Financial Crisis: Risks, Basel II, Securitization, and Northern Rock

VerifiedAdded on 2020/06/06

|15

|5104

|38

Report

AI Summary

This report provides a comprehensive overview of financial crises, examining key risks within financial services and illustrating them with real-life examples. It explores methods to improve a bank's return on equity, including the use of financial leverage. The report details the process of securitization, including its role during recessions and its potential misuse, and explains the key features of Basel II, including its three pillars. Furthermore, it analyzes the role of the Bank of England in banking crises, evaluates balance sheet management's impact on profitability, and offers a detailed description of bank runs, using the Northern Rock case study from September 2007 to illustrate the internal and external reasons that triggered the crisis. The report covers regulatory frameworks, credit markets, and operational work, offering a thorough analysis of financial instability.

FINANCIAL CRISIS

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION ..........................................................................................................................1

1. Key risks in financial services dealing with real life examples..............................................1

2. Numerical illustration how bank's return on equity can be improved....................................3

3. The process of Securitization including a diagram illustration...............................................4

4. The key features of Basel II including three pillars................................................................6

5. Role of the bank of England in banking crisis........................................................................7

6. Quantitative evaluation balance sheet management impact on profitability...........................8

7. Detailed description of bank run and impact its impact on Northern Rock between

September 2007...........................................................................................................................9

8. Internal and external reasons that caused the Northern Rock’s bank run in 2007 and its key

attributes......................................................................................................................................9

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................12

INTRODUCTION ..........................................................................................................................1

1. Key risks in financial services dealing with real life examples..............................................1

2. Numerical illustration how bank's return on equity can be improved....................................3

3. The process of Securitization including a diagram illustration...............................................4

4. The key features of Basel II including three pillars................................................................6

5. Role of the bank of England in banking crisis........................................................................7

6. Quantitative evaluation balance sheet management impact on profitability...........................8

7. Detailed description of bank run and impact its impact on Northern Rock between

September 2007...........................................................................................................................9

8. Internal and external reasons that caused the Northern Rock’s bank run in 2007 and its key

attributes......................................................................................................................................9

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................12

INTRODUCTION

Financial crisis is considered as a situation indicates towards loss and declining stage of

financial position and nominal value. There were types of financial crisis happened in 19th

centuries and 20th century (Karanikolos and et. al., 2013). Financial crisis was associated with the

banking panics, recessions with the banking crisis. This report is overview of financial crises.

Key financial risks, practical based bank's return on equity can be improved are defined in this

context. Basel II and role of Bank of England in order to overcome the financial crisis defined in

this report. Regulatory framework defined subject to credit market and operational work. Bank

run and the impact to the Northern Rock between September 2007 explained in this context.

Both the internal and external reasons caused the Northern Rock's bank run defined in this

context.

1. Key risks in financial services dealing with real life examples

Risk which remain associated with the management and control of financial services are

considered as financial risks. It is important to detect the financial risk to avoid financial

uncertainties and risks (Shiller, 2012). Financial risk services help global economies in order to

resolve international issues, fulfilling the requirements of a worldwide market, providing the

principle of the risk management framework. It assist the global economies to deal with the

financial challenges and financial risks. After facing the financial crisis five major financial risk

indicators were classified by the risk financial services. There are major five factors need to

considered by the financial and banking industries such as

Conduct risk: it is initial requirement for every financial or banking industry to manage

and mitigate conduct risk. This also remain at highest priority around the world with regulation

activeness and resources (Martin, 2011). It is centred the financial industries must behave

according to their financial feasibility. It is essential to conduct the risk and it is considered as a

clear expectation firms and organisations should make over their own working definitions

subject to define the conduct risk. Conduct risk is remain the major reason of debate for financial

experts that which is the good estimation in terms of conducting risk with particular individual's

reasonable approach being another sharp practice.

This also plays a conjunction role in at management level such as middle managers, high

quality management information, back up by internal audit oversight and practically relevant

with the liability and responsibilities.

1

Financial crisis is considered as a situation indicates towards loss and declining stage of

financial position and nominal value. There were types of financial crisis happened in 19th

centuries and 20th century (Karanikolos and et. al., 2013). Financial crisis was associated with the

banking panics, recessions with the banking crisis. This report is overview of financial crises.

Key financial risks, practical based bank's return on equity can be improved are defined in this

context. Basel II and role of Bank of England in order to overcome the financial crisis defined in

this report. Regulatory framework defined subject to credit market and operational work. Bank

run and the impact to the Northern Rock between September 2007 explained in this context.

Both the internal and external reasons caused the Northern Rock's bank run defined in this

context.

