Financial Decision Making: Accounting and Finance Functions, Ratios, and Sources of Finance

VerifiedAdded on 2023/06/11

|14

|3276

|316

AI Summary

This report discusses the accounting and finance functions of Panini Ltd, including financial accounting, management accounting, tax function, and auditing functions. It also covers various ratios such as gross profit margin, operating profit margin, return on capital employed, current ratio, quick ratio, inventory turnover ratio, debtor’s collection period, and creditors collection period. Additionally, it provides sources of finance for business growth and development such as loans and advances, bank overdrafts, firm credit cards, and crowdfunding.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Financial Decision

Making

Making

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Contents

INTRODUCTION...........................................................................................................................4

TASK...............................................................................................................................................4

PART A.......................................................................................................................................4

(a) Accounting Department:........................................................................................................4

(b) Finance department –.............................................................................................................6

Source of Finance for the growth and development of business:................................................6

Part B...........................................................................................................................................8

Gross profit margin –...................................................................................................................8

Operating profit Margin –............................................................................................................8

Return on capital Employed –.....................................................................................................9

Current ratio –............................................................................................................................10

Quick ratio –..............................................................................................................................11

Inventory Turnover Ratio –.......................................................................................................11

Debtor’s collection period –......................................................................................................12

Creditors collection period -......................................................................................................12

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION...........................................................................................................................4

TASK...............................................................................................................................................4

PART A.......................................................................................................................................4

(a) Accounting Department:........................................................................................................4

(b) Finance department –.............................................................................................................6

Source of Finance for the growth and development of business:................................................6

Part B...........................................................................................................................................8

Gross profit margin –...................................................................................................................8

Operating profit Margin –............................................................................................................8

Return on capital Employed –.....................................................................................................9

Current ratio –............................................................................................................................10

Quick ratio –..............................................................................................................................11

Inventory Turnover Ratio –.......................................................................................................11

Debtor’s collection period –......................................................................................................12

Creditors collection period -......................................................................................................12

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION

The term accounting may be defined as the process of recording and summarising the

transactions along with analysing and verifying the results of the reports (Ismoilova and

Sharapova, 2019)

. The transactions are recorded in a chronological order. The main purpose of accounting

is to keep all the transactions and to know the current financial position of an organisation.

There are various steps involved in accounting process. It helps in taking financial decisions

whether to invest more capital or withdraw. It supplements in attainment of organisational

goals. On the other hand, finance may be defined as the management of money in order to

earn more from it by undertaking various activities (Calás and Smircich, 2019). This report

is based on Panini Ltd and covers the information related to responsibilities and duties. In

addition to that it will also calculate various ratios and compares to the previous years and to

show the current position of company and effective recommendations in order to improve

the performance.

TASK

PART A

(a) Accounting Department:

It can also define as the department to retain information of all goods and services that the

organization pays and also make sure that all the company expenditures get paid on time.

(1) Financial Accounting Functions – The department of accounting plays an important role as it

manages various duties such as recording of transactions in order to examine their data for audit

purpose. It can also be used for formulating budgets and reports which may be benefitted in

declining the cost and increase profitability (Zhaokai and Moffitt, 2019)

. Business world is full of uncertainties and it is needed to forecast so they company can

anticipate the changes in their decision making process. Following are some functions of

financial accounting.

Promotes maintain of records – In this function of financial accounting, all the day to day

transactions are recorded in a chronological order. There are various types of transactions

such as sale of goods, purchase of goods/inventory or payment received from creditor.

The term accounting may be defined as the process of recording and summarising the

transactions along with analysing and verifying the results of the reports (Ismoilova and

Sharapova, 2019)

. The transactions are recorded in a chronological order. The main purpose of accounting

is to keep all the transactions and to know the current financial position of an organisation.

There are various steps involved in accounting process. It helps in taking financial decisions

whether to invest more capital or withdraw. It supplements in attainment of organisational

goals. On the other hand, finance may be defined as the management of money in order to

earn more from it by undertaking various activities (Calás and Smircich, 2019). This report

is based on Panini Ltd and covers the information related to responsibilities and duties. In

addition to that it will also calculate various ratios and compares to the previous years and to

show the current position of company and effective recommendations in order to improve

the performance.

TASK

PART A

(a) Accounting Department:

It can also define as the department to retain information of all goods and services that the

organization pays and also make sure that all the company expenditures get paid on time.

(1) Financial Accounting Functions – The department of accounting plays an important role as it

manages various duties such as recording of transactions in order to examine their data for audit

purpose. It can also be used for formulating budgets and reports which may be benefitted in

declining the cost and increase profitability (Zhaokai and Moffitt, 2019)

. Business world is full of uncertainties and it is needed to forecast so they company can

anticipate the changes in their decision making process. Following are some functions of

financial accounting.

