Understanding Budgeting Techniques

VerifiedAdded on 2020/11/23

|16

|4934

|74

Essay

AI Summary

This assignment delves into the world of budgeting techniques, exploring different approaches such as zero-based, activity-based, incremental, and rolling budgeting. It examines the advantages, disadvantages, and applications of each method, highlighting their suitability for various organizational contexts. The assignment encourages a critical understanding of how different budgeting techniques can contribute to effective financial planning and control.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Financial Control and

Budgeting

Budgeting

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

INTRODUCTION

The term financial control refers to a system of tracing or assessing the resources directed to

an organization for carrying on the business operations and thus measuring, evaluating and

monitoring resources implemented to determine the progress of business organisation. Financial

control helps in checking report accuracy so as to eliminate fraud, error or misstatements of

information if any, with the purpose of protecting the physical as well as intangible resources of

the organization. Furthermore, report has cover challenges & recent developments faced by

NHS. It has also explained alternative funding options available with health and social care

service organisation. The agency theory, corporate Governance and accountability issues faced

by health and social care organisation has been explained. Budgeting is a process of making

future plans for assessing future expected revenue and expenses form business operations of an

organization. It estimates about future events by considering internal and external factors of the

organization. Budgeting function includes planning of business activities, developing business

strategies etc. By using various budgeting approaches, profits can be increased within given

business environment.

MAIN BODY

TASK 1

a. The recent developments with regards to the legal, financial and regulatory environment of

health and social care

The NHS is a national health service which is a largest health and social care in the UK

providing the care services. There are various problems faced by NHS during their 70th

anniversary. These problems consist of providing better care to more people with less money.

The reforms for solving these problems consist of the legal environment of health and social

care. There have been various development in health and social care has their have been

significant technologies which have been emerged such as artificial intelligence, genomic and

personalised medicine (Atanelishvili and et.al., 2017). Also, there are some apps and devices

which assist people to manage chronic illness themselves.

Moreover, there are various laws and legislation which are being made in order to protect

the people and provide them better care services. Such as Health and Social Care act, 2012 which

The term financial control refers to a system of tracing or assessing the resources directed to

an organization for carrying on the business operations and thus measuring, evaluating and

monitoring resources implemented to determine the progress of business organisation. Financial

control helps in checking report accuracy so as to eliminate fraud, error or misstatements of

information if any, with the purpose of protecting the physical as well as intangible resources of

the organization. Furthermore, report has cover challenges & recent developments faced by

NHS. It has also explained alternative funding options available with health and social care

service organisation. The agency theory, corporate Governance and accountability issues faced

by health and social care organisation has been explained. Budgeting is a process of making

future plans for assessing future expected revenue and expenses form business operations of an

organization. It estimates about future events by considering internal and external factors of the

organization. Budgeting function includes planning of business activities, developing business

strategies etc. By using various budgeting approaches, profits can be increased within given

business environment.

MAIN BODY

TASK 1

a. The recent developments with regards to the legal, financial and regulatory environment of

health and social care

The NHS is a national health service which is a largest health and social care in the UK

providing the care services. There are various problems faced by NHS during their 70th

anniversary. These problems consist of providing better care to more people with less money.

The reforms for solving these problems consist of the legal environment of health and social

care. There have been various development in health and social care has their have been

significant technologies which have been emerged such as artificial intelligence, genomic and

personalised medicine (Atanelishvili and et.al., 2017). Also, there are some apps and devices

which assist people to manage chronic illness themselves.

Moreover, there are various laws and legislation which are being made in order to protect

the people and provide them better care services. Such as Health and Social Care act, 2012 which

provide understanding about the health inequalities and include specified duties for the health

bodies (Rogulenko and et.al., 2016). This Act also brought changes for local authorities on

public health functions. NHS is funded through central government. With the recent

development the NHS is able to solve these problems which assist in providing better services to

the patients.

The health and social care require funding for their operations which is provided through

central taxation to the NHS. The health and social have to follow the regulations of the quality

and safety of care offered by health care provider. So there have been development in the legal

environment of NHS as there have been developed laws such as health and social care 2014. The

regulation followed properly are monitored by care quality commission and department of health

(Burtonshaw-Gunn, 2017). Also, the financial environment of the health and social care is

improving as there are may trust and other organisation investing in the NHS for improving the

quality of services provided by NHS.

b. Usefulness of alternatives funding options

The organisation can use alternative funding options for performing its key operations

and provide better services to the patients. The following are the alternative funding options :

Private finance initiative : It is the way of financing the public sector project through

the private sector. The government authority make payment to the private company. It

reduces the burden of government to finance the public project. The government provide

the private company with the amount with interest. The NHS in order to get the funds

can use the private finance initiative which assist in building long term relationship with

the private company and getting the funds for their projects.

Resources : It means using the resources for getting the funds which assist in providing

the funds for the operations through use of resources of organisation. These resources

which act as funding option for the health and social care does not involve interest rates

and thus it is the easy source of funding.

Agency partnership : It is the firm that does not hold the decision making in the

company but holds and share or profit. NHS can use the funding from the agency partners

for performing their duties and operation and fulfilled the requirement of capital through

the agency partnership. It is useful source of alternative funding for the NHS because

these agencies are under their control can the NHS have control over their operations.

bodies (Rogulenko and et.al., 2016). This Act also brought changes for local authorities on

public health functions. NHS is funded through central government. With the recent

development the NHS is able to solve these problems which assist in providing better services to

the patients.