1. Key risks in financial services dealing with real life examples

Risk which remain associated with the management and control of financial services are

considered as financial risks. It is important to detect the financial risk to avoid financial

uncertainties and risks (Shiller, 2012). Financial risk services help global economies in order to

resolve international issues, fulfilling the requirements of a worldwide market, providing the

principle of the risk management framework. It assist the global economies to deal with the

financial challenges and financial risks. After facing the financial crisis five major financial risk

indicators were classified by the risk financial services. There are major five factors need to

considered by the financial and banking industries such as

Conduct risk: it is initial requirement for every financial or banking industry to manage

and mitigate conduct risk. This also remain at highest priority around the world with regulation

activeness and resources (Martin, 2011). It is centred the financial industries must behave

according to their financial feasibility. It is essential to conduct the risk and it is considered as a

clear expectation firms and organisations should make over their own working definitions

subject to define the conduct risk. Conduct risk is remain the major reason of debate for financial

experts that which is the good estimation in terms of conducting risk with particular individual's

reasonable approach being another sharp practice.

This also plays a conjunction role in at management level such as middle managers, high

quality management information, back up by internal audit oversight and practically relevant

with the liability and responsibilities.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Person liability: It is considered as a practical reality with the changing trends and

theories (Peters and et. al., 2012). As per theoretical prospective a person can hold the

accountability of routine practice subject to personal liability which stay easier, fast to regulate

aims and objectives of firms and also help in complaint behaviours. This is approach is basically

centralised around senior individuals and used for key personnel to accounts in order to led to the

vast financial crisis. Whilst previous process indicate towards regulators to enforce senior

managers. It was considered as costly exercise subject to money and time. The UK has opted

several decisions and steps towards changing the expectations and requirements for higher level

managements. There is a risk assessment done by the finance managers in respect of financial

uncertainties. UK Prudential Regulation authority Designated investment firms are formed to

deal with the financial risks.

Compensation practices: these practices remain interrelated with both the conduct risk

and personal liabilities (Erkens, Hung and Matos, 2012). It is seen that the practice remain

associated with the changes in reforms and regulators. It is becoming the growing sense subject

to compensation instigated with the helps of financial stability board. Banking conduct and

culture which is a call for comprehensive and sustained reforms.

As per the accumulation of G30 work showcase the downright depth and breadth of work

to address the near universal flaws in banking culture. Reports do not present clear picture

related to good and bad culture and propose future regulation to govern culture.

Data protection: this is one of the blistery topic of debate subject to Data protection

under the European General Data Protection Regulation. This is the main regulation which was

firstly proposed by the European government subject to application of risk policies on residential

of European union. Financial firms need to ensure the financial risks and identify the needs of

clients. Regulations, policies, procedures and controls are made for those who are deemed to be

resident in the European countries. Data protection is one of the major aspect which can not be

avoided by the financial risk reforms and firms (Taylor, 2013). There are chances to loose the

reputation and image by the lack of proper supervision and legislation. To protect the identity

and data of clients to maintain integrity is one of the prime objective of this risk assessment.

Regulatory fatigue: it indicates towards the continues sheer volume, range of changes

and reforming financial services. It is important to avoid the factors remain associated with the

improper. There are some temporary changes done to repair the regulatory bodies, require,

2

theories (Peters and et. al., 2012). As per theoretical prospective a person can hold the

accountability of routine practice subject to personal liability which stay easier, fast to regulate

aims and objectives of firms and also help in complaint behaviours. This is approach is basically

centralised around senior individuals and used for key personnel to accounts in order to led to the

vast financial crisis. Whilst previous process indicate towards regulators to enforce senior

managers. It was considered as costly exercise subject to money and time. The UK has opted

several decisions and steps towards changing the expectations and requirements for higher level

managements. There is a risk assessment done by the finance managers in respect of financial

uncertainties. UK Prudential Regulation authority Designated investment firms are formed to

deal with the financial risks.

Compensation practices: these practices remain interrelated with both the conduct risk

and personal liabilities (Erkens, Hung and Matos, 2012). It is seen that the practice remain

associated with the changes in reforms and regulators. It is becoming the growing sense subject

to compensation instigated with the helps of financial stability board. Banking conduct and

culture which is a call for comprehensive and sustained reforms.

As per the accumulation of G30 work showcase the downright depth and breadth of work

to address the near universal flaws in banking culture. Reports do not present clear picture

related to good and bad culture and propose future regulation to govern culture.

Data protection: this is one of the blistery topic of debate subject to Data protection

under the European General Data Protection Regulation. This is the main regulation which was

firstly proposed by the European government subject to application of risk policies on residential

of European union. Financial firms need to ensure the financial risks and identify the needs of

clients. Regulations, policies, procedures and controls are made for those who are deemed to be

resident in the European countries. Data protection is one of the major aspect which can not be

avoided by the financial risk reforms and firms (Taylor, 2013). There are chances to loose the

reputation and image by the lack of proper supervision and legislation. To protect the identity

and data of clients to maintain integrity is one of the prime objective of this risk assessment.

Regulatory fatigue: it indicates towards the continues sheer volume, range of changes

and reforming financial services. It is important to avoid the factors remain associated with the

improper. There are some temporary changes done to repair the regulatory bodies, require,

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

structural changes. Front end changes are the main skilled resources being employed to

considered practical impact of consultation papers and further policy documents.

2. Numerical illustration how bank's return on equity can be improved

Financial leverages: It is considered as the degree by which a company can calculate the

financial variations such as fixed income, debts, preferred equities and a high degree of financial

leverage (Mera, 2016). High payment interest means that to encompass the financial debts and

the use of method to detect the bottom line of earning profits.

