

Current Assets / Current Liabilities

13889 / 22284 0.62: 1

2020 (13893/18656) 0.74: 1

2021 (10807/15997) 0.68: 1

Quick Ratio

Formula Calculations Answer

2019

(Current Assets -

Inventories) /

Current Liabilities

(13889 -

2433) /

22284 0.51: 1

2020 (13893 -

2433) /

18656

0.61: 1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2021

(10807 -

2069) /

15997 0.55: 1

Interpretation: The current ratio of the organisation is less than one in all three years, 0.62

in 2019, 0.74 in 2020, and 0.68 in 2021, reflecting a negative impact on their ability to repay

their short-term loan on schedule. They will, however, repay their current debt in 2021, but

their current assets will shrink. When Tesco's quick ratio is assessed, it also shows a decline,

which is considered riskier because their payback cycle is lengthier at this moment due to

their lack of liquidity in past years.

Gearing Ratios:

Debt Equity Ratio

Formula Calculations Answer

2019

(Debt / Equity)

5580 / 13548 0.41: 1

2020 (6005 / 13369) 0.45: 1

2021 (6188 / 12325) 0.50: 1

Interest Earned Ratio

Formula Calculations Answer

2019

Earnings before interest and tax / Interest Expense

1617 / 1089 1.49

2020 1315 / 1244 1.06

2021 595 / 497.4 1.2

Analysis: The company's debt equity ratio was lower in 2019, but it climbed in both 2020

and 2021. Although, based on the overall state, the optimal ratio is 1: 1, which is higher than

the company's acquisition ratio. It indicates that the company is in good shape and that the

borrowing is less than the investment. It signifies that the company has this much financial

capacity to invest in its project without relying on outsourced financing. As a result, the cost

of paying interest is reduced, and the business entity benefits in every way.

Conclusion and Recommendations (200).

The corporation TESCO has a strong presence in the market and has amassed a

significant quantity of goodwill. It has established and maintained its position

throughout time by expanding and introducing new technology and convenient factors

that satisfy their customers. As a result, it contributes to the corporation's long-term

sustainability. In addition, it has maintained a profit margin of around 10% in 2021. It

should not be diminished, and the corporation should focus more on cutting costs.

The company is well aware of the circumstances and its position in the market. The

return it has provided to its investors has been satisfactory, and they will be eager to

invest more in the company in order to receive a higher return. The company's debt is

negligible in relation to the amount of cash it has on hand. It is beneficial to the

organisation. The company has a modest debt level and chooses short and long-term

financing options. Because maintaining a balance between both sources is essential for

all businesses.

(10807 -

2069) /

15997 0.55: 1

Interpretation: The current ratio of the organisation is less than one in all three years, 0.62

in 2019, 0.74 in 2020, and 0.68 in 2021, reflecting a negative impact on their ability to repay

their short-term loan on schedule. They will, however, repay their current debt in 2021, but

their current assets will shrink. When Tesco's quick ratio is assessed, it also shows a decline,

which is considered riskier because their payback cycle is lengthier at this moment due to

their lack of liquidity in past years.

Gearing Ratios:

Debt Equity Ratio

Formula Calculations Answer

2019

(Debt / Equity)

5580 / 13548 0.41: 1

2020 (6005 / 13369) 0.45: 1

2021 (6188 / 12325) 0.50: 1

Interest Earned Ratio

Formula Calculations Answer

2019

Earnings before interest and tax / Interest Expense

1617 / 1089 1.49

2020 1315 / 1244 1.06

2021 595 / 497.4 1.2

Analysis: The company's debt equity ratio was lower in 2019, but it climbed in both 2020

and 2021. Although, based on the overall state, the optimal ratio is 1: 1, which is higher than

the company's acquisition ratio. It indicates that the company is in good shape and that the

borrowing is less than the investment. It signifies that the company has this much financial

capacity to invest in its project without relying on outsourced financing. As a result, the cost

of paying interest is reduced, and the business entity benefits in every way.

Conclusion and Recommendations (200).

