Financial Analysis and Variance Report

VerifiedAdded on 2020/07/22

|14

|3793

|71

AI Summary

The provided document is a detailed report on various types of financial analysis and variance reports. It covers fixed and actual budgets, management reports, financial statements, break-even analysis, profits calculation, and rate of return (ARR) and internal rate of return (IRR). The report also discusses the credibility of investment plans with regard to profitability and specific rate of return. References are provided from books and journals, including Oxford University Press and National Bureau of Economic Research.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Finance For Managers

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1 ...........................................................................................................................................1

1.1 The purpose and required for keeping financial recordes................................................1

1.2 Techniques for recording financial information in a business organisation.....................2

1.3 Legal and organisational requirement for financial reporting..........................................2

1.4 Usefulness of financial statements to stakeholders..........................................................2

TASK 2............................................................................................................................................3

2.1 Components of working capital........................................................................................3

2.2 Business organisations can effectively manage working capital.....................................3

TASK 3............................................................................................................................................3

3.1 Difference between management and financial Accounting............................................3

3.2 The budgetary control process..........................................................................................4

3.3 Calculation and interpretation of variances from budget.................................................4

3.4 Evaluate the use of different costing methods for pricing purpose..................................5

TASK 4............................................................................................................................................6

4.1 Demonstration Methods of project appraisals..................................................................6

4.2 Evaluation of project appraisal.........................................................................................9

4.3 How finance might be obtained for a business project...................................................10

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................12

INTRODUCTION...........................................................................................................................1

TASK 1 ...........................................................................................................................................1

1.1 The purpose and required for keeping financial recordes................................................1

1.2 Techniques for recording financial information in a business organisation.....................2

1.3 Legal and organisational requirement for financial reporting..........................................2

1.4 Usefulness of financial statements to stakeholders..........................................................2

TASK 2............................................................................................................................................3

2.1 Components of working capital........................................................................................3

2.2 Business organisations can effectively manage working capital.....................................3

TASK 3............................................................................................................................................3

3.1 Difference between management and financial Accounting............................................3

3.2 The budgetary control process..........................................................................................4

3.3 Calculation and interpretation of variances from budget.................................................4

3.4 Evaluate the use of different costing methods for pricing purpose..................................5

TASK 4............................................................................................................................................6

4.1 Demonstration Methods of project appraisals..................................................................6

4.2 Evaluation of project appraisal.........................................................................................9

4.3 How finance might be obtained for a business project...................................................10

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................12

INTRODUCTION

Criteria of finance management and accounting remain essential in respect of managers

and higher level of management (Baker and Wurgler, 2011). There are different types of cost and

financial reports provided to managers like budgetary reports, reconciliation statements, cash

flow and fund flow statements, financial positions reports, etc. These reports represent particular

divisions of company. These information are used in decision making and strategic planning.

Budgetary reports, variance analysis report, investment rates and accounting rate of returns are

the reports described in this report (Fan, Wei and Xu, 2011). As a finance manager of small scale

ice cream company, planning and strategies are prepared in this report. Company wants to launch

a new ice cream product in market in respect this subject cost and variance analysis done here.

TASK 1

1.1 The purpose and required for keeping financial recordes

A small scale organisation deals in ice cream products and planning to launch new

product. There are various types of variances analysed to determine the cost of production units.

Current situation of production indicates towards further extension and new product launch.

Company want to introduce new ice cream product for children and wants to manufacture ice

cream boxes which contains the unit of 24 ice cream. There are various types of variances and

cost analysis made to evaluate the consistency and stability of plan.

Purpose and requirements

Internal control requirements: By the assistance of this, organization can undoubtedly

have the capacity to chose aggregate sum of costs and wages organization is paying inside a

Accounting period.

Legal requirements: Companies act substance budgetary explanations used to get ready

as per material accounting norms under area 291(Ang, Gregoriouand Lean, 2014).

Tax requirements: Tax show up in some shape in each three budgetary explanations.

Conceded charge obligation can be considered in the long haul liabilities area of the accounting

report. It would determine, regardless of whether organizations are paying charges according to

the chose approaches of the nation.

1

Criteria of finance management and accounting remain essential in respect of managers

and higher level of management (Baker and Wurgler, 2011). There are different types of cost and

financial reports provided to managers like budgetary reports, reconciliation statements, cash

flow and fund flow statements, financial positions reports, etc. These reports represent particular

divisions of company. These information are used in decision making and strategic planning.

Budgetary reports, variance analysis report, investment rates and accounting rate of returns are

the reports described in this report (Fan, Wei and Xu, 2011). As a finance manager of small scale

ice cream company, planning and strategies are prepared in this report. Company wants to launch

a new ice cream product in market in respect this subject cost and variance analysis done here.

TASK 1

1.1 The purpose and required for keeping financial recordes

A small scale organisation deals in ice cream products and planning to launch new

product. There are various types of variances analysed to determine the cost of production units.

Current situation of production indicates towards further extension and new product launch.

Company want to introduce new ice cream product for children and wants to manufacture ice

cream boxes which contains the unit of 24 ice cream. There are various types of variances and

cost analysis made to evaluate the consistency and stability of plan.

Purpose and requirements

Internal control requirements: By the assistance of this, organization can undoubtedly

have the capacity to chose aggregate sum of costs and wages organization is paying inside a

Accounting period.

Legal requirements: Companies act substance budgetary explanations used to get ready

as per material accounting norms under area 291(Ang, Gregoriouand Lean, 2014).

Tax requirements: Tax show up in some shape in each three budgetary explanations.

Conceded charge obligation can be considered in the long haul liabilities area of the accounting

report. It would determine, regardless of whether organizations are paying charges according to

the chose approaches of the nation.

1

1.2 Techniques for recording financial information in a business organisation

Day book and ledger: A buys day book is a Accounting record in which purchasing

exchange are recorded viably. All the monetary exchange is recorded into record books.

Double entry Accounting: It is a successful framework that is utilized to post a wide

range of monetary sections. It gives profitable data that each record would impactful affect the

announcements.

The trail balance: An declaration of the considerable number of obligations and credit in

a Double entry Accounting with any difference showing a blunders are breaking down through

this trail adjust. In the wake of chronicle all the exchange into the record at that point posted into

the trail adjust.

1.3 Legal and organisational requirement for financial reporting

Financial reporting requirements for sole traders: An individual back are more firmly

connected business tasks than with some other kinds of business structure. The money related

record of sole dealer organizations of exchanging Accounting. Independently employed sole

merchants and most organizations don't have to make a formal benefit and losses explanations.

Private limited companies: It is required for each private restricted organization to hold

an AGM in consistently for the information for shutting the monetary year. they are required to

keep up appropriate records of information which will be useful in introducing it before different

financial specialists.

Public limited companies: It is most extreme essential for general society restricted

organization to arranged money related explanations so that to issues shares and in addition bring

IPO. It will help with masterminding all the basic alternatives those are useful in producing most

extreme benefit.

1.4 Usefulness of financial statements to stakeholders

Usefulness of stakeholders: In any sort of business, a partner is fundamentally

considered as a financial specialists of the organization whose activities decide the results of

their business choice. Utilizing of partner ability and expanded responsibility of lead

organization. They don't need to be value investors.

Users/stakeholders: End clients have not been taken into thought about a need gathering

of people. Be that as it may, the standing board of trustees avows the critical piece of the

organization. A few people, for example, chiefs, inspectors and banks and in addition other

2

Day book and ledger: A buys day book is a Accounting record in which purchasing

exchange are recorded viably. All the monetary exchange is recorded into record books.

Double entry Accounting: It is a successful framework that is utilized to post a wide

range of monetary sections. It gives profitable data that each record would impactful affect the

announcements.

The trail balance: An declaration of the considerable number of obligations and credit in

a Double entry Accounting with any difference showing a blunders are breaking down through

this trail adjust. In the wake of chronicle all the exchange into the record at that point posted into

the trail adjust.

