Netflix Financial and Business Analysis: Industry and Ratio Analysis

VerifiedAdded on 2020/07/23

|24

|5174

|119

Report

AI Summary

This report provides a comprehensive financial and business analysis of Netflix, a leading entertainment company. The analysis begins with an executive summary and then delves into industry analysis using Porter's Five Forces model to assess competitive dynamics. The report then calculates and interprets various financial ratios, including liquidity, solvency, and profitability ratios, over a five-year period to evaluate Netflix's financial health. Furthermore, the report explores valuation techniques, including the Gordon Growth Model and Free Cash Flow valuation, to estimate the company's intrinsic value. The report also includes an analysis of the company's profile, strategy, and the risks it faces, such as exchange rate risk. The analysis includes tables and illustrations to support the findings and concludes with an overall assessment of Netflix's business performance and financial position.

FINANCIAL AND

BUSINESS ANALYSIS

BUSINESS ANALYSIS

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

EXECUTIVE SUMMARY.............................................................................................................1

INDUSTRY ANALYSIS................................................................................................................3

Rivalry among existing competitors.......................................................................................4

Threat of new entrants............................................................................................................4

Threat of substitute products..................................................................................................4

Bargaining power of buyers...................................................................................................5

Bargaining power of suppliers................................................................................................5

FINANCIAL RATIOS.....................................................................................................................5

Liquidity ratios.......................................................................................................................5

Solvency ratios.......................................................................................................................6

Profitability ratios...................................................................................................................7

Employee count measures......................................................................................................9

Accuracy of the Financial statements...................................................................................10

Absolute Valuation with Gordan Growth Model.................................................................11

Free cash flow valuation.......................................................................................................17

Relative Valuation based on comparable data......................................................................17

REFERENCES..............................................................................................................................19

EXECUTIVE SUMMARY.............................................................................................................1

INDUSTRY ANALYSIS................................................................................................................3

Rivalry among existing competitors.......................................................................................4

Threat of new entrants............................................................................................................4

Threat of substitute products..................................................................................................4

Bargaining power of buyers...................................................................................................5

Bargaining power of suppliers................................................................................................5

FINANCIAL RATIOS.....................................................................................................................5

Liquidity ratios.......................................................................................................................5

Solvency ratios.......................................................................................................................6

Profitability ratios...................................................................................................................7

Employee count measures......................................................................................................9

Accuracy of the Financial statements...................................................................................10

Absolute Valuation with Gordan Growth Model.................................................................11

Free cash flow valuation.......................................................................................................17

Relative Valuation based on comparable data......................................................................17

REFERENCES..............................................................................................................................19

ILLUSTRATION INDEX

Illustration 1: Revenue on International Platform...........................................................................2

Illustration 2: Porter's five force model...........................................................................................4

Illustration 3: Current ratio..............................................................................................................6

Illustration 4: Debt to equity ratio....................................................................................................7

Illustration 5: Interest coverage ratio...............................................................................................7

Illustration 6: Gross profit ratio.......................................................................................................8

Illustration 7: Operating profit ratio.................................................................................................8

Illustration 8: Net profit ratio...........................................................................................................9

Illustration 9: Revenue per employee............................................................................................10

Illustration 10: Comparison of earning per share..........................................................................14

Index of Tables

Table 1: Calculation of liquidity ratio..............................................................................................5

Table 2: Solvency Ratios.................................................................................................................6

Table 3: Calculation of Profitability ratios......................................................................................7

Table 4: Calculation of Employee count measures..........................................................................9

Table 5: Balance Sheet based accrual ratio....................................................................................10

Table 6: Cash Flow based accrual ratio.........................................................................................11

Table 7: Calculation of operating cash flow to operating income.................................................11

Table 8: Estimated Return on Equity.............................................................................................12

Table 9: Forecasted Net income....................................................................................................12

Table 10: Calculation of Retention rate.........................................................................................13

Table 11: Calculation of Sensitivity Analysis...............................................................................16

Table 12: Free Cash Flow Valuation.............................................................................................17

Illustration 1: Revenue on International Platform...........................................................................2

Illustration 2: Porter's five force model...........................................................................................4

Illustration 3: Current ratio..............................................................................................................6

Illustration 4: Debt to equity ratio....................................................................................................7

Illustration 5: Interest coverage ratio...............................................................................................7

Illustration 6: Gross profit ratio.......................................................................................................8

Illustration 7: Operating profit ratio.................................................................................................8

Illustration 8: Net profit ratio...........................................................................................................9

Illustration 9: Revenue per employee............................................................................................10

Illustration 10: Comparison of earning per share..........................................................................14

Index of Tables

Table 1: Calculation of liquidity ratio..............................................................................................5

Table 2: Solvency Ratios.................................................................................................................6

Table 3: Calculation of Profitability ratios......................................................................................7

Table 4: Calculation of Employee count measures..........................................................................9

Table 5: Balance Sheet based accrual ratio....................................................................................10

Table 6: Cash Flow based accrual ratio.........................................................................................11

Table 7: Calculation of operating cash flow to operating income.................................................11

Table 8: Estimated Return on Equity.............................................................................................12

Table 9: Forecasted Net income....................................................................................................12

Table 10: Calculation of Retention rate.........................................................................................13

Table 11: Calculation of Sensitivity Analysis...............................................................................16

Table 12: Free Cash Flow Valuation.............................................................................................17

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

EXECUTIVE SUMMARY

In order to make analysis of business performance there are mainly two aspects included

which are financial and non-financial. In the present study, financial aspect is covered for

assessing company's performance in the relevant industry. In the current research, Netflix

company is taken as a base which is one of the largest firm operating in entertainment industry. It

is American based public enterprise and having presence in more than 190 countries. The present

study focuses on industry analysis using Porter’s five force model. Apart from this, financial

ratios are calculated up to five accounting periods and financial statements on the basis of

accuracy are prepared. In addition to this, valuation process is shown of the company after

consisting Gordon Growth Model. Free cash flow valuation of Netflix entertainment entity is

also described in the present study. At the end of report, technical analysis is presented of the

cited firm and then business performance is analysed in proper direction.

