Financial Analysis of Toyota Motors and Sustainability Reporting under GRI

VerifiedAdded on 2023/06/06

|18

|3903

|229

AI Summary

This report analyses the sustainability reporting of Toyota Motors under GRI and compares it with BMW Group. It discusses the environmental and social impact of Toyota's operations, compliance with GRI disclosures, and the importance of global reporting standards. It also includes a breakeven analysis and evaluation of success using a balanced scorecard.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: FINANCIAL MANAGEMENT

Financial Management

Name of the Student:

Name of the University:

Author’s Note:

Financial Management

Name of the Student:

Name of the University:

Author’s Note:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

FINANCIAL ANALYSIS

Executive Summary

This report takes an honest attempt to analyse various aspect of sustainability reporting under

GRI for the business operations of Toyota Motors. This report takes into account the major

effects of the business operations of Toyota Motors. After that, it shows the compliance of

the company with the disclosure requirement of GRI. The next part compares the

sustainability reports of Toyota Motors and BMW Group. The last part indicates towards the

benefits of sustainability reporting for the investors.

Executive Summary

This report takes an honest attempt to analyse various aspect of sustainability reporting under

GRI for the business operations of Toyota Motors. This report takes into account the major

effects of the business operations of Toyota Motors. After that, it shows the compliance of

the company with the disclosure requirement of GRI. The next part compares the

sustainability reports of Toyota Motors and BMW Group. The last part indicates towards the

benefits of sustainability reporting for the investors.

FINANCIAL ANALYSIS

Table of Contents

Part A.........................................................................................................................................4

Introduction............................................................................................................................4

Environmental and Social Impact of Toyota Motor Corporation’s Operations.....................4

Four Key GRI Disclosures.....................................................................................................5

Importance of Global Reporting Standards............................................................................8

Part B........................................................................................................................................10

Part C........................................................................................................................................12

Breakeven Analysis..............................................................................................................12

Memo...................................................................................................................................14

Conclusion................................................................................................................................16

Reference..................................................................................................................................17

Table of Contents

Part A.........................................................................................................................................4

Introduction............................................................................................................................4

Environmental and Social Impact of Toyota Motor Corporation’s Operations.....................4

Four Key GRI Disclosures.....................................................................................................5

Importance of Global Reporting Standards............................................................................8

Part B........................................................................................................................................10

Part C........................................................................................................................................12

Breakeven Analysis..............................................................................................................12

Memo...................................................................................................................................14

Conclusion................................................................................................................................16

Reference..................................................................................................................................17

FINANCIAL ANALYSIS

Part A

Introduction

In today’s business worlds, it has become mandatory for the business entities around

the globe to disclose all of their activities related to environment and sustainability as the

customers all over the world has become aware of the negative effects of the business

activities on the environment. For this reason, it has become necessary for the companies to

publish their sustainability reports from which the customers can obtain information about the

sustainability activities of the companies. In this context, it is needed to mention about Global

Reporting Initiative (GRI) Standards as it is the first global standards for the purpose of

sustainability reporting. More specifically, ‘GRI-102: General Disclosures’ puts the

obligation on the business organization to disclose all the required information related to the

sustainability reporting of the companies (globalreporting.org, 2018). The main aim of this

report is to conduct an analysis and evaluation of different sustainability reporting related

activities of Toyota Motor Corporation.

Environmental and Social Impact of Toyota Motor Corporation’s Operations

It can be seen from the 2017 Annual Report as well as Sustainability Report of Toyota

Motors that the business operations of the company have some major effects on the

environment as well as the society and they are discussed below:

The first major negative impact of the business operations of Toyota Motors is the

emission of carbon. Carbon emission from the motor vehicles of Toyota Motors has major

negative impact on the environment. Apart from this, another major source of carbon

emission in Toyota Motors is their production facility (Toyota-global.com, 2018). In this

context, it needs to be mentioned that some of the operations of Toyota Motors involve in

massive carbon emission like process of material production and others; and all these

Part A

Introduction

In today’s business worlds, it has become mandatory for the business entities around

the globe to disclose all of their activities related to environment and sustainability as the

customers all over the world has become aware of the negative effects of the business

activities on the environment. For this reason, it has become necessary for the companies to

publish their sustainability reports from which the customers can obtain information about the

sustainability activities of the companies. In this context, it is needed to mention about Global

Reporting Initiative (GRI) Standards as it is the first global standards for the purpose of

sustainability reporting. More specifically, ‘GRI-102: General Disclosures’ puts the

obligation on the business organization to disclose all the required information related to the

sustainability reporting of the companies (globalreporting.org, 2018). The main aim of this

report is to conduct an analysis and evaluation of different sustainability reporting related

activities of Toyota Motor Corporation.

Environmental and Social Impact of Toyota Motor Corporation’s Operations

It can be seen from the 2017 Annual Report as well as Sustainability Report of Toyota

Motors that the business operations of the company have some major effects on the

environment as well as the society and they are discussed below:

The first major negative impact of the business operations of Toyota Motors is the

emission of carbon. Carbon emission from the motor vehicles of Toyota Motors has major

negative impact on the environment. Apart from this, another major source of carbon

emission in Toyota Motors is their production facility (Toyota-global.com, 2018). In this

context, it needs to be mentioned that some of the operations of Toyota Motors involve in

massive carbon emission like process of material production and others; and all these

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

FINANCIAL ANALYSIS

processes have major negative impact on the society After that, the next major positive

impact of Toyota Motors’ operation comes in the form of Recycling-based society and

system. It needs to be mentioned that, over the last 40 years, the aim of Toyota Motors has

been to recycle the environmental and social resources for the betterment of the society

(toyota-global.com, 2018). After that, excessive usage of water along with wastage of water

has been the major negative impact of the business operations of Toyota Motors. Excessive

use of water can be seen in the plants of Toyota Motors for various purposes like painting,

forging and other processes. For this reason, it is considered as a major environmental issue

of the business of Toyota Motors. At the same time, Toyota Motors has been engaged in

some specific social activities like plantation of trees, environmental consecutive activities

and others that are majorly helpful for the environment as well as the society (toyota-

global.com, 2018).

