Financial Analysis of Tesco PLC: Expansion, Budgeting, and Planning

VerifiedAdded on 2020/01/07

|16

|3874

|166

Report

AI Summary

This report provides a comprehensive financial analysis of Tesco PLC, addressing key aspects of financial management in the context of a planned expansion. The analysis begins with an examination of various sources of finance available to Tesco, evaluating their suitability for the company'...

Mohammad Zubair

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CONTENTS

INTRODUCTION...........................................................................................................................4

TASK 1............................................................................................................................................4

Sources of finance that can be used by firm and evaluating their appropriateness.....................4

TASK 2............................................................................................................................................5

Impact of finances on financial statements..................................................................................5

TASK 3............................................................................................................................................6

Importance of financial budgeting and planning.........................................................................6

Information needs of different decision makers..........................................................................6

TASK 4............................................................................................................................................6

Calculation of variances...............................................................................................................6

TASK 5............................................................................................................................................7

Pay back period............................................................................................................................7

Accounting rate of return (ARR).................................................................................................8

Net present value (NPV) and Internal rate of return (IRR).........................................................8

TASK 6..........................................................................................................................................10

1. Calculation of gross profit and net profit ..............................................................................10

2. Calculation of most profitable plan........................................................................................10

3. Profit computation on dealing with ASDA............................................................................11

TASK 7..........................................................................................................................................12

Comparison of appropriate formats of financial statement for different types of firms............12

TASK 8..........................................................................................................................................12

Interpretation of 2012 annual reports for Tesco Plc using suitable ratios.................................12

Conclusion ....................................................................................................................................15

REFERENCES..............................................................................................................................16

2

INTRODUCTION...........................................................................................................................4

TASK 1............................................................................................................................................4

Sources of finance that can be used by firm and evaluating their appropriateness.....................4

TASK 2............................................................................................................................................5

Impact of finances on financial statements..................................................................................5

TASK 3............................................................................................................................................6

Importance of financial budgeting and planning.........................................................................6

Information needs of different decision makers..........................................................................6

TASK 4............................................................................................................................................6

Calculation of variances...............................................................................................................6

TASK 5............................................................................................................................................7

Pay back period............................................................................................................................7

Accounting rate of return (ARR).................................................................................................8

Net present value (NPV) and Internal rate of return (IRR).........................................................8

TASK 6..........................................................................................................................................10

1. Calculation of gross profit and net profit ..............................................................................10

2. Calculation of most profitable plan........................................................................................10

3. Profit computation on dealing with ASDA............................................................................11

TASK 7..........................................................................................................................................12

Comparison of appropriate formats of financial statement for different types of firms............12

TASK 8..........................................................................................................................................12

Interpretation of 2012 annual reports for Tesco Plc using suitable ratios.................................12

Conclusion ....................................................................................................................................15

REFERENCES..............................................................................................................................16

2

Index of Tables

Table 1: Calculation of pay back period of Bend it Well BiW36....................................................7

Table 2: Calculation of pay back period of Turn it Fast TiF21......................................................8

Table 3: Calculation of NPV and IRR of Bend it Well BiW36.......................................................9

Table 4: Calculation of NPV and IRR of Turn it Fast TiF21.........................................................9

Table 5: Calculation of profits under both the proposals...............................................................11

Table 6: Computation of profit with dealing with ASDA.............................................................11

3

Table 1: Calculation of pay back period of Bend it Well BiW36....................................................7

Table 2: Calculation of pay back period of Turn it Fast TiF21......................................................8

Table 3: Calculation of NPV and IRR of Bend it Well BiW36.......................................................9

Table 4: Calculation of NPV and IRR of Turn it Fast TiF21.........................................................9

Table 5: Calculation of profits under both the proposals...............................................................11

Table 6: Computation of profit with dealing with ASDA.............................................................11

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Managing financial resources is a crucial business activity that assists in attaining business goals

in an effective manner. It is important for the business to make allocation of resources as per the

need of finances (Caglayan and Demir, 2014) This is because it ensures proper management of

cash. In the present study, management of financial resources will be discussed with respect to

Tesco plc. This study includes sources of finance and their implications. Furthermore it covers

importance of financial planning and information needs for different decision makers.

TASK 1

In the scenario given, Tesco, one of the major retailers, is planning for expansion of its

operations. In regards to this, the points below have been discussed:

Sources of finance that can be used by firm and evaluating their appropriateness

There are various sources of finance that can be used by Tesco. These includes

Factoring: This is considered as one of the sources available within the business. It is referred to

as financial transaction among the owner of the business and a third party that offers cash

instantly on the exchange of account receivables of the firm. It is sales of receivables of the

organisation (Fabregat-Sanjuan, Ferrando and De la Flor, 2015). It is appropriate in the sense

that it gives Tesco quick cash. In addition to this it minimizes the risk associated with bad debt.

Overdraft: Under this source of finance, the organisation can withdraw more amounts in

comparison to the existing one in the bank. This facility can be availed by Tesco in order to meet

its working capital requirements.

Bank loan: Tesco can also borrow funds by taking loans from financial institutions. This requires

the business to keep some assets as security (Gertler and Kiyotaki, 2010). This acts as an aid for

the company in meeting its long term need for finance. Debenture: Furthermore, the corporation can issue debentures to the public in order to

borrow funds for the purpose of accomplishing its long term obligations.

4

Managing financial resources is a crucial business activity that assists in attaining business goals

in an effective manner. It is important for the business to make allocation of resources as per the

need of finances (Caglayan and Demir, 2014) This is because it ensures proper management of

cash. In the present study, management of financial resources will be discussed with respect to

Tesco plc. This study includes sources of finance and their implications. Furthermore it covers

importance of financial planning and information needs for different decision makers.

TASK 1

In the scenario given, Tesco, one of the major retailers, is planning for expansion of its

operations. In regards to this, the points below have been discussed:

Sources of finance that can be used by firm and evaluating their appropriateness

There are various sources of finance that can be used by Tesco. These includes

Factoring: This is considered as one of the sources available within the business. It is referred to

as financial transaction among the owner of the business and a third party that offers cash

instantly on the exchange of account receivables of the firm. It is sales of receivables of the

organisation (Fabregat-Sanjuan, Ferrando and De la Flor, 2015). It is appropriate in the sense

that it gives Tesco quick cash. In addition to this it minimizes the risk associated with bad debt.

Overdraft: Under this source of finance, the organisation can withdraw more amounts in

comparison to the existing one in the bank. This facility can be availed by Tesco in order to meet

its working capital requirements.

