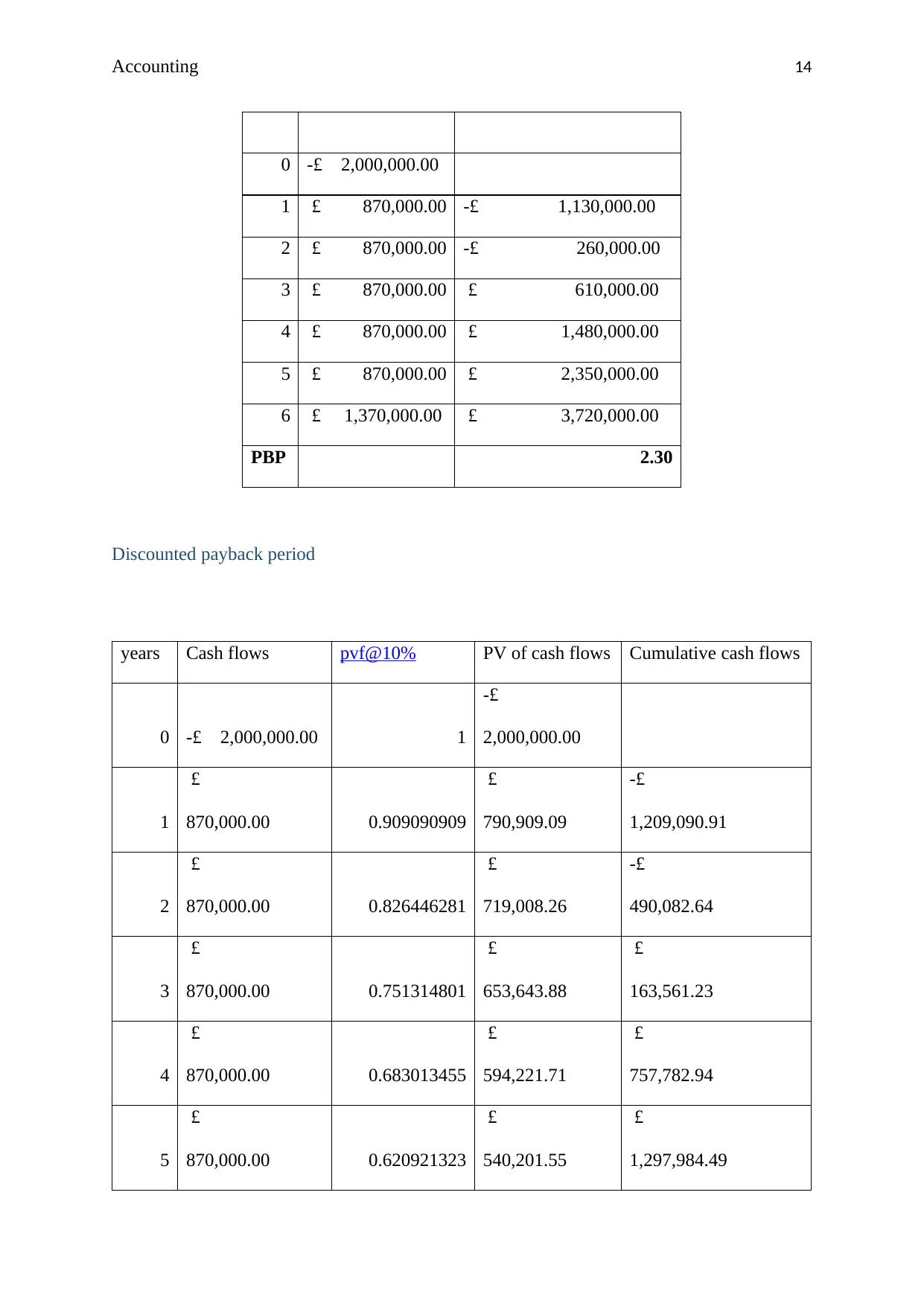

Financial Analysis of Zurich Plc and Johnson Ltd

VerifiedAdded on 2023/06/10

|27

|5445

|80

AI Summary

This report provides a detail financial analysis of Zurich Plc and Johnson Ltd. The report uses ratio analysis to measure company’s financial performance and position over the past years. It also deals with the calculation of capital budgeting techniques required by Johnson Ltd.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

RUNNING HEAD: ACCOUNTING

financial analysis

financial analysis

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Accounting 1

Contents

Introduction...........................................................................................................................................2

Part A - Zurich Plc.................................................................................................................................2

Requirement 1...................................................................................................................................2

Profitability ratios..........................................................................................................................2

Liquidity ratios..............................................................................................................................5

Gearing ratios................................................................................................................................6

Asset utilization ratios...................................................................................................................8

Investor potential ratios...............................................................................................................10

Requirement 2.................................................................................................................................11

Limitation of ratio analysis..........................................................................................................11

Part B - Johnson Ltd............................................................................................................................12

Requirement 1.................................................................................................................................12

Payback period............................................................................................................................13

Discounted payback period..........................................................................................................14

Accounting rate of return.............................................................................................................14

Net present value.........................................................................................................................16

Internal rate of return...................................................................................................................16

Requirement 2.................................................................................................................................18

Evaluation of capital budgeting techniques and their benefits and limitations.............................18

Possible sources of finance..........................................................................................................22

Conclusion...........................................................................................................................................23

References...........................................................................................................................................24

Contents

Introduction...........................................................................................................................................2

Part A - Zurich Plc.................................................................................................................................2

Requirement 1...................................................................................................................................2

Profitability ratios..........................................................................................................................2

Liquidity ratios..............................................................................................................................5

Gearing ratios................................................................................................................................6

Asset utilization ratios...................................................................................................................8

Investor potential ratios...............................................................................................................10

Requirement 2.................................................................................................................................11

Limitation of ratio analysis..........................................................................................................11

Part B - Johnson Ltd............................................................................................................................12

Requirement 1.................................................................................................................................12

Payback period............................................................................................................................13

Discounted payback period..........................................................................................................14

Accounting rate of return.............................................................................................................14

Net present value.........................................................................................................................16

Internal rate of return...................................................................................................................16

Requirement 2.................................................................................................................................18

Evaluation of capital budgeting techniques and their benefits and limitations.............................18

Possible sources of finance..........................................................................................................22

Conclusion...........................................................................................................................................23

References...........................................................................................................................................24

Accounting 2

Introduction

This report provides a detail financial analysis of Zurich Plc. Which is a public limited

company engaged in manufacturing and supplying office equipment. The board of directors

of the company has raised certain concerns after looking at the financial statements of the

company for the past two years. They found the results unsatisfactory and want a report on

the performance of Zurich in aspects of its profitability and liquidity. For this purpose, the

most effective tool of financial management that is ratio analysis is been used to measure

company’s financial performance and position over the past years. Apart from measuring the

financial components the ratio analysis also provides a deep and typical interpretation of the

results. In addition to this the report also states the limitations of the analysis to be carried

out.

The second part of the report deals with the calculation of capital budgeting techniques

required by Johnson Ltd who is a manufacturer of office equipment. The company is looking

forward to make an investment in purchasing a new machine. For this purpose various

investment appraisal techniques are been used like Net present value, payback period,

accounting rate of return and many more. The part also deals with the benefits and limitations

of each technique along with describing the possible and various sources for raising finance

for this investment purpose.

Part A - Zurich Plc.

Requirement 1

Profitability ratios

These are most important ratios used by an investor for evaluating the performance of a

company. They reflect the capability of a company in making sound and sufficient profits

from its operations. Profit is basically a surplus amount left after pay all the expense from the

Introduction

This report provides a detail financial analysis of Zurich Plc. Which is a public limited

company engaged in manufacturing and supplying office equipment. The board of directors

of the company has raised certain concerns after looking at the financial statements of the

company for the past two years. They found the results unsatisfactory and want a report on

the performance of Zurich in aspects of its profitability and liquidity. For this purpose, the

most effective tool of financial management that is ratio analysis is been used to measure

company’s financial performance and position over the past years. Apart from measuring the

financial components the ratio analysis also provides a deep and typical interpretation of the

results. In addition to this the report also states the limitations of the analysis to be carried

out.

The second part of the report deals with the calculation of capital budgeting techniques

required by Johnson Ltd who is a manufacturer of office equipment. The company is looking

forward to make an investment in purchasing a new machine. For this purpose various

investment appraisal techniques are been used like Net present value, payback period,

accounting rate of return and many more. The part also deals with the benefits and limitations

of each technique along with describing the possible and various sources for raising finance

for this investment purpose.

Part A - Zurich Plc.

Requirement 1

Profitability ratios

These are most important ratios used by an investor for evaluating the performance of a

company. They reflect the capability of a company in making sound and sufficient profits

from its operations. Profit is basically a surplus amount left after pay all the expense from the

Accounting 3

revenue generated by the business during a specific financial year. A company has a sound

profitability position only when it can earn high profits which contributes to its growth and

success. However, it is a fact that profits of a company have significant impact on the

financial health of the company (Bragg, 2012). Therefore, in order to evaluate the

profitability of Zurich three main ratios are been calculated as follows:

Gross profit ratio

GPR of a company shows the amount of profit earned or made after paying all of its cost of

goods sold. It is expressed as a percentage of total revenue earned. The ratio is calculated by

dividing the amount of gross profit with the amount of total revenue earned.

Gross profit

margin 2015 2016

Gross profit (A) £ 7,382.00 £ 5,825.00

Total revenue (B) £ 18,920.00 £ 16,243.00

GPR (A/B) 39.02% 35.86%

Analysis

In case of Zurich Plc., the gross profit has reduced from 39.02% in 2015 to 35.86% in 2016.

This was due to the reduction of sales in 2016. However the direct expenses of the company

does not reduces in the same proportion as sales. Though the manufacturing cost of Zurich

has decreased in year 2016 but still the company needs to control it achieve the heights of

profit in near future. Decline in manufacturing costs may lead to higher profits for Zurich.

Net profit ratio

It is also a profitability ratio which determines the quantum of net profit earned after paying

all its operating and non-operating expenses. The amount of net profit is also expressed in

revenue generated by the business during a specific financial year. A company has a sound

profitability position only when it can earn high profits which contributes to its growth and

success. However, it is a fact that profits of a company have significant impact on the

financial health of the company (Bragg, 2012). Therefore, in order to evaluate the

profitability of Zurich three main ratios are been calculated as follows:

Gross profit ratio

GPR of a company shows the amount of profit earned or made after paying all of its cost of

goods sold. It is expressed as a percentage of total revenue earned. The ratio is calculated by

dividing the amount of gross profit with the amount of total revenue earned.

Gross profit

margin 2015 2016

Gross profit (A) £ 7,382.00 £ 5,825.00

Total revenue (B) £ 18,920.00 £ 16,243.00

GPR (A/B) 39.02% 35.86%

Analysis

In case of Zurich Plc., the gross profit has reduced from 39.02% in 2015 to 35.86% in 2016.

This was due to the reduction of sales in 2016. However the direct expenses of the company

does not reduces in the same proportion as sales. Though the manufacturing cost of Zurich

has decreased in year 2016 but still the company needs to control it achieve the heights of

profit in near future. Decline in manufacturing costs may lead to higher profits for Zurich.

Net profit ratio

It is also a profitability ratio which determines the quantum of net profit earned after paying

all its operating and non-operating expenses. The amount of net profit is also expressed in

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Accounting 4

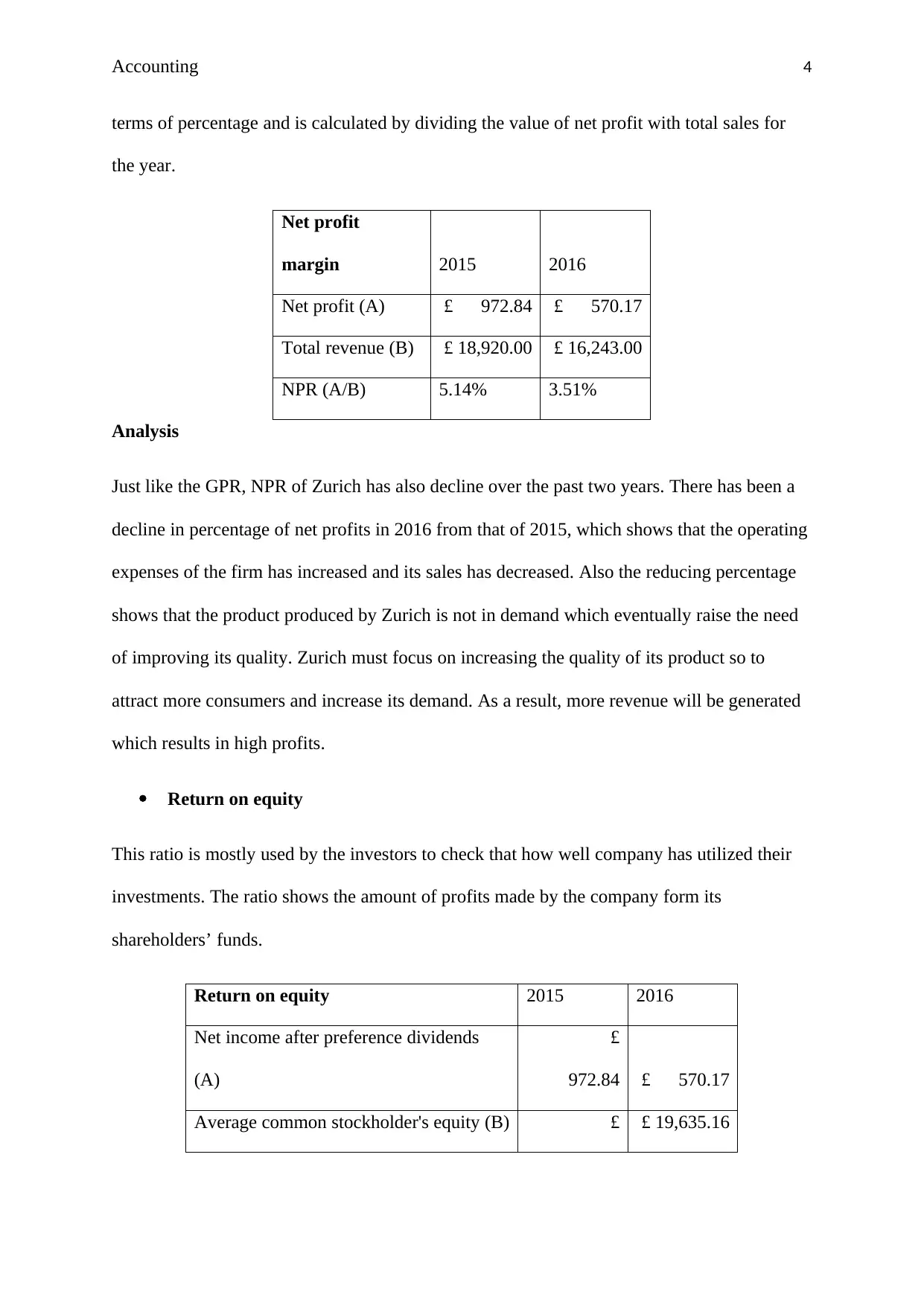

terms of percentage and is calculated by dividing the value of net profit with total sales for

the year.