Four Key GRI Disclosures

It can be seen from the earlier discussion that the GRI reporting framework puts the

obligation on the business entities to disclose different aspects and the below discussion

shows four of them:

According to GRI Disclosure 102-18 Governance Structure, it is the obligation on the

business organizations provide the information related to their governance structure and its

composition. At the same time, it is needed for the companies to provide information of the

role of governance body, governance for audit, sustainability reporting and others. After that,

as per GRI Disclosure 102-45, it is needed for the business entities to include the

consolidated financial statements for providing the required information (globalreporting.org,

2018). After that, as per GRI Disclosure 102-30, the companies are needed to disclose the

details about their risk management process along with their effectiveness. Lastly, as per GRI

processes have major negative impact on the society After that, the next major positive

impact of Toyota Motors’ operation comes in the form of Recycling-based society and

system. It needs to be mentioned that, over the last 40 years, the aim of Toyota Motors has

been to recycle the environmental and social resources for the betterment of the society

(toyota-global.com, 2018). After that, excessive usage of water along with wastage of water

has been the major negative impact of the business operations of Toyota Motors. Excessive

use of water can be seen in the plants of Toyota Motors for various purposes like painting,

forging and other processes. For this reason, it is considered as a major environmental issue

of the business of Toyota Motors. At the same time, Toyota Motors has been engaged in

some specific social activities like plantation of trees, environmental consecutive activities

and others that are majorly helpful for the environment as well as the society (toyota-

global.com, 2018).

Four Key GRI Disclosures

It can be seen from the earlier discussion that the GRI reporting framework puts the

obligation on the business entities to disclose different aspects and the below discussion

shows four of them:

According to GRI Disclosure 102-18 Governance Structure, it is the obligation on the

business organizations provide the information related to their governance structure and its

composition. At the same time, it is needed for the companies to provide information of the

role of governance body, governance for audit, sustainability reporting and others. After that,

as per GRI Disclosure 102-45, it is needed for the business entities to include the

consolidated financial statements for providing the required information (globalreporting.org,

2018). After that, as per GRI Disclosure 102-30, the companies are needed to disclose the

details about their risk management process along with their effectiveness. Lastly, as per GRI

FINANCIAL ANALYSIS

Disclosure 102-35, it is needed for the business organizations to provide all the details about

the remuneration policies of the companies (globalreporting.org, 2018).

It needs to be mentioned that Toyota Motors develops their annual report as well as

sustainability report after complying with the disclosure requirements of GRI 102: General

Disclosures. As per the 2017 Annual Report of Toyota Motors, the company has provided the

required information about corporate governance by complying with the principles of GRI

Disclosure 102-45 (toyota-global.com, 2018). This Section includes fundamental approach of

governance, board composition, business executives and supervisions, audit and supervisory

board and others. After that, it can also be observed from the 2017 Annual Report of Toyota

Motors that the company has included all the required financial statements in their annual

report like consolidated balance sheet, statement of cash flow, consolidated statement of

income and others; and it shows the compliance of the company with GRI 102-45 (toyota-

global.com, 2018). This report of Toyota Motors also includes all the details about the risk

management process that includes business and other risks; and it shows the compliance of

Toyota Motors with GRI Disclosure 102-30. Lastly, Toyota Motors has provided the

information about the remuneration of board members and audit committee in the report that

shows the compliance with GRI Disclosure 102-35 (toyota-global.com, 2018).

Disclosure 102-35, it is needed for the business organizations to provide all the details about

the remuneration policies of the companies (globalreporting.org, 2018).

It needs to be mentioned that Toyota Motors develops their annual report as well as

sustainability report after complying with the disclosure requirements of GRI 102: General

Disclosures. As per the 2017 Annual Report of Toyota Motors, the company has provided the

required information about corporate governance by complying with the principles of GRI

Disclosure 102-45 (toyota-global.com, 2018). This Section includes fundamental approach of

governance, board composition, business executives and supervisions, audit and supervisory

board and others. After that, it can also be observed from the 2017 Annual Report of Toyota

Motors that the company has included all the required financial statements in their annual

report like consolidated balance sheet, statement of cash flow, consolidated statement of

income and others; and it shows the compliance of the company with GRI 102-45 (toyota-

global.com, 2018). This report of Toyota Motors also includes all the details about the risk

management process that includes business and other risks; and it shows the compliance of

Toyota Motors with GRI Disclosure 102-30. Lastly, Toyota Motors has provided the

information about the remuneration of board members and audit committee in the report that

shows the compliance with GRI Disclosure 102-35 (toyota-global.com, 2018).

FINANCIAL ANALYSIS

Quality and Depth Analysis of the Sustainability Report.

The sustainability report is prepared by the company along with the annual report of the

company for providing a comprehensive knowledge about the sustainable strategy about the

company and the progress the companies are making in the sustainable corporate progress.

Both the companies have a wide and diversified wide range of the initiatives it takes in

addressing the global environmental issues. The issue, which the Toyota Motor Corporation

deals with is the extreme nature and climate effects such as weather changes, emissions of

greenhouse gas, focus on depleting biodiversity, which gets indirectly influenced by the

operations of the company. The Toyota Motor Corporation has developed and built strategies

like the Toyota environmental Challenge 2050 in lieu of the changing and depleting

environmental resources and the surroundings. The main motive behind such initiatives

would be reducing the environmental burden on automobiles and other products. Addressing

key issues, which directly influence the environment and the biodiversity and measures for

the same would be taken to reduce the same (Toyota Environmental Challenge 2050, 2018).

