Comprehensive Financial Report: Stell Co Ltd Analysis and Review

VerifiedAdded on 2023/06/07

|13

|3032

|58

Report

AI Summary

This report provides a comprehensive financial analysis of Stell Co Ltd, examining its profitability, break-even point, and variance analysis. The report calculates the gross and net profit for 2020 and 2021, along with their respective sales ratios, highlighting a decline in profits and increasing cash flow problems. It explores the reasons for these issues, including reduced sales revenue, increased labor costs, and delayed cash collection. Recommendations are made to improve the financial position, such as online sales, training programs, and early payment discounts. The report also calculates the break-even point using the net contribution method and discusses the advantages and disadvantages of activity-based costing. Furthermore, it calculates sales, direct material, and direct labor variances, analyzes their possible causes and consequences, and recommends implementing a six sigma model and adopting a flexible budget. Lastly, the report evaluates the advantages and disadvantages of switching from incremental-based budgeting to zero-based budgeting.

QUESTION PAPER

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Question 1........................................................................................................................................3

1. Calculation of Gross and Net profit made by Stell Co Ltd in the year 2020 and 2021...........3

2. Calculation of Gross and Net profit to sales ratios of Stell Co Ltd for year 2020 and 2021...4

3. Reason of declining profits and increasing cash flow problems between 2020 and 2021 in

Stell Co. Ltd.................................................................................................................................4

4. Recommendations....................................................................................................................5

Question 2........................................................................................................................................6

1. Calculation of break-even point...............................................................................................6

2. Advantage and disadvantage of activity based costing...........................................................7

Question 3........................................................................................................................................7

1. Calculation of variance............................................................................................................7

2. Possible causes of sales, direct material and direct labour variance........................................8

3. Consequences of selected variance for the business and its objectives...................................9

4. Recommendation.....................................................................................................................9

5. Evaluation of advantage and disadvantage of switching from Incremental based budgeting

to Zero based budgeting.............................................................................................................10

REFERENCES................................................................................................................................1

Question 1........................................................................................................................................3

1. Calculation of Gross and Net profit made by Stell Co Ltd in the year 2020 and 2021...........3

2. Calculation of Gross and Net profit to sales ratios of Stell Co Ltd for year 2020 and 2021...4

3. Reason of declining profits and increasing cash flow problems between 2020 and 2021 in

Stell Co. Ltd.................................................................................................................................4

4. Recommendations....................................................................................................................5

Question 2........................................................................................................................................6

1. Calculation of break-even point...............................................................................................6

2. Advantage and disadvantage of activity based costing...........................................................7

Question 3........................................................................................................................................7

1. Calculation of variance............................................................................................................7

2. Possible causes of sales, direct material and direct labour variance........................................8

3. Consequences of selected variance for the business and its objectives...................................9

4. Recommendation.....................................................................................................................9

5. Evaluation of advantage and disadvantage of switching from Incremental based budgeting

to Zero based budgeting.............................................................................................................10

REFERENCES................................................................................................................................1

