Budgeting, Legal and Financial Aspects of Health and Social Care

VerifiedAdded on 2023/06/12

|16

|4970

|360

Portfolio

AI Summary

This portfolio provides an in-depth analysis of financial management within the health and social care sector. It covers the legal, financial, and regulatory environment, focusing on the Health and Social Care Act 2012 and the Equality Act 2010. Alternative funding options like Private Finance Initiatives (PFI) and agency partnerships are evaluated. The portfolio discusses the impact of financial constraints, costs, and budgets on service managers, clients, and stakeholders. Challenges of budgeting in public sector organizations, advantages and disadvantages of incremental and zero-based budgeting, and the importance of agency theory are examined. The breakeven point and margin of safety for 2018 and 2019 are computed. Desklib provides access to this and other solved assignments, offering students essential study tools.

Portfolio of Tasks

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Table of Contents.................................................................................................................................

INTRODUCTION................................................................................................................................

MAIN BODY.......................................................................................................................................

Task 1...................................................................................................................................................

Legal, financial and regulatory environment of health and social care.......................................

Private Finance Initiatives (PFI), agency partnerships, competitive tendering and

outsourcing in the health and social care sector..........................................................................

Agency theory and explanation of importance of and ways of communicating with

stakeholders in the context of budgeting.....................................................................................

Task 2...................................................................................................................................................

Impact of financial constraints, costs and budgets on health and social care service

managers, their clients and other stakeholders............................................................................

Challenges of budgeting in public sector organisations..............................................................

Advantages and disadvantages of incremental and zero-based budgeting..................................

Task 3.................................................................................................................................................

Compute the breakeven point and margin of safety for the year 2018 and 2019......................

CONCLUSION..................................................................................................................................

REFERENCES...................................................................................................................................

Books and Journals:...................................................................................................................

Table of Contents.................................................................................................................................

INTRODUCTION................................................................................................................................

MAIN BODY.......................................................................................................................................

Task 1...................................................................................................................................................

Legal, financial and regulatory environment of health and social care.......................................

Private Finance Initiatives (PFI), agency partnerships, competitive tendering and

outsourcing in the health and social care sector..........................................................................

Agency theory and explanation of importance of and ways of communicating with

stakeholders in the context of budgeting.....................................................................................

Task 2...................................................................................................................................................

Impact of financial constraints, costs and budgets on health and social care service

managers, their clients and other stakeholders............................................................................

Challenges of budgeting in public sector organisations..............................................................

Advantages and disadvantages of incremental and zero-based budgeting..................................

Task 3.................................................................................................................................................

Compute the breakeven point and margin of safety for the year 2018 and 2019......................

CONCLUSION..................................................................................................................................

REFERENCES...................................................................................................................................

Books and Journals:...................................................................................................................

INTRODUCTION

In the organization, it is identified that budgetary control is playing an important role

as it helps to manage expenditure and income (Bogoslavtseva and et.al., 2019). It is

comparing actual income or expenditure that they are required corrective action or not. This

report aims to understand the importance of financial control and budgeting and health and

social care. It will discuss the analysis of the legal, financial and regulatory environment of

the health and social care sector, evaluation of different alternative funding options in the

health and social care sector, and agency theory in the context of NHS. In addition to this, it

will also discuss the impact of financial constraints on health and social care services. In this

report, there will be a discussion of particular challenges of budgeting and the advantages and

disadvantages of zero-based budgeting.

MAIN BODY

Task 1

Legal, financial and regulatory environment of health and social care

The Health and Social Care Act 2012 introduce the legal duties of health inequalities.

This act says reducing the health inequalities among the people. This Act also changes local

authorities on a public health function (Yusuf, 2021). The Equality Act 2010 says that

establishing equalities in all public sector which aim to integrate with all the business bodies.

The legalisation may be seen as complimentary for the public sector to take action to reduce

inequality at a local and national level.

The primary aim is the act is to ensure public safety. The UK government is

responsible for 32 regulating. In health care, professional regulation is the much broader term

for ensuring the patient is service care unit. But the UK framework is inconsistent, poorly

understood. There is a wide range of inconsistencies with different regulators' different

power. But the major drawback is the expensiveness of the current system Because of this

change regulatory bodies must be developed scrutinised and secured by the government.

Health care gives the power to the regulator for making their own rules. Make a new barring

scheme for prevention professionals who did crimes in their profession. Greater use of

meditation for fitness in their profession. The regulator should consult the public and work to

collaborate less than government interference. The regulator should make a very clear

framework that is needed to protect the public.

In the organization, it is identified that budgetary control is playing an important role

as it helps to manage expenditure and income (Bogoslavtseva and et.al., 2019). It is

comparing actual income or expenditure that they are required corrective action or not. This

report aims to understand the importance of financial control and budgeting and health and

social care. It will discuss the analysis of the legal, financial and regulatory environment of

the health and social care sector, evaluation of different alternative funding options in the

health and social care sector, and agency theory in the context of NHS. In addition to this, it

will also discuss the impact of financial constraints on health and social care services. In this

report, there will be a discussion of particular challenges of budgeting and the advantages and

disadvantages of zero-based budgeting.

MAIN BODY

Task 1

Legal, financial and regulatory environment of health and social care

The Health and Social Care Act 2012 introduce the legal duties of health inequalities.

