Financial Control and Budgeting - Assignment

VerifiedAdded on 2020/12/30

|14

|4852

|389

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Financial Control and

Budgeting

Budgeting

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

a) Challenges faced by NHS and the recent developments....................................................1

b) The Usefulness of alternative funding options...................................................................2

c) Identification of the key stakeholders within the social care sector and ways of

communication.......................................................................................................................3

TASK 2............................................................................................................................................4

a) Break Even capacity usage rate of ABC care home ltd.....................................................4

b) Calculation of the Targeted profit at 90% and 95% of the total usage capacity................5

c) Uses of Break Even analysis in short term and long term decision making......................5

TASK 3............................................................................................................................................6

A. Advantages and disadvantages of different budgeting approaches...................................6

B. Discussion of particular difficulties encountered when budgeting in public sector

organisation............................................................................................................................7

C. Preparation of cash budget for a health and social care organisation................................8

D. Awareness on the impact of financial constraints, costs and budget on health and social

care service managers, their clients and stakeholders............................................................9

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

a) Challenges faced by NHS and the recent developments....................................................1

b) The Usefulness of alternative funding options...................................................................2

c) Identification of the key stakeholders within the social care sector and ways of

communication.......................................................................................................................3

TASK 2............................................................................................................................................4

a) Break Even capacity usage rate of ABC care home ltd.....................................................4

b) Calculation of the Targeted profit at 90% and 95% of the total usage capacity................5

c) Uses of Break Even analysis in short term and long term decision making......................5

TASK 3............................................................................................................................................6

A. Advantages and disadvantages of different budgeting approaches...................................6

B. Discussion of particular difficulties encountered when budgeting in public sector

organisation............................................................................................................................7

C. Preparation of cash budget for a health and social care organisation................................8

D. Awareness on the impact of financial constraints, costs and budget on health and social

care service managers, their clients and stakeholders............................................................9

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION

Financial controlling and budgeting plays an important role in the preparation of the

financial accounts (Lins, Volpin and Wagner, 2013.). It also helps the company to measure its

efficiency and strengths and see the inflows and outflows from the company. Budgeting gives

the earlier report which helps the managers to take necessary decisions to overcome those

problems due to which it was not able to achieve its target. Financial controls help the managers

to control the expenses to maximize their profit. These reports help the mangers to make

meaning full decisions for the company. Financial control gives the total control of the income

and expenses of the company. Budget reports helps the mangers to see the growth and take make

necessary decisions for the continuous growth of the company.

To understand the importance of financial control and budgeting this report contains a case

study on UK National Health Service which states the importance of financial control and

budgeting in decision making. This case study highlights the certain questions which help us to

understand the problems faced by the National Health Service on their 70th anniversary and how

they resolved it with the help of financial controlling and budgeting.

TASK 1

a) Challenges faced by NHS and the recent developments.

NHS is UK based health service which helps the people around the country to get the

medical treatment at reasonably low prices (Piercy, 2014). The problem faced by the National

Health Services is to properly manage the funds raised by the ministers to settle the additional

20bn per year for the development of the National Health Service by the year 2023. The biggest

problem is to properly utilize this huge amount of fund to the right place in the development of

the health care given to the people using the UK National Health Service. Financial control helps

the mangers of the National Health Service to find the proper way to utilize these funds. In the

past 20 years the health numbers are fallen according the data given in the case study 10385 less

people died due to the heart attack, the number of people dying from the strokes haven fallen by

8390 persons a year and the people dying from cancer has fallen by 634 people. The overall

productivity growth in the treatment of people dying from certain disease is averaged at 1.4% a

year recorded during the last five years.

1

Financial controlling and budgeting plays an important role in the preparation of the

financial accounts (Lins, Volpin and Wagner, 2013.). It also helps the company to measure its

efficiency and strengths and see the inflows and outflows from the company. Budgeting gives

the earlier report which helps the managers to take necessary decisions to overcome those

problems due to which it was not able to achieve its target. Financial controls help the managers

to control the expenses to maximize their profit. These reports help the mangers to make

meaning full decisions for the company. Financial control gives the total control of the income

and expenses of the company. Budget reports helps the mangers to see the growth and take make

necessary decisions for the continuous growth of the company.

To understand the importance of financial control and budgeting this report contains a case

study on UK National Health Service which states the importance of financial control and

budgeting in decision making. This case study highlights the certain questions which help us to

understand the problems faced by the National Health Service on their 70th anniversary and how

they resolved it with the help of financial controlling and budgeting.

TASK 1

a) Challenges faced by NHS and the recent developments.

NHS is UK based health service which helps the people around the country to get the

medical treatment at reasonably low prices (Piercy, 2014). The problem faced by the National

Health Services is to properly manage the funds raised by the ministers to settle the additional

20bn per year for the development of the National Health Service by the year 2023. The biggest

problem is to properly utilize this huge amount of fund to the right place in the development of

the health care given to the people using the UK National Health Service. Financial control helps

the mangers of the National Health Service to find the proper way to utilize these funds. In the

past 20 years the health numbers are fallen according the data given in the case study 10385 less

people died due to the heart attack, the number of people dying from the strokes haven fallen by

8390 persons a year and the people dying from cancer has fallen by 634 people. The overall

productivity growth in the treatment of people dying from certain disease is averaged at 1.4% a

year recorded during the last five years.