Bank loan: Tesco can also borrow funds by taking loans from financial institutions. This requires

the business to keep some assets as security (Gertler and Kiyotaki, 2010). This acts as an aid for

the company in meeting its long term need for finance. Debenture: Furthermore, the corporation can issue debentures to the public in order to

borrow funds for the purpose of accomplishing its long term obligations.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Shares: Issue of shares is considered as a permanent source of capital for the business.

With this, the firm can gain financial resources from the general public by means of

issuing them shares.

There are various implications associated with different sources of finance. In case of

overdraft and bank loans, timely payments need to be made to the financial institution otherwise

legal actions can be taken against the company and it can be declared bankrupt (Shul'ga, 2014).

In addition to this issue of shares and debentures requires Tesco to make payment of dividend on

time. If the payment is not made, this forces the appropriate people to take legal action against

the firm.

TASK 2

Impact of finances on financial statements

According to the scenario, the company wishes to buy a warehouse costing £300,000. It is

considering debenture of a share issue for this purpose.

Debenture issue: The rate of interest on debenture is 4% and must be repaid within 25 years.

Hence, it will impose a financial cost of £12000 each year in the form of interest. In the

profitability statement, it will be shown as business expenses hence, profits will be reduced.

However, in the balance sheet, it will be subtracted from the cash balance while the amount of

debt taken amounted to £300,000 will be added in cash. Another point is, it is a long term loan

hence, it will be shown as a long term debt under the liability side. Furthermore, as it shows in

the assignment brief, the corporation tax rate is 20% and the interest payment on debt is

considered as an allowable expense. Therefore, it will reduce tax obligations and increase profits

for the organisation.

5

With this, the firm can gain financial resources from the general public by means of

issuing them shares.

There are various implications associated with different sources of finance. In case of

overdraft and bank loans, timely payments need to be made to the financial institution otherwise

legal actions can be taken against the company and it can be declared bankrupt (Shul'ga, 2014).

In addition to this issue of shares and debentures requires Tesco to make payment of dividend on

time. If the payment is not made, this forces the appropriate people to take legal action against

the firm.

TASK 2

Impact of finances on financial statements

According to the scenario, the company wishes to buy a warehouse costing £300,000. It is

considering debenture of a share issue for this purpose.

Debenture issue: The rate of interest on debenture is 4% and must be repaid within 25 years.

Hence, it will impose a financial cost of £12000 each year in the form of interest. In the

profitability statement, it will be shown as business expenses hence, profits will be reduced.

However, in the balance sheet, it will be subtracted from the cash balance while the amount of

debt taken amounted to £300,000 will be added in cash. Another point is, it is a long term loan

hence, it will be shown as a long term debt under the liability side. Furthermore, as it shows in

the assignment brief, the corporation tax rate is 20% and the interest payment on debt is

considered as an allowable expense. Therefore, it will reduce tax obligations and increase profits

for the organisation.

5

Share capital: If funds will be collected through issuing shares, than it will increase equity

capital and impose cost in the form of shareholders return. As per the scenario, expected returns

on dividend is 7% hence, will be equal to £21000. Issued share capital will be shown as equity in

the liability side of the balance sheet. What is more, it will increase cash balance in the current

assets head. However, payment of investors return to £21000 and will be reported as expenses in

the profit and loss account and will be subtracted from the available cash balance.

TASK 3

Importance of financial budgeting and planning

Financial planning and budgeting plays a significant role in carrying out the flow of business

operations in a smooth manner. The importance of financial planning is enumerated in the

manner as below:

Effective management of cash: There is a major role of financial planning towards effective cash

management. With this, this organisation can observe the outflow of financial resources while it

can also increase the amount of cash inflow within the organisation (Hannam, Liao, Davis and

Oppenheimer, 2015). Therefor, there is an appropriate role of financial planning in assisting

organisations to grow and expand.

Optimum utilization of financial resources: Through effective financial planning, assurance can

be given regarding the use of financial resources in optimum manner (Overton, 2007). With the

assistance, this decision can be taken by financial managers regarding the allotment of resources

in several business activities.

Information needs of different decision makers

There is existence of various decision makers who needs varied business information in order to

carry out decision making process. The decision makers along with their needs for information

have been stated below:

6

capital and impose cost in the form of shareholders return. As per the scenario, expected returns

on dividend is 7% hence, will be equal to £21000. Issued share capital will be shown as equity in

the liability side of the balance sheet. What is more, it will increase cash balance in the current

assets head. However, payment of investors return to £21000 and will be reported as expenses in

the profit and loss account and will be subtracted from the available cash balance.

TASK 3

Importance of financial budgeting and planning

Financial planning and budgeting plays a significant role in carrying out the flow of business

operations in a smooth manner. The importance of financial planning is enumerated in the

manner as below:

Effective management of cash: There is a major role of financial planning towards effective cash

management. With this, this organisation can observe the outflow of financial resources while it

can also increase the amount of cash inflow within the organisation (Hannam, Liao, Davis and

Oppenheimer, 2015). Therefor, there is an appropriate role of financial planning in assisting

organisations to grow and expand.

Optimum utilization of financial resources: Through effective financial planning, assurance can

be given regarding the use of financial resources in optimum manner (Overton, 2007). With the

assistance, this decision can be taken by financial managers regarding the allotment of resources

in several business activities.

Information needs of different decision makers

There is existence of various decision makers who needs varied business information in order to

carry out decision making process. The decision makers along with their needs for information

have been stated below:

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Investors: They are referred to as individuals who make investments in the organisation.

Therefor, in order to develop decisions for this sake, investors require information regarding

profitability positions of the companies like Tesco. This assists them in taking, regarding

whether the investment would yield in profitable returns (Jagman and et.al., 2014).

Suppliers: It includes the people who make supply of raw material to the business. Thus they

need information on liquidity and profitability position of the organisation. This is because they

want the company to make timely payments for their invoices.

TASK 4

Calculation of variances

Particulars Budgeted Actual Flex Variance

Units 2000 2700

Direct material 3200 3800 4320 520

Direct labour 2500 3500 3375 -125

Maintenance 1000 1300 1350 50

Depreciation 2000 2000 -2000

Rent and rates 1400 1900 1890 -10

Other costs 2500 2800 3375 575

From the above table of variance calculation it can be interpreted that there is variance in the

product units by 700. It can be because of increase in the demand for the product due to which

the company has to increase the number of production units. There is negative variance in the

direct material. This implies that the cost of material has increased significantly. Later on, this

increases the operations of the company to a greater extent. In addition to this there is presence

of negative variance within the direct labour. This presents the cost of labour that has increased

to a greater extent. Sometime later, it increases the entire labour cost incurred by the firm

(Larkin, 2011). The cost of maintenance has increased greatly when compared with actual

figures. This demonstrates that which is due to increase in volume of production and the overall

cost of maintenance which has enhanced to a greater extent. From the analysis of the variances it

7

Therefor, in order to develop decisions for this sake, investors require information regarding

profitability positions of the companies like Tesco. This assists them in taking, regarding

whether the investment would yield in profitable returns (Jagman and et.al., 2014).