Company profile – Netflix

Netflix is an America – based company which is the world's leading organisation in the

internet television network. It has total subscribers list of 104 million in around 190 countries

with 5 million + subscribers in United Kingdom and 52 million in United States and an

employee count of 3500 employees. It earned a total revenue of US $ 8.83 billion in the year

2016. Netflix has an incredible count of 125 million hours of TV shows and movies per day. Any

subscriber is allowed to play, pause, and resume any video with any commercial commitments.

The company has an offering capacity of more than 15,000 titles and also maintains an inventory

of more than 5 million discs of movies and TV series. Netflix provides its streaming services on

a number of compatible devices which include Blu-ray Disc players, tablet computers, mobile

phones, high definition television (HDTV) receivers, home theatre systems, set top boxes, and

video game consoles. Company's biggest competitors are Amazon Prime Inc. and Hulu plus,

these two companies cover a market share of 13% and 6.5% respectively against the huge market

share of 36% hold by Netflix of the American households.

Revenues of can be divided as follows: The company have been planning to opt for

global expansion in order to expand its business. It has already been present in most of the

countries of the world.

Revenues of can be divided as follows :

1

In order to make analysis of business performance there are mainly two aspects included

which are financial and non-financial. In the present study, financial aspect is covered for

assessing company's performance in the relevant industry. In the current research, Netflix

company is taken as a base which is one of the largest firm operating in entertainment industry. It

is American based public enterprise and having presence in more than 190 countries. The present

study focuses on industry analysis using Porter’s five force model. Apart from this, financial

ratios are calculated up to five accounting periods and financial statements on the basis of

accuracy are prepared. In addition to this, valuation process is shown of the company after

consisting Gordon Growth Model. Free cash flow valuation of Netflix entertainment entity is

also described in the present study. At the end of report, technical analysis is presented of the

cited firm and then business performance is analysed in proper direction.

Company profile – Netflix

Netflix is an America – based company which is the world's leading organisation in the

internet television network. It has total subscribers list of 104 million in around 190 countries

with 5 million + subscribers in United Kingdom and 52 million in United States and an

employee count of 3500 employees. It earned a total revenue of US $ 8.83 billion in the year

2016. Netflix has an incredible count of 125 million hours of TV shows and movies per day. Any

subscriber is allowed to play, pause, and resume any video with any commercial commitments.

The company has an offering capacity of more than 15,000 titles and also maintains an inventory

of more than 5 million discs of movies and TV series. Netflix provides its streaming services on

a number of compatible devices which include Blu-ray Disc players, tablet computers, mobile

phones, high definition television (HDTV) receivers, home theatre systems, set top boxes, and

video game consoles. Company's biggest competitors are Amazon Prime Inc. and Hulu plus,

these two companies cover a market share of 13% and 6.5% respectively against the huge market

share of 36% hold by Netflix of the American households.

Revenues of can be divided as follows: The company have been planning to opt for

global expansion in order to expand its business. It has already been present in most of the

countries of the world.

Revenues of can be divided as follows :

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

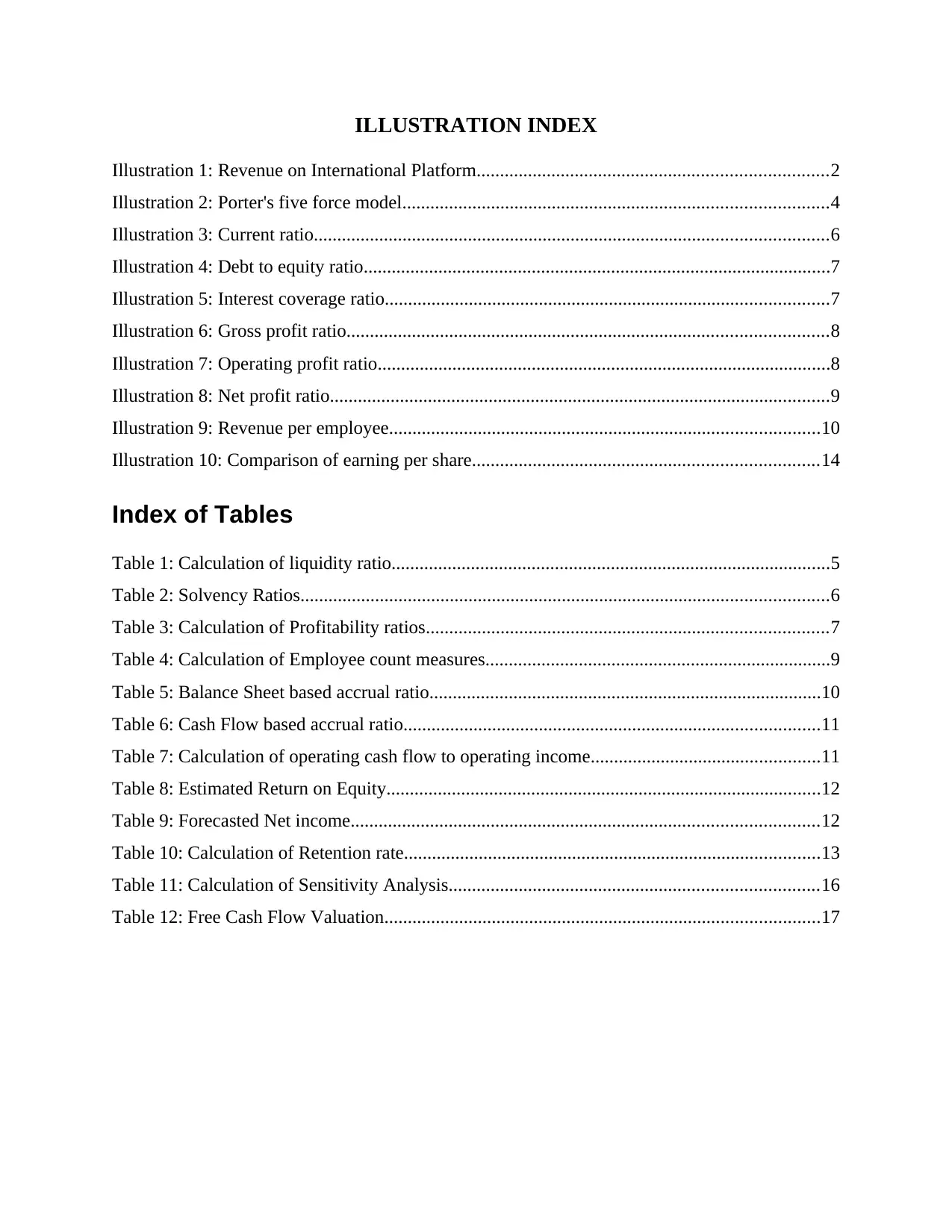

The above graph shows a significant increase in its revenue in comparison to 2007. The