Net profit

margin 2015 2016

Net profit (A) £ 972.84 £ 570.17

Total revenue (B) £ 18,920.00 £ 16,243.00

NPR (A/B) 5.14% 3.51%

Analysis

Just like the GPR, NPR of Zurich has also decline over the past two years. There has been a

decline in percentage of net profits in 2016 from that of 2015, which shows that the operating

expenses of the firm has increased and its sales has decreased. Also the reducing percentage

shows that the product produced by Zurich is not in demand which eventually raise the need

of improving its quality. Zurich must focus on increasing the quality of its product so to

attract more consumers and increase its demand. As a result, more revenue will be generated

which results in high profits.

Return on equity

This ratio is mostly used by the investors to check that how well company has utilized their

investments. The ratio shows the amount of profits made by the company form its

shareholders’ funds.

Return on equity 2015 2016

Net income after preference dividends

(A)

£

972.84 £ 570.17

Average common stockholder's equity (B) £ £ 19,635.16

terms of percentage and is calculated by dividing the value of net profit with total sales for

the year.

Net profit

margin 2015 2016

Net profit (A) £ 972.84 £ 570.17

Total revenue (B) £ 18,920.00 £ 16,243.00

NPR (A/B) 5.14% 3.51%

Analysis

Just like the GPR, NPR of Zurich has also decline over the past two years. There has been a

decline in percentage of net profits in 2016 from that of 2015, which shows that the operating

expenses of the firm has increased and its sales has decreased. Also the reducing percentage

shows that the product produced by Zurich is not in demand which eventually raise the need

of improving its quality. Zurich must focus on increasing the quality of its product so to

attract more consumers and increase its demand. As a result, more revenue will be generated

which results in high profits.

Return on equity

This ratio is mostly used by the investors to check that how well company has utilized their

investments. The ratio shows the amount of profits made by the company form its

shareholders’ funds.

Return on equity 2015 2016

Net income after preference dividends

(A)

£

972.84 £ 570.17

Average common stockholder's equity (B) £ £ 19,635.16

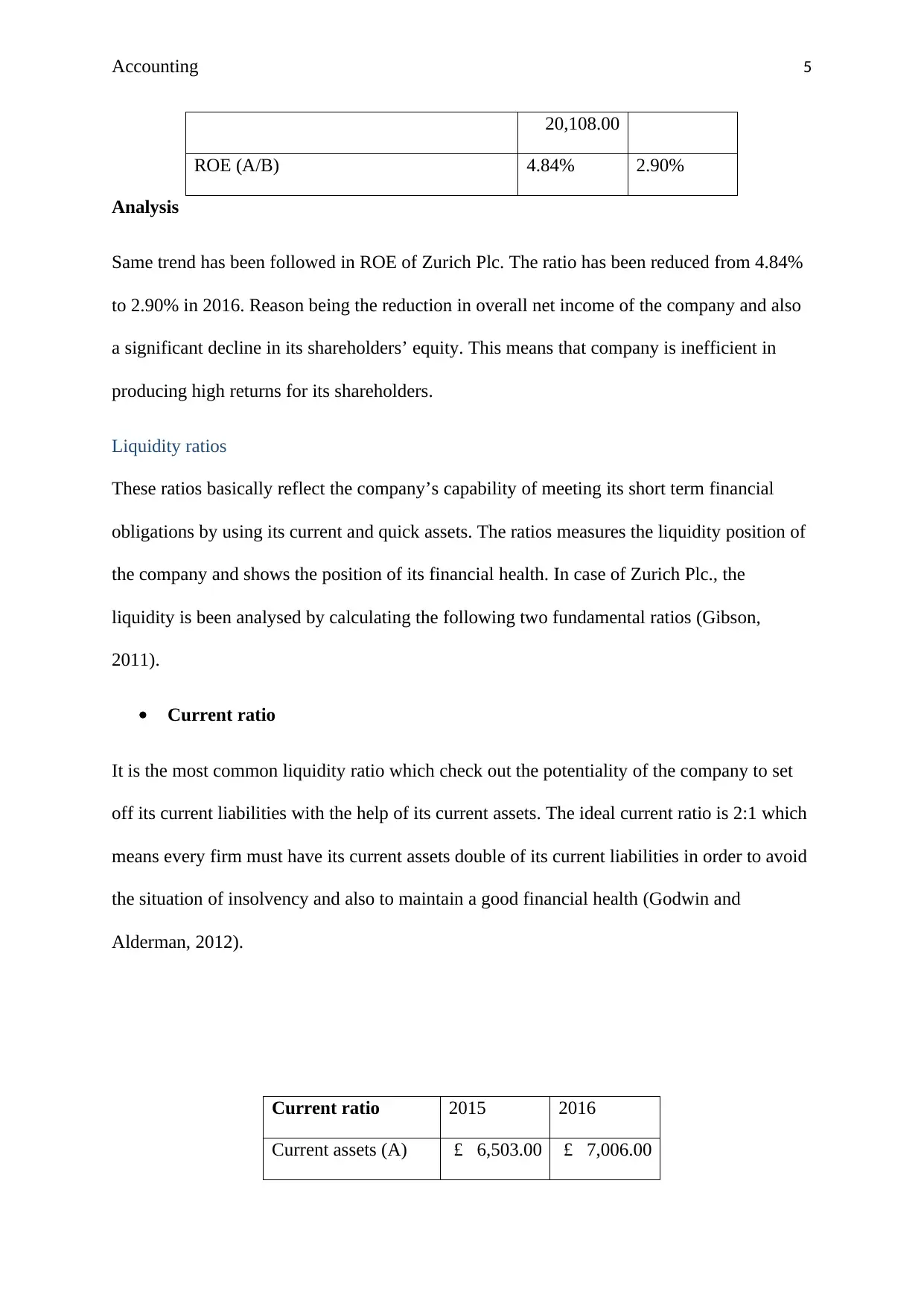

Accounting 5

20,108.00

ROE (A/B) 4.84% 2.90%

Analysis

Same trend has been followed in ROE of Zurich Plc. The ratio has been reduced from 4.84%

to 2.90% in 2016. Reason being the reduction in overall net income of the company and also

a significant decline in its shareholders’ equity. This means that company is inefficient in

producing high returns for its shareholders.

Liquidity ratios

These ratios basically reflect the company’s capability of meeting its short term financial

obligations by using its current and quick assets. The ratios measures the liquidity position of

the company and shows the position of its financial health. In case of Zurich Plc., the

liquidity is been analysed by calculating the following two fundamental ratios (Gibson,

2011).

Current ratio

It is the most common liquidity ratio which check out the potentiality of the company to set

off its current liabilities with the help of its current assets. The ideal current ratio is 2:1 which

means every firm must have its current assets double of its current liabilities in order to avoid

the situation of insolvency and also to maintain a good financial health (Godwin and

Alderman, 2012).

Current ratio 2015 2016

Current assets (A) £ 6,503.00 £ 7,006.00

20,108.00

ROE (A/B) 4.84% 2.90%

Analysis

Same trend has been followed in ROE of Zurich Plc. The ratio has been reduced from 4.84%

to 2.90% in 2016. Reason being the reduction in overall net income of the company and also

a significant decline in its shareholders’ equity. This means that company is inefficient in

producing high returns for its shareholders.

Liquidity ratios

These ratios basically reflect the company’s capability of meeting its short term financial

obligations by using its current and quick assets. The ratios measures the liquidity position of

the company and shows the position of its financial health. In case of Zurich Plc., the

liquidity is been analysed by calculating the following two fundamental ratios (Gibson,

2011).

Current ratio

It is the most common liquidity ratio which check out the potentiality of the company to set

off its current liabilities with the help of its current assets. The ideal current ratio is 2:1 which

means every firm must have its current assets double of its current liabilities in order to avoid

the situation of insolvency and also to maintain a good financial health (Godwin and

Alderman, 2012).

Current ratio 2015 2016

Current assets (A) £ 6,503.00 £ 7,006.00

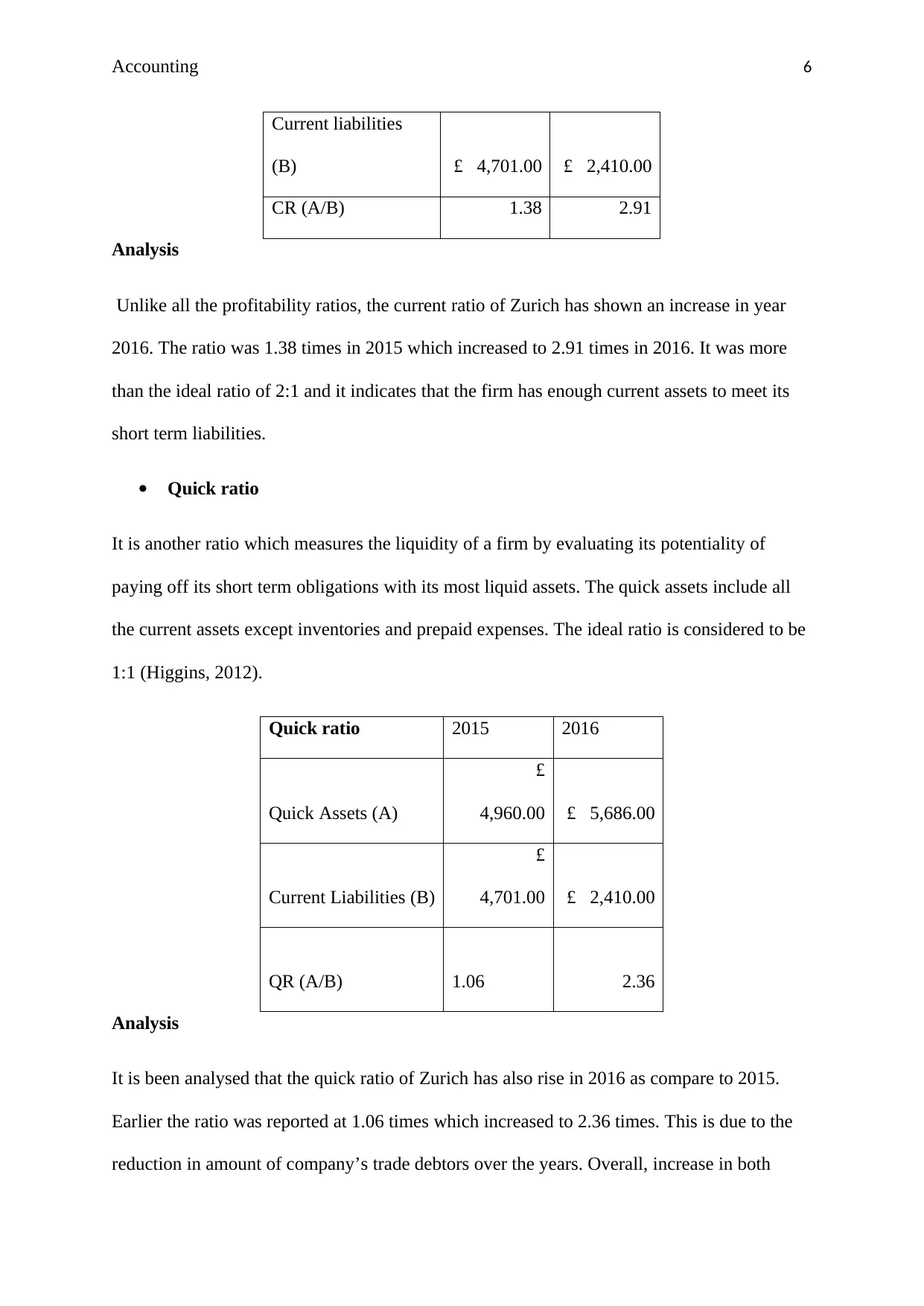

Accounting 6

Current liabilities

(B) £ 4,701.00 £ 2,410.00

CR (A/B) 1.38 2.91

Analysis

Unlike all the profitability ratios, the current ratio of Zurich has shown an increase in year

2016. The ratio was 1.38 times in 2015 which increased to 2.91 times in 2016. It was more

than the ideal ratio of 2:1 and it indicates that the firm has enough current assets to meet its

short term liabilities.