Promotes maintain of records – In this function of financial accounting, all the day to day

transactions are recorded in a chronological order. There are various types of transactions

such as sale of goods, purchase of goods/inventory or payment received from creditor.

Promotes attainment of objectives – Under this concept, an accountant collects the data and

interpretate in order to formulate effective strategic policies for the attainment of objectives. If

the policies are effectively formulated, then for a company it becomes easier to accomplish

organisational objectives (Liu, Chen and Zhuo., 2020).

(2) Management Accounting Functions – This function is primarily used for taking correct

decision in an organisation. It includes various stages that involves collection, analysation

and interpreting in order to take right decision. It enables in achieving organisation’s

objectives effectively. Management accounting functions are discussed below.

Planning – It is the first step of management accounting as states that planning is deciding in

advance what to do, when to do and how to do and act as a bridge between the current position

and the desired position (Batashev and Bisultanov., 2021)

Organising activities – It includes organising the activities in a structured manner and

assigning the duties to each individual based on their skills and knowledge.

(3) Tax Function – In order to minimise the risk of taxation it is required to maintain the

necessary data. It also helps in planning the functions, prediction of uncertainties along

with key decision process. Tax management functions are discussed below.

To provide suggestions – It is needed to recommend the company based on its

transactions. Companies don’t exceed the transaction limits if they are not paying

higher taxes.

Report to stakeholders – It is needed to deliver annual report to its stakeholders in

order to show the current performance of the company by comparing to last

year’s financial figures.

(4) Auditing Functions- In order to obtain the accuracy of financial figures, it is needed to audit

all the report of a firm (Kotarba, 2018). The present situation of a firm reflects the accuracy of

financial statements. The functions of auditing are discussed below.

Analysation of accounting structure – The auditing function helps in identification

of timing and essence along with extension of audit. So it is needed to analyse the

accounting figures of an organisation.

interpretate in order to formulate effective strategic policies for the attainment of objectives. If

the policies are effectively formulated, then for a company it becomes easier to accomplish

organisational objectives (Liu, Chen and Zhuo., 2020).

(2) Management Accounting Functions – This function is primarily used for taking correct

decision in an organisation. It includes various stages that involves collection, analysation

and interpreting in order to take right decision. It enables in achieving organisation’s

objectives effectively. Management accounting functions are discussed below.

Planning – It is the first step of management accounting as states that planning is deciding in

advance what to do, when to do and how to do and act as a bridge between the current position

and the desired position (Batashev and Bisultanov., 2021)

Organising activities – It includes organising the activities in a structured manner and

assigning the duties to each individual based on their skills and knowledge.

(3) Tax Function – In order to minimise the risk of taxation it is required to maintain the

necessary data. It also helps in planning the functions, prediction of uncertainties along

with key decision process. Tax management functions are discussed below.

To provide suggestions – It is needed to recommend the company based on its

transactions. Companies don’t exceed the transaction limits if they are not paying

higher taxes.

Report to stakeholders – It is needed to deliver annual report to its stakeholders in

order to show the current performance of the company by comparing to last

year’s financial figures.

(4) Auditing Functions- In order to obtain the accuracy of financial figures, it is needed to audit

all the report of a firm (Kotarba, 2018). The present situation of a firm reflects the accuracy of

financial statements. The functions of auditing are discussed below.

Analysation of accounting structure – The auditing function helps in identification

of timing and essence along with extension of audit. So it is needed to analyse the

accounting figures of an organisation.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Assets Confirmation – It is needed to confirm all the assets of the company by the

auditor. It involves in assessing the value and its possession in company. The

auditor must check if the assets that are shown in balance sheet do exist or not.

(b) Finance department –

This department deals in all the financial statement related issues along with

controlling all the income and expenses so that company do not encounter with

financial crisis.

(1) Investment function – This function involves in showing the relation between

investment and interest rate It is provided with a formula which states amount of

investment minus rate of interest along with the slope of downwards of investment.

Dependency of income level on investor investment – The level of income is

directly relying on the investment of investor. If the investor’s income level is

high, then he invests in high amount but in case of low he will invest in IPO’s and

in interest based securities.

Investment in innovation – If a certain customer invests his earnings in new innovative

technology then he will gain profit in future (Triantis, 2018). As today’s world is full of

advancement that makes life easier. So it has been recommended that the investor should invest

in technology sector in order to earn more profit.