This act says reducing the health inequalities among the people. This Act also changes local

authorities on a public health function (Yusuf, 2021). The Equality Act 2010 says that

establishing equalities in all public sector which aim to integrate with all the business bodies.

The legalisation may be seen as complimentary for the public sector to take action to reduce

inequality at a local and national level.

The primary aim is the act is to ensure public safety. The UK government is

responsible for 32 regulating. In health care, professional regulation is the much broader term

for ensuring the patient is service care unit. But the UK framework is inconsistent, poorly

understood. There is a wide range of inconsistencies with different regulators' different

power. But the major drawback is the expensiveness of the current system Because of this

change regulatory bodies must be developed scrutinised and secured by the government.

Health care gives the power to the regulator for making their own rules. Make a new barring

scheme for prevention professionals who did crimes in their profession. Greater use of

meditation for fitness in their profession. The regulator should consult the public and work to

collaborate less than government interference. The regulator should make a very clear

framework that is needed to protect the public.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Local authorities are the main source of funding in health and social care. In recent

years, this increased share also come from NHS. Its half of service care is spent on services

for older people and 52% spend on working-age people mainly support for mental health

conditions or learning disabilities (Aung and Mon, 2020). This service is tested and funded

by local taxation and Government grant. Some user gives a relatively large number of funders

in this section. Funding is recovered in recent years but the population is increasing day by

day. That means pressure on the government.

Because of the pressure, needy people do not access formal care and service. It seems

that the increasing population reduced the funding according to data funding in 2018/19

subsequently is lower than 2010/11. So that the government will increase funding in 2019-20.

Five priorities for the government to take initiative for social care is that stabilise the current

social care system and include boosting staff pay or much sure about to improve access to

services. This improvement increases people's health and their access to services. More

reform in funding care unit is shown as fair and provide government protection against social

care cost. Requiring any option genuine government system that is an investment in the

Health care system include the long term funding settlement for capital driven by the need of

patient and staff. The government need to stabilise and improve the current system because it

is in collapse boosting staff pay to alleviate the problem of recruitment and retention.

Government need to improve public care funding.

Private Finance Initiatives (PFI), agency partnerships, competitive tendering and outsourcing

in the health and social care sector

The private firm is collaborating to complete the public project. It starts in 1992 with

the UK printer. PFI is part of privatisation or financial and presents the accountability of

public spending. The Private Finance Initiative is a method that is used for privatisation.

Which is an investment in the private sector to deliver to the public sector. Infrastructure or

specification according to the public sector (Shuaib and Olanrewaju, 2020). It is broader

procurement for public and private partnerships main using of project finance to deliver

public service. PFI involves contracting the design building and operation to public sector

private sector companies and long term contracts. It increases competition between private

providers. PFI is used for the investment needed to build assets for ongoing service

requirements. PFI was used to build prisons, hospitals, schools, roads. NHS and PFI will

increase the hospital they are coordinate with each other and give good results in making a

hospital.

years, this increased share also come from NHS. Its half of service care is spent on services

for older people and 52% spend on working-age people mainly support for mental health

conditions or learning disabilities (Aung and Mon, 2020). This service is tested and funded

by local taxation and Government grant. Some user gives a relatively large number of funders

in this section. Funding is recovered in recent years but the population is increasing day by

day. That means pressure on the government.

Because of the pressure, needy people do not access formal care and service. It seems

that the increasing population reduced the funding according to data funding in 2018/19

subsequently is lower than 2010/11. So that the government will increase funding in 2019-20.

Five priorities for the government to take initiative for social care is that stabilise the current

social care system and include boosting staff pay or much sure about to improve access to

services. This improvement increases people's health and their access to services. More

reform in funding care unit is shown as fair and provide government protection against social

care cost. Requiring any option genuine government system that is an investment in the

Health care system include the long term funding settlement for capital driven by the need of

patient and staff. The government need to stabilise and improve the current system because it

is in collapse boosting staff pay to alleviate the problem of recruitment and retention.

Government need to improve public care funding.

Private Finance Initiatives (PFI), agency partnerships, competitive tendering and outsourcing

in the health and social care sector

The private firm is collaborating to complete the public project. It starts in 1992 with

the UK printer. PFI is part of privatisation or financial and presents the accountability of

public spending. The Private Finance Initiative is a method that is used for privatisation.

Which is an investment in the private sector to deliver to the public sector. Infrastructure or

specification according to the public sector (Shuaib and Olanrewaju, 2020). It is broader

procurement for public and private partnerships main using of project finance to deliver

public service. PFI involves contracting the design building and operation to public sector

private sector companies and long term contracts. It increases competition between private

providers. PFI is used for the investment needed to build assets for ongoing service

requirements. PFI was used to build prisons, hospitals, schools, roads. NHS and PFI will

increase the hospital they are coordinate with each other and give good results in making a

hospital.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

It means two separate entities work together for the completion of a goal. Separate

organise to come together to share the resource and pooled expertise, power-sharing. It means

to increase efficiency quality of service. All parties come together for some interest and they

achieve some common goal. The parties have some common ethos and belief and they work

for some reasonable time or it will increase mutual understating and trust. Partnership

working in social care increase the knowledge and understanding of the new technology

together. A partnership can be formed between several individuals, organisations, agencies. It

is made for long term and short term aspects (Gamayuni, 2020). Partnerships need to clear

effective leadership. Each of the partners must understand each other in the partnership. Time

and allocation of resources are must on the time shown the partnership is very effective the

partner understand responsibility. Open communication reduce conflict in the partnership.