The health and social care require funding for their operations which is provided through

central taxation to the NHS. The health and social have to follow the regulations of the quality

and safety of care offered by health care provider. So there have been development in the legal

environment of NHS as there have been developed laws such as health and social care 2014. The

regulation followed properly are monitored by care quality commission and department of health

(Burtonshaw-Gunn, 2017). Also, the financial environment of the health and social care is

improving as there are may trust and other organisation investing in the NHS for improving the

quality of services provided by NHS.

b. Usefulness of alternatives funding options

The organisation can use alternative funding options for performing its key operations

and provide better services to the patients. The following are the alternative funding options :

Private finance initiative : It is the way of financing the public sector project through

the private sector. The government authority make payment to the private company. It

reduces the burden of government to finance the public project. The government provide

the private company with the amount with interest. The NHS in order to get the funds

can use the private finance initiative which assist in building long term relationship with

the private company and getting the funds for their projects.

Resources : It means using the resources for getting the funds which assist in providing

the funds for the operations through use of resources of organisation. These resources

which act as funding option for the health and social care does not involve interest rates

and thus it is the easy source of funding.

Agency partnership : It is the firm that does not hold the decision making in the

company but holds and share or profit. NHS can use the funding from the agency partners

for performing their duties and operation and fulfilled the requirement of capital through

the agency partnership. It is useful source of alternative funding for the NHS because

these agencies are under their control can the NHS have control over their operations.

Outsourcing : It is business practice in which the company hires another company for

performing tasks, operations, for providing services etc. Outsourcing assist in reducing

the cost for the firm. NHS through use of Outsourcing is able to provide better services to

the patients by hiring the individual for outsourcing which reduces the cost for the health

and social care and are able to reach to large number of people.

Tendering : It means using the tenders for providing health and social care services and

agreeing to the details of contract. In health and social sectors tendering assist in inviting

the health and social care providers to provide their services to the people which assist in

reducing the cost for the health and social sector and assist in reaching to the large

number of people.

NHS can use the alternative financing options for funding its operations which assist in

reducing their cost and are able to provide better care services to the patients and satisfy them

through their better care services. This options are used as funding options because this options

assist in reducing the cost of the company and are able to provide better services to the patients.

c. The key stakeholders within the social sector and the way of communication with the

stakeholders

Stakeholders are those individuals which have their interest in the firm's operations.

Followings are the various stakeholders which are involved in Health and Social sector :

Commissioners : The commissioner are those which provide funds in the health and

social sector for performing various operations.

Patients : These are customers in the health and social care which are provided with the

care services.

Collaborators : This are the companies and individuals in the health and social sector

with which the organisation collaborate in order to provide care services (Di Francesco

and Alford, 2016).

Contributors : This are the organisation and individuals with which the health and social

care providers work to deliver their services.

Channels or media : The media play a key role in promoting the services and capturing

the news regrading the improvement in the health and social sector. It assists in reaching

the market and customers.

performing tasks, operations, for providing services etc. Outsourcing assist in reducing

the cost for the firm. NHS through use of Outsourcing is able to provide better services to

the patients by hiring the individual for outsourcing which reduces the cost for the health

and social care and are able to reach to large number of people.

Tendering : It means using the tenders for providing health and social care services and

agreeing to the details of contract. In health and social sectors tendering assist in inviting

the health and social care providers to provide their services to the people which assist in

reducing the cost for the health and social sector and assist in reaching to the large

number of people.

NHS can use the alternative financing options for funding its operations which assist in

reducing their cost and are able to provide better care services to the patients and satisfy them

through their better care services. This options are used as funding options because this options

assist in reducing the cost of the company and are able to provide better services to the patients.

c. The key stakeholders within the social sector and the way of communication with the

stakeholders

Stakeholders are those individuals which have their interest in the firm's operations.

Followings are the various stakeholders which are involved in Health and Social sector :

Commissioners : The commissioner are those which provide funds in the health and

social sector for performing various operations.

Patients : These are customers in the health and social care which are provided with the

care services.

Collaborators : This are the companies and individuals in the health and social sector

with which the organisation collaborate in order to provide care services (Di Francesco

and Alford, 2016).

Contributors : This are the organisation and individuals with which the health and social

care providers work to deliver their services.

Channels or media : The media play a key role in promoting the services and capturing

the news regrading the improvement in the health and social sector. It assists in reaching

the market and customers.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Staff : These are people working in the organisation and provide the services to the

patients and includes nurses , doctors etc.

Competitors : These are the people working in the same areas and are providing the

same services to the patients.

These are the key stakeholders of the NHS which are required to be informed regarding

the various operations and performance of the organisation.

There are various ways which assist in communicating with the stakeholders that are as

follows :

Face -to -Face commination : It is the way in which the health and social care providers

can communicate with the stakeholders such as patients, staff etc. this communication

method is adopted in NHS for communicating with patients regarding their health

treatment and other concerns. Whereas staff is also involved in face to face

communication in which it communicates regarding the health of their patients to the

doctors and change sin the treatment required for better heath of patients (Osadchy and

Akhmetshin, 2015).

Electronic media : It consists of email, social media, telephone etc. Which are used by

the health and social care providers for communicating with the stakeholders. This

communication method is effective for communicating with those stakeholders which are

not located in the same area or country. It assists in providing details regarding the

various operations of the health and social care. NHS is using this method

communication in order to communicate with the investors, contributors etc. which are

not present in the same city or country. Paper- based communication or written communication : It assists in communicate

formally with the stakeholders regarding the services and other matters. This method is

used in order have physical evidence of communication. The health and social care

service providers can use this method in order to communicate with suppliers, customers,

staff etc.

1. Agency theory : It is the principle used to explain and resolve the issues in

relationship between principle and agents. There are various issues between the

principle and agent in this sector (Burns and Walker, 2015). The principle in this

sector is the patients which appoints an agent that is health providers to advise the

patients and includes nurses , doctors etc.

Competitors : These are the people working in the same areas and are providing the

same services to the patients.

These are the key stakeholders of the NHS which are required to be informed regarding

the various operations and performance of the organisation.