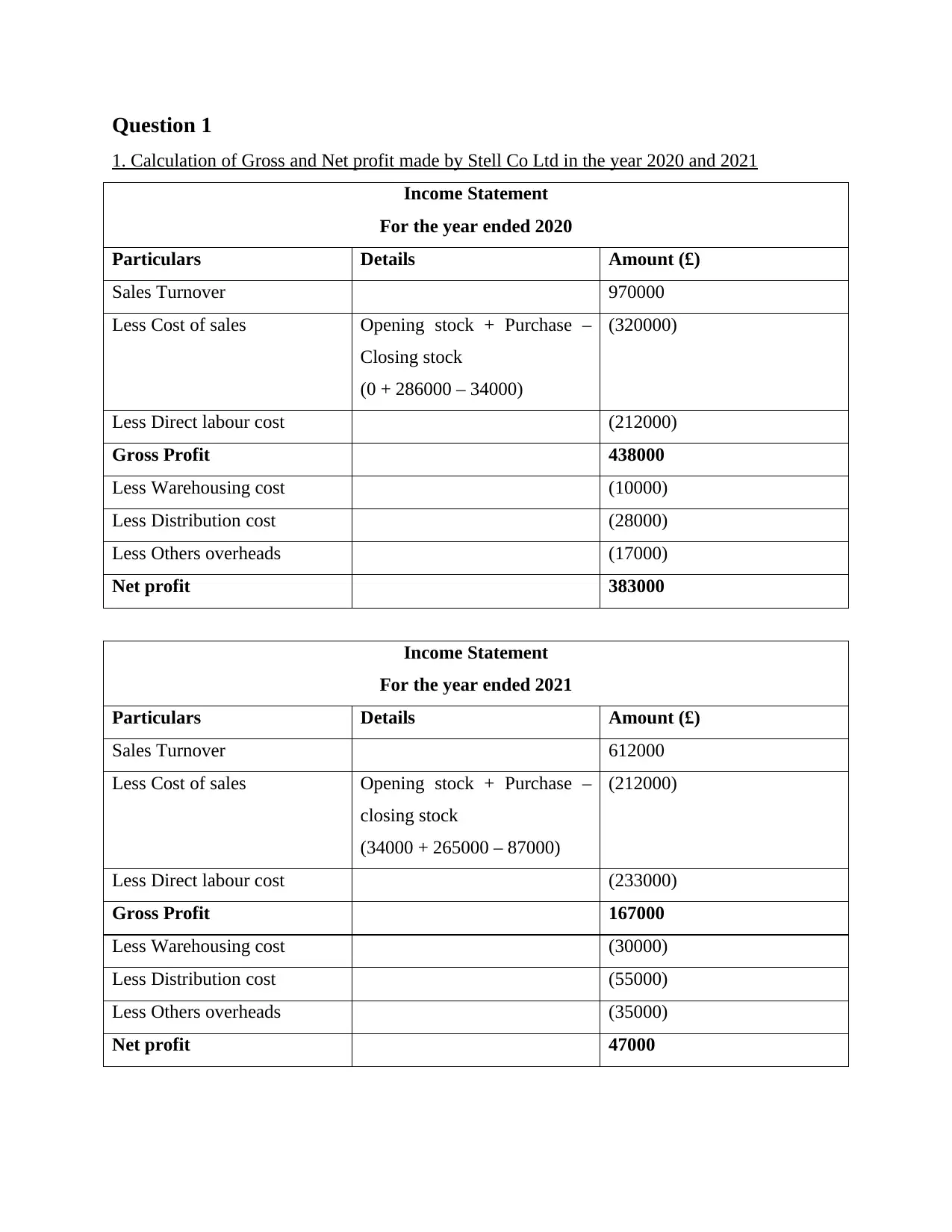

Question 1

1. Calculation of Gross and Net profit made by Stell Co Ltd in the year 2020 and 2021

Income Statement

For the year ended 2020

Particulars Details Amount (£)

Sales Turnover 970000

Less Cost of sales Opening stock + Purchase –

Closing stock

(0 + 286000 – 34000)

(320000)

Less Direct labour cost (212000)

Gross Profit 438000

Less Warehousing cost (10000)

Less Distribution cost (28000)

Less Others overheads (17000)

Net profit 383000

Income Statement

For the year ended 2021

Particulars Details Amount (£)

Sales Turnover 612000

Less Cost of sales Opening stock + Purchase –

closing stock

(34000 + 265000 – 87000)

(212000)

Less Direct labour cost (233000)

Gross Profit 167000

Less Warehousing cost (30000)

Less Distribution cost (55000)

Less Others overheads (35000)

Net profit 47000

1. Calculation of Gross and Net profit made by Stell Co Ltd in the year 2020 and 2021

Income Statement

For the year ended 2020

Particulars Details Amount (£)

Sales Turnover 970000

Less Cost of sales Opening stock + Purchase –

Closing stock

(0 + 286000 – 34000)

(320000)

Less Direct labour cost (212000)

Gross Profit 438000

Less Warehousing cost (10000)

Less Distribution cost (28000)

Less Others overheads (17000)

Net profit 383000

Income Statement

For the year ended 2021

Particulars Details Amount (£)

Sales Turnover 612000

Less Cost of sales Opening stock + Purchase –

closing stock

(34000 + 265000 – 87000)

(212000)

Less Direct labour cost (233000)

Gross Profit 167000

Less Warehousing cost (30000)

Less Distribution cost (55000)

Less Others overheads (35000)

Net profit 47000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2. Calculation of Gross and Net profit to sales ratios of Stell Co Ltd for year 2020 and 2021

Formula of Gross profit to sales ratio:

Gross profit / Net sales * 100

Year 2020 = £438000 / £970000 * 100

= 45.15%

Year 2021 = £167000 / £612000 * 100

= 27.28%

Formula of Net profit to sales ratio: Net profit / Net sales * 100

Net profit / Net sales * 100

Year 2020 = £383000 / £970000 * 100

= 39.48%

Year 2021 = £47000 / £612000 * 100

= 7.67%

Importance of gross and net profit while analysing profitability of Stell Co. Ltd:

Profitability performance state the ability of the company to generate earnings from the

sales revenue after covering all the operating, administration and distribution cost. To analyse the

profitability performance of Stell company, the gross and net profit ratio is significant. It is

because the gross profit margin state the ability of company to reduce the production cost and

increase the sales revenue. While on the other hand, the net profit margin is important for the

company to measure efficiency of Stell to generate earning from sales revenue after bearing all

operating, production, marketing and finance related expenses (Miransyah and Dempo, 2021).