Quick ratio

It is another ratio which measures the liquidity of a firm by evaluating its potentiality of

paying off its short term obligations with its most liquid assets. The quick assets include all

the current assets except inventories and prepaid expenses. The ideal ratio is considered to be

1:1 (Higgins, 2012).

Quick ratio 2015 2016

Quick Assets (A)

£

4,960.00 £ 5,686.00

Current Liabilities (B)

£

4,701.00 £ 2,410.00

QR (A/B) 1.06 2.36

Analysis

It is been analysed that the quick ratio of Zurich has also rise in 2016 as compare to 2015.

Earlier the ratio was reported at 1.06 times which increased to 2.36 times. This is due to the

reduction in amount of company’s trade debtors over the years. Overall, increase in both

Current liabilities

(B) £ 4,701.00 £ 2,410.00

CR (A/B) 1.38 2.91

Analysis

Unlike all the profitability ratios, the current ratio of Zurich has shown an increase in year

2016. The ratio was 1.38 times in 2015 which increased to 2.91 times in 2016. It was more

than the ideal ratio of 2:1 and it indicates that the firm has enough current assets to meet its

short term liabilities.

Quick ratio

It is another ratio which measures the liquidity of a firm by evaluating its potentiality of

paying off its short term obligations with its most liquid assets. The quick assets include all

the current assets except inventories and prepaid expenses. The ideal ratio is considered to be

1:1 (Higgins, 2012).

Quick ratio 2015 2016

Quick Assets (A)

£

4,960.00 £ 5,686.00

Current Liabilities (B)

£

4,701.00 £ 2,410.00

QR (A/B) 1.06 2.36

Analysis

It is been analysed that the quick ratio of Zurich has also rise in 2016 as compare to 2015.

Earlier the ratio was reported at 1.06 times which increased to 2.36 times. This is due to the

reduction in amount of company’s trade debtors over the years. Overall, increase in both

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting 7

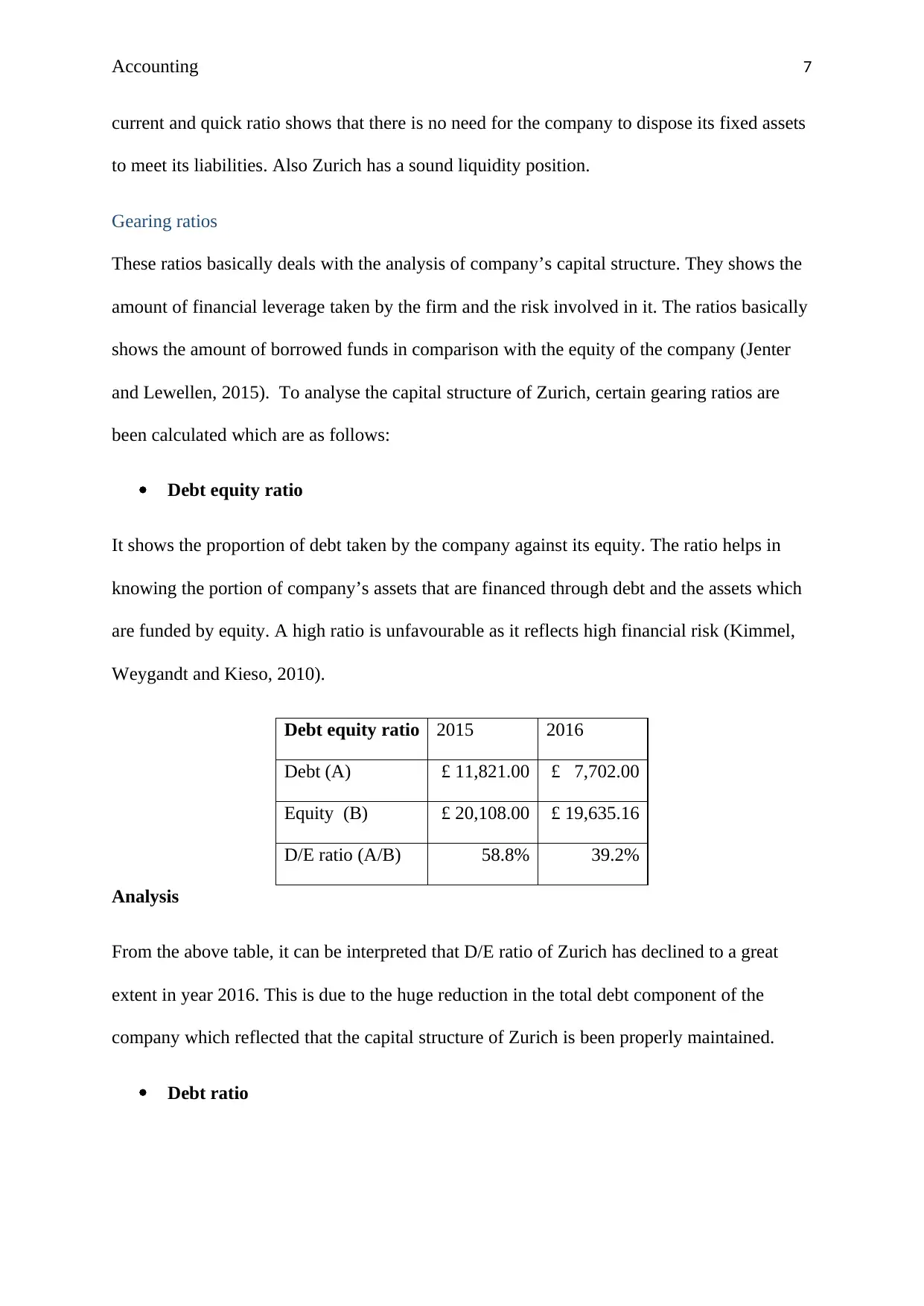

current and quick ratio shows that there is no need for the company to dispose its fixed assets

to meet its liabilities. Also Zurich has a sound liquidity position.

Gearing ratios

These ratios basically deals with the analysis of company’s capital structure. They shows the

amount of financial leverage taken by the firm and the risk involved in it. The ratios basically

shows the amount of borrowed funds in comparison with the equity of the company (Jenter

and Lewellen, 2015). To analyse the capital structure of Zurich, certain gearing ratios are

been calculated which are as follows:

Debt equity ratio

It shows the proportion of debt taken by the company against its equity. The ratio helps in

knowing the portion of company’s assets that are financed through debt and the assets which

are funded by equity. A high ratio is unfavourable as it reflects high financial risk (Kimmel,

Weygandt and Kieso, 2010).

Debt equity ratio 2015 2016

Debt (A) £ 11,821.00 £ 7,702.00

Equity (B) £ 20,108.00 £ 19,635.16

D/E ratio (A/B) 58.8% 39.2%

Analysis

From the above table, it can be interpreted that D/E ratio of Zurich has declined to a great

extent in year 2016. This is due to the huge reduction in the total debt component of the

company which reflected that the capital structure of Zurich is been properly maintained.

Debt ratio

current and quick ratio shows that there is no need for the company to dispose its fixed assets

to meet its liabilities. Also Zurich has a sound liquidity position.

Gearing ratios

These ratios basically deals with the analysis of company’s capital structure. They shows the

amount of financial leverage taken by the firm and the risk involved in it. The ratios basically

shows the amount of borrowed funds in comparison with the equity of the company (Jenter

and Lewellen, 2015). To analyse the capital structure of Zurich, certain gearing ratios are

been calculated which are as follows:

Debt equity ratio

It shows the proportion of debt taken by the company against its equity. The ratio helps in

knowing the portion of company’s assets that are financed through debt and the assets which

are funded by equity. A high ratio is unfavourable as it reflects high financial risk (Kimmel,

Weygandt and Kieso, 2010).

Debt equity ratio 2015 2016

Debt (A) £ 11,821.00 £ 7,702.00

Equity (B) £ 20,108.00 £ 19,635.16

D/E ratio (A/B) 58.8% 39.2%

Analysis

From the above table, it can be interpreted that D/E ratio of Zurich has declined to a great

extent in year 2016. This is due to the huge reduction in the total debt component of the

company which reflected that the capital structure of Zurich is been properly maintained.

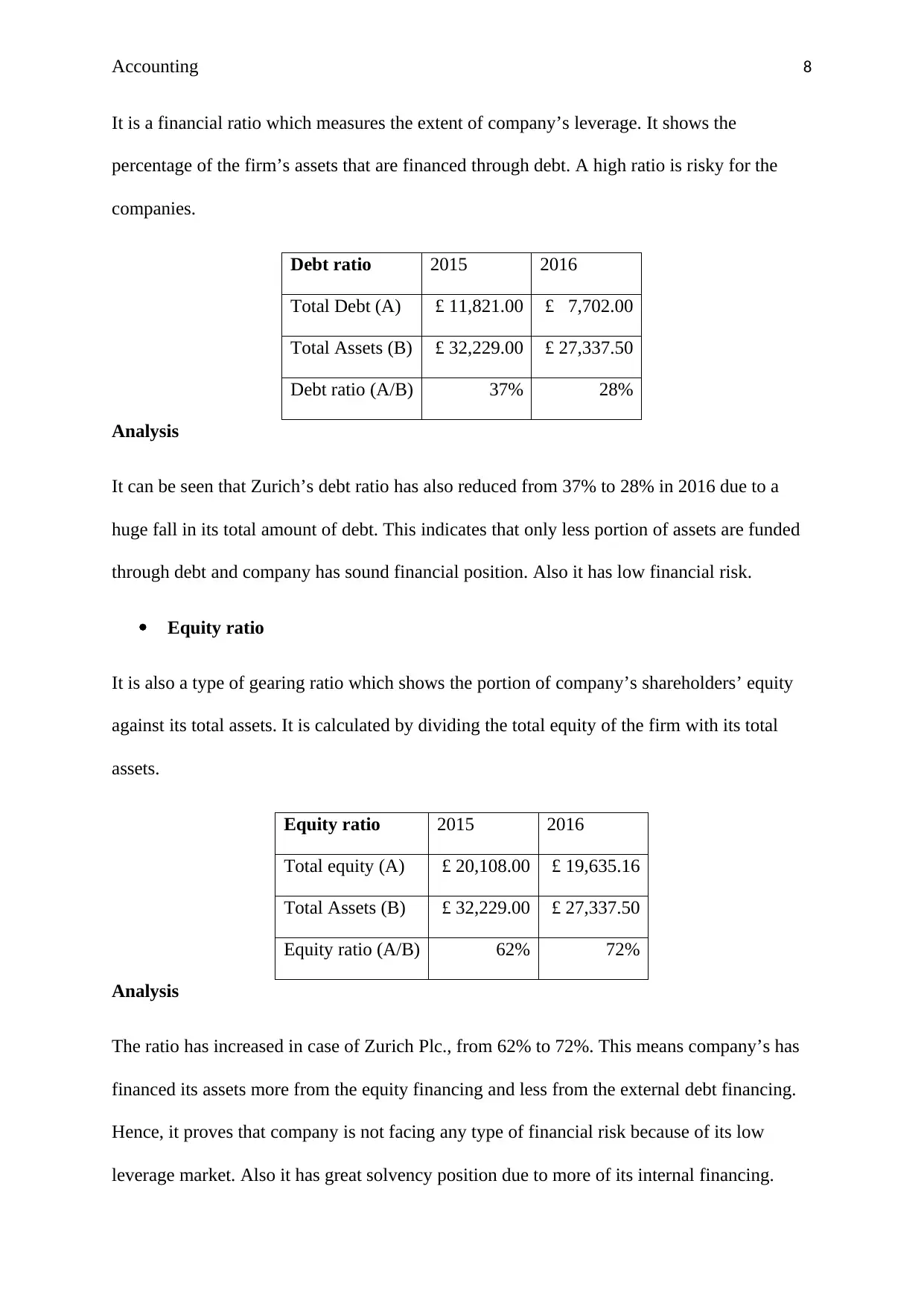

Debt ratio

Accounting 8

It is a financial ratio which measures the extent of company’s leverage. It shows the

percentage of the firm’s assets that are financed through debt. A high ratio is risky for the

companies.

Debt ratio 2015 2016

Total Debt (A) £ 11,821.00 £ 7,702.00

Total Assets (B) £ 32,229.00 £ 27,337.50

Debt ratio (A/B) 37% 28%

Analysis

It can be seen that Zurich’s debt ratio has also reduced from 37% to 28% in 2016 due to a

huge fall in its total amount of debt. This indicates that only less portion of assets are funded

through debt and company has sound financial position. Also it has low financial risk.

Equity ratio

It is also a type of gearing ratio which shows the portion of company’s shareholders’ equity

against its total assets. It is calculated by dividing the total equity of the firm with its total

assets.

Equity ratio 2015 2016

Total equity (A) £ 20,108.00 £ 19,635.16

Total Assets (B) £ 32,229.00 £ 27,337.50

Equity ratio (A/B) 62% 72%

Analysis

The ratio has increased in case of Zurich Plc., from 62% to 72%. This means company’s has

financed its assets more from the equity financing and less from the external debt financing.

