Investment Appraisal Techniques and Financial Decision-Making Analysis

VerifiedAdded on 2019/12/04

|13

|3443

|195

Report

AI Summary

This report delves into various investment appraisal techniques, crucial for financial decision-making. It explores methods like Net Present Value (NPV), Accounting Rate of Return (ARR), Payback Period, and Internal Rate of Return (IRR), detailing their assumptions, limitations, and applicability. The report includes examples and comparative analyses to illustrate how these techniques aid in evaluating investment proposals. It also covers the comparison of inter-firm and intra-firm techniques. The report emphasizes the importance of choosing the right capital appraisal technique to maximize benefits and minimize risks. The analysis includes tables and calculations demonstrating the application of these techniques in real-world scenarios, providing a comprehensive overview for effective financial management.

Financial and

decision making

1

decision making

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION ..........................................................................................................................3

2. Explain investment appraisal techniques with assumptions, limitations, context and

applicability.................................................................................................................................4

Risk management techniques in capital appraisal.......................................................................7

CONCLUSION ...............................................................................................................................8

REFERENCES................................................................................................................................9

2

INTRODUCTION ..........................................................................................................................3

2. Explain investment appraisal techniques with assumptions, limitations, context and

applicability.................................................................................................................................4

Risk management techniques in capital appraisal.......................................................................7

CONCLUSION ...............................................................................................................................8

REFERENCES................................................................................................................................9

2

INTRODUCTION

Investment appraisal techniques is mathematical method which management use to

determine the benefit for future. There is managerial person use this method for better

forecasting in future time-period. It assumption based techniques which provided possible helps

to managerial or investor for taking best decision which provided maximum profit to company.

In this present report consist of various type of appraisal techniques which used by investor for

for purpose of earn maximum benefit (Allen and Economy, 2011). In other hands it consist of

example in table formate which is analysis by applied appraisal technique. For purpose of taking

better decision for maximum profit in future time period. Investment appraisal technique it

determines that spend of investment which provide return in highly (Allen and Economy, 2011).

Right decision at right time take Benefit as well as leadership team work as accordingly while

poor decision take does not effective and company suffer loss. In this report contain the various

techniques which helpful in right step by the management. Appraisal technique also known as

the capital budgeting is primarily planning process which facilitated to manage investment

either short term or long term. It is the techniques to use better use of their various expenditure

thus such saving from the right management called the saving for enterprise (Bennouna,

Meredith and Marchant, 2010). It is also mange by inter firm and intra firm comparison thus it

helps to manges and serves investment as according to requirement.

Type of the business techniques

1. Real option analysis

2. Accounting rate of return

3. Adjusted present value

4. Profitability index

5. Equivalent equity

6. Pay back period

7. Discounted pay back period

8. Modified internal rate of return (Bennouna, Meredith and Marchant, 2010).

9. Internal rate of return

Type of resources

1. Equity investment

3

Investment appraisal techniques is mathematical method which management use to

determine the benefit for future. There is managerial person use this method for better

forecasting in future time-period. It assumption based techniques which provided possible helps

to managerial or investor for taking best decision which provided maximum profit to company.

In this present report consist of various type of appraisal techniques which used by investor for

for purpose of earn maximum benefit (Allen and Economy, 2011). In other hands it consist of

example in table formate which is analysis by applied appraisal technique. For purpose of taking

better decision for maximum profit in future time period. Investment appraisal technique it

determines that spend of investment which provide return in highly (Allen and Economy, 2011).

Right decision at right time take Benefit as well as leadership team work as accordingly while

poor decision take does not effective and company suffer loss. In this report contain the various

techniques which helpful in right step by the management. Appraisal technique also known as

the capital budgeting is primarily planning process which facilitated to manage investment

either short term or long term. It is the techniques to use better use of their various expenditure

thus such saving from the right management called the saving for enterprise (Bennouna,

Meredith and Marchant, 2010). It is also mange by inter firm and intra firm comparison thus it

helps to manges and serves investment as according to requirement.

Type of the business techniques

1. Real option analysis

2. Accounting rate of return

3. Adjusted present value

4. Profitability index

5. Equivalent equity

6. Pay back period

7. Discounted pay back period

8. Modified internal rate of return (Bennouna, Meredith and Marchant, 2010).

9. Internal rate of return

Type of resources

1. Equity investment

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2. Human resources

3. Interest on investment

4. Organisation profitably

Hence, this present study contain, decision making of the managerial person in selecting

the capital appraisal technique which gives the better knowledge that any of the particular project

gives the maximum benefit to company.

Explain investment appraisal techniques with assumptions, limitations, context and applicability.