The corporation TESCO has a strong presence in the market and has amassed a

significant quantity of goodwill. It has established and maintained its position

throughout time by expanding and introducing new technology and convenient factors

that satisfy their customers. As a result, it contributes to the corporation's long-term

sustainability. In addition, it has maintained a profit margin of around 10% in 2021. It

should not be diminished, and the corporation should focus more on cutting costs.

The company is well aware of the circumstances and its position in the market. The

return it has provided to its investors has been satisfactory, and they will be eager to

invest more in the company in order to receive a higher return. The company's debt is

negligible in relation to the amount of cash it has on hand. It is beneficial to the

organisation. The company has a modest debt level and chooses short and long-term

financing options. Because maintaining a balance between both sources is essential for

all businesses.

References

Allouhi, A. and Amine, M.B., 2019. Effect analysis on energetic, exergetic and financial

performance of a flat plate collector with heat pipes. Energy Conversion and

Management, 195, pp.274-289.

Huth, C., 2020. Who invests in financial instruments of sport clubs? An empirical analysis of

actual and potential individual investors of professional European football clubs.

European Sport Management Quarterly, 20(4), pp.500-519.

Liu, Z. and Shang, P., 2018. Generalized information entropy analysis of financial time

series. Physica A: Statistical Mechanics and its Applications, 505, pp.1170-1185.

Ong, S.L. and Sato, K., 2018. Regional or global shock? A global VAR analysis of Asian

economic and financial integration. The North American Journal of Economics and

Finance, 46, pp.232-248.

Ottaviani, C. and Vandone, D., 2018. Financial literacy, debt burden and impulsivity: A

mediation analysis. Economic Notes: Review of Banking, Finance and Monetary

Economics, 47(2-3), pp.439-454.

Rao, U. and Mishra, T., 2020. Posterior analysis of mergers and acquisitions in the

international financial market: A re-appraisal. Research in International Business

and Finance, 51, p.101062.

Rizi, A.P., Ashrafzadeh, A. and Ramezani, A., 2019. A financial comparative study of solar

and regular irrigation pumps: Case studies in eastern and southern Iran. Renewable

Energy, 138, pp.1096-1103.

Wu, Y., Shang, P. and Li, Y., 2018. Modified generalized multiscale sample entropy and

surrogate data analysis for financial time series. Nonlinear Dynamics, 92(3),

pp.1335-1350.

Allouhi, A. and Amine, M.B., 2019. Effect analysis on energetic, exergetic and financial

performance of a flat plate collector with heat pipes. Energy Conversion and

Management, 195, pp.274-289.

Huth, C., 2020. Who invests in financial instruments of sport clubs? An empirical analysis of

actual and potential individual investors of professional European football clubs.

European Sport Management Quarterly, 20(4), pp.500-519.

Liu, Z. and Shang, P., 2018. Generalized information entropy analysis of financial time

series. Physica A: Statistical Mechanics and its Applications, 505, pp.1170-1185.

Ong, S.L. and Sato, K., 2018. Regional or global shock? A global VAR analysis of Asian

economic and financial integration. The North American Journal of Economics and

Finance, 46, pp.232-248.

Ottaviani, C. and Vandone, D., 2018. Financial literacy, debt burden and impulsivity: A

mediation analysis. Economic Notes: Review of Banking, Finance and Monetary

Economics, 47(2-3), pp.439-454.

Rao, U. and Mishra, T., 2020. Posterior analysis of mergers and acquisitions in the

international financial market: A re-appraisal. Research in International Business

and Finance, 51, p.101062.

Rizi, A.P., Ashrafzadeh, A. and Ramezani, A., 2019. A financial comparative study of solar

and regular irrigation pumps: Case studies in eastern and southern Iran. Renewable

Energy, 138, pp.1096-1103.

Wu, Y., Shang, P. and Li, Y., 2018. Modified generalized multiscale sample entropy and

surrogate data analysis for financial time series. Nonlinear Dynamics, 92(3),

pp.1335-1350.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Appendixes

1 out of 7

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.