1.3 Legal and organisational requirement for financial reporting

Financial reporting requirements for sole traders: An individual back are more firmly

connected business tasks than with some other kinds of business structure. The money related

record of sole dealer organizations of exchanging Accounting. Independently employed sole

merchants and most organizations don't have to make a formal benefit and losses explanations.

Private limited companies: It is required for each private restricted organization to hold

an AGM in consistently for the information for shutting the monetary year. they are required to

keep up appropriate records of information which will be useful in introducing it before different

financial specialists.

Public limited companies: It is most extreme essential for general society restricted

organization to arranged money related explanations so that to issues shares and in addition bring

IPO. It will help with masterminding all the basic alternatives those are useful in producing most

extreme benefit.

1.4 Usefulness of financial statements to stakeholders

Usefulness of stakeholders: In any sort of business, a partner is fundamentally

considered as a financial specialists of the organization whose activities decide the results of

their business choice. Utilizing of partner ability and expanded responsibility of lead

organization. They don't need to be value investors.

Users/stakeholders: End clients have not been taken into thought about a need gathering

of people. Be that as it may, the standing board of trustees avows the critical piece of the

organization. A few people, for example, chiefs, inspectors and banks and in addition other

2

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

office those are utilizing money related explanations for investigating the execution of the

organization.

TASK 2

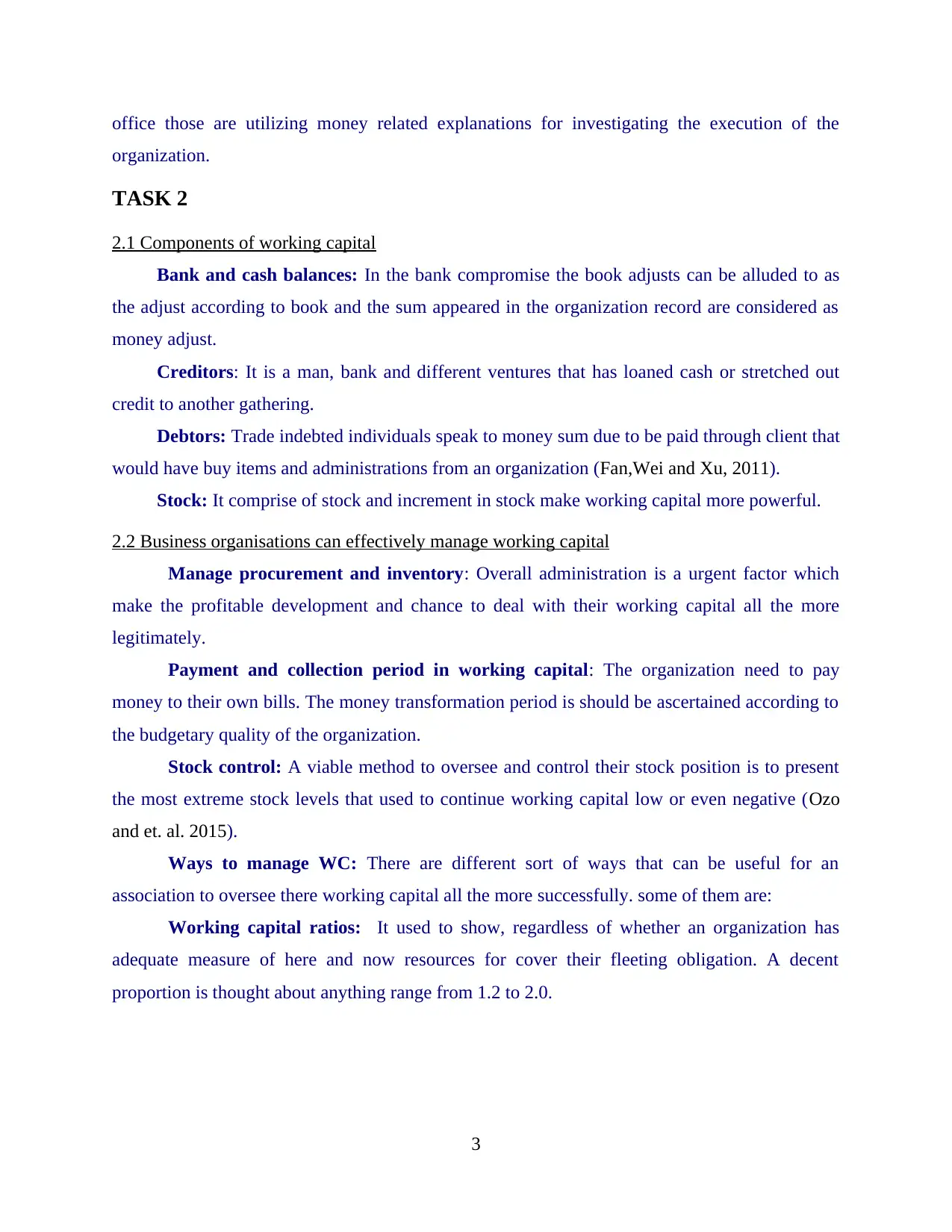

2.1 Components of working capital

Bank and cash balances: In the bank compromise the book adjusts can be alluded to as

the adjust according to book and the sum appeared in the organization record are considered as

money adjust.

Creditors: It is a man, bank and different ventures that has loaned cash or stretched out

credit to another gathering.

Debtors: Trade indebted individuals speak to money sum due to be paid through client that

would have buy items and administrations from an organization (Fan,Wei and Xu, 2011).

Stock: It comprise of stock and increment in stock make working capital more powerful.

2.2 Business organisations can effectively manage working capital

Manage procurement and inventory: Overall administration is a urgent factor which

make the profitable development and chance to deal with their working capital all the more

legitimately.

Payment and collection period in working capital: The organization need to pay

money to their own bills. The money transformation period is should be ascertained according to

the budgetary quality of the organization.

Stock control: A viable method to oversee and control their stock position is to present

the most extreme stock levels that used to continue working capital low or even negative (Ozo

and et. al. 2015).

Ways to manage WC: There are different sort of ways that can be useful for an

association to oversee there working capital all the more successfully. some of them are:

Working capital ratios: It used to show, regardless of whether an organization has

adequate measure of here and now resources for cover their fleeting obligation. A decent

proportion is thought about anything range from 1.2 to 2.0.

3

organization.

TASK 2

2.1 Components of working capital

Bank and cash balances: In the bank compromise the book adjusts can be alluded to as

the adjust according to book and the sum appeared in the organization record are considered as

money adjust.

Creditors: It is a man, bank and different ventures that has loaned cash or stretched out

credit to another gathering.

Debtors: Trade indebted individuals speak to money sum due to be paid through client that

would have buy items and administrations from an organization (Fan,Wei and Xu, 2011).

Stock: It comprise of stock and increment in stock make working capital more powerful.

2.2 Business organisations can effectively manage working capital

Manage procurement and inventory: Overall administration is a urgent factor which

make the profitable development and chance to deal with their working capital all the more

legitimately.

Payment and collection period in working capital: The organization need to pay

money to their own bills. The money transformation period is should be ascertained according to

the budgetary quality of the organization.

Stock control: A viable method to oversee and control their stock position is to present

the most extreme stock levels that used to continue working capital low or even negative (Ozo

and et. al. 2015).

Ways to manage WC: There are different sort of ways that can be useful for an

association to oversee there working capital all the more successfully. some of them are:

Working capital ratios: It used to show, regardless of whether an organization has

adequate measure of here and now resources for cover their fleeting obligation. A decent

proportion is thought about anything range from 1.2 to 2.0.