Degree of financial leverage

Financial risk is one of the main aspect which enlarge the scope of financial leverages

and it also effect the profitability and the minority changes in capital and equities (Chor and

Manova, 2012). Financial risk remain associated with the risk of stock holders by increasing in

debts and preferred equities. There is a specific formula is made to calculate the degree of

financial leverage such as:

DFL = percentage change in earnings per share over the percentage change in EBIT. DFL is the

measure of the sensitivity of earning per share. It is important to maintain an optimum level of

percentage of financial leverage.

DFL = Percentage change in EPS or EBIT / Portion change in EBIT – EBIT interest

For example: A Aviva life insurance company has a production sale is £8 million

annually. Variable cost of sales are 40% of the sales and the fixed cost are £3.4 million. The

annual interest expenses was £200000. if the rate of EBIT is by 20% then what would be the

degree of financial leverage of company.

DFL = (£8000000 - £3200000 – £3400000) / (£8000000 - £3200000 – £3400000 -

£200000)

= £1400000 / £1200000 = 1.1667

leverage plays vital role in respect of maintaining the banking competition and stability.

Trade off between banking competition and financial stability is one of the essential element and

subject for the banking and financial institutions. Legislations and rules and guidelines are made

to maintain effectiveness and optimum level of cash flow with in the organisation.

Portfolio Risk competition: this is the method to calculate the potential risk remain

associated with the portfolio risk and competition. Three type of major active agents remain

3

considered practical impact of consultation papers and further policy documents.

2. Numerical illustration how bank's return on equity can be improved

Financial leverages: It is considered as the degree by which a company can calculate the

financial variations such as fixed income, debts, preferred equities and a high degree of financial

leverage (Mera, 2016). High payment interest means that to encompass the financial debts and

the use of method to detect the bottom line of earning profits.

Degree of financial leverage

Financial risk is one of the main aspect which enlarge the scope of financial leverages

and it also effect the profitability and the minority changes in capital and equities (Chor and

Manova, 2012). Financial risk remain associated with the risk of stock holders by increasing in

debts and preferred equities. There is a specific formula is made to calculate the degree of

financial leverage such as:

DFL = percentage change in earnings per share over the percentage change in EBIT. DFL is the

measure of the sensitivity of earning per share. It is important to maintain an optimum level of

percentage of financial leverage.

DFL = Percentage change in EPS or EBIT / Portion change in EBIT – EBIT interest

For example: A Aviva life insurance company has a production sale is £8 million

annually. Variable cost of sales are 40% of the sales and the fixed cost are £3.4 million. The

annual interest expenses was £200000. if the rate of EBIT is by 20% then what would be the

degree of financial leverage of company.

DFL = (£8000000 - £3200000 – £3400000) / (£8000000 - £3200000 – £3400000 -

£200000)

= £1400000 / £1200000 = 1.1667

leverage plays vital role in respect of maintaining the banking competition and stability.

Trade off between banking competition and financial stability is one of the essential element and

subject for the banking and financial institutions. Legislations and rules and guidelines are made

to maintain effectiveness and optimum level of cash flow with in the organisation.

Portfolio Risk competition: this is the method to calculate the potential risk remain

associated with the portfolio risk and competition. Three type of major active agents remain

3

effective such as entrepreneurs, banks and whole sale financiers. Retail depositors are considered

as purely risky projects. It is calculated as per following formula such as:

E(U) = P(x − r) − P 2 / 2b

where P [0, 1]∈ refers to maximising the expected utility.

Bank funding and liquidity risk: bank holds a unit portfolio of loans and financiers. It

is calculated as per following equation such as θ / 1 + λ where long term assets can be attributed

subject to intangible human capital and in monitoring entrepreneurs or adverse selection. Buyers

remain concerned with the banks subject to selling he lemon loans.

Endogenous leverage: this leverage is used to maximise the value of existing share

holders (Fratzscher, 2012). Since the retail deposits remain fixed in supply F and the issuance of

whole sale debt is indicated as D. expected return on capital is calculated as 1 + K. basically this

leverage method helps subject to tax benefits or debts.