The major steps taken by the company are:

Reducing CO2 emissions by enhancing the framework of the production and

designing of the product

Minimizing and efficient utilization of water

Creation of a recyclable society and systems involved

Reducing Energy Consumption by adopting renewable sources of energy.

The BMW group on the other hand the largest automobile company is also having

several measure and steps for reducing the environmental burden and influence on the same

through some key strategies. The BMW 2020 year plan is the key initiative the company is

undergoing through by reducing the emission amount of CO2 and other harmful pollutants,

Quality and Depth Analysis of the Sustainability Report.

The sustainability report is prepared by the company along with the annual report of the

company for providing a comprehensive knowledge about the sustainable strategy about the

company and the progress the companies are making in the sustainable corporate progress.

Both the companies have a wide and diversified wide range of the initiatives it takes in

addressing the global environmental issues. The issue, which the Toyota Motor Corporation

deals with is the extreme nature and climate effects such as weather changes, emissions of

greenhouse gas, focus on depleting biodiversity, which gets indirectly influenced by the

operations of the company. The Toyota Motor Corporation has developed and built strategies

like the Toyota environmental Challenge 2050 in lieu of the changing and depleting

environmental resources and the surroundings. The main motive behind such initiatives

would be reducing the environmental burden on automobiles and other products. Addressing

key issues, which directly influence the environment and the biodiversity and measures for

the same would be taken to reduce the same (Toyota Environmental Challenge 2050, 2018).

The major steps taken by the company are:

Reducing CO2 emissions by enhancing the framework of the production and

designing of the product

Minimizing and efficient utilization of water

Creation of a recyclable society and systems involved

Reducing Energy Consumption by adopting renewable sources of energy.

The BMW group on the other hand the largest automobile company is also having

several measure and steps for reducing the environmental burden and influence on the same

through some key strategies. The BMW 2020 year plan is the key initiative the company is

undergoing through by reducing the emission amount of CO2 and other harmful pollutants,

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCIAL ANALYSIS

which could indirectly influence the environment. The company through its plan has decided

to reduce the emission of the CO2 gas by about 50% in the European new vehicles fleet

(BMW Group, 2017). Some of the key target and measure by the company are:

Reducing CO2 emissions of the BMW group company.

Delivering more electric cars

Creation and adoption of renewable sources of energy.

Importance of Global Reporting Standards

The Global Reporting Standards is the standard for reporting sustainable reporting of

financial information and statements. The Global Reporting standards help the investors,

stakeholders and other shareholder of the company by creating a modular structure and thus

that would enable the best practices of financial reporting (Fernandez-Feijoo, Romero &

Ruiz, 2014). The widespread compliance with the GRI standards from the other motor

vehicle corporations in the industry would benefit the stakeholders of the company’s

operating in and around the same sector of the industry. The common and adherence to the

global reporting standard would enable the investor to form a basis for comparison of

financial information presented in the financial report of the company. The reporting standard

would enable the companies to accurately classify and record transactions according to the

guidelines and principles mentioned by the reporting standards. The common reporting

standard would also enhance the transparency and fairness in the financial information

provided by the company. The main motive behind the global reporting standard is that the

investors and stakeholder of the company should be able to compare returns and financial

information presented by companies by different way of accounting (del Mar Alonso‐

Almeida, Llach & Marimon, 2014).

which could indirectly influence the environment. The company through its plan has decided

to reduce the emission of the CO2 gas by about 50% in the European new vehicles fleet

(BMW Group, 2017). Some of the key target and measure by the company are:

Reducing CO2 emissions of the BMW group company.

Delivering more electric cars

Creation and adoption of renewable sources of energy.

Importance of Global Reporting Standards

The Global Reporting Standards is the standard for reporting sustainable reporting of

financial information and statements. The Global Reporting standards help the investors,

stakeholders and other shareholder of the company by creating a modular structure and thus

that would enable the best practices of financial reporting (Fernandez-Feijoo, Romero &

Ruiz, 2014). The widespread compliance with the GRI standards from the other motor

vehicle corporations in the industry would benefit the stakeholders of the company’s

operating in and around the same sector of the industry. The common and adherence to the

global reporting standard would enable the investor to form a basis for comparison of

financial information presented in the financial report of the company. The reporting standard

would enable the companies to accurately classify and record transactions according to the

guidelines and principles mentioned by the reporting standards. The common reporting

standard would also enhance the transparency and fairness in the financial information

provided by the company. The main motive behind the global reporting standard is that the

investors and stakeholder of the company should be able to compare returns and financial

information presented by companies by different way of accounting (del Mar Alonso‐

Almeida, Llach & Marimon, 2014).

FINANCIAL ANALYSIS

The benefits and the features of common financial reporting would be that the

classification of accounts based on accrual and judgemental basis is eliminated when certain

guidelines and principles will be accounted. There might be companies recording the same

nature of income or expenses for the company in different ways. Companies following the

global reporting standard would be benefited by treating expenses and income for the

company under common head. Common Accountability and transactions of the accounts is

necessary for the industry. Thus global accounting standard would bring about best corporate

governance in the industry by common reporting of financial informations and statements

(Tschopp, & Nastanski, 2014).

The benefits and the features of common financial reporting would be that the

classification of accounts based on accrual and judgemental basis is eliminated when certain

guidelines and principles will be accounted. There might be companies recording the same

nature of income or expenses for the company in different ways. Companies following the

global reporting standard would be benefited by treating expenses and income for the

company under common head. Common Accountability and transactions of the accounts is

necessary for the industry. Thus global accounting standard would bring about best corporate

governance in the industry by common reporting of financial informations and statements

(Tschopp, & Nastanski, 2014).

