Evaluating GPI's Performance: A Balance Scorecard Management Report

VerifiedAdded on 2023/01/20

|19

|4022

|28

Report

AI Summary

This report provides a detailed analysis of GPI's financial and performance management, focusing on the application of a balance scorecard (BSC). The report begins with an overview of the BSC process, followed by a discussion of its advantages and disadvantages. It then identifies critical success factors (CSFs) from client, internal process, financial, and workforce perspectives, crucial for GPI's performance. The report proposes a BSC framework and performance measurement metrics tailored to GPI, including a strategy map to visualize the organization's objectives. The analysis highlights the importance of client satisfaction, internal process improvements, financial stability, and workforce motivation in achieving GPI's long-term goals. The document emphasizes the need for effective resource management, employee training, and continuous evaluation to enhance service standards and overall performance within the non-profit context. The report concludes with a summary of the findings and recommendations for GPI's future performance management strategies.

FINANCIAL AND PERFORMANCE MANAGEMENT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Table of Contents.............................................................................................................................2

1.0 Summary of the Process............................................................................................................3

2.0 Advantages and Disadvantages of Balance Scorecard (BSC)...................................................6

2.1 Advantages............................................................................................................................6

2.2 Disadvantages........................................................................................................................6

3.0 Identification of Critical Success Factors (CSFs)......................................................................8

3.1 Clients’ Perspectives..............................................................................................................8

3.2 Internal Process Perspectives.................................................................................................8

3.3 Financial Perspectives...........................................................................................................9

3.4 Workforce Perspectives.......................................................................................................10

4.0 Proposed Balance Scorecard and Performance Measurement.................................................11

5.0 Proposed Strategy Map............................................................................................................15

6.0 Conclusion...............................................................................................................................16

References......................................................................................................................................17

Appendices....................................................................................................................................19

Page 2 of 19

Table of Contents.............................................................................................................................2

1.0 Summary of the Process............................................................................................................3

2.0 Advantages and Disadvantages of Balance Scorecard (BSC)...................................................6

2.1 Advantages............................................................................................................................6

2.2 Disadvantages........................................................................................................................6

3.0 Identification of Critical Success Factors (CSFs)......................................................................8

3.1 Clients’ Perspectives..............................................................................................................8

3.2 Internal Process Perspectives.................................................................................................8

3.3 Financial Perspectives...........................................................................................................9

3.4 Workforce Perspectives.......................................................................................................10

4.0 Proposed Balance Scorecard and Performance Measurement.................................................11

5.0 Proposed Strategy Map............................................................................................................15

6.0 Conclusion...............................................................................................................................16

References......................................................................................................................................17

Appendices....................................................................................................................................19

