Capital Structure and Lending: A Study on Banking Sector

VerifiedAdded on 2019/11/14

|33

|7693

|171

Report

AI Summary

The provided content discusses various aspects of risk management, capital structure, and lending at banks, with a focus on Indian banking institutions. The articles explore the relationships between financial ratios, bank performance, and risk-based capital ratios, as well as the impact of internet banking on bank performance. Other topics covered include efficiency measurement, corporate governance, and the determinants of bank profitability. The studies employ various analytical techniques, including data envelopment analysis, event history analysis, and multiple discriminant analysis.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: FINANCIAL COMPARISION BETWEEN BANKS

Financial Comparison between Standard Chartered Bank and United Overseas Bank

Name of the University:

Name of the Student:

Authors Note:

Financial Comparison between Standard Chartered Bank and United Overseas Bank

Name of the University:

Name of the Student:

Authors Note:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1FINANCIAL COMPARISION BETWEEN BANKS

Table of Contents

1. Introduction..................................................................................................................................3

1.1. Research Background...........................................................................................................3

1.2. Company Background..........................................................................................................3

1.3. Research Significance...........................................................................................................4

2. Literature Review........................................................................................................................5

2.1. Financial Analysis Concept..................................................................................................5

2.2. Financial Ratios Concept......................................................................................................5

2.3. Use of Financial Ratios in Banks..........................................................................................6

2.3.1. Credit Loss Ratio...........................................................................................................6

2.3.2. Cost/Income Ratio.........................................................................................................7

2.3.3. Net Interest Margin Ratio..............................................................................................8

2.3.4. Earnings per Share Ratio...............................................................................................8

2.3.5. Return on Equity............................................................................................................8

2.3.6. Capital Adequacy Ratio.................................................................................................9

3. Research Questions and Objectives...........................................................................................10

3.1. Research Questions:............................................................................................................10

3.2. Research Objectives............................................................................................................10

4. Research Methodology..............................................................................................................10

Table of Contents

1. Introduction..................................................................................................................................3

1.1. Research Background...........................................................................................................3

1.2. Company Background..........................................................................................................3

1.3. Research Significance...........................................................................................................4

2. Literature Review........................................................................................................................5

2.1. Financial Analysis Concept..................................................................................................5

2.2. Financial Ratios Concept......................................................................................................5

2.3. Use of Financial Ratios in Banks..........................................................................................6

2.3.1. Credit Loss Ratio...........................................................................................................6

2.3.2. Cost/Income Ratio.........................................................................................................7

2.3.3. Net Interest Margin Ratio..............................................................................................8

2.3.4. Earnings per Share Ratio...............................................................................................8

2.3.5. Return on Equity............................................................................................................8

2.3.6. Capital Adequacy Ratio.................................................................................................9

3. Research Questions and Objectives...........................................................................................10

3.1. Research Questions:............................................................................................................10

3.2. Research Objectives............................................................................................................10

4. Research Methodology..............................................................................................................10

2FINANCIAL COMPARISION BETWEEN BANKS

4.1. Research Design.................................................................................................................10

4.2. Data Collection...................................................................................................................11

4.3. Data Analysis......................................................................................................................12

4.4. Limitations..........................................................................................................................12

4.5. Reliability and Suitability...................................................................................................12

5. Findings and Analysis................................................................................................................14

5.1. Financial Statements of Standard Chartered Bank and United Overseas Bank.................14

5.1. Credit Loss Ratio Analysis.................................................................................................20

5.2. Cost/Income Ratio Analysis...............................................................................................21

5.3. Net Interest Margin Ratio Analysis....................................................................................22

5.4. Earnings per Share Ratio Analysis.....................................................................................24

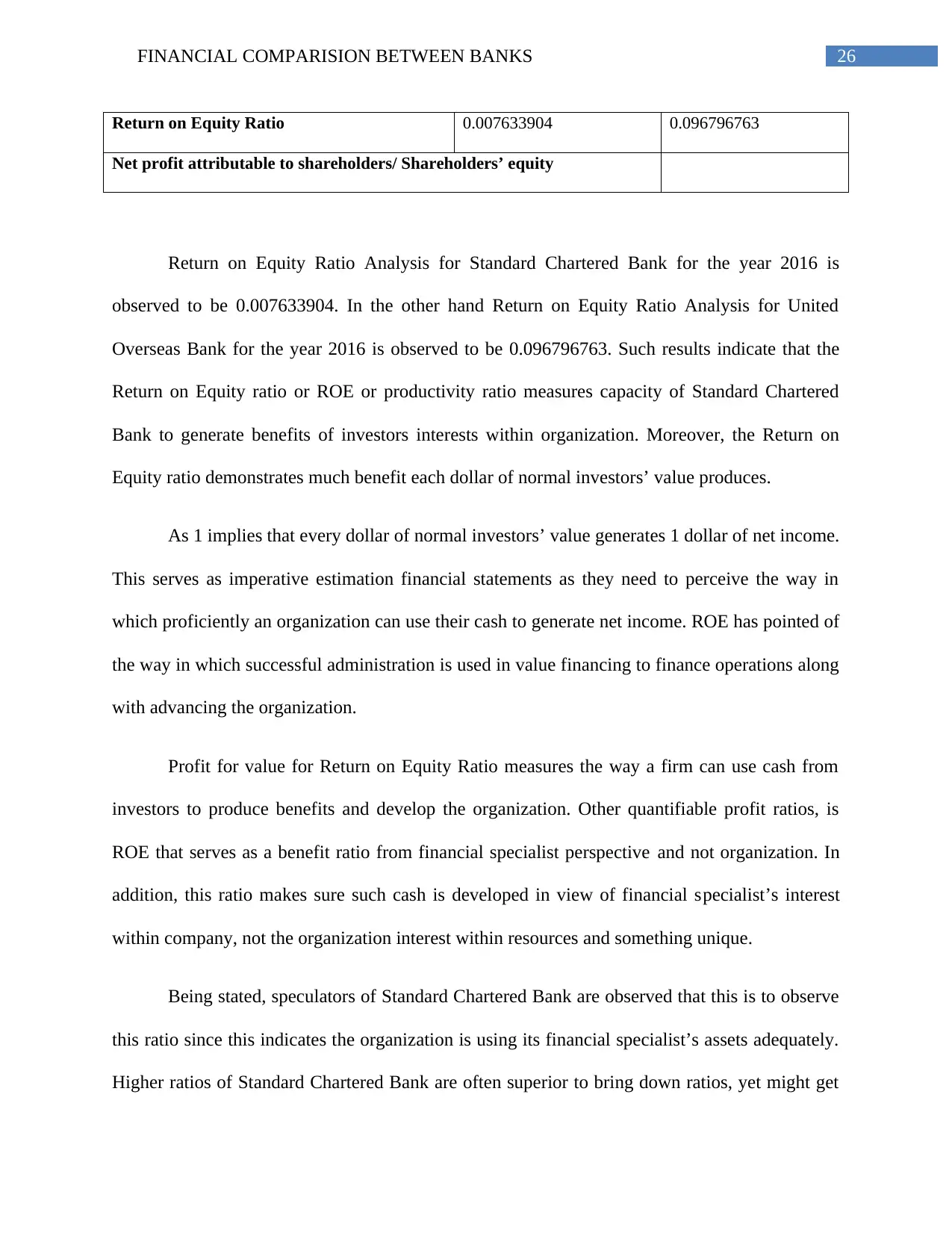

5.5. Return on Equity Ratio Analysis........................................................................................25

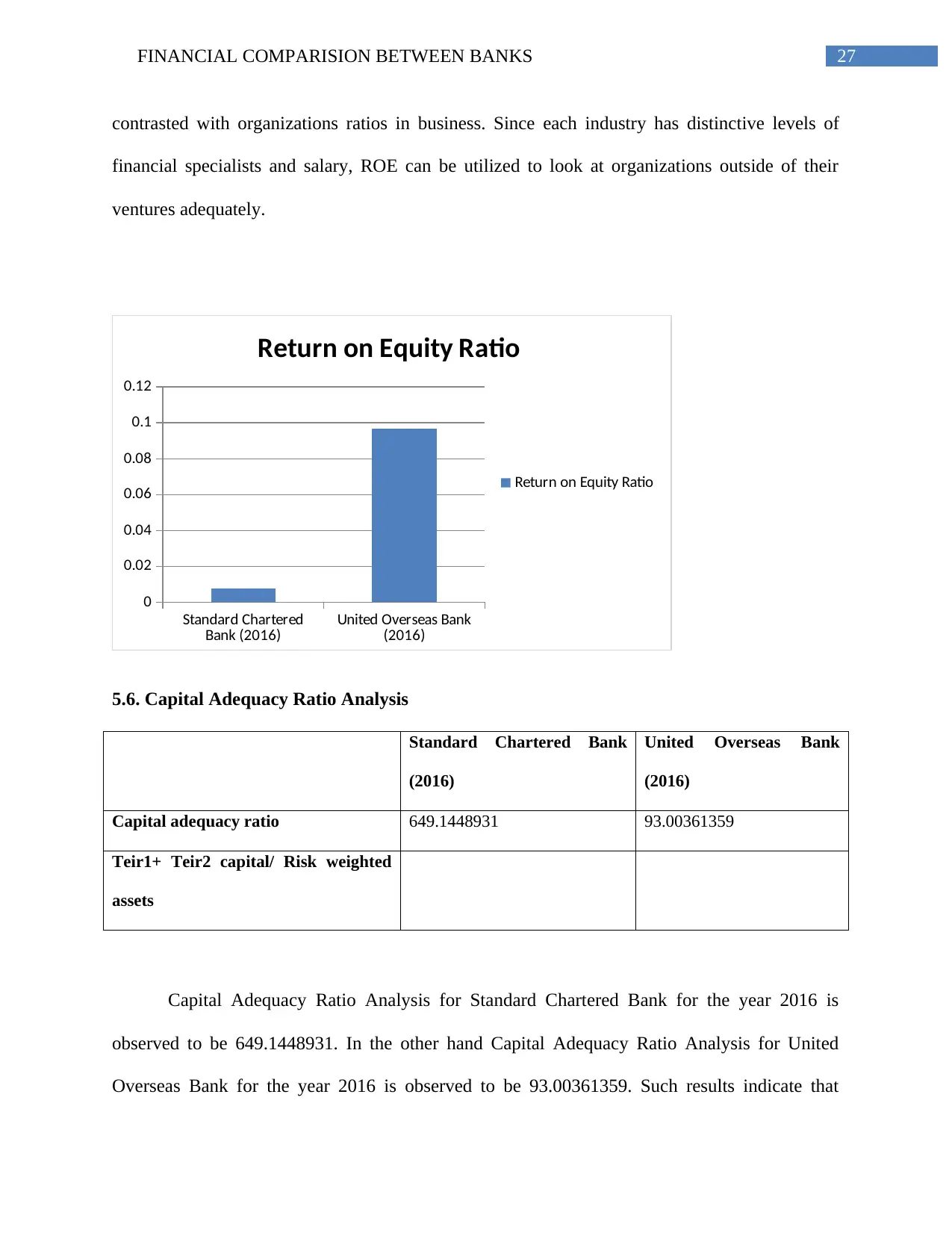

5.6. Capital Adequacy Ratio Analysis.......................................................................................27

6. Conclusion and Recommendations............................................................................................28

6.1. Conclusion..........................................................................................................................28

6.2. Recommendations to Banks...............................................................................................29

Reference List................................................................................................................................31

4.1. Research Design.................................................................................................................10

4.2. Data Collection...................................................................................................................11

4.3. Data Analysis......................................................................................................................12

4.4. Limitations..........................................................................................................................12

4.5. Reliability and Suitability...................................................................................................12

5. Findings and Analysis................................................................................................................14

5.1. Financial Statements of Standard Chartered Bank and United Overseas Bank.................14

5.1. Credit Loss Ratio Analysis.................................................................................................20

5.2. Cost/Income Ratio Analysis...............................................................................................21

5.3. Net Interest Margin Ratio Analysis....................................................................................22

5.4. Earnings per Share Ratio Analysis.....................................................................................24

5.5. Return on Equity Ratio Analysis........................................................................................25

5.6. Capital Adequacy Ratio Analysis.......................................................................................27

6. Conclusion and Recommendations............................................................................................28

6.1. Conclusion..........................................................................................................................28

6.2. Recommendations to Banks...............................................................................................29

Reference List................................................................................................................................31

3FINANCIAL COMPARISION BETWEEN BANKS

1. Introduction

1.1. Research Background

In economic improvement, banks serves as critical part for the economy as these are

fundamental financial interlinks that facilitate borrowing and lending exercises within indirect

market. In the event that banks might not fit well within industry, it might contribute to huge

failure within the economy (Altman 2013). Commercial banks (CBs) are different from other

partnership organizations as they have unique components within the assets and liabilities

section. Then again, same as few organizations, the business operation of CBs are measured by

the basic offer that they issue to their investors.