There are various ways which assist in communicating with the stakeholders that are as

follows :

Face -to -Face commination : It is the way in which the health and social care providers

can communicate with the stakeholders such as patients, staff etc. this communication

method is adopted in NHS for communicating with patients regarding their health

treatment and other concerns. Whereas staff is also involved in face to face

communication in which it communicates regarding the health of their patients to the

doctors and change sin the treatment required for better heath of patients (Osadchy and

Akhmetshin, 2015).

Electronic media : It consists of email, social media, telephone etc. Which are used by

the health and social care providers for communicating with the stakeholders. This

communication method is effective for communicating with those stakeholders which are

not located in the same area or country. It assists in providing details regarding the

various operations of the health and social care. NHS is using this method

communication in order to communicate with the investors, contributors etc. which are

not present in the same city or country. Paper- based communication or written communication : It assists in communicate

formally with the stakeholders regarding the services and other matters. This method is

used in order have physical evidence of communication. The health and social care

service providers can use this method in order to communicate with suppliers, customers,

staff etc.

1. Agency theory : It is the principle used to explain and resolve the issues in

relationship between principle and agents. There are various issues between the

principle and agent in this sector (Burns and Walker, 2015). The principle in this

sector is the patients which appoints an agent that is health providers to advise the

principle to make decision regarding their treatment. But the issues are there

because the providers chooses to maximise its profitability rather than advising

the patients with proper treatment.

2. Corporate governance issues : It is the system which assist the health care

bodies lead, direct and control their operations in order to achieve the

organisational objectives (Van der Stede, 2015). The governance issues includes

the conflict of interest, serious clinical incidents, quality problems etc.

3. Accountability issues : It is the responsibility taken for one's action in the

organisation. This issues are Due to lack of accountability such as lack of trust in

the individual in the organisation.

TASK 2

a. Determine the break even capacity usage rate for ABC care Home Ltd

Break even units = Fixed cost /sales per unit- variable cost per unit

= £45,000 per month/ (1500- 9) = 30 units

Break even capacity usage rate = 30/60*100 = 50%

b. Calculate the targeted profit if the care home achieves 90% and 95% capacity

At 90% capacity BEP = 30 / 50 * 90

= 54 units

At 95% capacity BEP = 30 / 50 * 95

= 57 units

because the providers chooses to maximise its profitability rather than advising

the patients with proper treatment.

2. Corporate governance issues : It is the system which assist the health care

bodies lead, direct and control their operations in order to achieve the

organisational objectives (Van der Stede, 2015). The governance issues includes

the conflict of interest, serious clinical incidents, quality problems etc.

3. Accountability issues : It is the responsibility taken for one's action in the

organisation. This issues are Due to lack of accountability such as lack of trust in

the individual in the organisation.

TASK 2

a. Determine the break even capacity usage rate for ABC care Home Ltd

Break even units = Fixed cost /sales per unit- variable cost per unit

= £45,000 per month/ (1500- 9) = 30 units

Break even capacity usage rate = 30/60*100 = 50%

b. Calculate the targeted profit if the care home achieves 90% and 95% capacity

At 90% capacity BEP = 30 / 50 * 90

= 54 units

At 95% capacity BEP = 30 / 50 * 95

= 57 units

c. Break even analysis could be used in short-term and long-term

decision-making.

A break-even analysis is a financial tool which determines that at what level company,

will earn profit. It helps in computing the number of products or services every business

organisation or company has to sell so as to cover its production and other business

operation costs, specially fixed costs (Papapetrou, M. and et.al., 2018).

Break even point arises when total cost is equal to total revenue.

Short-term decision-making - The total cost of a product or service comprises of both

fixed and the variable cost. By using break even analysis, the effect of changing unit

selling price, unit variable cost or unit fixed cost can be determined which helps in

making decision for short term period. It helps in making changes in production and

other business operations.

Long-term decision-making - It helps when company wants to introduce or launch new

products into production line, or wants to start new service range thereby reducing

uncertainty about the failure after introduction or launch of a new project and service of

the company. When company wants to invest in heavy machinery or plants, it is useful

as it helps in assessing or estimating increase

in production volume in relation to new production

capacities.

decision-making.

A break-even analysis is a financial tool which determines that at what level company,

will earn profit. It helps in computing the number of products or services every business

organisation or company has to sell so as to cover its production and other business

operation costs, specially fixed costs (Papapetrou, M. and et.al., 2018).

Break even point arises when total cost is equal to total revenue.

Short-term decision-making - The total cost of a product or service comprises of both

fixed and the variable cost. By using break even analysis, the effect of changing unit

selling price, unit variable cost or unit fixed cost can be determined which helps in

making decision for short term period. It helps in making changes in production and

other business operations.

Long-term decision-making - It helps when company wants to introduce or launch new

products into production line, or wants to start new service range thereby reducing

uncertainty about the failure after introduction or launch of a new project and service of

the company. When company wants to invest in heavy machinery or plants, it is useful

as it helps in assessing or estimating increase

in production volume in relation to new production

capacities.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Task 3

a. Advantages and disadvantages of various budgeting approaches.

Budgeting is a practice of making future estimation or projection about future expenses. It

emphasises on preparation of budgets, business plans, business strategies for meeting future cash

and other resource requirements of business operations (Mauro, S.G. and et.al., 2017). The

various budgeting approaches are as follows:

1. Incremental budgeting - In this budgeting approach, budget is prepared by using as a basis

the actual performance or by considering budget of previous time period for making new budget

for the period with adding some incremental amount (de Campos, C.M.P. and Rodrigues, L.L.,

2016).

ADVANTAGE - It is simple & easy to prepare as current period financial results is taken as

basis for preparing incremental budget & can perform on continuity of funds in the future. It

reduces conflict among departments related to fund allocation.