The partner suggests ideas in front of anyone this is open communication with no fear of

anyone. It increases the number of benefits for the patient. A one-stop shop is a place the

patient doesn’t go anywhere it is a shop that have all item that the patient needed this is an

effective partnership.

The use of outsourcing by the public sector is dramatically increased. The public

sector is defined as an act of a public organism transferring internal services. While the

immediate impetus for reform in the outsourcing sector is the need to reduce government

spending. It increases the greater efficiency comes in Covid 19 increase outsourcing some

countries take ventilator form to outsource. Public health care services increasing to view

outsourcing as critically successful (Kisaata, 2019). Outsourcing increases efficiency also

because they give new technology comes from different countries by way of outsourcing. All

social health people will use this technology and take care of all patients. This is proven by

covid 19 every country outsource. Among the different non-clinical activities logistics and is

great importance they represent a large portion of health care organism and are essential for

their operational performance.

Agency theory and explanation of importance of and ways of communicating with

stakeholders in the context of budgeting

It is necessary to understand for an organisation that agency theories play a crucial

road in order to enhance of performance of the company. NHS is the National Health Service

which is a publicly funded healthcare system in England. It is found to be one of the four

National Health Service systems in the UK (Gray, Jenkins and Segsworth, 2020). Agency

theory refers to an economic theory that focuses on the firm which set contracts among self-

organise to come together to share the resource and pooled expertise, power-sharing. It means

to increase efficiency quality of service. All parties come together for some interest and they

achieve some common goal. The parties have some common ethos and belief and they work

for some reasonable time or it will increase mutual understating and trust. Partnership

working in social care increase the knowledge and understanding of the new technology

together. A partnership can be formed between several individuals, organisations, agencies. It

is made for long term and short term aspects (Gamayuni, 2020). Partnerships need to clear

effective leadership. Each of the partners must understand each other in the partnership. Time

and allocation of resources are must on the time shown the partnership is very effective the

partner understand responsibility. Open communication reduce conflict in the partnership.

The partner suggests ideas in front of anyone this is open communication with no fear of

anyone. It increases the number of benefits for the patient. A one-stop shop is a place the

patient doesn’t go anywhere it is a shop that have all item that the patient needed this is an

effective partnership.

The use of outsourcing by the public sector is dramatically increased. The public

sector is defined as an act of a public organism transferring internal services. While the

immediate impetus for reform in the outsourcing sector is the need to reduce government

spending. It increases the greater efficiency comes in Covid 19 increase outsourcing some

countries take ventilator form to outsource. Public health care services increasing to view

outsourcing as critically successful (Kisaata, 2019). Outsourcing increases efficiency also

because they give new technology comes from different countries by way of outsourcing. All

social health people will use this technology and take care of all patients. This is proven by

covid 19 every country outsource. Among the different non-clinical activities logistics and is

great importance they represent a large portion of health care organism and are essential for

their operational performance.

Agency theory and explanation of importance of and ways of communicating with

stakeholders in the context of budgeting

It is necessary to understand for an organisation that agency theories play a crucial

road in order to enhance of performance of the company. NHS is the National Health Service

which is a publicly funded healthcare system in England. It is found to be one of the four

National Health Service systems in the UK (Gray, Jenkins and Segsworth, 2020). Agency

theory refers to an economic theory that focuses on the firm which set contracts among self-

interested individuals. It is very helpful to understand the relationship between principals and

agents for a particular business transaction. Agency theory is found to be clearly articulate the

need to monitor and control management activity. It is identified that the UK reflects an

agency model India public sector organisation which includes the NHS board. Is identified

that there are some difficulties which are identified in agency theory as it becomes difficult

for the public and non-profit sectors. It is found that agency theory dimensions the purpose of

the board related to the set of values and vision of the company. Agency theories found a

contract which formed between one or more persons by engaging other people so that they

can perform some important services on their behalf. It invoice delegation of some important

decision making authority to the agent so that they can able to deal with the patient. It is used

for explaining and resolving issues between principals and agents.

Communication is found to be very important with stakeholders when the company is

making a budget. Budgeting is found to be a process in which a company is creating a plan in

order to spend their money and it is necessary to communicate with each and every person so

that they can act accordingly (Volosovych and Baraniuk, 2019). If it is found any lack of

communication with the stakeholders then it is not possible to achieve the objectives. It is

also identified that communication with the stakeholders in the budgeting process becomes

more important as they are responsible for financial control and if they do not have any

information about the budget then they will not able to achieve the goals and objectives. So

that's why they need to use different ways of effective communication with the stakeholders.

Some important ways are mentioned below:

For the purpose of discussing any information related to budgeting, it is necessary to

schedule a meeting with the stakeholders so that they can save time in conveying the

message to a large number of people.

In addition to this, they can also use the screen to screen meetings which are really

very less time consuming as compared to face to face meetings.

Task 2

Impact of financial constraints, costs and budgets on health and social care service managers,

their clients and other stakeholders

It is experienced by England that there are some constraints on public expenditure in

the healthcare and social care sector. A financial constraint has restricted a course of

economic activity. It is a real issue that is necessary to understand by an individual as they

agents for a particular business transaction. Agency theory is found to be clearly articulate the

need to monitor and control management activity. It is identified that the UK reflects an

agency model India public sector organisation which includes the NHS board. Is identified

that there are some difficulties which are identified in agency theory as it becomes difficult

for the public and non-profit sectors. It is found that agency theory dimensions the purpose of

the board related to the set of values and vision of the company. Agency theories found a

contract which formed between one or more persons by engaging other people so that they

can perform some important services on their behalf. It invoice delegation of some important

decision making authority to the agent so that they can able to deal with the patient. It is used

for explaining and resolving issues between principals and agents.