1.2. Company Background

Standard Chartered Bank Plc (alluded as "the bank") is among the renowned commercial

banks that has it’s headquarter in London, UK. The bank is set up after The Standard Bank

merger with The Chartered Bank in 1969. Standard Chartered Bank Plc obtained Standard

Chartered Merchant Bank Asia Limited in 1985, Korea First Bank in 2005, ANZ Grindlays Bank

in 2000 and American Express Bank Ltd in 2008. Starting at 30 June 2010, the aggregate

resource of Standard Chartered Bank Plc achieved USD 480.8 billion and is positioned ninth in

UK. The bank had acquired 18.4% of Temasek Holdings and 6.2% of Blackrock Inc (Altman

2013).

UOB is positioned among the renowned banks that has set up itself as a main and local

bank in Singapore and in Asia through business acquisitions. Today, the UOB Company has its

business operations worldwide in 19 nations within Asia Pacific, Western Europe and North

America - having a system of more than 500 workplaces. Singapore, Malaysia, Indonesia,

1. Introduction

1.1. Research Background

In economic improvement, banks serves as critical part for the economy as these are

fundamental financial interlinks that facilitate borrowing and lending exercises within indirect

market. In the event that banks might not fit well within industry, it might contribute to huge

failure within the economy (Altman 2013). Commercial banks (CBs) are different from other

partnership organizations as they have unique components within the assets and liabilities

section. Then again, same as few organizations, the business operation of CBs are measured by

the basic offer that they issue to their investors.

1.2. Company Background

Standard Chartered Bank Plc (alluded as "the bank") is among the renowned commercial

banks that has it’s headquarter in London, UK. The bank is set up after The Standard Bank

merger with The Chartered Bank in 1969. Standard Chartered Bank Plc obtained Standard

Chartered Merchant Bank Asia Limited in 1985, Korea First Bank in 2005, ANZ Grindlays Bank

in 2000 and American Express Bank Ltd in 2008. Starting at 30 June 2010, the aggregate

resource of Standard Chartered Bank Plc achieved USD 480.8 billion and is positioned ninth in

UK. The bank had acquired 18.4% of Temasek Holdings and 6.2% of Blackrock Inc (Altman

2013).

UOB is positioned among the renowned banks that has set up itself as a main and local

bank in Singapore and in Asia through business acquisitions. Today, the UOB Company has its

business operations worldwide in 19 nations within Asia Pacific, Western Europe and North

America - having a system of more than 500 workplaces. Singapore, Malaysia, Indonesia,

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4FINANCIAL COMPARISION BETWEEN BANKS

Thailand and China are managing an account backups of UOB. UOB offers a broad range of

financial services through its international business partners (Avkiran 2011). The company offers

consumers with access to financial services like private management of an account, individual

money management, business and corporate money saving.

1.3. Research Significance

The financial performance of the commercial banks is required to be assessed and

financial ratio analysis serves as an effective measure to evaluate the bank performance in the

current paper. In addition, there are many causes due to which such financial condition becomes

more intensified, for example, fluctuation on loan fees and external trade rates, liquidity hazard,

decreasing society dependence through financial framework, confinement within lending

exercises and decreased financial movement. In a situation of loss on operation or working

capital deficiency, the company can use the information from its annual report to make effective

business decisions (Barathi Kamath 2017). In such scenario, ratio analysis is considered to be an

effective analysis that can signify the financial position of the company. In addition the ratio

analysis demonstrates a connection between all the elements in income statement or balance

sheet or can help in analyzing the profitability or loss trend within the financial statements.

Along these lines, in this analysis, it will look out which financial ratios must be utilized in the

company to counteract bank failure. A research report regarding "Forecast of bank failure" taken

from Aggarwal, Paruthi and Kumar (2014) will be adjusted and those important financial ratios

are likewise at that point to be clarified in this analysis.

Thailand and China are managing an account backups of UOB. UOB offers a broad range of

financial services through its international business partners (Avkiran 2011). The company offers

consumers with access to financial services like private management of an account, individual

money management, business and corporate money saving.

1.3. Research Significance

The financial performance of the commercial banks is required to be assessed and

financial ratio analysis serves as an effective measure to evaluate the bank performance in the

current paper. In addition, there are many causes due to which such financial condition becomes

more intensified, for example, fluctuation on loan fees and external trade rates, liquidity hazard,

decreasing society dependence through financial framework, confinement within lending

exercises and decreased financial movement. In a situation of loss on operation or working

capital deficiency, the company can use the information from its annual report to make effective

business decisions (Barathi Kamath 2017). In such scenario, ratio analysis is considered to be an

effective analysis that can signify the financial position of the company. In addition the ratio

analysis demonstrates a connection between all the elements in income statement or balance

sheet or can help in analyzing the profitability or loss trend within the financial statements.

Along these lines, in this analysis, it will look out which financial ratios must be utilized in the

company to counteract bank failure. A research report regarding "Forecast of bank failure" taken

from Aggarwal, Paruthi and Kumar (2014) will be adjusted and those important financial ratios

are likewise at that point to be clarified in this analysis.

5FINANCIAL COMPARISION BETWEEN BANKS

2. Literature Review

2.1. Financial Analysis Concept

Financial analysis is observed to give supplementary information for various leaders. A

Several indicators including an analysis in light of characteristics and effects on economy

focused organizations will be sought out or discovered and utilized in investigation cash process.

A lot of indicators are given to settle on choice regarding picking the vital operating exercises

tool along with choosing sorts of venture that must be to be financed (Beaver, Correia and

McNichols 2012). Along these lines, an idea has been turned out in the procedure of financial

investigation that financial ratios, designs or certain strategies was decided for analyzing. In this

way, the indicators are then to research the implementation of the major aspect in deciding.

2.2. Financial Ratios Concept

Keeping in mind the end goal to assess the performance of depository organizations,

financial proclamations of commercial banks manages wide range of accessible financial data for

public. In contrast with financial explanation accounts, financial ratios are less demanding to

clarify an organization’s business operation as in financial reports. In addition, financial ratios

are dependably a significant measurement when they work out with an analysis or a reason for

reviewing changes in propensity; or the consequences will be severe, a ratio itself is an un-

significant number in light of the fact that the ratios utilized as a part does not totally explain the

business performance of the company (Berger et al. 2012). Organization analyses those ratios at

that point to compare them and develop standard ratios for itself or different organizations in a

similar industry. This helps in analyzing the organization's propensity by utilizing same ratio

over a long time that is picked arbitrarily relying upon organization needs.

2. Literature Review

2.1. Financial Analysis Concept

Financial analysis is observed to give supplementary information for various leaders. A

Several indicators including an analysis in light of characteristics and effects on economy

focused organizations will be sought out or discovered and utilized in investigation cash process.

A lot of indicators are given to settle on choice regarding picking the vital operating exercises

tool along with choosing sorts of venture that must be to be financed (Beaver, Correia and

McNichols 2012). Along these lines, an idea has been turned out in the procedure of financial

investigation that financial ratios, designs or certain strategies was decided for analyzing. In this

way, the indicators are then to research the implementation of the major aspect in deciding.

2.2. Financial Ratios Concept

Keeping in mind the end goal to assess the performance of depository organizations,

financial proclamations of commercial banks manages wide range of accessible financial data for

public. In contrast with financial explanation accounts, financial ratios are less demanding to

clarify an organization’s business operation as in financial reports. In addition, financial ratios

are dependably a significant measurement when they work out with an analysis or a reason for

reviewing changes in propensity; or the consequences will be severe, a ratio itself is an un-

significant number in light of the fact that the ratios utilized as a part does not totally explain the

business performance of the company (Berger et al. 2012). Organization analyses those ratios at

that point to compare them and develop standard ratios for itself or different organizations in a

similar industry. This helps in analyzing the organization's propensity by utilizing same ratio

over a long time that is picked arbitrarily relying upon organization needs.

6FINANCIAL COMPARISION BETWEEN BANKS

Applying pertinent financial ratios, is an approach to screen an organization's position by

drawing out the outcome on how the organization effectively created stores and benefits. As

indicated by the ratios with a year based investigation (financial proclamation is examined in a

particular time), it perfectly secured the count by alluding the measurement taken from an

association's financial explanation, with the goal that those ratios can demonstrate an

organization financial status. The correlation which utilizes organization's comparable ratios in a

portion of year is deemed as cross-sectional analysis (Bhattacharyya, Lovell and Sahay 2013).

Cross-sectional analysis utilizes organization's comparative ratios in a portion of years to do a

correlation. Despite utilizing several financial analysis techniques, ratio analysis is attempting to

give a portrayal of organization's strengths and shortcomings for assessing the vital part on of

financial situation of the company. In this way, those data offers a few chances for financial

specialists, experts and supervisors to conduct a ratio analysis before settling on a choice.

2.3. Use of Financial Ratios in Banks

Banks are financial organization, despite the fact that they are also financial

establishments, which offers detailed financial data different from other financial establishments.

Inclination of economy acts as vital part that affects banks' benefits, as banks' income majorly

originate from the cash they have in net premium salary. This is an aspect based on which the

loan costs rely upon the financial condition, so the interest free margin can be kept up as high as

it could. "Expectation of bank collapse", the example has drawn a perfect decision based on six

financial ratios clarified in this analysis.

2.3.1. Credit Loss Ratio

Credit loss ratio signifies changes on liquidity are a critical change to be expected. In

addition, defaulting credits are vital to be considered than liquidity changes. Credit loss ratio can

Applying pertinent financial ratios, is an approach to screen an organization's position by

drawing out the outcome on how the organization effectively created stores and benefits. As

indicated by the ratios with a year based investigation (financial proclamation is examined in a

particular time), it perfectly secured the count by alluding the measurement taken from an

association's financial explanation, with the goal that those ratios can demonstrate an

organization financial status. The correlation which utilizes organization's comparable ratios in a

portion of year is deemed as cross-sectional analysis (Bhattacharyya, Lovell and Sahay 2013).

Cross-sectional analysis utilizes organization's comparative ratios in a portion of years to do a

correlation. Despite utilizing several financial analysis techniques, ratio analysis is attempting to

give a portrayal of organization's strengths and shortcomings for assessing the vital part on of

financial situation of the company. In this way, those data offers a few chances for financial

specialists, experts and supervisors to conduct a ratio analysis before settling on a choice.

2.3. Use of Financial Ratios in Banks

Banks are financial organization, despite the fact that they are also financial

establishments, which offers detailed financial data different from other financial establishments.

Inclination of economy acts as vital part that affects banks' benefits, as banks' income majorly

originate from the cash they have in net premium salary. This is an aspect based on which the

loan costs rely upon the financial condition, so the interest free margin can be kept up as high as

it could. "Expectation of bank collapse", the example has drawn a perfect decision based on six

financial ratios clarified in this analysis.

2.3.1. Credit Loss Ratio

Credit loss ratio signifies changes on liquidity are a critical change to be expected. In

addition, defaulting credits are vital to be considered than liquidity changes. Credit loss ratio can

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7FINANCIAL COMPARISION BETWEEN BANKS

be understood as ratio which signifies net measure of credit faults remains connected in

aggregate sum of bank offering with borrowers. It is an attainment rate that remains decreased

than one within ratio.

Credit loss ratio= Net credit loss/Total lending

At the point the banks considered lending exercises; it is conceivable to realize

importance of credit loss. By taking a look at credits, bank will expect that most of them will end

up being a default installment. In estimation of banks' benefit before charge, banks might follow

conceivable costs. Consequently, banks were ensured that when borrowers neglect to pay; they

remain within controller capital necessity along with financial commitments. Negative situation

has appeared to bank's business at the time credit loss was increased (Chaudhary and Sharma

2011). Conversely, an analysis in credit loss will be done with different banks through explaining

credit loss over aggregate lending. By focusing on default credits, it can be said that more

prominent the bank can deal with aggregate lending, the more littler the rate will be observed

within this ratio.