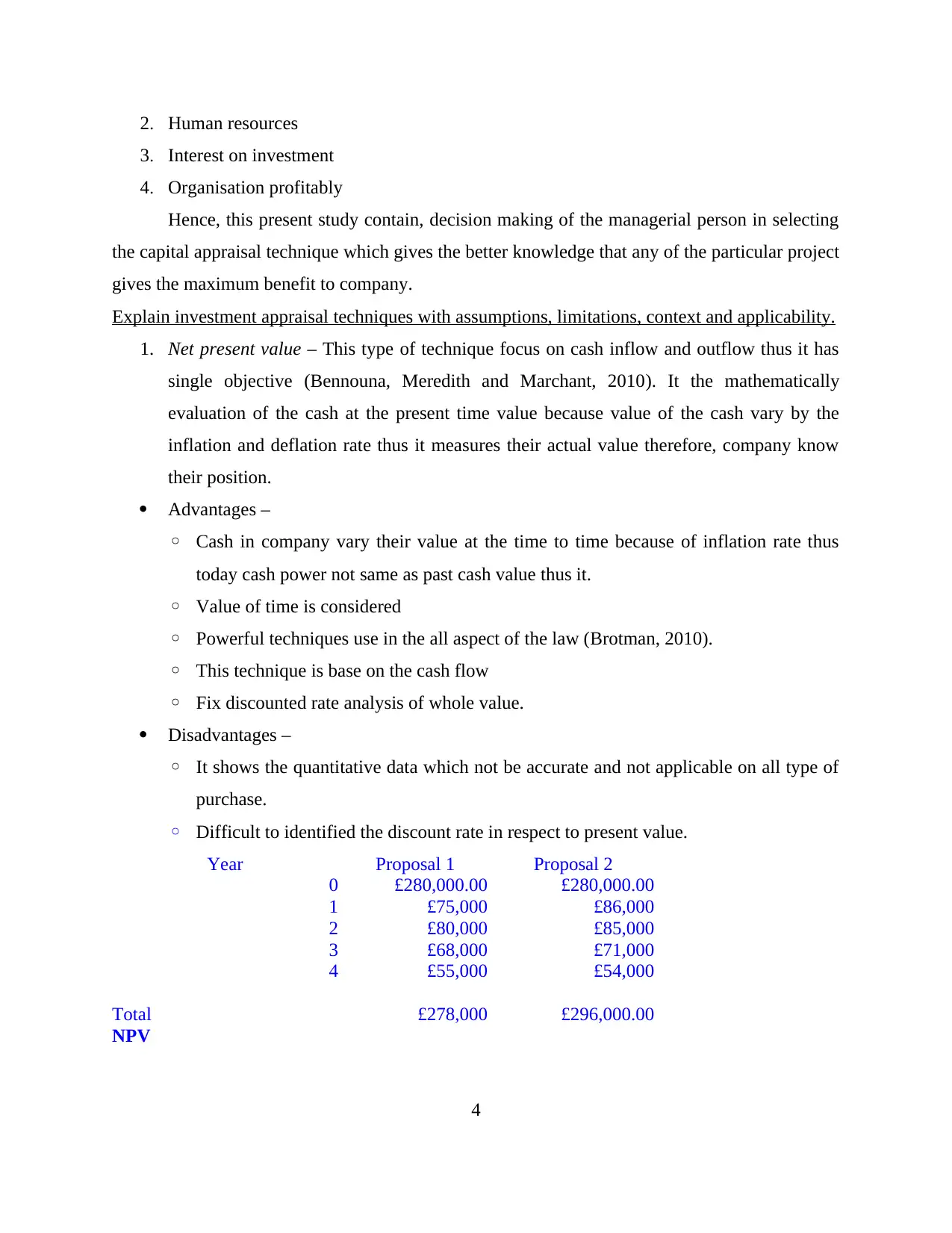

1. Net present value – This type of technique focus on cash inflow and outflow thus it has

single objective (Bennouna, Meredith and Marchant, 2010). It the mathematically

evaluation of the cash at the present time value because value of the cash vary by the

inflation and deflation rate thus it measures their actual value therefore, company know

their position.

Advantages –

◦ Cash in company vary their value at the time to time because of inflation rate thus

today cash power not same as past cash value thus it.

◦ Value of time is considered

◦ Powerful techniques use in the all aspect of the law (Brotman, 2010).

◦ This technique is base on the cash flow

◦ Fix discounted rate analysis of whole value.

Disadvantages –

◦ It shows the quantitative data which not be accurate and not applicable on all type of

purchase.

◦ Difficult to identified the discount rate in respect to present value.

Year Proposal 1 Proposal 2

0 £280,000.00 £280,000.00

1 £75,000 £86,000

2 £80,000 £85,000

3 £68,000 £71,000

4 £55,000 £54,000

Total £278,000 £296,000.00

NPV

4

3. Interest on investment

4. Organisation profitably

Hence, this present study contain, decision making of the managerial person in selecting

the capital appraisal technique which gives the better knowledge that any of the particular project

gives the maximum benefit to company.

Explain investment appraisal techniques with assumptions, limitations, context and applicability.

1. Net present value – This type of technique focus on cash inflow and outflow thus it has

single objective (Bennouna, Meredith and Marchant, 2010). It the mathematically

evaluation of the cash at the present time value because value of the cash vary by the

inflation and deflation rate thus it measures their actual value therefore, company know

their position.

Advantages –

◦ Cash in company vary their value at the time to time because of inflation rate thus

today cash power not same as past cash value thus it.

◦ Value of time is considered

◦ Powerful techniques use in the all aspect of the law (Brotman, 2010).

◦ This technique is base on the cash flow

◦ Fix discounted rate analysis of whole value.

Disadvantages –

◦ It shows the quantitative data which not be accurate and not applicable on all type of

purchase.

◦ Difficult to identified the discount rate in respect to present value.