DISADVANTAGE - It maintains same resource & fund allocation in present period to

department who previously required more funds, even though that department id not in need of

such funds. It doesn't emphasise on innovation and creativity as it rely on previous period

budget.

2. Zero based budgeting - A budgeting approach in which, budget is prepared by setting it to

zero or starting from scratch by re-evaluating business activities. It helps the organisation in

minimizing and mitigating unnecessary expenditure (Nnoli, U.F. and et.al., 2016).

ADVANTAGE - It ensures proper & efficient resource allocation thereby minimizing resource

wastage and identifying out dated business operations. It emphasises on detecting inflated budget

as well and helps management in ensuring effective fund expenditure to core business activities.

DISADVANTAGE - This approach is most time consuming process as heavy and necessary

expenditure requires proper discussion and knowledge for its successful implementation (Nnoli,

U.F. and et.al., 2016).

3. Activity based budgeting - It is a system in which business activities are taken into

consideration for recording, analysing and assessing the cost associated with such business

activities. After that expenditure forecasted for future is complied on the basis of expected level

of activity (Mahal, I. and Hossain, A., 2015).

a. Advantages and disadvantages of various budgeting approaches.

Budgeting is a practice of making future estimation or projection about future expenses. It

emphasises on preparation of budgets, business plans, business strategies for meeting future cash

and other resource requirements of business operations (Mauro, S.G. and et.al., 2017). The

various budgeting approaches are as follows:

1. Incremental budgeting - In this budgeting approach, budget is prepared by using as a basis

the actual performance or by considering budget of previous time period for making new budget

for the period with adding some incremental amount (de Campos, C.M.P. and Rodrigues, L.L.,

2016).

ADVANTAGE - It is simple & easy to prepare as current period financial results is taken as

basis for preparing incremental budget & can perform on continuity of funds in the future. It

reduces conflict among departments related to fund allocation.

DISADVANTAGE - It maintains same resource & fund allocation in present period to

department who previously required more funds, even though that department id not in need of

such funds. It doesn't emphasise on innovation and creativity as it rely on previous period

budget.

2. Zero based budgeting - A budgeting approach in which, budget is prepared by setting it to

zero or starting from scratch by re-evaluating business activities. It helps the organisation in

minimizing and mitigating unnecessary expenditure (Nnoli, U.F. and et.al., 2016).

ADVANTAGE - It ensures proper & efficient resource allocation thereby minimizing resource

wastage and identifying out dated business operations. It emphasises on detecting inflated budget

as well and helps management in ensuring effective fund expenditure to core business activities.

DISADVANTAGE - This approach is most time consuming process as heavy and necessary

expenditure requires proper discussion and knowledge for its successful implementation (Nnoli,

U.F. and et.al., 2016).

3. Activity based budgeting - It is a system in which business activities are taken into

consideration for recording, analysing and assessing the cost associated with such business

activities. After that expenditure forecasted for future is complied on the basis of expected level

of activity (Mahal, I. and Hossain, A., 2015).

ADVANTAGE - It helps the organisation in assessing cost associated with each business activity

& operations and the amount of funds required to be allocated to every business activity for

achieving organisation goals. It helps organisation in assessing the value added to each business

activity and determining cost of each unit of business operations as performed by the

organisation. It ascertains unnecessary activities of business and eliminates it thereby leading to

cost saving and maximizing profits.

DISADVANTAGE - It is traditional technique of budgeting which requires a lot of time and

information for successful attainment of business goals and objectives. It also requires more

resource allocation and insight maintenance from the management for development of such

budget (Mahal, I. and Hossain, A., 2015).

4. Rolling budgeting - It is a budgeting approach in which existing budget is incrementally

extended for upto the period of one year in the future. In this budget, a new budget period is

continually added on completion of existing budget period (Sarancha, S.Y. and et.al., 2016).

ADVANTAGE - It ensures reassessment of existing budget on regular basis thereby producing

new and update budget timely for future. It reduces uncertainty level associated with budgeting

by concentrating on short term period for more effective development of successful budgeting

approach.

DISADVANTAGE - It might demotivate employees of organisation when budgeting targets are

changing continuously. Rolling budgets are considered as costly ans timer consuming process as

it focuses on extension of existing budget for future (Sarancha, S.Y. and et.al., 2016).

b. Difficulties encountered when budgeting in public sector organisations.

While budgeting in public sector organisation, following difficulties are faced:

1. Limited Resources - Resource is one of the most important asset for every business

organisation useful in performing business operations. Proper, effective and timely allocation of

resources helps in gaining competitive advantage but at the same time scarcity or limited

resource availability leads to downfall in the profit & performance level of the organisation.

Time and money are special scarce resources which has to utilize in efficient and effective

manner. Thus, budgeting helps in planning, controlling & sustainable use of resources (Jauch, S.

and Watzka, S., 2016).

& operations and the amount of funds required to be allocated to every business activity for

achieving organisation goals. It helps organisation in assessing the value added to each business

activity and determining cost of each unit of business operations as performed by the

organisation. It ascertains unnecessary activities of business and eliminates it thereby leading to

cost saving and maximizing profits.

DISADVANTAGE - It is traditional technique of budgeting which requires a lot of time and

information for successful attainment of business goals and objectives. It also requires more

resource allocation and insight maintenance from the management for development of such

budget (Mahal, I. and Hossain, A., 2015).

4. Rolling budgeting - It is a budgeting approach in which existing budget is incrementally

extended for upto the period of one year in the future. In this budget, a new budget period is

continually added on completion of existing budget period (Sarancha, S.Y. and et.al., 2016).

ADVANTAGE - It ensures reassessment of existing budget on regular basis thereby producing

new and update budget timely for future. It reduces uncertainty level associated with budgeting

by concentrating on short term period for more effective development of successful budgeting

approach.