2.3.2. Cost/Income Ratio

The second ratio within exploration shows critical connection among operating income

along with operating costs. This ratio measures the effective way in which bank has a capacity to

manage working costs by producing operating income. In this way, this ratio will be looked for

maintaining a high ratio under such circumstances (Malhotra and Singh 2016).

Income/Cost ratio= Income/Cost

Cost-to-income ratio is all the regularly utilized by bank to show operational

effectiveness after financial emergency that happened. In this ratio, bank's capacity is not to

be understood as ratio which signifies net measure of credit faults remains connected in

aggregate sum of bank offering with borrowers. It is an attainment rate that remains decreased

than one within ratio.

Credit loss ratio= Net credit loss/Total lending

At the point the banks considered lending exercises; it is conceivable to realize

importance of credit loss. By taking a look at credits, bank will expect that most of them will end

up being a default installment. In estimation of banks' benefit before charge, banks might follow

conceivable costs. Consequently, banks were ensured that when borrowers neglect to pay; they

remain within controller capital necessity along with financial commitments. Negative situation

has appeared to bank's business at the time credit loss was increased (Chaudhary and Sharma

2011). Conversely, an analysis in credit loss will be done with different banks through explaining

credit loss over aggregate lending. By focusing on default credits, it can be said that more

prominent the bank can deal with aggregate lending, the more littler the rate will be observed

within this ratio.

2.3.2. Cost/Income Ratio

The second ratio within exploration shows critical connection among operating income

along with operating costs. This ratio measures the effective way in which bank has a capacity to

manage working costs by producing operating income. In this way, this ratio will be looked for

maintaining a high ratio under such circumstances (Malhotra and Singh 2016).

Income/Cost ratio= Income/Cost

Cost-to-income ratio is all the regularly utilized by bank to show operational

effectiveness after financial emergency that happened. In this ratio, bank's capacity is not to

8FINANCIAL COMPARISION BETWEEN BANKS

focus on dealing with working costs which it probably ought to be limited. Thus, bring down

value is more favored.

Cost/Income – ratio= Cost/Income

In this ratio, adding up to working expense is best for computing those charges on poor

obligation along with suspicious obligation. Moreover, working salary is including the aggregate

sum of net intrigue and salary with no intrigue.

2.3.3. Net Interest Margin Ratio

This ratio can be explained as the way in which banks create net interest pay from credit

resources (additionally called as interest acquiring resources). It is likewise maintaining a

proximity ratio along with non-financial organizations' gross profit edge (Hill, Perry and Andes

2011).

Net interest margin = Net Interest Income/Average Total Assets

2.3.4. Earnings per Share Ratio

Earnings per share are a ratio that gauges net benefit gained by banks or participating

organizations in connection to amount of customary offers issued. In financial investigation, this

ratio is typically used to give compensation to basic investors on their venture. In any case, EPS

is largely affected by the amount of regular offers issued (Chu and Lim 2014).

Earnings per share = Net income/Number of ordinary shares issued

2.3.5. Return on Equity

This ratio is among the most important ratios that remain within the strategy of producing

more cash. In such scenario, Return on Equity (ROE) is important among them. With respect to

focus on dealing with working costs which it probably ought to be limited. Thus, bring down

value is more favored.

Cost/Income – ratio= Cost/Income

In this ratio, adding up to working expense is best for computing those charges on poor

obligation along with suspicious obligation. Moreover, working salary is including the aggregate

sum of net intrigue and salary with no intrigue.

2.3.3. Net Interest Margin Ratio

This ratio can be explained as the way in which banks create net interest pay from credit

resources (additionally called as interest acquiring resources). It is likewise maintaining a

proximity ratio along with non-financial organizations' gross profit edge (Hill, Perry and Andes

2011).

Net interest margin = Net Interest Income/Average Total Assets

2.3.4. Earnings per Share Ratio

Earnings per share are a ratio that gauges net benefit gained by banks or participating

organizations in connection to amount of customary offers issued. In financial investigation, this

ratio is typically used to give compensation to basic investors on their venture. In any case, EPS

is largely affected by the amount of regular offers issued (Chu and Lim 2014).

Earnings per share = Net income/Number of ordinary shares issued

2.3.5. Return on Equity

This ratio is among the most important ratios that remain within the strategy of producing

more cash. In such scenario, Return on Equity (ROE) is important among them. With respect to

9FINANCIAL COMPARISION BETWEEN BANKS

measuring benefit, ROE is the financial ratio that explains utilizing investor contributed cash to

bank's reserve.

Return for Equity = Net income owing to investors/Shareholders' value

As a financial specialist, bank investors are probably going to see this ratio to be as high

as expected under certain circumstances (Chiaramonte and Casu 2017). In any case, a higher

ROE additionally bring up an increase in risks. On the other hand, a development risk of

dissolvability issue is because of the reason that bank has a trouble to maintain the least standard

of controller capital along these lines that causes a major fall in investors' finance.

2.3.6. Capital Adequacy Ratio

In capital adequacy ratio, a controller ratio was made to ensure banks or other financial

organizations have adequate cash-flow to remove them from trouble and furthermore ready to

deal with a huge number of loss.

Capital adequacy ratio = Teir1+ Teir2 capital/Risk weighted assets

Number of volume that bank is ready to find is controlled by the bank's capacity to

payback its investors on time and extra risk taken (Chiaramonte and Casu 2017). This ratio

focuses on analyzing a measure of capital used to deal with the risks in saving money. Since

bank has different sorts of benefits, a few assets are discarded in the record, for example, credits

and credit risk of advances. In view of Basel II, CAR is not permitted to maintain a standard

level of 8%.

measuring benefit, ROE is the financial ratio that explains utilizing investor contributed cash to

bank's reserve.

Return for Equity = Net income owing to investors/Shareholders' value

As a financial specialist, bank investors are probably going to see this ratio to be as high

as expected under certain circumstances (Chiaramonte and Casu 2017). In any case, a higher

ROE additionally bring up an increase in risks. On the other hand, a development risk of

dissolvability issue is because of the reason that bank has a trouble to maintain the least standard

of controller capital along these lines that causes a major fall in investors' finance.

2.3.6. Capital Adequacy Ratio

In capital adequacy ratio, a controller ratio was made to ensure banks or other financial

organizations have adequate cash-flow to remove them from trouble and furthermore ready to

deal with a huge number of loss.

Capital adequacy ratio = Teir1+ Teir2 capital/Risk weighted assets

Number of volume that bank is ready to find is controlled by the bank's capacity to

payback its investors on time and extra risk taken (Chiaramonte and Casu 2017). This ratio

focuses on analyzing a measure of capital used to deal with the risks in saving money. Since

bank has different sorts of benefits, a few assets are discarded in the record, for example, credits

and credit risk of advances. In view of Basel II, CAR is not permitted to maintain a standard

level of 8%.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10FINANCIAL COMPARISION BETWEEN BANKS

3. Research Questions and Objectives

3.1. Research Questions:

The research questions those are to be answered in carrying out Financial Comparison

between Standard Chartered Bank and United Overseas Bank are explained under:

Why financial ratio evaluation is selected for investigating performance of selected

companies?

What are financial ratios that will be used in order to prevent banking collapse?

What is the importance of analyzing six selected financial ratios?

3.2. Research Objectives

The research objectives those are to be addressed in carrying out Financial Comparison

between Standard Chartered Bank and United Overseas Bank are explained under:

To evaluate whether the financial ratio evaluation should be selected for investigating

performance of selected companies

To evaluate whether the financial ratios will be used in order to prevent banking collapse

To evaluate the importance of analyzing six selected financial ratios of the selected banks

4. Research Methodology

4.1. Research Design

Exploratory research is carried out in the analysis for the reason that financial ratios were

being found from case of forecasting bank emergency. Thus, it offers increased sense to this

point. In this manner, between major research approaches that includes quantitative research and

subjective research, subjective research is highly appropriate to employ for such research (Hill,

3. Research Questions and Objectives

3.1. Research Questions:

The research questions those are to be answered in carrying out Financial Comparison

between Standard Chartered Bank and United Overseas Bank are explained under:

Why financial ratio evaluation is selected for investigating performance of selected

companies?

What are financial ratios that will be used in order to prevent banking collapse?

What is the importance of analyzing six selected financial ratios?

3.2. Research Objectives

The research objectives those are to be addressed in carrying out Financial Comparison

between Standard Chartered Bank and United Overseas Bank are explained under:

To evaluate whether the financial ratio evaluation should be selected for investigating

performance of selected companies

To evaluate whether the financial ratios will be used in order to prevent banking collapse

To evaluate the importance of analyzing six selected financial ratios of the selected banks

4. Research Methodology

4.1. Research Design

Exploratory research is carried out in the analysis for the reason that financial ratios were

being found from case of forecasting bank emergency. Thus, it offers increased sense to this

point. In this manner, between major research approaches that includes quantitative research and

subjective research, subjective research is highly appropriate to employ for such research (Hill,

11FINANCIAL COMPARISION BETWEEN BANKS

Perry and Andes 2011). The cause of selecting subjective research as an exploration approach is

because such research is depended on an improvement of hypothesis.

In the research, procedure that is utilized is managing the contextual investigations is

focused on contemplating financial ratios that is utilized inside bank to avert insolvency. A

reference is coded from previous research explains that, it is appropriate as a solitary outline of

contextual analysis and in case when the hypothesis presents a detailed rule in basic case.

Furthermore, contextual investigation is required in the exploration as best approach to

distinguish significant financial ratios.

4.2. Data Collection

There exist two approaches for information accumulation for an analysis:

1) Essential information; and

2) Optional information. Information which is gathered in view of addressing particular

objective to settle the research question is considered as essential information.

Optional information is likewise called as secondary information which explains that a

collection of assets is taken from the analysis that is already available in previous researches and

is there for utilization. In this research, it has turned out to be a source of attaining optional

information, for example, diary, article, online reading material, solid site and few more.

Furthermore, this analysis was not carrying out any essential information accumulation as it is

not required to do as such (Hill, Perry and Andes 2011). The secondary information appears to

be gathered for other reason other than analyzing in this investigation therefore this

supplementary information has been checked properly. The collection process selected was

principally to understand major part of the issue by analyzing that information.

Perry and Andes 2011). The cause of selecting subjective research as an exploration approach is

because such research is depended on an improvement of hypothesis.

In the research, procedure that is utilized is managing the contextual investigations is

focused on contemplating financial ratios that is utilized inside bank to avert insolvency. A

reference is coded from previous research explains that, it is appropriate as a solitary outline of

contextual analysis and in case when the hypothesis presents a detailed rule in basic case.

Furthermore, contextual investigation is required in the exploration as best approach to

distinguish significant financial ratios.

4.2. Data Collection

There exist two approaches for information accumulation for an analysis:

1) Essential information; and

2) Optional information. Information which is gathered in view of addressing particular

objective to settle the research question is considered as essential information.

Optional information is likewise called as secondary information which explains that a

collection of assets is taken from the analysis that is already available in previous researches and

is there for utilization. In this research, it has turned out to be a source of attaining optional

information, for example, diary, article, online reading material, solid site and few more.

Furthermore, this analysis was not carrying out any essential information accumulation as it is

not required to do as such (Hill, Perry and Andes 2011). The secondary information appears to

be gathered for other reason other than analyzing in this investigation therefore this

supplementary information has been checked properly. The collection process selected was

principally to understand major part of the issue by analyzing that information.

12FINANCIAL COMPARISION BETWEEN BANKS

4.3. Data Analysis

Information analysis serves as a strategy breakdown from graphic analysis, was utilized

as a part of carrying out investigation for the research. The example of Meyer and Pifer

demonstrated six financial ratios remain essential as best approach to deal with insolvency.

Considering the same, research was conducted by utilizing associated accessible information.

Significance of these ratios must be analyzed before utilizing such aspects to conduct analysis on

two selected banks.

4.4. Limitations

By utilizing secondary information in this exploration, a couple of limitations are

experienced that reduced information usefulness. Due to such limitations, researcher ought to be

inefficient while utilizing the secondary information. In view of those issues, the researcher may

require significant investment in examining the ratios as it perhaps serves as an appropriate

analysis (Goyal and Joshi 2011). Thus, it offers increased sense to this point. In this manner,

between major research approaches that includes quantitative research and subjective research,

subjective research is highly appropriate to employ for such research. Consequently, in this

analysis, use of secondary information is important to get an alternate complaint with initial

information originator.