Suppliers: It includes the people who make supply of raw material to the business. Thus they

need information on liquidity and profitability position of the organisation. This is because they

want the company to make timely payments for their invoices.

TASK 4

Calculation of variances

Particulars Budgeted Actual Flex Variance

Units 2000 2700

Direct material 3200 3800 4320 520

Direct labour 2500 3500 3375 -125

Maintenance 1000 1300 1350 50

Depreciation 2000 2000 -2000

Rent and rates 1400 1900 1890 -10

Other costs 2500 2800 3375 575

From the above table of variance calculation it can be interpreted that there is variance in the

product units by 700. It can be because of increase in the demand for the product due to which

the company has to increase the number of production units. There is negative variance in the

direct material. This implies that the cost of material has increased significantly. Later on, this

increases the operations of the company to a greater extent. In addition to this there is presence

of negative variance within the direct labour. This presents the cost of labour that has increased

to a greater extent. Sometime later, it increases the entire labour cost incurred by the firm

(Larkin, 2011). The cost of maintenance has increased greatly when compared with actual

figures. This demonstrates that which is due to increase in volume of production and the overall

cost of maintenance which has enhanced to a greater extent. From the analysis of the variances it

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

is shown that there is increase in other costs as well. This may be due to the increase in activities

relating with marketing, promotion and distribution that affects the entire production cost of the

organisation.

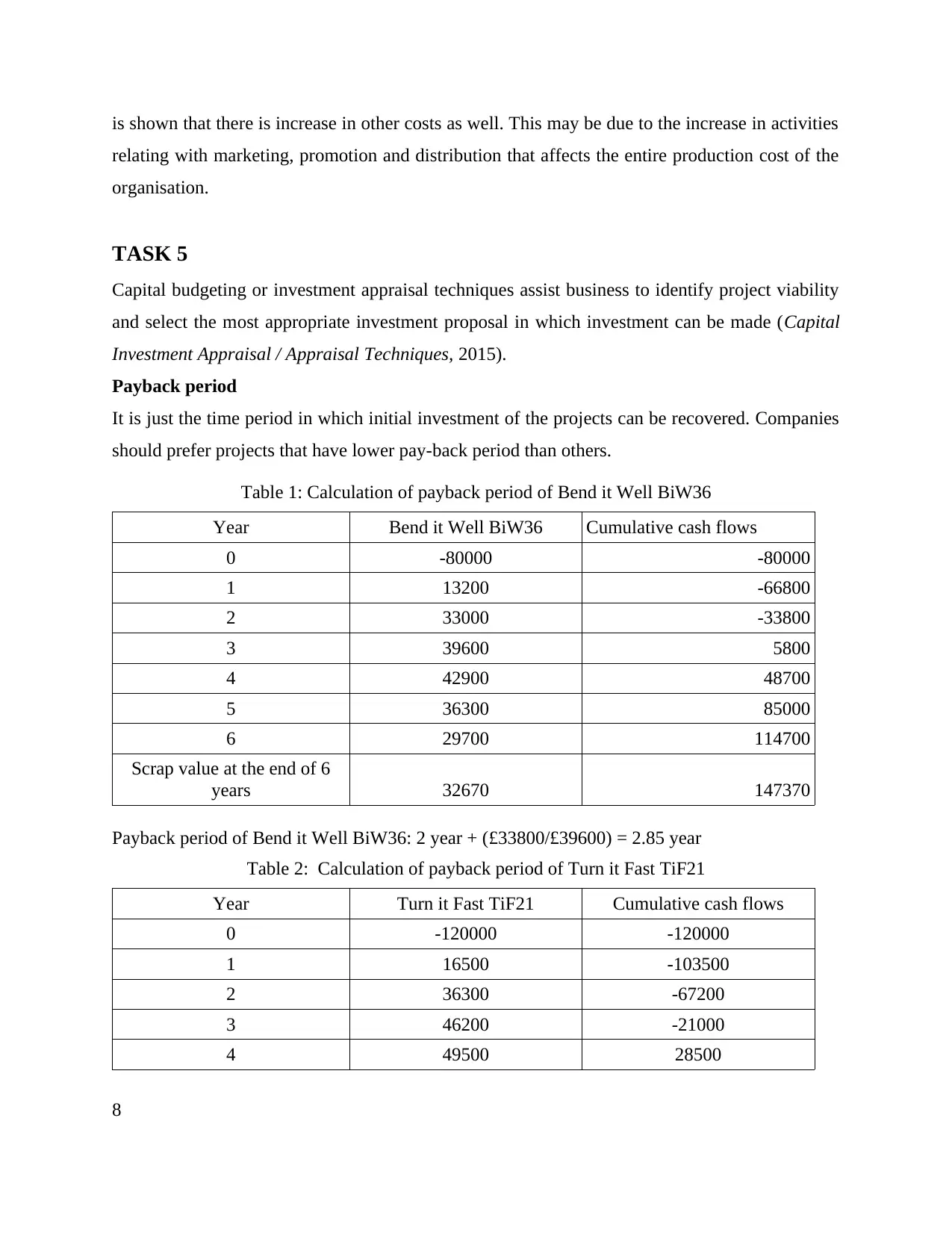

TASK 5

Capital budgeting or investment appraisal techniques assist business to identify project viability

and select the most appropriate investment proposal in which investment can be made (Capital

Investment Appraisal / Appraisal Techniques, 2015).

Payback period

It is just the time period in which initial investment of the projects can be recovered. Companies

should prefer projects that have lower pay-back period than others.

Table 1: Calculation of payback period of Bend it Well BiW36

Year Bend it Well BiW36 Cumulative cash flows

0 -80000 -80000

1 13200 -66800

2 33000 -33800

3 39600 5800

4 42900 48700

5 36300 85000

6 29700 114700

Scrap value at the end of 6

years 32670 147370

Payback period of Bend it Well BiW36: 2 year + (£33800/£39600) = 2.85 year

Table 2: Calculation of payback period of Turn it Fast TiF21

Year Turn it Fast TiF21 Cumulative cash flows

0 -120000 -120000

1 16500 -103500

2 36300 -67200

3 46200 -21000

4 49500 28500

8

relating with marketing, promotion and distribution that affects the entire production cost of the

organisation.