The gross profit helps the company to known whether they capable to manage and control its

production cost or not. While, the net profit helps company to control its overhead cost of the

business. By using this two ratio, the company able to analyse the overall financial health of the

business and identify the area which create loss within the business.

3. Reason of declining profits and increasing cash flow problems between 2020 and 2021 in Stell

Co. Ltd.

The reasons of declining and increasing cash flow problem are as follows:

Formula of Gross profit to sales ratio:

Gross profit / Net sales * 100

Year 2020 = £438000 / £970000 * 100

= 45.15%

Year 2021 = £167000 / £612000 * 100

= 27.28%

Formula of Net profit to sales ratio: Net profit / Net sales * 100

Net profit / Net sales * 100

Year 2020 = £383000 / £970000 * 100

= 39.48%

Year 2021 = £47000 / £612000 * 100

= 7.67%

Importance of gross and net profit while analysing profitability of Stell Co. Ltd:

Profitability performance state the ability of the company to generate earnings from the

sales revenue after covering all the operating, administration and distribution cost. To analyse the

profitability performance of Stell company, the gross and net profit ratio is significant. It is

because the gross profit margin state the ability of company to reduce the production cost and

increase the sales revenue. While on the other hand, the net profit margin is important for the

company to measure efficiency of Stell to generate earning from sales revenue after bearing all

operating, production, marketing and finance related expenses (Miransyah and Dempo, 2021).

The gross profit helps the company to known whether they capable to manage and control its

production cost or not. While, the net profit helps company to control its overhead cost of the

business. By using this two ratio, the company able to analyse the overall financial health of the

business and identify the area which create loss within the business.

3. Reason of declining profits and increasing cash flow problems between 2020 and 2021 in Stell

Co. Ltd.

The reasons of declining and increasing cash flow problem are as follows:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Reduction in sales revenue: On the basis of the above table, it has been identified that

the profitability of company in the year 2021 has reduced to £47000 from £383000 in

year 2020 (Kurniawan, 2022). It is because the sales revenue of company has reduced in

current year which might because of least demand or low selling price.

Increase in direct labour cost: The rise in the direct labour cost of company from year

2020 to 2021 is also one of the reason of declining net and gross profit of Stell Co Ltd.

Increase in administration and distribution overheads: The warehousing, distribution

and other overheads of Stell company in year 2021 is higher as compared to previous

year. On one hand the sales have reduced while cost has increased which ultimately leads

to reduction in profit.

Delay in cash collection from customer: It is identified from the above question that

Stell company collect cash from its customer on 28 days, 33 days and also sometime 90

days. While they need to pay its supplier in full in every 28 days. Thus, the cash problem

in Stell company has arises because customer does not pay outstanding payment to

company on time (Ningsih, 2020).

4. Recommendations

The three strategies recommended to Directors of Stell company for improving financial

position and profit in next financial year are as follows:

Online sales: This is one of the strategy through which company improve its sales,

profitability as well as financial position. As per this strategy, the company should also

start offering its products & services through online mode. Also, they should market and

promote its product on social media platforms to gain large customer base and increase

sales.

Training and development program: This is also one of the strategy which is

recommended to company with the help of which Stell company can reduce its

production and administration cost. The training to employees enhance their productivity,

reduces cost of wastage of resources and lastly increase the profitability as well as

financial performance.

Offering early payment discounts to customer: Early payment discount to customer

attract the customer to buy more products of Stell and make early payment to get

the profitability of company in the year 2021 has reduced to £47000 from £383000 in

year 2020 (Kurniawan, 2022). It is because the sales revenue of company has reduced in

current year which might because of least demand or low selling price.

Increase in direct labour cost: The rise in the direct labour cost of company from year

2020 to 2021 is also one of the reason of declining net and gross profit of Stell Co Ltd.