Dividend Functions – The primary function is to distribute the dividend to its

shareholders. When a company earns surplus profit then it distributes those profit in

the form of dividend. Firstly, the company should pay the dividend to preference

shareholders and if surplus then it would be distributed to equity shareholders.

(4) Working capital Functions – It helps in meeting all the short term or day to day

expenses that are needed to operate in s year. It includes various functions such as payment

to debtors or payment of electricity bills etc.

auditor. It involves in assessing the value and its possession in company. The

auditor must check if the assets that are shown in balance sheet do exist or not.

(b) Finance department –

This department deals in all the financial statement related issues along with

controlling all the income and expenses so that company do not encounter with

financial crisis.

(1) Investment function – This function involves in showing the relation between

investment and interest rate It is provided with a formula which states amount of

investment minus rate of interest along with the slope of downwards of investment.

Dependency of income level on investor investment – The level of income is

directly relying on the investment of investor. If the investor’s income level is

high, then he invests in high amount but in case of low he will invest in IPO’s and

in interest based securities.

Investment in innovation – If a certain customer invests his earnings in new innovative

technology then he will gain profit in future (Triantis, 2018). As today’s world is full of

advancement that makes life easier. So it has been recommended that the investor should invest

in technology sector in order to earn more profit.

Dividend Functions – The primary function is to distribute the dividend to its

shareholders. When a company earns surplus profit then it distributes those profit in

the form of dividend. Firstly, the company should pay the dividend to preference

shareholders and if surplus then it would be distributed to equity shareholders.

(4) Working capital Functions – It helps in meeting all the short term or day to day

expenses that are needed to operate in s year. It includes various functions such as payment

to debtors or payment of electricity bills etc.

Source of Finance for the growth and development of business:

1. Loans and Advances: The company usually take a loan from the private banks and

government banks which is helpful for the organization to generate more funds for the

growth and development of the company (Nso, 2020). Every firm or organization take

loan for the company betterment and safety. There are following types of loans and

advances are:

Secured Loans: These type of loans is provided after getting some personnel security

against the loan like property and shares of the business. This problem of assets forfeit

arises if the company is failed to pay the loan amount.

Unsecured Loans: This type of security is more friendly for the borrower because

unsecured loans are not provided against any personnel security.

2. Bank Overdrafts: It is also a important part of source of finance and usually helpful for

short-term finance. Bank overdraft is also refers to company overdrafts. In this bank

account the bank provides a credit limit facility to their customer based on their

relationship with the bank. In the other word, the bank overdraft is an unsecured from of

credit. There are two types of overdrafts are as follows:

Authorised Bank Overdrafts: It is the type of overdraft is permitted by the bank to their

account holder customer. The credit limit of the bank overdraft is set by both the parties

the customer and the bank.

Unauthorised Bank Overdrafts: This overdraft occurs when the account holder spent

more money than the balance available in their account without any permission or mutual

decision.

3. Firm Credit cards: Credit card is the special facility for the customer from the bank and

the also a source of finance which is helpful in short-term borrowings to make a payment

of company expenses like rent, bill and any interest paid against business. Apart from that

it is also important to pay the credit card bills timely.

4. Crowdfunding: It is way of source of finance which include small investment is done by

the large numbers of peoples. Following two types of crowdfunding are:

On the basis of equity: Equity crowdfunding is the popular for company

development in the market as way of reaching the another alternative company

1. Loans and Advances: The company usually take a loan from the private banks and

government banks which is helpful for the organization to generate more funds for the

growth and development of the company (Nso, 2020). Every firm or organization take

loan for the company betterment and safety. There are following types of loans and

advances are:

Secured Loans: These type of loans is provided after getting some personnel security

against the loan like property and shares of the business. This problem of assets forfeit

arises if the company is failed to pay the loan amount.

Unsecured Loans: This type of security is more friendly for the borrower because

unsecured loans are not provided against any personnel security.

2. Bank Overdrafts: It is also a important part of source of finance and usually helpful for

short-term finance. Bank overdraft is also refers to company overdrafts. In this bank

account the bank provides a credit limit facility to their customer based on their

relationship with the bank. In the other word, the bank overdraft is an unsecured from of

credit. There are two types of overdrafts are as follows:

Authorised Bank Overdrafts: It is the type of overdraft is permitted by the bank to their

account holder customer. The credit limit of the bank overdraft is set by both the parties

the customer and the bank.

Unauthorised Bank Overdrafts: This overdraft occurs when the account holder spent

more money than the balance available in their account without any permission or mutual

decision.