TASK 5

Capital budgeting or investment appraisal techniques assist business to identify project viability

and select the most appropriate investment proposal in which investment can be made (Capital

Investment Appraisal / Appraisal Techniques, 2015).

Payback period

It is just the time period in which initial investment of the projects can be recovered. Companies

should prefer projects that have lower pay-back period than others.

Table 1: Calculation of payback period of Bend it Well BiW36

Year Bend it Well BiW36 Cumulative cash flows

0 -80000 -80000

1 13200 -66800

2 33000 -33800

3 39600 5800

4 42900 48700

5 36300 85000

6 29700 114700

Scrap value at the end of 6

years 32670 147370

Payback period of Bend it Well BiW36: 2 year + (£33800/£39600) = 2.85 year

Table 2: Calculation of payback period of Turn it Fast TiF21

Year Turn it Fast TiF21 Cumulative cash flows

0 -120000 -120000

1 16500 -103500

2 36300 -67200

3 46200 -21000

4 49500 28500

8

5 42900 71400

6 26400 97800

Scrap value at the end of 6

years 30492 128292

Payback period of Turn it Fast TiF21 = 3 year + (£21000/£49500) = 3.42 year

Accounting rate of return (ARR)

It measures the rate of potential profits that can be generated over the initial project cost.

High ARR project seems to be more beneficial for the organisation because it provides greater

return.

ARR = Average annual profits/Inital investment*100

Bend it Well BiW36: (£227370/6)/(£80000)*100 = 47.37%

Turn it Fast TiF21: (£248292/6)/(£120000)*100 = 34.48%

Net present value (NPV) and Internal rate of return (IRR)

Both the methods are discounted methods and consider time and value of money. In NPV

method, all the associated future cash inflows will be discounted using a discount rate while the

excess of total discounted cash inflows over initial cash outlay is termed as NPV. Besides this,

IRR is the discount rate at which NPV of the project will be nil.

Table 3: Calculation of NPV and IRR of Bend it Well BiW36

Year Bend it Well BiW36 Discounted value

Discounted cash

flows

0 -80000 1 -80000

1 13200 0.9259259259 12222.22

2 33000 0.8573388203 28292.18

3 39600 0.793832241 31435.76

4 42900 0.7350298528 31532.78

5 36300 0.680583197 24705.17

6 29700 0.6301696269 18716.04

Scrap value at the end

of 6 years 32670 0.630169627 20587.64

Total 31.82% 87491.790406391

9

6 26400 97800

Scrap value at the end of 6

years 30492 128292

Payback period of Turn it Fast TiF21 = 3 year + (£21000/£49500) = 3.42 year

Accounting rate of return (ARR)

It measures the rate of potential profits that can be generated over the initial project cost.

High ARR project seems to be more beneficial for the organisation because it provides greater

return.

ARR = Average annual profits/Inital investment*100

Bend it Well BiW36: (£227370/6)/(£80000)*100 = 47.37%

Turn it Fast TiF21: (£248292/6)/(£120000)*100 = 34.48%

Net present value (NPV) and Internal rate of return (IRR)

Both the methods are discounted methods and consider time and value of money. In NPV

method, all the associated future cash inflows will be discounted using a discount rate while the

excess of total discounted cash inflows over initial cash outlay is termed as NPV. Besides this,

IRR is the discount rate at which NPV of the project will be nil.

Table 3: Calculation of NPV and IRR of Bend it Well BiW36

Year Bend it Well BiW36 Discounted value

Discounted cash

flows

0 -80000 1 -80000

1 13200 0.9259259259 12222.22

2 33000 0.8573388203 28292.18

3 39600 0.793832241 31435.76

4 42900 0.7350298528 31532.78

5 36300 0.680583197 24705.17

6 29700 0.6301696269 18716.04

Scrap value at the end

of 6 years 32670 0.630169627 20587.64

Total 31.82% 87491.790406391

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Table 4: Calculation of NPV and IRR of Turn it Fast TiF21

Year Turn it Fast TiF21 Discounted value

Discounted cash

flows

0 -120000 1 -120000

1 16500 0.9259259259 15277.78

2 36300 0.8573388203 31121.4

3 46200 0.793832241 36675.05

4 49500 0.7350298528 36383.98

5 42900 0.680583197 29197.02

6 26400 0.6301696269 16636.47

Scrap value at the end

of 6 years 30492 0.6301696269 19215.13

Total 21.17% 64506.83

Interpretation: From the basis of above computation, it became clear that the company should

adopt Bend it Well BiW36. Lower PP, high ARR, IRR and NPV are the reasons behind this

decision.

TASK 6

1. Calculation of gross profit and net profit

As per the scenario, per unit cost and selling price are £5.60 and £15.50 respectively. However,

annual fixed overhead is amounted to £79000. Gross profit is the excess of the total sales

revenue over the cost of sales. However, net profit is the excess of total revenues, over all the

fixed as well as variable overheads. For the given scenario, it has been calculated for 49500 units

and 39600 units as follows:

Particulars Amount Amount

Sales units 39600 49500

Sales 613,800 767,250

Less: Cost of sales 221,760 277,200

Gross profit 392,040 490,050

Less; Annual fixed overheads 79,000 79,000

10

Year Turn it Fast TiF21 Discounted value

Discounted cash

flows

0 -120000 1 -120000

1 16500 0.9259259259 15277.78

2 36300 0.8573388203 31121.4

3 46200 0.793832241 36675.05

4 49500 0.7350298528 36383.98

5 42900 0.680583197 29197.02

6 26400 0.6301696269 16636.47

Scrap value at the end

of 6 years 30492 0.6301696269 19215.13

Total 21.17% 64506.83

Interpretation: From the basis of above computation, it became clear that the company should

adopt Bend it Well BiW36. Lower PP, high ARR, IRR and NPV are the reasons behind this

decision.