Hence, it proves that company is not facing any type of financial risk because of its low

leverage market. Also it has great solvency position due to more of its internal financing.

It is a financial ratio which measures the extent of company’s leverage. It shows the

percentage of the firm’s assets that are financed through debt. A high ratio is risky for the

companies.

Debt ratio 2015 2016

Total Debt (A) £ 11,821.00 £ 7,702.00

Total Assets (B) £ 32,229.00 £ 27,337.50

Debt ratio (A/B) 37% 28%

Analysis

It can be seen that Zurich’s debt ratio has also reduced from 37% to 28% in 2016 due to a

huge fall in its total amount of debt. This indicates that only less portion of assets are funded

through debt and company has sound financial position. Also it has low financial risk.

Equity ratio

It is also a type of gearing ratio which shows the portion of company’s shareholders’ equity

against its total assets. It is calculated by dividing the total equity of the firm with its total

assets.

Equity ratio 2015 2016

Total equity (A) £ 20,108.00 £ 19,635.16

Total Assets (B) £ 32,229.00 £ 27,337.50

Equity ratio (A/B) 62% 72%

Analysis

The ratio has increased in case of Zurich Plc., from 62% to 72%. This means company’s has

financed its assets more from the equity financing and less from the external debt financing.

Hence, it proves that company is not facing any type of financial risk because of its low

leverage market. Also it has great solvency position due to more of its internal financing.

Accounting 9

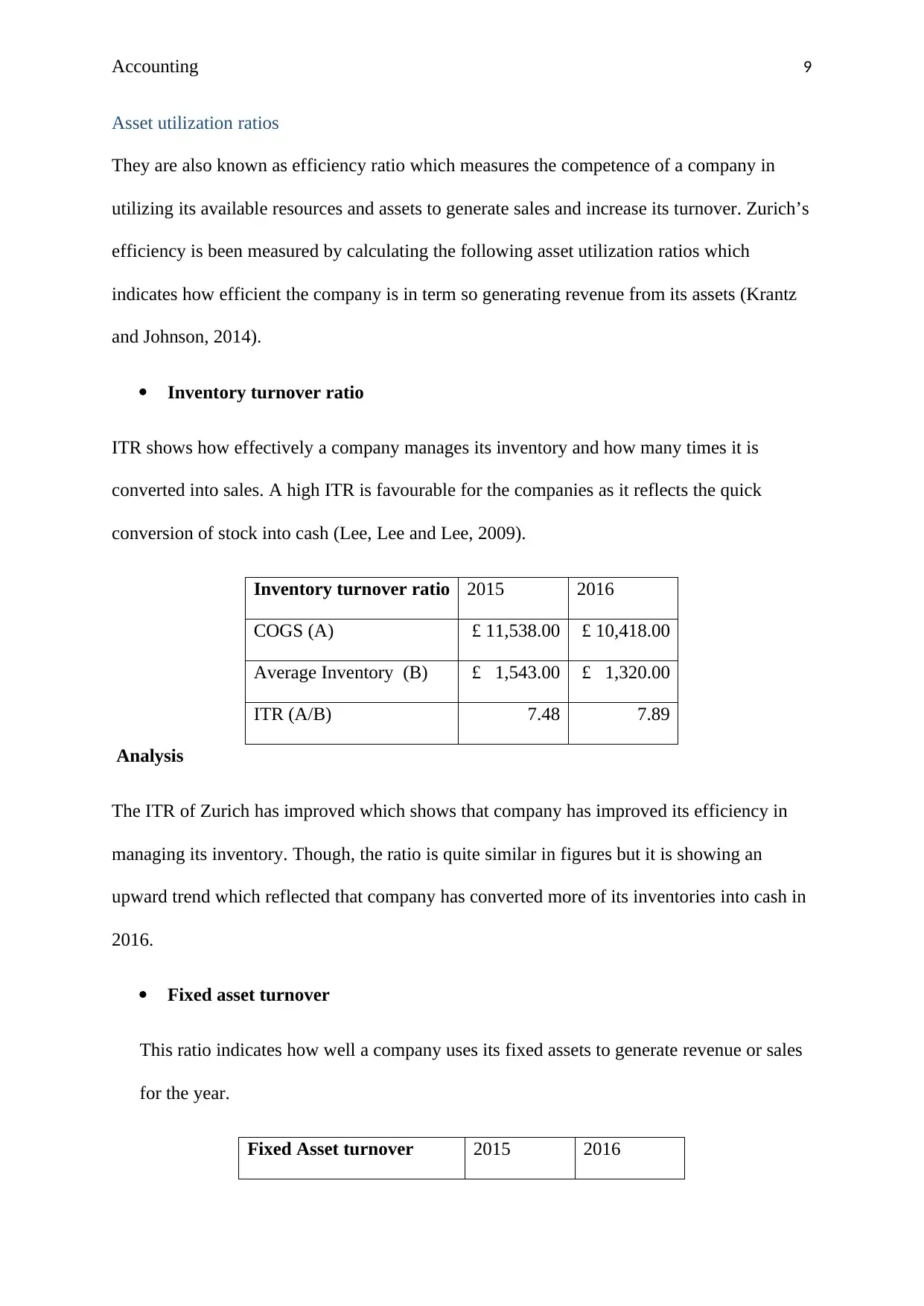

Asset utilization ratios

They are also known as efficiency ratio which measures the competence of a company in

utilizing its available resources and assets to generate sales and increase its turnover. Zurich’s

efficiency is been measured by calculating the following asset utilization ratios which

indicates how efficient the company is in term so generating revenue from its assets (Krantz

and Johnson, 2014).

Inventory turnover ratio

ITR shows how effectively a company manages its inventory and how many times it is

converted into sales. A high ITR is favourable for the companies as it reflects the quick

conversion of stock into cash (Lee, Lee and Lee, 2009).

Inventory turnover ratio 2015 2016

COGS (A) £ 11,538.00 £ 10,418.00

Average Inventory (B) £ 1,543.00 £ 1,320.00

ITR (A/B) 7.48 7.89

Analysis

The ITR of Zurich has improved which shows that company has improved its efficiency in

managing its inventory. Though, the ratio is quite similar in figures but it is showing an

upward trend which reflected that company has converted more of its inventories into cash in

2016.

Fixed asset turnover

This ratio indicates how well a company uses its fixed assets to generate revenue or sales

for the year.

Fixed Asset turnover 2015 2016

Asset utilization ratios

They are also known as efficiency ratio which measures the competence of a company in

utilizing its available resources and assets to generate sales and increase its turnover. Zurich’s

efficiency is been measured by calculating the following asset utilization ratios which

indicates how efficient the company is in term so generating revenue from its assets (Krantz

and Johnson, 2014).

Inventory turnover ratio

ITR shows how effectively a company manages its inventory and how many times it is

converted into sales. A high ITR is favourable for the companies as it reflects the quick

conversion of stock into cash (Lee, Lee and Lee, 2009).

Inventory turnover ratio 2015 2016

COGS (A) £ 11,538.00 £ 10,418.00

Average Inventory (B) £ 1,543.00 £ 1,320.00

ITR (A/B) 7.48 7.89

Analysis

The ITR of Zurich has improved which shows that company has improved its efficiency in

managing its inventory. Though, the ratio is quite similar in figures but it is showing an

upward trend which reflected that company has converted more of its inventories into cash in

2016.

Fixed asset turnover

This ratio indicates how well a company uses its fixed assets to generate revenue or sales

for the year.

Fixed Asset turnover 2015 2016

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Accounting 10

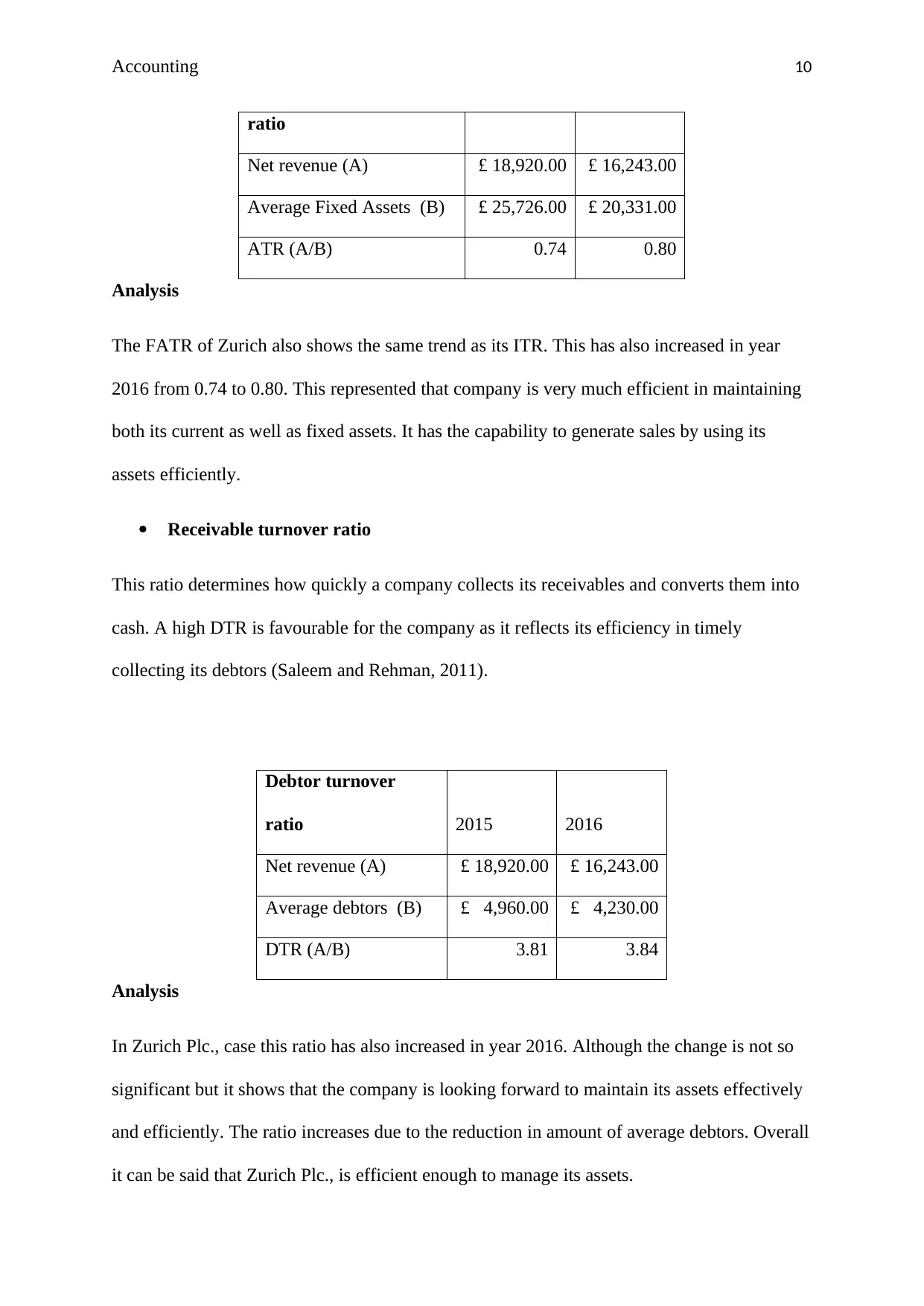

ratio

Net revenue (A) £ 18,920.00 £ 16,243.00

Average Fixed Assets (B) £ 25,726.00 £ 20,331.00

ATR (A/B) 0.74 0.80

Analysis

The FATR of Zurich also shows the same trend as its ITR. This has also increased in year

2016 from 0.74 to 0.80. This represented that company is very much efficient in maintaining

both its current as well as fixed assets. It has the capability to generate sales by using its

assets efficiently.

Receivable turnover ratio

This ratio determines how quickly a company collects its receivables and converts them into

cash. A high DTR is favourable for the company as it reflects its efficiency in timely

collecting its debtors (Saleem and Rehman, 2011).

Debtor turnover

ratio 2015 2016

Net revenue (A) £ 18,920.00 £ 16,243.00

Average debtors (B) £ 4,960.00 £ 4,230.00

DTR (A/B) 3.81 3.84

Analysis

In Zurich Plc., case this ratio has also increased in year 2016. Although the change is not so

significant but it shows that the company is looking forward to maintain its assets effectively

and efficiently. The ratio increases due to the reduction in amount of average debtors. Overall

it can be said that Zurich Plc., is efficient enough to manage its assets.

ratio

Net revenue (A) £ 18,920.00 £ 16,243.00

Average Fixed Assets (B) £ 25,726.00 £ 20,331.00

ATR (A/B) 0.74 0.80

Analysis

The FATR of Zurich also shows the same trend as its ITR. This has also increased in year

2016 from 0.74 to 0.80. This represented that company is very much efficient in maintaining

both its current as well as fixed assets. It has the capability to generate sales by using its

assets efficiently.

Receivable turnover ratio

This ratio determines how quickly a company collects its receivables and converts them into

cash. A high DTR is favourable for the company as it reflects its efficiency in timely

collecting its debtors (Saleem and Rehman, 2011).

Debtor turnover

ratio 2015 2016

Net revenue (A) £ 18,920.00 £ 16,243.00

Average debtors (B) £ 4,960.00 £ 4,230.00

DTR (A/B) 3.81 3.84

Analysis

In Zurich Plc., case this ratio has also increased in year 2016. Although the change is not so

significant but it shows that the company is looking forward to maintain its assets effectively

and efficiently. The ratio increases due to the reduction in amount of average debtors. Overall

it can be said that Zurich Plc., is efficient enough to manage its assets.