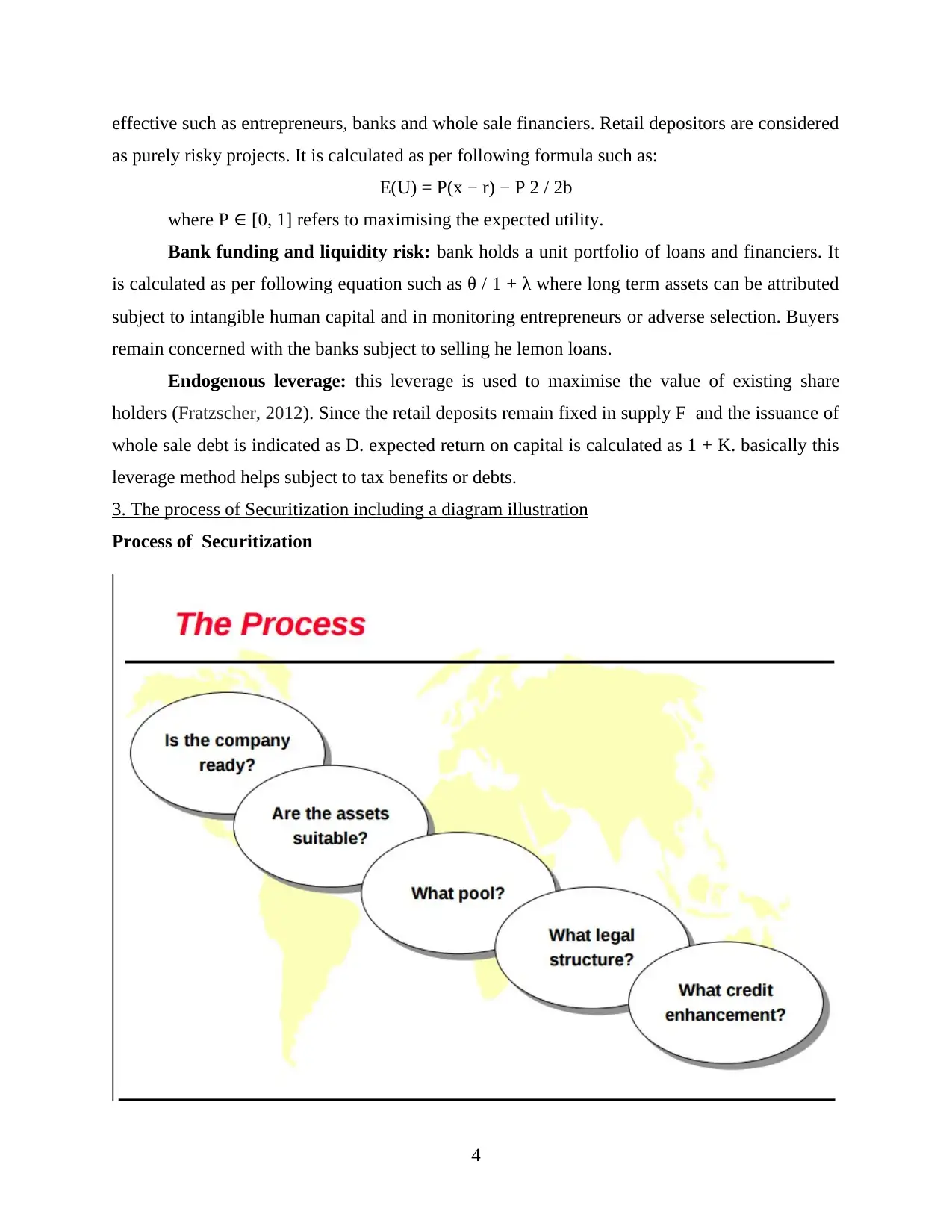

3. The process of Securitization including a diagram illustration

Process of Securitization

4

as purely risky projects. It is calculated as per following formula such as:

E(U) = P(x − r) − P 2 / 2b

where P [0, 1]∈ refers to maximising the expected utility.

Bank funding and liquidity risk: bank holds a unit portfolio of loans and financiers. It

is calculated as per following equation such as θ / 1 + λ where long term assets can be attributed

subject to intangible human capital and in monitoring entrepreneurs or adverse selection. Buyers

remain concerned with the banks subject to selling he lemon loans.

Endogenous leverage: this leverage is used to maximise the value of existing share

holders (Fratzscher, 2012). Since the retail deposits remain fixed in supply F and the issuance of

whole sale debt is indicated as D. expected return on capital is calculated as 1 + K. basically this

leverage method helps subject to tax benefits or debts.

3. The process of Securitization including a diagram illustration

Process of Securitization

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

this is the process of taking an illiquid asset or group of assets and through financial

engineering. There are major factors are taken in to consistence related to transforming into a

security (Aebi, Sabato and Schmid, 2012). The derisive phrase such as “ securitization food

chain”, popularized by the film. “inside job” is made on the basis of 2007-08 financial crisis and

describes the procedure by which groups such illiqued assets.

It is considered as a basic example of securitization is a mortgage – backed security

(MBS). This process is a creation of Larry Fink at first Boston in 1983. there are types of assets

backed security defined in respect of collecting mortgage. There are some standards defined by

which were centralised towards centralising towards transformation of an illiquid assets into a

security. Securitization remain centralised around below major points such as:

Group of consumer loans can be transformed into a publically issued debts security.

Securities which are in terms of trade are underlined in this process.

Loans and receivables risks are optimised subject to securitization of assets at lower risk.

Improving the level of liquidity to enhance the capability and performance of economic

efficiency.

Technique for creating asset- backed securities

lender originates loans to home owner or corporation

there is a structure added in respect of bank or firm sells and assigns certain assets. Such

as consumer receivables to special purpose vehicles.