3. Firm Credit cards: Credit card is the special facility for the customer from the bank and

the also a source of finance which is helpful in short-term borrowings to make a payment

of company expenses like rent, bill and any interest paid against business. Apart from that

it is also important to pay the credit card bills timely.

4. Crowdfunding: It is way of source of finance which include small investment is done by

the large numbers of peoples. Following two types of crowdfunding are:

On the basis of equity: Equity crowdfunding is the popular for company

development in the market as way of reaching the another alternative company

because it is useful for the new company to increase money even with giving up

authority to risk capital investors.

On the basis of loan: It is a source of finance for the company or firm. New company

is usually raise capital by receiving loans from more investor who are interested to

invest in their company or expect to collect the amount in return with huge interest.

Part B

Gross profit margin –

It shows that what fraction of each dollar does the company saves in their business. It is

calculated by gross profit of by COGS of the firm.

Company’s performance indicator – This ratio is used to indicate the percentage of gross margin

earned by the firm after deducting COGS. This shows the current performance of company.

Comparison of 2018 and 2019 figures

Gross profit margin = Gross Profit / Net sales * 100

Year 2018,

= 3500 / 10000 *100

= 35%

Year 2019,

= 3265 / 11500 *100

= 28.39%

Reason for change – The ratio has changed as compared to 2018 as the company’s performance

is not good. As the company is having high net sales in 2019 but the COGS is also high and this

is the main reason of declining the gross profit of the company.

Recommendation – By analysing all the above figures it was concluded that high cost of goods

sold is the main reason for declining the gross profit of the company. So the company should

authority to risk capital investors.

On the basis of loan: It is a source of finance for the company or firm. New company

is usually raise capital by receiving loans from more investor who are interested to

invest in their company or expect to collect the amount in return with huge interest.

Part B

Gross profit margin –

It shows that what fraction of each dollar does the company saves in their business. It is

calculated by gross profit of by COGS of the firm.

Company’s performance indicator – This ratio is used to indicate the percentage of gross margin

earned by the firm after deducting COGS. This shows the current performance of company.

Comparison of 2018 and 2019 figures

Gross profit margin = Gross Profit / Net sales * 100

Year 2018,

= 3500 / 10000 *100

= 35%

Year 2019,

= 3265 / 11500 *100

= 28.39%

Reason for change – The ratio has changed as compared to 2018 as the company’s performance

is not good. As the company is having high net sales in 2019 but the COGS is also high and this

is the main reason of declining the gross profit of the company.

Recommendation – By analysing all the above figures it was concluded that high cost of goods

sold is the main reason for declining the gross profit of the company. So the company should

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

reduce its cost by optimally using the resources and eliminates the waste of resources in order to

increase gross profit.

Operating profit Margin –

This profit margin is used to calculate the overall profitability from all the activities of a

business. It also calculates the profit that a business makes after deducting wages and cost of

raw material but before paying tax and interest.

This ratio helps in understanding the current situation in terms of profitability and assess whether

the company is enjoying the profit or suffering losses. It also helps in knowing long term

sustainability of the business.

Comparison between 2018 and 2019 figures

Year 2018,

= 2765 / 10000 *100

= 27.65 %

Year 2019,

= 2305 / 11500 *100

= 20.04

Reason for change – As the company has incurred high operating expenses along with low

efficiency in operations, this leads to change the operating ratio between 2018 and 2019.

Recommendation – The company should minimise the operating expenses as it leads to

reduction of profit of the firm. In addition to that it should use its resources in an efficient

manner so that it could elevate the profits of company. Moreover, it will save money and thus

reduces its expenses.

Return on capital Employed –

This helps in determining the capital and profit efficiency of the firm. In other words, it

can be said that how efficiently a company generates profit by using capital.

increase gross profit.

Operating profit Margin –

This profit margin is used to calculate the overall profitability from all the activities of a

business. It also calculates the profit that a business makes after deducting wages and cost of

raw material but before paying tax and interest.

This ratio helps in understanding the current situation in terms of profitability and assess whether

the company is enjoying the profit or suffering losses. It also helps in knowing long term

sustainability of the business.

Comparison between 2018 and 2019 figures

Year 2018,

= 2765 / 10000 *100

= 27.65 %

Year 2019,

= 2305 / 11500 *100

= 20.04

Reason for change – As the company has incurred high operating expenses along with low

efficiency in operations, this leads to change the operating ratio between 2018 and 2019.

Recommendation – The company should minimise the operating expenses as it leads to

reduction of profit of the firm. In addition to that it should use its resources in an efficient

manner so that it could elevate the profits of company. Moreover, it will save money and thus

reduces its expenses.

