Financial and Economic Literacy for Managers Report - University Name

VerifiedAdded on 2021/04/17

|20

|4304

|25

Report

AI Summary

This report provides a detailed analysis of financial and economic literacy for managers. It begins by defining market structures, including perfect competition, monopoly, oligopoly, and monopolistic competition. The report then explores basic concepts of small and medium enterprises (SMEs) and multinational corporations (MNCs), followed by a discussion of growth strategies. The second section examines the concepts of demand and supply, and the monetary policy of the Bank of England in relation to the UK housing market. The report also covers key macroeconomic indicators such as GDP, employment rate, money supply, and inflation rate, along with their trends in the UK over the last five years. Empirical evidence and relevant figures are included to support the analysis, making it a comprehensive overview of business economics and its practical applications.

Running head: FINANCIAL AND ECONOMIC LITERACY FOR MANAGERS

Financial and Economic Literacy for Managers

University Name

Student Name

Authors’ Note

Financial and Economic Literacy for Managers

University Name

Student Name

Authors’ Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

FINANCIAL AND ECONOMIC LITERACY FOR MANAGERS

Table of Contents

Solution to Question 1:...............................................................................................................2

Solution to Question 2:...............................................................................................................6

Solution to Question 3:...............................................................................................................9

Solution to Question 4:.............................................................................................................12

Solution to Question 5:.............................................................................................................14

References................................................................................................................................18

FINANCIAL AND ECONOMIC LITERACY FOR MANAGERS

Table of Contents

Solution to Question 1:...............................................................................................................2

Solution to Question 2:...............................................................................................................6

Solution to Question 3:...............................................................................................................9

Solution to Question 4:.............................................................................................................12

Solution to Question 5:.............................................................................................................14

References................................................................................................................................18

3

FINANCIAL AND ECONOMIC LITERACY FOR MANAGERS

Solution to Question 1:

Business economics concepts of market structure

As rightly indicated by Lusardi and Mitchell (2014), market structure can be defined as

organizational as well as other features of a market that in turn elucidates the nature of

competition along with pricing policy pursued in the market. Market Structure refers to a

categorisation system for the important market traits, counting the total number of firms,

overall similarity of products marketed and the ease of entry as well as exit from the specific

market.

The categories of market structure include the following:

Perfect Competition: This market is characterised by large number of business firms,

homogeneous products, and firm’s freedom of entry and exit from the market (Fernandes et

al. 2014).

Monopoly: Monopoly market structure refers to one where there is only one business firm

prevailing in a specific segment. Essentially, a specific firm dominates the entire market and

there are barriers for entrance of new firms along with supernormal profit.

Oligopoly: An industry that is dominated by a few number of business concerns. Essentially,

it can be said that oligopoly is a specific market structure in which few firms dominate and

the time when a particular market is shared between corporations, it is said to be highly

concentrated (Mitchell and Lusardi 2015).

Monopolistic Competition: Monopolistic competition refers to a specific market structure

that combines diverse components of monopoly as well as competitive markets. In itself,

FINANCIAL AND ECONOMIC LITERACY FOR MANAGERS

Solution to Question 1:

Business economics concepts of market structure

As rightly indicated by Lusardi and Mitchell (2014), market structure can be defined as

organizational as well as other features of a market that in turn elucidates the nature of

competition along with pricing policy pursued in the market. Market Structure refers to a

categorisation system for the important market traits, counting the total number of firms,

overall similarity of products marketed and the ease of entry as well as exit from the specific

market.

The categories of market structure include the following:

Perfect Competition: This market is characterised by large number of business firms,

homogeneous products, and firm’s freedom of entry and exit from the market (Fernandes et

al. 2014).

Monopoly: Monopoly market structure refers to one where there is only one business firm

prevailing in a specific segment. Essentially, a specific firm dominates the entire market and

there are barriers for entrance of new firms along with supernormal profit.

Oligopoly: An industry that is dominated by a few number of business concerns. Essentially,

it can be said that oligopoly is a specific market structure in which few firms dominate and

the time when a particular market is shared between corporations, it is said to be highly

concentrated (Mitchell and Lusardi 2015).

Monopolistic Competition: Monopolistic competition refers to a specific market structure

that combines diverse components of monopoly as well as competitive markets. In itself,

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4

FINANCIAL AND ECONOMIC LITERACY FOR MANAGERSmonopolistic competitive market can be characterised by freedom of entry as well as exit, but

corporations can differentiate between products of the firm (Allgood and Walstad 2016).