1

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

The rise in the chronic conditions of the people is seen, the older fragile people are also

increasing, and the demand for the National Health Services is increasing at a very fast

speed. In order to meet the demand, the National Health Service has to properly control their

financial positions (Bodiako, and e.t.all. 2016.). The financial control gives the framework to

the NHS to work on the control of the expenses incurred by them in order to treat these

people with their multiple chronic conditions. The recent changes in the trends and the

development in the methods of the treatment. The National Health Service is trying to adopt

the latest technology for the treatment of the persons from these chronic diseases. Some latest

technologies in the field of medical are the artificial intelligence, genomic and personalized

medicine that will replace the older methods of the treatment and start the new revolutionize

care in the field of medical science. Budgeting helps the mangers to identify the problems

which were faced by the NHS to improve the quality of care, the efficiency and the cost of

the care. The data provided by the previous budgets helps the NHS to identify the problems

and run the test to correct those problems. This budget helps the National Health Service to

design new test and run them to improve the efficiency and safety for both the staff and the

patients getting their treatments.

b) The Usefulness of alternative funding options

The usefulness of the alternative funding options provide for the National Health Service is

the Private Finance Initiates, Resources, Financial Aspects of the Agency Partnership. Some of

these alternatives are listed as below:

Private Finance Initiatives (PFI): In the Private Finance Initiative the Private sectors helps the

public sector projects by providing the financial support and helping them to control the cost of

the production (Dorogovs, Solovjova and Romanovs, 2013.). It helps the government to reduce the

burden from the taxpayers of the immediate coming up capital for these projects. These types of

private funding are used in the countries like United Kingdom and Australia. Under these

programs the up-front cost for these projects are taken care by the private investors who invest

their money in the government projects. It was started in the year 1992 when United Kingdom

first started to raise the capital for government projects from the private financial institutions.

Later till the year 1997 it became more popular to raise the capital from the private investors for

such kind of government health care projects.

2

increasing, and the demand for the National Health Services is increasing at a very fast

speed. In order to meet the demand, the National Health Service has to properly control their

financial positions (Bodiako, and e.t.all. 2016.). The financial control gives the framework to

the NHS to work on the control of the expenses incurred by them in order to treat these

people with their multiple chronic conditions. The recent changes in the trends and the

development in the methods of the treatment. The National Health Service is trying to adopt

the latest technology for the treatment of the persons from these chronic diseases. Some latest

technologies in the field of medical are the artificial intelligence, genomic and personalized

medicine that will replace the older methods of the treatment and start the new revolutionize

care in the field of medical science. Budgeting helps the mangers to identify the problems

which were faced by the NHS to improve the quality of care, the efficiency and the cost of

the care. The data provided by the previous budgets helps the NHS to identify the problems

and run the test to correct those problems. This budget helps the National Health Service to

design new test and run them to improve the efficiency and safety for both the staff and the

patients getting their treatments.

b) The Usefulness of alternative funding options

The usefulness of the alternative funding options provide for the National Health Service is

the Private Finance Initiates, Resources, Financial Aspects of the Agency Partnership. Some of

these alternatives are listed as below:

Private Finance Initiatives (PFI): In the Private Finance Initiative the Private sectors helps the

public sector projects by providing the financial support and helping them to control the cost of

the production (Dorogovs, Solovjova and Romanovs, 2013.). It helps the government to reduce the

burden from the taxpayers of the immediate coming up capital for these projects. These types of

private funding are used in the countries like United Kingdom and Australia. Under these

programs the up-front cost for these projects are taken care by the private investors who invest

their money in the government projects. It was started in the year 1992 when United Kingdom

first started to raise the capital for government projects from the private financial institutions.

Later till the year 1997 it became more popular to raise the capital from the private investors for

such kind of government health care projects.

2

Agency Partnership: Agency Partnership is the partnership where the decision making power is

usually held by the one party and the other party just helps in the process of raising funds,

managing the resources, for the other party in order to work more effectively and efficiently

(Ferry and Eckersley, 2012). This type of financial helps option is also available with the

government to formulate the agency with the private sectors to take care for the funds, managing

the resources, and helping the government projects to achieve their sole purpose of helping the

people requiring the medical attention. In the above case study, it was mentioned that the UK

National Health Service has the option to raise the funds from getting into the agency with the

private sectors.

Resources: This is type of privately raising the fund for the governmental projects from the

different available resources from the private sector and also the reserves and surplus created by

the governmental project (Simmons, 2012). National Health Service uses this type of private

funding to meet their expectations to take care of the maximum patients to help them recover

from their multiple chronical health conditions. These types of private funding give the

advantage to the government to solely focus on the health care of the people seeking their

medical services.

These are some of the private financial methods adopted by the National Health Services to

raise the capital to reduce the number of people dying from these chronic medical conditions

such as the Hearth attack, cardiac arrest and many more. In the above given case study it is

clearly stated that the National Health Services are funded with the central taxation from the last

30 years but now the NHS wants to take some steps in the expansion of their projects and trying

to adopt the new technologies in the world of medical science.

c) Identification of the key stakeholders within the social care sector and ways of

communication.

Stakeholders: Stakeholders are the individual or the group of individuals who have the

direct interest in the earning of the organizations and sometimes takes the necessary

decisions in the benefit of the organization (Kaye III, Frances, Kaye, 2016). Stakeholders can

be the employees of the company, investors who have invested in the organizations, in some

cases government can be the stakeholders in the company which take the benefits from the

earning of the company.

3

usually held by the one party and the other party just helps in the process of raising funds,

managing the resources, for the other party in order to work more effectively and efficiently

(Ferry and Eckersley, 2012). This type of financial helps option is also available with the

government to formulate the agency with the private sectors to take care for the funds, managing

the resources, and helping the government projects to achieve their sole purpose of helping the

people requiring the medical attention. In the above case study, it was mentioned that the UK

National Health Service has the option to raise the funds from getting into the agency with the

private sectors.

Resources: This is type of privately raising the fund for the governmental projects from the

different available resources from the private sector and also the reserves and surplus created by

the governmental project (Simmons, 2012). National Health Service uses this type of private

funding to meet their expectations to take care of the maximum patients to help them recover

from their multiple chronical health conditions. These types of private funding give the

advantage to the government to solely focus on the health care of the people seeking their

medical services.

These are some of the private financial methods adopted by the National Health Services to

raise the capital to reduce the number of people dying from these chronic medical conditions

such as the Hearth attack, cardiac arrest and many more. In the above given case study it is

clearly stated that the National Health Services are funded with the central taxation from the last

30 years but now the NHS wants to take some steps in the expansion of their projects and trying

to adopt the new technologies in the world of medical science.

c) Identification of the key stakeholders within the social care sector and ways of

communication.