Return on capital Employed –

This helps in determining the capital and profit efficiency of the firm. In other words, it

can be said that how efficiently a company generates profit by using capital.

This ratio helps in determining the efficiency of capital and how much profit it may able to earn

by the capital. It shows how efficiently uses its capital to earn more profit.

Comparison of 2018 and 2019 figures.

ROCE = Earnings before interest and tax / capital employed

Capital employed = Fixed assets + working capital

Year 2018,

= 2765 / 8755

= 31.58 %

Year 2019,

=2305 / 10211

= 22.57 %

Reason – The main reason is poor utilisation of funds as the company generates very less profit

by its capital due to inefficiency of allocating the fund in an optimum manner. The efficiency of

the company decreases its efficiency in 2019 which leads to lower the return on capital employed

ratio.

Recommendation – The company should work efficiently and make more profit along with

reducing the overall expenses because of that company is earning low profit before interest and

tax. By implementing this suggestion, the company can earn more profit.

Current ratio –

It is also known as liquid ratio and it helps in determining the firm’s capacity in paying

the short term payments which are due within one year. It also shoes the difference between

current assets and current liabilities.

This ration helps in determining the firm’s ability to pay short term obligations which are due in

a year. It also defines the relation between current assets and liabilities.

Comparing the 2018 and 2019 figures.

by the capital. It shows how efficiently uses its capital to earn more profit.

Comparison of 2018 and 2019 figures.

ROCE = Earnings before interest and tax / capital employed

Capital employed = Fixed assets + working capital

Year 2018,

= 2765 / 8755

= 31.58 %

Year 2019,

=2305 / 10211

= 22.57 %

Reason – The main reason is poor utilisation of funds as the company generates very less profit

by its capital due to inefficiency of allocating the fund in an optimum manner. The efficiency of

the company decreases its efficiency in 2019 which leads to lower the return on capital employed

ratio.

Recommendation – The company should work efficiently and make more profit along with

reducing the overall expenses because of that company is earning low profit before interest and

tax. By implementing this suggestion, the company can earn more profit.