data reveals that the reveue of the entity was 7.48 million in 2007 which has increased to 86.74

million according to quarter 3 results of the organization. The main reason of this increase is due

to rise in the prevalence of internet where people can watch online series, films etc.

Collaboration:

Netflix a part of producing its original content and copy rights on several other contents,

also fixed a deal of collaborations with a good deal of entertainment production houses. In 2013,

Netflix and Dream works made a deal to produce turbo fast (Pianosi, Sarrazin and Wagener,

2015). And in the same year Netflix and Marvel collaborated to create several marvels sciences –

fiction superhero based TV series for the sci-fi audience which included Daredevil, Jessica

Jones, Iron Fist and Luke Cage. These series were set to run for an initial of 5 seasons. It was

calculated that marvel deal costed Netflix about $300 million in total. Netflix also collaborated

with many stand-up artists to create stand-up shows. Also, Netflix and Ruko partnered to provide

2

Illustration 1: Revenue on International Platform

data reveals that the reveue of the entity was 7.48 million in 2007 which has increased to 86.74

million according to quarter 3 results of the organization. The main reason of this increase is due

to rise in the prevalence of internet where people can watch online series, films etc.

Collaboration:

Netflix a part of producing its original content and copy rights on several other contents,

also fixed a deal of collaborations with a good deal of entertainment production houses. In 2013,

Netflix and Dream works made a deal to produce turbo fast (Pianosi, Sarrazin and Wagener,

2015). And in the same year Netflix and Marvel collaborated to create several marvels sciences –

fiction superhero based TV series for the sci-fi audience which included Daredevil, Jessica

Jones, Iron Fist and Luke Cage. These series were set to run for an initial of 5 seasons. It was

calculated that marvel deal costed Netflix about $300 million in total. Netflix also collaborated

with many stand-up artists to create stand-up shows. Also, Netflix and Ruko partnered to provide

2

Illustration 1: Revenue on International Platform

super high definition content to the subscribers. Netflix also have a huge base with a

collaboration made with Leonardo DiCaprio for his documentaries. Deal between Netflix and

Disney was made in 2012 by creation of movies.

Strategy to expand business :

Strategy to expand business:

Netflix opted for an excellent strategy to co produce shows with other entertainment units

whose content was already a success in other sources available giving it a boost to the revenue. It

also gave a decent focus on the R&D activities to keep the content updated and attractive to the

subscribers (Tian, 2013).

Exchange rate risk:

As, Netflix operates in 190 countries it's risk of exchange rate is particularly high. Its

rate risk between United Kingdom and America has been good for the company as it has jumped

for $1.8-1.3 to every one euro. Netflix also shares big risks in the countries like India, China as

the exchange rate is quite high of 0.15 US dollar to one Chinese Yuan and 0.016 US$ to 1 Indian

Rupee.

It is an important driving factor which is considered by Netflix while planning for global

expansion. The currency exchange rate and economy of the country helps in deciding that how

much revenue it can generate from the same. The prices are decided according to the purchasing

power of the company and this is the reason why prices of the entity fluctuates among the

countries.