Stakeholders: Stakeholders are the individual or the group of individuals who have the

direct interest in the earning of the organizations and sometimes takes the necessary

decisions in the benefit of the organization (Kaye III, Frances, Kaye, 2016). Stakeholders can

be the employees of the company, investors who have invested in the organizations, in some

cases government can be the stakeholders in the company which take the benefits from the

earning of the company.

3

Stake holders in the social care sectors can be the private sectors investors who has

invested the money in the governmental projects, employees and the staff working in the national

Health Services, and the patients who are there for their treatments. It can be communicated to

the key stake holders in their financial reports and annual general meetings and also can be

published in the office journals. The data which the key stakeholders requires is the annual report

to see the growth of the company in which they have invested a huge amount of capital in the

development of the national Health Services. The budgets reports give the stakeholders the map

for the investments that whether their invested money is utilized in the proper manner or not.

These data are also required by the staff to measure their efficiency in context of the previous

year. These budgets help the mangers to the gives the proper actual position of the company.

The agency theory states that the government raises their fund through forming the

agency with the private sectors in which the controlling is not given to the agency only the part

for the raising of fund is done through the private agency. Corporate governance plays an

important part on the decision making process. It helps the mangers to properly organize their

staff for the betterment of the company. It also helps the organization to make the meaning full

decisions to help the company to grow. Corporate governance helps the organization to properly

govern their resources and the proper utilization of their resources and helping them to use it

efficiently and effectively.

TASK 2

a) Break Even capacity usage rate of ABC care home ltd.

Break Even Capacity: Break even capacity is the capacity at which the organisation

works at the level where it does not earn any profit from the revenues generated from the

services it provides to its customers and patients (Scherer and Wimmer, 2012). Break even points

shows the organisations capacity to meet their expenses. Breakeven is achieved when the

organisation is only able to recover it fixed cost and does not have any profit. From the above

given data it is established that the brake even capacity of the ABC care homes ltd is 50.6%

which shows that the care home is working to their potential to earn the maximum profit.

Total Fixed Cost 45000x12 540000

Contribution

Revenue 372000

4

invested the money in the governmental projects, employees and the staff working in the national

Health Services, and the patients who are there for their treatments. It can be communicated to

the key stake holders in their financial reports and annual general meetings and also can be

published in the office journals. The data which the key stakeholders requires is the annual report

to see the growth of the company in which they have invested a huge amount of capital in the

development of the national Health Services. The budgets reports give the stakeholders the map

for the investments that whether their invested money is utilized in the proper manner or not.

These data are also required by the staff to measure their efficiency in context of the previous

year. These budgets help the mangers to the gives the proper actual position of the company.

The agency theory states that the government raises their fund through forming the

agency with the private sectors in which the controlling is not given to the agency only the part

for the raising of fund is done through the private agency. Corporate governance plays an

important part on the decision making process. It helps the mangers to properly organize their

staff for the betterment of the company. It also helps the organization to make the meaning full

decisions to help the company to grow. Corporate governance helps the organization to properly

govern their resources and the proper utilization of their resources and helping them to use it

efficiently and effectively.

TASK 2

a) Break Even capacity usage rate of ABC care home ltd.

Break Even Capacity: Break even capacity is the capacity at which the organisation

works at the level where it does not earn any profit from the revenues generated from the

services it provides to its customers and patients (Scherer and Wimmer, 2012). Break even points

shows the organisations capacity to meet their expenses. Breakeven is achieved when the

organisation is only able to recover it fixed cost and does not have any profit. From the above

given data it is established that the brake even capacity of the ABC care homes ltd is 50.6%

which shows that the care home is working to their potential to earn the maximum profit.

Total Fixed Cost 45000x12 540000

Contribution

Revenue 372000

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Total Cost

[(150+180+120)x12x60x90%]

356400

61560x 90% 11400

Break Even Point 540000/11400 47.36

b) Calculation of the Targeted profit at 90% and 95% of the total usage capacity

Targeted profit: Targeted profit is the profit which the company targets to earn in an

accounting year with the projections of the costs related to the production of the product. It helps

the managers to make the budgets according to the requirements of the company.

Total Fixed Cost 45000x12 540000

Contribution

Revenue

Total Cost

[(150+180+120)x12x60x90%]

372000

356400

615600x 95%/90%

Profit 109800

c) Uses of Break Even analysis in short term and long term decision making.

Break even analysis is a business tool used by production management to decide if a

company should or should not start production of products and selling it. Its helps in the

determination of that volume of sale at which costs and revenue are in equilibrium. The

equilibrium point is often referred to as the breakeven point. It is useful in setting up flexible

budgets which indicates costs and profits at various levels of activity. This analysis also assists in

formulating price policies by showing the effect of different price structures on cost and profits.

It helps to execute the idea of profit planning. We arrive at the sales level to be attempted for a

desired profit by the knowledge of relationship existing between cost volume and profit.

Analysis of cost-volume profit relationship also helps the management to decide whether to shut

down or to run the organization at a loss.

5

[(150+180+120)x12x60x90%]

356400

61560x 90% 11400

Break Even Point 540000/11400 47.36

b) Calculation of the Targeted profit at 90% and 95% of the total usage capacity

Targeted profit: Targeted profit is the profit which the company targets to earn in an

accounting year with the projections of the costs related to the production of the product. It helps

the managers to make the budgets according to the requirements of the company.

Total Fixed Cost 45000x12 540000

Contribution

Revenue

Total Cost

[(150+180+120)x12x60x90%]

372000

356400

615600x 95%/90%

Profit 109800

c) Uses of Break Even analysis in short term and long term decision making.

Break even analysis is a business tool used by production management to decide if a

company should or should not start production of products and selling it. Its helps in the

determination of that volume of sale at which costs and revenue are in equilibrium. The

equilibrium point is often referred to as the breakeven point. It is useful in setting up flexible

budgets which indicates costs and profits at various levels of activity. This analysis also assists in

formulating price policies by showing the effect of different price structures on cost and profits.

It helps to execute the idea of profit planning. We arrive at the sales level to be attempted for a

desired profit by the knowledge of relationship existing between cost volume and profit.