FINANCIAL ANALYSIS

Part B

1) The major costs associated with the ongoing operations of the production line with the

Smart Vehicle is all about developing the overall company from an hardware

company to a new companies, which has the capabilities of transforming itself into a

technology driven company. The improvements by the company could be in the field

of Artificial intelligence, automated driving facilities, robotic and high tech advanced

features for the new modern and smart cars. The cost associated with the same would

be advancement in the field of technology, which could be explored by company

investing more into the research and development section of the company. The

advancement in the field of Artificial Intelligence, which would help the company

gather important relevant data about the taste and preference of the consumers. The

advancement in the smart car through robotic features and tech drive cars could

enhance the driving experience of the customers. Advancement in the human

resources skills and knowledge could be one of the major factor driving the company

toward long term growth and prosperity (Palia, 2014).

2) The cost behaviour may be classified into three major categories either fixed or

variable cost. The major costs identified was creating and pooling of data through

artificial intelligence, whose classification of expense could be classified as variable

expense. Inclusion of robotic features and new tech driven facilities and amenities in

the car would be done by the company by investing more and more into technology

driven software’s, hardware’s and equipment’s. The classification for such expenses

done would come other as fixed expenses as the cost incurred for buying those

products will be used in the long term. Advancement in human resources skills and

knowledge could be done through extensive training and development of the

Part B

1) The major costs associated with the ongoing operations of the production line with the

Smart Vehicle is all about developing the overall company from an hardware

company to a new companies, which has the capabilities of transforming itself into a

technology driven company. The improvements by the company could be in the field

of Artificial intelligence, automated driving facilities, robotic and high tech advanced

features for the new modern and smart cars. The cost associated with the same would

be advancement in the field of technology, which could be explored by company

investing more into the research and development section of the company. The

advancement in the field of Artificial Intelligence, which would help the company

gather important relevant data about the taste and preference of the consumers. The

advancement in the smart car through robotic features and tech drive cars could

enhance the driving experience of the customers. Advancement in the human

resources skills and knowledge could be one of the major factor driving the company

toward long term growth and prosperity (Palia, 2014).

2) The cost behaviour may be classified into three major categories either fixed or

variable cost. The major costs identified was creating and pooling of data through

artificial intelligence, whose classification of expense could be classified as variable

expense. Inclusion of robotic features and new tech driven facilities and amenities in

the car would be done by the company by investing more and more into technology

driven software’s, hardware’s and equipment’s. The classification for such expenses

done would come other as fixed expenses as the cost incurred for buying those

products will be used in the long term. Advancement in human resources skills and

knowledge could be done through extensive training and development of the

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

FINANCIAL ANALYSIS

employees. The classification for such kind of expenses would be variable as the cost

would depend from employee’s base to training requirements.

3) Yes the use of breakeven analysis could be one of the useful and reliable screening

tools for the Toyota Motor Corporation. The company should go along with the

scenario analysis and breakeven strategy in order to perform a better screening tool

for the company cost benefit analysis. The desirability of the new product would only

fit into the company’s business model if the cost incurred for the same and the return

generated from the same is sufficient for the company. The breakeven analysis for the

product would give the company an estimate about the minimum products, which

needs to be sold and delivered in the market to at least get cover for the primary costs

of developing the products.