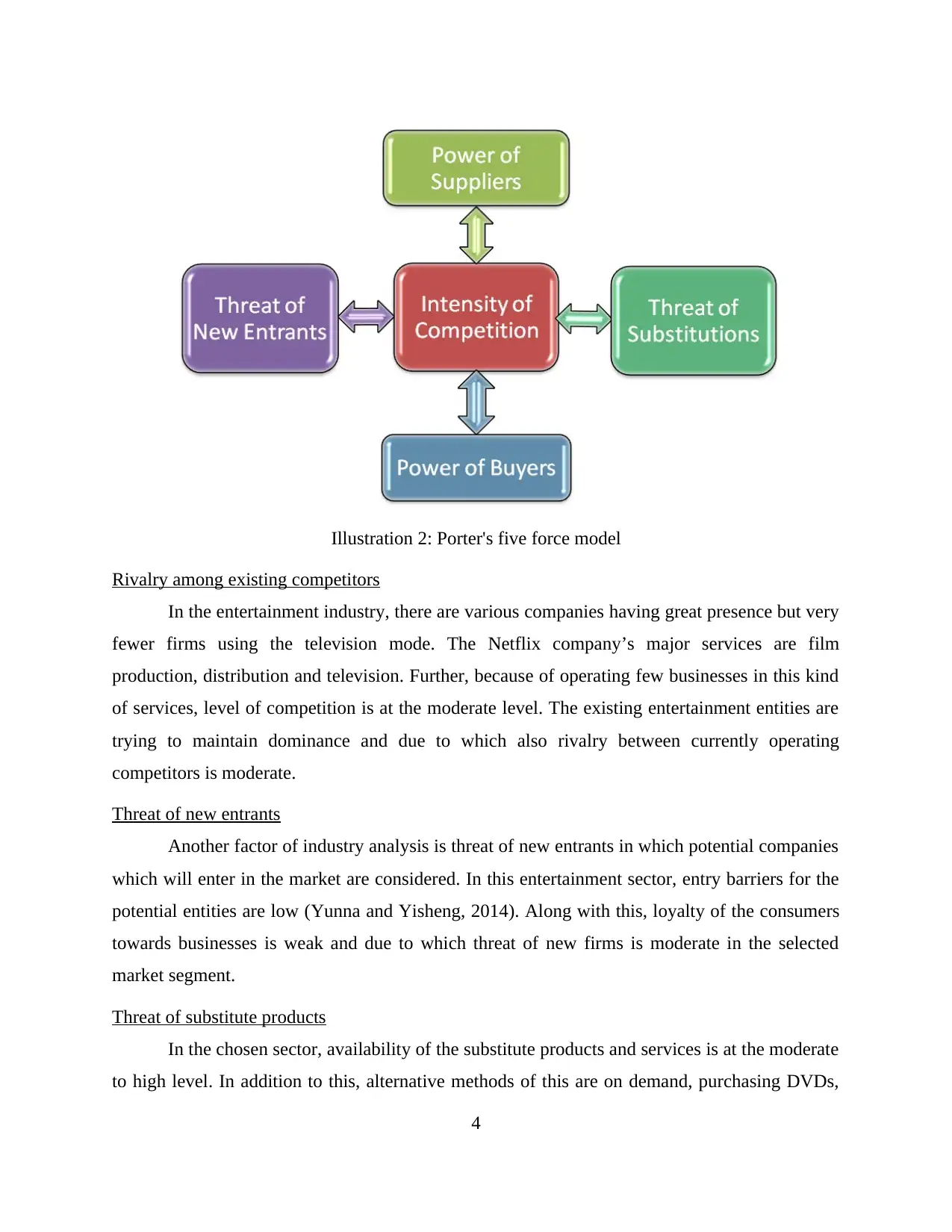

INDUSTRY ANALYSIS

Entertainment industry is one of the fastest growing and having high contribution in

growth rate of every economy. For analysing particular sector there are several kinds of methods

available with the analyst and one of them is Porter's five forces model. By using this, basically

four aspects of the overall industry are analysed in appropriate direction. In this respective

market segment, there are various companies operating in the present era but level of substitute

products is very low (Porter's Five Forces, 2016). Moreover, industry analysis of entertainment

with the help of Porter's five forces is such as follows:

3

collaboration made with Leonardo DiCaprio for his documentaries. Deal between Netflix and

Disney was made in 2012 by creation of movies.

Strategy to expand business :

Strategy to expand business:

Netflix opted for an excellent strategy to co produce shows with other entertainment units

whose content was already a success in other sources available giving it a boost to the revenue. It

also gave a decent focus on the R&D activities to keep the content updated and attractive to the

subscribers (Tian, 2013).

Exchange rate risk:

As, Netflix operates in 190 countries it's risk of exchange rate is particularly high. Its

rate risk between United Kingdom and America has been good for the company as it has jumped

for $1.8-1.3 to every one euro. Netflix also shares big risks in the countries like India, China as

the exchange rate is quite high of 0.15 US dollar to one Chinese Yuan and 0.016 US$ to 1 Indian

Rupee.

It is an important driving factor which is considered by Netflix while planning for global

expansion. The currency exchange rate and economy of the country helps in deciding that how

much revenue it can generate from the same. The prices are decided according to the purchasing

power of the company and this is the reason why prices of the entity fluctuates among the

countries.

INDUSTRY ANALYSIS

Entertainment industry is one of the fastest growing and having high contribution in

growth rate of every economy. For analysing particular sector there are several kinds of methods

available with the analyst and one of them is Porter's five forces model. By using this, basically

four aspects of the overall industry are analysed in appropriate direction. In this respective

market segment, there are various companies operating in the present era but level of substitute

products is very low (Porter's Five Forces, 2016). Moreover, industry analysis of entertainment

with the help of Porter's five forces is such as follows:

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Illustration 2: Porter's five force model

Rivalry among existing competitors

In the entertainment industry, there are various companies having great presence but very

fewer firms using the television mode. The Netflix company’s major services are film

production, distribution and television. Further, because of operating few businesses in this kind

of services, level of competition is at the moderate level. The existing entertainment entities are

trying to maintain dominance and due to which also rivalry between currently operating

competitors is moderate.

Threat of new entrants

Another factor of industry analysis is threat of new entrants in which potential companies

which will enter in the market are considered. In this entertainment sector, entry barriers for the

potential entities are low (Yunna and Yisheng, 2014). Along with this, loyalty of the consumers

towards businesses is weak and due to which threat of new firms is moderate in the selected

market segment.

Threat of substitute products

In the chosen sector, availability of the substitute products and services is at the moderate

to high level. In addition to this, alternative methods of this are on demand, purchasing DVDs,

4

Rivalry among existing competitors

In the entertainment industry, there are various companies having great presence but very

fewer firms using the television mode. The Netflix company’s major services are film

production, distribution and television. Further, because of operating few businesses in this kind

of services, level of competition is at the moderate level. The existing entertainment entities are

trying to maintain dominance and due to which also rivalry between currently operating

competitors is moderate.

Threat of new entrants

Another factor of industry analysis is threat of new entrants in which potential companies

which will enter in the market are considered. In this entertainment sector, entry barriers for the

potential entities are low (Yunna and Yisheng, 2014). Along with this, loyalty of the consumers

towards businesses is weak and due to which threat of new firms is moderate in the selected

market segment.

Threat of substitute products

In the chosen sector, availability of the substitute products and services is at the moderate

to high level. In addition to this, alternative methods of this are on demand, purchasing DVDs,

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

theatres etc. Henceforth, it can be analysed that, threat of substitute items in entertainment

industry is moderate and little high.

Bargaining power of buyers

When talking about bargaining at the time of purchases from the consumers side then it is

high in entertainment sector. Very basic reason of this is that, buyer's loyalty towards the

company is weak. Along with this, revenue generated from customers at the majority level is

included in this segment. Moreover, bargaining power of buyers in entertainment field is high (E.

Dobbs 2014).

Bargaining power of suppliers

The last force through which industry is assessed is similar to bargaining power of

suppliers which is high in the entertainment. There is availability so many legal issues that are to

be dealt with along with licensing deals. Hence, bargaining power of the entertainment

businesses like Netflix is high.