Year Proposal 1 Proposal 2

0 £280,000.00 £280,000.00

1 £75,000 £86,000

2 £80,000 £85,000

3 £68,000 £71,000

4 £55,000 £54,000

Total £278,000 £296,000.00

NPV

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

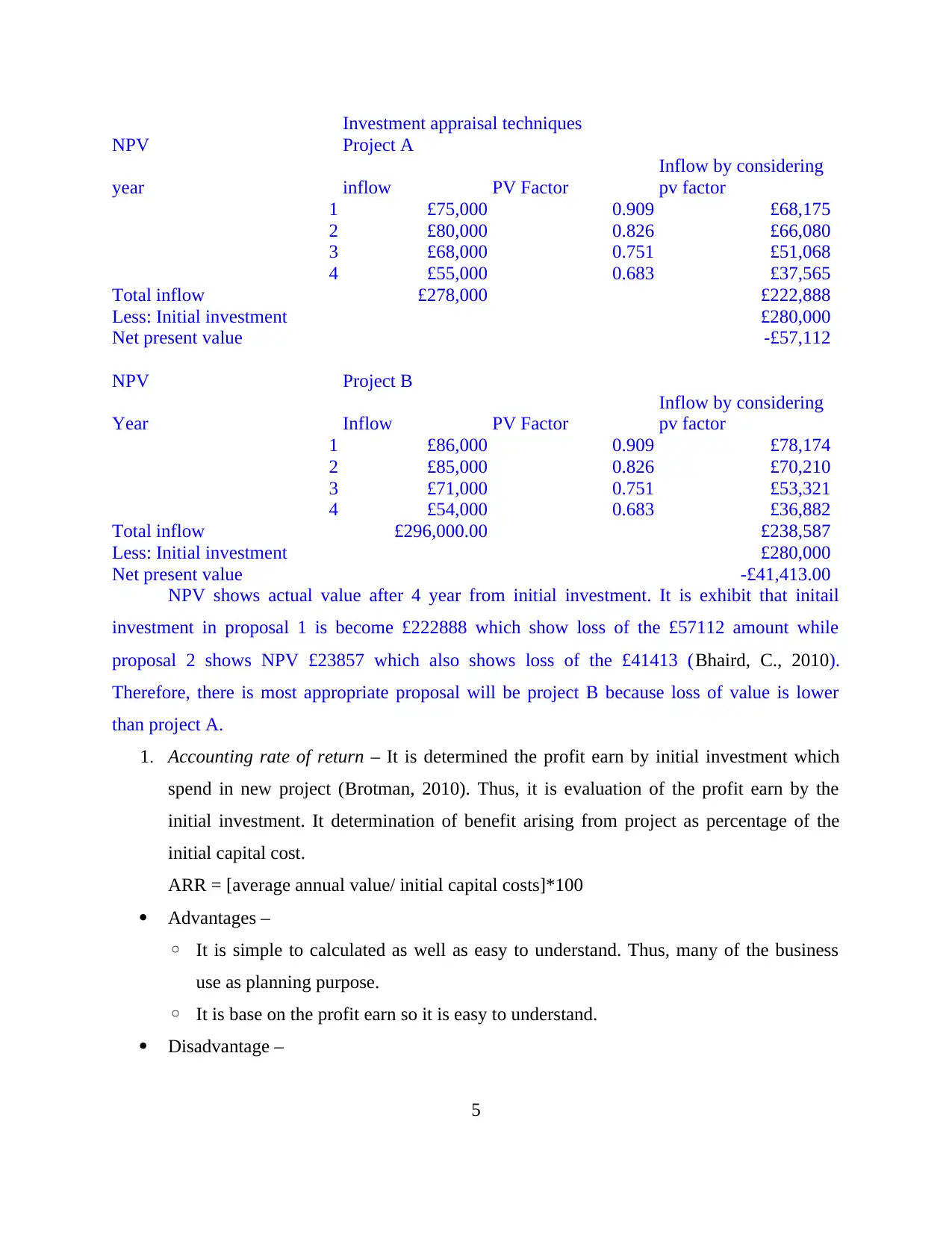

Investment appraisal techniques

NPV Project A

year inflow PV Factor

Inflow by considering

pv factor

1 £75,000 0.909 £68,175

2 £80,000 0.826 £66,080

3 £68,000 0.751 £51,068

4 £55,000 0.683 £37,565

Total inflow £278,000 £222,888

Less: Initial investment £280,000

Net present value -£57,112

NPV Project B

Year Inflow PV Factor

Inflow by considering

pv factor

1 £86,000 0.909 £78,174

2 £85,000 0.826 £70,210

3 £71,000 0.751 £53,321

4 £54,000 0.683 £36,882

Total inflow £296,000.00 £238,587

Less: Initial investment £280,000

Net present value -£41,413.00

NPV shows actual value after 4 year from initial investment. It is exhibit that initail

investment in proposal 1 is become £222888 which show loss of the £57112 amount while

proposal 2 shows NPV £23857 which also shows loss of the £41413 (Bhaird, C., 2010).

Therefore, there is most appropriate proposal will be project B because loss of value is lower

than project A.

1. Accounting rate of return – It is determined the profit earn by initial investment which

spend in new project (Brotman, 2010). Thus, it is evaluation of the profit earn by the

initial investment. It determination of benefit arising from project as percentage of the

initial capital cost.

ARR = [average annual value/ initial capital costs]*100

Advantages –

◦ It is simple to calculated as well as easy to understand. Thus, many of the business

use as planning purpose.

◦ It is base on the profit earn so it is easy to understand.

Disadvantage –

5

NPV Project A

year inflow PV Factor

Inflow by considering

pv factor

1 £75,000 0.909 £68,175

2 £80,000 0.826 £66,080

3 £68,000 0.751 £51,068

4 £55,000 0.683 £37,565

Total inflow £278,000 £222,888

Less: Initial investment £280,000

Net present value -£57,112

NPV Project B

Year Inflow PV Factor

Inflow by considering

pv factor

1 £86,000 0.909 £78,174

2 £85,000 0.826 £70,210

3 £71,000 0.751 £53,321

4 £54,000 0.683 £36,882

Total inflow £296,000.00 £238,587

Less: Initial investment £280,000

Net present value -£41,413.00

NPV shows actual value after 4 year from initial investment. It is exhibit that initail

investment in proposal 1 is become £222888 which show loss of the £57112 amount while

proposal 2 shows NPV £23857 which also shows loss of the £41413 (Bhaird, C., 2010).

Therefore, there is most appropriate proposal will be project B because loss of value is lower

than project A.

1. Accounting rate of return – It is determined the profit earn by initial investment which

spend in new project (Brotman, 2010). Thus, it is evaluation of the profit earn by the

initial investment. It determination of benefit arising from project as percentage of the

initial capital cost.

ARR = [average annual value/ initial capital costs]*100

Advantages –

◦ It is simple to calculated as well as easy to understand. Thus, many of the business

use as planning purpose.

◦ It is base on the profit earn so it is easy to understand.

Disadvantage –

5

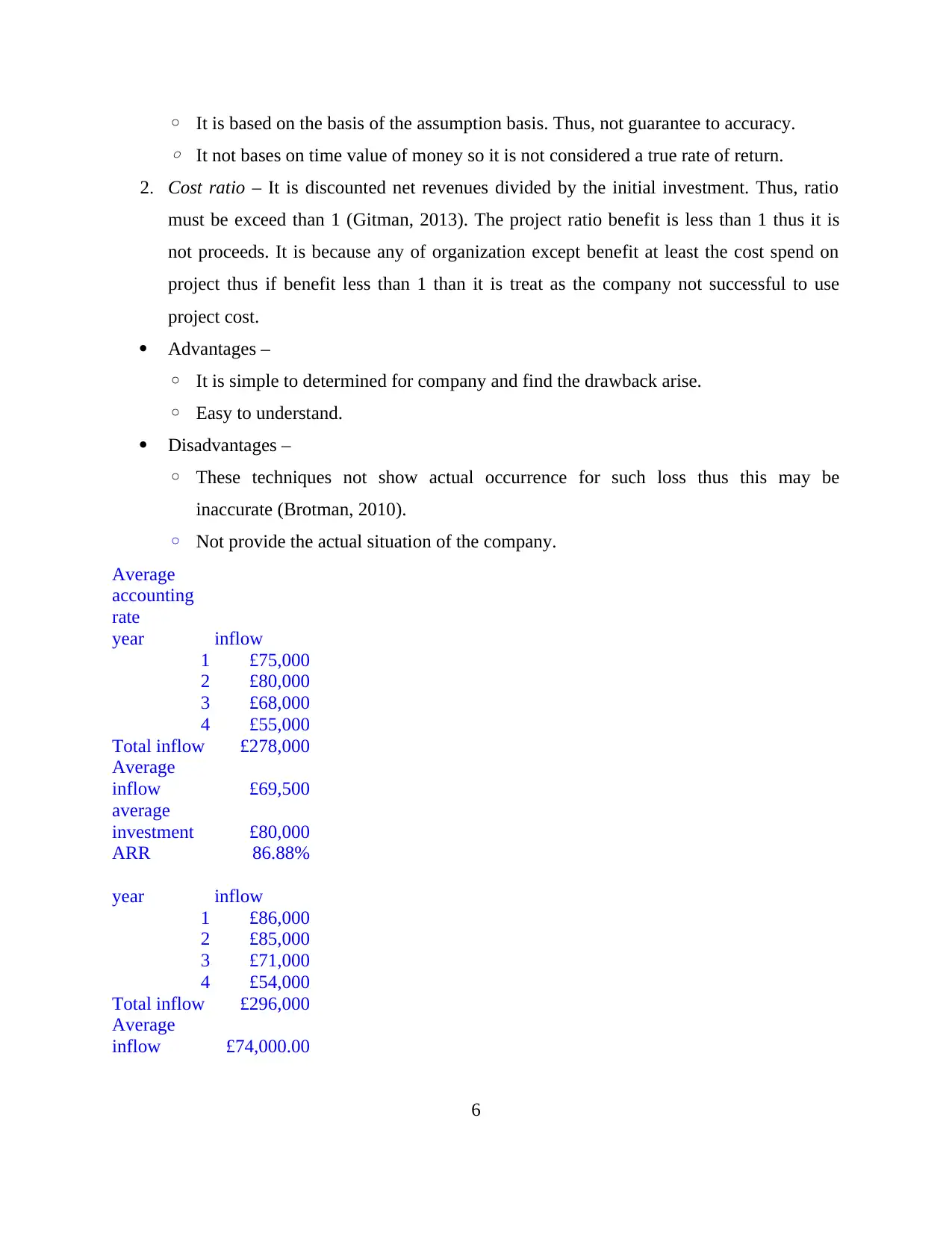

◦ It is based on the basis of the assumption basis. Thus, not guarantee to accuracy.