4.5. Reliability and Suitability

As per Goyal and Joshi (2011), certain optional information was utilized focused on the

researcher that ought to guarantee that they could satisfy the accompanying qualities:

• Reliability

4.3. Data Analysis

Information analysis serves as a strategy breakdown from graphic analysis, was utilized

as a part of carrying out investigation for the research. The example of Meyer and Pifer

demonstrated six financial ratios remain essential as best approach to deal with insolvency.

Considering the same, research was conducted by utilizing associated accessible information.

Significance of these ratios must be analyzed before utilizing such aspects to conduct analysis on

two selected banks.

4.4. Limitations

By utilizing secondary information in this exploration, a couple of limitations are

experienced that reduced information usefulness. Due to such limitations, researcher ought to be

inefficient while utilizing the secondary information. In view of those issues, the researcher may

require significant investment in examining the ratios as it perhaps serves as an appropriate

analysis (Goyal and Joshi 2011). Thus, it offers increased sense to this point. In this manner,

between major research approaches that includes quantitative research and subjective research,

subjective research is highly appropriate to employ for such research. Consequently, in this

analysis, use of secondary information is important to get an alternate complaint with initial

information originator.

4.5. Reliability and Suitability

As per Goyal and Joshi (2011), certain optional information was utilized focused on the

researcher that ought to guarantee that they could satisfy the accompanying qualities:

• Reliability

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

13FINANCIAL COMPARISION BETWEEN BANKS

Since secondary information is accessible and simple to attain, it ought to be focused on

feeling of unwavering quality. In such aspect, it might be tried through discovering appropriate

response from pertinent inquiries. Those inquiries are:

(a) Who is individual that gathered information?

(b) What sort of sources are available for information turned out with?

(c) Were all information gathered through a moral ways?

(d) When were such information gathered?

(e) Was there certain contentions showed up with first specialist?

(f) Which type exact information was desired? Is it accurate to say that it was accomplished or

not?

• Suitability

As secondary information must be gathered from accessible data, as, those information

accumulations were done to suit the research analysis. Hence, rationality of information relies

upon the agent's exploration prerequisite, it might be reasonable for one however not another.

Along these lines, the clearness of layout and company units are utilized at the occasion of

gathering essential information sources must be investigated precisely by researcher. The

comparable approach to do as such on considered the reason, range and nature of first analysis.

In conclusion, the researcher ought not to utilize that information if any distinctions were found

in, in light of the fact that they demonstrated inadmissible with as of now analysis.

• Sufficiency

Since secondary information is accessible and simple to attain, it ought to be focused on

feeling of unwavering quality. In such aspect, it might be tried through discovering appropriate

response from pertinent inquiries. Those inquiries are:

(a) Who is individual that gathered information?

(b) What sort of sources are available for information turned out with?

(c) Were all information gathered through a moral ways?

(d) When were such information gathered?

(e) Was there certain contentions showed up with first specialist?

(f) Which type exact information was desired? Is it accurate to say that it was accomplished or

not?

• Suitability

As secondary information must be gathered from accessible data, as, those information

accumulations were done to suit the research analysis. Hence, rationality of information relies

upon the agent's exploration prerequisite, it might be reasonable for one however not another.

Along these lines, the clearness of layout and company units are utilized at the occasion of

gathering essential information sources must be investigated precisely by researcher. The

comparable approach to do as such on considered the reason, range and nature of first analysis.

In conclusion, the researcher ought not to utilize that information if any distinctions were found

in, in light of the fact that they demonstrated inadmissible with as of now analysis.

• Sufficiency

14FINANCIAL COMPARISION BETWEEN BANKS

The researcher might not utilize the optional information that was discovered to be

inadequate despite the fact that the information achieved maintains the level of exactness; they

are as yet considered to be lacking. In the event that the range of information which is either

more extensive or smaller than the at present analysis zone, the information was moreover

considered as deficient. From every one of the attributes, it was being evidenced that a high risk

is involved in utilizing the prepared accessible information. The prepared accessible information

is a concern just when they are deemed to be adequate, appropriate and dependable for the

researcher. In other perspective, if the prepared accessible information was turned out from

reliable sources and likewise reasonable and adequate. Analysis of the same is deemed to be

simply aimless for using it as it is not worth to rely on utilizing study to gather data. Now and

again, helpfulness of optional information might be profited by the researcher who must utilize

the data under self-assurance.

5. Findings and Analysis

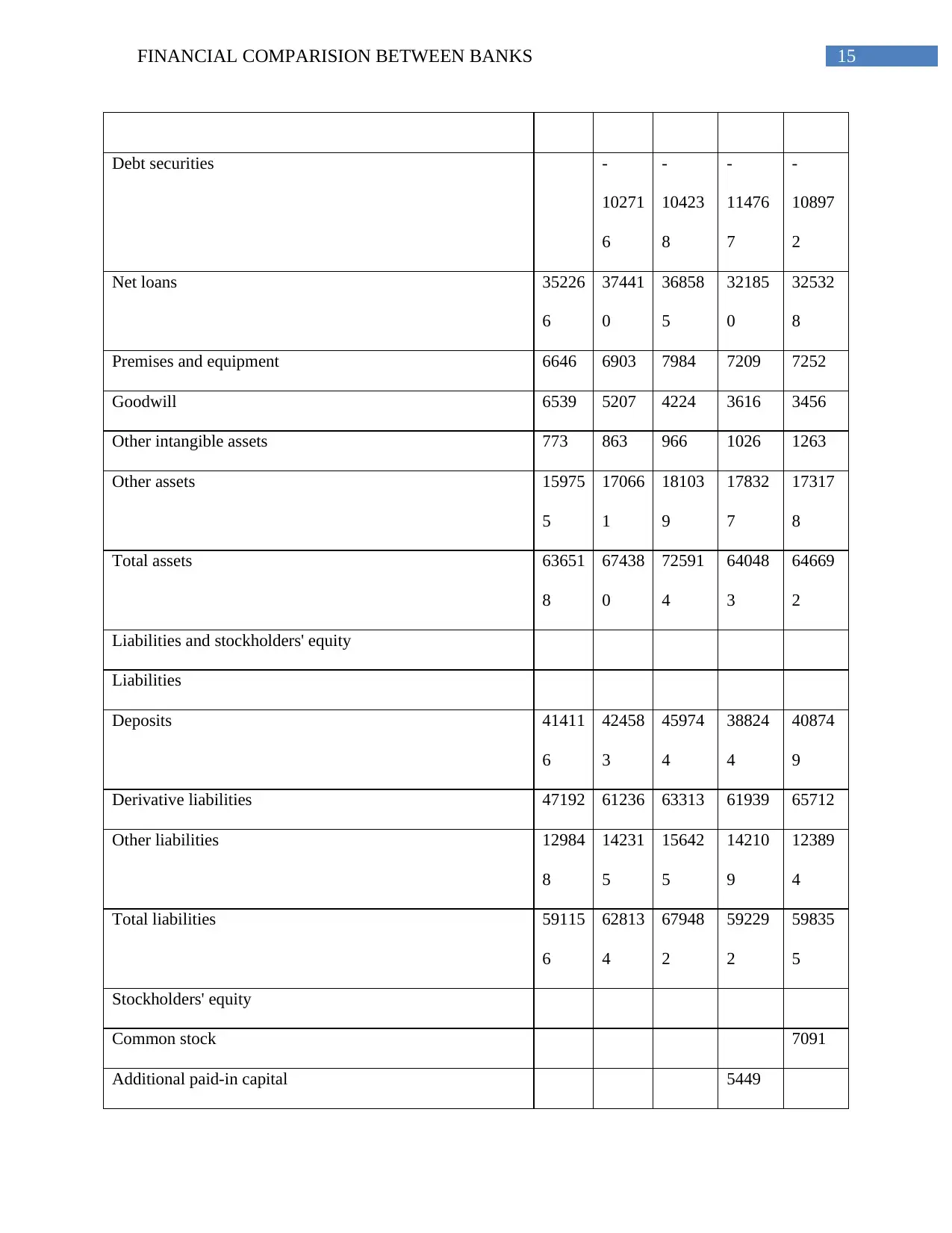

5.1. Financial Statements of Standard Chartered Bank and United Overseas Bank

STANDARD CHARTERED PLC (02888) CashFlowFlag

BALANCE SHEET

Fiscal year ends in December. USD in millions except per

share data.

2012-

12

2013-

12

2014-

12

2015-

12

2016-

12

Assets

Cash and due from banks 61043 54534 97282 65312 70706

Trading assets 10271

6

10423

8

11476

7

10897

2

Derivative assets 49496 61802 65834 63143 65509

The researcher might not utilize the optional information that was discovered to be

inadequate despite the fact that the information achieved maintains the level of exactness; they

are as yet considered to be lacking. In the event that the range of information which is either

more extensive or smaller than the at present analysis zone, the information was moreover

considered as deficient. From every one of the attributes, it was being evidenced that a high risk

is involved in utilizing the prepared accessible information. The prepared accessible information

is a concern just when they are deemed to be adequate, appropriate and dependable for the

researcher. In other perspective, if the prepared accessible information was turned out from

reliable sources and likewise reasonable and adequate. Analysis of the same is deemed to be

simply aimless for using it as it is not worth to rely on utilizing study to gather data. Now and

again, helpfulness of optional information might be profited by the researcher who must utilize

the data under self-assurance.

5. Findings and Analysis

5.1. Financial Statements of Standard Chartered Bank and United Overseas Bank

STANDARD CHARTERED PLC (02888) CashFlowFlag

BALANCE SHEET

Fiscal year ends in December. USD in millions except per

share data.