Accounting 11

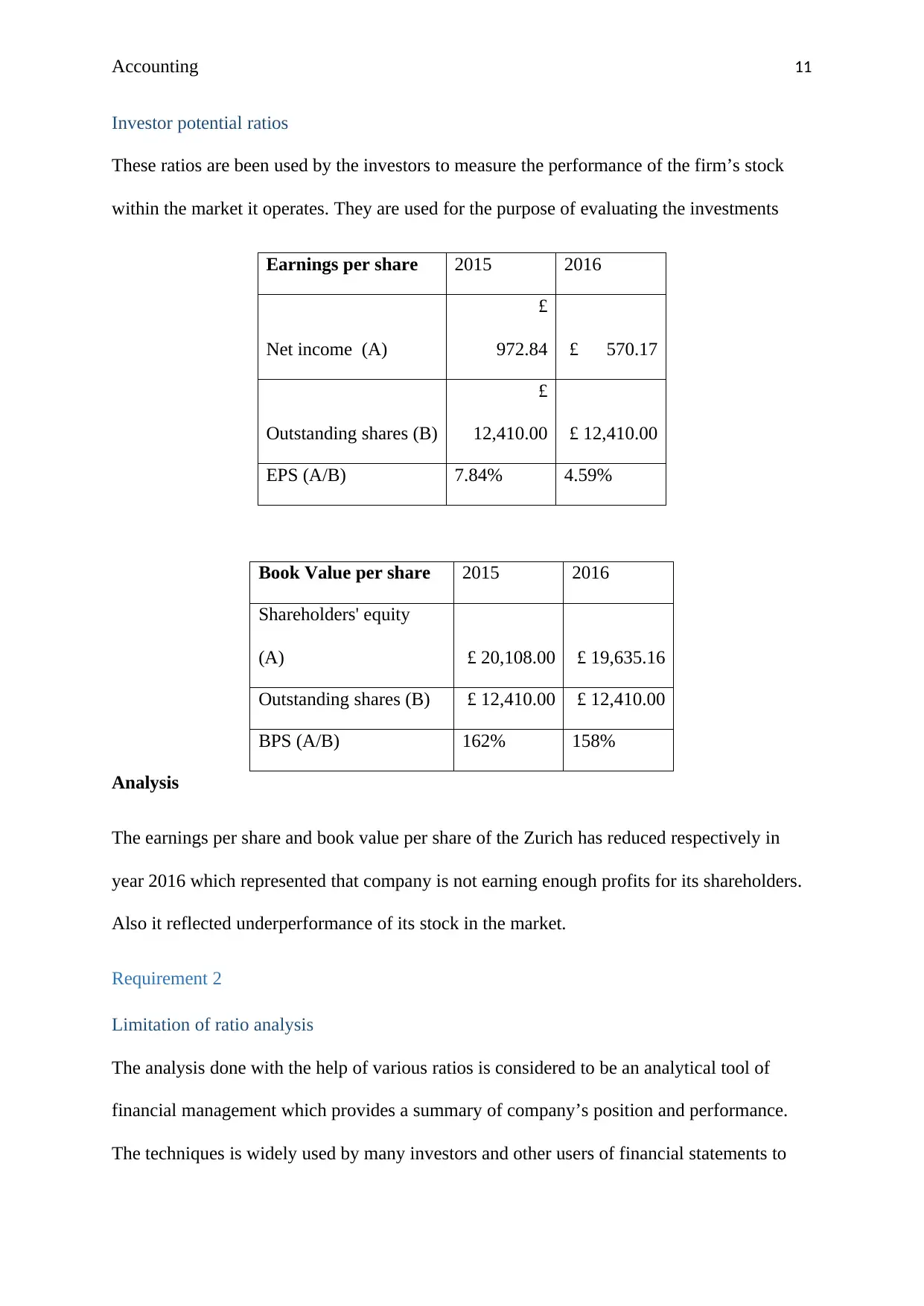

Investor potential ratios

These ratios are been used by the investors to measure the performance of the firm’s stock

within the market it operates. They are used for the purpose of evaluating the investments

Earnings per share 2015 2016

Net income (A)

£

972.84 £ 570.17

Outstanding shares (B)

£

12,410.00 £ 12,410.00

EPS (A/B) 7.84% 4.59%

Book Value per share 2015 2016

Shareholders' equity

(A) £ 20,108.00 £ 19,635.16

Outstanding shares (B) £ 12,410.00 £ 12,410.00

BPS (A/B) 162% 158%

Analysis

The earnings per share and book value per share of the Zurich has reduced respectively in

year 2016 which represented that company is not earning enough profits for its shareholders.

Also it reflected underperformance of its stock in the market.

Requirement 2

Limitation of ratio analysis

The analysis done with the help of various ratios is considered to be an analytical tool of

financial management which provides a summary of company’s position and performance.

The techniques is widely used by many investors and other users of financial statements to

Investor potential ratios

These ratios are been used by the investors to measure the performance of the firm’s stock

within the market it operates. They are used for the purpose of evaluating the investments

Earnings per share 2015 2016

Net income (A)

£

972.84 £ 570.17

Outstanding shares (B)

£

12,410.00 £ 12,410.00

EPS (A/B) 7.84% 4.59%

Book Value per share 2015 2016

Shareholders' equity

(A) £ 20,108.00 £ 19,635.16

Outstanding shares (B) £ 12,410.00 £ 12,410.00

BPS (A/B) 162% 158%

Analysis

The earnings per share and book value per share of the Zurich has reduced respectively in

year 2016 which represented that company is not earning enough profits for its shareholders.

Also it reflected underperformance of its stock in the market.

Requirement 2

Limitation of ratio analysis

The analysis done with the help of various ratios is considered to be an analytical tool of

financial management which provides a summary of company’s position and performance.

The techniques is widely used by many investors and other users of financial statements to

Accounting 12

analyse the annual and financial reports of the companies. However, despite of several

benefits ratio analysis has its own limitations which are as follows:

Based on historical data

The data used in ratio analysis is derived from the past events and transaction of the business.

However, it is not always true that past trends of the business will continue in its future also.

Apart from financial there are various factors which has a significant impact on company’s

performance such as environmental, social and many more. Ratio analysis does not consider

such impacts and changes on the business (Tracy, 2012).

Inflation

It is one of the factor which has a high impact on the components of financial statements. If

inflation has impacted one financial year, then it became difficult to compare the information

of other period. In that case, the technique of ratio analysis fails (Vogel, 2014).

Different strategies

It is not always possible that the companies follow the same strategies and policies o that

their financial data can be comparable. Sometimes, firms change their strategies as per their

requirement and modify their policy which makes it difficult to compare their data and

performance. In such case ratio analysis cannot compare the firms having different strategies.

Quantitative and not qualitative

Ratio analysis only take into account the quantitative analysis and ignores the qualitative

factors which also impact the financial health of the organization. It focuses only on the

financial results of the company and ignore the data related to sustainability, corporate social

responsibility and many more (Warren and Jones, 2018).

analyse the annual and financial reports of the companies. However, despite of several

benefits ratio analysis has its own limitations which are as follows:

Based on historical data

The data used in ratio analysis is derived from the past events and transaction of the business.

However, it is not always true that past trends of the business will continue in its future also.

Apart from financial there are various factors which has a significant impact on company’s

performance such as environmental, social and many more. Ratio analysis does not consider

such impacts and changes on the business (Tracy, 2012).

Inflation

It is one of the factor which has a high impact on the components of financial statements. If

inflation has impacted one financial year, then it became difficult to compare the information

of other period. In that case, the technique of ratio analysis fails (Vogel, 2014).

Different strategies

It is not always possible that the companies follow the same strategies and policies o that

their financial data can be comparable. Sometimes, firms change their strategies as per their

requirement and modify their policy which makes it difficult to compare their data and

performance. In such case ratio analysis cannot compare the firms having different strategies.

Quantitative and not qualitative

Ratio analysis only take into account the quantitative analysis and ignores the qualitative

factors which also impact the financial health of the organization. It focuses only on the

financial results of the company and ignore the data related to sustainability, corporate social

responsibility and many more (Warren and Jones, 2018).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting 13

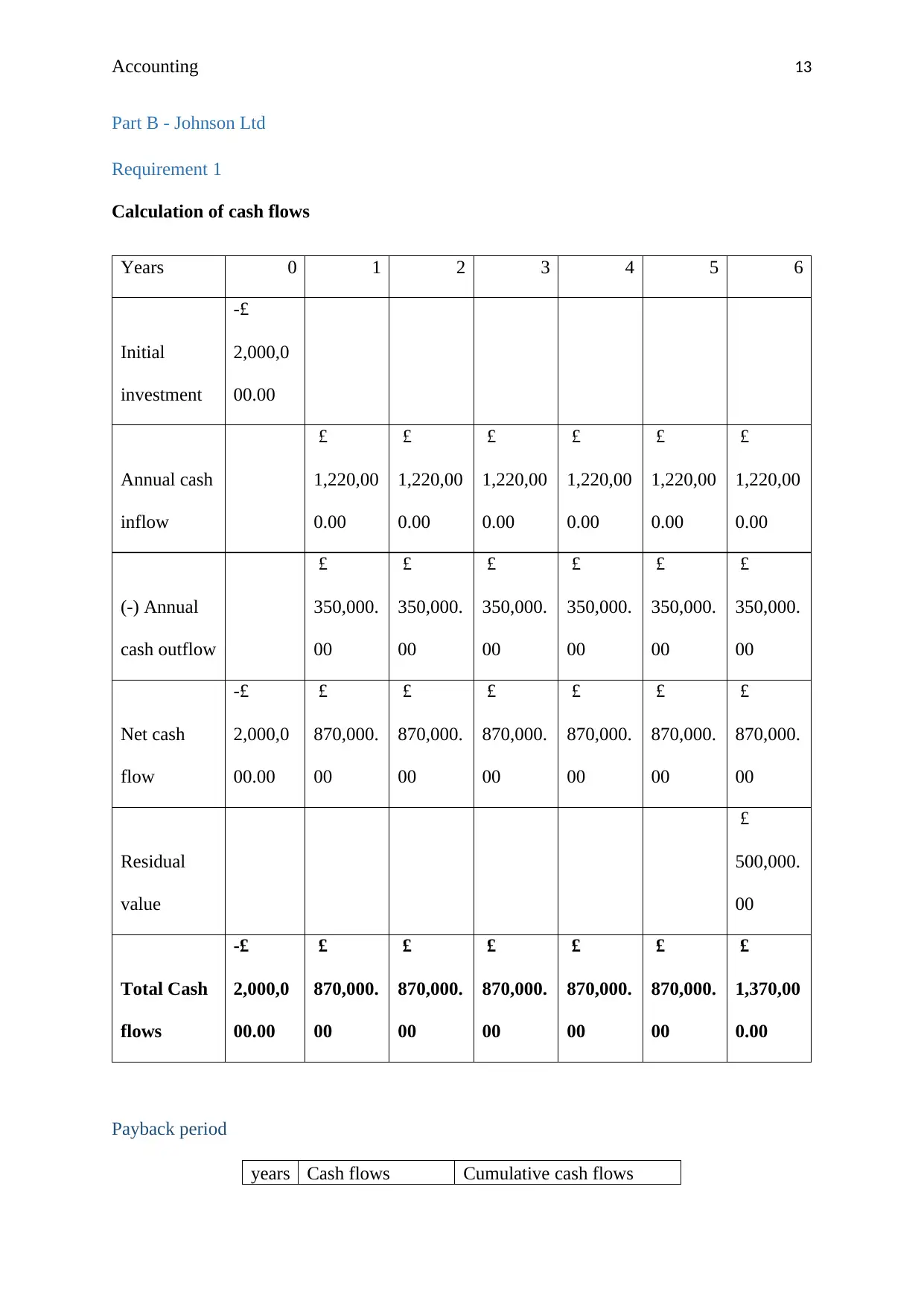

Part B - Johnson Ltd

Requirement 1

Calculation of cash flows

Years 0 1 2 3 4 5 6

Initial

investment

-£

2,000,0

00.00

Annual cash

inflow

£

1,220,00

0.00

£

1,220,00

0.00

£

1,220,00

0.00

£

1,220,00

0.00

£

1,220,00

0.00

£

1,220,00

0.00

(-) Annual

cash outflow

£

350,000.

00

£

350,000.

00

£

350,000.

00

£

350,000.

00

£

350,000.

00

£

350,000.

00

Net cash

flow

-£

2,000,0

00.00

£

870,000.

00

£

870,000.

00

£

870,000.

00

£

870,000.

00

£

870,000.

00

£

870,000.

00

Residual

value

£

500,000.

00

Total Cash

flows

-£

2,000,0

00.00

£

870,000.

00

£

870,000.

00

£

870,000.

00

£

870,000.

00

£

870,000.

00

£

1,370,00

0.00

Payback period

years Cash flows Cumulative cash flows

Part B - Johnson Ltd

Requirement 1

Calculation of cash flows

Years 0 1 2 3 4 5 6

Initial

investment

-£

2,000,0

00.00

Annual cash

inflow

£

1,220,00

0.00

£

1,220,00

0.00

£

1,220,00

0.00

£

1,220,00

0.00

£

1,220,00

0.00

£

1,220,00

0.00

(-) Annual

cash outflow

£

350,000.

00

£

350,000.

00

£

350,000.