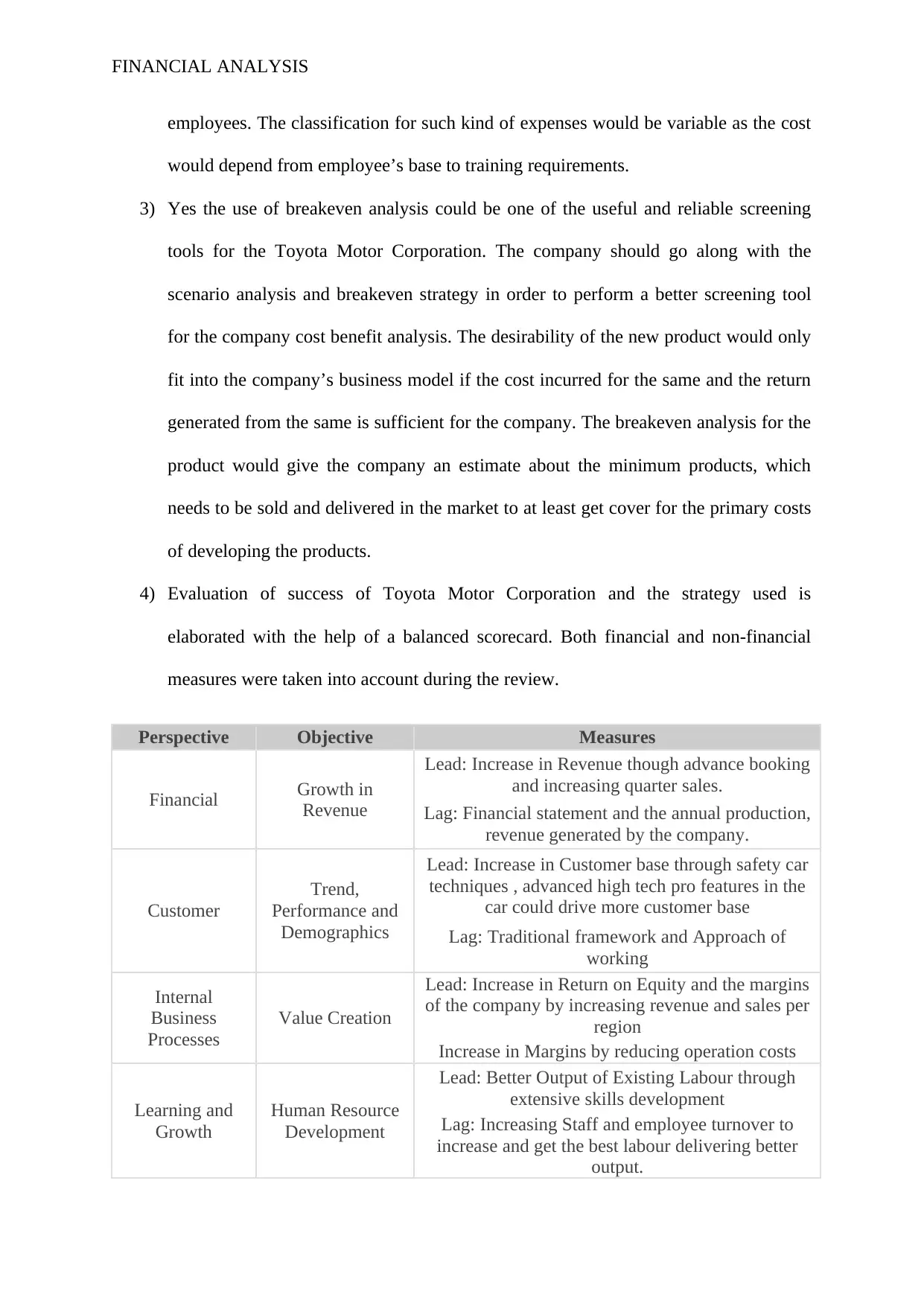

4) Evaluation of success of Toyota Motor Corporation and the strategy used is

elaborated with the help of a balanced scorecard. Both financial and non-financial

measures were taken into account during the review.

Perspective Objective Measures

Financial Growth in

Revenue

Lead: Increase in Revenue though advance booking

and increasing quarter sales.

Lag: Financial statement and the annual production,

revenue generated by the company.

Customer

Trend,

Performance and

Demographics

Lead: Increase in Customer base through safety car

techniques , advanced high tech pro features in the

car could drive more customer base

Lag: Traditional framework and Approach of

working

Internal

Business

Processes

Value Creation

Lead: Increase in Return on Equity and the margins

of the company by increasing revenue and sales per

region

Increase in Margins by reducing operation costs

Learning and

Growth

Human Resource

Development

Lead: Better Output of Existing Labour through

extensive skills development

Lag: Increasing Staff and employee turnover to

increase and get the best labour delivering better

output.

employees. The classification for such kind of expenses would be variable as the cost

would depend from employee’s base to training requirements.

3) Yes the use of breakeven analysis could be one of the useful and reliable screening

tools for the Toyota Motor Corporation. The company should go along with the

scenario analysis and breakeven strategy in order to perform a better screening tool

for the company cost benefit analysis. The desirability of the new product would only

fit into the company’s business model if the cost incurred for the same and the return

generated from the same is sufficient for the company. The breakeven analysis for the

product would give the company an estimate about the minimum products, which

needs to be sold and delivered in the market to at least get cover for the primary costs

of developing the products.

4) Evaluation of success of Toyota Motor Corporation and the strategy used is

elaborated with the help of a balanced scorecard. Both financial and non-financial

measures were taken into account during the review.

Perspective Objective Measures

Financial Growth in

Revenue

Lead: Increase in Revenue though advance booking

and increasing quarter sales.

Lag: Financial statement and the annual production,

revenue generated by the company.

Customer

Trend,

Performance and

Demographics

Lead: Increase in Customer base through safety car

techniques , advanced high tech pro features in the

car could drive more customer base

Lag: Traditional framework and Approach of

working

Internal

Business

Processes

Value Creation

Lead: Increase in Return on Equity and the margins

of the company by increasing revenue and sales per

region

Increase in Margins by reducing operation costs

Learning and

Growth

Human Resource

Development

Lead: Better Output of Existing Labour through

extensive skills development

Lag: Increasing Staff and employee turnover to

increase and get the best labour delivering better

output.

FINANCIAL ANALYSIS

The key features involved in the scorecard and the reasons which explains the overall

success of the Toyota Motor Corporation is about development of products and ideas through

which the company caters its customers. The financial perspective taken, which explains the

growth in revenue can be done through different strategies of revenue generation like

advance booking and by increasing the sales of the company. The old traditional method

should be avoided which just include buying selling products instead of buying selling

products and after sales services. The customer approach was identified in order to get an

overview of the type and category of customer, which the company caters. The quality and

the type of advanced services they expect to be included in the product. Internal Business

process or the value creation as the primary objective was chosen to check and observe the

return company generates. Companies should operate in a way, which would adhere to the

customer according to their preference and the type of product expectation they. Traditional

method included volume activity of buying and selling similar products, which would not

differentiate between various classes and kinds of customer base and profile. The learning

and development of the human resources of the company is the most important and

significant category in the overall success of the company. The company through extensive

training and development of trained and skilled employee could achieve the same. Turnover

of employee base would often distort the company’s working environment and would be

ineffective for long-term growth and prosperity of the company.