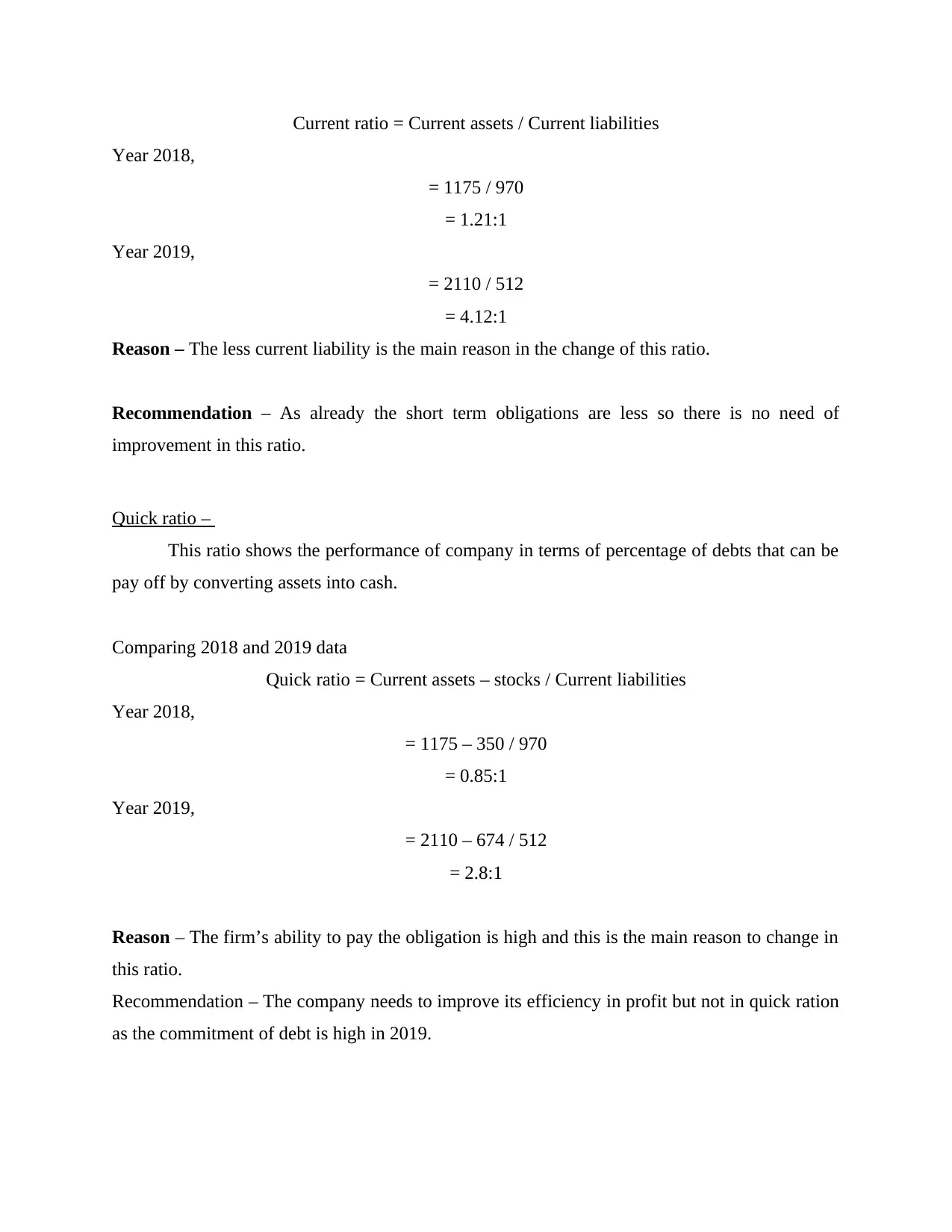

Current ratio –

It is also known as liquid ratio and it helps in determining the firm’s capacity in paying

the short term payments which are due within one year. It also shoes the difference between

current assets and current liabilities.

This ration helps in determining the firm’s ability to pay short term obligations which are due in

a year. It also defines the relation between current assets and liabilities.

Comparing the 2018 and 2019 figures.

Current ratio = Current assets / Current liabilities

Year 2018,

= 1175 / 970

= 1.21:1

Year 2019,

= 2110 / 512

= 4.12:1

Reason – The less current liability is the main reason in the change of this ratio.

Recommendation – As already the short term obligations are less so there is no need of

improvement in this ratio.

Quick ratio –

This ratio shows the performance of company in terms of percentage of debts that can be

pay off by converting assets into cash.

Comparing 2018 and 2019 data

Quick ratio = Current assets – stocks / Current liabilities

Year 2018,

= 1175 – 350 / 970

= 0.85:1

Year 2019,

= 2110 – 674 / 512

= 2.8:1

Reason – The firm’s ability to pay the obligation is high and this is the main reason to change in

this ratio.

Recommendation – The company needs to improve its efficiency in profit but not in quick ration

as the commitment of debt is high in 2019.

Year 2018,

= 1175 / 970

= 1.21:1

Year 2019,

= 2110 / 512

= 4.12:1

Reason – The less current liability is the main reason in the change of this ratio.

Recommendation – As already the short term obligations are less so there is no need of

improvement in this ratio.

Quick ratio –

This ratio shows the performance of company in terms of percentage of debts that can be

pay off by converting assets into cash.

Comparing 2018 and 2019 data

Quick ratio = Current assets – stocks / Current liabilities

Year 2018,

= 1175 – 350 / 970

= 0.85:1

Year 2019,

= 2110 – 674 / 512

= 2.8:1

Reason – The firm’s ability to pay the obligation is high and this is the main reason to change in

this ratio.

Recommendation – The company needs to improve its efficiency in profit but not in quick ration

as the commitment of debt is high in 2019.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Inventory Turnover Ratio –

This ratio helps in determining the company’s performance on the basis of turnover of

inventory. The company having high inventory turnover enjoys high liquidity.

Comparison of 2018 and 2019 figures

Inventory turnover ratio = Cost of goods sold / average inventory

Year 2018,

= 6500 / 512

= 12.6 times

Year 2019,

= 8235 / 512

= 16.08 times

Reason – Due to higher liquidity the changes in ratio are made.

Recommendation – There is no need for improvement as the company is having high liquidity

in 2019. \

Debtor’s collection period –

This ratio helps in calculating the time period of collection of payments from debtors.

Comparing 2018 and 2019 figures

Debtor collection period = 365 / sales on credit / accounts receivable

Year 2018,

= 365 / 10000 / 760

= 27.74 days

Year 2019,

= 365 / 11500 / 1340

= 42.54 days

Reason for change –As year 2019 takes more time for collection of debt, so the difference can

be seen in the ratio.

This ratio helps in determining the company’s performance on the basis of turnover of

inventory. The company having high inventory turnover enjoys high liquidity.

Comparison of 2018 and 2019 figures

Inventory turnover ratio = Cost of goods sold / average inventory

Year 2018,

= 6500 / 512

= 12.6 times

Year 2019,

= 8235 / 512

= 16.08 times

Reason – Due to higher liquidity the changes in ratio are made.