Analysis of cost-volume profit relationship also helps the management to decide whether to shut

down or to run the organization at a loss.

5

TASK 3

A. Advantages and disadvantages of different budgeting approaches

Budgeting is the process of planning for future and formulating budgets for future to spend

finance in proper manner. The whole plan is known as budget and the procedure of this

formulation is known as budgeting. On the other hand, it can be defined as the balancing tool

which is used to balance incomes and expenses of the organisation. It is vital for business entities

to prepare budgets using different techniques and make future projections that are based upon

past data. There are various types of budgeting techniques that are used by enterprises in order to

formulate their budget in appropriate manner (Guess and Ma, 2015). It is very important for all

of the to follow a specific technique so that it can help to manage all the monetary resources

effectively. Some of the techniques are discussed below:

Incremental budgeting: It is process which is used to form incremental budget. Such type

of budget is formulated by using previous period’s data or considering current position and

performance as a base of amount for new budget. It is a part of management accounting which is

also used to make small changes in the budgets of the companies. No formula is required to

conduct this budgeting because only additional amount is added to the previous year’s budget.

Some of the advantages and disadvantages of it are as follows:

Advantages: It is an easy and effective methods which can be used by organisations whether

they are small or large. Calculation process is very simple in this budgeting that may help the

managers to record accurate aunt in the books of accounting. In most of the companies it is used

to reduce competition and build the value of equality among functional departments (Incremental

budgeting, 2019).

Disadvantages: In this method there is a lack of innovation and no cost reduction for the

top-level executives. It encourages large spending in order to attain favourable or positive

variances.

Zero based budgeting: It is mainly used in management accounting as a planning tool in which

budget is formulated from the scratch with a zero value. In this method managers make sure that

all the expenses are justified with the related period. Need for the future period is the base for

this type of budgeting technique (Lauth, 2014). Advantages and disadvantages of this approach

are as follows:

6

A. Advantages and disadvantages of different budgeting approaches

Budgeting is the process of planning for future and formulating budgets for future to spend

finance in proper manner. The whole plan is known as budget and the procedure of this

formulation is known as budgeting. On the other hand, it can be defined as the balancing tool

which is used to balance incomes and expenses of the organisation. It is vital for business entities

to prepare budgets using different techniques and make future projections that are based upon

past data. There are various types of budgeting techniques that are used by enterprises in order to

formulate their budget in appropriate manner (Guess and Ma, 2015). It is very important for all

of the to follow a specific technique so that it can help to manage all the monetary resources

effectively. Some of the techniques are discussed below:

Incremental budgeting: It is process which is used to form incremental budget. Such type

of budget is formulated by using previous period’s data or considering current position and

performance as a base of amount for new budget. It is a part of management accounting which is

also used to make small changes in the budgets of the companies. No formula is required to

conduct this budgeting because only additional amount is added to the previous year’s budget.

Some of the advantages and disadvantages of it are as follows:

Advantages: It is an easy and effective methods which can be used by organisations whether

they are small or large. Calculation process is very simple in this budgeting that may help the

managers to record accurate aunt in the books of accounting. In most of the companies it is used

to reduce competition and build the value of equality among functional departments (Incremental

budgeting, 2019).

Disadvantages: In this method there is a lack of innovation and no cost reduction for the

top-level executives. It encourages large spending in order to attain favourable or positive

variances.

Zero based budgeting: It is mainly used in management accounting as a planning tool in which

budget is formulated from the scratch with a zero value. In this method managers make sure that

all the expenses are justified with the related period. Need for the future period is the base for

this type of budgeting technique (Lauth, 2014). Advantages and disadvantages of this approach

are as follows:

6

Advantages: Zero based budgeting guides the managers to allocate budgets to the

departments of the organisation according to their requirements. As every expense is

justified in this approach so it can help managers to overcome the weaknesses of

incremental budgeting.

Disadvantages: Large number of employees are required to form budgets under this

method. It required higher time to form the budgets as it a time-consuming process.

Activity based budgeting: Activity based costing is used to form budgets under this

budgeting technique. Under this method budget or resources to each activity performed by the

organisation is allotted according to their requirements. Advantages and disadvantages of this

method are as follows:

Advantages: Each and every cost driver is being evaluated in this method as it takes all the steps

involved in the activity in to consideration. All the unnecessary activities are being eliminated by

this budgeting approach (Piercy, 2014).

Disadvantages: The process of formulating budget under this approach is very difficult

and complex. Effective and appropriate knowledge is required to conducting this type of

budgeting and for this purpose companies are required to hire skilled staff members.

Rolling budgeting: This approach of budgeting is used to form rolling budget which

involves incremental extension of the existing budget model. Advantages and disadvantages

of this approach are as follows:

Advantages: It is flexible budget in which changes are made according to the previous

year’s data. Justification of each and every expense can be determined with the help of

this budgeting approach.

Disadvantages: The process of formulating rolling budget is a time consuming which

requires a large time period to accomplish all the activities successfully.

B. Discussion of particular difficulties encountered when budgeting in public sector organisation

When managers of public sector conduct budgeting activities they have to different type of

challenges and difficulties. For all type of business entities, it is very important to conduct

budgeting every so that monetary resources could be utilised effectively and efficiently

(McKinney, 2015). Some of the challenges that are faced by managers of public sector

companies while formulating budget are as follows:

7

departments of the organisation according to their requirements. As every expense is

justified in this approach so it can help managers to overcome the weaknesses of

incremental budgeting.

Disadvantages: Large number of employees are required to form budgets under this

method. It required higher time to form the budgets as it a time-consuming process.

Activity based budgeting: Activity based costing is used to form budgets under this

budgeting technique. Under this method budget or resources to each activity performed by the

organisation is allotted according to their requirements. Advantages and disadvantages of this

method are as follows:

Advantages: Each and every cost driver is being evaluated in this method as it takes all the steps

involved in the activity in to consideration. All the unnecessary activities are being eliminated by

this budgeting approach (Piercy, 2014).