◦ It not bases on time value of money so it is not considered a true rate of return.

2. Cost ratio – It is discounted net revenues divided by the initial investment. Thus, ratio

must be exceed than 1 (Gitman, 2013). The project ratio benefit is less than 1 thus it is

not proceeds. It is because any of organization except benefit at least the cost spend on

project thus if benefit less than 1 than it is treat as the company not successful to use

project cost.

Advantages –

◦ It is simple to determined for company and find the drawback arise.

◦ Easy to understand.

Disadvantages –

◦ These techniques not show actual occurrence for such loss thus this may be

inaccurate (Brotman, 2010).

◦ Not provide the actual situation of the company.

Average

accounting

rate

year inflow

1 £75,000

2 £80,000

3 £68,000

4 £55,000

Total inflow £278,000

Average

inflow £69,500

average

investment £80,000

ARR 86.88%

year inflow

1 £86,000

2 £85,000

3 £71,000

4 £54,000

Total inflow £296,000

Average

inflow £74,000.00

6

◦ It not bases on time value of money so it is not considered a true rate of return.

2. Cost ratio – It is discounted net revenues divided by the initial investment. Thus, ratio

must be exceed than 1 (Gitman, 2013). The project ratio benefit is less than 1 thus it is

not proceeds. It is because any of organization except benefit at least the cost spend on

project thus if benefit less than 1 than it is treat as the company not successful to use

project cost.

Advantages –

◦ It is simple to determined for company and find the drawback arise.

◦ Easy to understand.

Disadvantages –

◦ These techniques not show actual occurrence for such loss thus this may be

inaccurate (Brotman, 2010).

◦ Not provide the actual situation of the company.

Average

accounting

rate

year inflow

1 £75,000

2 £80,000

3 £68,000

4 £55,000

Total inflow £278,000

Average

inflow £69,500

average

investment £80,000

ARR 86.88%

year inflow

1 £86,000

2 £85,000

3 £71,000

4 £54,000

Total inflow £296,000

Average

inflow £74,000.00

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

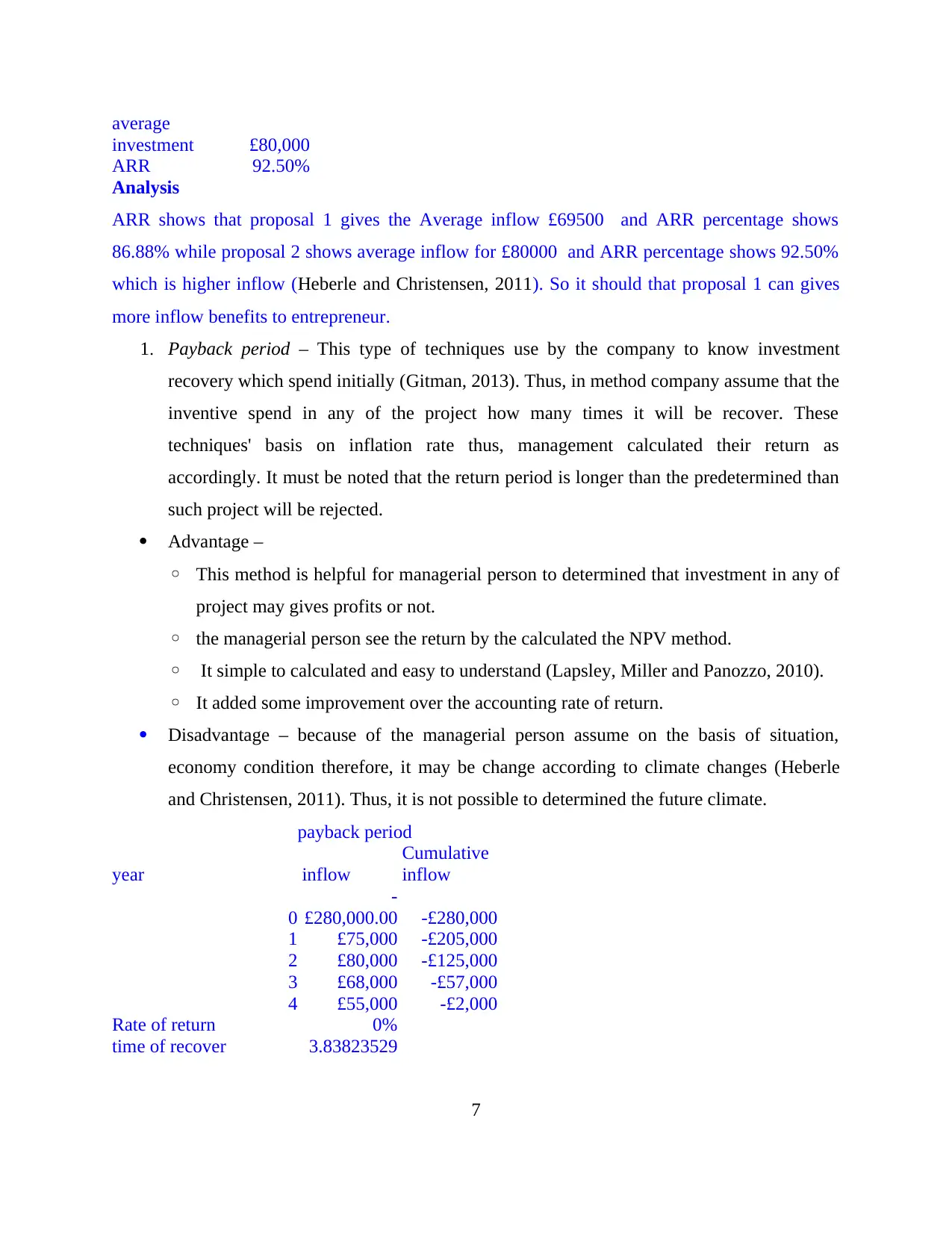

average

investment £80,000

ARR 92.50%

Analysis

ARR shows that proposal 1 gives the Average inflow £69500 and ARR percentage shows

86.88% while proposal 2 shows average inflow for £80000 and ARR percentage shows 92.50%

which is higher inflow (Heberle and Christensen, 2011). So it should that proposal 1 can gives

more inflow benefits to entrepreneur.