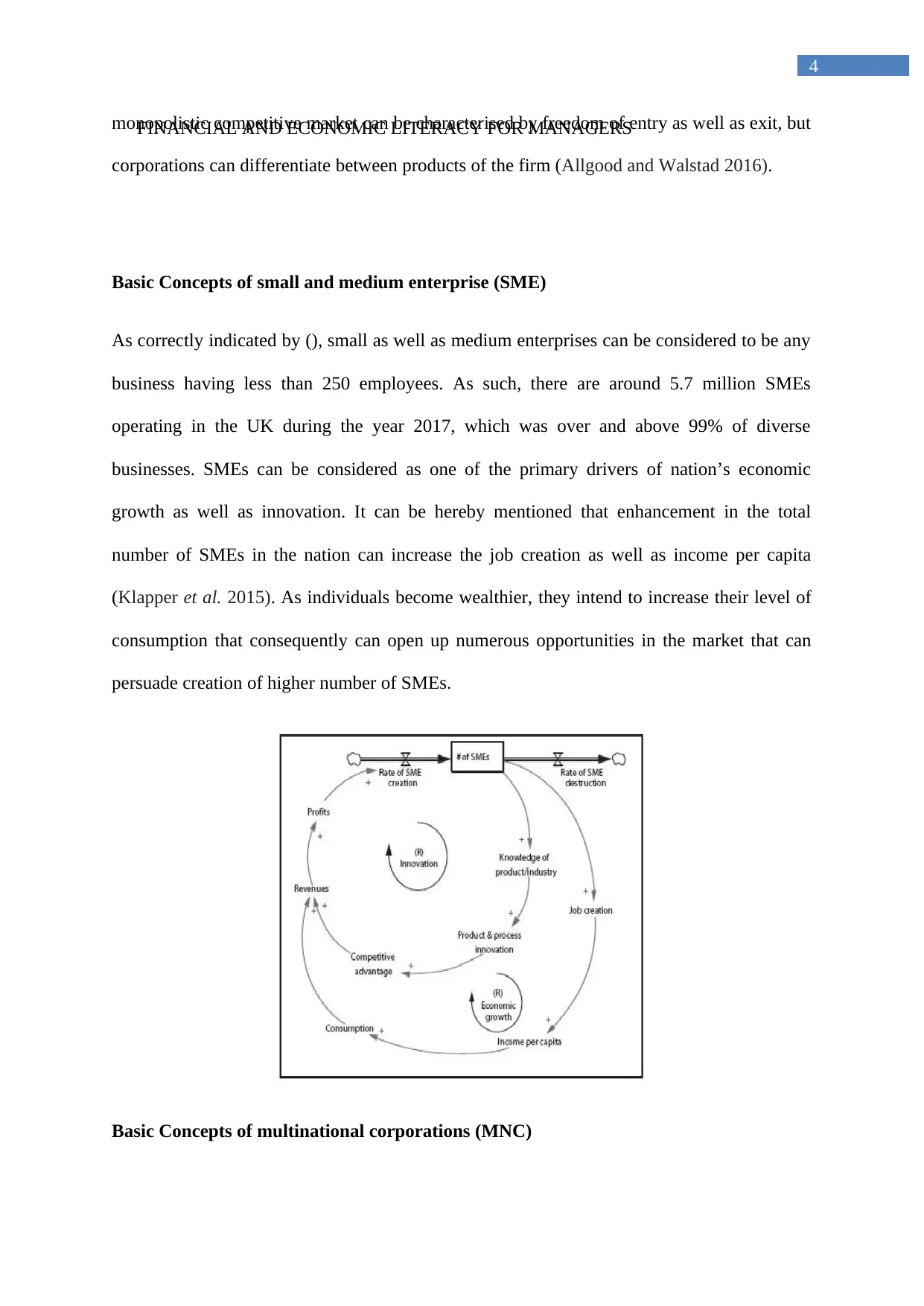

Basic Concepts of small and medium enterprise (SME)

As correctly indicated by (), small as well as medium enterprises can be considered to be any

business having less than 250 employees. As such, there are around 5.7 million SMEs

operating in the UK during the year 2017, which was over and above 99% of diverse

businesses. SMEs can be considered as one of the primary drivers of nation’s economic

growth as well as innovation. It can be hereby mentioned that enhancement in the total

number of SMEs in the nation can increase the job creation as well as income per capita

(Klapper et al. 2015). As individuals become wealthier, they intend to increase their level of

consumption that consequently can open up numerous opportunities in the market that can

persuade creation of higher number of SMEs.