Part C

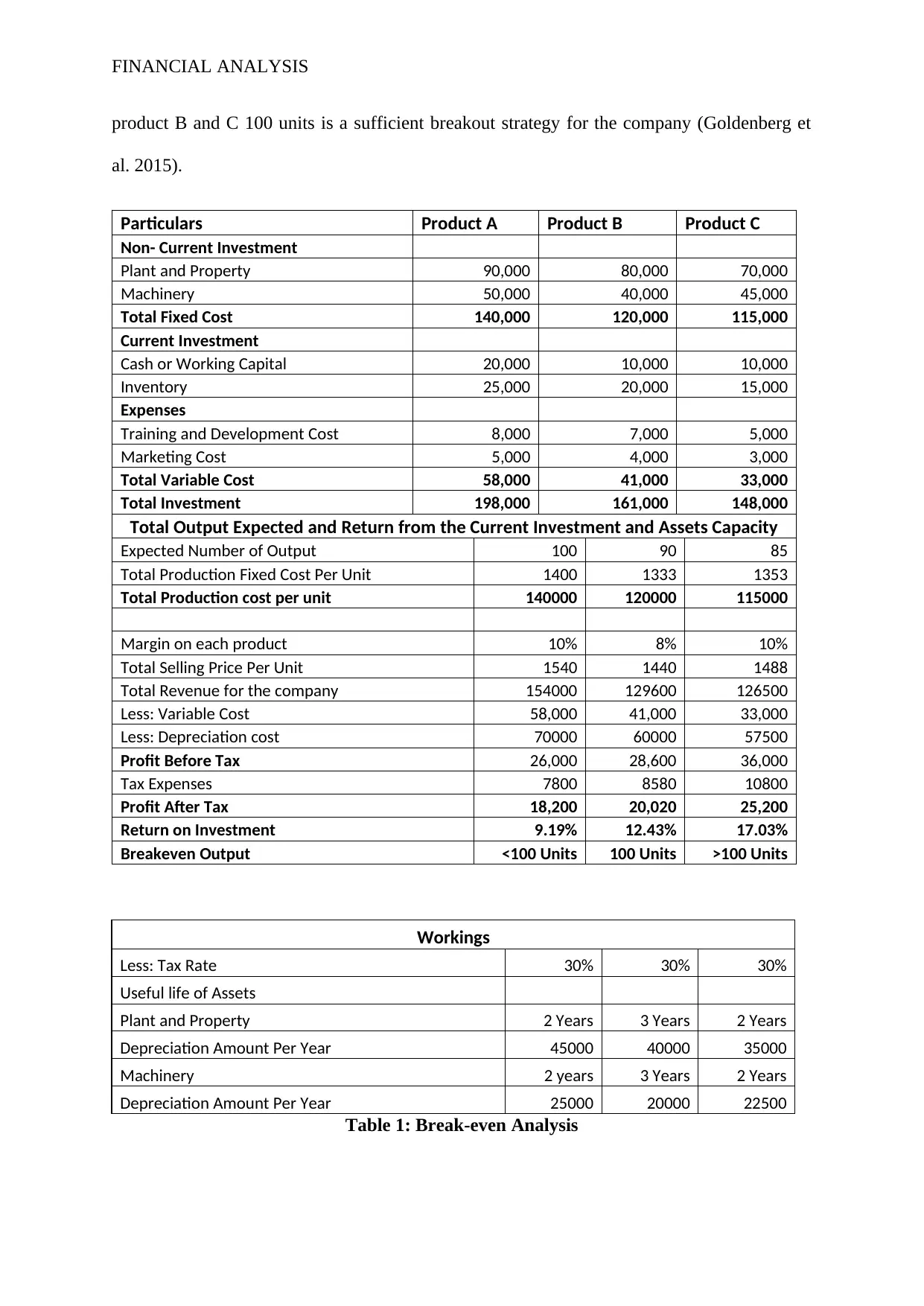

Breakeven Analysis

There were a total number of three hypothetical products selected of which the

breakdown of the cost and variance analysis is performed. The fixed cost and the variance

cost of the company is broken down as per unit production cost to the company. The breakout

for Product A will be when the company produces product greater than 100 units. In case of

The key features involved in the scorecard and the reasons which explains the overall

success of the Toyota Motor Corporation is about development of products and ideas through

which the company caters its customers. The financial perspective taken, which explains the

growth in revenue can be done through different strategies of revenue generation like

advance booking and by increasing the sales of the company. The old traditional method

should be avoided which just include buying selling products instead of buying selling

products and after sales services. The customer approach was identified in order to get an

overview of the type and category of customer, which the company caters. The quality and

the type of advanced services they expect to be included in the product. Internal Business

process or the value creation as the primary objective was chosen to check and observe the

return company generates. Companies should operate in a way, which would adhere to the

customer according to their preference and the type of product expectation they. Traditional

method included volume activity of buying and selling similar products, which would not

differentiate between various classes and kinds of customer base and profile. The learning

and development of the human resources of the company is the most important and

significant category in the overall success of the company. The company through extensive

training and development of trained and skilled employee could achieve the same. Turnover

of employee base would often distort the company’s working environment and would be

ineffective for long-term growth and prosperity of the company.

Part C

Breakeven Analysis

There were a total number of three hypothetical products selected of which the

breakdown of the cost and variance analysis is performed. The fixed cost and the variance

cost of the company is broken down as per unit production cost to the company. The breakout

for Product A will be when the company produces product greater than 100 units. In case of

FINANCIAL ANALYSIS

product B and C 100 units is a sufficient breakout strategy for the company (Goldenberg et

al. 2015).

Particulars Product A Product B Product C

Non- Current Investment

Plant and Property 90,000 80,000 70,000

Machinery 50,000 40,000 45,000

Total Fixed Cost 140,000 120,000 115,000

Current Investment

Cash or Working Capital 20,000 10,000 10,000

Inventory 25,000 20,000 15,000

Expenses

Training and Development Cost 8,000 7,000 5,000

Marketing Cost 5,000 4,000 3,000

Total Variable Cost 58,000 41,000 33,000

Total Investment 198,000 161,000 148,000

Total Output Expected and Return from the Current Investment and Assets Capacity

Expected Number of Output 100 90 85

Total Production Fixed Cost Per Unit 1400 1333 1353

Total Production cost per unit 140000 120000 115000

Margin on each product 10% 8% 10%

Total Selling Price Per Unit 1540 1440 1488

Total Revenue for the company 154000 129600 126500

Less: Variable Cost 58,000 41,000 33,000

Less: Depreciation cost 70000 60000 57500

Profit Before Tax 26,000 28,600 36,000

Tax Expenses 7800 8580 10800

Profit After Tax 18,200 20,020 25,200

Return on Investment 9.19% 12.43% 17.03%

Breakeven Output <100 Units 100 Units >100 Units

Workings

Less: Tax Rate 30% 30% 30%

Useful life of Assets

Plant and Property 2 Years 3 Years 2 Years

Depreciation Amount Per Year 45000 40000 35000

Machinery 2 years 3 Years 2 Years

Depreciation Amount Per Year 25000 20000 22500

Table 1: Break-even Analysis

product B and C 100 units is a sufficient breakout strategy for the company (Goldenberg et

al. 2015).