1. Payback period – This type of techniques use by the company to know investment

recovery which spend initially (Gitman, 2013). Thus, in method company assume that the

inventive spend in any of the project how many times it will be recover. These

techniques' basis on inflation rate thus, management calculated their return as

accordingly. It must be noted that the return period is longer than the predetermined than

such project will be rejected.

Advantage –

◦ This method is helpful for managerial person to determined that investment in any of

project may gives profits or not.

◦ the managerial person see the return by the calculated the NPV method.

◦ It simple to calculated and easy to understand (Lapsley, Miller and Panozzo, 2010).

◦ It added some improvement over the accounting rate of return.

Disadvantage – because of the managerial person assume on the basis of situation,

economy condition therefore, it may be change according to climate changes (Heberle

and Christensen, 2011). Thus, it is not possible to determined the future climate.

payback period

year inflow

Cumulative

inflow

0

-

£280,000.00 -£280,000

1 £75,000 -£205,000

2 £80,000 -£125,000

3 £68,000 -£57,000

4 £55,000 -£2,000

Rate of return 0%

time of recover 3.83823529

7

investment £80,000

ARR 92.50%

Analysis

ARR shows that proposal 1 gives the Average inflow £69500 and ARR percentage shows

86.88% while proposal 2 shows average inflow for £80000 and ARR percentage shows 92.50%

which is higher inflow (Heberle and Christensen, 2011). So it should that proposal 1 can gives

more inflow benefits to entrepreneur.

1. Payback period – This type of techniques use by the company to know investment

recovery which spend initially (Gitman, 2013). Thus, in method company assume that the

inventive spend in any of the project how many times it will be recover. These

techniques' basis on inflation rate thus, management calculated their return as

accordingly. It must be noted that the return period is longer than the predetermined than

such project will be rejected.

Advantage –

◦ This method is helpful for managerial person to determined that investment in any of

project may gives profits or not.

◦ the managerial person see the return by the calculated the NPV method.

◦ It simple to calculated and easy to understand (Lapsley, Miller and Panozzo, 2010).

◦ It added some improvement over the accounting rate of return.

Disadvantage – because of the managerial person assume on the basis of situation,

economy condition therefore, it may be change according to climate changes (Heberle

and Christensen, 2011). Thus, it is not possible to determined the future climate.

payback period

year inflow

Cumulative

inflow

0

-

£280,000.00 -£280,000

1 £75,000 -£205,000

2 £80,000 -£125,000

3 £68,000 -£57,000

4 £55,000 -£2,000

Rate of return 0%

time of recover 3.83823529

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

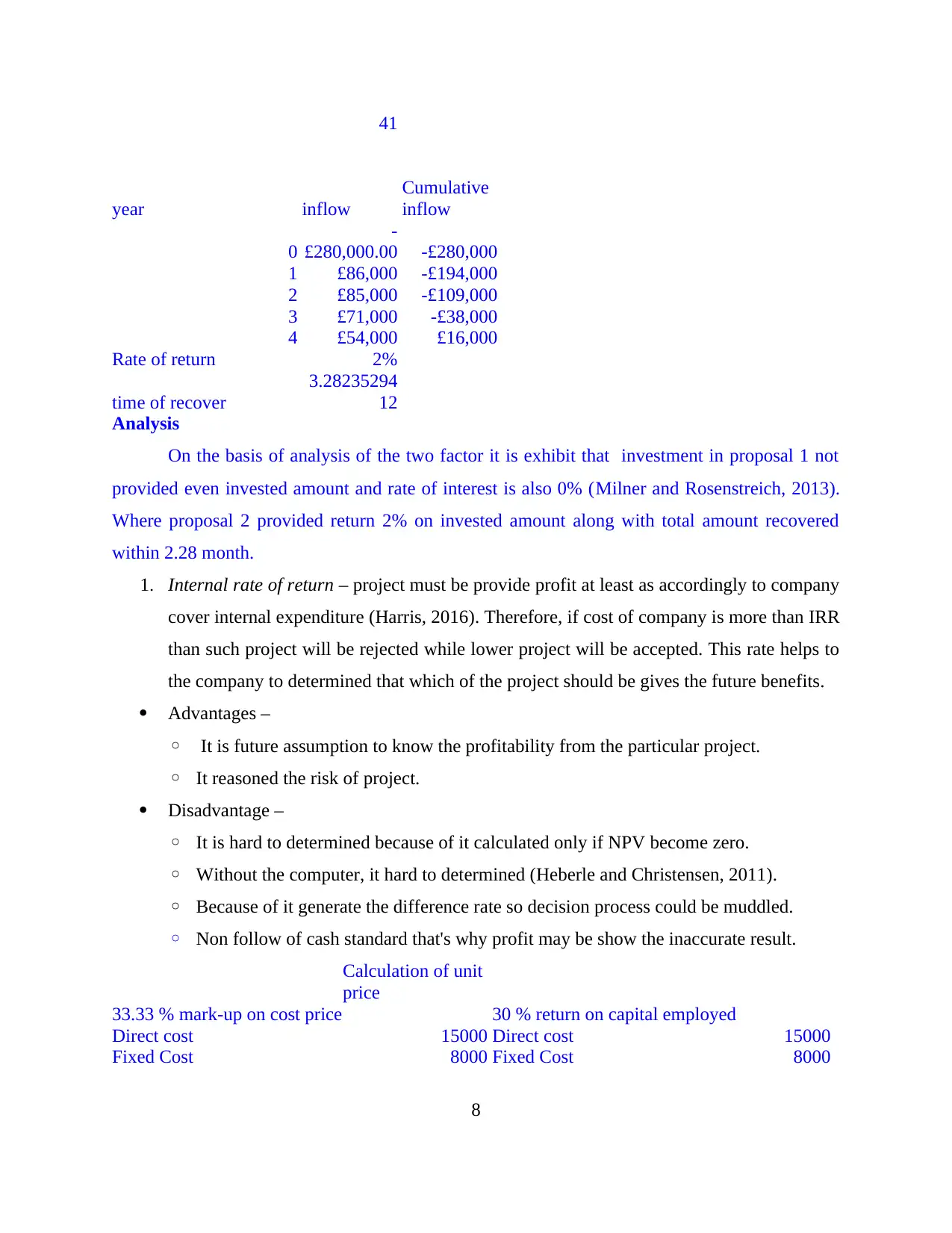

41

year inflow

Cumulative

inflow

0

-

£280,000.00 -£280,000

1 £86,000 -£194,000

2 £85,000 -£109,000

3 £71,000 -£38,000

4 £54,000 £16,000

Rate of return 2%

time of recover

3.28235294

12

Analysis

On the basis of analysis of the two factor it is exhibit that investment in proposal 1 not

provided even invested amount and rate of interest is also 0% (Milner and Rosenstreich, 2013).