Increase in administration and distribution overheads: The warehousing, distribution

and other overheads of Stell company in year 2021 is higher as compared to previous

year. On one hand the sales have reduced while cost has increased which ultimately leads

to reduction in profit.

Delay in cash collection from customer: It is identified from the above question that

Stell company collect cash from its customer on 28 days, 33 days and also sometime 90

days. While they need to pay its supplier in full in every 28 days. Thus, the cash problem

in Stell company has arises because customer does not pay outstanding payment to

company on time (Ningsih, 2020).

4. Recommendations

The three strategies recommended to Directors of Stell company for improving financial

position and profit in next financial year are as follows:

Online sales: This is one of the strategy through which company improve its sales,

profitability as well as financial position. As per this strategy, the company should also

start offering its products & services through online mode. Also, they should market and

promote its product on social media platforms to gain large customer base and increase

sales.

Training and development program: This is also one of the strategy which is

recommended to company with the help of which Stell company can reduce its

production and administration cost. The training to employees enhance their productivity,

reduces cost of wastage of resources and lastly increase the profitability as well as

financial performance.

Offering early payment discounts to customer: Early payment discount to customer

attract the customer to buy more products of Stell and make early payment to get

discounts. This is best strategy to resolve the declining cash problem within the

organization.

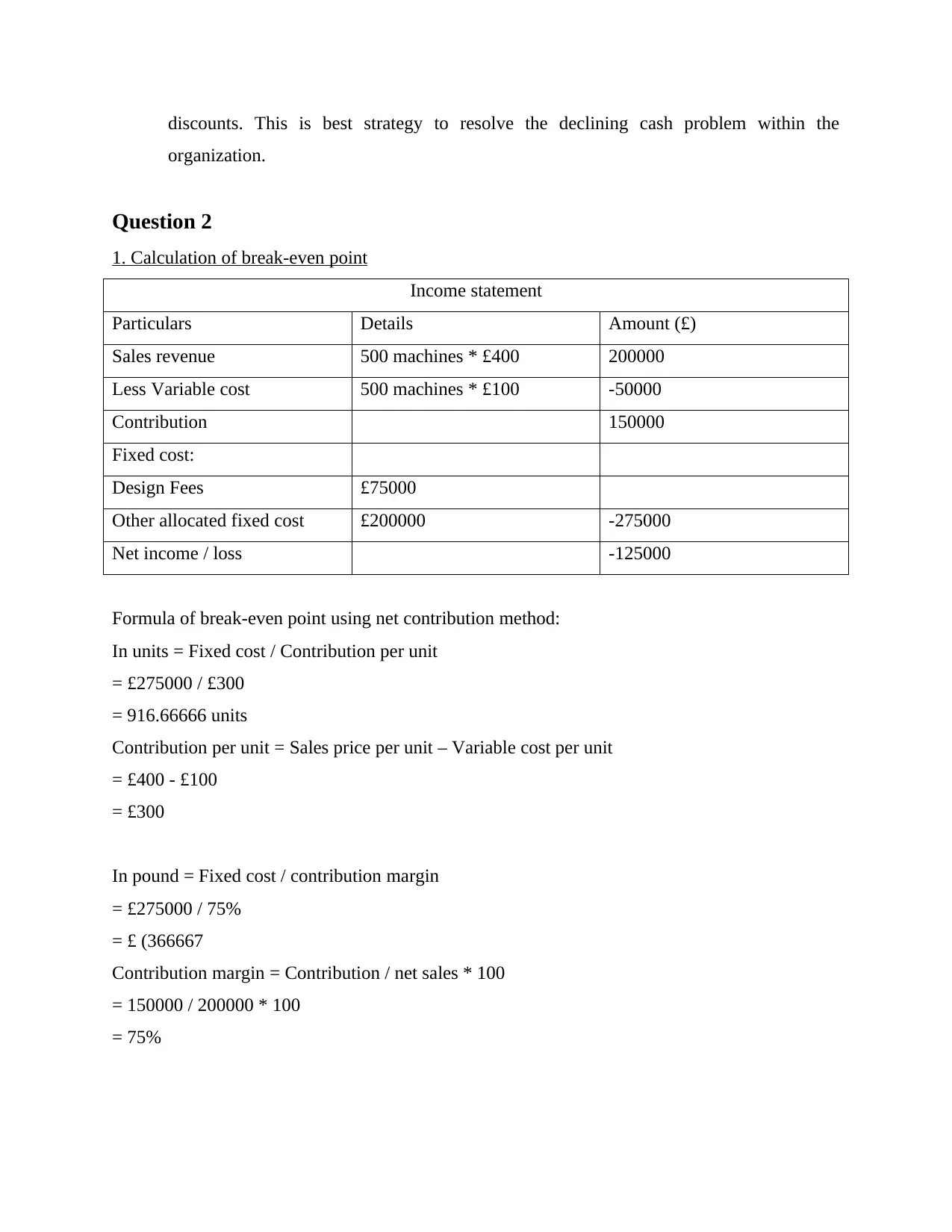

Question 2

1. Calculation of break-even point

Income statement

Particulars Details Amount (£)