TASK 6

1. Calculation of gross profit and net profit

As per the scenario, per unit cost and selling price are £5.60 and £15.50 respectively. However,

annual fixed overhead is amounted to £79000. Gross profit is the excess of the total sales

revenue over the cost of sales. However, net profit is the excess of total revenues, over all the

fixed as well as variable overheads. For the given scenario, it has been calculated for 49500 units

and 39600 units as follows:

Particulars Amount Amount

Sales units 39600 49500

Sales 613,800 767,250

Less: Cost of sales 221,760 277,200

Gross profit 392,040 490,050

Less; Annual fixed overheads 79,000 79,000

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

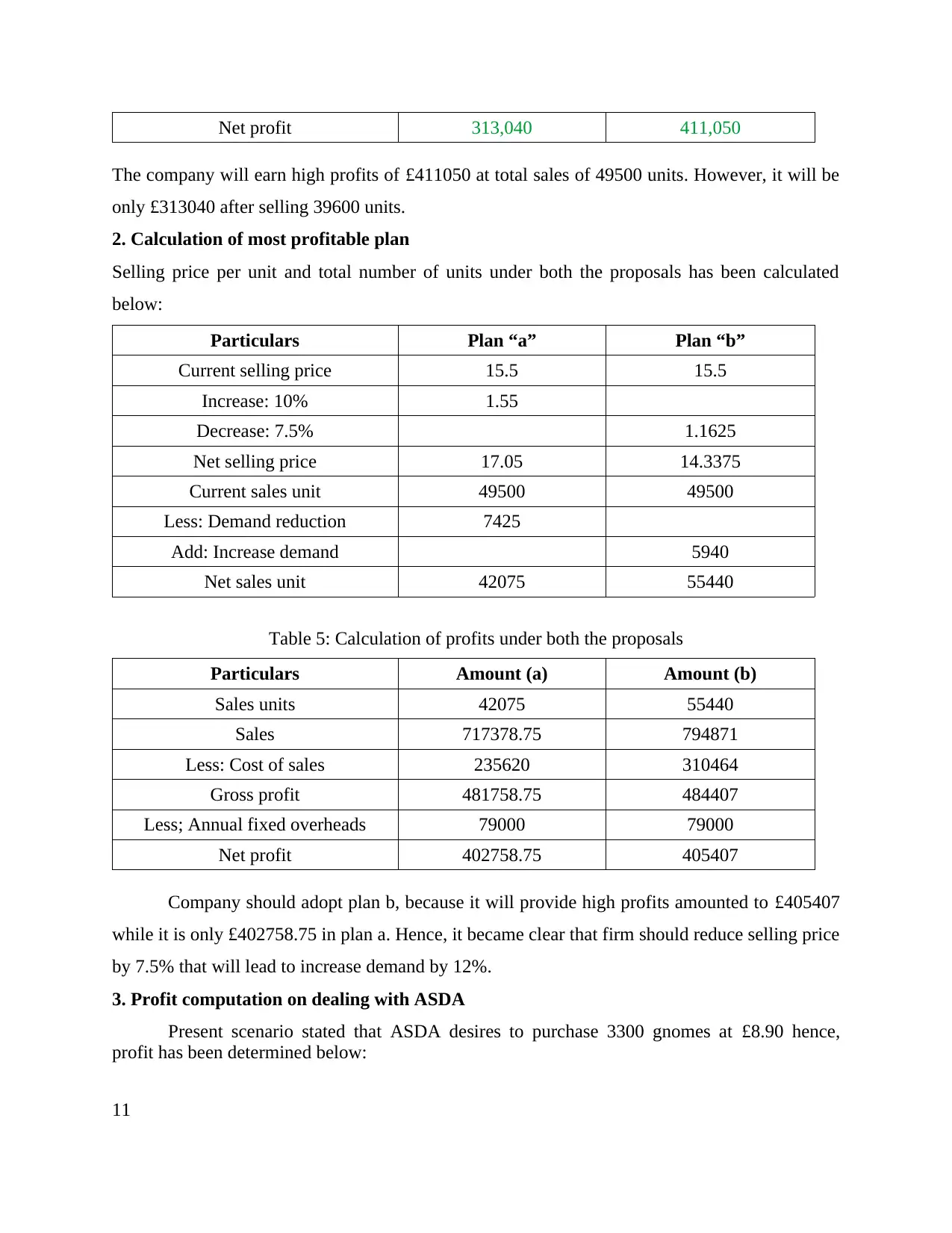

Net profit 313,040 411,050

The company will earn high profits of £411050 at total sales of 49500 units. However, it will be

only £313040 after selling 39600 units.

2. Calculation of most profitable plan

Selling price per unit and total number of units under both the proposals has been calculated

below:

Particulars Plan “a” Plan “b”

Current selling price 15.5 15.5

Increase: 10% 1.55

Decrease: 7.5% 1.1625

Net selling price 17.05 14.3375

Current sales unit 49500 49500

Less: Demand reduction 7425

Add: Increase demand 5940

Net sales unit 42075 55440

Table 5: Calculation of profits under both the proposals

Particulars Amount (a) Amount (b)

Sales units 42075 55440

Sales 717378.75 794871

Less: Cost of sales 235620 310464

Gross profit 481758.75 484407

Less; Annual fixed overheads 79000 79000

Net profit 402758.75 405407

Company should adopt plan b, because it will provide high profits amounted to £405407

while it is only £402758.75 in plan a. Hence, it became clear that firm should reduce selling price

by 7.5% that will lead to increase demand by 12%.

3. Profit computation on dealing with ASDA

Present scenario stated that ASDA desires to purchase 3300 gnomes at £8.90 hence,

profit has been determined below:

11

The company will earn high profits of £411050 at total sales of 49500 units. However, it will be

only £313040 after selling 39600 units.

2. Calculation of most profitable plan

Selling price per unit and total number of units under both the proposals has been calculated

below:

Particulars Plan “a” Plan “b”

Current selling price 15.5 15.5

Increase: 10% 1.55

Decrease: 7.5% 1.1625

Net selling price 17.05 14.3375

Current sales unit 49500 49500

Less: Demand reduction 7425

Add: Increase demand 5940

Net sales unit 42075 55440

Table 5: Calculation of profits under both the proposals

Particulars Amount (a) Amount (b)

Sales units 42075 55440

Sales 717378.75 794871

Less: Cost of sales 235620 310464

Gross profit 481758.75 484407

Less; Annual fixed overheads 79000 79000

Net profit 402758.75 405407

Company should adopt plan b, because it will provide high profits amounted to £405407

while it is only £402758.75 in plan a. Hence, it became clear that firm should reduce selling price

by 7.5% that will lead to increase demand by 12%.

3. Profit computation on dealing with ASDA

Present scenario stated that ASDA desires to purchase 3300 gnomes at £8.90 hence,

profit has been determined below:

11

Table 6: Computation of profit with dealing with ASDA

Particulars Amount Previous sales Total profit

Sales units 3300 49500 52800

Selling price 8.9 15.5

Sales 29370 767250 796620

Less: Cost of sales 18480 277200 295680

Gross profit 10890 490050 500940

Less; Annual fixed

overheads 79000 79000

Net profit 10890 411050 421940

Hence, it can be seen that if the company sells products to ASDA than it will provide advantage

of high profits by £10890. However, its disadvantage is, the selling price that is £8.90 is

significantly lower than the current market selling price of £15.50. Hence, it will affect profits in

an adverse manner.