DISADVANTAGE - It might demotivate employees of organisation when budgeting targets are

changing continuously. Rolling budgets are considered as costly ans timer consuming process as

it focuses on extension of existing budget for future (Sarancha, S.Y. and et.al., 2016).

b. Difficulties encountered when budgeting in public sector organisations.

While budgeting in public sector organisation, following difficulties are faced:

1. Limited Resources - Resource is one of the most important asset for every business

organisation useful in performing business operations. Proper, effective and timely allocation of

resources helps in gaining competitive advantage but at the same time scarcity or limited

resource availability leads to downfall in the profit & performance level of the organisation.

Time and money are special scarce resources which has to utilize in efficient and effective

manner. Thus, budgeting helps in planning, controlling & sustainable use of resources (Jauch, S.

and Watzka, S., 2016).

2. Communication - It helps the organization in planning, formulating and developing strategies,

procedures and concepts. Proper & effective communication helps in conducting budget

meetings, discussions & implementation of budget plans. Communication is considered as a key

to success, it fails when other people unable to understand intention of performing such activity.

3. Changing Culture - Organisation culture comprises collective values, behaviours, assumptions

and principles which contributes to social, psychological and external environment of a business

organisations. Changing culture of organisation on regular basis made it difficult for successful

implementation of effective budgeting approach. For successful implementation of budget plans,

it is very necessary to have a uniform, stable & flexible working culture in the organisation

(Mauro, S.G. and et.al., 2017).

4. Infrastructure - Organizational infrastructure is defined as collection of the business strategies,

methods, concepts, procedures, actions and policies adopted in a business organisation

emphasizing on the said define rules, responsibilities and duties of its employees. A good

infrastructure fosters profit levels. When organisation invest in some projects, it should ensures

that such investment is growing and giving return at the rate higher than cost expenses of

business. Lack of adequate infrastructure facility leads to improper budget planning and its

successful implementation.

5. Visions - Every organisation should have a clear and definite vision and mission statements

for their business, to be achieved in near future. Vision should be made by keeping in mind the

goals and resource available. Unclear or undefined vision of organisation affects the budgeting

process to be made for meeting future goals. Budget programme, plans formulated should be in

line with the organisation vision (Mauro, S.G. and et.al., 2017).

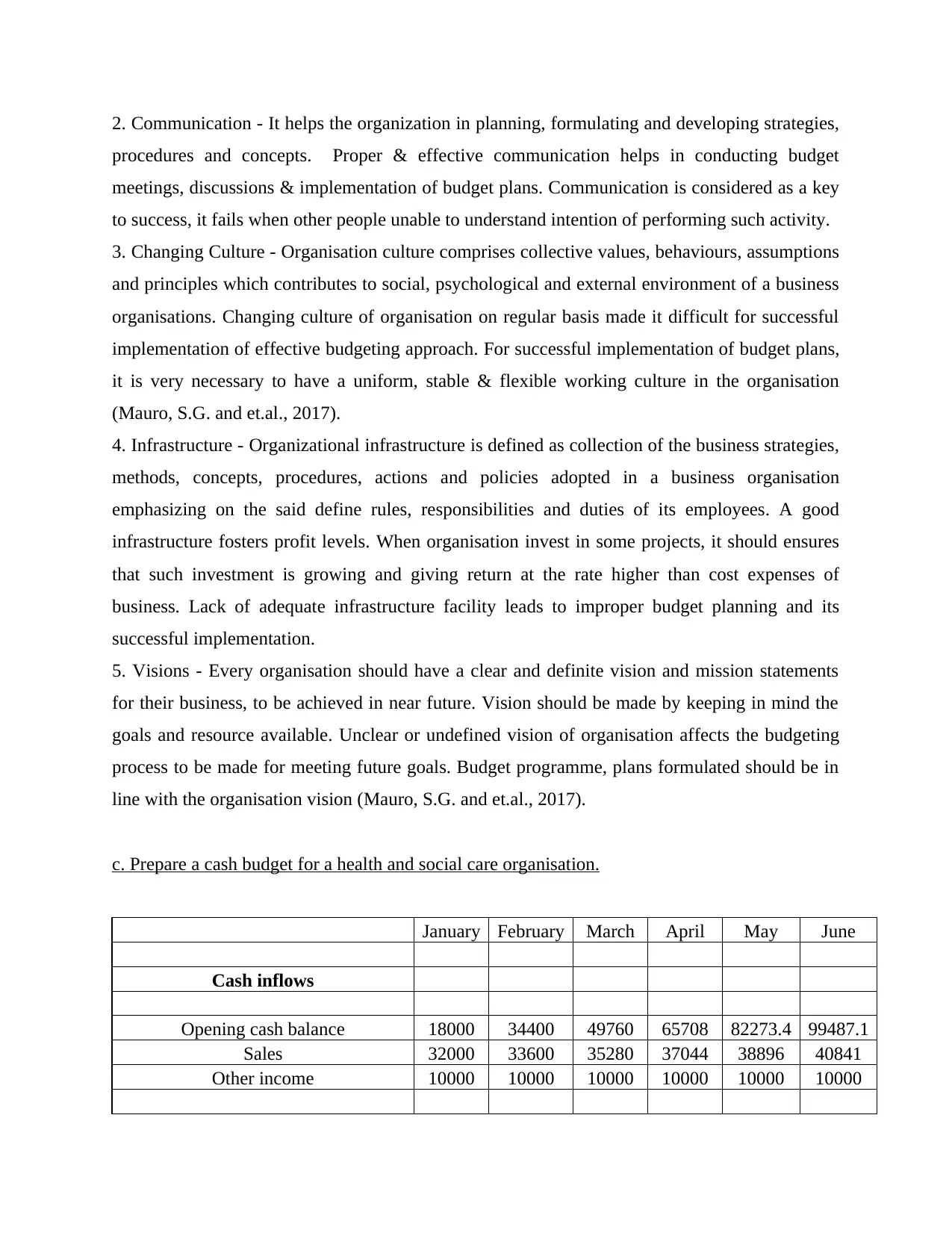

c. Prepare a cash budget for a health and social care organisation.