Sales revenue 500 machines * £400 200000

Less Variable cost 500 machines * £100 -50000

Contribution 150000

Fixed cost:

Design Fees £75000

Other allocated fixed cost £200000 -275000

Net income / loss -125000

Formula of break-even point using net contribution method:

In units = Fixed cost / Contribution per unit

= £275000 / £300

= 916.66666 units

Contribution per unit = Sales price per unit – Variable cost per unit

= £400 - £100

= £300

In pound = Fixed cost / contribution margin

= £275000 / 75%

= £ (366667

Contribution margin = Contribution / net sales * 100

= 150000 / 200000 * 100

= 75%

organization.

Question 2

1. Calculation of break-even point

Income statement

Particulars Details Amount (£)

Sales revenue 500 machines * £400 200000

Less Variable cost 500 machines * £100 -50000

Contribution 150000

Fixed cost:

Design Fees £75000

Other allocated fixed cost £200000 -275000

Net income / loss -125000

Formula of break-even point using net contribution method:

In units = Fixed cost / Contribution per unit

= £275000 / £300

= 916.66666 units

Contribution per unit = Sales price per unit – Variable cost per unit

= £400 - £100

= £300

In pound = Fixed cost / contribution margin

= £275000 / 75%

= £ (366667

Contribution margin = Contribution / net sales * 100

= 150000 / 200000 * 100

= 75%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The calculation of breakeven point is quite helpful for company to identify the level of

sales at which the company will earn profit. It is because the sales level at break-even point

indicate no profit no loss sales point. For example, as per above calculation, it is identified that

the breakeven sales unit of DK machines is 916 units where the net income of company is zero.

Now, on this basis, the company can further set the sales target which should be higher than 916

machines to earn profit (Kravchyk, Okur and Kovalenko, 2021).

2. Advantage and disadvantage of activity based costing

Advantages:

The activity based costing is helpful in bringing the accuracy and reliability in product

cost through cost and effect relationship.

It is also helpful for identifying the real nature of cost behaviour which further helps in

reducing costs and add value to the product.

It traces overhead costs related to managerial responsibility, customer, departments

besides the products cost (Hafizan and et.al., 2020).

The ABC analysis is best for analysing the use of excess resources within department,

process etc. and further adopting ways to reduce the same.

Disadvantages:

The activity based costing is one of the expensive and complex method of cost allocation.

Selecting drivers of cost allocation is difficult task for the company.

It is not beneficial for smaller business.

The activity based costing make sure that the overheads costs are properly allocated between

each process, department etc. of the company. After proper allocation of cost, the manager of

each department able to identify set profitable price for their products line (Sintha, 2020). This

costing method is best for the larger companies having more than one product line to earn higher

profits.

Question 3

1. Calculation of variance

The three most significant variance and its calculation are as follows:

sales at which the company will earn profit. It is because the sales level at break-even point

indicate no profit no loss sales point. For example, as per above calculation, it is identified that

the breakeven sales unit of DK machines is 916 units where the net income of company is zero.

Now, on this basis, the company can further set the sales target which should be higher than 916

machines to earn profit (Kravchyk, Okur and Kovalenko, 2021).

2. Advantage and disadvantage of activity based costing

Advantages:

The activity based costing is helpful in bringing the accuracy and reliability in product

cost through cost and effect relationship.

It is also helpful for identifying the real nature of cost behaviour which further helps in

reducing costs and add value to the product.

It traces overhead costs related to managerial responsibility, customer, departments

besides the products cost (Hafizan and et.al., 2020).

The ABC analysis is best for analysing the use of excess resources within department,

process etc. and further adopting ways to reduce the same.

Disadvantages:

The activity based costing is one of the expensive and complex method of cost allocation.

Selecting drivers of cost allocation is difficult task for the company.

It is not beneficial for smaller business.

The activity based costing make sure that the overheads costs are properly allocated between

each process, department etc. of the company. After proper allocation of cost, the manager of

each department able to identify set profitable price for their products line (Sintha, 2020). This

costing method is best for the larger companies having more than one product line to earn higher

profits.