Page 2 of 19

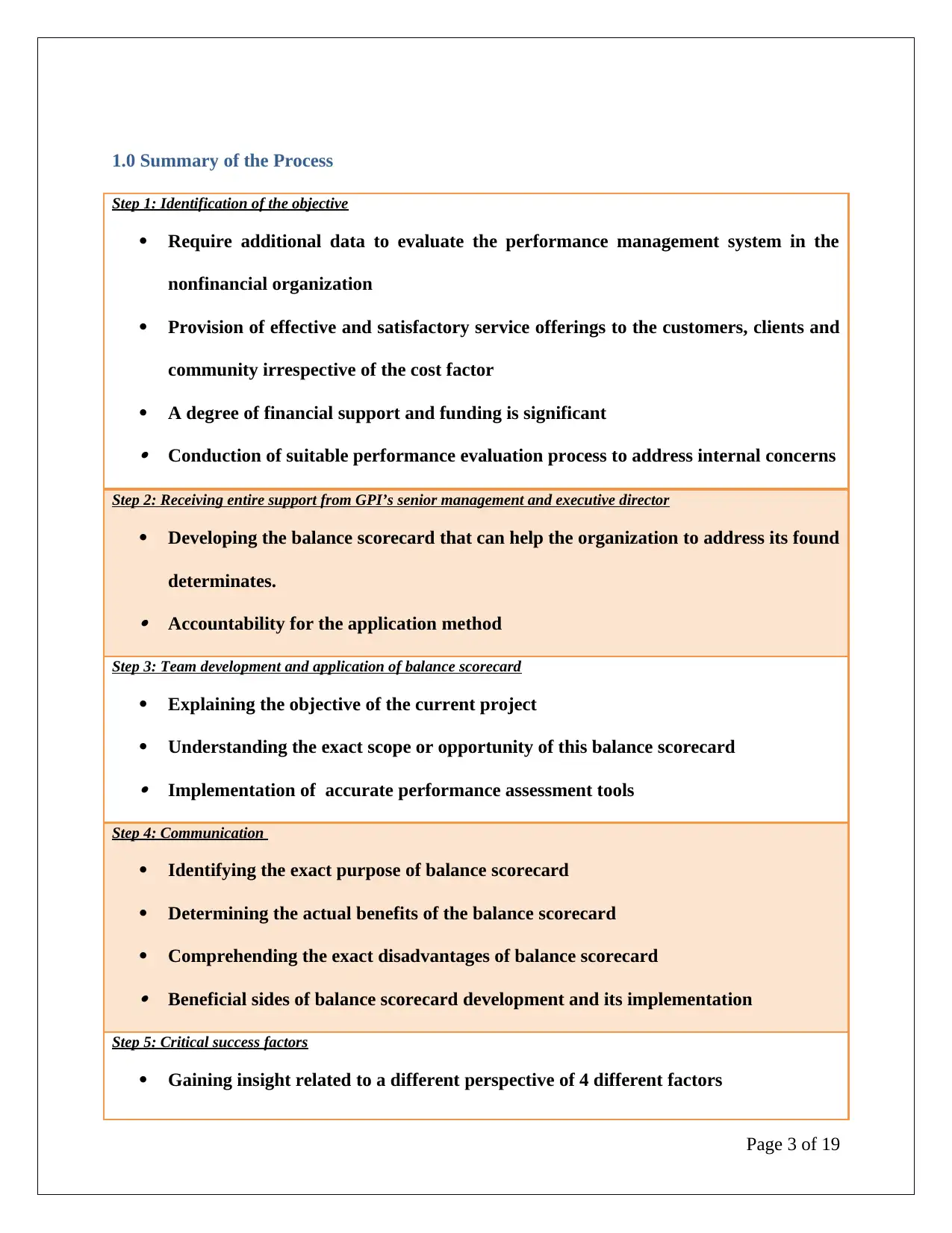

1.0 Summary of the Process

Step 1: Identification of the objective

Require additional data to evaluate the performance management system in the

nonfinancial organization

Provision of effective and satisfactory service offerings to the customers, clients and

community irrespective of the cost factor

A degree of financial support and funding is significant Conduction of suitable performance evaluation process to address internal concerns

Step 2: Receiving entire support from GPI’s senior management and executive director

Developing the balance scorecard that can help the organization to address its found

determinates. Accountability for the application method

Step 3: Team development and application of balance scorecard

Explaining the objective of the current project

Understanding the exact scope or opportunity of this balance scorecard Implementation of accurate performance assessment tools

Step 4: Communication

Identifying the exact purpose of balance scorecard

Determining the actual benefits of the balance scorecard

Comprehending the exact disadvantages of balance scorecard Beneficial sides of balance scorecard development and its implementation

Step 5: Critical success factors

Gaining insight related to a different perspective of 4 different factors

Page 3 of 19

Step 1: Identification of the objective

Require additional data to evaluate the performance management system in the

nonfinancial organization

Provision of effective and satisfactory service offerings to the customers, clients and

community irrespective of the cost factor

A degree of financial support and funding is significant Conduction of suitable performance evaluation process to address internal concerns

Step 2: Receiving entire support from GPI’s senior management and executive director

Developing the balance scorecard that can help the organization to address its found

determinates. Accountability for the application method

Step 3: Team development and application of balance scorecard

Explaining the objective of the current project

Understanding the exact scope or opportunity of this balance scorecard Implementation of accurate performance assessment tools

Step 4: Communication

Identifying the exact purpose of balance scorecard

Determining the actual benefits of the balance scorecard

Comprehending the exact disadvantages of balance scorecard Beneficial sides of balance scorecard development and its implementation