00

£

350,000.

00

£

350,000.

00

£

350,000.

00

Net cash

flow

-£

2,000,0

00.00

£

870,000.

00

£

870,000.

00

£

870,000.

00

£

870,000.

00

£

870,000.

00

£

870,000.

00

Residual

value

£

500,000.

00

Total Cash

flows

-£

2,000,0

00.00

£

870,000.

00

£

870,000.

00

£

870,000.

00

£

870,000.

00

£

870,000.

00

£

1,370,00

0.00

Payback period

years Cash flows Cumulative cash flows

Accounting 14

0 -£ 2,000,000.00

1 £ 870,000.00 -£ 1,130,000.00

2 £ 870,000.00 -£ 260,000.00

3 £ 870,000.00 £ 610,000.00

4 £ 870,000.00 £ 1,480,000.00

5 £ 870,000.00 £ 2,350,000.00

6 £ 1,370,000.00 £ 3,720,000.00

PBP 2.30

Discounted payback period

years Cash flows pvf@10% PV of cash flows Cumulative cash flows

0 -£ 2,000,000.00 1

-£

2,000,000.00

1

£

870,000.00 0.909090909

£

790,909.09

-£

1,209,090.91

2

£

870,000.00 0.826446281

£

719,008.26

-£

490,082.64

3

£

870,000.00 0.751314801

£

653,643.88

£

163,561.23

4

£

870,000.00 0.683013455

£

594,221.71

£

757,782.94

5

£

870,000.00 0.620921323

£

540,201.55

£

1,297,984.49

0 -£ 2,000,000.00

1 £ 870,000.00 -£ 1,130,000.00

2 £ 870,000.00 -£ 260,000.00

3 £ 870,000.00 £ 610,000.00

4 £ 870,000.00 £ 1,480,000.00

5 £ 870,000.00 £ 2,350,000.00

6 £ 1,370,000.00 £ 3,720,000.00

PBP 2.30

Discounted payback period

years Cash flows pvf@10% PV of cash flows Cumulative cash flows

0 -£ 2,000,000.00 1

-£

2,000,000.00

1

£

870,000.00 0.909090909

£

790,909.09

-£

1,209,090.91

2

£

870,000.00 0.826446281

£

719,008.26

-£

490,082.64

3

£

870,000.00 0.751314801

£

653,643.88

£

163,561.23

4

£

870,000.00 0.683013455

£

594,221.71

£

757,782.94

5

£

870,000.00 0.620921323

£

540,201.55

£

1,297,984.49

Accounting 15

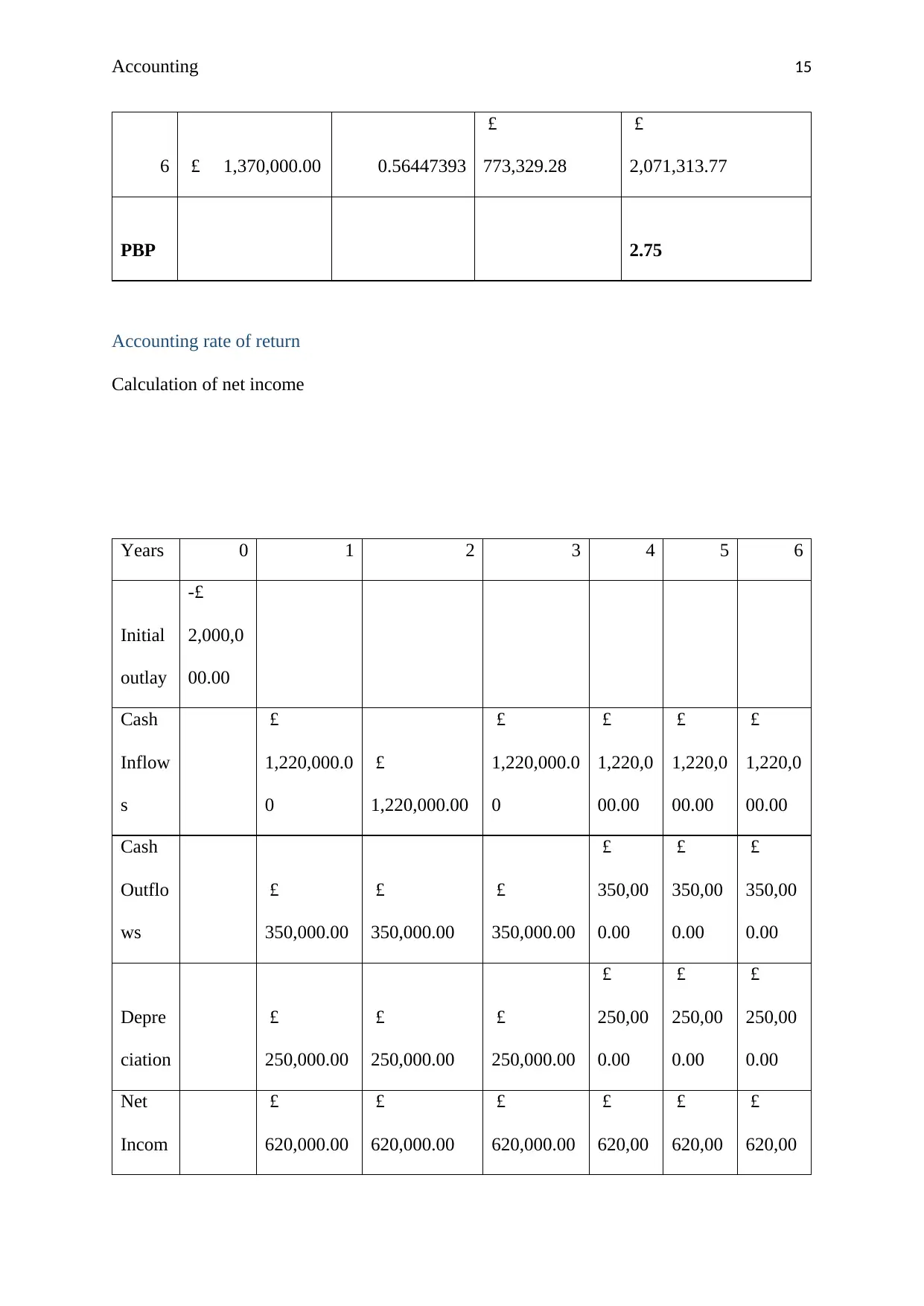

6 £ 1,370,000.00 0.56447393

£

773,329.28

£

2,071,313.77

PBP 2.75

Accounting rate of return

Calculation of net income

Years 0 1 2 3 4 5 6

Initial

outlay

-£

2,000,0

00.00

Cash

Inflow

s

£

1,220,000.0

0

£

1,220,000.00

£

1,220,000.0

0

£

1,220,0

00.00

£

1,220,0

00.00

£

1,220,0

00.00

Cash

Outflo

ws

£

350,000.00

£

350,000.00

£

350,000.00

£

350,00

0.00

£

350,00

0.00

£

350,00

0.00

Depre

ciation

£

250,000.00

£

250,000.00

£

250,000.00

£

250,00

0.00

£

250,00

0.00

£

250,00

0.00

Net

Incom

£

620,000.00

£

620,000.00

£

620,000.00

£

620,00

£

620,00

£

620,00

6 £ 1,370,000.00 0.56447393

£

773,329.28

£

2,071,313.77

PBP 2.75

Accounting rate of return

Calculation of net income

Years 0 1 2 3 4 5 6

Initial

outlay

-£

2,000,0

00.00

Cash

Inflow

s

£

1,220,000.0

0

£

1,220,000.00

£

1,220,000.0

0

£

1,220,0

00.00

£

1,220,0

00.00

£

1,220,0

00.00

Cash

Outflo

ws

£

350,000.00

£

350,000.00

£

350,000.00

£

350,00

0.00

£

350,00

0.00

£

350,00

0.00

Depre

ciation

£

250,000.00

£

250,000.00

£

250,000.00

£

250,00

0.00

£

250,00

0.00

£

250,00

0.00

Net

Incom

£

620,000.00

£

620,000.00

£

620,000.00

£

620,00

£

620,00

£

620,00

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Accounting 16

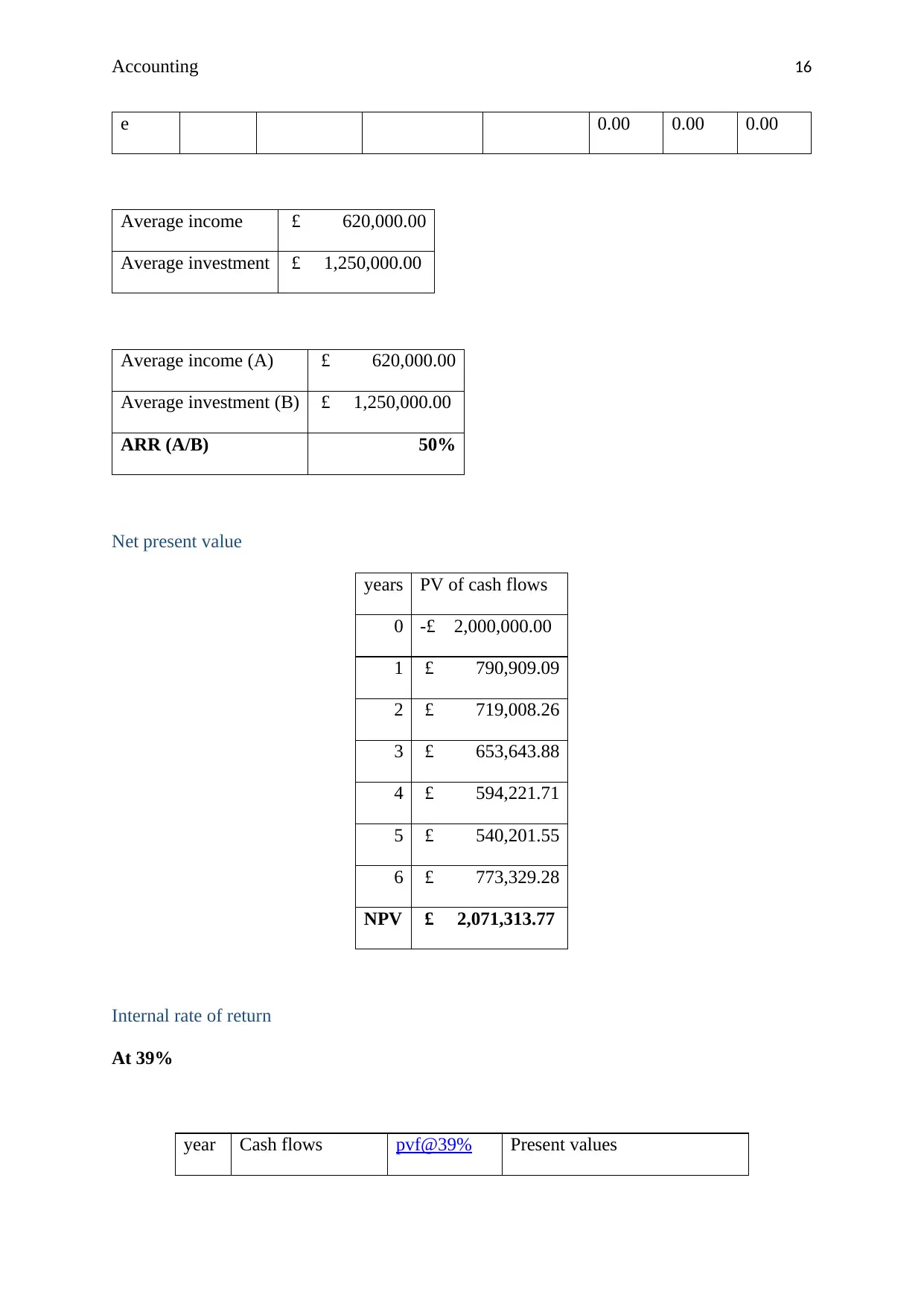

e 0.00 0.00 0.00

Average income £ 620,000.00

Average investment £ 1,250,000.00

Average income (A) £ 620,000.00

Average investment (B) £ 1,250,000.00

ARR (A/B) 50%

Net present value

years PV of cash flows

0 -£ 2,000,000.00

1 £ 790,909.09

2 £ 719,008.26

3 £ 653,643.88

4 £ 594,221.71

5 £ 540,201.55

6 £ 773,329.28

NPV £ 2,071,313.77

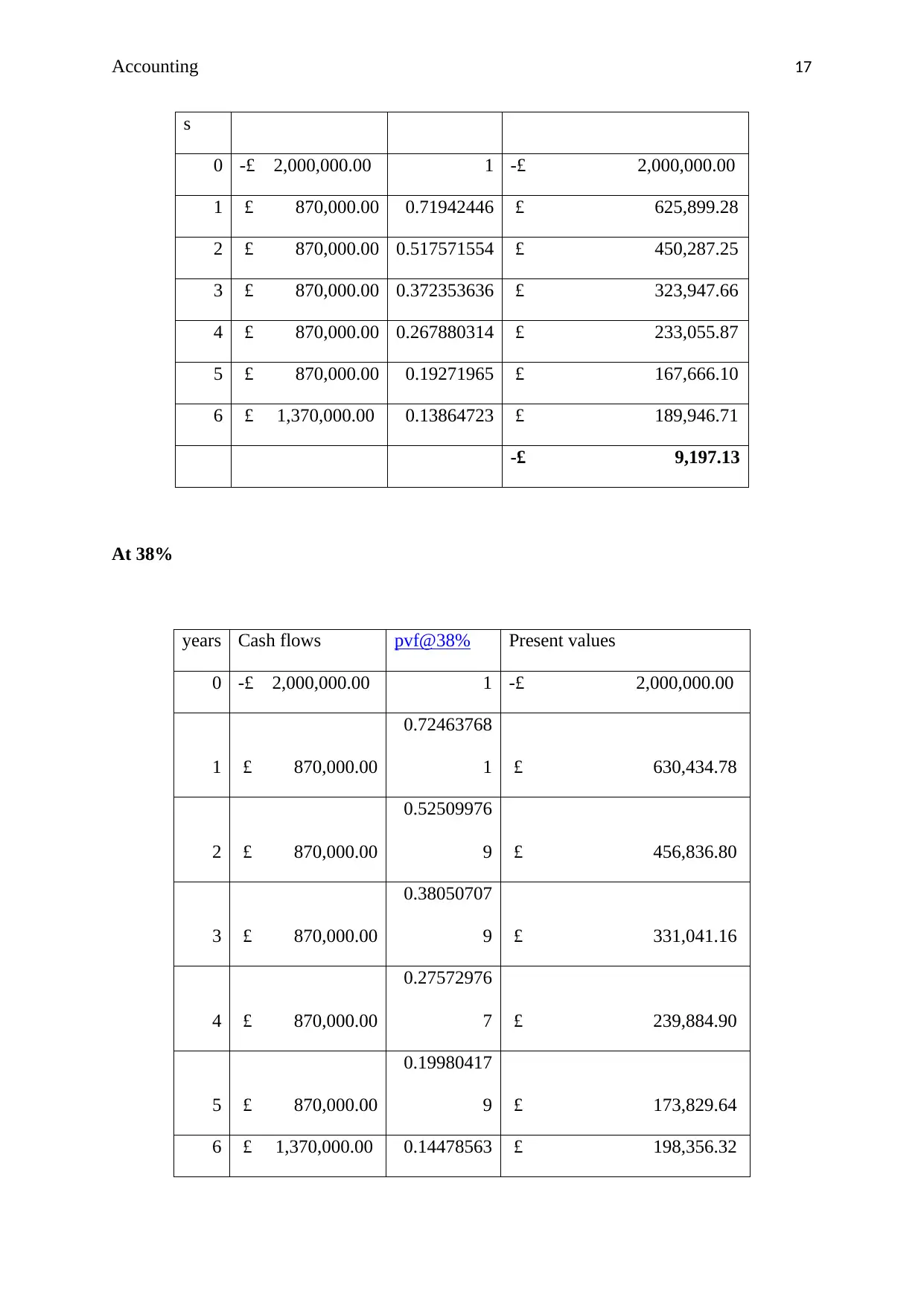

Internal rate of return

At 39%

year Cash flows pvf@39% Present values

e 0.00 0.00 0.00

Average income £ 620,000.00

Average investment £ 1,250,000.00

Average income (A) £ 620,000.00

Average investment (B) £ 1,250,000.00

ARR (A/B) 50%

Net present value

years PV of cash flows

0 -£ 2,000,000.00

1 £ 790,909.09

2 £ 719,008.26

3 £ 653,643.88

4 £ 594,221.71

5 £ 540,201.55

6 £ 773,329.28

NPV £ 2,071,313.77

Internal rate of return

At 39%

year Cash flows pvf@39% Present values

Accounting 17

s

0 -£ 2,000,000.00 1 -£ 2,000,000.00

1 £ 870,000.00 0.71942446 £ 625,899.28

2 £ 870,000.00 0.517571554 £ 450,287.25

3 £ 870,000.00 0.372353636 £ 323,947.66

4 £ 870,000.00 0.267880314 £ 233,055.87

5 £ 870,000.00 0.19271965 £ 167,666.10

6 £ 1,370,000.00 0.13864723 £ 189,946.71

-£ 9,197.13

At 38%

years Cash flows pvf@38% Present values

0 -£ 2,000,000.00 1 -£ 2,000,000.00

1 £ 870,000.00

0.72463768

1 £ 630,434.78

2 £ 870,000.00

0.52509976

9 £ 456,836.80

3 £ 870,000.00

0.38050707

9 £ 331,041.16

4 £ 870,000.00

0.27572976

7 £ 239,884.90

5 £ 870,000.00

0.19980417

9 £ 173,829.64

6 £ 1,370,000.00 0.14478563 £ 198,356.32

s

0 -£ 2,000,000.00 1 -£ 2,000,000.00

1 £ 870,000.00 0.71942446 £ 625,899.28

2 £ 870,000.00 0.517571554 £ 450,287.25

3 £ 870,000.00 0.372353636 £ 323,947.66

4 £ 870,000.00 0.267880314 £ 233,055.87

5 £ 870,000.00 0.19271965 £ 167,666.10

6 £ 1,370,000.00 0.13864723 £ 189,946.71

-£ 9,197.13

At 38%

years Cash flows pvf@38% Present values

0 -£ 2,000,000.00 1 -£ 2,000,000.00

1 £ 870,000.00

0.72463768

1 £ 630,434.78

2 £ 870,000.00

0.52509976

9 £ 456,836.80

3 £ 870,000.00

0.38050707