Basic Concepts of multinational corporations (MNC)

FINANCIAL AND ECONOMIC LITERACY FOR MANAGERSmonopolistic competitive market can be characterised by freedom of entry as well as exit, but

corporations can differentiate between products of the firm (Allgood and Walstad 2016).

Basic Concepts of small and medium enterprise (SME)

As correctly indicated by (), small as well as medium enterprises can be considered to be any

business having less than 250 employees. As such, there are around 5.7 million SMEs

operating in the UK during the year 2017, which was over and above 99% of diverse

businesses. SMEs can be considered as one of the primary drivers of nation’s economic

growth as well as innovation. It can be hereby mentioned that enhancement in the total

number of SMEs in the nation can increase the job creation as well as income per capita

(Klapper et al. 2015). As individuals become wealthier, they intend to increase their level of

consumption that consequently can open up numerous opportunities in the market that can

persuade creation of higher number of SMEs.

Basic Concepts of multinational corporations (MNC)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

FINANCIAL AND ECONOMIC LITERACY FOR MANAGERSA multinational corporation can be considered to be an enterprise that undertakes business

functions in more than one nation. This necessarily extends both manufacturing and

manufacturing operation by means of a network of diverse branches as well as subsidiaries

that are referred to as foreign affiliates (Singh 2014). The characteristics of MNC comprise of

large sized firms, universal functions, centralized system of control, and higher level of brand

equity, advanced technology and international market.

Basic Concepts of growth strategy

Growth strategy aims at winning higher share of market, sometimes even at costs of firm’s

short term income. Growth strategy of a business refers to diverse methods a particular can

utilize to expand their business and it is largely dependent upon financial circumstances,

competition and even government regulation. In essence, growth stratagems for retail

business basically concentrates on the subsisting business comprises spectrum of

intensification of the present business scope, reasonable extension and strategic

diversification (Farnham 2014). Also, management of the retail firms can develop growth

strategy of the firm by taking into consideration the Ansoff’s Strategy that entails product

development, diversification, market development and market penetration.

Empirical Evidence: As per the report presented by Hirschey (2016), growth is normally

one of the most important agenda for the chief executive officers of firms operating in UK.

Corporations target aggressive strategies of growth in response to particular structural shifts

brought about by advanced technologies (Mankiw 2014). In the latest retail growth strategies,

around half (that is 42%) of retailers of UK said that they planned to merge with otherwise

acquire another business for entering into a new market space. For instance, Green King Plc

of particularly UK acquired the company Spirit Pub Plc operating in the UK, Carphone

FINANCIAL AND ECONOMIC LITERACY FOR MANAGERSA multinational corporation can be considered to be an enterprise that undertakes business

functions in more than one nation. This necessarily extends both manufacturing and

manufacturing operation by means of a network of diverse branches as well as subsidiaries

that are referred to as foreign affiliates (Singh 2014). The characteristics of MNC comprise of

large sized firms, universal functions, centralized system of control, and higher level of brand

equity, advanced technology and international market.

Basic Concepts of growth strategy

Growth strategy aims at winning higher share of market, sometimes even at costs of firm’s

short term income. Growth strategy of a business refers to diverse methods a particular can

utilize to expand their business and it is largely dependent upon financial circumstances,

competition and even government regulation. In essence, growth stratagems for retail

business basically concentrates on the subsisting business comprises spectrum of

intensification of the present business scope, reasonable extension and strategic

diversification (Farnham 2014). Also, management of the retail firms can develop growth

strategy of the firm by taking into consideration the Ansoff’s Strategy that entails product

development, diversification, market development and market penetration.

Empirical Evidence: As per the report presented by Hirschey (2016), growth is normally

one of the most important agenda for the chief executive officers of firms operating in UK.

Corporations target aggressive strategies of growth in response to particular structural shifts

brought about by advanced technologies (Mankiw 2014). In the latest retail growth strategies,

around half (that is 42%) of retailers of UK said that they planned to merge with otherwise

acquire another business for entering into a new market space. For instance, Green King Plc

of particularly UK acquired the company Spirit Pub Plc operating in the UK, Carphone

6

FINANCIAL AND ECONOMIC LITERACY FOR MANAGERSWarehouse Group PLC operating in the UK entered into a merger with Dixons Retail Plc of

the UK.