Communication is found to be very important with stakeholders when the company is

making a budget. Budgeting is found to be a process in which a company is creating a plan in

order to spend their money and it is necessary to communicate with each and every person so

that they can act accordingly (Volosovych and Baraniuk, 2019). If it is found any lack of

communication with the stakeholders then it is not possible to achieve the objectives. It is

also identified that communication with the stakeholders in the budgeting process becomes

more important as they are responsible for financial control and if they do not have any

information about the budget then they will not able to achieve the goals and objectives. So

that's why they need to use different ways of effective communication with the stakeholders.

Some important ways are mentioned below:

For the purpose of discussing any information related to budgeting, it is necessary to

schedule a meeting with the stakeholders so that they can save time in conveying the

message to a large number of people.

In addition to this, they can also use the screen to screen meetings which are really

very less time consuming as compared to face to face meetings.

Task 2

Impact of financial constraints, costs and budgets on health and social care service managers,

their clients and other stakeholders

It is experienced by England that there are some constraints on public expenditure in

the healthcare and social care sector. A financial constraint has restricted a course of

economic activity. It is a real issue that is necessary to understand by an individual as they

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

should not be confused with emotional or subjective excuses (Butyugina and Gorbunova,

2021). These are the obstacles that restrict the number of investment options. For example,

poor cash flow and lack of knowledge are found to be the internal constraint faced by every

individual in their life. It is also necessary for every individual that it provides a negative

impact on health and social care service managers, clients and other stakeholders. The

negative impact can be understood with the help of the below points:

It is identified that financial constraints are including inadequate access to venture

capital. It also includes the rising interest rate and inflation rates. Health and social

care sector is found to be one of the important sectors which require excess financial

arrangements so that they can able to maximize the treatment of people. But due to

financial constraints, they are unable to provide maximum benefits. It is identified that

managers of the health and social care sector face the difficulty that how they will

manage their limited financial resources to provide maximum benefits to the

customers. It is found to be the negative impact of financial constraint as it limits the

scope of the health and social care sector.

It is also found that the customers also face many problems due to financial

constraints as they do have not enough money to get all the facilities provided by the

health and social care sector (Bialowolski, Weziak-Bialowolska and McNeely, 2021).

This is analysed more with the help of the current pandemic situation in which people

are feeling very helpless due to financial constraints as they are not able to take the

facility of ventilators due to high cost.

It is identified that the other stakeholders of the health and social care sector are

facing many challenges due to financial constraints. It includes patients, government,

charities, inspecting bodies, community, etc. will be facing many challenges due to

financial constraints. The government is facing in educate budgetary allocation to

health which becomes the main issue. Due to this, they are unable to hire human

resources.

It is identified that financial cost is also providing an impact on healthcare service

managers, clients and other stakeholders. Financial cost includes direct as well as indirect

cost in the health and social care sector. It is identified that 2021 will be a dynamic year for

the UK in terms of healthcare policies. It is the year in which they need to reform their

policies so that they can help better access, equity and affordability. During the pandemic

2021). These are the obstacles that restrict the number of investment options. For example,

poor cash flow and lack of knowledge are found to be the internal constraint faced by every

individual in their life. It is also necessary for every individual that it provides a negative

impact on health and social care service managers, clients and other stakeholders. The

negative impact can be understood with the help of the below points:

It is identified that financial constraints are including inadequate access to venture

capital. It also includes the rising interest rate and inflation rates. Health and social

care sector is found to be one of the important sectors which require excess financial

arrangements so that they can able to maximize the treatment of people. But due to

financial constraints, they are unable to provide maximum benefits. It is identified that

managers of the health and social care sector face the difficulty that how they will

manage their limited financial resources to provide maximum benefits to the

customers. It is found to be the negative impact of financial constraint as it limits the

scope of the health and social care sector.

It is also found that the customers also face many problems due to financial

constraints as they do have not enough money to get all the facilities provided by the

health and social care sector (Bialowolski, Weziak-Bialowolska and McNeely, 2021).

This is analysed more with the help of the current pandemic situation in which people

are feeling very helpless due to financial constraints as they are not able to take the

facility of ventilators due to high cost.

It is identified that the other stakeholders of the health and social care sector are

facing many challenges due to financial constraints. It includes patients, government,

charities, inspecting bodies, community, etc. will be facing many challenges due to

financial constraints. The government is facing in educate budgetary allocation to

health which becomes the main issue. Due to this, they are unable to hire human

resources.

It is identified that financial cost is also providing an impact on healthcare service

managers, clients and other stakeholders. Financial cost includes direct as well as indirect

cost in the health and social care sector. It is identified that 2021 will be a dynamic year for

the UK in terms of healthcare policies. It is the year in which they need to reform their

policies so that they can help better access, equity and affordability. During the pandemic

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

situation, the United Kingdom get to know about the financial cost which hit their system of

health and social care. It includes both direct and indirect costs (Ibrahim and Mustapha,

2019). It is providing a great impact on health and social care service managers as it becomes

very difficult for them to manage the cost. Due to the access cost of health and social care

facilities, clients and other stakeholders are unable to take services. It is similarly found in the

case of financial budgets. Budget is not an easy task for health and social care service

managers as they need to make a budget that is appropriate for each and every stakeholder

including their patients also.