9 £ 331,041.16

4 £ 870,000.00

0.27572976

7 £ 239,884.90

5 £ 870,000.00

0.19980417

9 £ 173,829.64

6 £ 1,370,000.00 0.14478563 £ 198,356.32

Accounting 18

7

£ 30,383.60

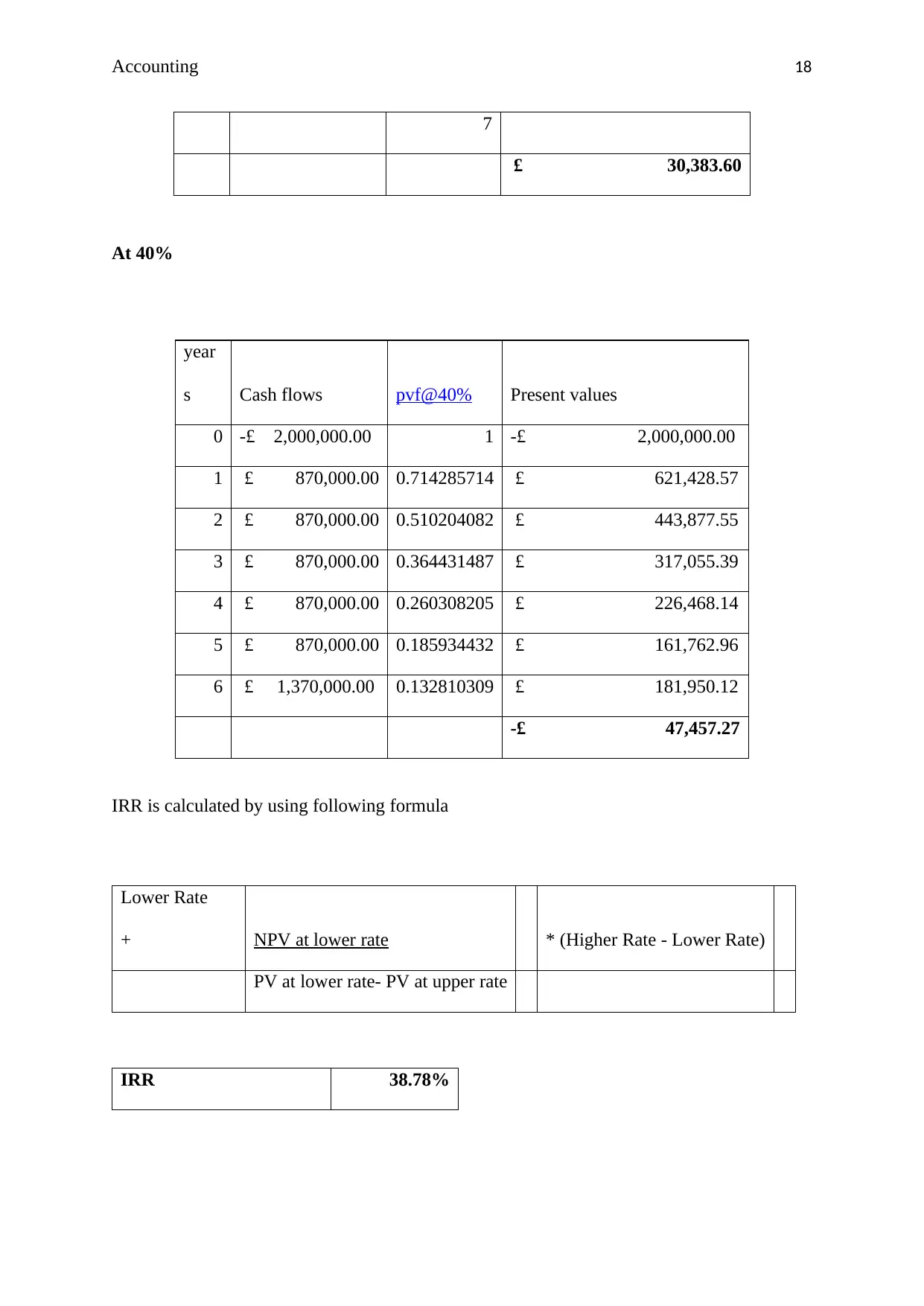

At 40%

year

s Cash flows pvf@40% Present values

0 -£ 2,000,000.00 1 -£ 2,000,000.00

1 £ 870,000.00 0.714285714 £ 621,428.57

2 £ 870,000.00 0.510204082 £ 443,877.55

3 £ 870,000.00 0.364431487 £ 317,055.39

4 £ 870,000.00 0.260308205 £ 226,468.14

5 £ 870,000.00 0.185934432 £ 161,762.96

6 £ 1,370,000.00 0.132810309 £ 181,950.12

-£ 47,457.27

IRR is calculated by using following formula

Lower Rate

+ NPV at lower rate * (Higher Rate - Lower Rate)

PV at lower rate- PV at upper rate

IRR 38.78%

7

£ 30,383.60

At 40%

year

s Cash flows pvf@40% Present values

0 -£ 2,000,000.00 1 -£ 2,000,000.00

1 £ 870,000.00 0.714285714 £ 621,428.57

2 £ 870,000.00 0.510204082 £ 443,877.55

3 £ 870,000.00 0.364431487 £ 317,055.39

4 £ 870,000.00 0.260308205 £ 226,468.14

5 £ 870,000.00 0.185934432 £ 161,762.96

6 £ 1,370,000.00 0.132810309 £ 181,950.12

-£ 47,457.27

IRR is calculated by using following formula

Lower Rate

+ NPV at lower rate * (Higher Rate - Lower Rate)

PV at lower rate- PV at upper rate

IRR 38.78%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting 19

Requirement 2

Evaluation of capital budgeting techniques and their benefits and limitations

Generally when a person thinks of investing in a project, he or she requires to take a major

decisions as making an investment is considered to be a capital expenditure. Usually,

decisions related to such expenditures are irreversible and are very crucial by nature.

Therefore it is very important for the investor to critically evaluate the project before making

any sort of investment. For that purpose various capital budgeting techniques are been used

that analyse the project from all the aspects and checks its feasibility and viability.

Payback period

It is the simplest investment appraisal technique which is always used by the investor to

check the attractiveness of the project. The method basically measures the amount of time

taken by a project to recover its initial investment. Generally, projects having shorter payback

period are more desirable as compare to the one which takes longer time to recoup its initial

outlay (Baker, Jabbouri and Dyaz, 2017). In case of Johnson Ltd., the payback period of

project is 2.30 year which is significantly less than its estimated life. Hence the project is

acceptable. However, many companies compare the calculated payback period with their

expected ones. If the calculated period is less than the expected one, then the project is

accepted. There are certain benefits and limitations of PBP method which are as follows:

Benefits

Easy to calculate and apply.

More beneficial for the companies having shortage of funds as it will help them in

selecting the projects which take less time to recover the investment.

It helps in determining the time required by the project to start generating required

returns. Hence, helps in identifying the risk involved.

Requirement 2

Evaluation of capital budgeting techniques and their benefits and limitations

Generally when a person thinks of investing in a project, he or she requires to take a major

decisions as making an investment is considered to be a capital expenditure. Usually,

decisions related to such expenditures are irreversible and are very crucial by nature.

Therefore it is very important for the investor to critically evaluate the project before making

any sort of investment. For that purpose various capital budgeting techniques are been used

that analyse the project from all the aspects and checks its feasibility and viability.

Payback period

It is the simplest investment appraisal technique which is always used by the investor to

check the attractiveness of the project. The method basically measures the amount of time

taken by a project to recover its initial investment. Generally, projects having shorter payback

period are more desirable as compare to the one which takes longer time to recoup its initial

outlay (Baker, Jabbouri and Dyaz, 2017). In case of Johnson Ltd., the payback period of

project is 2.30 year which is significantly less than its estimated life. Hence the project is

acceptable. However, many companies compare the calculated payback period with their

expected ones. If the calculated period is less than the expected one, then the project is

accepted. There are certain benefits and limitations of PBP method which are as follows:

Benefits

Easy to calculate and apply.

More beneficial for the companies having shortage of funds as it will help them in

selecting the projects which take less time to recover the investment.

It helps in determining the time required by the project to start generating required

returns. Hence, helps in identifying the risk involved.

Accounting 20

Limitations

The method ignores the time value of money.

It does not consider the net income to identify the risk rather than cash flows are been

used for making decisions. Cash flows often avoid the non-cash expenses like

depreciation.