TASK 7

Comparison of appropriate formats of financial statements for different types of firms

There is presence of various formats of financial statements that are being prepared by various

businesses. This includes the following:

Sole-traders: It is referred to as the types of business that prepares simple statements of profit

and loss. It is the kind of organisation that is owned and managed by single individuals (Murphy,

and Yetmar, 2010). Therefore, they are not required to reveal their accounts to others and enjoy

full profit margins and incur entire loss from the business transactions.

Partnership: In contrast to this partnership is a business that is carried out by two or more

individuals. This type of firm develops cash flow statements, balance sheets, as well as income

statement (Orlitzky, Schmidt and Rynes, 2003). In addition to this it also prepares partners with

12

Particulars Amount Previous sales Total profit

Sales units 3300 49500 52800

Selling price 8.9 15.5

Sales 29370 767250 796620

Less: Cost of sales 18480 277200 295680

Gross profit 10890 490050 500940

Less; Annual fixed

overheads 79000 79000

Net profit 10890 411050 421940

Hence, it can be seen that if the company sells products to ASDA than it will provide advantage

of high profits by £10890. However, its disadvantage is, the selling price that is £8.90 is

significantly lower than the current market selling price of £15.50. Hence, it will affect profits in

an adverse manner.

TASK 7

Comparison of appropriate formats of financial statements for different types of firms

There is presence of various formats of financial statements that are being prepared by various

businesses. This includes the following:

Sole-traders: It is referred to as the types of business that prepares simple statements of profit

and loss. It is the kind of organisation that is owned and managed by single individuals (Murphy,

and Yetmar, 2010). Therefore, they are not required to reveal their accounts to others and enjoy

full profit margins and incur entire loss from the business transactions.

Partnership: In contrast to this partnership is a business that is carried out by two or more

individuals. This type of firm develops cash flow statements, balance sheets, as well as income

statement (Orlitzky, Schmidt and Rynes, 2003). In addition to this it also prepares partners with

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

capital account that presents the contribution of capital done by each partner and the ratio in

which profits it will be distributed among them.

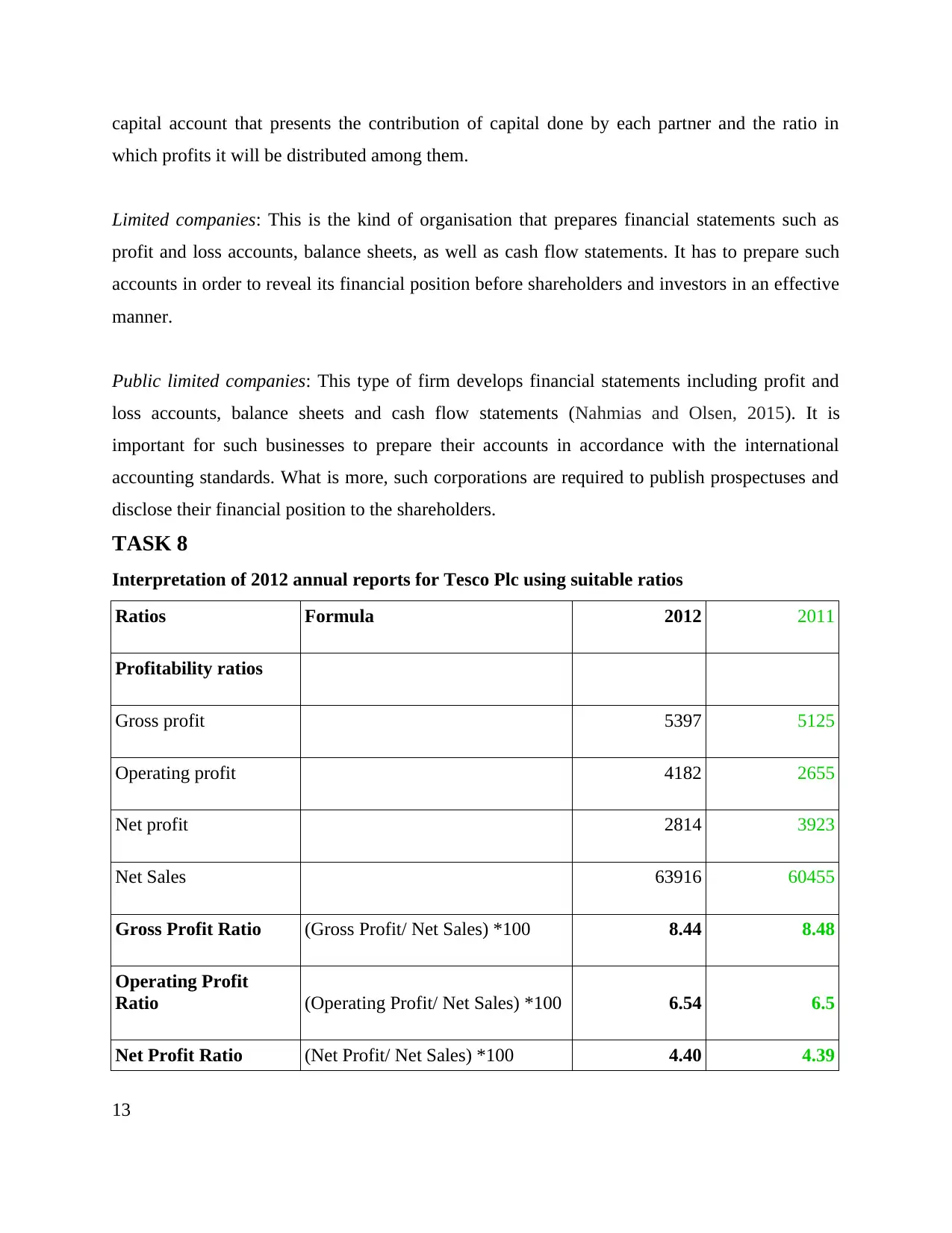

Limited companies: This is the kind of organisation that prepares financial statements such as

profit and loss accounts, balance sheets, as well as cash flow statements. It has to prepare such

accounts in order to reveal its financial position before shareholders and investors in an effective

manner.