Role of Securitiziation process during the recession and its misused

this process played vital role subject to take initial decisions subject to Securitize the

assets there decisions were

Form of transfer of assets

Form of special purpose vehicle

Form of credit enhancement

Form of cash flow allocation

Form of transformation of cash flow

there were some essential points were discussed in respect of legal risk and assessment

Certain categories were sorted out for the strategy such as credit risks, liquid risks,

service performance risk, swap counterparty risk, guarantor risk, legal risk, sovereign risk and

interest rate and currency risks (Campello and et. al., 2011). This process was started from the

5

engineering. There are major factors are taken in to consistence related to transforming into a

security (Aebi, Sabato and Schmid, 2012). The derisive phrase such as “ securitization food

chain”, popularized by the film. “inside job” is made on the basis of 2007-08 financial crisis and

describes the procedure by which groups such illiqued assets.

It is considered as a basic example of securitization is a mortgage – backed security

(MBS). This process is a creation of Larry Fink at first Boston in 1983. there are types of assets

backed security defined in respect of collecting mortgage. There are some standards defined by

which were centralised towards centralising towards transformation of an illiquid assets into a

security. Securitization remain centralised around below major points such as:

Group of consumer loans can be transformed into a publically issued debts security.

Securities which are in terms of trade are underlined in this process.

Loans and receivables risks are optimised subject to securitization of assets at lower risk.

Improving the level of liquidity to enhance the capability and performance of economic

efficiency.

Technique for creating asset- backed securities

lender originates loans to home owner or corporation

there is a structure added in respect of bank or firm sells and assigns certain assets. Such

as consumer receivables to special purpose vehicles.

Role of Securitiziation process during the recession and its misused

this process played vital role subject to take initial decisions subject to Securitize the

assets there decisions were

Form of transfer of assets

Form of special purpose vehicle

Form of credit enhancement

Form of cash flow allocation

Form of transformation of cash flow

there were some essential points were discussed in respect of legal risk and assessment

Certain categories were sorted out for the strategy such as credit risks, liquid risks,

service performance risk, swap counterparty risk, guarantor risk, legal risk, sovereign risk and

interest rate and currency risks (Campello and et. al., 2011). This process was started from the

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

forging a securitization food chain. The first step in the chain begins with the simple process of

home or property owners. This process was firstly applied for mortgage at commercial banks.

Loans and mortgages which remain associated with regulated and authorised financial institution

subject to securing loans and claims against the various properties and the mortgages.

4. The key features of Basel II including three pillars

Basel II

this is considered as a second of the Basel accords. There are recommendations on

banking laws and regulations are issued by the Basel committee subject to banking supervision

during finical crisis and recession duration (Covitz,Liang and Suarez, 2013). It was initially

published in June 2004 intended to serve as framework for the international occurrent of

supervision of the banking system. It was the second frame work which was considered as

beneficial subject to resolving the issues. It was issued long period of releasing the Basel I,

which was issued in 1998. this is considered new frame work of setting the first one and the

banking system. The main governance and supervision which was not monitored for the firm

were considered essential. The frame work was made around main three pillars such as

Pillar 1. Minimum capital requirement: this is the main pillar in respect of

miscellaneous reserve and capital. Regulatory capital is considered by the rules which are

adopted by a regulatory agency (Chodorow-Reich, 2013). Capital calculated under generally

accepted accounting principles. It is internally divided in two parts such as Tire 1 which was

related to core capital being the most important and consisting mainly by the share holders. Risk

weighted assets is one of the concept which helps to understand the riskiness and potential for

default. This pillar was centralised around credit risk, operational risk and market risk.

The credit risk components were calculated in three ways degree of sophistication which

are known as standardized approach, IRB foundations and advanced IRB. IRB known as

Internal based approach.

Operational risk is also biased in three parts such as basic approach, standardized

approach and advanced measurement.

In market risk VaR approach is considered preferable approach. Var Stands For Value at

risk.

Pillar 2. Supervisory review: This pillar was formed to deal with the regulatory

response to the first pillar, giving regulators much improved tools over those available under

6

home or property owners. This process was firstly applied for mortgage at commercial banks.

Loans and mortgages which remain associated with regulated and authorised financial institution

subject to securing loans and claims against the various properties and the mortgages.

4. The key features of Basel II including three pillars

Basel II

this is considered as a second of the Basel accords. There are recommendations on

banking laws and regulations are issued by the Basel committee subject to banking supervision

during finical crisis and recession duration (Covitz,Liang and Suarez, 2013). It was initially

published in June 2004 intended to serve as framework for the international occurrent of

supervision of the banking system. It was the second frame work which was considered as

beneficial subject to resolving the issues. It was issued long period of releasing the Basel I,

which was issued in 1998. this is considered new frame work of setting the first one and the

banking system. The main governance and supervision which was not monitored for the firm

were considered essential. The frame work was made around main three pillars such as

Pillar 1. Minimum capital requirement: this is the main pillar in respect of

miscellaneous reserve and capital. Regulatory capital is considered by the rules which are

adopted by a regulatory agency (Chodorow-Reich, 2013). Capital calculated under generally

accepted accounting principles. It is internally divided in two parts such as Tire 1 which was

related to core capital being the most important and consisting mainly by the share holders. Risk

weighted assets is one of the concept which helps to understand the riskiness and potential for

default. This pillar was centralised around credit risk, operational risk and market risk.