FINANCIAL AND ECONOMIC LITERACY FOR MANAGERSWarehouse Group PLC operating in the UK entered into a merger with Dixons Retail Plc of

the UK.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

FINANCIAL AND ECONOMIC LITERACY FOR MANAGERS

Solution to Question 2:

Business economics concept of demand and supply and monetary policy of the Bank of

England to particularly the UK Housing Market

Basic Concepts of demand and supply:

As rightly indicated by Agénor and Montiel (2015), supply and demand can be considered to

be fundamental notions of economics and is necessarily the backbone of the market economy.

Bernanke et al. (2015) mentions that demand indicates total amount of a specific product or

service that is desired by purchasers. Essentially, the quantity demanded can be regarded as

the total amount of a product individuals are willing to purchase at a specific price, the

association between price and quantity demand is referred to as the demand association.

Again, supply reflects the total amount a market can offer. Particularly, the quantity supplied

indicates towards total amount of specific product producers are keen to supply at the time of

receiving a specific price. The law of demand mentions that in case if all other facets remain

equal, the higher the price of a specific product, lower number of individuals will demand

that particular good.

FINANCIAL AND ECONOMIC LITERACY FOR MANAGERS

Solution to Question 2:

Business economics concept of demand and supply and monetary policy of the Bank of

England to particularly the UK Housing Market

Basic Concepts of demand and supply:

As rightly indicated by Agénor and Montiel (2015), supply and demand can be considered to

be fundamental notions of economics and is necessarily the backbone of the market economy.

Bernanke et al. (2015) mentions that demand indicates total amount of a specific product or

service that is desired by purchasers. Essentially, the quantity demanded can be regarded as

the total amount of a product individuals are willing to purchase at a specific price, the

association between price and quantity demand is referred to as the demand association.

Again, supply reflects the total amount a market can offer. Particularly, the quantity supplied

indicates towards total amount of specific product producers are keen to supply at the time of

receiving a specific price. The law of demand mentions that in case if all other facets remain

equal, the higher the price of a specific product, lower number of individuals will demand

that particular good.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

FINANCIAL AND ECONOMIC LITERACY FOR MANAGERSFigure: Demand and Supply

(Source: Ascari and Sbordone 2014)

Monetary Policy:

The monetary policy primarily includes utilization of rates of interest as well as other

monetary tools that can be used to influence the levels of consumer spending as well as

aggregate demand (AD). Particularly, monetary policy intends to stabilise the economic cycle

and maintain lower level of inflation and avert recessions. The aim of monetary policy is

lessening inflation. Low inflation can be regarded as a significant aim that can enable higher

investment during the long term period. In addition to this, aim of monetary policy is to

maintain stable growth rate of economy and low rate of unemployment. The monetary policy

of Bank of England maintains rate of interest and quantitative easing policy for attainment of

target of inflation and avoiding recession (Borio 2014). The rates of interest are increased for

the purpose of reducing demand and lowering inflation. Also, money supply is decreased for

decreasing demand and consequently inflation. On the other hand, in a bid to avert recession

in the economy, increase in money supply also augments both demand and firm’s investment.

Furthermore, rate of interest is lowered that in turn enhances consumer spending together

with investment. The monetary policy of UK is established by the Monetary Policy

Committee of the Bank of England. Essentially, they are self-governing in establishing rates

of interest but have to try and satisfy the inflation target of the government (Agénor and

Montiel 2015).

The monetary policy of UK is instituted by the Monetary Policy of the Bank of England. The

Bank of England can be considered to be independent of the government since the period of

1997 and monetary policy committee (MPC) has nine different members appointed by

government are responsible for formulation of the monetary policy. MPC take into account

FINANCIAL AND ECONOMIC LITERACY FOR MANAGERSFigure: Demand and Supply

(Source: Ascari and Sbordone 2014)

Monetary Policy:

The monetary policy primarily includes utilization of rates of interest as well as other

monetary tools that can be used to influence the levels of consumer spending as well as

aggregate demand (AD). Particularly, monetary policy intends to stabilise the economic cycle

and maintain lower level of inflation and avert recessions. The aim of monetary policy is

lessening inflation. Low inflation can be regarded as a significant aim that can enable higher

investment during the long term period. In addition to this, aim of monetary policy is to

maintain stable growth rate of economy and low rate of unemployment. The monetary policy

of Bank of England maintains rate of interest and quantitative easing policy for attainment of

target of inflation and avoiding recession (Borio 2014). The rates of interest are increased for

the purpose of reducing demand and lowering inflation. Also, money supply is decreased for

decreasing demand and consequently inflation. On the other hand, in a bid to avert recession

in the economy, increase in money supply also augments both demand and firm’s investment.