Challenges of budgeting in public sector organisations

Budgeting is a process that is found to be essential for the financial success of any

organisation and it becomes more important than in the health and social care sector. It helps

to pay off debt, grow money with the help of investment and save money also (Setyawan and

Gamayuni, 2020). But it is identified that there are many budgeting challenges are found

which is necessary to tackle why organisation so that they can able to perform effectively.

Some important budgeting challenges are mentioned below:

It is identified that budgeting involves a high degree of complexity. It is necessary to

understand that budgeting is a very complicated and multi-staff process. Due to this, it

involves unpredicted external changes which provide a great impact on budgeting. It

is found that any slightest modification in a budget will result in a complicated

process for managers as the need to recalculate all the numbers. In addition to this,

they also need to resend spreadsheets and respond to all the questions which arise

from the slightest modifications in a budget. It is found that financial budgeting has

no capability to accommodate mergers, acquisitions and reorganisation. It is not able

to perform and respond effectively as they have no ability to recognise changes. So it

becomes a challenge for an organisation how they can deal with the changes found in

the budgeting process.

Creating a budget is found to be a very expensive and time-consuming task. It has

also become a challenge for the company to create a budget as it is a very time-

consuming process that requires constant iterations. It is identified that many CF force

spends their 250 hours only on the budgeting process which is a really poor use of

resources and time. In the case of multiple users are working in the organisation in

different versions than it becomes more time consuming to compile, coordinate and

health and social care. It includes both direct and indirect costs (Ibrahim and Mustapha,

2019). It is providing a great impact on health and social care service managers as it becomes

very difficult for them to manage the cost. Due to the access cost of health and social care

facilities, clients and other stakeholders are unable to take services. It is similarly found in the

case of financial budgets. Budget is not an easy task for health and social care service

managers as they need to make a budget that is appropriate for each and every stakeholder

including their patients also.

Challenges of budgeting in public sector organisations

Budgeting is a process that is found to be essential for the financial success of any

organisation and it becomes more important than in the health and social care sector. It helps

to pay off debt, grow money with the help of investment and save money also (Setyawan and

Gamayuni, 2020). But it is identified that there are many budgeting challenges are found

which is necessary to tackle why organisation so that they can able to perform effectively.

Some important budgeting challenges are mentioned below:

It is identified that budgeting involves a high degree of complexity. It is necessary to

understand that budgeting is a very complicated and multi-staff process. Due to this, it

involves unpredicted external changes which provide a great impact on budgeting. It

is found that any slightest modification in a budget will result in a complicated

process for managers as the need to recalculate all the numbers. In addition to this,

they also need to resend spreadsheets and respond to all the questions which arise

from the slightest modifications in a budget. It is found that financial budgeting has

no capability to accommodate mergers, acquisitions and reorganisation. It is not able

to perform and respond effectively as they have no ability to recognise changes. So it

becomes a challenge for an organisation how they can deal with the changes found in

the budgeting process.

Creating a budget is found to be a very expensive and time-consuming task. It has

also become a challenge for the company to create a budget as it is a very time-

consuming process that requires constant iterations. It is identified that many CF force

spends their 250 hours only on the budgeting process which is a really poor use of

resources and time. In the case of multiple users are working in the organisation in

different versions than it becomes more time consuming to compile, coordinate and

consolidate. Due to the excess time, the cost of resources is increasingly and up in

budgeting.

It is identified in the budgeting process that lack of communication between

employees will become a challenge as it leads to errors in the budget. This is

necessary to understand for each and every organisation that there are many moving

parts that should be covered. It is found that every step of the budget process requires

information and input from users and different departments (Kunnathuvalappil

Hariharan, 2020). Due to this, it becomes very difficult for users to coordinate all the

activities with each other. It leads to ineffective communication which will be

provided negative implications on the resulting budget. This is necessary to

understand that when two users are not communicating with each other than how it

will be possible to coordinate all the activities and it will result in a lack of alignment

in the budget. Every organisation knows that communication is very important in

today's business environment after the pandemic situation. Due to covid-19, it is

found that there is a continuous increasing online work in which the importance of

communication is becoming very important and in the case of the budgeting process,

it is found that company management should focus on scheduling all the meetings so

that they can communicate with the employees.

One more challenge in budgeting is it leads to an excessive focus on financial

outcomes. It is very well known by every organisation that when they are creating

budgets then they need to spend time on numbers and the main focus of management

is always on financial outcomes. It is found that every organisation has an aim for

using the budget as they want to increase their revenue, profitability and reduce

expenses. This is the main reason that management of a company always overlooks

many qualitative aspects due to the focus on financial outcomes. They always ignore

employee satisfaction and the culture of the organisation.

Advantages and disadvantages of incremental and zero-based budgeting

It is identified that incremental budgeting is found to be a type of budgeting process

which is mainly based on the idea that a new budget can be developed only with the help of

some marginal changes in the current budget. That means it used a current budget as a base in

which they add or subtract some incremental assumptions in order to determine new budget

amounts (Schubert and Kirsten, 2021). It is found that incremental budgeting is one of the

budgeting.