The credit risk components were calculated in three ways degree of sophistication which

are known as standardized approach, IRB foundations and advanced IRB. IRB known as

Internal based approach.

Operational risk is also biased in three parts such as basic approach, standardized

approach and advanced measurement.

In market risk VaR approach is considered preferable approach. Var Stands For Value at

risk.

Pillar 2. Supervisory review: This pillar was formed to deal with the regulatory

response to the first pillar, giving regulators much improved tools over those available under

6

Basel I (Milesi-Ferretti, Tille, 2011). It supplies a framework for dealing with all other risks a

bank bear such as reputation risk, liquidity risk and legal risk. The accord merge under the

subject title of Residual risk.

Pillar 3. Market discipline: This pillar is generally used to elaborate the disclosures

related to banks. This pillar was designed to allow the counterparties of the bank to price and

deal with appropriately.

5. Role of the bank of England in banking crisis

Bank of England played vital role subject to tackle the financial crisis during late 2008

and 2009 (Role of Bank of England respond to financial crisis, 2015). as per the reports of Fresh

Scrutiny the review were commissioned in may when the bank remained the only major

institution. At the time of crisis bank court – akin to a board of directors promised that they will

pay close attention to the major problems issues such as intense period of financial crises 2008 –

09. it also includes the collapse of Lehman Brothers from the united states in September 2008.

there was a recapitalisation made of UK banks and the deep global recession. This review was

announced in which it was said that Mooney market operations will be conducted by bill winters.

Bankers were focused upon the macroeconomics management the like of which has never

been tried before (Aloui, Aïssa and Nguyen, 2011). In addition to existing strength interest rates

were also charged in respect of manage the money markets. Bank of England acquire the

responsibilities and liability just to make banking supervision for controlling the credit cycle.

This function is known as macro prudential regulation. As per the detailed analysis the view it

was concluded that bank become more focused as per the lady's command. The contribution of

financial markets helped to achieve the competence of banking plans. Bank newly formed as

financial policy committee. This committee was formed to adjust the supply of credit like water

through a sluice. Bank putted valuable contribution to enhance the structure of economy and

embracing power.

It inspired the confidence of bankers and the members to fight against the major reasons

and the key issues of factors. However the situation was similar as per the Northern Rock. The

minutes was related to flat-Footed by the first bank run in Britain. After putting the valuable

efforts the situations come in control and helped the bank to over come the financial recession.

7

bank bear such as reputation risk, liquidity risk and legal risk. The accord merge under the

subject title of Residual risk.

Pillar 3. Market discipline: This pillar is generally used to elaborate the disclosures

related to banks. This pillar was designed to allow the counterparties of the bank to price and

deal with appropriately.

5. Role of the bank of England in banking crisis

Bank of England played vital role subject to tackle the financial crisis during late 2008

and 2009 (Role of Bank of England respond to financial crisis, 2015). as per the reports of Fresh

Scrutiny the review were commissioned in may when the bank remained the only major

institution. At the time of crisis bank court – akin to a board of directors promised that they will

pay close attention to the major problems issues such as intense period of financial crises 2008 –

09. it also includes the collapse of Lehman Brothers from the united states in September 2008.

there was a recapitalisation made of UK banks and the deep global recession. This review was

announced in which it was said that Mooney market operations will be conducted by bill winters.

Bankers were focused upon the macroeconomics management the like of which has never

been tried before (Aloui, Aïssa and Nguyen, 2011). In addition to existing strength interest rates

were also charged in respect of manage the money markets. Bank of England acquire the

responsibilities and liability just to make banking supervision for controlling the credit cycle.

This function is known as macro prudential regulation. As per the detailed analysis the view it

was concluded that bank become more focused as per the lady's command. The contribution of

financial markets helped to achieve the competence of banking plans. Bank newly formed as

financial policy committee. This committee was formed to adjust the supply of credit like water

through a sluice. Bank putted valuable contribution to enhance the structure of economy and

embracing power.

It inspired the confidence of bankers and the members to fight against the major reasons

and the key issues of factors. However the situation was similar as per the Northern Rock. The

minutes was related to flat-Footed by the first bank run in Britain. After putting the valuable

efforts the situations come in control and helped the bank to over come the financial recession.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6. Quantitative evaluation balance sheet management impact on profitability

There is an critical analysis done for commercial bank in UK. This analysis was divided

in following parts such as:

Internal rate risk measure: this was the major factor for banks to analyse the effect in

respect of economy. There are some obvious effects were found due to the fluctuation in interest

rates and the affect of economy (Demirguc‐Kunt, Detragiache and Merrouche, 2013). As a

whole. It also helps to reduce the effectiveness in respect of long term and short term assets.

There were major changes were centralised around zero sum view. Interest risk were analysed

subject to controlling the regulations.

Gap analysis: this is one of the analysis which helps to find out the critical paths and

gaps to capture the yield curve and basis risk in adequate manner.

Duration of Equity: there is an equation is made to analyse the duration of movements

of interest. Estimated changes and portfolio's value are resulted in respect of small changes in

yield curve. The equation is defined as under:

D = − 1 B · dB dy = Xn i=1 ti · ( cf i · e −y·ti B ) .

where D= duration, b= Bond price, y = Interest rate Ti = Time of cash flow cfi = Cash

flow

Economic value of perspective: this perspective used to analyse the effective analysis

and the bank rates.