Particulars Product A Product B Product C

Non- Current Investment

Plant and Property 90,000 80,000 70,000

Machinery 50,000 40,000 45,000

Total Fixed Cost 140,000 120,000 115,000

Current Investment

Cash or Working Capital 20,000 10,000 10,000

Inventory 25,000 20,000 15,000

Expenses

Training and Development Cost 8,000 7,000 5,000

Marketing Cost 5,000 4,000 3,000

Total Variable Cost 58,000 41,000 33,000

Total Investment 198,000 161,000 148,000

Total Output Expected and Return from the Current Investment and Assets Capacity

Expected Number of Output 100 90 85

Total Production Fixed Cost Per Unit 1400 1333 1353

Total Production cost per unit 140000 120000 115000

Margin on each product 10% 8% 10%

Total Selling Price Per Unit 1540 1440 1488

Total Revenue for the company 154000 129600 126500

Less: Variable Cost 58,000 41,000 33,000

Less: Depreciation cost 70000 60000 57500

Profit Before Tax 26,000 28,600 36,000

Tax Expenses 7800 8580 10800

Profit After Tax 18,200 20,020 25,200

Return on Investment 9.19% 12.43% 17.03%

Breakeven Output <100 Units 100 Units >100 Units

Workings

Less: Tax Rate 30% 30% 30%

Useful life of Assets

Plant and Property 2 Years 3 Years 2 Years

Depreciation Amount Per Year 45000 40000 35000

Machinery 2 years 3 Years 2 Years

Depreciation Amount Per Year 25000 20000 22500

Table 1: Break-even Analysis

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCIAL ANALYSIS

Memo

To: Toyota Motor Corporation

Cc: Toyota Directors

From: Accounts Department

Date: September 16, 2018

Subject: Strategic Initiatives for Toyota Motor Corporation

The letter is to address about the key strategies, which can be implemented by the Toyota

Motor Corporation. The strategies, which can enhance the breakeven point is by reducing the

variable cost of the product or by increasing the selling price of the product. The same will

enable the company to deliver more revenue and deliver better output of the capital invested.

Three major strategies defined for the company to enhance the breakeven are:

Increasing Selling Price

Eliminating and Reducing Fixed Cost component

Cross selling of products and services.

The initiatives and strategies implemented could affect the companies selling price, variable

costs such as marketing costs for the company and reducing fixed costs by efficiently

utilisation of assets. The company would have to invest more into Research and development

cost for the product in order to deliver quality products. The company variable cost will be

dependent on the unit produced so the production and the turnover of the units produced. The

ability for the company in efficiently utilising its fixed and variable costs to enhance the

return on investment for the stakeholders of the company. The working shown in Table 1

shows the impact of changing variable and fixed costs for the company and the return

Memo

To: Toyota Motor Corporation

Cc: Toyota Directors

From: Accounts Department

Date: September 16, 2018

Subject: Strategic Initiatives for Toyota Motor Corporation

The letter is to address about the key strategies, which can be implemented by the Toyota

Motor Corporation. The strategies, which can enhance the breakeven point is by reducing the

variable cost of the product or by increasing the selling price of the product. The same will

enable the company to deliver more revenue and deliver better output of the capital invested.

Three major strategies defined for the company to enhance the breakeven are:

Increasing Selling Price

Eliminating and Reducing Fixed Cost component

Cross selling of products and services.

The initiatives and strategies implemented could affect the companies selling price, variable

costs such as marketing costs for the company and reducing fixed costs by efficiently

utilisation of assets. The company would have to invest more into Research and development

cost for the product in order to deliver quality products. The company variable cost will be

dependent on the unit produced so the production and the turnover of the units produced. The

ability for the company in efficiently utilising its fixed and variable costs to enhance the

return on investment for the stakeholders of the company. The working shown in Table 1

shows the impact of changing variable and fixed costs for the company and the return

FINANCIAL ANALYSIS

generated from the same. The company could also enhance the annual profit of the company

by the new product by the following strategies:

Removal of Unutilised products and services of the company

Creation of new customer base

Increasing the Inventory Turnover Ratio for the company.

Reviewing and monitoring the pricing structure of the company.

The following strategies could be beneficial for the company in enhancing the breakeven

point and the annual profit for the company.

Regards,

Andrew Lewis

Accounts Department

Toyota Motor Corporation.

generated from the same. The company could also enhance the annual profit of the company

by the new product by the following strategies:

Removal of Unutilised products and services of the company

Creation of new customer base

Increasing the Inventory Turnover Ratio for the company.

Reviewing and monitoring the pricing structure of the company.

The following strategies could be beneficial for the company in enhancing the breakeven

point and the annual profit for the company.

Regards,

Andrew Lewis

Accounts Department

Toyota Motor Corporation.

FINANCIAL ANALYSIS

Conclusion

The above discussion indicates towards the fact that Toyota Motors complies with

GRI for the development of their sustainability and integrated report. Some of the major

environmental issues of the company are carbon emission, wastage of water, waste disposal

and others. However, the above discussion also indicates towards the fact that the company

has complied with the major disclosure requirement of GRI at the time of sustainability and

financial reporting. The comparison between Toyota Motors and BMW Group shows that

both the companies have take initiatives while Toyota Motors has longer sustainability

initiatives than BMW.