Disadvantages: The process of formulating budget under this approach is very difficult

and complex. Effective and appropriate knowledge is required to conducting this type of

budgeting and for this purpose companies are required to hire skilled staff members.

Rolling budgeting: This approach of budgeting is used to form rolling budget which

involves incremental extension of the existing budget model. Advantages and disadvantages

of this approach are as follows:

Advantages: It is flexible budget in which changes are made according to the previous

year’s data. Justification of each and every expense can be determined with the help of

this budgeting approach.

Disadvantages: The process of formulating rolling budget is a time consuming which

requires a large time period to accomplish all the activities successfully.

B. Discussion of particular difficulties encountered when budgeting in public sector organisation

When managers of public sector conduct budgeting activities they have to different type of

challenges and difficulties. For all type of business entities, it is very important to conduct

budgeting every so that monetary resources could be utilised effectively and efficiently

(McKinney, 2015). Some of the challenges that are faced by managers of public sector

companies while formulating budget are as follows:

7

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Main goal of public sector organisations is the welfare of the society. They do not focus

on profit generating so the managers are required to make sure that they are using

monetary resources of public in effective manner.

The managers in public sector companies have to analyse that the budgets have higher

degree of flexibility so that they can modify them according to views of top authority but

in private sector it does not require flexibility because if one budgets are formed then

changes are not made.

The budgets in public sector companies are shown to the general public if they demand

for this so the managers have to face an issue which is related to accuracy of the amount

which is recorded in the books. If it is not accurate then it may create issues for

management and whole company.

In public sector the managers have to coop with the governmental regulations but the private

sector managers are not required to take all of them in to consideration while formulating the

budgets (Nilsson and Stockenstrand, 2015).

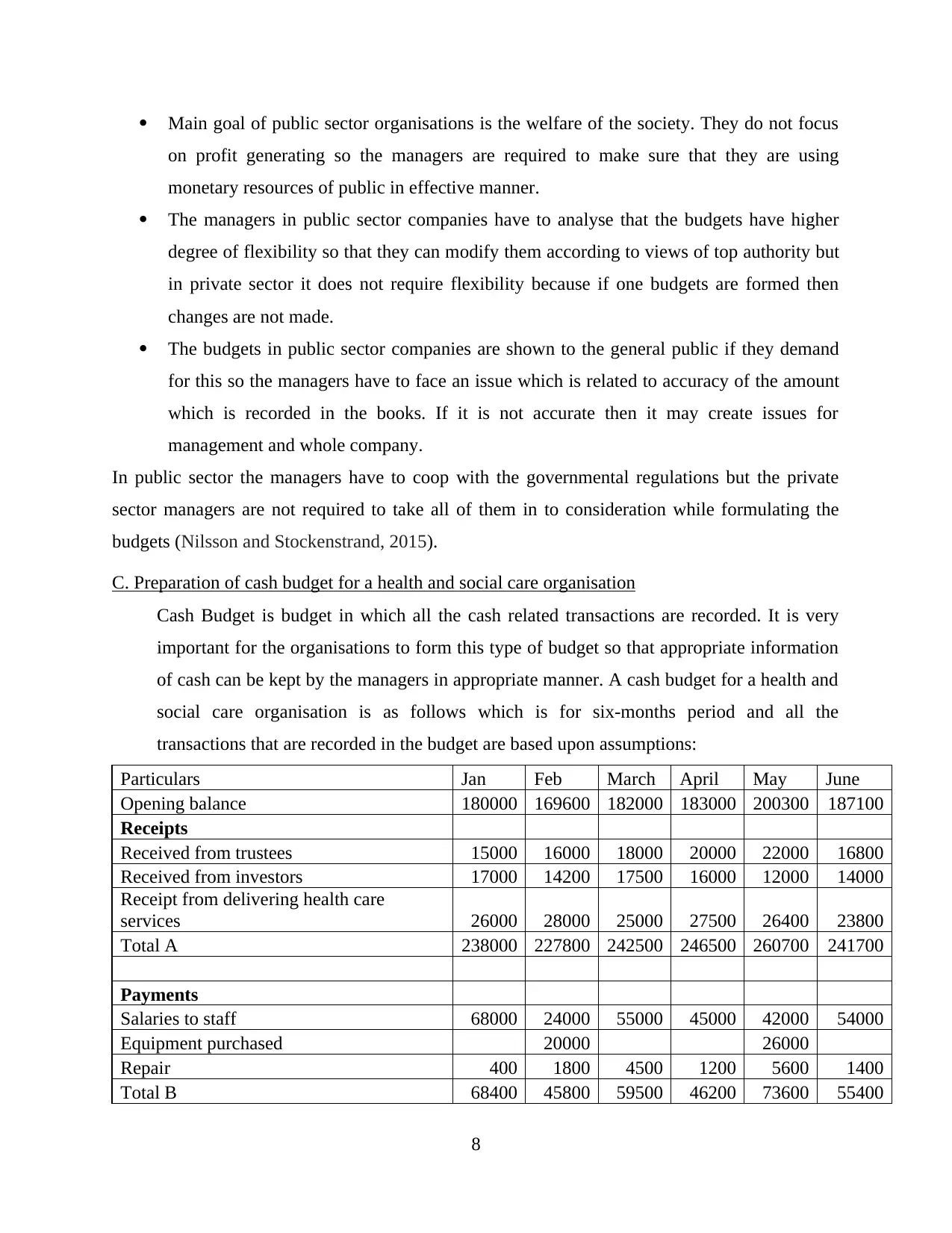

C. Preparation of cash budget for a health and social care organisation

Cash Budget is budget in which all the cash related transactions are recorded. It is very

important for the organisations to form this type of budget so that appropriate information

of cash can be kept by the managers in appropriate manner. A cash budget for a health and

social care organisation is as follows which is for six-months period and all the

transactions that are recorded in the budget are based upon assumptions:

Particulars Jan Feb March April May June

Opening balance 180000 169600 182000 183000 200300 187100

Receipts

Received from trustees 15000 16000 18000 20000 22000 16800

Received from investors 17000 14200 17500 16000 12000 14000

Receipt from delivering health care

services 26000 28000 25000 27500 26400 23800

Total A 238000 227800 242500 246500 260700 241700

Payments

Salaries to staff 68000 24000 55000 45000 42000 54000

Equipment purchased 20000 26000

Repair 400 1800 4500 1200 5600 1400

Total B 68400 45800 59500 46200 73600 55400

8

on profit generating so the managers are required to make sure that they are using

monetary resources of public in effective manner.