3

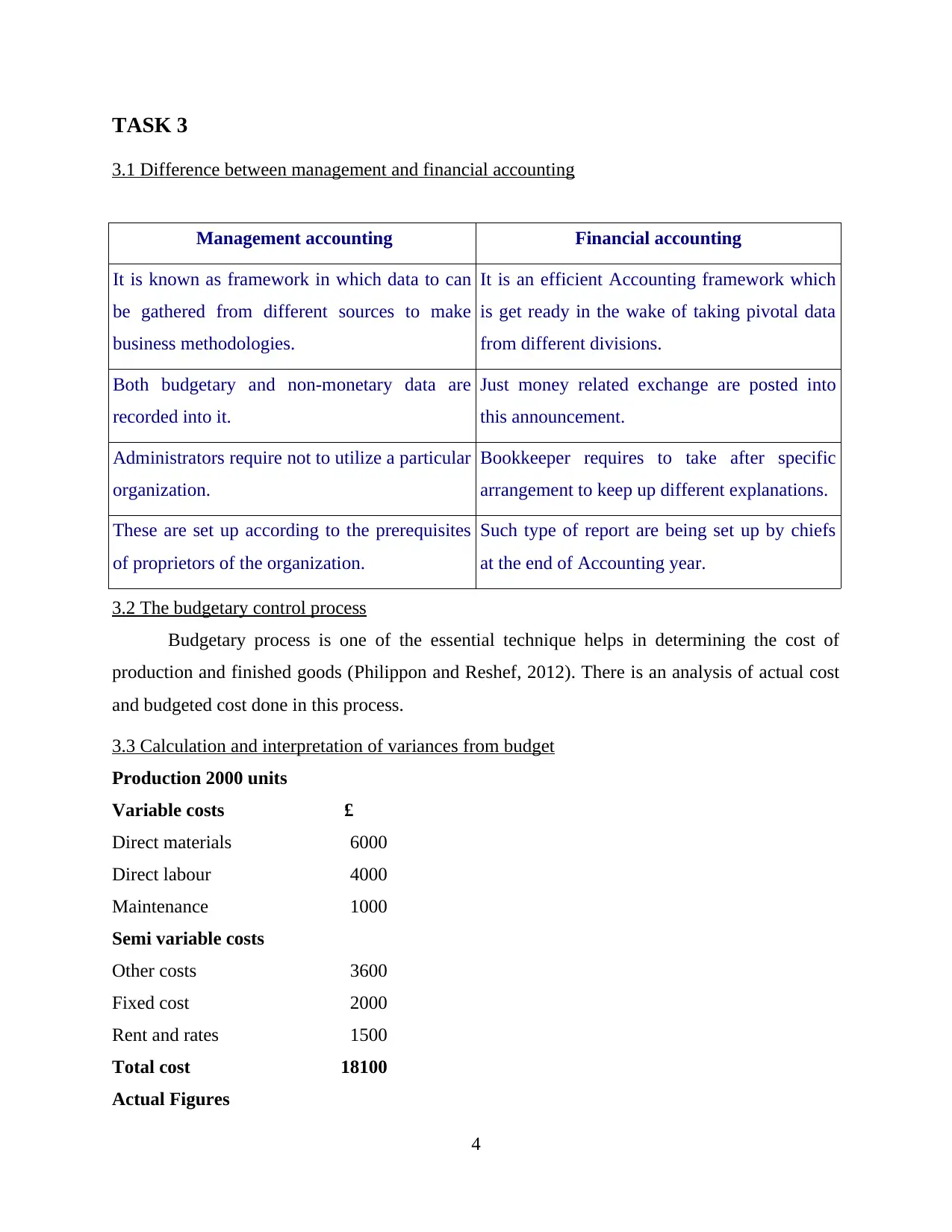

TASK 3

3.1 Difference between management and financial accounting

Management accounting Financial accounting

It is known as framework in which data to can

be gathered from different sources to make

business methodologies.

It is an efficient Accounting framework which

is get ready in the wake of taking pivotal data

from different divisions.

Both budgetary and non-monetary data are

recorded into it.

Just money related exchange are posted into

this announcement.

Administrators require not to utilize a particular

organization.

Bookkeeper requires to take after specific

arrangement to keep up different explanations.

These are set up according to the prerequisites

of proprietors of the organization.

Such type of report are being set up by chiefs

at the end of Accounting year.

3.2 The budgetary control process

Budgetary process is one of the essential technique helps in determining the cost of

production and finished goods (Philippon and Reshef, 2012). There is an analysis of actual cost

and budgeted cost done in this process.

3.3 Calculation and interpretation of variances from budget

Production 2000 units

Variable costs £

Direct materials 6000

Direct labour 4000

Maintenance 1000

Semi variable costs

Other costs 3600

Fixed cost 2000

Rent and rates 1500

Total cost 18100

Actual Figures

4

3.1 Difference between management and financial accounting

Management accounting Financial accounting

It is known as framework in which data to can

be gathered from different sources to make

business methodologies.

It is an efficient Accounting framework which

is get ready in the wake of taking pivotal data

from different divisions.

Both budgetary and non-monetary data are

recorded into it.

Just money related exchange are posted into

this announcement.

Administrators require not to utilize a particular

organization.

Bookkeeper requires to take after specific

arrangement to keep up different explanations.

These are set up according to the prerequisites

of proprietors of the organization.

Such type of report are being set up by chiefs

at the end of Accounting year.

3.2 The budgetary control process

Budgetary process is one of the essential technique helps in determining the cost of

production and finished goods (Philippon and Reshef, 2012). There is an analysis of actual cost

and budgeted cost done in this process.