It is identified in the budgeting process that lack of communication between

employees will become a challenge as it leads to errors in the budget. This is

necessary to understand for each and every organisation that there are many moving

parts that should be covered. It is found that every step of the budget process requires

information and input from users and different departments (Kunnathuvalappil

Hariharan, 2020). Due to this, it becomes very difficult for users to coordinate all the

activities with each other. It leads to ineffective communication which will be

provided negative implications on the resulting budget. This is necessary to

understand that when two users are not communicating with each other than how it

will be possible to coordinate all the activities and it will result in a lack of alignment

in the budget. Every organisation knows that communication is very important in

today's business environment after the pandemic situation. Due to covid-19, it is

found that there is a continuous increasing online work in which the importance of

communication is becoming very important and in the case of the budgeting process,

it is found that company management should focus on scheduling all the meetings so

that they can communicate with the employees.

One more challenge in budgeting is it leads to an excessive focus on financial

outcomes. It is very well known by every organisation that when they are creating

budgets then they need to spend time on numbers and the main focus of management

is always on financial outcomes. It is found that every organisation has an aim for

using the budget as they want to increase their revenue, profitability and reduce

expenses. This is the main reason that management of a company always overlooks

many qualitative aspects due to the focus on financial outcomes. They always ignore

employee satisfaction and the culture of the organisation.

Advantages and disadvantages of incremental and zero-based budgeting

It is identified that incremental budgeting is found to be a type of budgeting process

which is mainly based on the idea that a new budget can be developed only with the help of

some marginal changes in the current budget. That means it used a current budget as a base in

which they add or subtract some incremental assumptions in order to determine new budget

amounts (Schubert and Kirsten, 2021). It is found that incremental budgeting is one of the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

most commonly used budgeting methods as it is the most conservative approach. Some

advantages and disadvantages of incremental budgeting are mentioned below:

Advantages of incremental budgeting

It is identified that implemental budgeting is found to be the easiest budgeting

approach. The creation of a new budget is not required any complex calculation

incremental budgeting.

It is also identified that implemental budgeting is important for reducing internal

rivalry as it allocates equal incremental changes in the budget.

Incremental budgeting is helpful for a company as it ensures that funding should be

remain stable which helps the company with projects.

Disadvantages of incremental budgeting

It is found that it promotes unnecessary spending. It is identified that departments of a

company has always a tendency that they have to spend all the money which they

allocated in a budget so that they can obtain a greater amount of money in the next

budget. Due to this, it is identified that an incremental budget increases the budget

every year.

It also discourages innovation because it is based on the previous budget. Due to this,

the production of new and innovative ideas are stopped.

Zero-based budgeting is found to be a method in which a company is focusing on all

the expenses that should be justified for each and every which means companies analyse the

need and cost of the budget of every function.

Advantages of zero based budgeting

It is identified that zero-based budgeting is really very helpful for prioritizing resource

allocation efficiency.

It is necessary to understand that zero-based budgeting promotes optimisation in

business process management. Zero page budgeting is focusing on those items which

provide is a direct benefit to the business with the help of cost reduction and greater

efficiency. It actually trims the fat and focuses on continuous improvement. It is

advantages and disadvantages of incremental budgeting are mentioned below:

Advantages of incremental budgeting

It is identified that implemental budgeting is found to be the easiest budgeting

approach. The creation of a new budget is not required any complex calculation

incremental budgeting.

It is also identified that implemental budgeting is important for reducing internal

rivalry as it allocates equal incremental changes in the budget.

Incremental budgeting is helpful for a company as it ensures that funding should be

remain stable which helps the company with projects.

Disadvantages of incremental budgeting

It is found that it promotes unnecessary spending. It is identified that departments of a

company has always a tendency that they have to spend all the money which they

allocated in a budget so that they can obtain a greater amount of money in the next

budget. Due to this, it is identified that an incremental budget increases the budget

every year.

It also discourages innovation because it is based on the previous budget. Due to this,

the production of new and innovative ideas are stopped.

Zero-based budgeting is found to be a method in which a company is focusing on all

the expenses that should be justified for each and every which means companies analyse the

need and cost of the budget of every function.

Advantages of zero based budgeting

It is identified that zero-based budgeting is really very helpful for prioritizing resource

allocation efficiency.

It is necessary to understand that zero-based budgeting promotes optimisation in

business process management. Zero page budgeting is focusing on those items which

provide is a direct benefit to the business with the help of cost reduction and greater

efficiency. It actually trims the fat and focuses on continuous improvement. It is

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

identified that zero piece budgeting is very helpful in strategic decision making as

companies are more able to forecast finance in an effective way.

Zero base budgeting is strengthening strategic transparency and growth as it

encourages internal leadership to the project leaders. It promotes innovation and also

focuses on minimising waste.

Disadvantages of zero based budgeting

It is identified that zero-base budgeting is found to be a complex and expensive

procedure as it is very complicated to implement. It requires extra training which

increase the budget. It includes time constraints.

Zero-based budgeting is found to be difficult for managers to make changes in the

budget. It becomes disruptive when they are trying on changes.