January February March April May June

Cash inflows

Opening cash balance 18000 34400 49760 65708 82273.4 99487.1

Sales 32000 33600 35280 37044 38896 40841

Other income 10000 10000 10000 10000 10000 10000

procedures and concepts. Proper & effective communication helps in conducting budget

meetings, discussions & implementation of budget plans. Communication is considered as a key

to success, it fails when other people unable to understand intention of performing such activity.

3. Changing Culture - Organisation culture comprises collective values, behaviours, assumptions

and principles which contributes to social, psychological and external environment of a business

organisations. Changing culture of organisation on regular basis made it difficult for successful

implementation of effective budgeting approach. For successful implementation of budget plans,

it is very necessary to have a uniform, stable & flexible working culture in the organisation

(Mauro, S.G. and et.al., 2017).

4. Infrastructure - Organizational infrastructure is defined as collection of the business strategies,

methods, concepts, procedures, actions and policies adopted in a business organisation

emphasizing on the said define rules, responsibilities and duties of its employees. A good

infrastructure fosters profit levels. When organisation invest in some projects, it should ensures

that such investment is growing and giving return at the rate higher than cost expenses of

business. Lack of adequate infrastructure facility leads to improper budget planning and its

successful implementation.

5. Visions - Every organisation should have a clear and definite vision and mission statements

for their business, to be achieved in near future. Vision should be made by keeping in mind the

goals and resource available. Unclear or undefined vision of organisation affects the budgeting

process to be made for meeting future goals. Budget programme, plans formulated should be in

line with the organisation vision (Mauro, S.G. and et.al., 2017).

c. Prepare a cash budget for a health and social care organisation.

January February March April May June

Cash inflows

Opening cash balance 18000 34400 49760 65708 82273.4 99487.1

Sales 32000 33600 35280 37044 38896 40841

Other income 10000 10000 10000 10000 10000 10000

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Total cash inflows 60000 78000 95040 112752 131170 150328

Cash outflows

Material 11200 11760 12348 12965 13614 14294

Labour 6400 6400 6400 6400 6400 6400

other expenses 8000 10080 10584 11113 11669 12252

Sum of cash outflows 25600 28240 29332 30479 31683 32947

Cash surplus / closing cash balance 34400 49760 65708 82273 99487 117381

d. The impact of financial constraints, costs and budgets on health and social care service

managers, their clients and other stakeholders.

Financial Constraints means shortage of funds or lack of money resources, as a result of which

unable to perform any task. Impact of Financial constraints on:

1. Managers - Due to lack of funds or money with the business organisations, managers have to

face a problem of limited availability of banking financial assistance required for acquiring new

and innovative health care instruments. Also, access to bank finance is limited upto an extent due

to little savings. Such organisation thus have a lower chance of survival and growth in the future.

2. Clients - As organisation is having a problem of financial constraints, it is unable to purchase

new, innovative and updated health care instruments and tools useful in field of health and social

care service for better treatments of patients. It affects the quality of treatment and health care

services rendered thereby impacting the health of patients (Atanelishvili, T. and et.al., 2017).

3. Stakeholders - As company is facing a situation of financial constraints, it will affect the

financial, economical and organisational performance of the organisation as well. When there is

no profit, its stakeholders will not be allotted any profit share which will affect their wealth and

investment proportions.

Cost means a monetary value for consumption of any resource, material, product or any service

used (Mauro, S.G. and et.al., 2017). Impact of Cost on:

Cash outflows

Material 11200 11760 12348 12965 13614 14294

Labour 6400 6400 6400 6400 6400 6400

other expenses 8000 10080 10584 11113 11669 12252

Sum of cash outflows 25600 28240 29332 30479 31683 32947

Cash surplus / closing cash balance 34400 49760 65708 82273 99487 117381

d. The impact of financial constraints, costs and budgets on health and social care service

managers, their clients and other stakeholders.

Financial Constraints means shortage of funds or lack of money resources, as a result of which

unable to perform any task. Impact of Financial constraints on:

1. Managers - Due to lack of funds or money with the business organisations, managers have to

face a problem of limited availability of banking financial assistance required for acquiring new

and innovative health care instruments. Also, access to bank finance is limited upto an extent due

to little savings. Such organisation thus have a lower chance of survival and growth in the future.

2. Clients - As organisation is having a problem of financial constraints, it is unable to purchase

new, innovative and updated health care instruments and tools useful in field of health and social

care service for better treatments of patients. It affects the quality of treatment and health care

services rendered thereby impacting the health of patients (Atanelishvili, T. and et.al., 2017).

3. Stakeholders - As company is facing a situation of financial constraints, it will affect the

financial, economical and organisational performance of the organisation as well. When there is

no profit, its stakeholders will not be allotted any profit share which will affect their wealth and

investment proportions.

Cost means a monetary value for consumption of any resource, material, product or any service

used (Mauro, S.G. and et.al., 2017). Impact of Cost on:

1. Managers - As the cost of carrying on any health care and social services & its related

business operations increases, the level of profit will either decrease or remain constant without

going up. This will lead to decline in the profit margins of managers.

2. Clients - With increase in cost of the health care products and services, many clients will not

be able to consume or afford it for their treatments. This will affect the health of patients as they

are unable to seek such costly health care services on time and it will lead to increase in number

of ill patients.

3. Stakeholders - With high cost, organisation will only earn from patients who can afford such

costly treatment. This will give low return and profitability of company will also decrease as a

result of which stakeholders profit share will get affected (Mauro, S.G. and et.al., 2017).