Step 5: Critical success factors

Gaining insight related to a different perspective of 4 different factors

Page 3 of 19

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

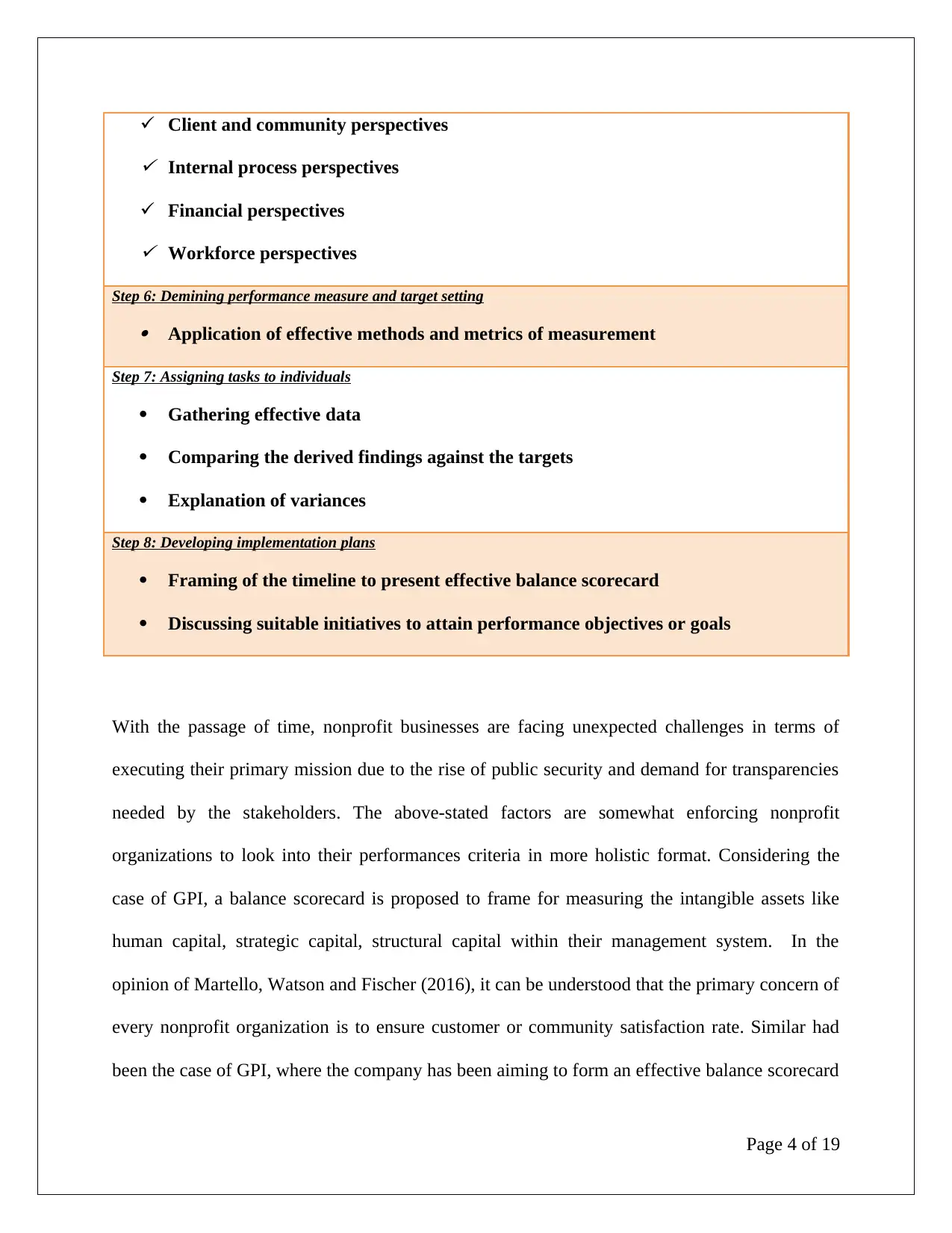

Client and community perspectives Internal process perspectives

Financial perspectives Workforce perspectives

Step 6: Demining performance measure and target setting Application of effective methods and metrics of measurement

Step 7: Assigning tasks to individuals

Gathering effective data

Comparing the derived findings against the targets

Explanation of variances

Step 8: Developing implementation plans

Framing of the timeline to present effective balance scorecard

Discussing suitable initiatives to attain performance objectives or goals

With the passage of time, nonprofit businesses are facing unexpected challenges in terms of

executing their primary mission due to the rise of public security and demand for transparencies

needed by the stakeholders. The above-stated factors are somewhat enforcing nonprofit

organizations to look into their performances criteria in more holistic format. Considering the

case of GPI, a balance scorecard is proposed to frame for measuring the intangible assets like

human capital, strategic capital, structural capital within their management system. In the

opinion of Martello, Watson and Fischer (2016), it can be understood that the primary concern of

every nonprofit organization is to ensure customer or community satisfaction rate. Similar had

been the case of GPI, where the company has been aiming to form an effective balance scorecard