7. Detailed description of bank run and impact its impact on Northern Rock between September

2007.

Bank run can be understood as when clients in a huge number withdraws their money

from financial institute because they already gets an idea of chances related to solvency of the

association in near future (Boddy, 2011). In other words, this situation come arises when

consumers of a bank starts pulling out their money as they get to know about some fraudulent

activities are going to take place in short period of time.

In September 2007, because of financial crisis Northern Rock faced ample number of

problems which were related to fund thus, at the same moment Bank of England on 14

September 2007 gave liquidity support. Liquidity is known as when financial institutions

borrows money from central bank for a short period of time so that necessities can be fulfilled

which are related to monitory (Frankel and Saravelos, 2012). But, on the same time this bank

8

There is an critical analysis done for commercial bank in UK. This analysis was divided

in following parts such as:

Internal rate risk measure: this was the major factor for banks to analyse the effect in

respect of economy. There are some obvious effects were found due to the fluctuation in interest

rates and the affect of economy (Demirguc‐Kunt, Detragiache and Merrouche, 2013). As a

whole. It also helps to reduce the effectiveness in respect of long term and short term assets.

There were major changes were centralised around zero sum view. Interest risk were analysed

subject to controlling the regulations.

Gap analysis: this is one of the analysis which helps to find out the critical paths and

gaps to capture the yield curve and basis risk in adequate manner.

Duration of Equity: there is an equation is made to analyse the duration of movements

of interest. Estimated changes and portfolio's value are resulted in respect of small changes in

yield curve. The equation is defined as under:

D = − 1 B · dB dy = Xn i=1 ti · ( cf i · e −y·ti B ) .

where D= duration, b= Bond price, y = Interest rate Ti = Time of cash flow cfi = Cash

flow

Economic value of perspective: this perspective used to analyse the effective analysis

and the bank rates.

7. Detailed description of bank run and impact its impact on Northern Rock between September

2007.

Bank run can be understood as when clients in a huge number withdraws their money

from financial institute because they already gets an idea of chances related to solvency of the

association in near future (Boddy, 2011). In other words, this situation come arises when

consumers of a bank starts pulling out their money as they get to know about some fraudulent

activities are going to take place in short period of time.

In September 2007, because of financial crisis Northern Rock faced ample number of

problems which were related to fund thus, at the same moment Bank of England on 14

September 2007 gave liquidity support. Liquidity is known as when financial institutions

borrows money from central bank for a short period of time so that necessities can be fulfilled

which are related to monitory (Frankel and Saravelos, 2012). But, on the same time this bank

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

faced restrictions which were related to credit supply because they already took huge amount

from market previously. This leaded, thousands of customers of Northern Bank started

withdrawing their savings with the fear of insolvency of the bank in near future.

Here, FSA had to convey the message among public that Northern Rock is in a good

condition and they is nothing to worry about. The information that they gave to people national

in a detailed manner and stated that the issue which Northern Rock is facing is of liquidity and

not of solvency. Many consumers become relieved with the stress of that they are going to loose

their money. In this context, Government of United Kingdom, Bank of England and FSA were

standing in support of Northern Rock which helped them in getting back belief of their clients

and customers.

8. Internal and external reasons that caused the Northern Rock’s bank run in 2007 and its key

attributes

Management of Northern Rock Bank, faced so many issues that led institution towards

failure. Some internal and external factors that caused bank run are as follows:

Internal Reasons:

Fluctuation in leverage of the financial system: as per the analysis it is seen that

traditional bank holds the sort term liabilities from of deposited and used to finance longer term.

There was less liquid assets found in respect of recognising the financial system in that similar

war. With the help of short term liabilities it was able to purchase more assets or could introduce

the borrowing in to capital. Leverage financial firms were in miserable conditions and failed to

provide required help to the bank in monetary firms. It was major internal causes which was

liable to Bank run on Northern bank.

As per the annual report of Northern bank internet and telephone accounts get decreased

up to 1712 million pounds in December 2007 which was 2752 million pounds in December

2006. outflows of wholesale was not in stable situation which was also one of the major reason

of fluctuation of leverage in financial terms.

Risk Management : In financial crisis, managing of risk is the main aim of bankers.

Liquidity risk, which was faced by Northern Rock Bank which led them to ask for funds from

Bank of England (Hunter, Kaufman and Krueger, 2012).

Strategies : Wrong decisions which has been taken by executives took Northern Rock

Bank down at marketplace. Financial crisis created money shortage in pocket of common people

9

from market previously. This leaded, thousands of customers of Northern Bank started

withdrawing their savings with the fear of insolvency of the bank in near future.

Here, FSA had to convey the message among public that Northern Rock is in a good

condition and they is nothing to worry about. The information that they gave to people national

in a detailed manner and stated that the issue which Northern Rock is facing is of liquidity and

not of solvency. Many consumers become relieved with the stress of that they are going to loose

their money. In this context, Government of United Kingdom, Bank of England and FSA were

standing in support of Northern Rock which helped them in getting back belief of their clients

and customers.