Furthermore, rate of interest is lowered that in turn enhances consumer spending together

with investment. The monetary policy of UK is established by the Monetary Policy

Committee of the Bank of England. Essentially, they are self-governing in establishing rates

of interest but have to try and satisfy the inflation target of the government (Agénor and

Montiel 2015).

The monetary policy of UK is instituted by the Monetary Policy of the Bank of England. The

Bank of England can be considered to be independent of the government since the period of

1997 and monetary policy committee (MPC) has nine different members appointed by

government are responsible for formulation of the monetary policy. MPC take into account

9

FINANCIAL AND ECONOMIC LITERACY FOR MANAGERScertain factors before arriving at rate decisions. The bank lending and figures on customer

credit includes equity levels withdrawal from the housing market and data on credit card

lending that supports demand of the customers. Furthermore, equity markets (prices of share)

and prices of houses are taken into consideration for the purpose of ascertainment of

household wealth that then feeds through to borrowing and retail spending (Bernanke et al.

2015). The monetary policy committee (MPC) necessarily has no official target for the yearly

house price inflation rate but the same has been criticised for not acting appropriately for

prevention of housing bubble till the period 2008. The alterations in the policy of the central

bank rates of interest also affect the housing market. Essentially, higher rates of interest

enhance the overall cost of mortgages and lessen overall demand for particularly housing.

Again, this can affect the overall wealth of the household and put a pressure on withdrawal of

equity.

Empirical evidence: As per reports published in Financial Times, Mark Carney, the central

banker tried to avert threats to economic recovery by imposition of limits on particularly

mortgage borrowing. The limitations on huge loans forced by the bank’s Financial policy

Committee sought to put off an increase in process of lending, even though they would not

have affected the current loans. As per the central banker, these measures would prevent

process of lending going too far ahead of earnings, growth as well as prevent a decline into

riskier proposition of lending and higher indebtedness that could undermine overall economic

expansion (Ascari and Sbordone 2014).

FINANCIAL AND ECONOMIC LITERACY FOR MANAGERScertain factors before arriving at rate decisions. The bank lending and figures on customer

credit includes equity levels withdrawal from the housing market and data on credit card

lending that supports demand of the customers. Furthermore, equity markets (prices of share)

and prices of houses are taken into consideration for the purpose of ascertainment of

household wealth that then feeds through to borrowing and retail spending (Bernanke et al.

2015). The monetary policy committee (MPC) necessarily has no official target for the yearly

house price inflation rate but the same has been criticised for not acting appropriately for

prevention of housing bubble till the period 2008. The alterations in the policy of the central

bank rates of interest also affect the housing market. Essentially, higher rates of interest

enhance the overall cost of mortgages and lessen overall demand for particularly housing.

Again, this can affect the overall wealth of the household and put a pressure on withdrawal of

equity.

Empirical evidence: As per reports published in Financial Times, Mark Carney, the central

banker tried to avert threats to economic recovery by imposition of limits on particularly

mortgage borrowing. The limitations on huge loans forced by the bank’s Financial policy

Committee sought to put off an increase in process of lending, even though they would not

have affected the current loans. As per the central banker, these measures would prevent

process of lending going too far ahead of earnings, growth as well as prevent a decline into

riskier proposition of lending and higher indebtedness that could undermine overall economic

expansion (Ascari and Sbordone 2014).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

FINANCIAL AND ECONOMIC LITERACY FOR MANAGERS

Solution to Question 3:

Key macroeconomics indicators and trend in these indicators in the UK over last 5

years

Key macroeconomic indicators are necessarily utilized for the purpose of calculating gross

national income (GNI) is particularly gross domestic product, employment, money supply

and inflation rate among many others.