2012-

12

2013-

12

2014-

12

2015-

12

2016-

12

Assets

Cash and due from banks 61043 54534 97282 65312 70706

Trading assets 10271

6

10423

8

11476

7

10897

2

Derivative assets 49496 61802 65834 63143 65509

15FINANCIAL COMPARISION BETWEEN BANKS

Debt securities -

10271

6

-

10423

8

-

11476

7

-

10897

2

Net loans 35226

6

37441

0

36858

5

32185

0

32532

8

Premises and equipment 6646 6903 7984 7209 7252

Goodwill 6539 5207 4224 3616 3456

Other intangible assets 773 863 966 1026 1263

Other assets 15975

5

17066

1

18103

9

17832

7

17317

8

Total assets 63651

8

67438

0

72591

4

64048

3

64669

2

Liabilities and stockholders' equity

Liabilities

Deposits 41411

6

42458

3

45974

4

38824

4

40874

9

Derivative liabilities 47192 61236 63313 61939 65712

Other liabilities 12984

8

14231

5

15642

5

14210

9

12389

4

Total liabilities 59115

6

62813

4

67948

2

59229

2

59835

5

Stockholders' equity

Common stock 7091

Additional paid-in capital 5449

Debt securities -

10271

6

-

10423

8

-

11476

7

-

10897

2

Net loans 35226

6

37441

0

36858

5

32185

0

32532

8

Premises and equipment 6646 6903 7984 7209 7252

Goodwill 6539 5207 4224 3616 3456

Other intangible assets 773 863 966 1026 1263

Other assets 15975

5

17066

1

18103

9

17832

7

17317

8

Total assets 63651

8

67438

0

72591

4

64048

3

64669

2

Liabilities and stockholders' equity

Liabilities

Deposits 41411

6

42458

3

45974

4

38824

4

40874

9

Derivative liabilities 47192 61236 63313 61939 65712

Other liabilities 12984

8

14231

5

15642

5

14210

9

12389

4

Total liabilities 59115

6

62813

4

67948

2

59229

2

59835

5

Stockholders' equity

Common stock 7091

Additional paid-in capital 5449

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

16FINANCIAL COMPARISION BETWEEN BANKS

Retained earnings 26934 25753

Accumulated other comprehensive income 45362 46246 46432 15808 15493

Total stockholders' equity 45362 46246 46432 48191 48337

Total liabilities and stockholders' equity 63651

8

67438

0

72591

4

64048

3

64669

2

Assets

Cash and due from banks 42547 57069 63775 60952 58434

Trading assets 260 628 738 1277 3127

Derivative assets 5456 5779 6306 6422 6982

Debt securities -260 -628 -738 -1277 -3127

Net loans 15293

0

17885

7

19590

3

20361

1

22173

4

Receivables 575 740 1579 3905 813

Premises and equipment 1234 1308 1428 1739 1885

Goodwill 4168 4144

Other intangible assets 4149 4144 4151

Other assets 45990 36331 33596 35239 46030

Total assets 25290

0

28422

9

30673

6

31601

1

34002

8

Liabilities and stockholders' equity

Liabilities

Deposits 20356

7

22825

4

24497

6

25251

1

26716

9

Derivative liabilities 5506 5878 6384 5969 6837

Retained earnings 26934 25753

Accumulated other comprehensive income 45362 46246 46432 15808 15493

Total stockholders' equity 45362 46246 46432 48191 48337

Total liabilities and stockholders' equity 63651

8

67438

0

72591

4

64048

3

64669

2

Assets

Cash and due from banks 42547 57069 63775 60952 58434

Trading assets 260 628 738 1277 3127

Derivative assets 5456 5779 6306 6422 6982

Debt securities -260 -628 -738 -1277 -3127

Net loans 15293

0

17885

7

19590

3

20361

1

22173

4

Receivables 575 740 1579 3905 813

Premises and equipment 1234 1308 1428 1739 1885

Goodwill 4168 4144

Other intangible assets 4149 4144 4151

Other assets 45990 36331 33596 35239 46030

Total assets 25290

0

28422

9

30673

6

31601

1

34002

8

Liabilities and stockholders' equity

Liabilities

Deposits 20356

7

22825

4

24497

6

25251

1

26716

9

Derivative liabilities 5506 5878 6384 5969 6837

17FINANCIAL COMPARISION BETWEEN BANKS

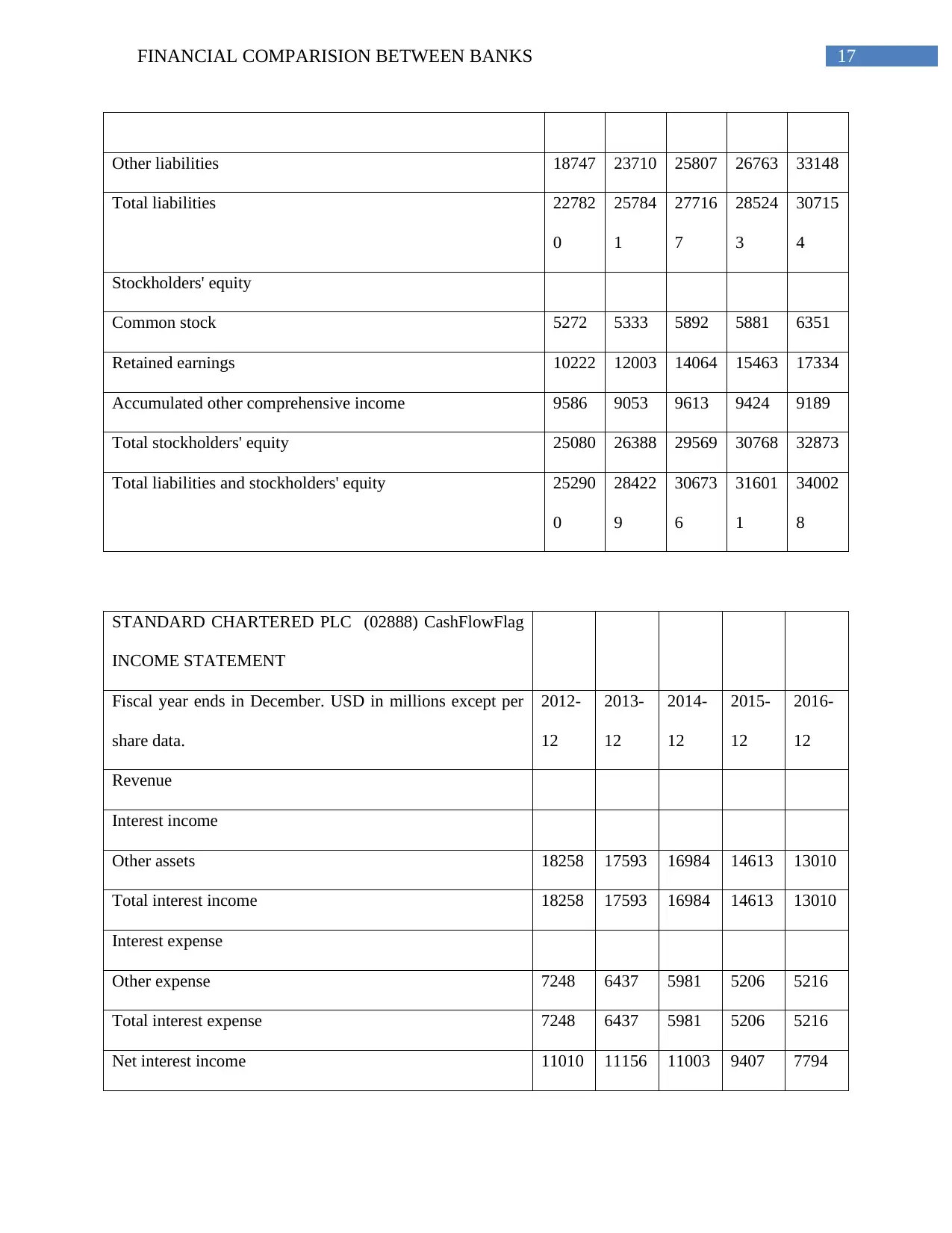

Other liabilities 18747 23710 25807 26763 33148

Total liabilities 22782

0

25784

1

27716

7

28524

3

30715

4

Stockholders' equity

Common stock 5272 5333 5892 5881 6351

Retained earnings 10222 12003 14064 15463 17334

Accumulated other comprehensive income 9586 9053 9613 9424 9189

Total stockholders' equity 25080 26388 29569 30768 32873

Total liabilities and stockholders' equity 25290

0

28422

9

30673

6

31601

1

34002

8

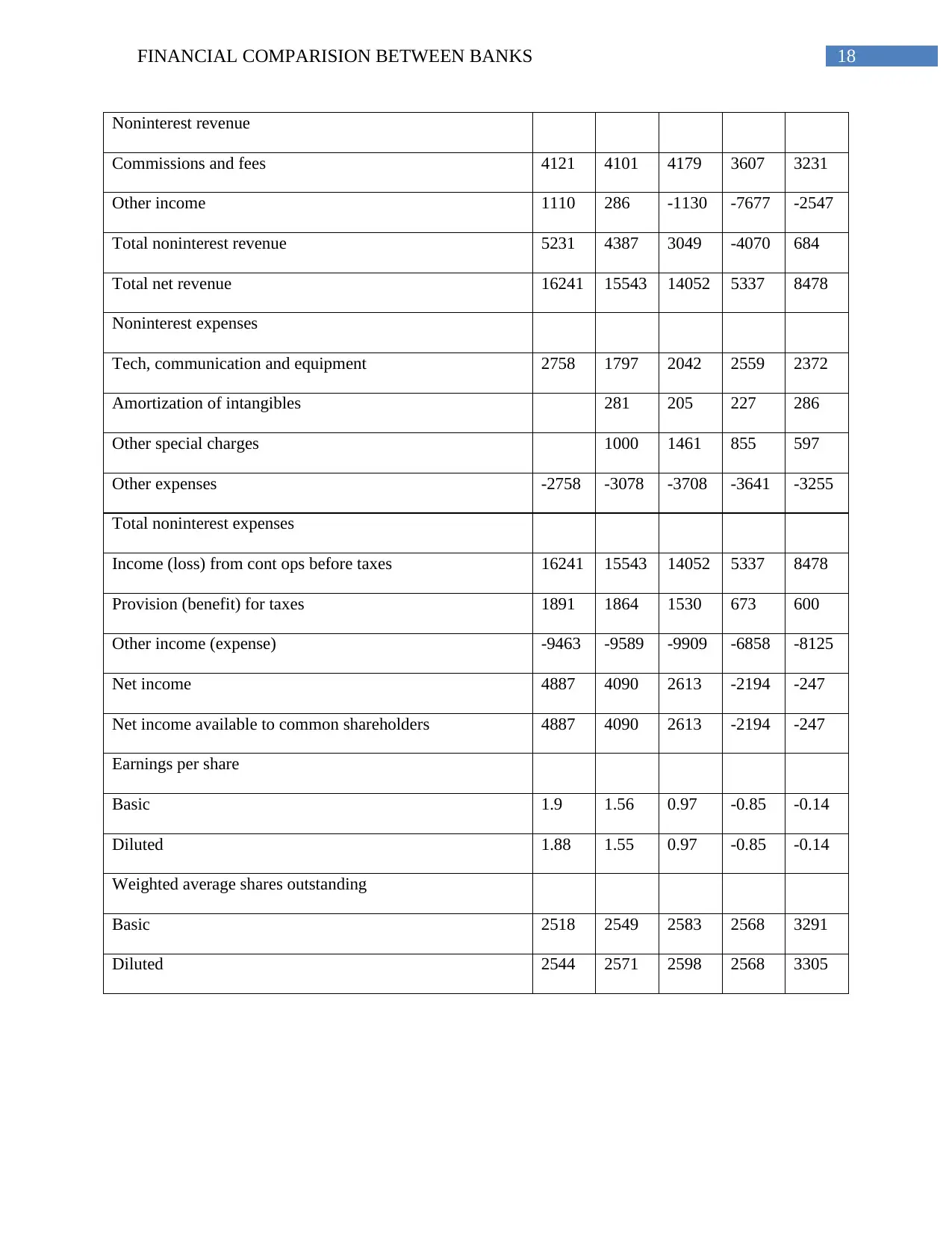

STANDARD CHARTERED PLC (02888) CashFlowFlag

INCOME STATEMENT

Fiscal year ends in December. USD in millions except per

share data.

2012-

12

2013-

12

2014-

12

2015-

12

2016-

12

Revenue

Interest income

Other assets 18258 17593 16984 14613 13010

Total interest income 18258 17593 16984 14613 13010

Interest expense

Other expense 7248 6437 5981 5206 5216

Total interest expense 7248 6437 5981 5206 5216

Net interest income 11010 11156 11003 9407 7794

Other liabilities 18747 23710 25807 26763 33148

Total liabilities 22782

0

25784

1

27716

7

28524

3

30715

4

Stockholders' equity

Common stock 5272 5333 5892 5881 6351

Retained earnings 10222 12003 14064 15463 17334

Accumulated other comprehensive income 9586 9053 9613 9424 9189

Total stockholders' equity 25080 26388 29569 30768 32873

Total liabilities and stockholders' equity 25290

0

28422

9

30673

6

31601

1

34002

8

STANDARD CHARTERED PLC (02888) CashFlowFlag

INCOME STATEMENT

Fiscal year ends in December. USD in millions except per

share data.

2012-

12

2013-

12

2014-

12

2015-

12

2016-

12

Revenue

Interest income

Other assets 18258 17593 16984 14613 13010

Total interest income 18258 17593 16984 14613 13010

Interest expense

Other expense 7248 6437 5981 5206 5216

Total interest expense 7248 6437 5981 5206 5216

Net interest income 11010 11156 11003 9407 7794

18FINANCIAL COMPARISION BETWEEN BANKS

Noninterest revenue

Commissions and fees 4121 4101 4179 3607 3231

Other income 1110 286 -1130 -7677 -2547

Total noninterest revenue 5231 4387 3049 -4070 684

Total net revenue 16241 15543 14052 5337 8478

Noninterest expenses

Tech, communication and equipment 2758 1797 2042 2559 2372

Amortization of intangibles 281 205 227 286

Other special charges 1000 1461 855 597

Other expenses -2758 -3078 -3708 -3641 -3255

Total noninterest expenses

Income (loss) from cont ops before taxes 16241 15543 14052 5337 8478

Provision (benefit) for taxes 1891 1864 1530 673 600

Other income (expense) -9463 -9589 -9909 -6858 -8125

Net income 4887 4090 2613 -2194 -247

Net income available to common shareholders 4887 4090 2613 -2194 -247

Earnings per share

Basic 1.9 1.56 0.97 -0.85 -0.14

Diluted 1.88 1.55 0.97 -0.85 -0.14

Weighted average shares outstanding

Basic 2518 2549 2583 2568 3291

Diluted 2544 2571 2598 2568 3305

Noninterest revenue

Commissions and fees 4121 4101 4179 3607 3231

Other income 1110 286 -1130 -7677 -2547

Total noninterest revenue 5231 4387 3049 -4070 684

Total net revenue 16241 15543 14052 5337 8478

Noninterest expenses

Tech, communication and equipment 2758 1797 2042 2559 2372

Amortization of intangibles 281 205 227 286

Other special charges 1000 1461 855 597

Other expenses -2758 -3078 -3708 -3641 -3255

Total noninterest expenses

Income (loss) from cont ops before taxes 16241 15543 14052 5337 8478

Provision (benefit) for taxes 1891 1864 1530 673 600

Other income (expense) -9463 -9589 -9909 -6858 -8125

Net income 4887 4090 2613 -2194 -247

Net income available to common shareholders 4887 4090 2613 -2194 -247

Earnings per share

Basic 1.9 1.56 0.97 -0.85 -0.14

Diluted 1.88 1.55 0.97 -0.85 -0.14

Weighted average shares outstanding

Basic 2518 2549 2583 2568 3291

Diluted 2544 2571 2598 2568 3305

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

19FINANCIAL COMPARISION BETWEEN BANKS

UNITED OVERSEAS BANK LTD (U11) CashFlowFlag

INCOME STATEMENT

Fiscal year ends in December. SGD in millions except per

share data.