FINANCIAL RATIOS

Method by which performance of the particular company is analysed in proper manner by

considering financial statements is known as financial ratios. It includes several measurements

and in the present study liquidity, solvency, profitability and employee count measures are used

(Babalola and Abiola, 2013). Further, the ratios for Netflix company are stated below:

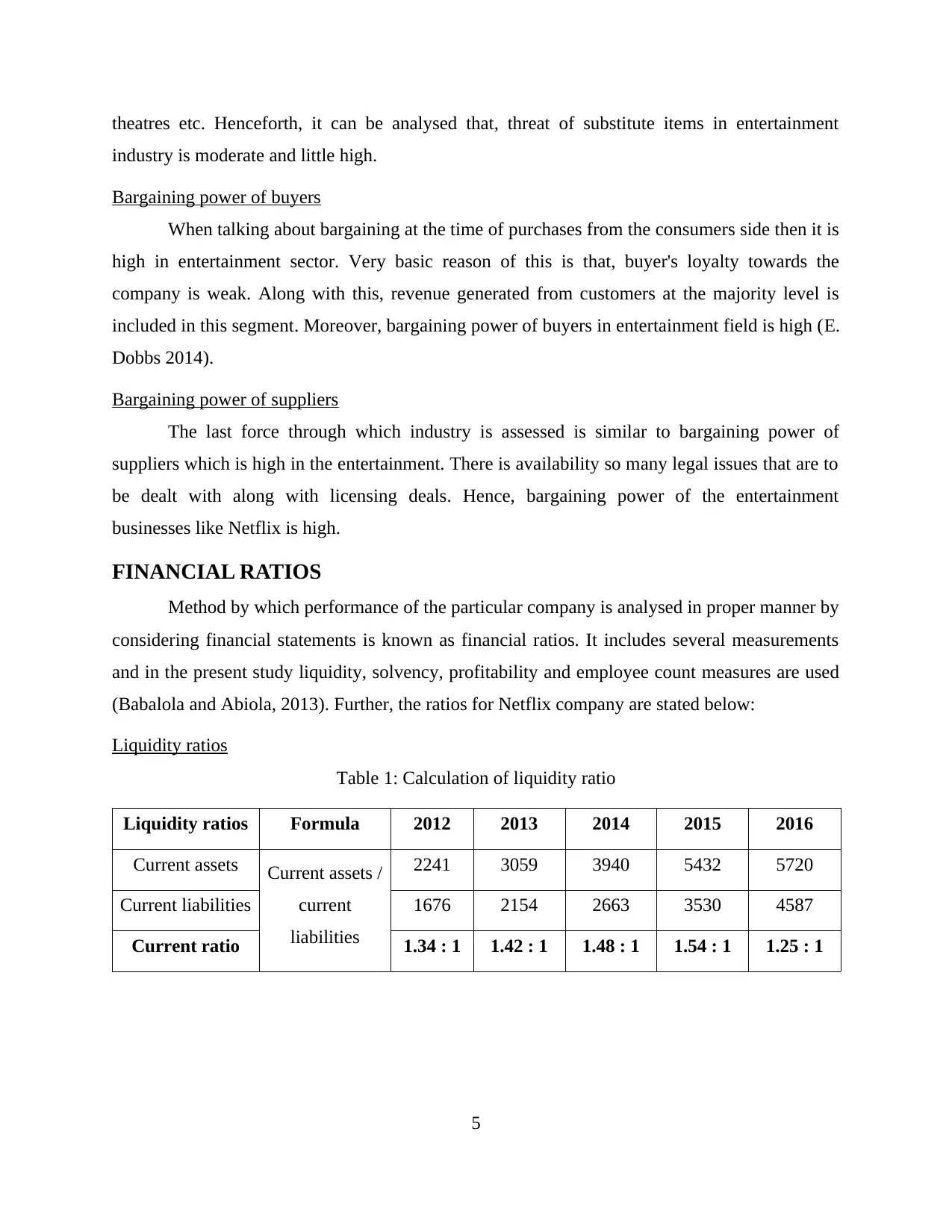

Liquidity ratios

Table 1: Calculation of liquidity ratio

Liquidity ratios Formula 2012 2013 2014 2015 2016

Current assets Current assets /

current

liabilities

2241 3059 3940 5432 5720

Current liabilities 1676 2154 2663 3530 4587

Current ratio 1.34 : 1 1.42 : 1 1.48 : 1 1.54 : 1 1.25 : 1

5

industry is moderate and little high.

Bargaining power of buyers

When talking about bargaining at the time of purchases from the consumers side then it is

high in entertainment sector. Very basic reason of this is that, buyer's loyalty towards the

company is weak. Along with this, revenue generated from customers at the majority level is

included in this segment. Moreover, bargaining power of buyers in entertainment field is high (E.

Dobbs 2014).

Bargaining power of suppliers

The last force through which industry is assessed is similar to bargaining power of

suppliers which is high in the entertainment. There is availability so many legal issues that are to

be dealt with along with licensing deals. Hence, bargaining power of the entertainment

businesses like Netflix is high.

FINANCIAL RATIOS

Method by which performance of the particular company is analysed in proper manner by

considering financial statements is known as financial ratios. It includes several measurements

and in the present study liquidity, solvency, profitability and employee count measures are used

(Babalola and Abiola, 2013). Further, the ratios for Netflix company are stated below:

Liquidity ratios

Table 1: Calculation of liquidity ratio

Liquidity ratios Formula 2012 2013 2014 2015 2016

Current assets Current assets /

current

liabilities

2241 3059 3940 5432 5720

Current liabilities 1676 2154 2663 3530 4587

Current ratio 1.34 : 1 1.42 : 1 1.48 : 1 1.54 : 1 1.25 : 1

5

2012 2013 2014 2015 2016

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

1.80

1.34 1.42 1.48 1.54

1.25

Illustration 3: Current ratio

From the above calculated ratio, it can be found that, from the FY 2012 to 2015

proportion of current ratio increases from 1.34:1 to 1.54:1 which indicates that business

performance is in positive direction. After the fiscal period 2015, current ratio declines from

1.54:1 to 1.25:1 where performance reduces. Further, overall liquidity position of Netflix

company is moderate in the entertainment industry.