Where proposal 2 provided return 2% on invested amount along with total amount recovered

within 2.28 month.

1. Internal rate of return – project must be provide profit at least as accordingly to company

cover internal expenditure (Harris, 2016). Therefore, if cost of company is more than IRR

than such project will be rejected while lower project will be accepted. This rate helps to

the company to determined that which of the project should be gives the future benefits.

Advantages –

◦ It is future assumption to know the profitability from the particular project.

◦ It reasoned the risk of project.

Disadvantage –

◦ It is hard to determined because of it calculated only if NPV become zero.

◦ Without the computer, it hard to determined (Heberle and Christensen, 2011).

◦ Because of it generate the difference rate so decision process could be muddled.

◦ Non follow of cash standard that's why profit may be show the inaccurate result.

Calculation of unit

price

33.33 % mark-up on cost price 30 % return on capital employed

Direct cost 15000 Direct cost 15000

Fixed Cost 8000 Fixed Cost 8000

8

year inflow

Cumulative

inflow

0

-

£280,000.00 -£280,000

1 £86,000 -£194,000

2 £85,000 -£109,000

3 £71,000 -£38,000

4 £54,000 £16,000

Rate of return 2%

time of recover

3.28235294

12

Analysis

On the basis of analysis of the two factor it is exhibit that investment in proposal 1 not

provided even invested amount and rate of interest is also 0% (Milner and Rosenstreich, 2013).

Where proposal 2 provided return 2% on invested amount along with total amount recovered

within 2.28 month.

1. Internal rate of return – project must be provide profit at least as accordingly to company

cover internal expenditure (Harris, 2016). Therefore, if cost of company is more than IRR

than such project will be rejected while lower project will be accepted. This rate helps to

the company to determined that which of the project should be gives the future benefits.

Advantages –

◦ It is future assumption to know the profitability from the particular project.

◦ It reasoned the risk of project.

Disadvantage –

◦ It is hard to determined because of it calculated only if NPV become zero.

◦ Without the computer, it hard to determined (Heberle and Christensen, 2011).

◦ Because of it generate the difference rate so decision process could be muddled.

◦ Non follow of cash standard that's why profit may be show the inaccurate result.

Calculation of unit

price

33.33 % mark-up on cost price 30 % return on capital employed

Direct cost 15000 Direct cost 15000

Fixed Cost 8000 Fixed Cost 8000

8

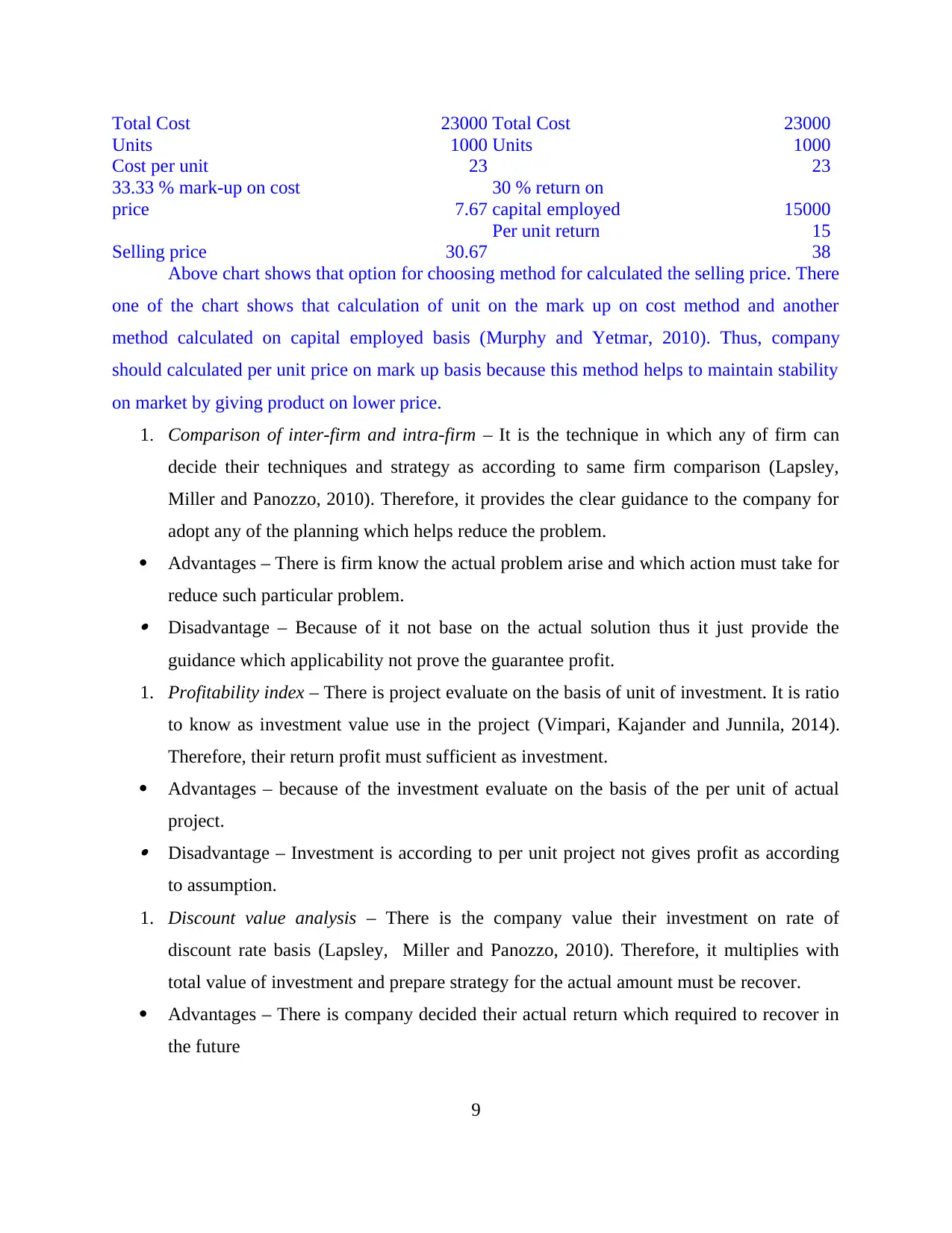

Total Cost 23000 Total Cost 23000

Units 1000 Units 1000

Cost per unit 23 23

33.33 % mark-up on cost

price 7.67

30 % return on

capital employed 15000

Per unit return 15

Selling price 30.67 38

Above chart shows that option for choosing method for calculated the selling price. There

one of the chart shows that calculation of unit on the mark up on cost method and another

method calculated on capital employed basis (Murphy and Yetmar, 2010). Thus, company

should calculated per unit price on mark up basis because this method helps to maintain stability

on market by giving product on lower price.