Task 3

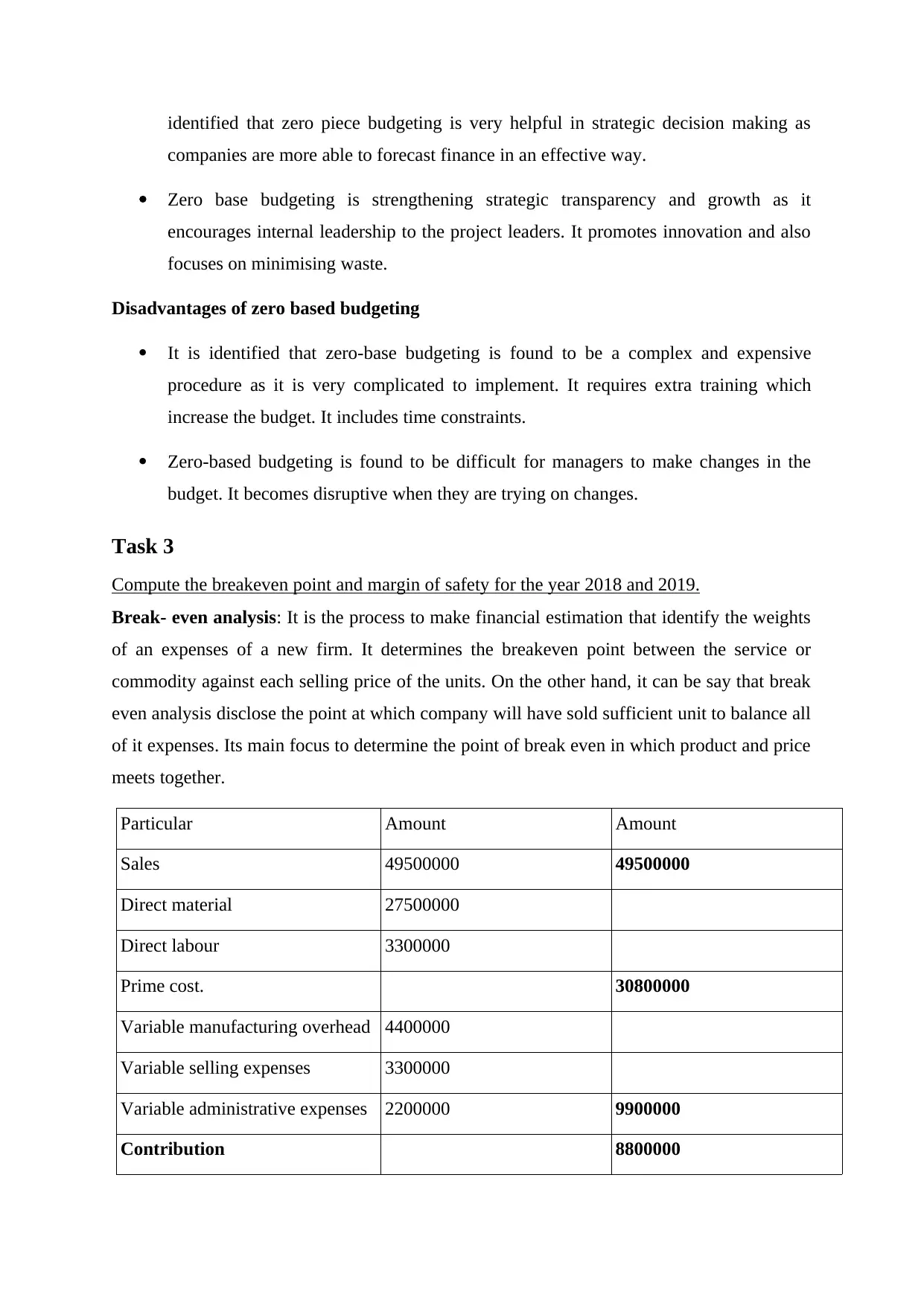

Compute the breakeven point and margin of safety for the year 2018 and 2019.

Break- even analysis: It is the process to make financial estimation that identify the weights

of an expenses of a new firm. It determines the breakeven point between the service or

commodity against each selling price of the units. On the other hand, it can be say that break

even analysis disclose the point at which company will have sold sufficient unit to balance all

of it expenses. Its main focus to determine the point of break even in which product and price

meets together.

Particular Amount Amount

Sales 49500000 49500000

Direct material 27500000

Direct labour 3300000

Prime cost. 30800000

Variable manufacturing overhead 4400000

Variable selling expenses 3300000

Variable administrative expenses 2200000 9900000

Contribution 8800000

companies are more able to forecast finance in an effective way.

Zero base budgeting is strengthening strategic transparency and growth as it

encourages internal leadership to the project leaders. It promotes innovation and also

focuses on minimising waste.

Disadvantages of zero based budgeting

It is identified that zero-base budgeting is found to be a complex and expensive

procedure as it is very complicated to implement. It requires extra training which

increase the budget. It includes time constraints.

Zero-based budgeting is found to be difficult for managers to make changes in the

budget. It becomes disruptive when they are trying on changes.

Task 3

Compute the breakeven point and margin of safety for the year 2018 and 2019.

Break- even analysis: It is the process to make financial estimation that identify the weights

of an expenses of a new firm. It determines the breakeven point between the service or

commodity against each selling price of the units. On the other hand, it can be say that break

even analysis disclose the point at which company will have sold sufficient unit to balance all

of it expenses. Its main focus to determine the point of break even in which product and price

meets together.