2012-

12

2013-

12

2014-

12

2015-

12

2016-

12

Revenue

Interest income

Other assets 6202 6508 7189 7826 8291

Total interest income 6202 6508 7189 7826 8291

Interest expense

Other expense 2285 2388 2632 2900 3300

Total interest expense 2285 2388 2632 2900 3300

Net interest income 3917 4120 4558 4926 4991

Noninterest revenue

Commissions and fees 1508 1731 1749 1883 1931

Securities gains (losses) 218 313 101

Other income -17 -41 -386 -453 -179

Total noninterest revenue 1490 1690 1581 1744 1852

Total net revenue 5407 5810 6139 6670 6843

Noninterest expenses

Tech, communication and equipment 1013 1022 1159 1349 1437

Amortization of intangibles 7

Other expenses -1021 -1022 -1159 -1349 -1437

Total noninterest expenses

Income (loss) from cont ops before taxes 5407 5810 6139 6670 6843

Provision (benefit) for taxes 531 559 561 649 669

UNITED OVERSEAS BANK LTD (U11) CashFlowFlag

INCOME STATEMENT

Fiscal year ends in December. SGD in millions except per

share data.

2012-

12

2013-

12

2014-

12

2015-

12

2016-

12

Revenue

Interest income

Other assets 6202 6508 7189 7826 8291

Total interest income 6202 6508 7189 7826 8291

Interest expense

Other expense 2285 2388 2632 2900 3300

Total interest expense 2285 2388 2632 2900 3300

Net interest income 3917 4120 4558 4926 4991

Noninterest revenue

Commissions and fees 1508 1731 1749 1883 1931

Securities gains (losses) 218 313 101

Other income -17 -41 -386 -453 -179

Total noninterest revenue 1490 1690 1581 1744 1852

Total net revenue 5407 5810 6139 6670 6843

Noninterest expenses

Tech, communication and equipment 1013 1022 1159 1349 1437

Amortization of intangibles 7

Other expenses -1021 -1022 -1159 -1349 -1437

Total noninterest expenses

Income (loss) from cont ops before taxes 5407 5810 6139 6670 6843

Provision (benefit) for taxes 531 559 561 649 669

20FINANCIAL COMPARISION BETWEEN BANKS

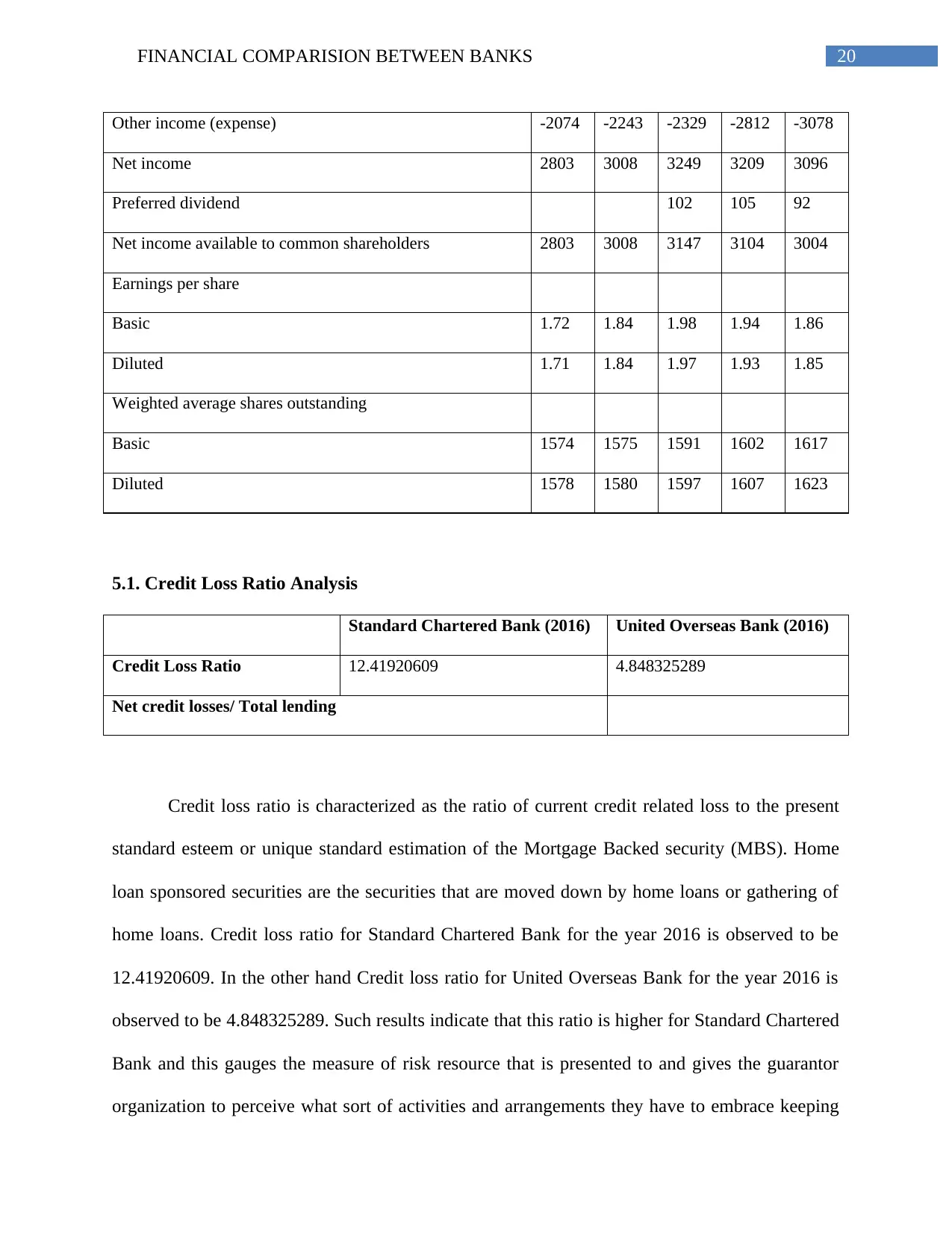

Other income (expense) -2074 -2243 -2329 -2812 -3078

Net income 2803 3008 3249 3209 3096

Preferred dividend 102 105 92

Net income available to common shareholders 2803 3008 3147 3104 3004

Earnings per share

Basic 1.72 1.84 1.98 1.94 1.86

Diluted 1.71 1.84 1.97 1.93 1.85

Weighted average shares outstanding

Basic 1574 1575 1591 1602 1617

Diluted 1578 1580 1597 1607 1623

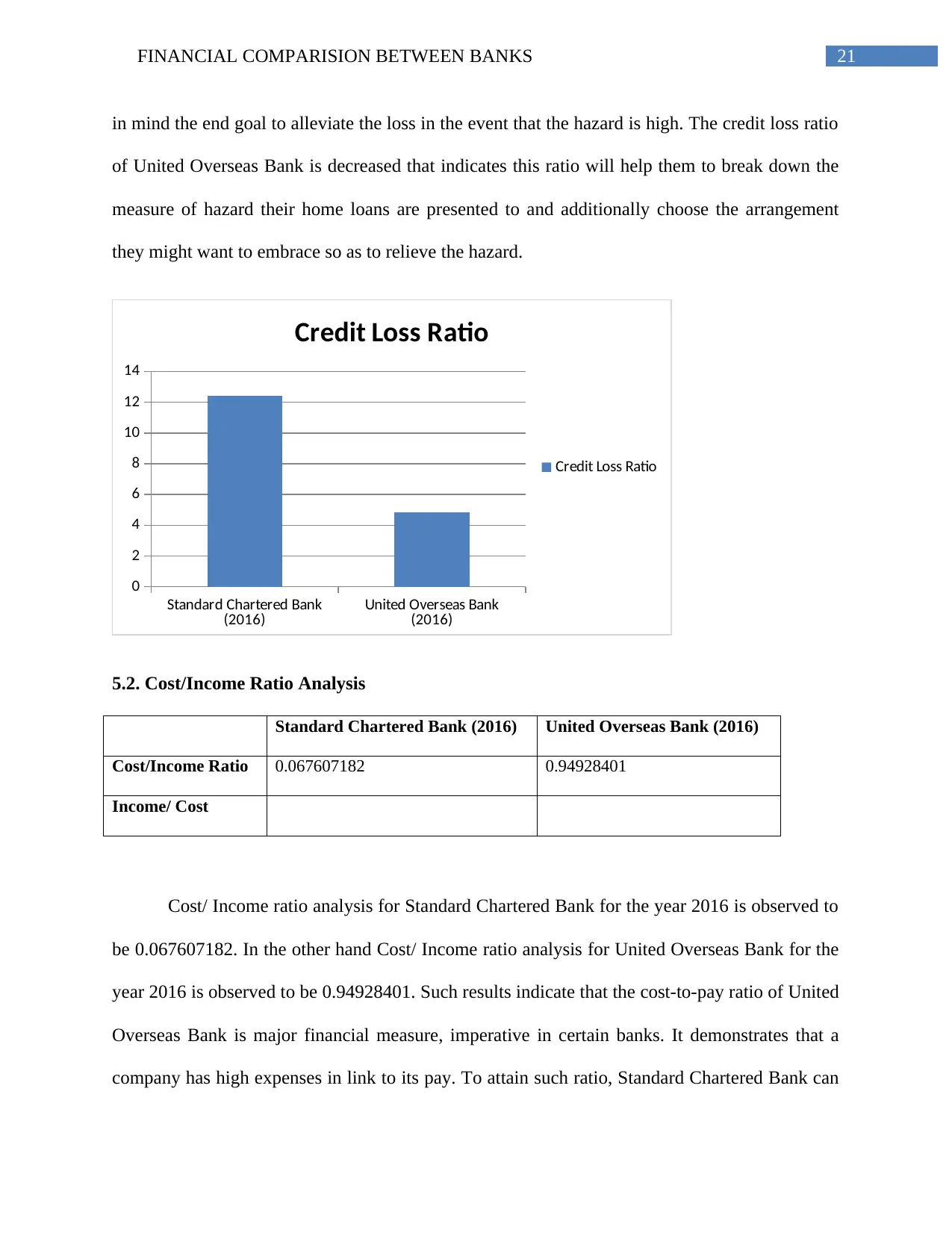

5.1. Credit Loss Ratio Analysis

Standard Chartered Bank (2016) United Overseas Bank (2016)

Credit Loss Ratio 12.41920609 4.848325289

Net credit losses/ Total lending

Credit loss ratio is characterized as the ratio of current credit related loss to the present

standard esteem or unique standard estimation of the Mortgage Backed security (MBS). Home

loan sponsored securities are the securities that are moved down by home loans or gathering of

home loans. Credit loss ratio for Standard Chartered Bank for the year 2016 is observed to be

12.41920609. In the other hand Credit loss ratio for United Overseas Bank for the year 2016 is

observed to be 4.848325289. Such results indicate that this ratio is higher for Standard Chartered

Bank and this gauges the measure of risk resource that is presented to and gives the guarantor

organization to perceive what sort of activities and arrangements they have to embrace keeping

Other income (expense) -2074 -2243 -2329 -2812 -3078

Net income 2803 3008 3249 3209 3096

Preferred dividend 102 105 92

Net income available to common shareholders 2803 3008 3147 3104 3004

Earnings per share

Basic 1.72 1.84 1.98 1.94 1.86

Diluted 1.71 1.84 1.97 1.93 1.85

Weighted average shares outstanding

Basic 1574 1575 1591 1602 1617

Diluted 1578 1580 1597 1607 1623

5.1. Credit Loss Ratio Analysis

Standard Chartered Bank (2016) United Overseas Bank (2016)

Credit Loss Ratio 12.41920609 4.848325289

Net credit losses/ Total lending

Credit loss ratio is characterized as the ratio of current credit related loss to the present

standard esteem or unique standard estimation of the Mortgage Backed security (MBS). Home

loan sponsored securities are the securities that are moved down by home loans or gathering of

home loans. Credit loss ratio for Standard Chartered Bank for the year 2016 is observed to be

12.41920609. In the other hand Credit loss ratio for United Overseas Bank for the year 2016 is

observed to be 4.848325289. Such results indicate that this ratio is higher for Standard Chartered

Bank and this gauges the measure of risk resource that is presented to and gives the guarantor

organization to perceive what sort of activities and arrangements they have to embrace keeping

21FINANCIAL COMPARISION BETWEEN BANKS

in mind the end goal to alleviate the loss in the event that the hazard is high. The credit loss ratio

of United Overseas Bank is decreased that indicates this ratio will help them to break down the

measure of hazard their home loans are presented to and additionally choose the arrangement

they might want to embrace so as to relieve the hazard.