Page 4 of 19

Financial perspectives Workforce perspectives

Step 6: Demining performance measure and target setting Application of effective methods and metrics of measurement

Step 7: Assigning tasks to individuals

Gathering effective data

Comparing the derived findings against the targets

Explanation of variances

Step 8: Developing implementation plans

Framing of the timeline to present effective balance scorecard

Discussing suitable initiatives to attain performance objectives or goals

With the passage of time, nonprofit businesses are facing unexpected challenges in terms of

executing their primary mission due to the rise of public security and demand for transparencies

needed by the stakeholders. The above-stated factors are somewhat enforcing nonprofit

organizations to look into their performances criteria in more holistic format. Considering the

case of GPI, a balance scorecard is proposed to frame for measuring the intangible assets like

human capital, strategic capital, structural capital within their management system. In the

opinion of Martello, Watson and Fischer (2016), it can be understood that the primary concern of

every nonprofit organization is to ensure customer or community satisfaction rate. Similar had

been the case of GPI, where the company has been aiming to form an effective balance scorecard

Page 4 of 19

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

to evaluate its performance criteria and the suitable propositions it can include in future to

resolve its existing shortcomings. It would also help the management to comprehend the

expertise level of its staff and also the potential of its internal methods to meet the rising

demands of the society. Since the brand entirely depends on fund collectors or donators,

therefore, it also needs to ensure that the funds are effectively used on elevating the service

standards that can help the dysfunctional community to enrich their standards of living.

The current project aims to evaluate the performance management process of GPI, based on

which a suitable balance scorecard framework would be proposed to enhance the service

standards and performances of GPI. At the beginning of the study, the researcher lays down the

detailed process flow as to the topic of BSC supported by a brief discussion on the advantages

and disadvantages of BSC. In the subsequent parts of the paper, the researcher identifies the

CSFs based on the given case study and thereby proposes the BSC required for the instant case

scenario. In addition, the paper provides a strategy map for the organization. Finally, the

researcher wraps up the discussion by way of concluding note.

Page 5 of 19

resolve its existing shortcomings. It would also help the management to comprehend the

expertise level of its staff and also the potential of its internal methods to meet the rising

demands of the society. Since the brand entirely depends on fund collectors or donators,

therefore, it also needs to ensure that the funds are effectively used on elevating the service

standards that can help the dysfunctional community to enrich their standards of living.

The current project aims to evaluate the performance management process of GPI, based on

which a suitable balance scorecard framework would be proposed to enhance the service

standards and performances of GPI. At the beginning of the study, the researcher lays down the

detailed process flow as to the topic of BSC supported by a brief discussion on the advantages

and disadvantages of BSC. In the subsequent parts of the paper, the researcher identifies the

CSFs based on the given case study and thereby proposes the BSC required for the instant case

scenario. In addition, the paper provides a strategy map for the organization. Finally, the

researcher wraps up the discussion by way of concluding note.

Page 5 of 19

2.0 Advantages and Disadvantages of Balance Scorecard (BSC)

2.1 Advantages

BSC may be considered to be one of the most widely used frameworks for the managerial

decision making as the model provides in insight into the CSFs of the organization in terms of

relevant measures and initiatives to be undertaken by the organization in order to achieve

operational excellence. First of all, it may be stated that the BSC provides a structure and well-

defined framework for the formulation of business strategy. Moreover, it helps the management

to align the various departments and units of the operations. There have been instances where the

implementation of the model has enabled to management to integrate the business processes and

its elements in coherent manner and thereby enhance the productivity as a whole. To put it

differently, it may be construed that the BSC provides guidelines for the management to align

individual aims with that of the organizational aims (Boateng, Akamavi and Ndoro, 2016). It

may also be noted that the framework helps the management to manage employees in terms of

their satisfaction, productivity and objectives (Cooper, Ezzamel and Qu, 2017).

2.2 Disadvantages

On the contrary, BSC may be alleged to have been suffering from certain inherent limitations.