3.3 Calculation and interpretation of variances from budget

Production 2000 units

Variable costs £

Direct materials 6000

Direct labour 4000

Maintenance 1000

Semi variable costs

Other costs 3600

Fixed cost 2000

Rent and rates 1500

Total cost 18100

Actual Figures

4

Production 3000 units

Variable costs 8500

Direct labour 4500

Maintenance 1400

Semi variable costs

Other costs 5000

Fixed costs

Depreciation 2200

Rent and rates 1600

23200

Fixed budget Flexible budget Actual budget Budget variance

a b c B-c

Production (units) 2000 3000 3000

Sales revenues 26000 39000 39000

variable cost

Direct material 6000 9000 8500 500 F

Direct labour 4000 6000 4500 1500 F

Maintenance 1000 1500 1400 100 F

Semi variable costs

Other costs 3600 4600 5000 -4000 A

Fixed costs

Depreciation 2000 2000 2200 -200 A

Rent and rates 1500 1500 1600 -100 A

Total cost 18100 24600 23200 1400 F

c) Full variance analysis

£ £

Fixed budget profit 7900 F

variance

Sales volume 6500 F

5

Variable costs 8500

Direct labour 4500

Maintenance 1400

Semi variable costs

Other costs 5000

Fixed costs

Depreciation 2200

Rent and rates 1600

23200

Fixed budget Flexible budget Actual budget Budget variance

a b c B-c

Production (units) 2000 3000 3000

Sales revenues 26000 39000 39000

variable cost

Direct material 6000 9000 8500 500 F

Direct labour 4000 6000 4500 1500 F

Maintenance 1000 1500 1400 100 F

Semi variable costs

Other costs 3600 4600 5000 -4000 A

Fixed costs

Depreciation 2000 2000 2200 -200 A

Rent and rates 1500 1500 1600 -100 A

Total cost 18100 24600 23200 1400 F

c) Full variance analysis

£ £

Fixed budget profit 7900 F

variance

Sales volume 6500 F

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

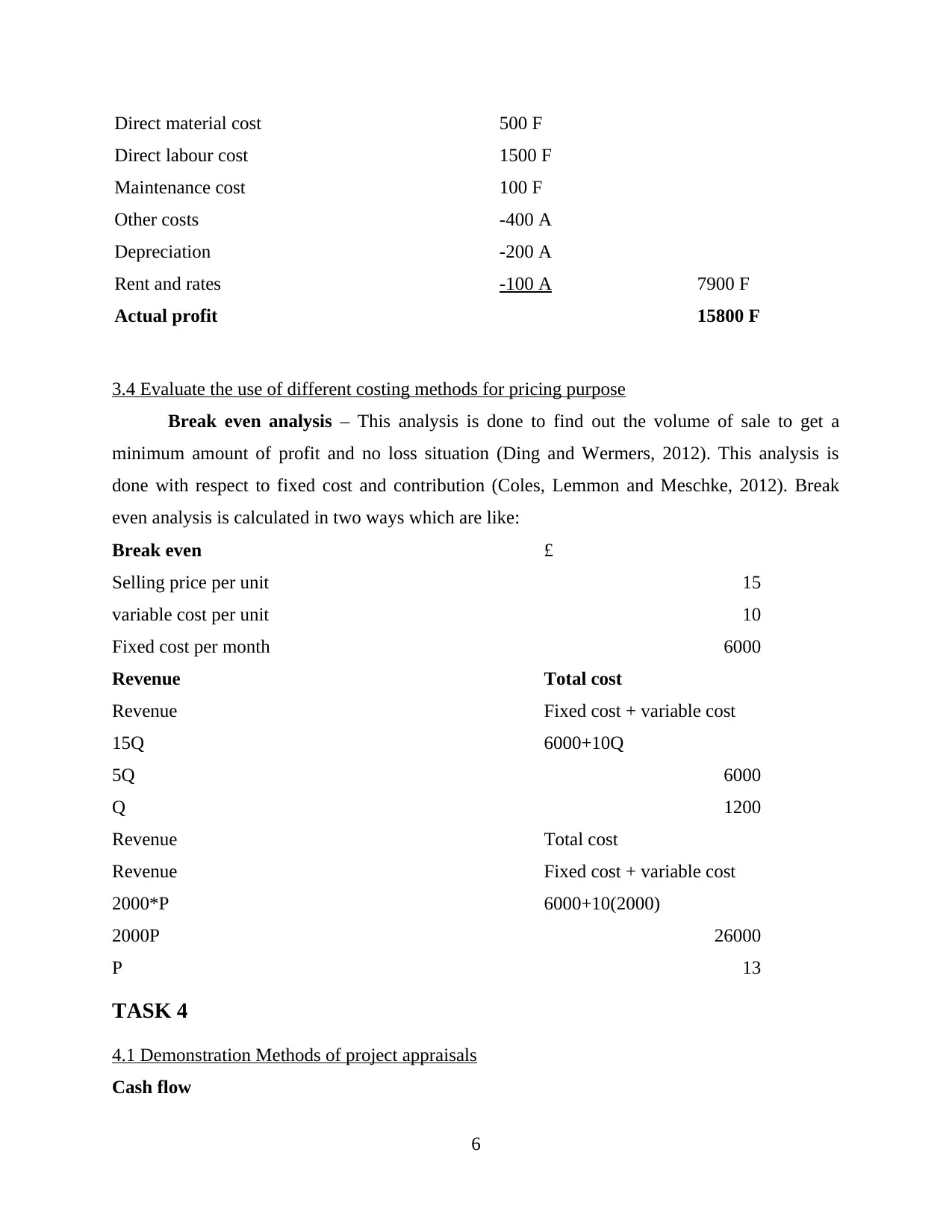

Direct material cost 500 F

Direct labour cost 1500 F

Maintenance cost 100 F

Other costs -400 A

Depreciation -200 A

Rent and rates -100 A 7900 F

Actual profit 15800 F

3.4 Evaluate the use of different costing methods for pricing purpose

Break even analysis – This analysis is done to find out the volume of sale to get a

minimum amount of profit and no loss situation (Ding and Wermers, 2012). This analysis is

done with respect to fixed cost and contribution (Coles, Lemmon and Meschke, 2012). Break

even analysis is calculated in two ways which are like:

Break even £

Selling price per unit 15

variable cost per unit 10

Fixed cost per month 6000

Revenue Total cost

Revenue Fixed cost + variable cost

15Q 6000+10Q

5Q 6000

Q 1200

Revenue Total cost

Revenue Fixed cost + variable cost

2000*P 6000+10(2000)

2000P 26000

P 13

TASK 4

4.1 Demonstration Methods of project appraisals

Cash flow

6

Direct labour cost 1500 F

Maintenance cost 100 F

Other costs -400 A

Depreciation -200 A

Rent and rates -100 A 7900 F

Actual profit 15800 F

3.4 Evaluate the use of different costing methods for pricing purpose

Break even analysis – This analysis is done to find out the volume of sale to get a

minimum amount of profit and no loss situation (Ding and Wermers, 2012). This analysis is

done with respect to fixed cost and contribution (Coles, Lemmon and Meschke, 2012). Break

even analysis is calculated in two ways which are like:

Break even £

Selling price per unit 15

variable cost per unit 10

Fixed cost per month 6000

Revenue Total cost

Revenue Fixed cost + variable cost

15Q 6000+10Q

5Q 6000

Q 1200

Revenue Total cost

Revenue Fixed cost + variable cost

2000*P 6000+10(2000)