Public limited companies: This type of firm develops financial statements including profit and

loss accounts, balance sheets and cash flow statements (Nahmias and Olsen, 2015). It is

important for such businesses to prepare their accounts in accordance with the international

accounting standards. What is more, such corporations are required to publish prospectuses and

disclose their financial position to the shareholders.

TASK 8

Interpretation of 2012 annual reports for Tesco Plc using suitable ratios

Ratios Formula 2012 2011

Profitability ratios

Gross profit 5397 5125

Operating profit 4182 2655

Net profit 2814 3923

Net Sales 63916 60455

Gross Profit Ratio (Gross Profit/ Net Sales) *100 8.44 8.48

Operating Profit

Ratio (Operating Profit/ Net Sales) *100 6.54 6.5

Net Profit Ratio (Net Profit/ Net Sales) *100 4.40 4.39

13

which profits it will be distributed among them.

Limited companies: This is the kind of organisation that prepares financial statements such as

profit and loss accounts, balance sheets, as well as cash flow statements. It has to prepare such

accounts in order to reveal its financial position before shareholders and investors in an effective

manner.

Public limited companies: This type of firm develops financial statements including profit and

loss accounts, balance sheets and cash flow statements (Nahmias and Olsen, 2015). It is

important for such businesses to prepare their accounts in accordance with the international

accounting standards. What is more, such corporations are required to publish prospectuses and

disclose their financial position to the shareholders.

TASK 8

Interpretation of 2012 annual reports for Tesco Plc using suitable ratios

Ratios Formula 2012 2011

Profitability ratios

Gross profit 5397 5125

Operating profit 4182 2655

Net profit 2814 3923

Net Sales 63916 60455

Gross Profit Ratio (Gross Profit/ Net Sales) *100 8.44 8.48

Operating Profit

Ratio (Operating Profit/ Net Sales) *100 6.54 6.5

Net Profit Ratio (Net Profit/ Net Sales) *100 4.40 4.39

13

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Liquidity ratios

Current Assets 12353 12039

Current Liabilities 19180 17731

Closing Stock 3598 3162

Current Ratio

Current Assets / current

Liabilities 0.64 0.68

Quick Ratio

(Cu. Assets - Cl. Stock)/Cu.

Liabilities 0.46 0.5

Efficiency Ratios

Net Sales 63916 60455

Total Assets 0 47206 50781

Total Assets Turnover

Ratio Net Sales/ Total Assets 1.35 1.19

Cost of goods sold 58519 55330

Inventory 3598 3162

Inventory Turnover

ratio COGS/Inventory 16.26 17.5

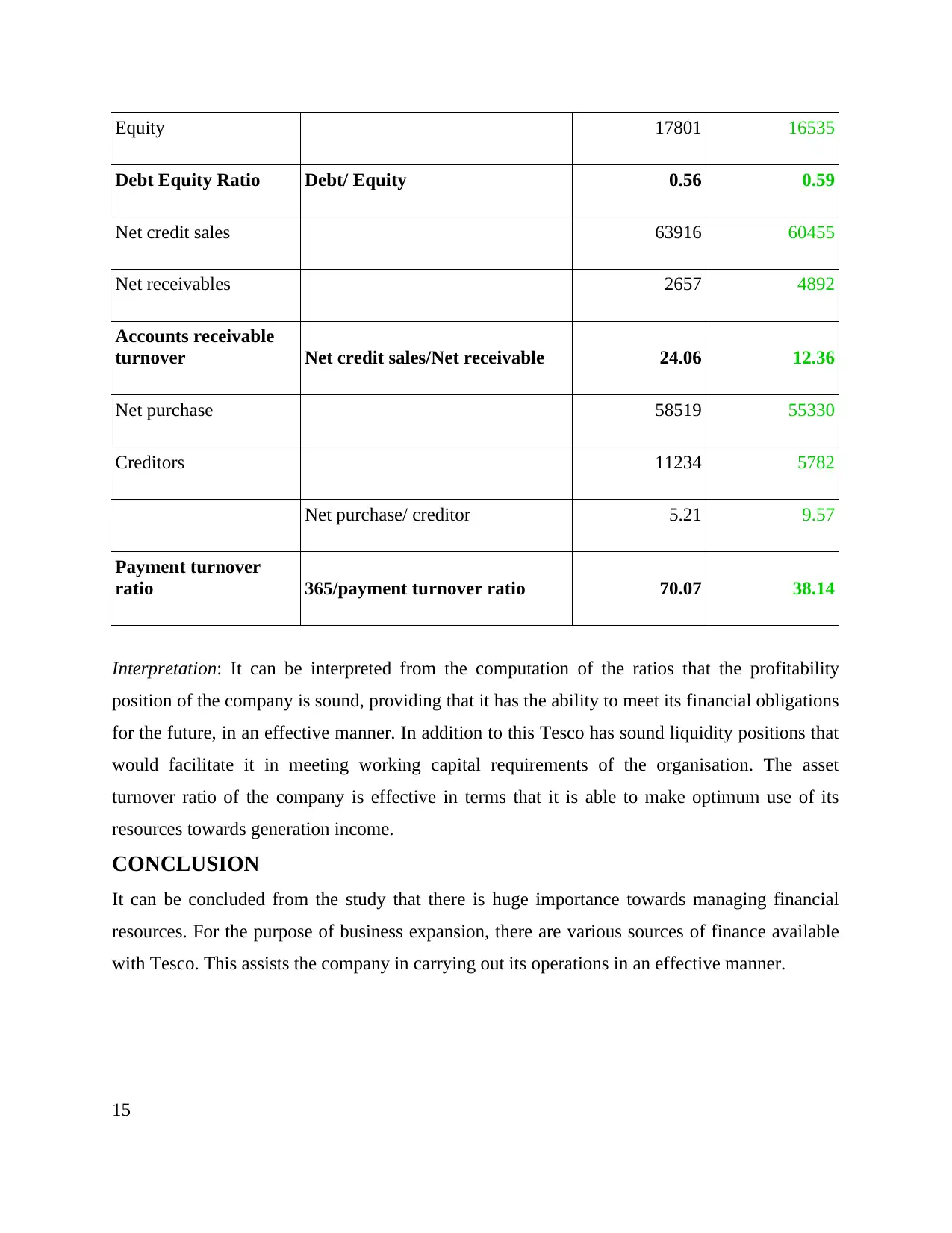

Gearing ratios

Debt 9911 9689

14

Current Assets 12353 12039

Current Liabilities 19180 17731

Closing Stock 3598 3162

Current Ratio

Current Assets / current

Liabilities 0.64 0.68

Quick Ratio

(Cu. Assets - Cl. Stock)/Cu.