One of the prominent disadvantages of BSC is that the implementation of BSC may prove to be

costly, especially for the small business houses. Since the model is comparatively complex to

understand and hence requires training, there remains a cost implication, which small-sized firms

may not be able to afford, at times. In addition, it may also be observed that the BSC may not be

replicated from the past examples and experiences. BSC assumes that every aspect of the

business is synced with each other which may not be true at times. Moreover, the primary

Page 6 of 19

2.1 Advantages

BSC may be considered to be one of the most widely used frameworks for the managerial

decision making as the model provides in insight into the CSFs of the organization in terms of

relevant measures and initiatives to be undertaken by the organization in order to achieve

operational excellence. First of all, it may be stated that the BSC provides a structure and well-

defined framework for the formulation of business strategy. Moreover, it helps the management

to align the various departments and units of the operations. There have been instances where the

implementation of the model has enabled to management to integrate the business processes and

its elements in coherent manner and thereby enhance the productivity as a whole. To put it

differently, it may be construed that the BSC provides guidelines for the management to align

individual aims with that of the organizational aims (Boateng, Akamavi and Ndoro, 2016). It

may also be noted that the framework helps the management to manage employees in terms of

their satisfaction, productivity and objectives (Cooper, Ezzamel and Qu, 2017).

2.2 Disadvantages

On the contrary, BSC may be alleged to have been suffering from certain inherent limitations.

One of the prominent disadvantages of BSC is that the implementation of BSC may prove to be

costly, especially for the small business houses. Since the model is comparatively complex to

understand and hence requires training, there remains a cost implication, which small-sized firms

may not be able to afford, at times. In addition, it may also be observed that the BSC may not be

replicated from the past examples and experiences. BSC assumes that every aspect of the

business is synced with each other which may not be true at times. Moreover, the primary

Page 6 of 19

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

essence of BSC may seem to be rigid to practically implement most of the times (Cooper,

Ezzamel and Qu, 2017)

Page 7 of 19

Ezzamel and Qu, 2017)

Page 7 of 19

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

3.0 Identification of Critical Success Factors (CSFs)

3.1 Clients’ Perspectives

It has been identified from the provided case study that the client plays the most significant role

in GPI business. Welfare and improving the standard of living of a dysfunction society has been

the foremost objective of the organization, therefore, understanding the accurate requirements of

clients and their perspectives would be highly necessitated for the nonprofit business. In the

opinion of Martello, Watson and Fischer (2016), customer satisfaction has been the core target of

this business. Hence, the organization shall not only focus on the basic service lines but also

render on activities that can help the business to enrich the value proposition index of its clients.

Establishing a new service line to accelerate the brand image shall not be the main consideration

of the organization, rather, helping the community to gain actual satisfaction shall be its key

performance indicator to depict or measure the actual success of this business (Gibbons and

Kaplan, 2015). Moreover, the provision of assessed quality service would be an effective

indicator to gauge the satisfaction level of clients and also his family members’ satisfaction level.

The specific method can be followed by conducting a periodical survey and collecting clients’

feedback against the offered services. This can definitely assist the management with adequate

positive and negative feedbacks. The negative opinions can definitely support GPI to identify

their loopholes and accordingly addressing with suitable solutions for process improvements.

This approach can guarantee the highest service standards where GPI definitely enhance its

clients' satisfaction ate with its offerings.

Page 8 of 19

3.1 Clients’ Perspectives

It has been identified from the provided case study that the client plays the most significant role

in GPI business. Welfare and improving the standard of living of a dysfunction society has been

the foremost objective of the organization, therefore, understanding the accurate requirements of

clients and their perspectives would be highly necessitated for the nonprofit business. In the

opinion of Martello, Watson and Fischer (2016), customer satisfaction has been the core target of

this business. Hence, the organization shall not only focus on the basic service lines but also

render on activities that can help the business to enrich the value proposition index of its clients.

Establishing a new service line to accelerate the brand image shall not be the main consideration

of the organization, rather, helping the community to gain actual satisfaction shall be its key

performance indicator to depict or measure the actual success of this business (Gibbons and

Kaplan, 2015). Moreover, the provision of assessed quality service would be an effective

indicator to gauge the satisfaction level of clients and also his family members’ satisfaction level.

The specific method can be followed by conducting a periodical survey and collecting clients’

feedback against the offered services. This can definitely assist the management with adequate

positive and negative feedbacks. The negative opinions can definitely support GPI to identify

their loopholes and accordingly addressing with suitable solutions for process improvements.

This approach can guarantee the highest service standards where GPI definitely enhance its

clients' satisfaction ate with its offerings.