2000P 26000

P 13

TASK 4

4.1 Demonstration Methods of project appraisals

Cash flow

6

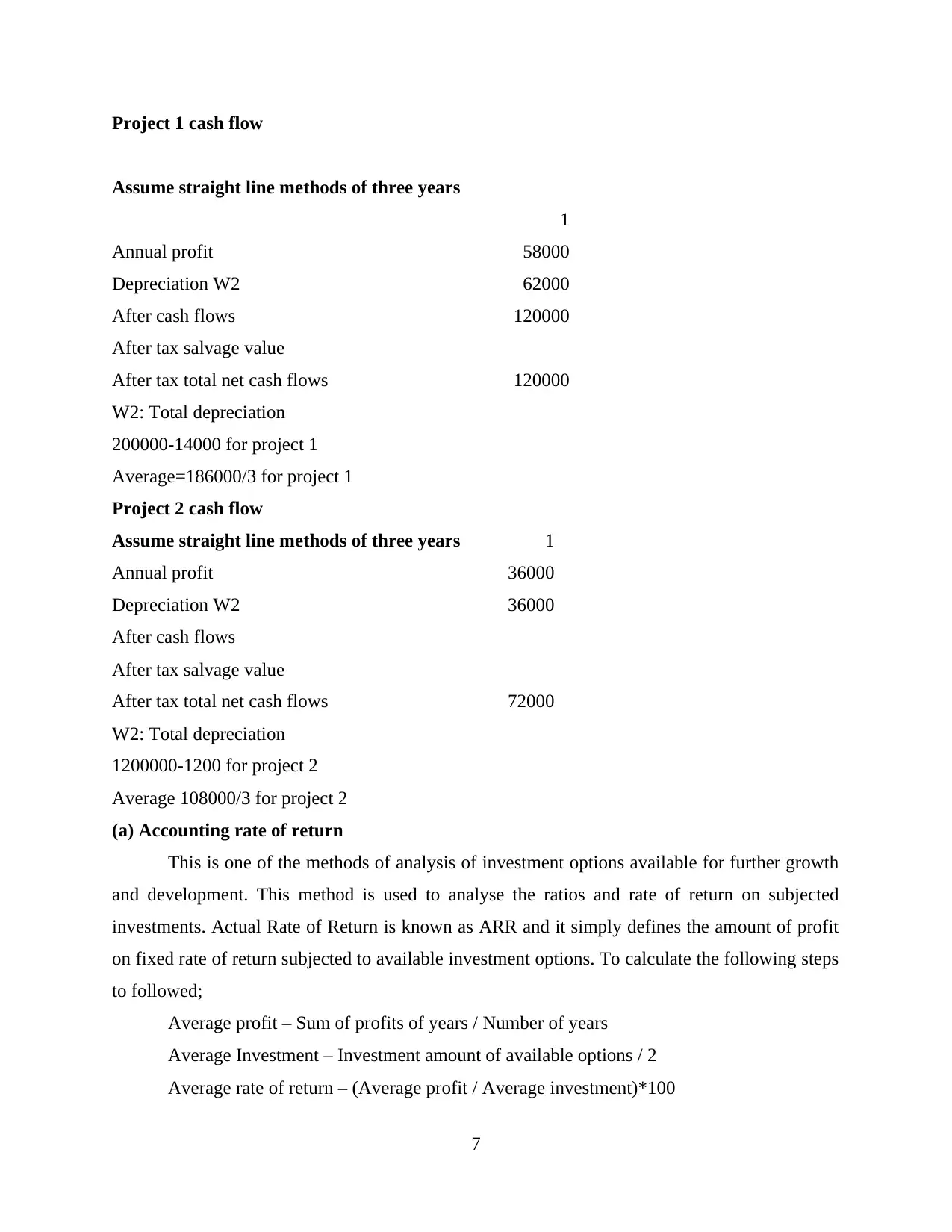

Project 1 cash flow

Assume straight line methods of three years

1

Annual profit 58000

Depreciation W2 62000

After cash flows 120000

After tax salvage value

After tax total net cash flows 120000

W2: Total depreciation

200000-14000 for project 1

Average=186000/3 for project 1

Project 2 cash flow

Assume straight line methods of three years 1

Annual profit 36000

Depreciation W2 36000

After cash flows

After tax salvage value

After tax total net cash flows 72000

W2: Total depreciation

1200000-1200 for project 2

Average 108000/3 for project 2

(a) Accounting rate of return

This is one of the methods of analysis of investment options available for further growth

and development. This method is used to analyse the ratios and rate of return on subjected

investments. Actual Rate of Return is known as ARR and it simply defines the amount of profit

on fixed rate of return subjected to available investment options. To calculate the following steps

to followed;

Average profit – Sum of profits of years / Number of years

Average Investment – Investment amount of available options / 2

Average rate of return – (Average profit / Average investment)*100

7

Assume straight line methods of three years

1

Annual profit 58000

Depreciation W2 62000

After cash flows 120000

After tax salvage value

After tax total net cash flows 120000

W2: Total depreciation

200000-14000 for project 1

Average=186000/3 for project 1

Project 2 cash flow

Assume straight line methods of three years 1

Annual profit 36000

Depreciation W2 36000

After cash flows

After tax salvage value

After tax total net cash flows 72000

W2: Total depreciation

1200000-1200 for project 2

Average 108000/3 for project 2

(a) Accounting rate of return

This is one of the methods of analysis of investment options available for further growth

and development. This method is used to analyse the ratios and rate of return on subjected

investments. Actual Rate of Return is known as ARR and it simply defines the amount of profit

on fixed rate of return subjected to available investment options. To calculate the following steps

to followed;

Average profit – Sum of profits of years / Number of years

Average Investment – Investment amount of available options / 2

Average rate of return – (Average profit / Average investment)*100

7

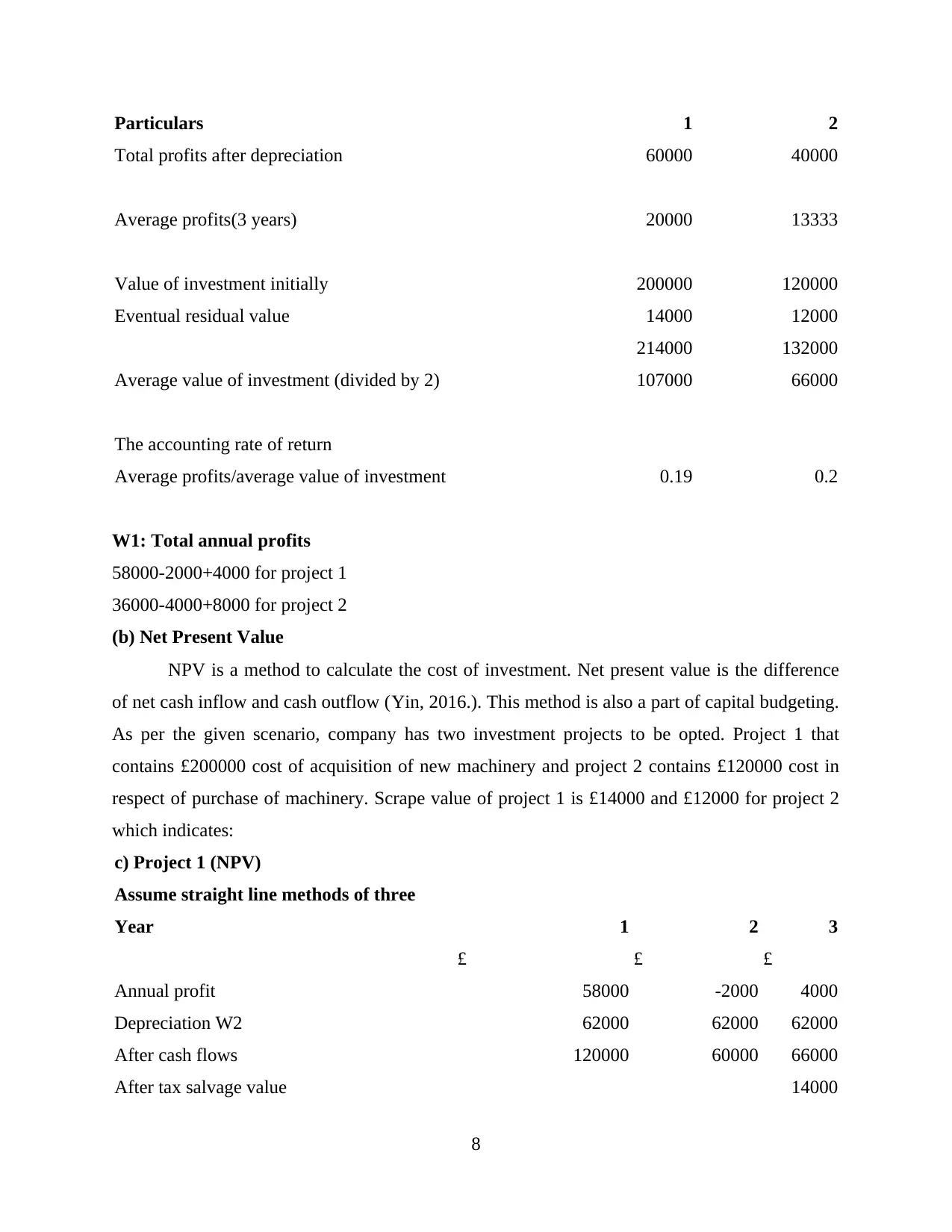

Particulars 1 2

Total profits after depreciation 60000 40000

Average profits(3 years) 20000 13333

Value of investment initially 200000 120000

Eventual residual value 14000 12000

214000 132000

Average value of investment (divided by 2) 107000 66000

The accounting rate of return

Average profits/average value of investment 0.19 0.2

W1: Total annual profits

58000-2000+4000 for project 1

36000-4000+8000 for project 2

(b) Net Present Value

NPV is a method to calculate the cost of investment. Net present value is the difference

of net cash inflow and cash outflow (Yin, 2016.). This method is also a part of capital budgeting.

As per the given scenario, company has two investment projects to be opted. Project 1 that

contains £200000 cost of acquisition of new machinery and project 2 contains £120000 cost in

respect of purchase of machinery. Scrape value of project 1 is £14000 and £12000 for project 2

which indicates:

c) Project 1 (NPV)

Assume straight line methods of three

Year 1 2 3

£ £ £

Annual profit 58000 -2000 4000

Depreciation W2 62000 62000 62000

After cash flows 120000 60000 66000

After tax salvage value 14000

8

Total profits after depreciation 60000 40000

Average profits(3 years) 20000 13333

Value of investment initially 200000 120000

Eventual residual value 14000 12000

214000 132000

Average value of investment (divided by 2) 107000 66000

The accounting rate of return

Average profits/average value of investment 0.19 0.2

W1: Total annual profits

58000-2000+4000 for project 1

36000-4000+8000 for project 2

(b) Net Present Value

NPV is a method to calculate the cost of investment. Net present value is the difference

of net cash inflow and cash outflow (Yin, 2016.). This method is also a part of capital budgeting.