Budget means preparing an outline for meeting future business operation expenses to eliminate

or mitigate any financial risk or other business related risk associated with the organisation. It

also compares actual results with estimated budget prepared, to ascertain the actual variances, if

any thereby maximizing the profitability (Heupel, T. and Schmitz, S., 2015).

1. Managers - It helps manager on emphasizing how much number of health care instruments,

units are required to be purchased or acquired for a definite period of time for effective treatment

of patients. It also helps in considering expenses related to health care services to be render in

future. Budget prepare helps manager in creating and outlining a clear and definite vision for

betterment of organisation success and for effective working of team towards attainment of

organisational as well as individual goals (Mauro, S.G. and et.al., 2017).

2. Clients - Budget brings plans, strategies for meeting future event expenses. It ensures proper

and effective financial as well as non financial planning for organisation to mitigate and

eliminate the risk associated with business. As budget confines the amount to be utilised, it limits

the company from purchasing good and updated health care instruments which affects patients

treatments (Heupel, T. and Schmitz, S., 2015).

3. Stakeholders - When company is having a projected budget amount, it will growth within that

respective budget amount. The quality of performance will not improve & leads to low profit

margins. Because of this low profits margin, company will not be able to fulfill its stakeholders

needs of profit distribution.

business operations increases, the level of profit will either decrease or remain constant without

going up. This will lead to decline in the profit margins of managers.

2. Clients - With increase in cost of the health care products and services, many clients will not

be able to consume or afford it for their treatments. This will affect the health of patients as they

are unable to seek such costly health care services on time and it will lead to increase in number

of ill patients.

3. Stakeholders - With high cost, organisation will only earn from patients who can afford such

costly treatment. This will give low return and profitability of company will also decrease as a

result of which stakeholders profit share will get affected (Mauro, S.G. and et.al., 2017).

Budget means preparing an outline for meeting future business operation expenses to eliminate

or mitigate any financial risk or other business related risk associated with the organisation. It

also compares actual results with estimated budget prepared, to ascertain the actual variances, if

any thereby maximizing the profitability (Heupel, T. and Schmitz, S., 2015).

1. Managers - It helps manager on emphasizing how much number of health care instruments,

units are required to be purchased or acquired for a definite period of time for effective treatment

of patients. It also helps in considering expenses related to health care services to be render in

future. Budget prepare helps manager in creating and outlining a clear and definite vision for

betterment of organisation success and for effective working of team towards attainment of

organisational as well as individual goals (Mauro, S.G. and et.al., 2017).

2. Clients - Budget brings plans, strategies for meeting future event expenses. It ensures proper

and effective financial as well as non financial planning for organisation to mitigate and

eliminate the risk associated with business. As budget confines the amount to be utilised, it limits

the company from purchasing good and updated health care instruments which affects patients

treatments (Heupel, T. and Schmitz, S., 2015).

3. Stakeholders - When company is having a projected budget amount, it will growth within that

respective budget amount. The quality of performance will not improve & leads to low profit

margins. Because of this low profits margin, company will not be able to fulfill its stakeholders

needs of profit distribution.

CONCLUSION

From the above report its can be concluded that, Financial control is a system of tracing

the resources directed for carrying on the organisation business operations. It keeps a check on

accuracy of report to eliminate fraud, error so as to protect physical & intangible resources of the

organization. Furthermore, report has cover challenges & recent developments of NHS. It has

also explained the various funding options available with health and social care service

organisation. Detailed explanation about the agency theory, corporate

governance and accountability issues faced by health and social care organisation has been

given. At last it has explain the concept of budgeting that, Budgeting is a process of preparing

budget, business plans, business strategies for meeting future cash and other resource

requirements of business operations. There are number of budgeting approaches which a

organisation can use for improving its performance quality and profit margins.

From the above report its can be concluded that, Financial control is a system of tracing

the resources directed for carrying on the organisation business operations. It keeps a check on

accuracy of report to eliminate fraud, error so as to protect physical & intangible resources of the

organization. Furthermore, report has cover challenges & recent developments of NHS. It has

also explained the various funding options available with health and social care service

organisation. Detailed explanation about the agency theory, corporate

governance and accountability issues faced by health and social care organisation has been

given. At last it has explain the concept of budgeting that, Budgeting is a process of preparing

budget, business plans, business strategies for meeting future cash and other resource

requirements of business operations. There are number of budgeting approaches which a

organisation can use for improving its performance quality and profit margins.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Atanelishvili, T. and et.al., 2017. About state Financial control. Ecoforum Journal. 6(1).

Bodiako, A.V. and et. al., 2016. The goal setting of internal control in the system of project

financing. International journal of economics and financial issues. 6(4). pp.1945-1955.

Burns, R. and Walker, J., 2015. Capital budgeting surveys: the future is now.

Burtonshaw-Gunn, S. A., 2017. Risk and financial management in construction. Routledge.

de Campos, C.M.P. and Rodrigues, L.L., 2016. Budgeting Techniques: Incremental Based,

Performance Based, Activity Based, Zero Based, and Priority Based. Global Encyclopedia of

Public Administration, Public Policy, and Governance, pp.1-10.

Di Francesco, M. and Alford, J., 2016. Balancing control and flexibility in public budgeting: A

new role for rule variability. Springer.

Heupel, T. and Schmitz, S., 2015. Beyond Budgeting-a high-hanging fruit The impact of

managers’ mindset on the advantages of Beyond Budgeting. Procedia Economics and

Finance. 26.pp.729-736.

Jauch, S. and Watzka, S., 2016. Financial development and income inequality: a panel data

approach. Empirical Economics. 51(1). pp.291-314.

Books and Journals

Atanelishvili, T. and et.al., 2017. About state Financial control. Ecoforum Journal. 6(1).

Bodiako, A.V. and et. al., 2016. The goal setting of internal control in the system of project

financing. International journal of economics and financial issues. 6(4). pp.1945-1955.