Page 8 of 19

3.2 Internal Process Perspectives

The internal process perspectives for the balance scorecard need to stem from the business

methods of GPI that can manage to create maximum impact on its community or customer

satisfaction. Factors that usually affect the internal process of GPI include cycle time, employee

skills, quality, clients’ expectation management and productivity. In the consideration of

Gibbons and Kaplan (2015), organizations especially the one operating in the nonprofit zone

shall attempt to recognize and determine it's business’ core competencies and installation of right

technical support to elevate clients’ satisfaction level. It has been assessed from the provided

case that GPI has a number of effective internal processes to elevate the value margin amongst

clients and the community as a whole. The brand is also experiencing a constant alternation in

the process, which required effective and proactive technical servers to trace and record the huge

lists of the client and the services they require or have been offered to them (Muda, Erlina and

Nasution, 2018). This approach can help GPI to maintain a positive and healthy relationship with

clients and community members. A rise in the efficacy level ensures that clients or customers

are getting required attentions through the necessary tools and equipment. On the other hand, the

allocation of budget and its application in the right process has been another critical factor to

guarantee that community has been entirely benefitted from the fund collected for the purpose

rather 5than spending on miscellaneous or variable expenses.

3.3 Financial Perspectives

The financial performance of the organization has been considered to be stable as the appendices

establish the same. However, an insight into the financial facts and figures may reveal that the

organization primarily depends on the state funding for revenue generation. In this context, it

may be stated that the CSFS with respect to the financial perspectives of a non-profit

Page 9 of 19

The internal process perspectives for the balance scorecard need to stem from the business

methods of GPI that can manage to create maximum impact on its community or customer

satisfaction. Factors that usually affect the internal process of GPI include cycle time, employee

skills, quality, clients’ expectation management and productivity. In the consideration of

Gibbons and Kaplan (2015), organizations especially the one operating in the nonprofit zone

shall attempt to recognize and determine it's business’ core competencies and installation of right

technical support to elevate clients’ satisfaction level. It has been assessed from the provided

case that GPI has a number of effective internal processes to elevate the value margin amongst

clients and the community as a whole. The brand is also experiencing a constant alternation in

the process, which required effective and proactive technical servers to trace and record the huge

lists of the client and the services they require or have been offered to them (Muda, Erlina and

Nasution, 2018). This approach can help GPI to maintain a positive and healthy relationship with

clients and community members. A rise in the efficacy level ensures that clients or customers

are getting required attentions through the necessary tools and equipment. On the other hand, the

allocation of budget and its application in the right process has been another critical factor to

guarantee that community has been entirely benefitted from the fund collected for the purpose

rather 5than spending on miscellaneous or variable expenses.

3.3 Financial Perspectives

The financial performance of the organization has been considered to be stable as the appendices

establish the same. However, an insight into the financial facts and figures may reveal that the

organization primarily depends on the state funding for revenue generation. In this context, it

may be stated that the CSFS with respect to the financial perspectives of a non-profit

Page 9 of 19

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

organization is critical to assess before implementing a BSC framework therein. Since the

primary goal of the organization is not oriented towards profit seeing, the financial parameters

should be prioritized to accumulate the surplus which, in turn, will be utilized towards the

community and society as a whole (Kalender and Vayvay, 2016).

3.4 Workforce Perspectives

According to Moullin (2017), the above-mentioned factors and activities cannot be conducted if

the resources management in done inefficiently within the workplace. Since GPI is a nonprofit

organization that specifically offers health-related and welfare service to the community,

therefore, the resources need to be well trained to have the correct product knowledge and

understand the actual issues of clients and prescribe the best fit services accordingly. To serve

effectively to the disabled society required adequate training in which the workforce shall use

their expertise to improve the standards of living. Employees also require effective rewards and

support to retain their degree of motivation in the workplace. Hence, the management of GPI

needs to identify its employees' needs and the supports they require further to improve their

service offerings (Hansen and Schaltegger, 2017).

Page 10 of 19

primary goal of the organization is not oriented towards profit seeing, the financial parameters

should be prioritized to accumulate the surplus which, in turn, will be utilized towards the

community and society as a whole (Kalender and Vayvay, 2016).

3.4 Workforce Perspectives

According to Moullin (2017), the above-mentioned factors and activities cannot be conducted if

the resources management in done inefficiently within the workplace. Since GPI is a nonprofit

organization that specifically offers health-related and welfare service to the community,

therefore, the resources need to be well trained to have the correct product knowledge and

understand the actual issues of clients and prescribe the best fit services accordingly. To serve

effectively to the disabled society required adequate training in which the workforce shall use

their expertise to improve the standards of living. Employees also require effective rewards and

support to retain their degree of motivation in the workplace. Hence, the management of GPI

needs to identify its employees' needs and the supports they require further to improve their

service offerings (Hansen and Schaltegger, 2017).