Standard Chartered Bank

(2016) United Overseas Bank

(2016)

0

2

4

6

8

10

12

14

Credit Loss Ratio

Credit Loss Ratio

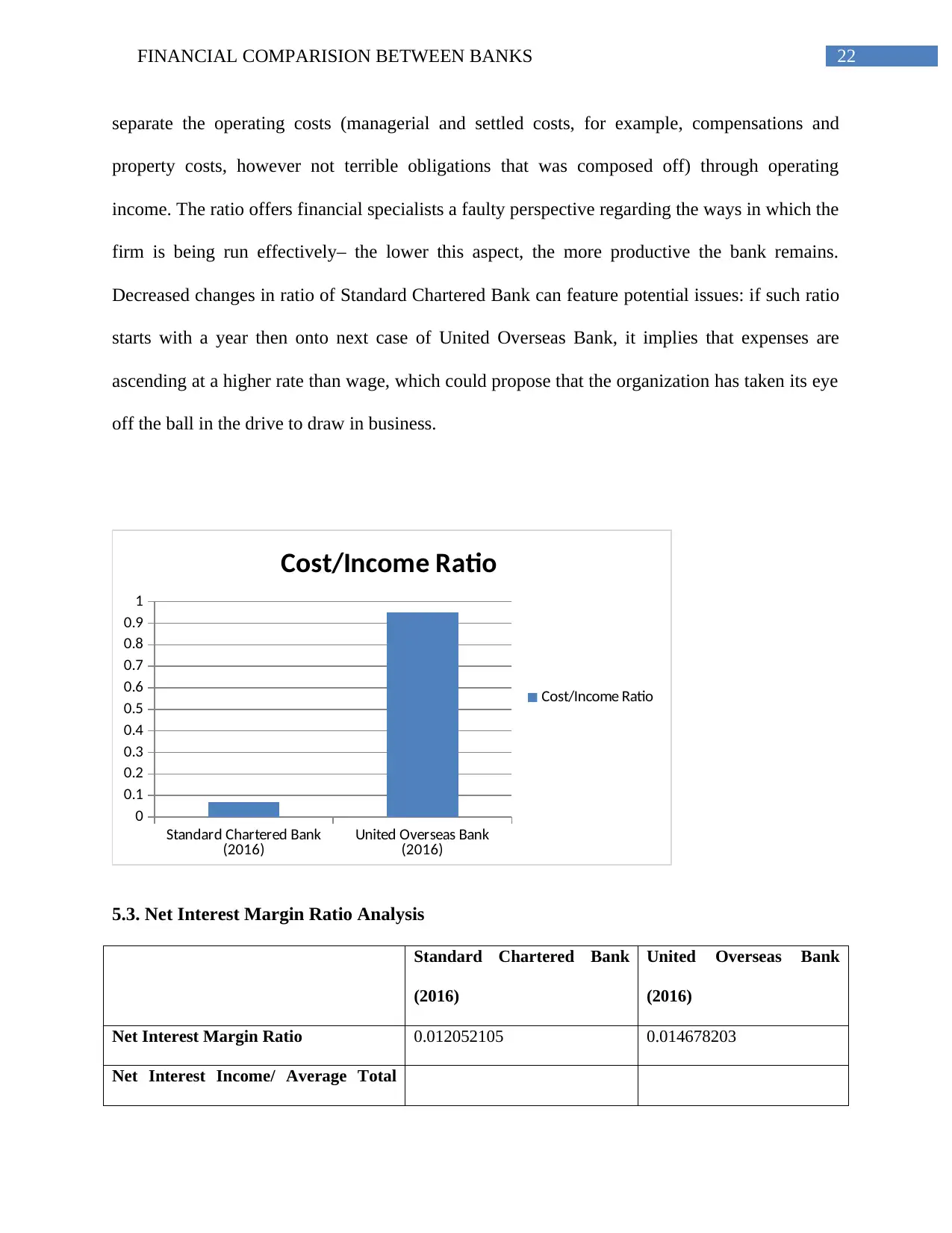

5.2. Cost/Income Ratio Analysis

Standard Chartered Bank (2016) United Overseas Bank (2016)

Cost/Income Ratio 0.067607182 0.94928401

Income/ Cost

Cost/ Income ratio analysis for Standard Chartered Bank for the year 2016 is observed to

be 0.067607182. In the other hand Cost/ Income ratio analysis for United Overseas Bank for the

year 2016 is observed to be 0.94928401. Such results indicate that the cost-to-pay ratio of United

Overseas Bank is major financial measure, imperative in certain banks. It demonstrates that a

company has high expenses in link to its pay. To attain such ratio, Standard Chartered Bank can

in mind the end goal to alleviate the loss in the event that the hazard is high. The credit loss ratio

of United Overseas Bank is decreased that indicates this ratio will help them to break down the

measure of hazard their home loans are presented to and additionally choose the arrangement

they might want to embrace so as to relieve the hazard.

Standard Chartered Bank

(2016) United Overseas Bank

(2016)

0

2

4

6

8

10

12

14

Credit Loss Ratio

Credit Loss Ratio

5.2. Cost/Income Ratio Analysis

Standard Chartered Bank (2016) United Overseas Bank (2016)

Cost/Income Ratio 0.067607182 0.94928401

Income/ Cost

Cost/ Income ratio analysis for Standard Chartered Bank for the year 2016 is observed to

be 0.067607182. In the other hand Cost/ Income ratio analysis for United Overseas Bank for the

year 2016 is observed to be 0.94928401. Such results indicate that the cost-to-pay ratio of United

Overseas Bank is major financial measure, imperative in certain banks. It demonstrates that a

company has high expenses in link to its pay. To attain such ratio, Standard Chartered Bank can

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

22FINANCIAL COMPARISION BETWEEN BANKS

separate the operating costs (managerial and settled costs, for example, compensations and

property costs, however not terrible obligations that was composed off) through operating

income. The ratio offers financial specialists a faulty perspective regarding the ways in which the

firm is being run effectively– the lower this aspect, the more productive the bank remains.

Decreased changes in ratio of Standard Chartered Bank can feature potential issues: if such ratio

starts with a year then onto next case of United Overseas Bank, it implies that expenses are

ascending at a higher rate than wage, which could propose that the organization has taken its eye

off the ball in the drive to draw in business.

Standard Chartered Bank

(2016) United Overseas Bank

(2016)

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1

Cost/Income Ratio

Cost/Income Ratio

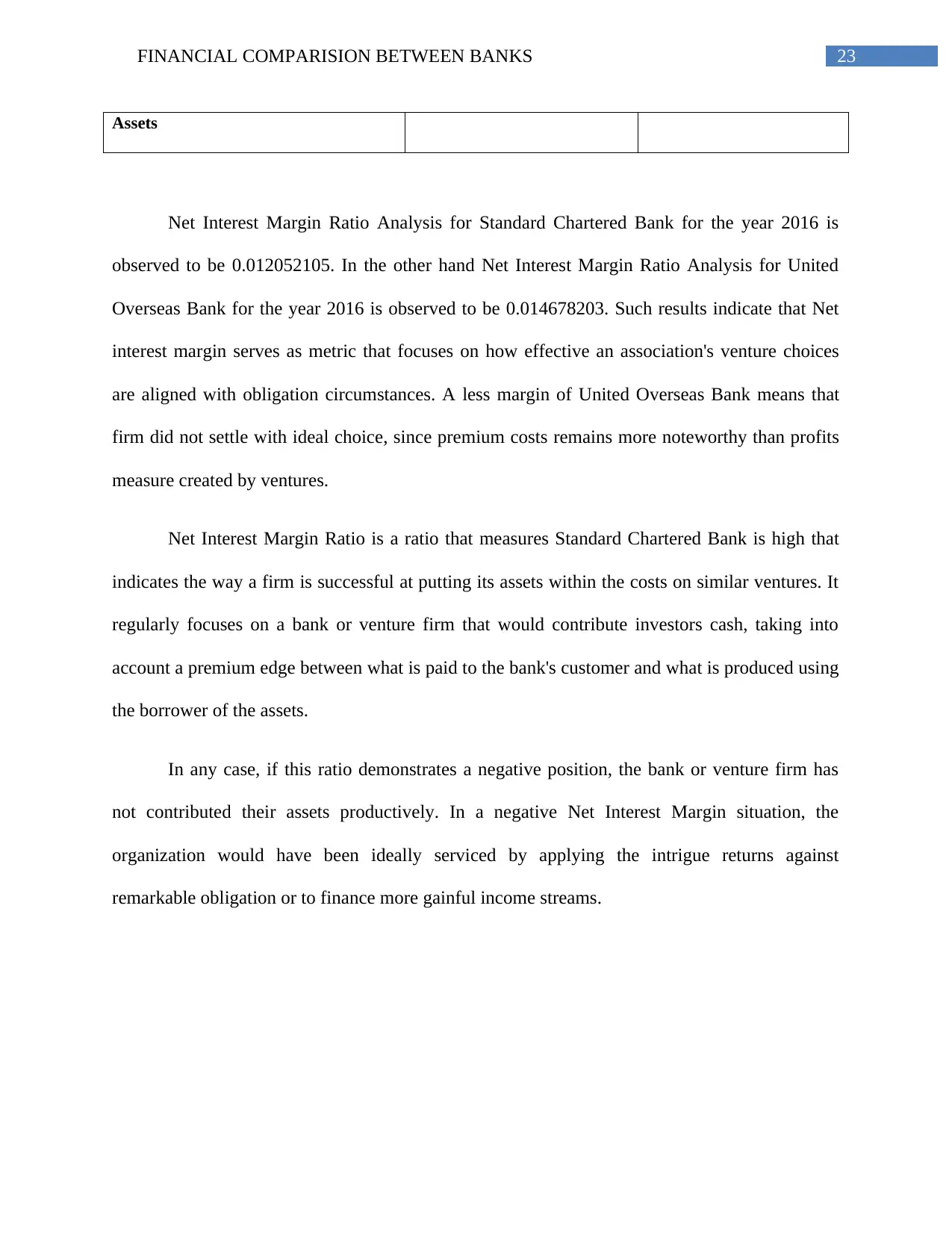

5.3. Net Interest Margin Ratio Analysis

Standard Chartered Bank

(2016)

United Overseas Bank

(2016)

Net Interest Margin Ratio 0.012052105 0.014678203

Net Interest Income/ Average Total

separate the operating costs (managerial and settled costs, for example, compensations and

property costs, however not terrible obligations that was composed off) through operating

income. The ratio offers financial specialists a faulty perspective regarding the ways in which the

firm is being run effectively– the lower this aspect, the more productive the bank remains.