Question 3

1. Calculation of variance

The three most significant variance and its calculation are as follows:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Sales variance, direct material variance and direct labour variance are the three most

significant variance. It is because sales, raw material and labour volume, hours and prices get

change over the period of time.

Formula of sales variance = Actual sales – Budgeted sales

= £820000 - £1560000

= -£740000 Unfavourable

Formula of direct raw material variance = Actual raw material cost – Budgeted raw material cost

= £275000 - £400000

= -£125000 Favourable

Formula of direct labour variance = Actual direct labour – Budgeted direct labour

= £240000 - £170000

= £70000 Unfavourable

2. Possible causes of sales, direct material and direct labour variance

Change in competition and sales price: This is one of the possible cause of sales

variance. It is because with the reduction in the sales price of the products and services of

the company the variance between actual and budget sales revenue arises (Schneider and

O'Bryan, 2018). Hence, it means that the increase in level of competition and reduction in

sales price reduces the actual sales of company as compared to budgeted.

Shortage of material: The shortage of material is one of the possible causes of variance

between actual and budgeted raw material cost. It might be arising because of the non-

availability of raw material in market or increase in the price of material by the supplier

side.

Excess staff wages: The gap between the actual number of staff and expected number of

staff is might be one of the possible cause of direct labour variance within the

organization. In case if the wages of the staff are changes over the period of time than in

that situation this leads to direct labour variance. The rise in ideal hours is also a cause of

direct labour variance (Javed and Shafait, 2018).

significant variance. It is because sales, raw material and labour volume, hours and prices get

change over the period of time.

Formula of sales variance = Actual sales – Budgeted sales

= £820000 - £1560000

= -£740000 Unfavourable

Formula of direct raw material variance = Actual raw material cost – Budgeted raw material cost

= £275000 - £400000

= -£125000 Favourable

Formula of direct labour variance = Actual direct labour – Budgeted direct labour

= £240000 - £170000

= £70000 Unfavourable

2. Possible causes of sales, direct material and direct labour variance

Change in competition and sales price: This is one of the possible cause of sales

variance. It is because with the reduction in the sales price of the products and services of

the company the variance between actual and budget sales revenue arises (Schneider and

O'Bryan, 2018). Hence, it means that the increase in level of competition and reduction in

sales price reduces the actual sales of company as compared to budgeted.

Shortage of material: The shortage of material is one of the possible causes of variance

between actual and budgeted raw material cost. It might be arising because of the non-

availability of raw material in market or increase in the price of material by the supplier

side.

Excess staff wages: The gap between the actual number of staff and expected number of

staff is might be one of the possible cause of direct labour variance within the

organization. In case if the wages of the staff are changes over the period of time than in

that situation this leads to direct labour variance. The rise in ideal hours is also a cause of

direct labour variance (Javed and Shafait, 2018).

3. Consequences of selected variance for the business and its objectives

Reduction in net profit of company: The likely consequences of sales variance, direct

material and labour variance on Concorde construction company is that their profit will

start reducing or increasing. For example, in the above case, the direct labour and sales

variance is unfavourable which leads to reduction in net income of company.

High staff turnover: This is one of the major consequence or effect of direct labour

variance on Concorde Construction. The employee expects high wages from its company

and if company provide the same it leads to rise in labour cost. But in case, if company

fails to provide the same, then it would lead to reduction in the loss of employee and

increase in employee turnover.

Decreased brand reputation: Increasing brand reputation of Concorde construction

company is the main objective of the company. But due to the unfavourable variance the

sales of the company decreases which leads to lower profit as well as reputation of brand

in the market.

Costly and lengthy process: Another effect of variance on the business is that it enhances

the further cost of the company. It is because to analyse the variance and adopt the proper

strategy for eliminating variance, Concorde construction company require expert and to

hire them company need to pay extra cost. Also, in case if company avoid to hire expert

and do it by themselves than it would lead to time consuming process (Al-Mahasneh and

et.al., 2018).

4. Recommendation

On the basis of the analysis of the consequence of the selected variance on the business and

its objectives, the following strategies are recommended to Concorde construction company:

Implementation of six sigma model: This is best strategy recommended to company. As

per this strategy, the company is required to adopt and implement six sigma model which

help the company to optimize process to decrease total waste time.

Adopting flex budget rather than static: The flexible budget helps the company to make

changes in their budget depends based on the change in the internal and external factors.