Page 10 of 19

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

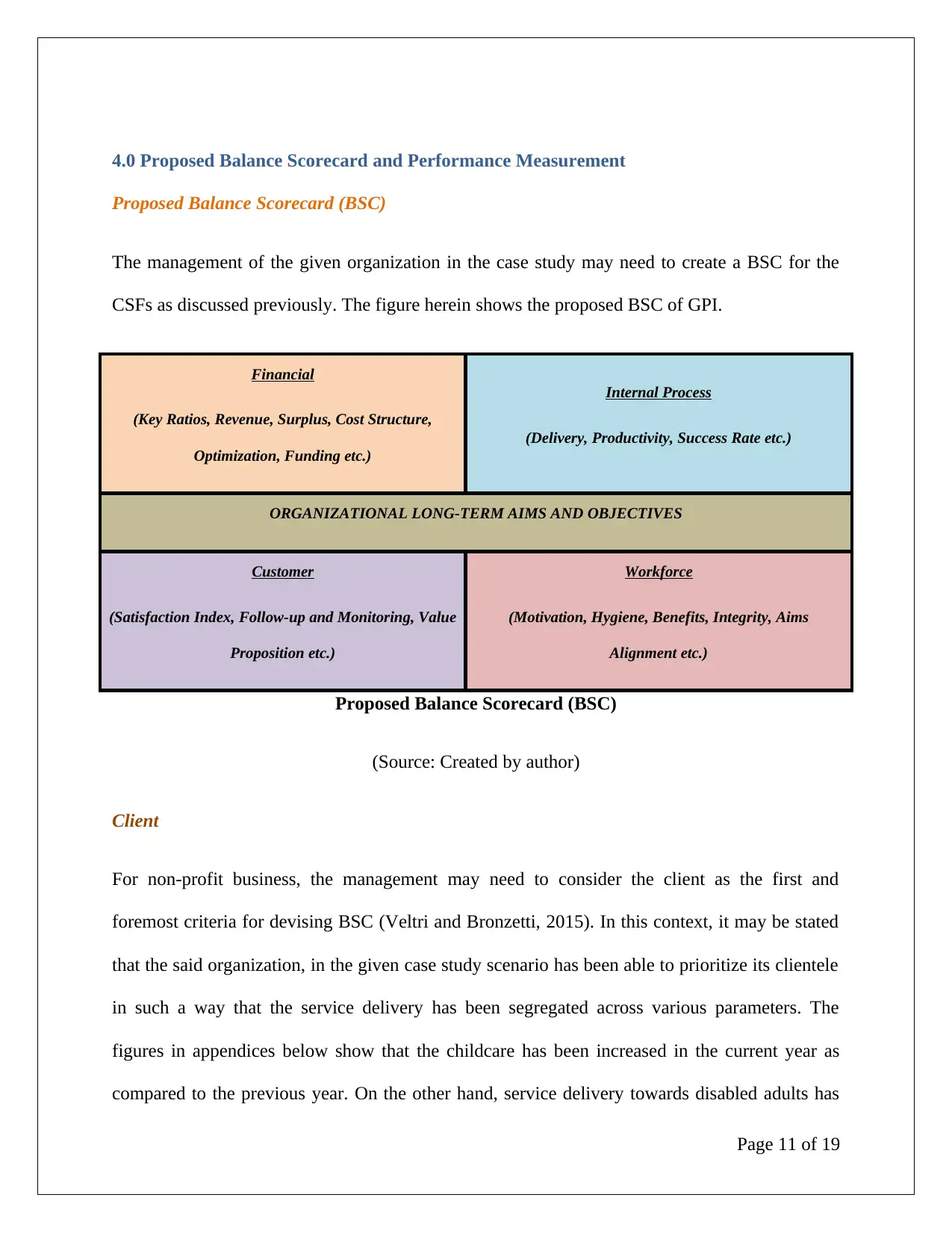

4.0 Proposed Balance Scorecard and Performance Measurement

Proposed Balance Scorecard (BSC)

The management of the given organization in the case study may need to create a BSC for the

CSFs as discussed previously. The figure herein shows the proposed BSC of GPI.

Financial

(Key Ratios, Revenue, Surplus, Cost Structure,

Optimization, Funding etc.)

Internal Process

(Delivery, Productivity, Success Rate etc.)

ORGANIZATIONAL LONG-TERM AIMS AND OBJECTIVES

Customer

(Satisfaction Index, Follow-up and Monitoring, Value

Proposition etc.)