As per the given scenario, company has two investment projects to be opted. Project 1 that

contains £200000 cost of acquisition of new machinery and project 2 contains £120000 cost in

respect of purchase of machinery. Scrape value of project 1 is £14000 and £12000 for project 2

which indicates:

c) Project 1 (NPV)

Assume straight line methods of three

Year 1 2 3

£ £ £

Annual profit 58000 -2000 4000

Depreciation W2 62000 62000 62000

After cash flows 120000 60000 66000

After tax salvage value 14000

8

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

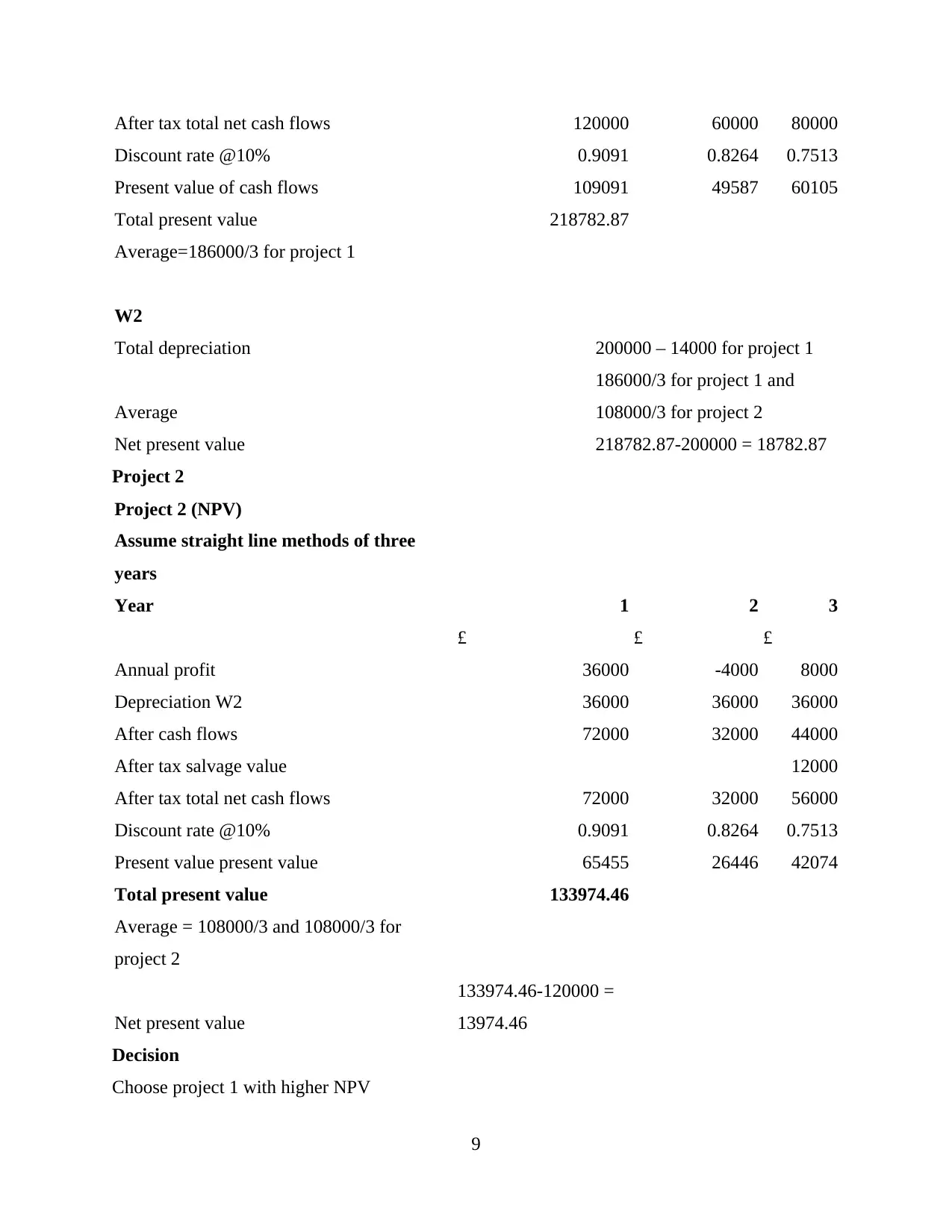

After tax total net cash flows 120000 60000 80000

Discount rate @10% 0.9091 0.8264 0.7513

Present value of cash flows 109091 49587 60105

Total present value 218782.87

Average=186000/3 for project 1

W2

Total depreciation 200000 – 14000 for project 1

Average

186000/3 for project 1 and

108000/3 for project 2

Net present value 218782.87-200000 = 18782.87

Project 2

Project 2 (NPV)

Assume straight line methods of three

years

Year 1 2 3

£ £ £

Annual profit 36000 -4000 8000

Depreciation W2 36000 36000 36000

After cash flows 72000 32000 44000

After tax salvage value 12000

After tax total net cash flows 72000 32000 56000

Discount rate @10% 0.9091 0.8264 0.7513

Present value present value 65455 26446 42074

Total present value 133974.46

Average = 108000/3 and 108000/3 for

project 2

Net present value

133974.46-120000 =

13974.46

Decision

Choose project 1 with higher NPV

9

Discount rate @10% 0.9091 0.8264 0.7513

Present value of cash flows 109091 49587 60105

Total present value 218782.87

Average=186000/3 for project 1

W2

Total depreciation 200000 – 14000 for project 1

Average

186000/3 for project 1 and

108000/3 for project 2

Net present value 218782.87-200000 = 18782.87

Project 2

Project 2 (NPV)

