ACT610: Financial and Corporate Reporting Final Term Assignment

VerifiedAdded on 2022/12/28

|7

|635

|64

Homework Assignment

AI Summary

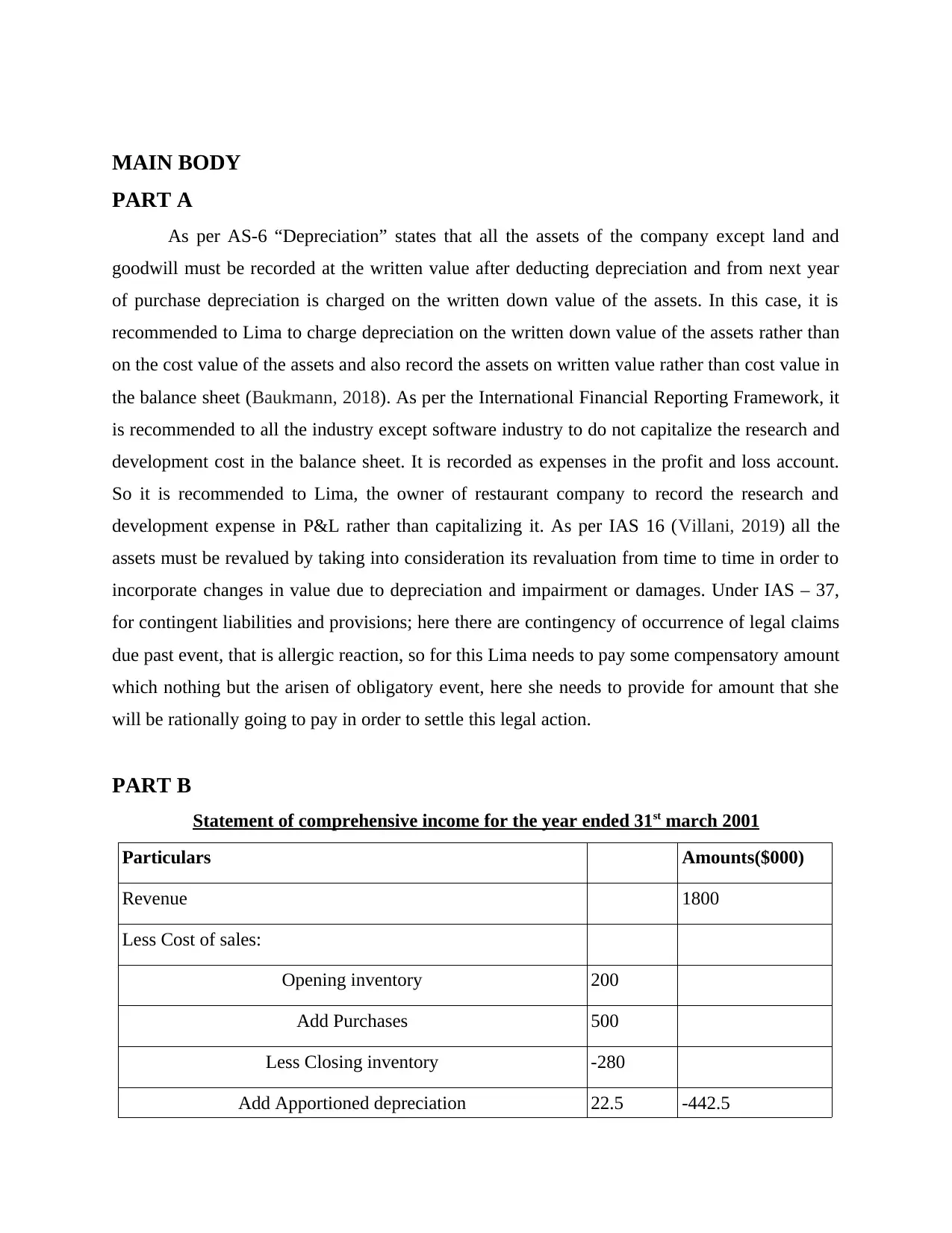

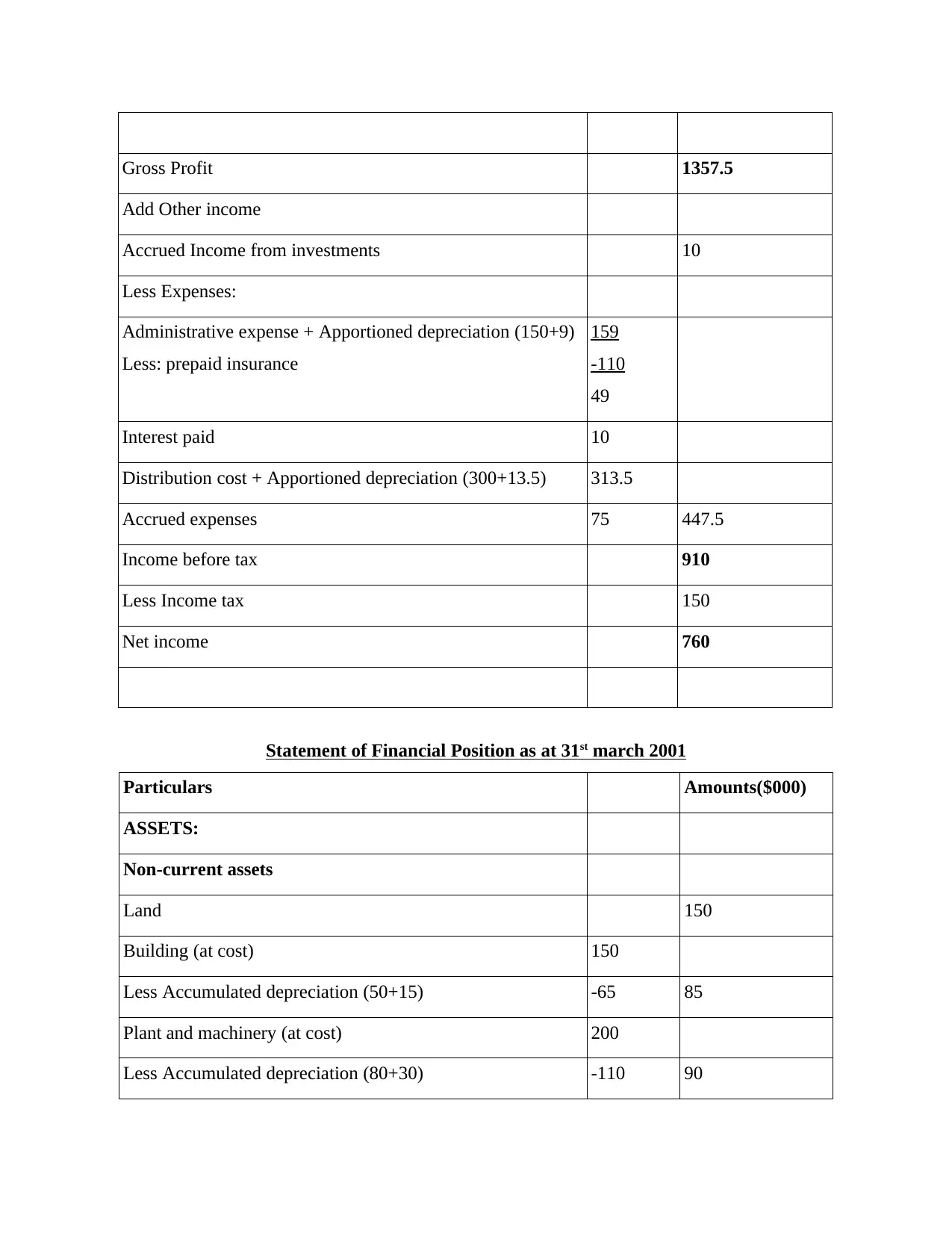

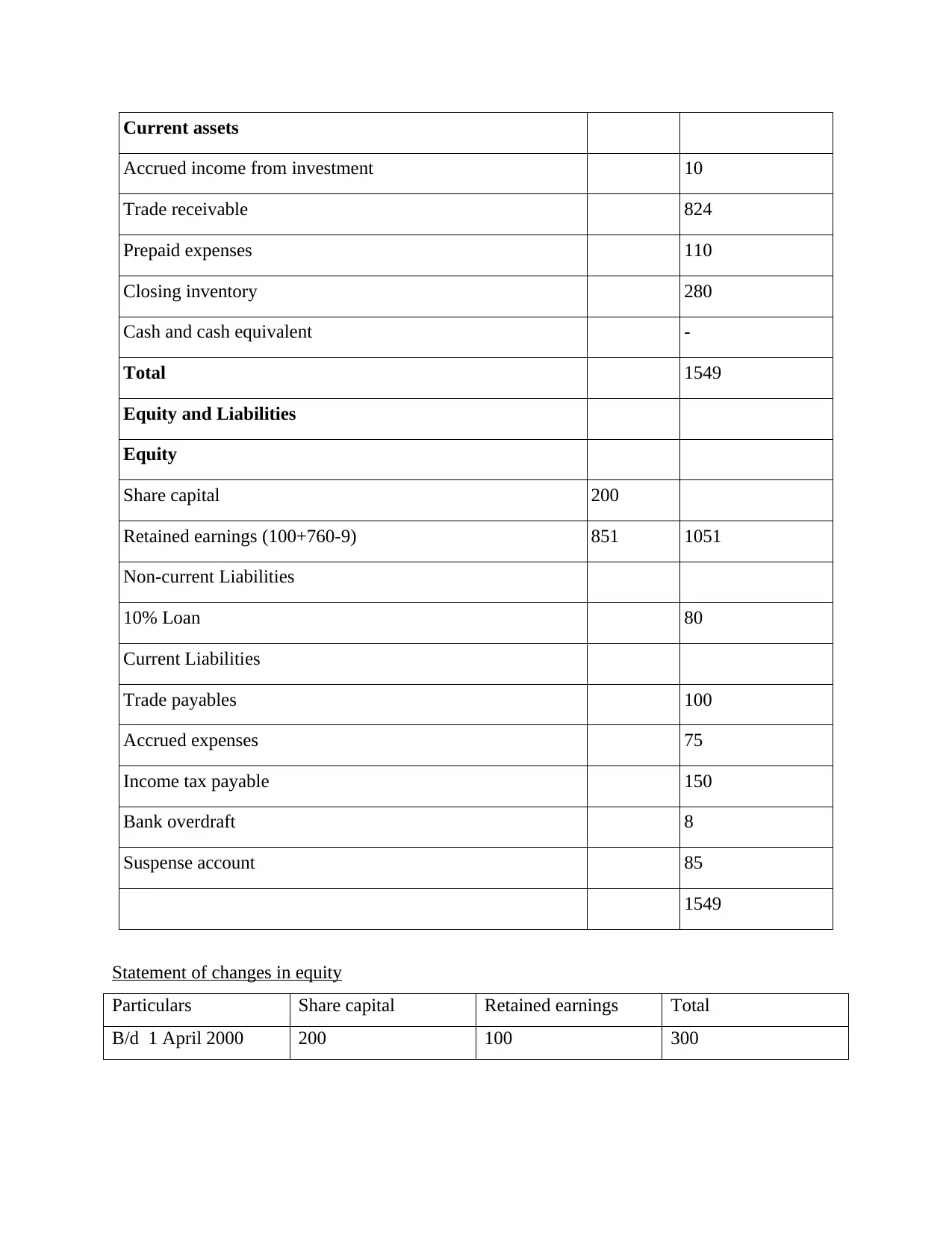

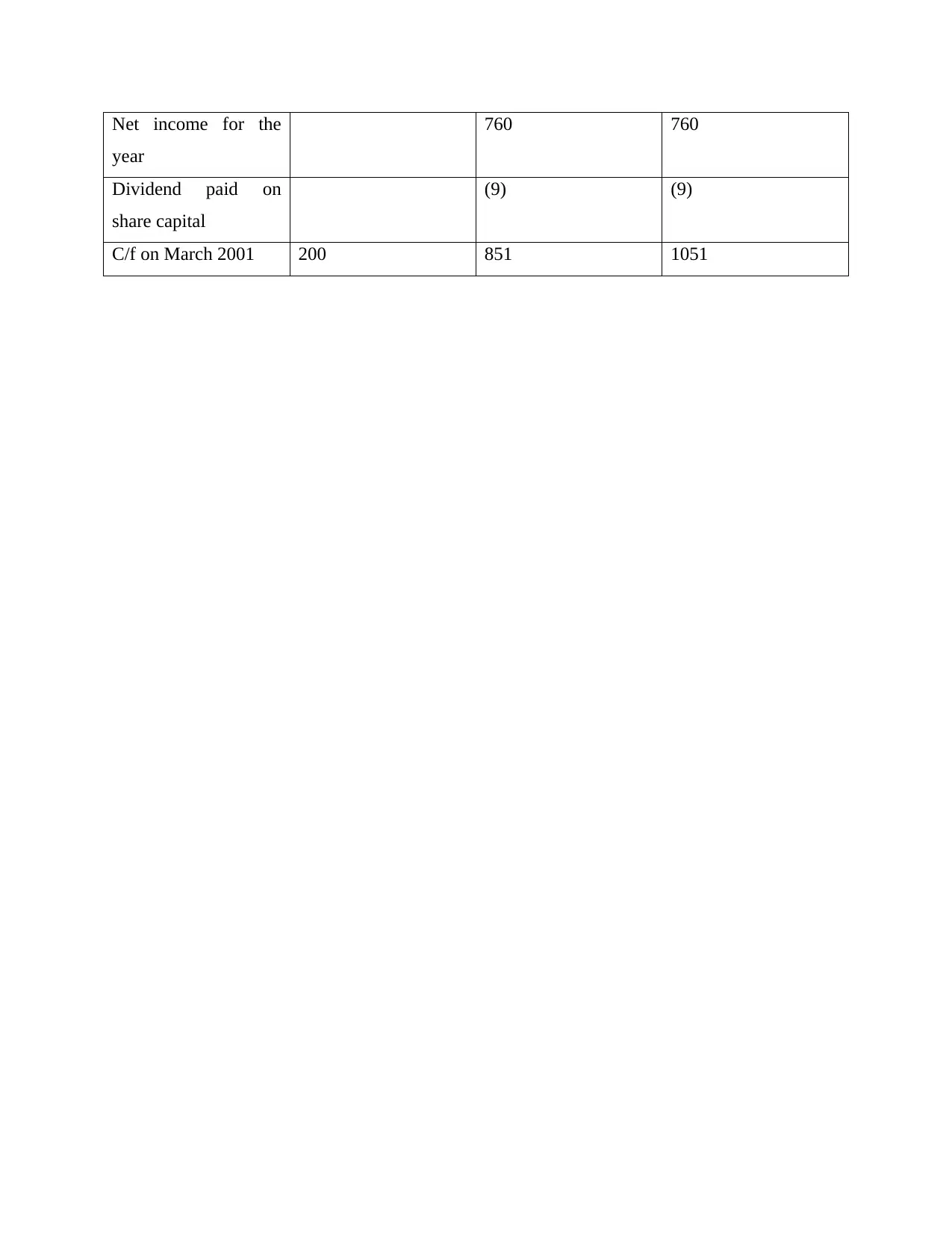

This document provides a comprehensive solution to a financial and corporate reporting assignment for Southeast University's ACT610 course. The assignment addresses a case study involving a restaurant business, Lima, and requires the application of accounting standards such as AS-6, IAS 16, and IAS 37. Part A focuses on accounting recommendations regarding asset valuation, depreciation, and research and development costs, while also addressing the treatment of contingent liabilities. Part B includes the preparation of a statement of comprehensive income, a statement of financial position, and a statement of changes in equity for the restaurant. The solution demonstrates the application of accounting principles to real-world business scenarios and provides a detailed breakdown of financial statements.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.