Liabilities 0.46 0.5

Efficiency Ratios

Net Sales 63916 60455

Total Assets 0 47206 50781

Total Assets Turnover

Ratio Net Sales/ Total Assets 1.35 1.19

Cost of goods sold 58519 55330

Inventory 3598 3162

Inventory Turnover

ratio COGS/Inventory 16.26 17.5

Gearing ratios

Debt 9911 9689

14

Equity 17801 16535

Debt Equity Ratio Debt/ Equity 0.56 0.59

Net credit sales 63916 60455

Net receivables 2657 4892

Accounts receivable

turnover Net credit sales/Net receivable 24.06 12.36

Net purchase 58519 55330

Creditors 11234 5782

Net purchase/ creditor 5.21 9.57

Payment turnover

ratio 365/payment turnover ratio 70.07 38.14

Interpretation: It can be interpreted from the computation of the ratios that the profitability

position of the company is sound, providing that it has the ability to meet its financial obligations

for the future, in an effective manner. In addition to this Tesco has sound liquidity positions that

would facilitate it in meeting working capital requirements of the organisation. The asset

turnover ratio of the company is effective in terms that it is able to make optimum use of its

resources towards generation income.

CONCLUSION

It can be concluded from the study that there is huge importance towards managing financial

resources. For the purpose of business expansion, there are various sources of finance available

with Tesco. This assists the company in carrying out its operations in an effective manner.

15

Debt Equity Ratio Debt/ Equity 0.56 0.59

Net credit sales 63916 60455

Net receivables 2657 4892

Accounts receivable

turnover Net credit sales/Net receivable 24.06 12.36

Net purchase 58519 55330

Creditors 11234 5782

Net purchase/ creditor 5.21 9.57

Payment turnover

ratio 365/payment turnover ratio 70.07 38.14

Interpretation: It can be interpreted from the computation of the ratios that the profitability

position of the company is sound, providing that it has the ability to meet its financial obligations

for the future, in an effective manner. In addition to this Tesco has sound liquidity positions that

would facilitate it in meeting working capital requirements of the organisation. The asset

turnover ratio of the company is effective in terms that it is able to make optimum use of its

resources towards generation income.

CONCLUSION

It can be concluded from the study that there is huge importance towards managing financial

resources. For the purpose of business expansion, there are various sources of finance available

with Tesco. This assists the company in carrying out its operations in an effective manner.

15

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Journals and Books

Caglayan, M. and Demir, F., 2014. Firm Productivity, Exchange Rate Movements, Sources of

Finance, and Export Orientation. World Development. 54. pp. 204-219.

Fabregat-Sanjuan, A., Ferrando, F. and De la Flor, S., 2015. NiTiCu Transverse to Axial Strain

Ratio Analysis During Tension/Compression Tests. Materials Today: Proceedings. 2.pp.

S759-S762.

Gertler, M. and Kiyotaki, N., 2010. Financial intermediation and credit policy in business cycle

analysis. Handbook of monetary economics. 3(3). pp.547-599.

Hannam, P. M., Liao, Z., Davis, S. J. and Oppenheimer, M., 2015. Developing country finance

in a post-2020 global climate agreement. Nature Climate Change. 5(11). pp.983-987.

Jagman, H. and et.al., 2014. Financial literacy across the curriculum (and beyond) Opportunities

for academic libraries. College & Research Libraries News. 75(5).pp.254-257.

Larkin, P. J., 2011. To Iterate Or Not To Iterate? Using The WACC In Equity Valuation. Journal

of Business & Economics Research (JBER). 9(11). pp. 29-34.

Murphy, D., S. and Yetmar, S.,2010. Personal financial planning attitudes: a preliminary study of

graduate students. Management Research Review. 33(8). pp. 811–817.

Nahmias, S. and Olsen, T. L., 2015. Production and operations analysis. Waveland Press.

Orlitzky, M., Schmidt, F. L. and Rynes, S. L., 2003. Corporate social and financial performance:

A meta-analysis. Organization studies. 24(3). pp.403-441.

Overton, R. H., 2007. An Empirical Study of Financial Planning Theory and Practice. ProQues.

Shul'ga, S. V., 2014. Information disclosure in financial statements: evolution of national

systems and integration determinants. Journal International accounting. 38.pp. 332.

Online

Capital Investment Appraisal / Appraisal Techniques. 2015. Online. [Available through: <

http://www.capital-investment.co.uk/capital-investment-appraisal.php>. [Accessed on 9th

March 2016].

16

Journals and Books

Caglayan, M. and Demir, F., 2014. Firm Productivity, Exchange Rate Movements, Sources of

Finance, and Export Orientation. World Development. 54. pp. 204-219.

Fabregat-Sanjuan, A., Ferrando, F. and De la Flor, S., 2015. NiTiCu Transverse to Axial Strain

Ratio Analysis During Tension/Compression Tests. Materials Today: Proceedings. 2.pp.

S759-S762.

Gertler, M. and Kiyotaki, N., 2010. Financial intermediation and credit policy in business cycle

analysis. Handbook of monetary economics. 3(3). pp.547-599.

Hannam, P. M., Liao, Z., Davis, S. J. and Oppenheimer, M., 2015. Developing country finance

in a post-2020 global climate agreement. Nature Climate Change. 5(11). pp.983-987.

Jagman, H. and et.al., 2014. Financial literacy across the curriculum (and beyond) Opportunities

for academic libraries. College & Research Libraries News. 75(5).pp.254-257.

Larkin, P. J., 2011. To Iterate Or Not To Iterate? Using The WACC In Equity Valuation. Journal

of Business & Economics Research (JBER). 9(11). pp. 29-34.

Murphy, D., S. and Yetmar, S.,2010. Personal financial planning attitudes: a preliminary study of

graduate students. Management Research Review. 33(8). pp. 811–817.

Nahmias, S. and Olsen, T. L., 2015. Production and operations analysis. Waveland Press.

Orlitzky, M., Schmidt, F. L. and Rynes, S. L., 2003. Corporate social and financial performance:

A meta-analysis. Organization studies. 24(3). pp.403-441.

Overton, R. H., 2007. An Empirical Study of Financial Planning Theory and Practice. ProQues.

Shul'ga, S. V., 2014. Information disclosure in financial statements: evolution of national

systems and integration determinants. Journal International accounting. 38.pp. 332.

Online

Capital Investment Appraisal / Appraisal Techniques. 2015. Online. [Available through: <

http://www.capital-investment.co.uk/capital-investment-appraisal.php>. [Accessed on 9th

March 2016].

16

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.