Assume straight line methods of three

years

Year 1 2 3

£ £ £

Annual profit 36000 -4000 8000

Depreciation W2 36000 36000 36000

After cash flows 72000 32000 44000

After tax salvage value 12000

After tax total net cash flows 72000 32000 56000

Discount rate @10% 0.9091 0.8264 0.7513

Present value present value 65455 26446 42074

Total present value 133974.46

Average = 108000/3 and 108000/3 for

project 2

Net present value

133974.46-120000 =

13974.46

Decision

Choose project 1 with higher NPV

9

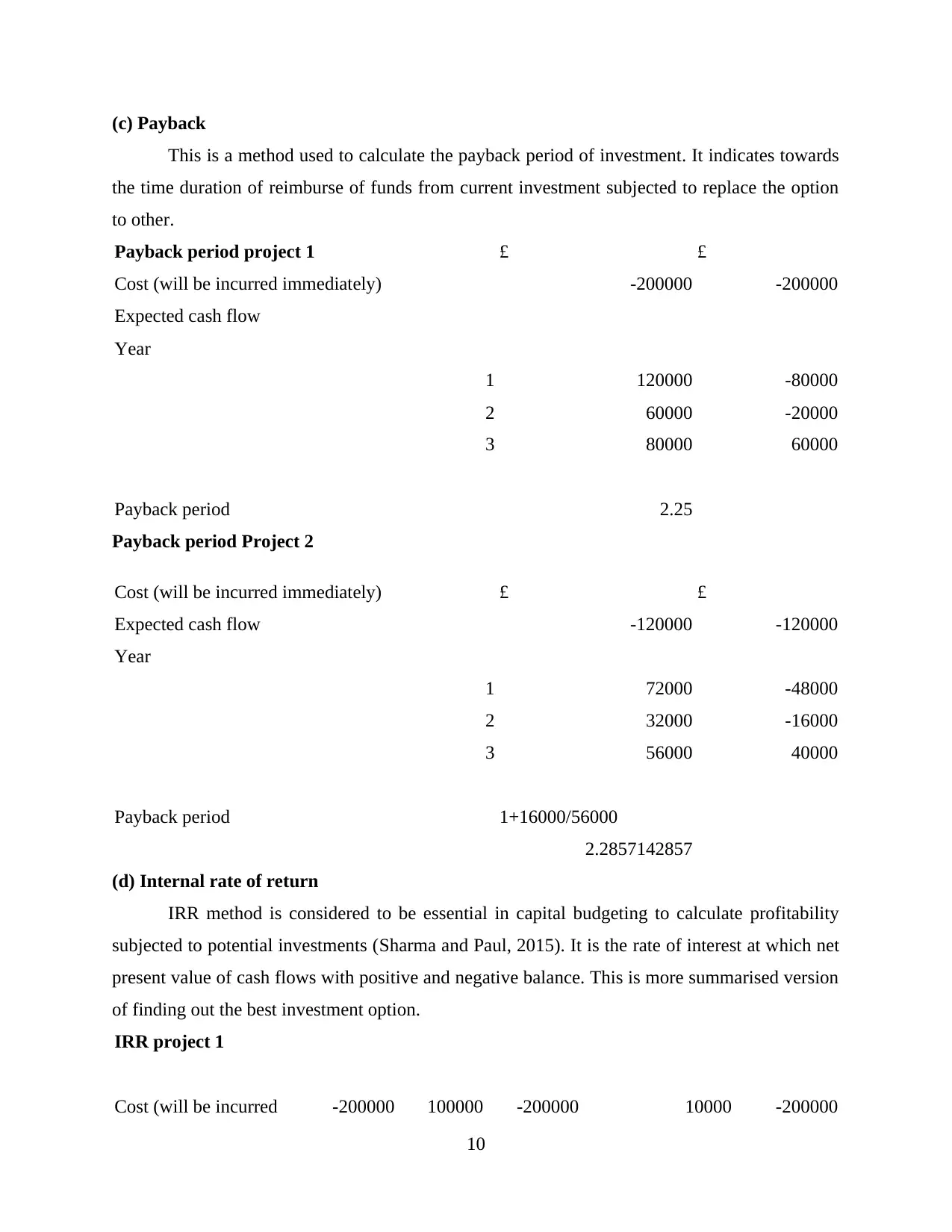

(c) Payback

This is a method used to calculate the payback period of investment. It indicates towards

the time duration of reimburse of funds from current investment subjected to replace the option

to other.

Payback period project 1 £ £

Cost (will be incurred immediately) -200000 -200000

Expected cash flow

Year

1 120000 -80000

2 60000 -20000

3 80000 60000

Payback period 2.25

Payback period Project 2

Cost (will be incurred immediately) £ £

Expected cash flow -120000 -120000

Year

1 72000 -48000

2 32000 -16000

3 56000 40000

Payback period 1+16000/56000

2.2857142857

(d) Internal rate of return

IRR method is considered to be essential in capital budgeting to calculate profitability

subjected to potential investments (Sharma and Paul, 2015). It is the rate of interest at which net

present value of cash flows with positive and negative balance. This is more summarised version

of finding out the best investment option.

IRR project 1

Cost (will be incurred -200000 100000 -200000 10000 -200000

10

This is a method used to calculate the payback period of investment. It indicates towards

the time duration of reimburse of funds from current investment subjected to replace the option

to other.

Payback period project 1 £ £

Cost (will be incurred immediately) -200000 -200000

Expected cash flow

Year

1 120000 -80000

2 60000 -20000

3 80000 60000

Payback period 2.25

Payback period Project 2

Cost (will be incurred immediately) £ £

Expected cash flow -120000 -120000

Year

1 72000 -48000

2 32000 -16000

3 56000 40000

Payback period 1+16000/56000

2.2857142857

(d) Internal rate of return

IRR method is considered to be essential in capital budgeting to calculate profitability

subjected to potential investments (Sharma and Paul, 2015). It is the rate of interest at which net

present value of cash flows with positive and negative balance. This is more summarised version

of finding out the best investment option.

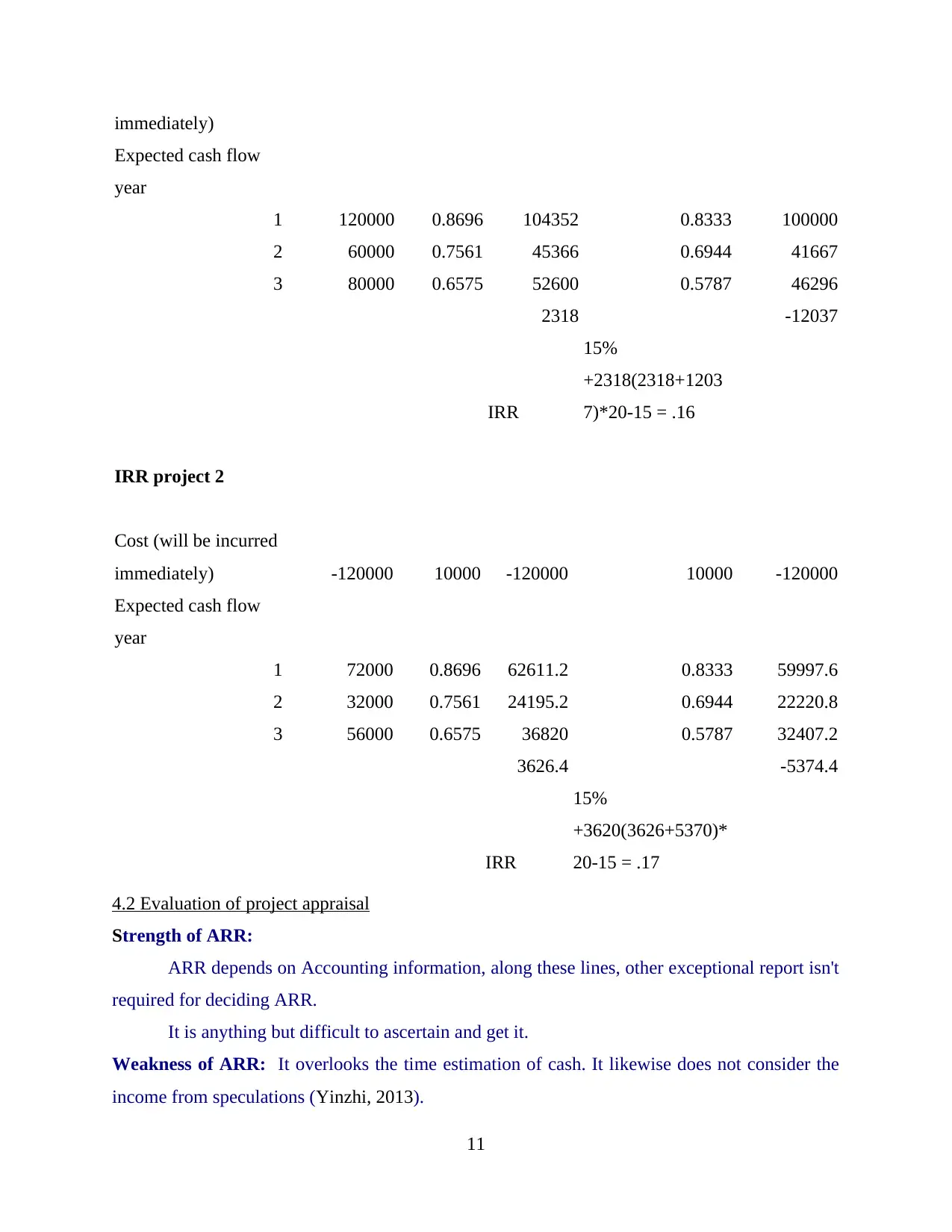

IRR project 1

Cost (will be incurred -200000 100000 -200000 10000 -200000

10

immediately)

Expected cash flow

year

1 120000 0.8696 104352 0.8333 100000

2 60000 0.7561 45366 0.6944 41667

3 80000 0.6575 52600 0.5787 46296

2318 -12037

IRR

15%

+2318(2318+1203

7)*20-15 = .16

IRR project 2

Cost (will be incurred

immediately) -120000 10000 -120000 10000 -120000

Expected cash flow

year

1 72000 0.8696 62611.2 0.8333 59997.6

2 32000 0.7561 24195.2 0.6944 22220.8

3 56000 0.6575 36820 0.5787 32407.2

3626.4 -5374.4

IRR

15%

+3620(3626+5370)*

20-15 = .17

4.2 Evaluation of project appraisal

Strength of ARR:

ARR depends on Accounting information, along these lines, other exceptional report isn't

required for deciding ARR.