The managers in public sector companies have to analyse that the budgets have higher

degree of flexibility so that they can modify them according to views of top authority but

in private sector it does not require flexibility because if one budgets are formed then

changes are not made.

The budgets in public sector companies are shown to the general public if they demand

for this so the managers have to face an issue which is related to accuracy of the amount

which is recorded in the books. If it is not accurate then it may create issues for

management and whole company.

In public sector the managers have to coop with the governmental regulations but the private

sector managers are not required to take all of them in to consideration while formulating the

budgets (Nilsson and Stockenstrand, 2015).

C. Preparation of cash budget for a health and social care organisation

Cash Budget is budget in which all the cash related transactions are recorded. It is very

important for the organisations to form this type of budget so that appropriate information

of cash can be kept by the managers in appropriate manner. A cash budget for a health and

social care organisation is as follows which is for six-months period and all the

transactions that are recorded in the budget are based upon assumptions:

Particulars Jan Feb March April May June

Opening balance 180000 169600 182000 183000 200300 187100

Receipts

Received from trustees 15000 16000 18000 20000 22000 16800

Received from investors 17000 14200 17500 16000 12000 14000

Receipt from delivering health care

services 26000 28000 25000 27500 26400 23800

Total A 238000 227800 242500 246500 260700 241700

Payments

Salaries to staff 68000 24000 55000 45000 42000 54000

Equipment purchased 20000 26000

Repair 400 1800 4500 1200 5600 1400

Total B 68400 45800 59500 46200 73600 55400

8

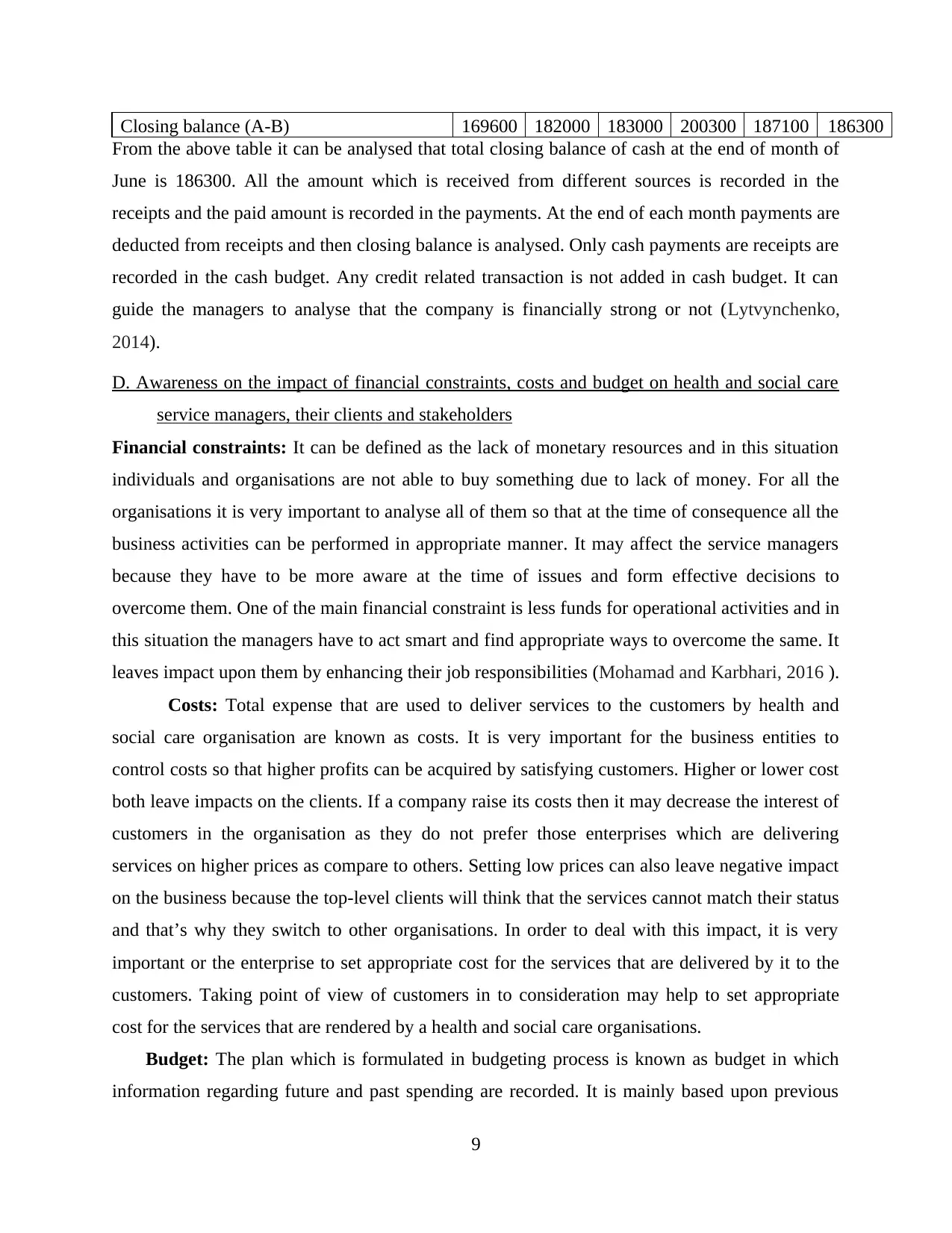

Closing balance (A-B) 169600 182000 183000 200300 187100 186300

From the above table it can be analysed that total closing balance of cash at the end of month of

June is 186300. All the amount which is received from different sources is recorded in the

receipts and the paid amount is recorded in the payments. At the end of each month payments are

deducted from receipts and then closing balance is analysed. Only cash payments are receipts are

recorded in the cash budget. Any credit related transaction is not added in cash budget. It can

guide the managers to analyse that the company is financially strong or not (Lytvynchenko,

2014).