Conclusion

The above discussion indicates towards the fact that Toyota Motors complies with

GRI for the development of their sustainability and integrated report. Some of the major

environmental issues of the company are carbon emission, wastage of water, waste disposal

and others. However, the above discussion also indicates towards the fact that the company

has complied with the major disclosure requirement of GRI at the time of sustainability and

financial reporting. The comparison between Toyota Motors and BMW Group shows that

both the companies have take initiatives while Toyota Motors has longer sustainability

initiatives than BMW.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

FINANCIAL ANALYSIS

Reference

BMW Group. (2017). Sustainable Value Report [Ebook]. Retrieved from

https://www.bmwgroup.com/content/dam/bmw-group-

websites/bmwgroup_com/ir/downloads/en/2017/BMW-Group-

SustainableValueReport-2017--EN.pdf

del Mar Alonso‐Almeida, M., Llach, J., & Marimon, F. (2014). A closer look at the ‘Global

Reporting Initiative’sustainability reporting as a tool to implement environmental and

social policies: A worldwide sector analysis. Corporate Social Responsibility and

Environmental

Fernandez-Feijoo, B., Romero, S., & Ruiz, S. (2014). Commitment to corporate social

responsibility measured through global reporting initiative reporting: Factors affecting

the behavior of companies. Journal of Cleaner Production, 81, 244-254.

Goldenberg, S. D., Bacelar, M., Brazier, P., Bisnauthsing, K., & Edgeworth, J. D. (2015). A

cost benefit analysis of the Luminex xTAG Gastrointestinal Pathogen Panel for

detection of infectious gastroenteritis in hospitalised patients. Journal of Infection,

70(5), 504-511.

GRI Standards Download Center. (2018). Globalreporting.org. Retrieved 16 September

2018, from https://www.globalreporting.org/standards/gri-standards-download-center/

GRI Standards. (2018). GRI 102: GENERAL DISCLOSURES 2016. Retrieved 16 September

2018, from https://www.globalreporting.org/standards/media/1037/gri-102-general-

disclosures-2016.pdf

Reference

BMW Group. (2017). Sustainable Value Report [Ebook]. Retrieved from

https://www.bmwgroup.com/content/dam/bmw-group-

websites/bmwgroup_com/ir/downloads/en/2017/BMW-Group-

SustainableValueReport-2017--EN.pdf

del Mar Alonso‐Almeida, M., Llach, J., & Marimon, F. (2014). A closer look at the ‘Global

Reporting Initiative’sustainability reporting as a tool to implement environmental and

social policies: A worldwide sector analysis. Corporate Social Responsibility and

Environmental

Fernandez-Feijoo, B., Romero, S., & Ruiz, S. (2014). Commitment to corporate social

responsibility measured through global reporting initiative reporting: Factors affecting

the behavior of companies. Journal of Cleaner Production, 81, 244-254.

Goldenberg, S. D., Bacelar, M., Brazier, P., Bisnauthsing, K., & Edgeworth, J. D. (2015). A

cost benefit analysis of the Luminex xTAG Gastrointestinal Pathogen Panel for

detection of infectious gastroenteritis in hospitalised patients. Journal of Infection,

70(5), 504-511.

GRI Standards Download Center. (2018). Globalreporting.org. Retrieved 16 September

2018, from https://www.globalreporting.org/standards/gri-standards-download-center/

GRI Standards. (2018). GRI 102: GENERAL DISCLOSURES 2016. Retrieved 16 September

2018, from https://www.globalreporting.org/standards/media/1037/gri-102-general-

disclosures-2016.pdf

FINANCIAL ANALYSIS

Palia, A. P. (2014, January). Target profit pricing with the web-based breakeven analysis

package. In Developments in Business Simulation and Experiential Learning:

Proceedings of the Annual ABSEL conference (Vol. 35).

Toyota-global.com. (2018). Toyota Environmental Challenge 2050. Retrieved from

https://www.toyota-global.com/sustainability/report/archive/sr17/pdf/sdb17_077-

128_en.pdf

Toyota Global Site | Plant Zero CO<sub>2</sub> Emissions Challenge. (2018). Toyota

Motor Corporation Global Website. Retrieved 16 September 2018, from

https://www.toyota-global.com/sustainability/environment/challenge3/

Toyota Motor Corporations. (2018). Environmental Report 2017. Retrieved 16 September

2018, from https://

www.toyota-global.com/sustainability/report/archive/er17/pdf/er17_full_en.pdf

Toyota. (2018). 2017 Annual Report. Retrieved 16 September 2018, from https://

www.toyota-global.com/pages/contents/investors/ir_library/annual/pdf/2017/

annual_report_2017_fie.pdf

Tschopp, D., & Nastanski, M. (2014). The harmonization and convergence of corporate

social responsibility reporting standards. Journal of Business Ethics, 125(1), 147-162.

Palia, A. P. (2014, January). Target profit pricing with the web-based breakeven analysis

package. In Developments in Business Simulation and Experiential Learning:

Proceedings of the Annual ABSEL conference (Vol. 35).

Toyota-global.com. (2018). Toyota Environmental Challenge 2050. Retrieved from

https://www.toyota-global.com/sustainability/report/archive/sr17/pdf/sdb17_077-

128_en.pdf

Toyota Global Site | Plant Zero CO<sub>2</sub> Emissions Challenge. (2018). Toyota

Motor Corporation Global Website. Retrieved 16 September 2018, from

https://www.toyota-global.com/sustainability/environment/challenge3/

Toyota Motor Corporations. (2018). Environmental Report 2017. Retrieved 16 September

2018, from https://

www.toyota-global.com/sustainability/report/archive/er17/pdf/er17_full_en.pdf

Toyota. (2018). 2017 Annual Report. Retrieved 16 September 2018, from https://

www.toyota-global.com/pages/contents/investors/ir_library/annual/pdf/2017/

annual_report_2017_fie.pdf

Tschopp, D., & Nastanski, M. (2014). The harmonization and convergence of corporate

social responsibility reporting standards. Journal of Business Ethics, 125(1), 147-162.

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.