Particular Amount Amount

Sales 49500000 49500000

Direct material 27500000

Direct labour 3300000

Prime cost. 30800000

Variable manufacturing overhead 4400000

Variable selling expenses 3300000

Variable administrative expenses 2200000 9900000

Contribution 8800000

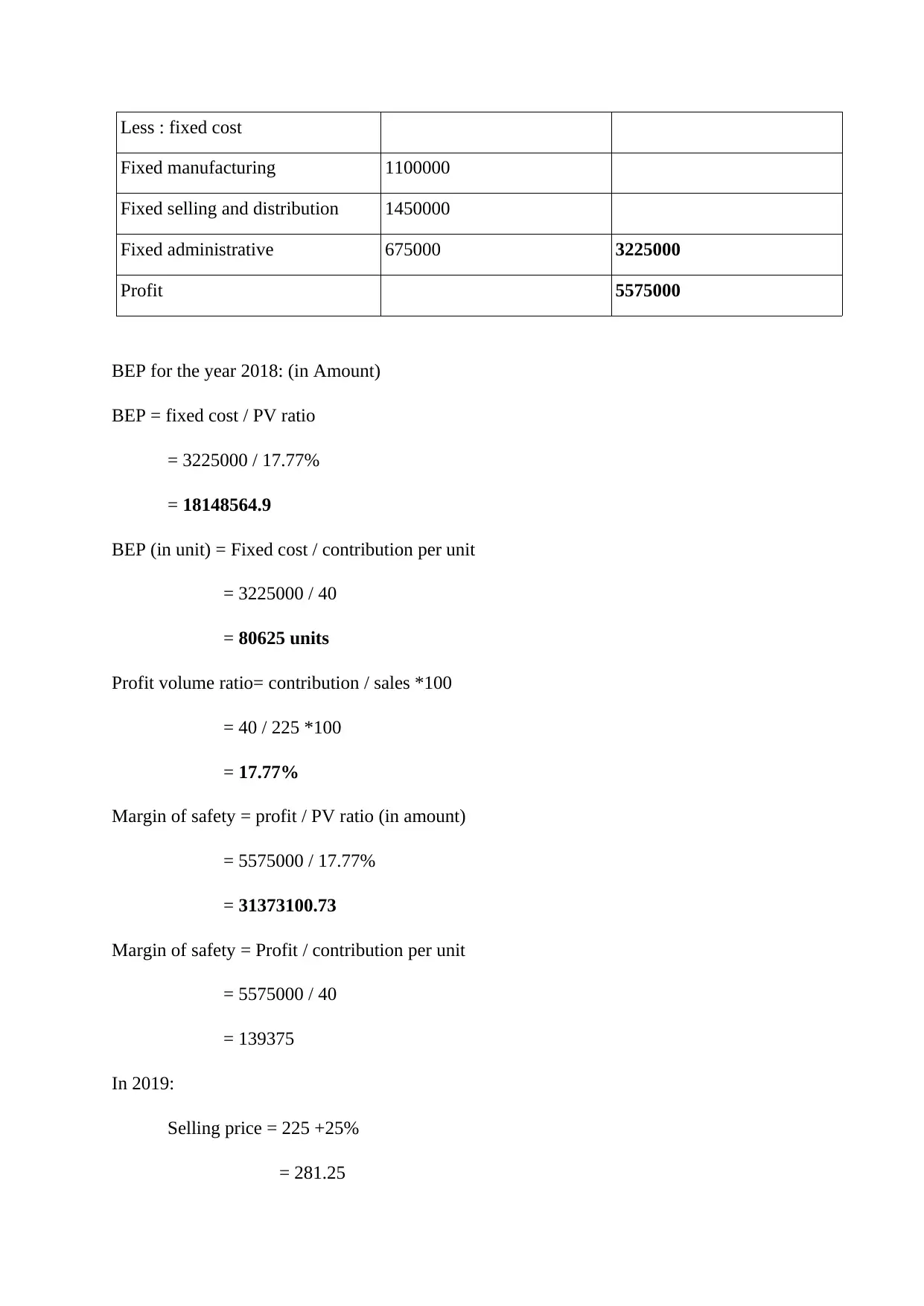

Less : fixed cost

Fixed manufacturing 1100000

Fixed selling and distribution 1450000

Fixed administrative 675000 3225000

Profit 5575000

BEP for the year 2018: (in Amount)

BEP = fixed cost / PV ratio

= 3225000 / 17.77%

= 18148564.9

BEP (in unit) = Fixed cost / contribution per unit

= 3225000 / 40

= 80625 units

Profit volume ratio= contribution / sales *100

= 40 / 225 *100

= 17.77%

Margin of safety = profit / PV ratio (in amount)

= 5575000 / 17.77%

= 31373100.73

Margin of safety = Profit / contribution per unit

= 5575000 / 40

= 139375

In 2019:

Selling price = 225 +25%

= 281.25

Fixed manufacturing 1100000

Fixed selling and distribution 1450000

Fixed administrative 675000 3225000

Profit 5575000

BEP for the year 2018: (in Amount)

BEP = fixed cost / PV ratio

= 3225000 / 17.77%

= 18148564.9

BEP (in unit) = Fixed cost / contribution per unit

= 3225000 / 40

= 80625 units

Profit volume ratio= contribution / sales *100

= 40 / 225 *100

= 17.77%

Margin of safety = profit / PV ratio (in amount)

= 5575000 / 17.77%

= 31373100.73

Margin of safety = Profit / contribution per unit

= 5575000 / 40

= 139375

In 2019:

Selling price = 225 +25%

= 281.25

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.