It is anything but difficult to ascertain and get it.

Weakness of ARR: It overlooks the time estimation of cash. It likewise does not consider the

income from speculations (Yinzhi, 2013).

11

Expected cash flow

year

1 120000 0.8696 104352 0.8333 100000

2 60000 0.7561 45366 0.6944 41667

3 80000 0.6575 52600 0.5787 46296

2318 -12037

IRR

15%

+2318(2318+1203

7)*20-15 = .16

IRR project 2

Cost (will be incurred

immediately) -120000 10000 -120000 10000 -120000

Expected cash flow

year

1 72000 0.8696 62611.2 0.8333 59997.6

2 32000 0.7561 24195.2 0.6944 22220.8

3 56000 0.6575 36820 0.5787 32407.2

3626.4 -5374.4

IRR

15%

+3620(3626+5370)*

20-15 = .17

4.2 Evaluation of project appraisal

Strength of ARR:

ARR depends on Accounting information, along these lines, other exceptional report isn't

required for deciding ARR.

It is anything but difficult to ascertain and get it.

Weakness of ARR: It overlooks the time estimation of cash. It likewise does not consider the

income from speculations (Yinzhi, 2013).

11

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

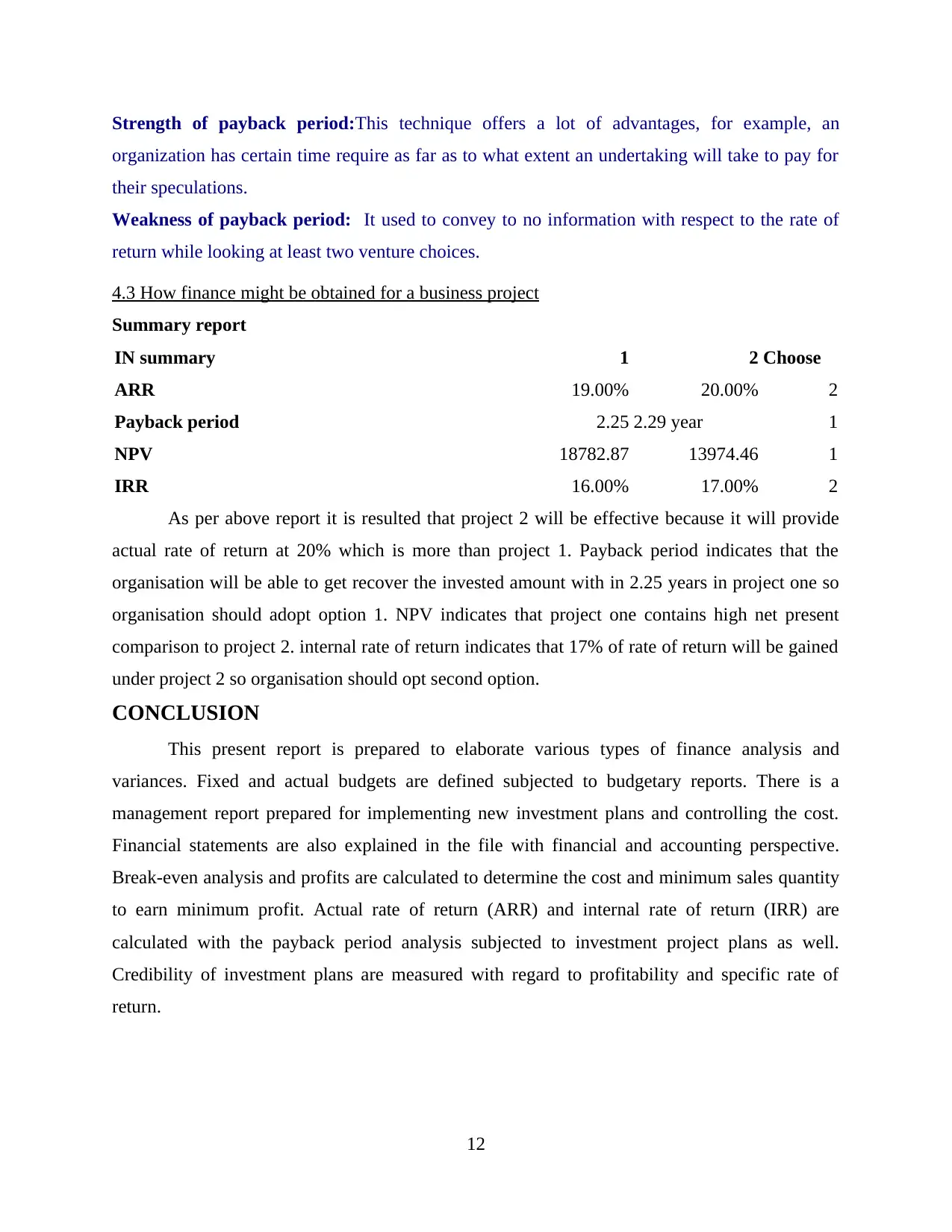

Strength of payback period:This technique offers a lot of advantages, for example, an

organization has certain time require as far as to what extent an undertaking will take to pay for

their speculations.

Weakness of payback period: It used to convey to no information with respect to the rate of

return while looking at least two venture choices.

4.3 How finance might be obtained for a business project

Summary report

IN summary 1 2 Choose

ARR 19.00% 20.00% 2

Payback period 2.25 2.29 year 1

NPV 18782.87 13974.46 1

IRR 16.00% 17.00% 2

As per above report it is resulted that project 2 will be effective because it will provide

actual rate of return at 20% which is more than project 1. Payback period indicates that the

organisation will be able to get recover the invested amount with in 2.25 years in project one so

organisation should adopt option 1. NPV indicates that project one contains high net present

comparison to project 2. internal rate of return indicates that 17% of rate of return will be gained

under project 2 so organisation should opt second option.

CONCLUSION

This present report is prepared to elaborate various types of finance analysis and

variances. Fixed and actual budgets are defined subjected to budgetary reports. There is a

management report prepared for implementing new investment plans and controlling the cost.

Financial statements are also explained in the file with financial and accounting perspective.

Break-even analysis and profits are calculated to determine the cost and minimum sales quantity

to earn minimum profit. Actual rate of return (ARR) and internal rate of return (IRR) are

calculated with the payback period analysis subjected to investment project plans as well.

Credibility of investment plans are measured with regard to profitability and specific rate of

return.

12

organization has certain time require as far as to what extent an undertaking will take to pay for

their speculations.

Weakness of payback period: It used to convey to no information with respect to the rate of

return while looking at least two venture choices.

4.3 How finance might be obtained for a business project

Summary report

IN summary 1 2 Choose

ARR 19.00% 20.00% 2

Payback period 2.25 2.29 year 1

NPV 18782.87 13974.46 1

IRR 16.00% 17.00% 2

As per above report it is resulted that project 2 will be effective because it will provide

actual rate of return at 20% which is more than project 1. Payback period indicates that the

organisation will be able to get recover the invested amount with in 2.25 years in project one so

organisation should adopt option 1. NPV indicates that project one contains high net present

comparison to project 2. internal rate of return indicates that 17% of rate of return will be gained

under project 2 so organisation should opt second option.

CONCLUSION

This present report is prepared to elaborate various types of finance analysis and

variances. Fixed and actual budgets are defined subjected to budgetary reports. There is a

management report prepared for implementing new investment plans and controlling the cost.

Financial statements are also explained in the file with financial and accounting perspective.

Break-even analysis and profits are calculated to determine the cost and minimum sales quantity

to earn minimum profit. Actual rate of return (ARR) and internal rate of return (IRR) are

calculated with the payback period analysis subjected to investment project plans as well.

Credibility of investment plans are measured with regard to profitability and specific rate of

return.

12

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.