8. Internal and external reasons that caused the Northern Rock’s bank run in 2007 and its key

attributes

Management of Northern Rock Bank, faced so many issues that led institution towards

failure. Some internal and external factors that caused bank run are as follows:

Internal Reasons:

Fluctuation in leverage of the financial system: as per the analysis it is seen that

traditional bank holds the sort term liabilities from of deposited and used to finance longer term.

There was less liquid assets found in respect of recognising the financial system in that similar

war. With the help of short term liabilities it was able to purchase more assets or could introduce

the borrowing in to capital. Leverage financial firms were in miserable conditions and failed to

provide required help to the bank in monetary firms. It was major internal causes which was

liable to Bank run on Northern bank.

As per the annual report of Northern bank internet and telephone accounts get decreased

up to 1712 million pounds in December 2007 which was 2752 million pounds in December

2006. outflows of wholesale was not in stable situation which was also one of the major reason

of fluctuation of leverage in financial terms.

Risk Management : In financial crisis, managing of risk is the main aim of bankers.

Liquidity risk, which was faced by Northern Rock Bank which led them to ask for funds from

Bank of England (Hunter, Kaufman and Krueger, 2012).

Strategies : Wrong decisions which has been taken by executives took Northern Rock

Bank down at marketplace. Financial crisis created money shortage in pocket of common people

9

who already took loan from this bank. Thus, they won't became able to return it back right on

time.

External Reasons:

Economic role of short term debt: There was also an opportunity available to avail in

front of the northern bank during the recession period. This was the main aspect which was

tackled by the bank in effective manner. The financial system was restructured in the form of

short term and long term finance and illiquid assets by short term portfolio. The pinch point was

clearly seen by the managers subject to managing the short term and long term assets and

liabilities.

Implications of financial regulations: capital requirements have also been regulated in

terms of financial control. Protecting the rights of clients and protect secure the funds in legal

form was the major criteria fulfilled by bank. As per the guidelines and the regulation there were

some rectification was required in respect of retaining the short term liabilities and equities. Raw

leverage ratio also was the second stage of proposal subject to risk weighted assets. Both the

liquidity regulations and leverage caps played effective role in the northern bank run in 2007.

Lack of confidence of outside world : When consumers of Northern Rock Bank got to

know about condition (Deaton, 2012). First thing that they did was started withdrawing their

deposited money which created shortage of liquidity funds. At this moment, World Bank and

FSA gave some support to this financial institute.

Control Institutions : This includes, governmental agencies, FSA and Bank of England.

These elements put both positive and negative type of impact on events which were related to

Northern Rock Bank (Von Hagen, Schuknecht and Wolswijk, 2011). Government authorities

were not active and was taking decision very slowly at time when world was going through

financial crisis. On the other hand, Bank of England gave full support which were related in

providing regulatory funds to NR Bank. Away from this, FSA created belief in people that the

bank is just facing a normal problem which is going to be resolved soon.

CONCLUSION

This unit is prepared to define the recent financial crisis raised due to various issues

relating to the regulation of the financial system. There were the needs specified in respect of

preventing recurrences of assets bubbles. This report highlight the scenario of financial crisis

during the year of 2007 and 2010. the issues relating to the regulation of the financial systems.

10

time.

External Reasons:

Economic role of short term debt: There was also an opportunity available to avail in

front of the northern bank during the recession period. This was the main aspect which was

tackled by the bank in effective manner. The financial system was restructured in the form of

short term and long term finance and illiquid assets by short term portfolio. The pinch point was

clearly seen by the managers subject to managing the short term and long term assets and

liabilities.

Implications of financial regulations: capital requirements have also been regulated in

terms of financial control. Protecting the rights of clients and protect secure the funds in legal

form was the major criteria fulfilled by bank. As per the guidelines and the regulation there were

some rectification was required in respect of retaining the short term liabilities and equities. Raw

leverage ratio also was the second stage of proposal subject to risk weighted assets. Both the

liquidity regulations and leverage caps played effective role in the northern bank run in 2007.

Lack of confidence of outside world : When consumers of Northern Rock Bank got to

know about condition (Deaton, 2012). First thing that they did was started withdrawing their

deposited money which created shortage of liquidity funds. At this moment, World Bank and

FSA gave some support to this financial institute.

Control Institutions : This includes, governmental agencies, FSA and Bank of England.

These elements put both positive and negative type of impact on events which were related to

Northern Rock Bank (Von Hagen, Schuknecht and Wolswijk, 2011). Government authorities

were not active and was taking decision very slowly at time when world was going through

financial crisis. On the other hand, Bank of England gave full support which were related in

providing regulatory funds to NR Bank. Away from this, FSA created belief in people that the

bank is just facing a normal problem which is going to be resolved soon.

CONCLUSION

This unit is prepared to define the recent financial crisis raised due to various issues

relating to the regulation of the financial system. There were the needs specified in respect of

preventing recurrences of assets bubbles. This report highlight the scenario of financial crisis

during the year of 2007 and 2010. the issues relating to the regulation of the financial systems.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.