Salvage value is ignored.

Discounted payback period

This method is the extension to PBP method as it takes into account the present values of

cash flows. In other words, discounted cash flows considers the time value of money and give

more realistic results. For Johnson, the DPBP of the project is 2.75 years which is also less

than the estimated life of the proposal, hence acceptable (Bierman and Smidt, 2014).

Benefits

It identifies actual risk associated with the investment

It considers time value of money.

Limitations

Implementation of this method is quite complex and is a time consuming process.

It does not reflect the fact that whether the project will improve or enhance the value

of firm.

Net present value

This technique basically measures the profitability of the project and is being widely used by

many financial analysts and investors. NPV is a simple accounting difference between the

present values of cash inflow and present values of cash outflow. The fundamental rule of

Limitations

The method ignores the time value of money.

It does not consider the net income to identify the risk rather than cash flows are been

used for making decisions. Cash flows often avoid the non-cash expenses like

depreciation.

Salvage value is ignored.

Discounted payback period

This method is the extension to PBP method as it takes into account the present values of

cash flows. In other words, discounted cash flows considers the time value of money and give

more realistic results. For Johnson, the DPBP of the project is 2.75 years which is also less

than the estimated life of the proposal, hence acceptable (Bierman and Smidt, 2014).

Benefits

It identifies actual risk associated with the investment

It considers time value of money.

Limitations

Implementation of this method is quite complex and is a time consuming process.

It does not reflect the fact that whether the project will improve or enhance the value

of firm.

Net present value

This technique basically measures the profitability of the project and is being widely used by

many financial analysts and investors. NPV is a simple accounting difference between the

present values of cash inflow and present values of cash outflow. The fundamental rule of

Accounting 21

NPV says that if the figure is greater than zero, accept the project and if it is less than zero or

negative, then reject the project (Borgonovo, 2017).

NPV of Johnson’s project is positive and therefore company can make investment in the new

machinery. However, following are the benefits and limitations of using this method.

Benefits

It considers the cash flows over the full life of the project.

It respects and takes into account time value of money.

Gives accurate and clear results.

Interpretation of results is quite easy.

Limitations

Difficult to apply as it includes the calculation of company’s cost of capital which is

required to determine the present values.

Not suitable for the projects having different life scales.

Accounting rate of return

This methods involves the two main components of financial statements that are net income

and capital investment. The average of both the elements is taken to calculate the ARR of the

project. In order to measure the proposal on ARR basis, firms are required to set a minimum

rate of return. If ARR is higher than the cut off, the project must be accepted and if it is lower

than the project should be rejected (Daunfeldt and Hartwig, 2014). The ARR of Johnson’s

project is 50% which way higher than the required rate of 10%.

Benefits

It involves the calculation of investment income rather than cash flows. The net

income shows the true profitability of the project.

NPV says that if the figure is greater than zero, accept the project and if it is less than zero or

negative, then reject the project (Borgonovo, 2017).

NPV of Johnson’s project is positive and therefore company can make investment in the new

machinery. However, following are the benefits and limitations of using this method.

Benefits

It considers the cash flows over the full life of the project.

It respects and takes into account time value of money.

Gives accurate and clear results.

Interpretation of results is quite easy.

Limitations

Difficult to apply as it includes the calculation of company’s cost of capital which is

required to determine the present values.

Not suitable for the projects having different life scales.

Accounting rate of return

This methods involves the two main components of financial statements that are net income

and capital investment. The average of both the elements is taken to calculate the ARR of the

project. In order to measure the proposal on ARR basis, firms are required to set a minimum

rate of return. If ARR is higher than the cut off, the project must be accepted and if it is lower

than the project should be rejected (Daunfeldt and Hartwig, 2014). The ARR of Johnson’s

project is 50% which way higher than the required rate of 10%.

Benefits

It involves the calculation of investment income rather than cash flows. The net

income shows the true profitability of the project.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Accounting 22

Easy and simple to apply as well as to understand.

Limitations

Money’s time value is not considered in this method.

The method cannot be applied in cases where capital investment is not made at initial

stage.

Internal rate of return

It is basically the rate where the NPV is equal to zero or in other words the PV of cash

outflow is equal to PV of cash inflow. In Johnson’s Ltd. case, the IRR of the project is

38.78%, higher than the company’s cost of capital. Hence the project must be accepted

(Gotze, Northcott and Schuster, 2016).

Benefits

Cash flows are considered for the total life of the project.

It meets the owner’s purpose of maximizing the wealth.

It is the most reliable and sophisticated method.

Limitations

Difficult to implement as it involves complex calculations.

Interpreting the results is difficult.

In practical context, only few capital budgeting techniques are applied. Generally net present

cash method is mostly used in real life by the investors and financial analyst. In addition to

that, in some examples payback period method is also used as it is very simple and easy to

use. Rest techniques are not found in the real life instances of capital budgeting decision

making (Shapiro, 2008).

Requirement 3

Easy and simple to apply as well as to understand.

Limitations

Money’s time value is not considered in this method.

The method cannot be applied in cases where capital investment is not made at initial

stage.

Internal rate of return

It is basically the rate where the NPV is equal to zero or in other words the PV of cash

outflow is equal to PV of cash inflow. In Johnson’s Ltd. case, the IRR of the project is

38.78%, higher than the company’s cost of capital. Hence the project must be accepted

(Gotze, Northcott and Schuster, 2016).

Benefits

Cash flows are considered for the total life of the project.

It meets the owner’s purpose of maximizing the wealth.

It is the most reliable and sophisticated method.

Limitations

Difficult to implement as it involves complex calculations.

Interpreting the results is difficult.

In practical context, only few capital budgeting techniques are applied. Generally net present

cash method is mostly used in real life by the investors and financial analyst. In addition to

that, in some examples payback period method is also used as it is very simple and easy to

use. Rest techniques are not found in the real life instances of capital budgeting decision

making (Shapiro, 2008).

Requirement 3

Accounting 23

Possible sources of finance

Johnson Ltd. is looking for making an investment in purchasing a machinery worth

£200,000. It seems to be a capital expenditure and hence it require raising funds from

different and appropriate sources. Generally there are external and internal sources of finance,

from where the company raises funds for its future and current projects. Some of the sources

are as follows:

Loan from banks

Johnson can borrow the money by taking loan from bank, if the company has a sound

financial position. Before granting the loan the bank will check the creditworthiness of the

company and its liquidity position in the market. A sound financial position can help Johnson

to easily take a loan from the bank.

Generating funds from internal sources

Another source to raise money is to use the retained earnings. Such source is generally used

for the purpose of expanding the business. Johnson’s Ltd can finance its requirements of

investment in new asset by using the earnings generated from its regular operations. Such

funds are ploughed back in the company for the purpose of business expansion (Jenter and

Lewellen, 2015).

Angel investors

They are those people who invest their own funds in the business rather than using the money

of other people to meet the financing requirements of the companies.

Conclusion

From the above report is concluded that it is very necessary to conduct a financial analysis to

know about the actual performance and position of the company. Ratio analysis provides a

brief scenario of the company’s financial performance as well as its position. Similarly, it is

Possible sources of finance

Johnson Ltd. is looking for making an investment in purchasing a machinery worth

£200,000. It seems to be a capital expenditure and hence it require raising funds from

different and appropriate sources. Generally there are external and internal sources of finance,

from where the company raises funds for its future and current projects. Some of the sources

are as follows:

Loan from banks

Johnson can borrow the money by taking loan from bank, if the company has a sound

financial position. Before granting the loan the bank will check the creditworthiness of the

company and its liquidity position in the market. A sound financial position can help Johnson

to easily take a loan from the bank.

Generating funds from internal sources

Another source to raise money is to use the retained earnings. Such source is generally used

for the purpose of expanding the business. Johnson’s Ltd can finance its requirements of

investment in new asset by using the earnings generated from its regular operations. Such

funds are ploughed back in the company for the purpose of business expansion (Jenter and

Lewellen, 2015).

Angel investors

They are those people who invest their own funds in the business rather than using the money

of other people to meet the financing requirements of the companies.

Conclusion

From the above report is concluded that it is very necessary to conduct a financial analysis to

know about the actual performance and position of the company. Ratio analysis provides a

brief scenario of the company’s financial performance as well as its position. Similarly, it is

Accounting 24

very important for the investors to apply proper techniques before making an investment in a

project. The investor should check the feasibility and viability of the project.

References

Baker, H.K., Jabbouri, I. and Dyaz, C. (2017). Corporate finance practices in

Morocco. Managerial Finance, 43(8), 865-880.

Bierman Jr, H. and Smidt, S. (2014). Advanced capital budgeting: Refinements in the

economic analysis of investment projects. Oxon: Routledge.

Borgonovo, E. (2017). Sensitivity Analysis: An Introduction for the Management

Scientist (Vol. 251). Switzerland: Springer.

very important for the investors to apply proper techniques before making an investment in a

project. The investor should check the feasibility and viability of the project.

References

Baker, H.K., Jabbouri, I. and Dyaz, C. (2017). Corporate finance practices in

Morocco. Managerial Finance, 43(8), 865-880.

Bierman Jr, H. and Smidt, S. (2014). Advanced capital budgeting: Refinements in the

economic analysis of investment projects. Oxon: Routledge.

Borgonovo, E. (2017). Sensitivity Analysis: An Introduction for the Management

Scientist (Vol. 251). Switzerland: Springer.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting 25

Bragg, S. M. (2012). Business ratios and formulas: a comprehensive guide (Vol. 577). New

Jersy: John Wiley and Sons.

Daunfeldt, S.O. and Hartwig, F. (2014). What determines the use of capital budgeting

methods?: Evidence from Swedish listed companies. Journal of Finance and

Economics, 2(4),101-112.

Gibson, C. H. (2011). Financial reporting and analysis. USA: South-Western Cengage

Learning.

Godwin, N. and Alderman, C. (2012). Financial ACCT2. USA: Cengage Learning.

Gotze, U., Northcott, D. and Schuster, P. (2016). INVESTMENT APPRAISAL. (2nd ed.). New

York: Springer.

Higgins, R. C. (2012). Analysis for financial management. New York: McGraw-Hill/Irwin.

Jenter, D. and Lewellen, K. (2015). CEO preferences and acquisitions. The Journal of

Finance, 70(6), pp.2813-2852.

Kimmel, P. D., Weygandt, J. J., and Kieso, D. E. (2010). Financial accounting: tools for

business decision making. New Jersy: John Wiley and Sons.

Krantz, M., and Johnson, R. R. (2014). Investment Banking for Dummies. New Jersy: John

Wiley and Sons.

Lee, A. C., Lee, J. C., and Lee, C. F. (2009). Financial analysis, planning and forecasting:

Theory and application. Singapore: World Scientific Publishing Co Inc.

Saleem, Q. and Rehman, R.U. (2011). Impacts of liquidity ratios on

profitability. Interdisciplinary Journal of Research in Business, 1(7), pp.95-98.

Shapiro, A. C. (2008). Capital budgeting and investment analysis. India: Pearson Education.

Bragg, S. M. (2012). Business ratios and formulas: a comprehensive guide (Vol. 577). New

Jersy: John Wiley and Sons.

Daunfeldt, S.O. and Hartwig, F. (2014). What determines the use of capital budgeting

methods?: Evidence from Swedish listed companies. Journal of Finance and

Economics, 2(4),101-112.

Gibson, C. H. (2011). Financial reporting and analysis. USA: South-Western Cengage

Learning.

Godwin, N. and Alderman, C. (2012). Financial ACCT2. USA: Cengage Learning.

Gotze, U., Northcott, D. and Schuster, P. (2016). INVESTMENT APPRAISAL. (2nd ed.). New

York: Springer.

Higgins, R. C. (2012). Analysis for financial management. New York: McGraw-Hill/Irwin.

Jenter, D. and Lewellen, K. (2015). CEO preferences and acquisitions. The Journal of

Finance, 70(6), pp.2813-2852.

Kimmel, P. D., Weygandt, J. J., and Kieso, D. E. (2010). Financial accounting: tools for

business decision making. New Jersy: John Wiley and Sons.

Krantz, M., and Johnson, R. R. (2014). Investment Banking for Dummies. New Jersy: John

Wiley and Sons.

Lee, A. C., Lee, J. C., and Lee, C. F. (2009). Financial analysis, planning and forecasting:

Theory and application. Singapore: World Scientific Publishing Co Inc.

Saleem, Q. and Rehman, R.U. (2011). Impacts of liquidity ratios on

profitability. Interdisciplinary Journal of Research in Business, 1(7), pp.95-98.

Shapiro, A. C. (2008). Capital budgeting and investment analysis. India: Pearson Education.

Accounting 26

Tracy, A. (2012). Ratio analysis fundamentals: how 17 financial ratios can allow you to

analyse any business on the planet. RatioAnalysis. Net.

Vogel, H.L. (2014). Entertainment industry economics: A guide for financial analysis. New

York: Cambridge University Press.

Warren, C. S., and Jones, J. (2018). Corporate financial accounting. USA: Cengage Learning.

Tracy, A. (2012). Ratio analysis fundamentals: how 17 financial ratios can allow you to

analyse any business on the planet. RatioAnalysis. Net.

Vogel, H.L. (2014). Entertainment industry economics: A guide for financial analysis. New

York: Cambridge University Press.

Warren, C. S., and Jones, J. (2018). Corporate financial accounting. USA: Cengage Learning.

1 out of 27

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.