Recommendation – There is no need for improvement as the company is having high liquidity

in 2019. \

Debtor’s collection period –

This ratio helps in calculating the time period of collection of payments from debtors.

Comparing 2018 and 2019 figures

Debtor collection period = 365 / sales on credit / accounts receivable

Year 2018,

= 365 / 10000 / 760

= 27.74 days

Year 2019,

= 365 / 11500 / 1340

= 42.54 days

Reason for change –As year 2019 takes more time for collection of debt, so the difference can

be seen in the ratio.

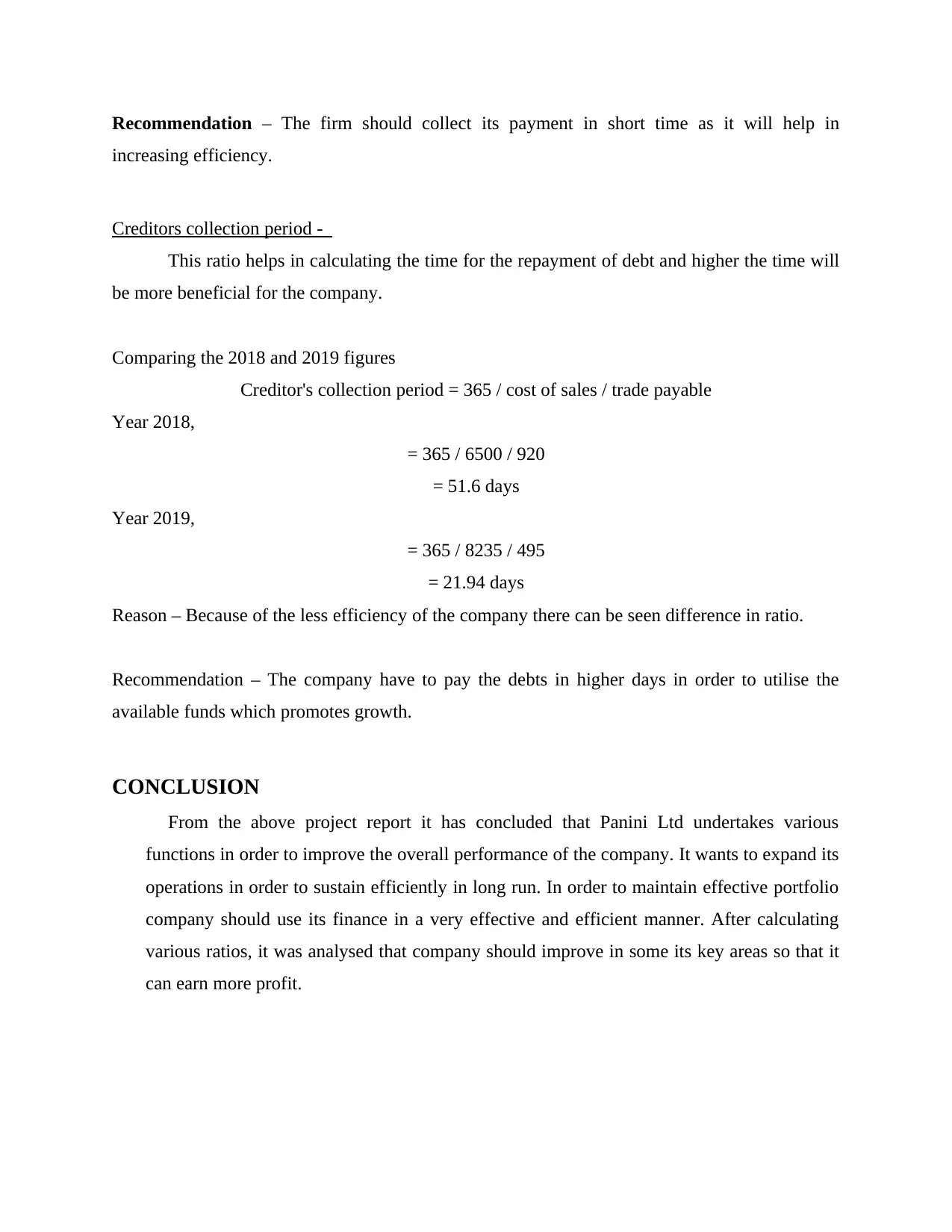

Recommendation – The firm should collect its payment in short time as it will help in

increasing efficiency.

Creditors collection period -

This ratio helps in calculating the time for the repayment of debt and higher the time will

be more beneficial for the company.