Burns, R. and Walker, J., 2015. Capital budgeting surveys: the future is now.

Burtonshaw-Gunn, S. A., 2017. Risk and financial management in construction. Routledge.

de Campos, C.M.P. and Rodrigues, L.L., 2016. Budgeting Techniques: Incremental Based,

Performance Based, Activity Based, Zero Based, and Priority Based. Global Encyclopedia of

Public Administration, Public Policy, and Governance, pp.1-10.

Di Francesco, M. and Alford, J., 2016. Balancing control and flexibility in public budgeting: A

new role for rule variability. Springer.

Heupel, T. and Schmitz, S., 2015. Beyond Budgeting-a high-hanging fruit The impact of

managers’ mindset on the advantages of Beyond Budgeting. Procedia Economics and

Finance. 26.pp.729-736.

Jauch, S. and Watzka, S., 2016. Financial development and income inequality: a panel data

approach. Empirical Economics. 51(1). pp.291-314.

Mahal, I. and Hossain, A., 2015. Activity-Based Costing (ABC)–An Effective Tool for Better

Management. Research Journal of Finance and Accounting. 6(4). pp.66-74.

Mauro, S.G. and et.al., 2017. Insights into performance-based budgeting in the public sector: a

literature review and a research agenda. Public Management Review. 19(7). pp.911-931.

Nnoli, U.F. and et.al., 2016. Zero-Based Budgeting: Pathway to Sustainable Budget

Implementation in Nigeria. Business Trends. 6(3). pp.28-35.

Oliver, L. and Nin, E., 2019. 10 Steps to Successful Budgeting. American Society for Training

and Development.

Oraka, A.O. and et.al., 2016. Zero-based budgeting: Pathway to sustainable budget

implementation in Nigeria.

Osadchy, E. A. and Akhmetshin, E. M., 2015. Development of the financial control system in

the company in crisis. Mediterranean Journal of Social Sciences. 6(5). p.390.

Papapetrou, M. and et.al., 2018. Evaluating the factors affecting the break-even cost of on-site

PV generation at industrial units.

Rogulenko, T. and et.al., 2016. Budgeting-Based Organization of Internal Control. International

Journal of Environmental and Science Education. 11(11). pp.4104-4117.

Sarancha, S.Y. and et.al., 2016. Technologies Budgeting in Metallurgical Branch on the

Example of Production of Section Rolling Products. Russian Internet Journal of Industrial

Engineering. 3(2). pp.65-67.

Van der Stede, W. A., 2015. Budgeting and management control. Wiley Encyclopedia of

Management. pp.1-7.

Wildavsky, A., 2017. Budgeting and governing. Routledge.

Online

Activity based Budgeting. 2017. [Online]. Available through: <http://blog.dawgen.com/activity-

based-budgeting-in-organizations/>.

Financial Control. [Online]. Available through: <http://ndi-innovation.eu/routes/route.php?

node_id=308#.XJDBmnV948o>.

Fontinelle, A., 2017. Budgeting basics. [Online]. Available through:

<https://www.investopedia.com/university/budgeting/>.

Management. Research Journal of Finance and Accounting. 6(4). pp.66-74.

Mauro, S.G. and et.al., 2017. Insights into performance-based budgeting in the public sector: a

literature review and a research agenda. Public Management Review. 19(7). pp.911-931.

Nnoli, U.F. and et.al., 2016. Zero-Based Budgeting: Pathway to Sustainable Budget

Implementation in Nigeria. Business Trends. 6(3). pp.28-35.

Oliver, L. and Nin, E., 2019. 10 Steps to Successful Budgeting. American Society for Training

and Development.

Oraka, A.O. and et.al., 2016. Zero-based budgeting: Pathway to sustainable budget

implementation in Nigeria.

Osadchy, E. A. and Akhmetshin, E. M., 2015. Development of the financial control system in

the company in crisis. Mediterranean Journal of Social Sciences. 6(5). p.390.

Papapetrou, M. and et.al., 2018. Evaluating the factors affecting the break-even cost of on-site

PV generation at industrial units.

Rogulenko, T. and et.al., 2016. Budgeting-Based Organization of Internal Control. International

Journal of Environmental and Science Education. 11(11). pp.4104-4117.

Sarancha, S.Y. and et.al., 2016. Technologies Budgeting in Metallurgical Branch on the

Example of Production of Section Rolling Products. Russian Internet Journal of Industrial

Engineering. 3(2). pp.65-67.

Van der Stede, W. A., 2015. Budgeting and management control. Wiley Encyclopedia of

Management. pp.1-7.

Wildavsky, A., 2017. Budgeting and governing. Routledge.

Online

Activity based Budgeting. 2017. [Online]. Available through: <http://blog.dawgen.com/activity-

based-budgeting-in-organizations/>.

Financial Control. [Online]. Available through: <http://ndi-innovation.eu/routes/route.php?

node_id=308#.XJDBmnV948o>.

Fontinelle, A., 2017. Budgeting basics. [Online]. Available through:

<https://www.investopedia.com/university/budgeting/>.

Incremental Budgeting. 2017. [Online]. Available through:

<http://managedcommunityanalytics.com/the-downsides-of-hoa-budgeting/>.

Rolling Budgeting. 2018. [Online]. Available through: <https://finmodelslab.com/rolling-

budgeting/>.

Zero based Budgeting. 2018. [Online]. Available through:

<https://www.wallstreetmojo.com/zero-based-budgeting/>.

<http://managedcommunityanalytics.com/the-downsides-of-hoa-budgeting/>.

Rolling Budgeting. 2018. [Online]. Available through: <https://finmodelslab.com/rolling-

budgeting/>.

Zero based Budgeting. 2018. [Online]. Available through:

<https://www.wallstreetmojo.com/zero-based-budgeting/>.

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.