D. Awareness on the impact of financial constraints, costs and budget on health and social care

service managers, their clients and stakeholders

Financial constraints: It can be defined as the lack of monetary resources and in this situation

individuals and organisations are not able to buy something due to lack of money. For all the

organisations it is very important to analyse all of them so that at the time of consequence all the

business activities can be performed in appropriate manner. It may affect the service managers

because they have to be more aware at the time of issues and form effective decisions to

overcome them. One of the main financial constraint is less funds for operational activities and in

this situation the managers have to act smart and find appropriate ways to overcome the same. It

leaves impact upon them by enhancing their job responsibilities (Mohamad and Karbhari, 2016 ).

Costs: Total expense that are used to deliver services to the customers by health and

social care organisation are known as costs. It is very important for the business entities to

control costs so that higher profits can be acquired by satisfying customers. Higher or lower cost

both leave impacts on the clients. If a company raise its costs then it may decrease the interest of

customers in the organisation as they do not prefer those enterprises which are delivering

services on higher prices as compare to others. Setting low prices can also leave negative impact

on the business because the top-level clients will think that the services cannot match their status

and that’s why they switch to other organisations. In order to deal with this impact, it is very

important or the enterprise to set appropriate cost for the services that are delivered by it to the

customers. Taking point of view of customers in to consideration may help to set appropriate

cost for the services that are rendered by a health and social care organisations.

Budget: The plan which is formulated in budgeting process is known as budget in which

information regarding future and past spending are recorded. It is mainly based upon previous

9

From the above table it can be analysed that total closing balance of cash at the end of month of

June is 186300. All the amount which is received from different sources is recorded in the

receipts and the paid amount is recorded in the payments. At the end of each month payments are

deducted from receipts and then closing balance is analysed. Only cash payments are receipts are

recorded in the cash budget. Any credit related transaction is not added in cash budget. It can

guide the managers to analyse that the company is financially strong or not (Lytvynchenko,

2014).

D. Awareness on the impact of financial constraints, costs and budget on health and social care

service managers, their clients and stakeholders

Financial constraints: It can be defined as the lack of monetary resources and in this situation

individuals and organisations are not able to buy something due to lack of money. For all the

organisations it is very important to analyse all of them so that at the time of consequence all the

business activities can be performed in appropriate manner. It may affect the service managers

because they have to be more aware at the time of issues and form effective decisions to

overcome them. One of the main financial constraint is less funds for operational activities and in

this situation the managers have to act smart and find appropriate ways to overcome the same. It

leaves impact upon them by enhancing their job responsibilities (Mohamad and Karbhari, 2016 ).

Costs: Total expense that are used to deliver services to the customers by health and

social care organisation are known as costs. It is very important for the business entities to

control costs so that higher profits can be acquired by satisfying customers. Higher or lower cost

both leave impacts on the clients. If a company raise its costs then it may decrease the interest of

customers in the organisation as they do not prefer those enterprises which are delivering

services on higher prices as compare to others. Setting low prices can also leave negative impact

on the business because the top-level clients will think that the services cannot match their status

and that’s why they switch to other organisations. In order to deal with this impact, it is very

important or the enterprise to set appropriate cost for the services that are delivered by it to the

customers. Taking point of view of customers in to consideration may help to set appropriate

cost for the services that are rendered by a health and social care organisations.

Budget: The plan which is formulated in budgeting process is known as budget in which

information regarding future and past spending are recorded. It is mainly based upon previous

9

year’s data. It is very important for the business entities to analyse the budget so that proper and

appropriate information of the company can be provided to the shareholders. It directly leaves

impact upon shareholders because when it is not created appropriately then it is not possible to

estimate future conditions and allot funds to organisational activities. In order to enhance their

interest in company the managers of entity are required to take appropriate decision and create

budgets effectively so that trust of shareholders could be gained (Villegas, 2015).

All the above described elements may leave impact upon shareholders, clients and managers

so it is very important for the top authority of a health and social care organisations to focus on

the negative aspects of these elements so that appropriate decisions can be formulated for future

period. In order to reduce negative impact of such components the managers may create plan in

advance so that if any uncertainty takes place in future, they can deal with them in effective

manner.

CONCLUSION

From the above project report it ahs been concluded that financial management and control

is very important for all the business entities whether they belong to any sector. There are

various types of budgeting approaches that are used by organisations for the purpose of

formulating different types of budgets. These techniques are zero based, activity based,

incremental and rolling budgeting. There are various types of aspects that are required to be

considered by the top authority in order to enhance interest of customers and shareholders. Break

even point is also used in companies to analyse the units that are required to be sold to recover

all the expenses that are made to manufacture them. Managers of public sector companies have

to face different types of challenges such as putting extra focus on the money spending activities

while formulating budgets.

10

appropriate information of the company can be provided to the shareholders. It directly leaves

impact upon shareholders because when it is not created appropriately then it is not possible to

estimate future conditions and allot funds to organisational activities. In order to enhance their

interest in company the managers of entity are required to take appropriate decision and create

budgets effectively so that trust of shareholders could be gained (Villegas, 2015).

All the above described elements may leave impact upon shareholders, clients and managers

so it is very important for the top authority of a health and social care organisations to focus on

the negative aspects of these elements so that appropriate decisions can be formulated for future

period. In order to reduce negative impact of such components the managers may create plan in

advance so that if any uncertainty takes place in future, they can deal with them in effective

manner.

CONCLUSION

From the above project report it ahs been concluded that financial management and control

is very important for all the business entities whether they belong to any sector. There are

various types of budgeting approaches that are used by organisations for the purpose of

formulating different types of budgets. These techniques are zero based, activity based,

incremental and rolling budgeting. There are various types of aspects that are required to be

considered by the top authority in order to enhance interest of customers and shareholders. Break

even point is also used in companies to analyse the units that are required to be sold to recover

all the expenses that are made to manufacture them. Managers of public sector companies have

to face different types of challenges such as putting extra focus on the money spending activities

while formulating budgets.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals:

Guess, G. M. and Ma, J., 2015. The risks of Chinese subnational debt for public financial

management. Public Administration and Development. 35(2). pp.128-139.