Solvency ratios

Table 2: Solvency Ratios

Solvency ratios Formula 2012 2013 2014 2015 2016

Debt

Debt / equity

400 500 900 2371 3364

Equity 745 1334 1858 2223 2680

Debt to equity

ratio 0.54:1 0.37:1 0.48:1 1.07:1 1.26:1

Earnings before

interest and taxes

Earnings before interest

and taxes / Interest

expenses

50 228 403 306 380

Interest expenses 20 29 53 133 150

Interest coverage

ratio 2.50 7.86 7.60 2.30 2.53

6

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

1.80

1.34 1.42 1.48 1.54

1.25

Illustration 3: Current ratio

From the above calculated ratio, it can be found that, from the FY 2012 to 2015

proportion of current ratio increases from 1.34:1 to 1.54:1 which indicates that business

performance is in positive direction. After the fiscal period 2015, current ratio declines from

1.54:1 to 1.25:1 where performance reduces. Further, overall liquidity position of Netflix

company is moderate in the entertainment industry.

Solvency ratios

Table 2: Solvency Ratios

Solvency ratios Formula 2012 2013 2014 2015 2016

Debt

Debt / equity

400 500 900 2371 3364

Equity 745 1334 1858 2223 2680

Debt to equity

ratio 0.54:1 0.37:1 0.48:1 1.07:1 1.26:1

Earnings before

interest and taxes

Earnings before interest

and taxes / Interest

expenses

50 228 403 306 380

Interest expenses 20 29 53 133 150

Interest coverage

ratio 2.50 7.86 7.60 2.30 2.53

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2012 2013 2014 2015 2016

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

0.54

0.37

0.48

1.07

1.26

Illustration 4: Debt to equity ratio

2012 2013 2014 2015 2016

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

9.00

2.50

7.86 7.60

2.30 2.53

Illustration 5: Interest coverage ratio

According to above stated graphs, company has not been performing well at the end of

two financial years i.e. 2015 and 2015. The reason is that, it has higher debt in comparison to the

equity share capital (Delen, Kuzey and Uyar, 2013). In addition to this, Netflix firm is less

capable to pay amount of interest from FY 2013 to 2016. Hence, according to solvency ratios

business performance of Netflix is poor. For reducing debt to equity ratio, the Netflix needs to

boost up profit and raise fund through equity rather than debt.