Workforce

(Motivation, Hygiene, Benefits, Integrity, Aims

Alignment etc.)

Proposed Balance Scorecard (BSC)

(Source: Created by author)

Client

For non-profit business, the management may need to consider the client as the first and

foremost criteria for devising BSC (Veltri and Bronzetti, 2015). In this context, it may be stated

that the said organization, in the given case study scenario has been able to prioritize its clientele

in such a way that the service delivery has been segregated across various parameters. The

figures in appendices below show that the childcare has been increased in the current year as

compared to the previous year. On the other hand, service delivery towards disabled adults has

Page 11 of 19

Proposed Balance Scorecard (BSC)

The management of the given organization in the case study may need to create a BSC for the

CSFs as discussed previously. The figure herein shows the proposed BSC of GPI.

Financial

(Key Ratios, Revenue, Surplus, Cost Structure,

Optimization, Funding etc.)

Internal Process

(Delivery, Productivity, Success Rate etc.)

ORGANIZATIONAL LONG-TERM AIMS AND OBJECTIVES

Customer

(Satisfaction Index, Follow-up and Monitoring, Value

Proposition etc.)

Workforce

(Motivation, Hygiene, Benefits, Integrity, Aims

Alignment etc.)

Proposed Balance Scorecard (BSC)

(Source: Created by author)

Client

For non-profit business, the management may need to consider the client as the first and

foremost criteria for devising BSC (Veltri and Bronzetti, 2015). In this context, it may be stated

that the said organization, in the given case study scenario has been able to prioritize its clientele

in such a way that the service delivery has been segregated across various parameters. The

figures in appendices below show that the childcare has been increased in the current year as

compared to the previous year. On the other hand, service delivery towards disabled adults has

Page 11 of 19

been declined substantially. Similarly, the various program undertaken by the organization for

the4 disabled persons have experienced a fluctuation in terms of service delivery and the

management hence, may need to take a note of the same for the purpose of devising BSC in this

regards (Boateng, Akamavi and Ndoro, 2016). The senior management and the persons

responsible for the given programs may be given the charge to look into the matter and adopt the

necessary measures in order to assess the implication for such fluctuation and enhance the client

servicing framework in line with organizational objectives.

Internal process

The internal process of the organization has been strong and efficient with effective internal

control in place. the figures and information as provided in the given case study may show that

the service provided by the firm has been well praised and critically acclaimed by various houses

and have been awarded largely. The service delivery may, therefore, be construed to be synced

with the larger framework of organization objectives of GPI.

Financial

The financial parameters of the firm may exhibit that the adult residential services have been the

major sources of expenditure with the lion's share of 62% of entire revenue earned for the given

financial year. On the contrary, state funding is the primary source of revenue for the firm with

67% proportion of total revenue. Therefore, the key elements in the financial framework are

these two heads where most of the revenues are generated and expended simultaneously. The

managers may need to consider these two aspects of the operations and evaluate the respective

risks of non-attaining the given parameters within the stipulated guidelines of GPI. The

deviations must be accounted for in a timely and efficient manner so that the necessary measures

Page 12 of 19

the4 disabled persons have experienced a fluctuation in terms of service delivery and the

management hence, may need to take a note of the same for the purpose of devising BSC in this

regards (Boateng, Akamavi and Ndoro, 2016). The senior management and the persons

responsible for the given programs may be given the charge to look into the matter and adopt the

necessary measures in order to assess the implication for such fluctuation and enhance the client

servicing framework in line with organizational objectives.

Internal process

The internal process of the organization has been strong and efficient with effective internal

control in place. the figures and information as provided in the given case study may show that

the service provided by the firm has been well praised and critically acclaimed by various houses

and have been awarded largely. The service delivery may, therefore, be construed to be synced

with the larger framework of organization objectives of GPI.

Financial

The financial parameters of the firm may exhibit that the adult residential services have been the

major sources of expenditure with the lion's share of 62% of entire revenue earned for the given

financial year. On the contrary, state funding is the primary source of revenue for the firm with

67% proportion of total revenue. Therefore, the key elements in the financial framework are

these two heads where most of the revenues are generated and expended simultaneously. The

managers may need to consider these two aspects of the operations and evaluate the respective

risks of non-attaining the given parameters within the stipulated guidelines of GPI. The

deviations must be accounted for in a timely and efficient manner so that the necessary measures

Page 12 of 19

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.