Decreased changes in ratio of Standard Chartered Bank can feature potential issues: if such ratio

starts with a year then onto next case of United Overseas Bank, it implies that expenses are

ascending at a higher rate than wage, which could propose that the organization has taken its eye

off the ball in the drive to draw in business.

Standard Chartered Bank

(2016) United Overseas Bank

(2016)

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1

Cost/Income Ratio

Cost/Income Ratio

5.3. Net Interest Margin Ratio Analysis

Standard Chartered Bank

(2016)

United Overseas Bank

(2016)

Net Interest Margin Ratio 0.012052105 0.014678203

Net Interest Income/ Average Total

23FINANCIAL COMPARISION BETWEEN BANKS

Assets

Net Interest Margin Ratio Analysis for Standard Chartered Bank for the year 2016 is

observed to be 0.012052105. In the other hand Net Interest Margin Ratio Analysis for United

Overseas Bank for the year 2016 is observed to be 0.014678203. Such results indicate that Net

interest margin serves as metric that focuses on how effective an association's venture choices

are aligned with obligation circumstances. A less margin of United Overseas Bank means that

firm did not settle with ideal choice, since premium costs remains more noteworthy than profits

measure created by ventures.

Net Interest Margin Ratio is a ratio that measures Standard Chartered Bank is high that

indicates the way a firm is successful at putting its assets within the costs on similar ventures. It

regularly focuses on a bank or venture firm that would contribute investors cash, taking into

account a premium edge between what is paid to the bank's customer and what is produced using

the borrower of the assets.

In any case, if this ratio demonstrates a negative position, the bank or venture firm has

not contributed their assets productively. In a negative Net Interest Margin situation, the

organization would have been ideally serviced by applying the intrigue returns against

remarkable obligation or to finance more gainful income streams.

Assets

Net Interest Margin Ratio Analysis for Standard Chartered Bank for the year 2016 is

observed to be 0.012052105. In the other hand Net Interest Margin Ratio Analysis for United

Overseas Bank for the year 2016 is observed to be 0.014678203. Such results indicate that Net

interest margin serves as metric that focuses on how effective an association's venture choices

are aligned with obligation circumstances. A less margin of United Overseas Bank means that

firm did not settle with ideal choice, since premium costs remains more noteworthy than profits

measure created by ventures.

Net Interest Margin Ratio is a ratio that measures Standard Chartered Bank is high that

indicates the way a firm is successful at putting its assets within the costs on similar ventures. It

regularly focuses on a bank or venture firm that would contribute investors cash, taking into

account a premium edge between what is paid to the bank's customer and what is produced using

the borrower of the assets.

In any case, if this ratio demonstrates a negative position, the bank or venture firm has

not contributed their assets productively. In a negative Net Interest Margin situation, the

organization would have been ideally serviced by applying the intrigue returns against

remarkable obligation or to finance more gainful income streams.

24FINANCIAL COMPARISION BETWEEN BANKS

Standard Chartered Bank

(2016) United Overseas Bank

(2016)

0

0.002

0.004

0.006

0.008

0.01

0.012

0.014

0.016

Net Interest Margin Ratio

Net Interest Margin Ratio

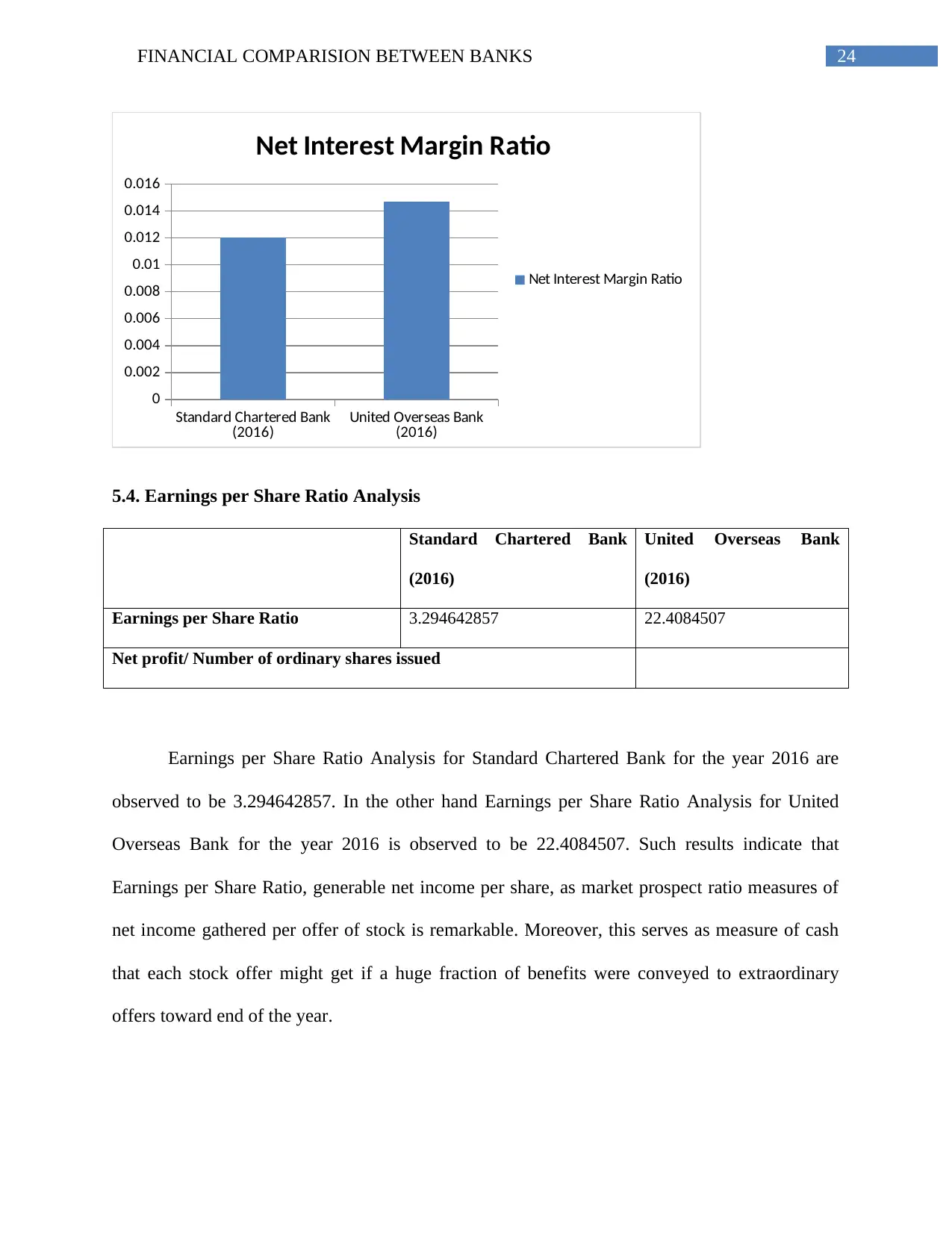

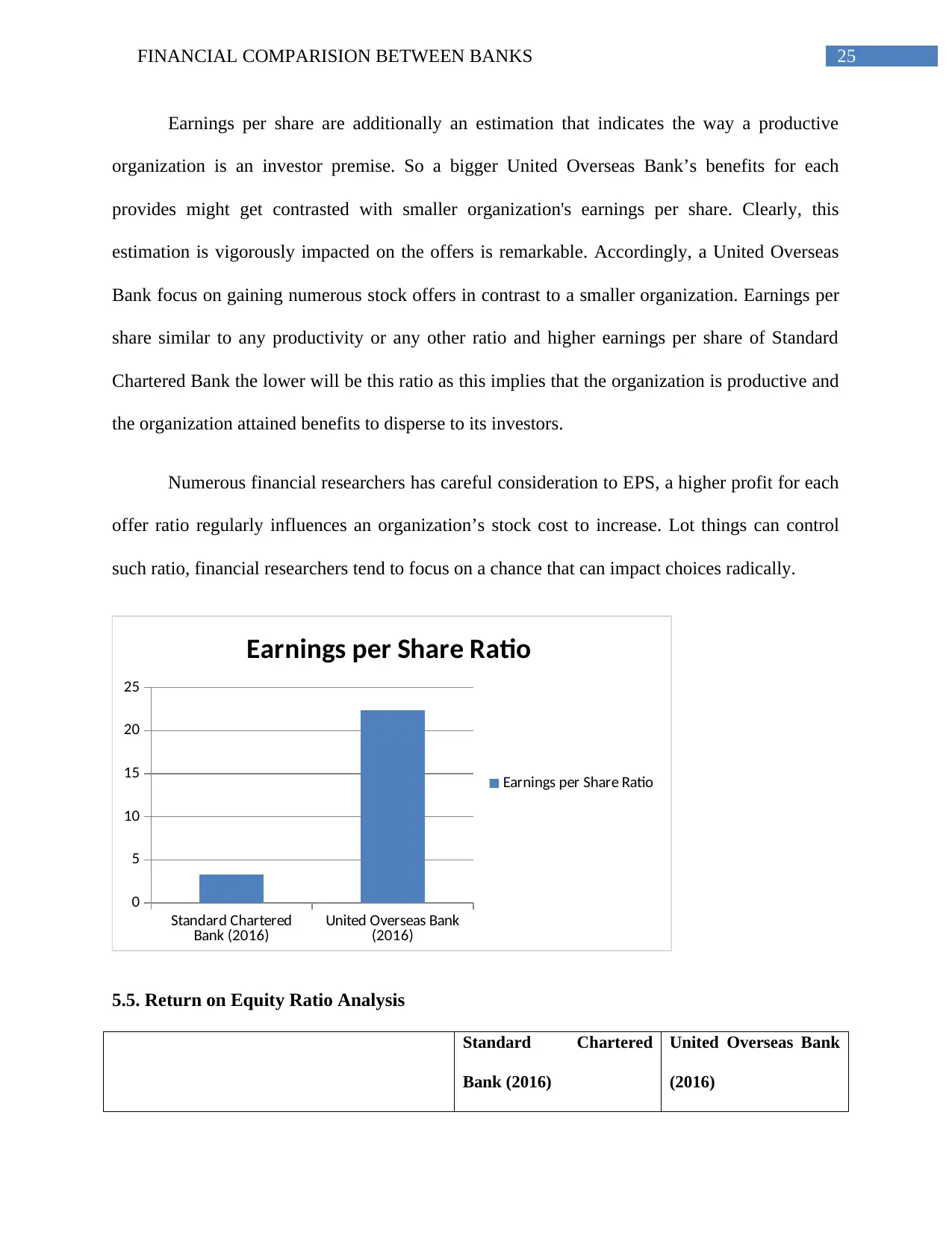

5.4. Earnings per Share Ratio Analysis

Standard Chartered Bank

(2016)

United Overseas Bank

(2016)

Earnings per Share Ratio 3.294642857 22.4084507

Net profit/ Number of ordinary shares issued

Earnings per Share Ratio Analysis for Standard Chartered Bank for the year 2016 are

observed to be 3.294642857. In the other hand Earnings per Share Ratio Analysis for United

Overseas Bank for the year 2016 is observed to be 22.4084507. Such results indicate that

Earnings per Share Ratio, generable net income per share, as market prospect ratio measures of

net income gathered per offer of stock is remarkable. Moreover, this serves as measure of cash

that each stock offer might get if a huge fraction of benefits were conveyed to extraordinary

offers toward end of the year.

Standard Chartered Bank

(2016) United Overseas Bank

(2016)

0

0.002

0.004

0.006

0.008

0.01

0.012

0.014

0.016

Net Interest Margin Ratio

Net Interest Margin Ratio

5.4. Earnings per Share Ratio Analysis

Standard Chartered Bank

(2016)

United Overseas Bank

(2016)

Earnings per Share Ratio 3.294642857 22.4084507

Net profit/ Number of ordinary shares issued

Earnings per Share Ratio Analysis for Standard Chartered Bank for the year 2016 are

observed to be 3.294642857. In the other hand Earnings per Share Ratio Analysis for United

Overseas Bank for the year 2016 is observed to be 22.4084507. Such results indicate that

Earnings per Share Ratio, generable net income per share, as market prospect ratio measures of

net income gathered per offer of stock is remarkable. Moreover, this serves as measure of cash

that each stock offer might get if a huge fraction of benefits were conveyed to extraordinary

offers toward end of the year.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

25FINANCIAL COMPARISION BETWEEN BANKS

Earnings per share are additionally an estimation that indicates the way a productive