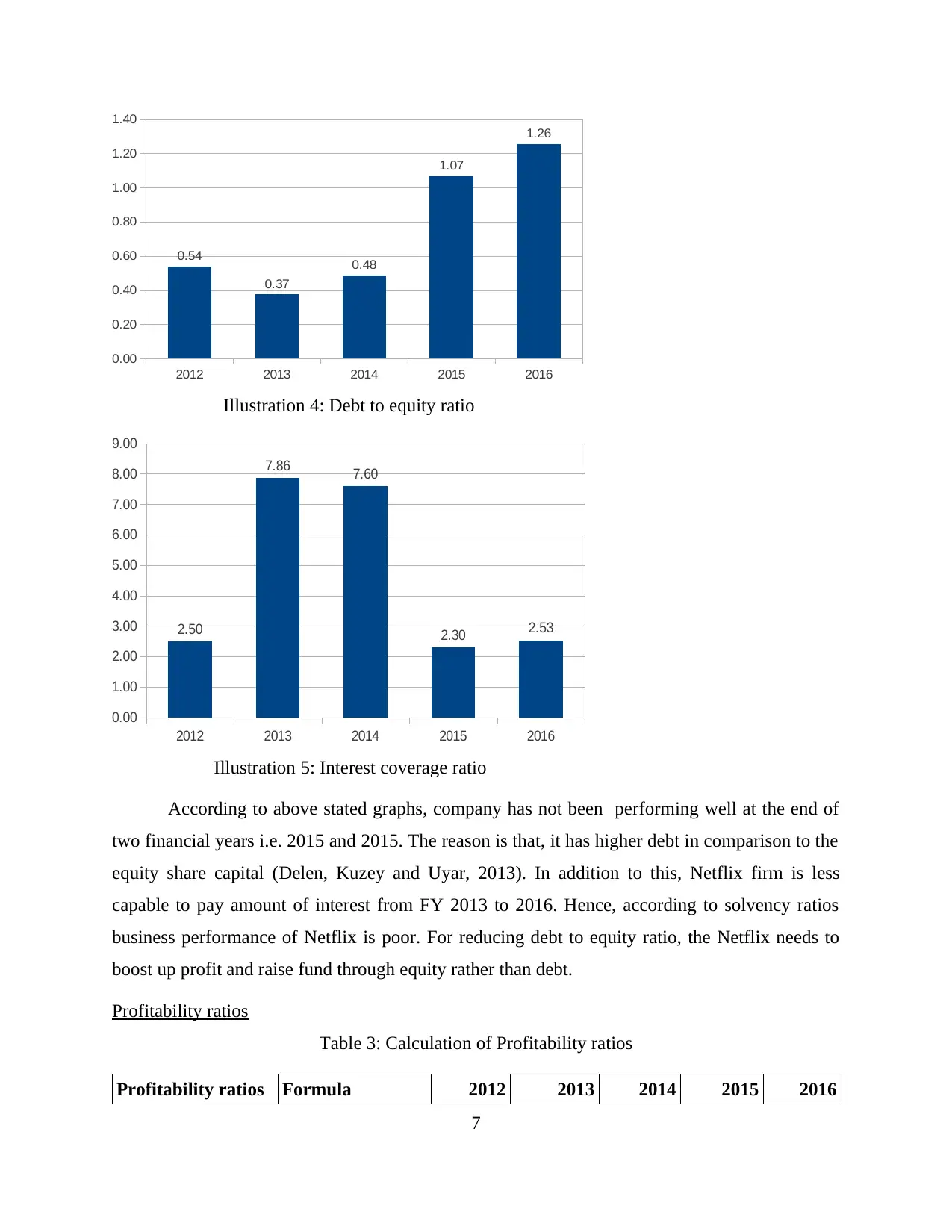

Profitability ratios

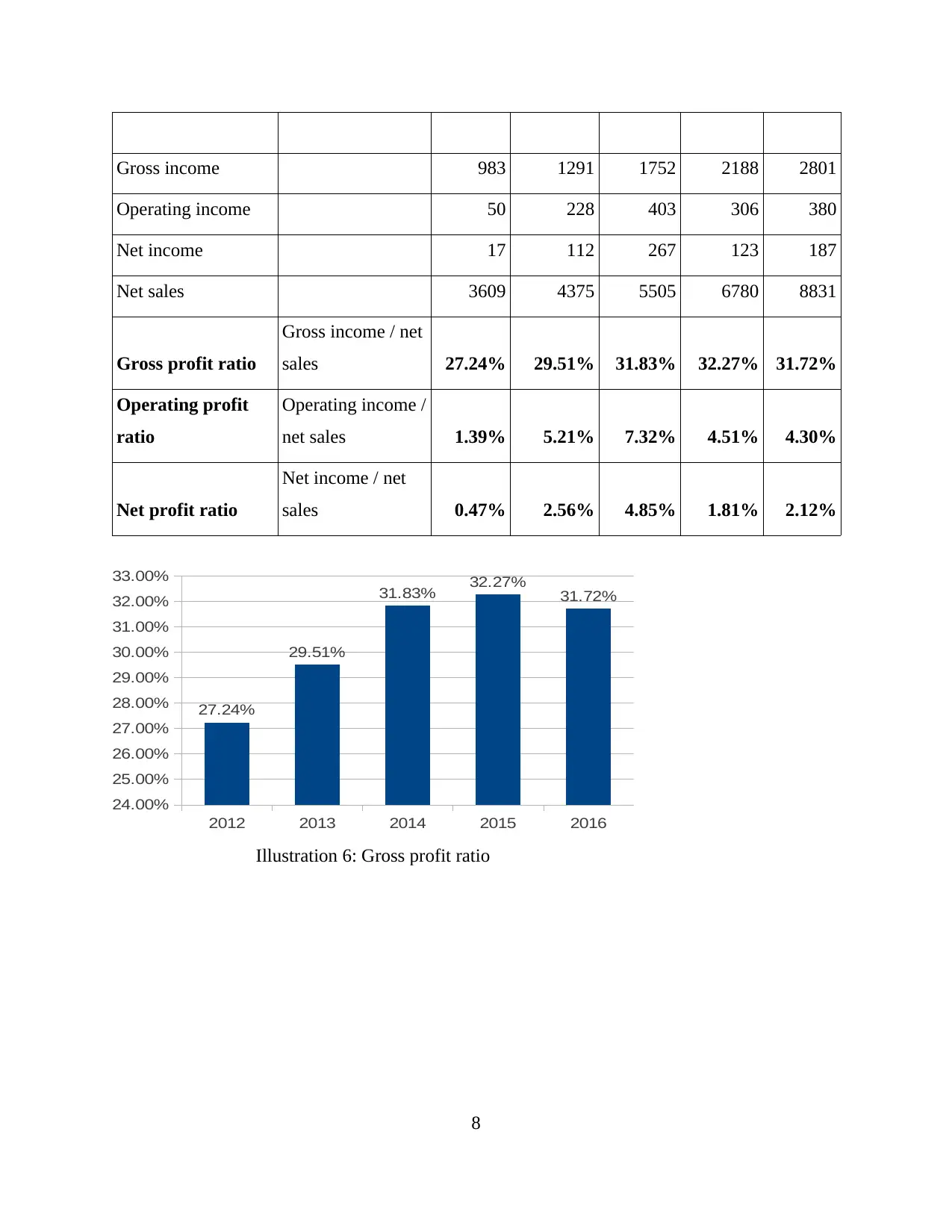

Table 3: Calculation of Profitability ratios

Profitability ratios Formula 2012 2013 2014 2015 2016

7

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

0.54

0.37

0.48

1.07

1.26

Illustration 4: Debt to equity ratio

2012 2013 2014 2015 2016

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

9.00

2.50

7.86 7.60

2.30 2.53

Illustration 5: Interest coverage ratio

According to above stated graphs, company has not been performing well at the end of

two financial years i.e. 2015 and 2015. The reason is that, it has higher debt in comparison to the

equity share capital (Delen, Kuzey and Uyar, 2013). In addition to this, Netflix firm is less

capable to pay amount of interest from FY 2013 to 2016. Hence, according to solvency ratios

business performance of Netflix is poor. For reducing debt to equity ratio, the Netflix needs to

boost up profit and raise fund through equity rather than debt.

Profitability ratios

Table 3: Calculation of Profitability ratios

Profitability ratios Formula 2012 2013 2014 2015 2016

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Gross income 983 1291 1752 2188 2801