The flexible budget is quite helpful for the company to update its budget and further

access whether the actual revenue or cost is one the track with the flexible or not.

Reduction in net profit of company: The likely consequences of sales variance, direct

material and labour variance on Concorde construction company is that their profit will

start reducing or increasing. For example, in the above case, the direct labour and sales

variance is unfavourable which leads to reduction in net income of company.

High staff turnover: This is one of the major consequence or effect of direct labour

variance on Concorde Construction. The employee expects high wages from its company

and if company provide the same it leads to rise in labour cost. But in case, if company

fails to provide the same, then it would lead to reduction in the loss of employee and

increase in employee turnover.

Decreased brand reputation: Increasing brand reputation of Concorde construction

company is the main objective of the company. But due to the unfavourable variance the

sales of the company decreases which leads to lower profit as well as reputation of brand

in the market.

Costly and lengthy process: Another effect of variance on the business is that it enhances

the further cost of the company. It is because to analyse the variance and adopt the proper

strategy for eliminating variance, Concorde construction company require expert and to

hire them company need to pay extra cost. Also, in case if company avoid to hire expert

and do it by themselves than it would lead to time consuming process (Al-Mahasneh and

et.al., 2018).

4. Recommendation

On the basis of the analysis of the consequence of the selected variance on the business and

its objectives, the following strategies are recommended to Concorde construction company:

Implementation of six sigma model: This is best strategy recommended to company. As

per this strategy, the company is required to adopt and implement six sigma model which

help the company to optimize process to decrease total waste time.

Adopting flex budget rather than static: The flexible budget helps the company to make

changes in their budget depends based on the change in the internal and external factors.

The flexible budget is quite helpful for the company to update its budget and further

access whether the actual revenue or cost is one the track with the flexible or not.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Reward and recognition to its employees: Providing proper rewards and recognition to

employees is significant for the company to encourage and motivate the company. This

also helps the company to encourage employee to do extra work during the peak season.

The extra work helps the company to meet the market demand and enhance the sales of

the company more than they budgeted and expected to sales during particular period

(Soderstrom and Heinze, 2021).

Training to employees: This is another most significant strategy for the company which

indicate that Concorde construction company should provide proper training and

development to its employees. It is because with the help of training the employees able

to complete their targets on time without wasting resources and money in the market.

5. Evaluation of advantage and disadvantage of switching from Incremental based budgeting to

Zero based budgeting

Advantage of Zero based budgeting:

In zero based budgeting managers of company are able to identify and justify all the

operating expenses incur by company in the specific period which is not possible in case

of incremental. The incremental budgeting promotes unnecessary spending.

The zero base uses innovation and technology to check the legacy cost of the company.

But incremental based budgeting is discouraging innovation ideas and growth in the

production.

It also provides incentives to the employees based on their performance review but in

case of incremental budgeting the incentives are lacking (Javed and Shafait, 2018).

Disadvantage of Zero based budgeting:

The disadvantage of zero base budgeting is that it rewards only short term thinking of the

company. It means it does not reward and view the long term investments in order to

increase the revenue of the company (Javed and Shafait, 2018).

This method is resource intensive as it takes more time as well as effort to closely look at

every element of budget. It reviews only new elements and items of budget rather than

analysing previous element as well which is done in incremental based budgeting.

employees is significant for the company to encourage and motivate the company. This

also helps the company to encourage employee to do extra work during the peak season.

The extra work helps the company to meet the market demand and enhance the sales of

the company more than they budgeted and expected to sales during particular period

(Soderstrom and Heinze, 2021).

Training to employees: This is another most significant strategy for the company which

indicate that Concorde construction company should provide proper training and

development to its employees. It is because with the help of training the employees able

to complete their targets on time without wasting resources and money in the market.

5. Evaluation of advantage and disadvantage of switching from Incremental based budgeting to

Zero based budgeting

Advantage of Zero based budgeting:

In zero based budgeting managers of company are able to identify and justify all the

operating expenses incur by company in the specific period which is not possible in case

of incremental. The incremental budgeting promotes unnecessary spending.

The zero base uses innovation and technology to check the legacy cost of the company.

But incremental based budgeting is discouraging innovation ideas and growth in the

production.

It also provides incentives to the employees based on their performance review but in

case of incremental budgeting the incentives are lacking (Javed and Shafait, 2018).

Disadvantage of Zero based budgeting:

The disadvantage of zero base budgeting is that it rewards only short term thinking of the

company. It means it does not reward and view the long term investments in order to

increase the revenue of the company (Javed and Shafait, 2018).