Lauth, T. P., 2014. Zero‐Base Budgeting Redux in Georgia: Efficiency or Ideology?. Public

Budgeting & Finance. 34(1). pp.1-17.

Piercy, N., 2014. Marketing Budgeting (RLE Marketing): A Political and Organisational Model.

Routledge.

McKinney, J. B., 2015. Effective financial management in public and nonprofit agencies. ABC-

CLIO.

Nilsson, F. and Stockenstrand, A. K., 2015. Financial accounting and management control. The

tensions and conflicts between uniformity and uniqueness. Springer, Cham.

Lytvynchenko, G., 2014. Programme management for public budgeting and fiscal

policy. Procedia-Social and Behavioral Sciences. 119. pp.576-580.

Mohamad, M. H. S. and Karbhari, Y., 2016. The NPFM in emerging economies: The modified

budgeting system (mbs) in malaysian government. Indonesian Management and Accounting

Research (IMAR). 9(1). pp.1-26.

Villegas, B. S., 2015. Factors influencing administrators’ empowerment and financial

management effectiveness. Procedia-Social and Behavioral Sciences. 176. pp.466-475.

Theriou, N. G. 2015. Strategic Management Process and the Importance of Structured Formality,

Financial and Non-Financial Information. European Research Studies. 18(2). p.3.

Kaye III, F. J., Frances J. Kaye and III, 2016. Automatic budgeting system. U.S. Patent

9,495,703.

Simmons, C. V., 2012. Budgeting and Organizational Trust in Canadian Universities. Journal of

Academic Administration in Higher Education. 8(1). pp.1-12.

Ferry, L. and Eckersley, P., 2012. Budgeting and governing for deficit reduction in the UK

public sector: act 2 ‘the annual budget’. Public Money & Management. 32(2). pp.119-126.

Dorogovs, P., Solovjova, I. and Romanovs, A., 2013. New tendencies of management and

control of operational risk in financial institutions. Procedia-Social and Behavioral Sciences. 99.

pp.911-918.

Bodiako, and e.t.all. 2016. The goal setting of internal control in the system of project

financing. International journal of economics and financial issues. 6(4). pp.1945-1955.

Piercy, N., 2014. Marketing Budgeting (RLE Marketing): A Political and Organisational Model.

Routledge.

Lins, K. V., Volpin, P. and Wagner, H. F., 2013. Does family control matter? International

evidence from the 2008–2009 financial crisis. The Review of Financial Studies. 26(10). pp.2583-

2619.

Scherer, S. and Wimmer, M. A., 2012, September. Reference process model for participatory

budgeting in Germany. In International Conference on Electronic Participation (pp. 97-111).

Springer, Berlin, Heidelberg.

Online

Incremental budgeting. 2019. [Online]. Available through:

< https://efinancemanagement.com/budgeting/incremental-budgeting>

11

Books and Journals:

Guess, G. M. and Ma, J., 2015. The risks of Chinese subnational debt for public financial

management. Public Administration and Development. 35(2). pp.128-139.

Lauth, T. P., 2014. Zero‐Base Budgeting Redux in Georgia: Efficiency or Ideology?. Public

Budgeting & Finance. 34(1). pp.1-17.

Piercy, N., 2014. Marketing Budgeting (RLE Marketing): A Political and Organisational Model.

Routledge.

McKinney, J. B., 2015. Effective financial management in public and nonprofit agencies. ABC-

CLIO.

Nilsson, F. and Stockenstrand, A. K., 2015. Financial accounting and management control. The

tensions and conflicts between uniformity and uniqueness. Springer, Cham.

Lytvynchenko, G., 2014. Programme management for public budgeting and fiscal

policy. Procedia-Social and Behavioral Sciences. 119. pp.576-580.

Mohamad, M. H. S. and Karbhari, Y., 2016. The NPFM in emerging economies: The modified

budgeting system (mbs) in malaysian government. Indonesian Management and Accounting

Research (IMAR). 9(1). pp.1-26.

Villegas, B. S., 2015. Factors influencing administrators’ empowerment and financial

management effectiveness. Procedia-Social and Behavioral Sciences. 176. pp.466-475.

Theriou, N. G. 2015. Strategic Management Process and the Importance of Structured Formality,

Financial and Non-Financial Information. European Research Studies. 18(2). p.3.

Kaye III, F. J., Frances J. Kaye and III, 2016. Automatic budgeting system. U.S. Patent

9,495,703.

Simmons, C. V., 2012. Budgeting and Organizational Trust in Canadian Universities. Journal of

Academic Administration in Higher Education. 8(1). pp.1-12.

Ferry, L. and Eckersley, P., 2012. Budgeting and governing for deficit reduction in the UK

public sector: act 2 ‘the annual budget’. Public Money & Management. 32(2). pp.119-126.

Dorogovs, P., Solovjova, I. and Romanovs, A., 2013. New tendencies of management and

control of operational risk in financial institutions. Procedia-Social and Behavioral Sciences. 99.

pp.911-918.

Bodiako, and e.t.all. 2016. The goal setting of internal control in the system of project

financing. International journal of economics and financial issues. 6(4). pp.1945-1955.

Piercy, N., 2014. Marketing Budgeting (RLE Marketing): A Political and Organisational Model.

Routledge.

Lins, K. V., Volpin, P. and Wagner, H. F., 2013. Does family control matter? International

evidence from the 2008–2009 financial crisis. The Review of Financial Studies. 26(10). pp.2583-

2619.

Scherer, S. and Wimmer, M. A., 2012, September. Reference process model for participatory

budgeting in Germany. In International Conference on Electronic Participation (pp. 97-111).

Springer, Berlin, Heidelberg.

Online

Incremental budgeting. 2019. [Online]. Available through:

< https://efinancemanagement.com/budgeting/incremental-budgeting>

11

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.