Operating income 50 228 403 306 380

Net income 17 112 267 123 187

Net sales 3609 4375 5505 6780 8831

Gross profit ratio

Gross income / net

sales 27.24% 29.51% 31.83% 32.27% 31.72%

Operating profit

ratio

Operating income /

net sales 1.39% 5.21% 7.32% 4.51% 4.30%

Net profit ratio

Net income / net

sales 0.47% 2.56% 4.85% 1.81% 2.12%

2012 2013 2014 2015 2016

24.00%

25.00%

26.00%

27.00%

28.00%

29.00%

30.00%

31.00%

32.00%

33.00%

27.24%

29.51%

31.83% 32.27% 31.72%

Illustration 6: Gross profit ratio

8

Operating income 50 228 403 306 380

Net income 17 112 267 123 187

Net sales 3609 4375 5505 6780 8831

Gross profit ratio

Gross income / net

sales 27.24% 29.51% 31.83% 32.27% 31.72%

Operating profit

ratio

Operating income /

net sales 1.39% 5.21% 7.32% 4.51% 4.30%

Net profit ratio

Net income / net

sales 0.47% 2.56% 4.85% 1.81% 2.12%

2012 2013 2014 2015 2016

24.00%

25.00%

26.00%

27.00%

28.00%

29.00%

30.00%

31.00%

32.00%

33.00%

27.24%

29.51%

31.83% 32.27% 31.72%

Illustration 6: Gross profit ratio

8

2012 2013 2014 2015 2016

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

8.00%

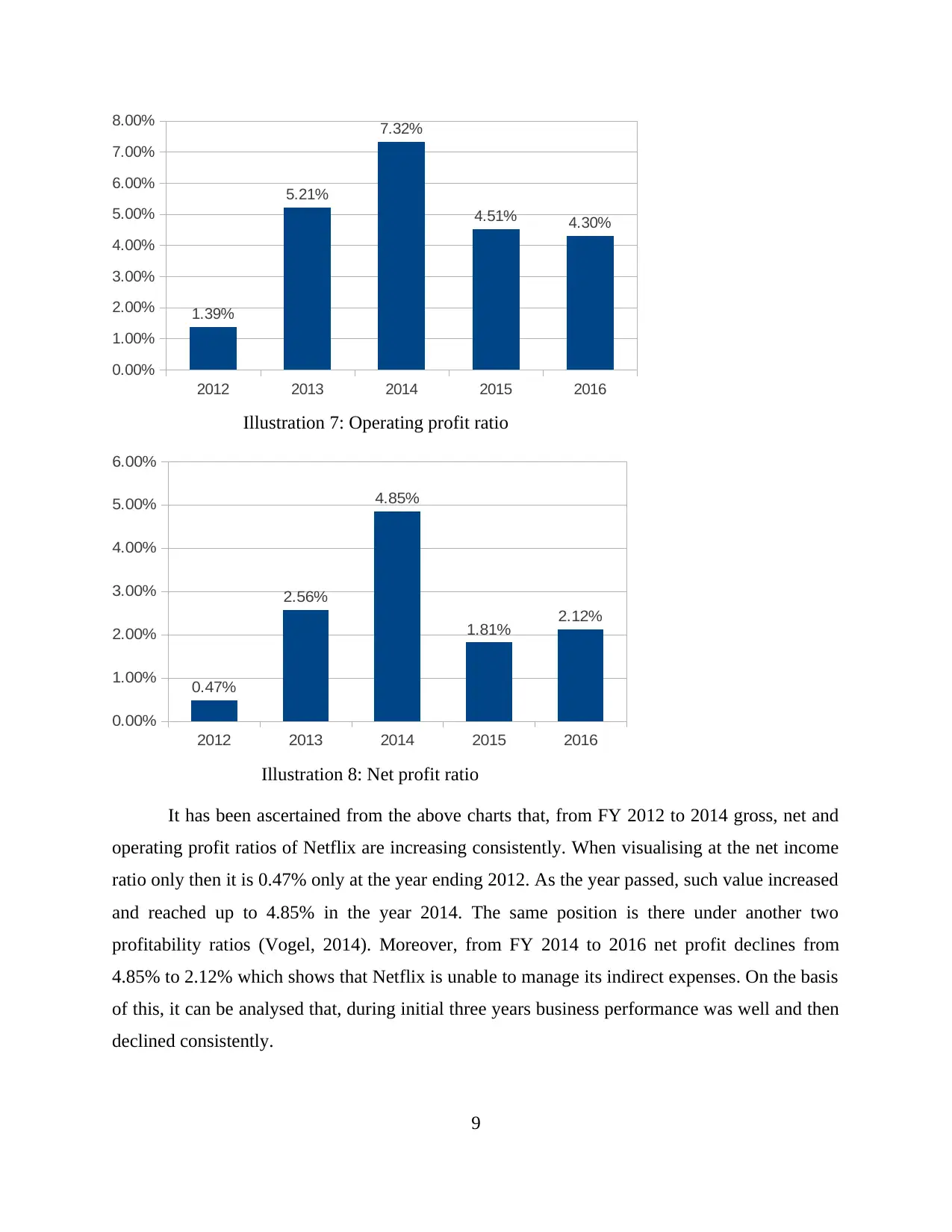

1.39%

5.21%

7.32%

4.51% 4.30%

Illustration 7: Operating profit ratio

2012 2013 2014 2015 2016

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

0.47%

2.56%

4.85%

1.81% 2.12%

Illustration 8: Net profit ratio

It has been ascertained from the above charts that, from FY 2012 to 2014 gross, net and

operating profit ratios of Netflix are increasing consistently. When visualising at the net income

ratio only then it is 0.47% only at the year ending 2012. As the year passed, such value increased

and reached up to 4.85% in the year 2014. The same position is there under another two

profitability ratios (Vogel, 2014). Moreover, from FY 2014 to 2016 net profit declines from

4.85% to 2.12% which shows that Netflix is unable to manage its indirect expenses. On the basis

of this, it can be analysed that, during initial three years business performance was well and then

declined consistently.

9

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

8.00%

1.39%

5.21%

7.32%

4.51% 4.30%

Illustration 7: Operating profit ratio

2012 2013 2014 2015 2016

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

0.47%

2.56%

4.85%

1.81% 2.12%

Illustration 8: Net profit ratio

It has been ascertained from the above charts that, from FY 2012 to 2014 gross, net and

operating profit ratios of Netflix are increasing consistently. When visualising at the net income

ratio only then it is 0.47% only at the year ending 2012. As the year passed, such value increased

and reached up to 4.85% in the year 2014. The same position is there under another two

profitability ratios (Vogel, 2014). Moreover, from FY 2014 to 2016 net profit declines from

4.85% to 2.12% which shows that Netflix is unable to manage its indirect expenses. On the basis

of this, it can be analysed that, during initial three years business performance was well and then

declined consistently.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 24

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.