This method is resource intensive as it takes more time as well as effort to closely look at

every element of budget. It reviews only new elements and items of budget rather than

analysing previous element as well which is done in incremental based budgeting.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and journals

Al-Mahasneh, A. J. and et.al., 2018, November. Evolving general regression neural networks

using limited incremental evolution for data-driven modeling of non-linear dynamic

systems. In 2018 IEEE Symposium Series on Computational Intelligence (SSCI) (pp.

335-341). IEEE.

Hafizan, A. M. and et.al., 2020. Design of optimal heat exchanger network with fluctuation

probability using break-even analysis. Energy. 212. p.118583.

Javed, K. and Shafait, F., 2018, December. Revisiting distillation and incremental classifier

learning. In Asian conference on computer vision (pp. 3-17). Springer, Cham.

Kravchyk, K. V., Okur, F. and Kovalenko, M. V., 2021. Break-even analysis of all-solid-state

batteries with Li-garnet solid electrolytes. ACS Energy Letters. 6(6). pp.2202-2207.

Kurniawan, A., 2022. Profitability Ratio Analysis of the Leather Tanning Industry With Loan

Capital Structure Interest System. Indonesian Journal of Food Technology. 1(1). pp.59-

69.

Miransyah, G. G. and Dempo, S. R. S., 2021. Profitability Ratio Analysis at PT. Medikaloka

Hermina, TBK. BINA BANGSA INTERNATIONAL JOURNAL OF BUSINESS AND

MANAGEMENT. 1(1). pp.60-67.

Ningsih, M., 2020. Liquidity and Profitability Ratio Analysis for Measuring The Financial

Performance of PT. Bank Bri Syariah 2012-2019 Period. Journal of Research in

Business, Economics, and Education. 2(4). pp.895-907.

Schneider, K. G. and O'Bryan, C., 2018. Zero-based budgeting in A cutback scenario for A small

academic library. Library Leadership & Management. 32(2).

Sintha, L., 2020. Importance of Break-Even Analysis for the Micro, Small and Medium

Enterprises. International Journal of Research-GRANTHAALAYAH, 8(6).

Soderstrom, S. B. and Heinze, K. L., 2021. From paradoxical thinking to practicing sustainable

business: The role of a business collective organization in supporting

entrepreneurs. Organization & Environment, 34(1), pp.74-98.

1

Books and journals

Al-Mahasneh, A. J. and et.al., 2018, November. Evolving general regression neural networks

using limited incremental evolution for data-driven modeling of non-linear dynamic

systems. In 2018 IEEE Symposium Series on Computational Intelligence (SSCI) (pp.

335-341). IEEE.

Hafizan, A. M. and et.al., 2020. Design of optimal heat exchanger network with fluctuation

probability using break-even analysis. Energy. 212. p.118583.

Javed, K. and Shafait, F., 2018, December. Revisiting distillation and incremental classifier

learning. In Asian conference on computer vision (pp. 3-17). Springer, Cham.

Kravchyk, K. V., Okur, F. and Kovalenko, M. V., 2021. Break-even analysis of all-solid-state

batteries with Li-garnet solid electrolytes. ACS Energy Letters. 6(6). pp.2202-2207.

Kurniawan, A., 2022. Profitability Ratio Analysis of the Leather Tanning Industry With Loan

Capital Structure Interest System. Indonesian Journal of Food Technology. 1(1). pp.59-

69.

Miransyah, G. G. and Dempo, S. R. S., 2021. Profitability Ratio Analysis at PT. Medikaloka

Hermina, TBK. BINA BANGSA INTERNATIONAL JOURNAL OF BUSINESS AND

MANAGEMENT. 1(1). pp.60-67.

Ningsih, M., 2020. Liquidity and Profitability Ratio Analysis for Measuring The Financial

Performance of PT. Bank Bri Syariah 2012-2019 Period. Journal of Research in

Business, Economics, and Education. 2(4). pp.895-907.

Schneider, K. G. and O'Bryan, C., 2018. Zero-based budgeting in A cutback scenario for A small

academic library. Library Leadership & Management. 32(2).

Sintha, L., 2020. Importance of Break-Even Analysis for the Micro, Small and Medium

Enterprises. International Journal of Research-GRANTHAALAYAH, 8(6).

Soderstrom, S. B. and Heinze, K. L., 2021. From paradoxical thinking to practicing sustainable

business: The role of a business collective organization in supporting

entrepreneurs. Organization & Environment, 34(1), pp.74-98.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13