Gross domestic product (GDP): This refers to the total market value of different goods as

well as services that is necessarily produced by a nation in a particular period of time (Borio

2014). The UK economy developed by around 0.4% on quarter in a period of three months

and is below the preliminary approximation of 0.5% and an upward revision of 0.5%

expansion can be witnessed in the earlier period. A slowdown can be observed in the overall

rate of growth of spending of households when viewed from expenditure side. The growth

rate of GDP in the UK averaged approximately 0.60% during the period 1955 to 2017,

thereafter reaching an all time high of approximately 5% during the first quarter of the year

1973 as well as a record low of -2.70% during the first quarter of 1974 (Agénor and Montiel

2015).

FINANCIAL AND ECONOMIC LITERACY FOR MANAGERS

Solution to Question 3:

Key macroeconomics indicators and trend in these indicators in the UK over last 5

years

Key macroeconomic indicators are necessarily utilized for the purpose of calculating gross

national income (GNI) is particularly gross domestic product, employment, money supply

and inflation rate among many others.

Gross domestic product (GDP): This refers to the total market value of different goods as

well as services that is necessarily produced by a nation in a particular period of time (Borio

2014). The UK economy developed by around 0.4% on quarter in a period of three months

and is below the preliminary approximation of 0.5% and an upward revision of 0.5%

expansion can be witnessed in the earlier period. A slowdown can be observed in the overall

rate of growth of spending of households when viewed from expenditure side. The growth

rate of GDP in the UK averaged approximately 0.60% during the period 1955 to 2017,

thereafter reaching an all time high of approximately 5% during the first quarter of the year

1973 as well as a record low of -2.70% during the first quarter of 1974 (Agénor and Montiel

2015).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11

FINANCIAL AND ECONOMIC LITERACY FOR MANAGERS

Figure: Growth Rate in UK

(Source: Titman et al. 2017)

Employment Rate: Employed can be referred to as full as well as part time workers, along

with part time together with temporary workers who necessarily accepted pay for specified

period (Block et al. 2015). The employment rate in the nation UK declined to approximately

75.20% during the period November to the registered figure of 75.20% in the period October

in the year 2017, thereby reaching the high of 75.30% in the month of June of the year 2017

and a recorded low of around 65.60% in the month of March of the year 1983.

FINANCIAL AND ECONOMIC LITERACY FOR MANAGERS

Figure: Growth Rate in UK

(Source: Titman et al. 2017)

Employment Rate: Employed can be referred to as full as well as part time workers, along

with part time together with temporary workers who necessarily accepted pay for specified

period (Block et al. 2015). The employment rate in the nation UK declined to approximately

75.20% during the period November to the registered figure of 75.20% in the period October

in the year 2017, thereby reaching the high of 75.30% in the month of June of the year 2017

and a recorded low of around 65.60% in the month of March of the year 1983.

12

FINANCIAL AND ECONOMIC LITERACY FOR MANAGERSFigure: Employment Rate in UK

(Source: Titman et al. 2017)

Money Supply: Money supply is necessarily a representation of the entire amount of money

that is in circulation in the economy (Andreou et al. 2014). Essentially, this comprises of

physical currency, savings of demand deposit and checking accounts, diverse traveller

checks, particular assets present in retail money market, money market mutual funds,

individuals time deposits as well as savings deposit. Money supply particularly in the United

Kingdom enhanced to 2833498 million GBP in January from the registered figure of

2814773 million GBP during December 2017 (Sharan 2015). Essentially, money supply

necessarily in the United Kingdom has an average of 1312724 million GBP from the period

1987 – 2018, reaching an all time high of 2833498 million GBP in the year 2018 and a record

low of approximately 263025 million GBP in the month of January of the year 1987.

Figure: Money Supply

(Source: Sharan 2015)

FINANCIAL AND ECONOMIC LITERACY FOR MANAGERSFigure: Employment Rate in UK

(Source: Titman et al. 2017)

Money Supply: Money supply is necessarily a representation of the entire amount of money

that is in circulation in the economy (Andreou et al. 2014). Essentially, this comprises of

physical currency, savings of demand deposit and checking accounts, diverse traveller

checks, particular assets present in retail money market, money market mutual funds,

individuals time deposits as well as savings deposit. Money supply particularly in the United

Kingdom enhanced to 2833498 million GBP in January from the registered figure of

2814773 million GBP during December 2017 (Sharan 2015). Essentially, money supply

necessarily in the United Kingdom has an average of 1312724 million GBP from the period

1987 – 2018, reaching an all time high of 2833498 million GBP in the year 2018 and a record

low of approximately 263025 million GBP in the month of January of the year 1987.

Figure: Money Supply

(Source: Sharan 2015)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.