1. Comparison of inter-firm and intra-firm – It is the technique in which any of firm can

decide their techniques and strategy as according to same firm comparison (Lapsley,

Miller and Panozzo, 2010). Therefore, it provides the clear guidance to the company for

adopt any of the planning which helps reduce the problem.

Advantages – There is firm know the actual problem arise and which action must take for

reduce such particular problem. Disadvantage – Because of it not base on the actual solution thus it just provide the

guidance which applicability not prove the guarantee profit.

1. Profitability index – There is project evaluate on the basis of unit of investment. It is ratio

to know as investment value use in the project (Vimpari, Kajander and Junnila, 2014).

Therefore, their return profit must sufficient as investment.

Advantages – because of the investment evaluate on the basis of the per unit of actual

project. Disadvantage – Investment is according to per unit project not gives profit as according

to assumption.

1. Discount value analysis – There is the company value their investment on rate of

discount rate basis (Lapsley, Miller and Panozzo, 2010). Therefore, it multiplies with

total value of investment and prepare strategy for the actual amount must be recover.

Advantages – There is company decided their actual return which required to recover in

the future

9

Units 1000 Units 1000

Cost per unit 23 23

33.33 % mark-up on cost

price 7.67

30 % return on

capital employed 15000

Per unit return 15

Selling price 30.67 38

Above chart shows that option for choosing method for calculated the selling price. There

one of the chart shows that calculation of unit on the mark up on cost method and another

method calculated on capital employed basis (Murphy and Yetmar, 2010). Thus, company

should calculated per unit price on mark up basis because this method helps to maintain stability

on market by giving product on lower price.

1. Comparison of inter-firm and intra-firm – It is the technique in which any of firm can

decide their techniques and strategy as according to same firm comparison (Lapsley,

Miller and Panozzo, 2010). Therefore, it provides the clear guidance to the company for

adopt any of the planning which helps reduce the problem.

Advantages – There is firm know the actual problem arise and which action must take for

reduce such particular problem. Disadvantage – Because of it not base on the actual solution thus it just provide the

guidance which applicability not prove the guarantee profit.

1. Profitability index – There is project evaluate on the basis of unit of investment. It is ratio

to know as investment value use in the project (Vimpari, Kajander and Junnila, 2014).

Therefore, their return profit must sufficient as investment.

Advantages – because of the investment evaluate on the basis of the per unit of actual

project. Disadvantage – Investment is according to per unit project not gives profit as according

to assumption.

1. Discount value analysis – There is the company value their investment on rate of

discount rate basis (Lapsley, Miller and Panozzo, 2010). Therefore, it multiplies with

total value of investment and prepare strategy for the actual amount must be recover.

Advantages – There is company decided their actual return which required to recover in

the future

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Disadvantage – because of the DRR is base on the assumption basis thus it not

guaranteed to success.

1. Real option analysis – In this manager, consider all the option and choose the option

which gives the more cash inflow (Milner and Rosenstreich, 2013). Therefore, cash

inflow must be on the basis of NPV value.

Risk management techniques in capital appraisal

Mini-max regret – It is one of the strategy to decide that what action taken if any of the adverse

situation arise cause by the wrong decision (Murphy and Yetmar, 2010). This type of action arise

by the wrongfulness of the managerial person decision making.

1. Sensitivity analysis – It is measure by the What if analysis (Hamad, 2016). There is the

objective and the strategy are in the written form which severs to all at one objective.

2. Maxi-mine – this of the decision work on the maximum profit with minimum alternative.

There is director assume the worse situation arise by the different decision and finally

choose accurate worst situation arise in the company (Vimpari, Kajander and Junnila,

2014).

3. Maxim-ax – This the alternative method to choose the highest alternative outcome arise

by the technique use (Milner and Rosenstreich, 2013). There is prepared table to choose

the different possible outcome. That is best for the managerial person. Therefore, it is

assumed analysis of outcome choose by the analysis of study of different situation.

4. Cost of uncertainty – In this the company maintain one of the account for adverse

situation arise at the time of the future occurrence (Prorokowski, 2011). Therefore, it is

essential to maintain the one of the small amount for the uncertain situation which arise

by future uncertainty.

5. Maintain loss - There is managerial person except possible loss from the outcome. There

is small part get separate from the total expected profit because of it is necessary in to

being secure in adverse situation (Nguyen, 2010). This because any of the company

should assume negative occurrence by the techniques otherwise it may gives large

amount of loss to company. Hence, it is called the managerial techniques.

6. Forecasting – There is management forecast the situation which assumed to happened

arise in the future and evaluate the decision as best which secure the investment on the

10

guaranteed to success.

1. Real option analysis – In this manager, consider all the option and choose the option

which gives the more cash inflow (Milner and Rosenstreich, 2013). Therefore, cash

inflow must be on the basis of NPV value.

Risk management techniques in capital appraisal

Mini-max regret – It is one of the strategy to decide that what action taken if any of the adverse

situation arise cause by the wrong decision (Murphy and Yetmar, 2010). This type of action arise

by the wrongfulness of the managerial person decision making.

1. Sensitivity analysis – It is measure by the What if analysis (Hamad, 2016). There is the

objective and the strategy are in the written form which severs to all at one objective.

2. Maxi-mine – this of the decision work on the maximum profit with minimum alternative.

There is director assume the worse situation arise by the different decision and finally

choose accurate worst situation arise in the company (Vimpari, Kajander and Junnila,

2014).

3. Maxim-ax – This the alternative method to choose the highest alternative outcome arise

by the technique use (Milner and Rosenstreich, 2013). There is prepared table to choose

the different possible outcome. That is best for the managerial person. Therefore, it is

assumed analysis of outcome choose by the analysis of study of different situation.

4. Cost of uncertainty – In this the company maintain one of the account for adverse

situation arise at the time of the future occurrence (Prorokowski, 2011). Therefore, it is

essential to maintain the one of the small amount for the uncertain situation which arise

by future uncertainty.

5. Maintain loss - There is managerial person except possible loss from the outcome. There

is small part get separate from the total expected profit because of it is necessary in to

being secure in adverse situation (Nguyen, 2010). This because any of the company

should assume negative occurrence by the techniques otherwise it may gives large

amount of loss to company. Hence, it is called the managerial techniques.

6. Forecasting – There is management forecast the situation which assumed to happened

arise in the future and evaluate the decision as best which secure the investment on the

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

basis of NPA (Nguyen, 2010). It is important techniques which use in any type of the

organization to determined by the higher authority of the company (Allen and Economy,

2011). Therefore, it is the method to applied by the higher authority of the company for

determine the future uncertainty that aware to the management for use any of the

techniques with determined future occurrence (Hamad, 2016).

7. Brainstorming techniques – In this type of the technique, management use group

discussion with subordinate or interest person and seek the problem arising from

particular situation from the selective techniques (Prorokowski, 2011). This is because

such list shown the actual problem thus director use it as priority basis. Because of the

every person view may be vary in the particular thing but ti helps to access the risk as

possible. Therefore, it reduces the possible damages.