Comparing the 2018 and 2019 figures

Creditor's collection period = 365 / cost of sales / trade payable

Year 2018,

= 365 / 6500 / 920

= 51.6 days

Year 2019,

= 365 / 8235 / 495

= 21.94 days

Reason – Because of the less efficiency of the company there can be seen difference in ratio.

Recommendation – The company have to pay the debts in higher days in order to utilise the

available funds which promotes growth.

CONCLUSION

From the above project report it has concluded that Panini Ltd undertakes various

functions in order to improve the overall performance of the company. It wants to expand its

operations in order to sustain efficiently in long run. In order to maintain effective portfolio

company should use its finance in a very effective and efficient manner. After calculating

various ratios, it was analysed that company should improve in some its key areas so that it

can earn more profit.

increasing efficiency.

Creditors collection period -

This ratio helps in calculating the time for the repayment of debt and higher the time will

be more beneficial for the company.

Comparing the 2018 and 2019 figures

Creditor's collection period = 365 / cost of sales / trade payable

Year 2018,

= 365 / 6500 / 920

= 51.6 days

Year 2019,

= 365 / 8235 / 495

= 21.94 days

Reason – Because of the less efficiency of the company there can be seen difference in ratio.

Recommendation – The company have to pay the debts in higher days in order to utilise the

available funds which promotes growth.

CONCLUSION

From the above project report it has concluded that Panini Ltd undertakes various

functions in order to improve the overall performance of the company. It wants to expand its

operations in order to sustain efficiently in long run. In order to maintain effective portfolio

company should use its finance in a very effective and efficient manner. After calculating

various ratios, it was analysed that company should improve in some its key areas so that it

can earn more profit.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Ismoilova, N. and Sharapova, M., 2019. Effective use of financial control in the public finance

management (PFM). International Journal on Economics, Finance and Sustainable

Development, 1(2), pp.8-10.

Calás, M.B. and Smircich, L. eds., 2019. Postmodern management theory. Routledge.

Engelbrecht, L., Yasseen, Y. and Omarjee, I., 2018. The role of the internal audit function in

integrated reporting: A developing economy perspective. Meditari Accountancy Research.

Ashdown, L., 2018. Performance Management: A practical introduction (Vol. 16). Kogan Page

Publishers.

Liu, Y., Chen, X. and Zhuo, W., 2020. Dividends under threshold dividend strategy with

randomized observation periods and capital-exchange agreement. Journal of Computational and

Applied Mathematics, 366, p.112426.

Batashev, R.V. and Bisultanov, A.N., 2021, December. Development of tax administration

principles in the modern conditions. In AIP Conference Proceedings (Vol. 2442, No. 1, p.

050025). AIP Publishing LLC.

Triantis, J.E., 2018. Project finance for business development. John Wiley & Sons.

Nso, M.A., 2020. How Small Businesses can access Finance in a Modern Financial

System?. Advances in Management, 13(1), pp.15-17.

Kotarba, M., 2018. Digital transformation of business models. Foundations of

management, 10(1), pp.123-142.

Zhaokai, Y. and Moffitt, K.C., 2019. Contract analytics in auditing. Accounting horizons, 33(3), pp.111-

126.

Books and Journals

Ismoilova, N. and Sharapova, M., 2019. Effective use of financial control in the public finance

management (PFM). International Journal on Economics, Finance and Sustainable

Development, 1(2), pp.8-10.

Calás, M.B. and Smircich, L. eds., 2019. Postmodern management theory. Routledge.

Engelbrecht, L., Yasseen, Y. and Omarjee, I., 2018. The role of the internal audit function in

integrated reporting: A developing economy perspective. Meditari Accountancy Research.

Ashdown, L., 2018. Performance Management: A practical introduction (Vol. 16). Kogan Page

Publishers.

Liu, Y., Chen, X. and Zhuo, W., 2020. Dividends under threshold dividend strategy with

randomized observation periods and capital-exchange agreement. Journal of Computational and

Applied Mathematics, 366, p.112426.

Batashev, R.V. and Bisultanov, A.N., 2021, December. Development of tax administration

principles in the modern conditions. In AIP Conference Proceedings (Vol. 2442, No. 1, p.

050025). AIP Publishing LLC.

Triantis, J.E., 2018. Project finance for business development. John Wiley & Sons.

Nso, M.A., 2020. How Small Businesses can access Finance in a Modern Financial

System?. Advances in Management, 13(1), pp.15-17.

Kotarba, M., 2018. Digital transformation of business models. Foundations of

management, 10(1), pp.123-142.

Zhaokai, Y. and Moffitt, K.C., 2019. Contract analytics in auditing. Accounting horizons, 33(3), pp.111-

126.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.