CONCLUSION

Summarise of above study shows that appraisal technique are more importance in

investment. It is used by management person for taking best investment decision. It is helps to

know that which type of investment gives maximum return in the future. Therefore, management

use various kind of techniques for determined best investment for their enterprise. Hence, in this

report added example which shows that management used techniques for choosing involvement

technique. Report shows that investment appraisal techniques used to provide maximum benefit

to organisation. As per given examples management should choose proposal 1 because this

proposal gives maximum benefit in all technique along with it is giving more profitability to

company for long time.

The present report concluded that various type of the appraisal technique use by

managerial person in the organisation. This helps to investment in right place with choose

accurate techniques that's why enterprise earn maximum profit. Thus, it chooses by company

with analysis of their actual position and also determined the worse situation. It also this report

also contain the adverse situation arise if decision making fail to apply proper way. Hence, their

report show that any of the strategy adopted by company must be focus on the adverse situation

arise if it fails to do. Thus, this report helps to better understanding of investment appraisal

strategy.

11

organization to determined by the higher authority of the company (Allen and Economy,

2011). Therefore, it is the method to applied by the higher authority of the company for

determine the future uncertainty that aware to the management for use any of the

techniques with determined future occurrence (Hamad, 2016).

7. Brainstorming techniques – In this type of the technique, management use group

discussion with subordinate or interest person and seek the problem arising from

particular situation from the selective techniques (Prorokowski, 2011). This is because

such list shown the actual problem thus director use it as priority basis. Because of the

every person view may be vary in the particular thing but ti helps to access the risk as

possible. Therefore, it reduces the possible damages.

CONCLUSION

Summarise of above study shows that appraisal technique are more importance in

investment. It is used by management person for taking best investment decision. It is helps to

know that which type of investment gives maximum return in the future. Therefore, management

use various kind of techniques for determined best investment for their enterprise. Hence, in this

report added example which shows that management used techniques for choosing involvement

technique. Report shows that investment appraisal techniques used to provide maximum benefit

to organisation. As per given examples management should choose proposal 1 because this

proposal gives maximum benefit in all technique along with it is giving more profitability to

company for long time.

The present report concluded that various type of the appraisal technique use by

managerial person in the organisation. This helps to investment in right place with choose

accurate techniques that's why enterprise earn maximum profit. Thus, it chooses by company

with analysis of their actual position and also determined the worse situation. It also this report

also contain the adverse situation arise if decision making fail to apply proper way. Hence, their

report show that any of the strategy adopted by company must be focus on the adverse situation

arise if it fails to do. Thus, this report helps to better understanding of investment appraisal

strategy.

11

REFERENCES

Books and journals

Allen, K. and Economy, P., 2011. Complete MBA For Dummies. John Wiley & Sons.

Bennouna, K., Meredith, G. G. and Marchant, T., 2010. Improved capital budgeting decision

making: evidence from Canada.Management Decision. 48(2). pp.225–247.

Bhaird, C. M. A., 2010. Resourcing Small and Medium Sized Enterprises: A Financial Growth

Life Cycle Approach. Springer.

Brotman, B. A., 2010. The impact of market conditions using appraisal models. Journal of

Property Investment & Finance. 28 (3). pp.237 – 242.

Gitman, J. L., 2013. Personal Financial Planning. Cengage Learning publication.

Heberle, L. C. and Christensen, I. M., 2011. US environmental governance and local climate

change mitigation policies: California's story. Management of Environmental Quality: An

International Journal. 22 (3). pp.317 – 329.

Lapsley, I, Miller, P. and Panozzo, F., 2010. Accounting for the city. Accounting, Auditing &

Accountability Journal. 23 (3). pp.305 – 324.

Milner, T. and Rosenstreich, D., 2013. Insights into mature consumers of financial services.

Journal of Consumer Marketing. 30 (3). pp.248 – 257.

Murphy, S. D. andYetmar, S., 2010. Personal financial planning attitudes: a preliminary study of

graduate students. Management Research Review. 33 8, pp.811–817.

Nguyen, K., 2010. Financial Statement Fraud: Motives, Methods, Cases and Detection.

Universal-Publishers.

Prorokowski, L., 2011. Trading strategies of individual investors in times of financial crisis: An

example from the Central European emerging stock market of Poland. Qualitative

Research in Financial Markets. 3 (1). pp.34 – 50.

Vimpari, J., Kajander, J. K. and Junnila, S., 2014. Valuing flexibility in a retrofit investment.

Journal of Corporate Real Estate. 16 (1) pp.3 – 21.

online

Hamad, S., 2016. Financial analysis and management. [online]. Available through

<http://www.academia.edu/8012185/Financial_Management_Investment_Appraisal_Tech

niques>. [Access on 4 May 2016].

12

Books and journals

Allen, K. and Economy, P., 2011. Complete MBA For Dummies. John Wiley & Sons.

Bennouna, K., Meredith, G. G. and Marchant, T., 2010. Improved capital budgeting decision

making: evidence from Canada.Management Decision. 48(2). pp.225–247.

Bhaird, C. M. A., 2010. Resourcing Small and Medium Sized Enterprises: A Financial Growth

Life Cycle Approach. Springer.

Brotman, B. A., 2010. The impact of market conditions using appraisal models. Journal of

Property Investment & Finance. 28 (3). pp.237 – 242.

Gitman, J. L., 2013. Personal Financial Planning. Cengage Learning publication.

Heberle, L. C. and Christensen, I. M., 2011. US environmental governance and local climate

change mitigation policies: California's story. Management of Environmental Quality: An

International Journal. 22 (3). pp.317 – 329.

Lapsley, I, Miller, P. and Panozzo, F., 2010. Accounting for the city. Accounting, Auditing &

Accountability Journal. 23 (3). pp.305 – 324.

Milner, T. and Rosenstreich, D., 2013. Insights into mature consumers of financial services.

Journal of Consumer Marketing. 30 (3). pp.248 – 257.

Murphy, S. D. andYetmar, S., 2010. Personal financial planning attitudes: a preliminary study of

graduate students. Management Research Review. 33 8, pp.811–817.

Nguyen, K., 2010. Financial Statement Fraud: Motives, Methods, Cases and Detection.

Universal-Publishers.

Prorokowski, L., 2011. Trading strategies of individual investors in times of financial crisis: An

example from the Central European emerging stock market of Poland. Qualitative

Research in Financial Markets. 3 (1). pp.34 – 50.

Vimpari, J., Kajander, J. K. and Junnila, S., 2014. Valuing flexibility in a retrofit investment.

Journal of Corporate Real Estate. 16 (1) pp.3 – 21.

online

Hamad, S., 2016. Financial analysis and management. [online]. Available through

<http://www.academia.edu/8012185/Financial_Management_Investment_Appraisal_Tech

niques>. [Access on 4 May 2016].

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.