Importance of Accounting and Finance Functions in Skanska Plc

VerifiedAdded on 2022/12/27

|12

|3578

|54

AI Summary

This study explores the importance of accounting and finance functions in Skanska Plc, a multinational construction company. It discusses the role of accounting in maintaining records, evaluating business performance, ensuring statutory compliance, budget creation, and financial statement filing. It also highlights the significance of finance in investment decision-making, capital decisions, effective fund utilization, dividend decisions, asset management, estimation of cash flows, negotiations with financiers, and financial performance analysis. The study further includes a ratio analysis of Skanska Plc's financial performance.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

FINANCIAL DECISION-

MAKING

MAKING

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

INTRODUCTION...........................................................................................................................3

Task 1...............................................................................................................................................4

Importance of accounting and finance functions........................................................................4

Importance of finance function...................................................................................................6

Task 2...............................................................................................................................................8

Ratio Analysis.............................................................................................................................8

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION...........................................................................................................................3

Task 1...............................................................................................................................................4

Importance of accounting and finance functions........................................................................4

Importance of finance function...................................................................................................6

Task 2...............................................................................................................................................8

Ratio Analysis.............................................................................................................................8

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION

The study is about accounting and finance functions importance in an organisation named

Skanska Plc. The company Skanska is a multi-national construction company founded in 1984

and having its presence in Nordic region, Europe and USA. It has been ranked as fifth largest

company in the world according to the Construction Global magazine. The ratio analysis of the

company is done through financial statements and a comparison of the company's performance is

done along with causes and reasons discussed for the change in ratios.

Task 1

Importance of accounting and finance functions

Every organisation whether big or small, has given importance to accounting and finance

functions. There are transactions which take place in every organisation and thus it becomes

important for organisations to record those transactions. Thus comes the accountancy function to

play its role. The points for the same can be listed as below:

a) It helps in maintenance of records of transactions happening of the company's products and

services. The cash flow coming and going out of the operational activities can be recorded easily

through accounts and following accounting terms (Syed, 2017). Skanska has many construction

activities going on around the world and thus following a sound accounting policy becomes

necessary to count in the daily transactions happening over raw material, labour and other

activities.

b) It helps in evaluation of business performance. The investors can see the accounts to judge the

standing of the company financially. This also gives an insight into the working capital, its

current assets, liabilities thus focusing on the operational aspect of the company. Investor is able

to assess the liquidity and solvency of the company. The expenses of the company can also be

judged with the accounting records (Cockcroft and Russell, 2018). As Skanska is a big company,

the business performance evaluation is required by investors through the annual report generated

of the company. The investors look forward to the financial statements released and thus make a

decision according to the current and past performance.

c) Statutory Compliance: Laws and regulations of accounting terms help ensure compliance and

thus company is saved from penalties in external audit.

The study is about accounting and finance functions importance in an organisation named

Skanska Plc. The company Skanska is a multi-national construction company founded in 1984

and having its presence in Nordic region, Europe and USA. It has been ranked as fifth largest

company in the world according to the Construction Global magazine. The ratio analysis of the

company is done through financial statements and a comparison of the company's performance is

done along with causes and reasons discussed for the change in ratios.

Task 1

Importance of accounting and finance functions

Every organisation whether big or small, has given importance to accounting and finance

functions. There are transactions which take place in every organisation and thus it becomes

important for organisations to record those transactions. Thus comes the accountancy function to

play its role. The points for the same can be listed as below:

a) It helps in maintenance of records of transactions happening of the company's products and

services. The cash flow coming and going out of the operational activities can be recorded easily

through accounts and following accounting terms (Syed, 2017). Skanska has many construction

activities going on around the world and thus following a sound accounting policy becomes

necessary to count in the daily transactions happening over raw material, labour and other

activities.

b) It helps in evaluation of business performance. The investors can see the accounts to judge the

standing of the company financially. This also gives an insight into the working capital, its

current assets, liabilities thus focusing on the operational aspect of the company. Investor is able

to assess the liquidity and solvency of the company. The expenses of the company can also be

judged with the accounting records (Cockcroft and Russell, 2018). As Skanska is a big company,

the business performance evaluation is required by investors through the annual report generated

of the company. The investors look forward to the financial statements released and thus make a

decision according to the current and past performance.

c) Statutory Compliance: Laws and regulations of accounting terms help ensure compliance and

thus company is saved from penalties in external audit.

Skanska has appointed its own team of internal audit which do the monitoring of

accounting reports and thus save the company from errors in financial statements.

d) Accounting helps in budget creation and projections of the company. The budget creation

helps to assess the right demand of goods and services which can help by giving the data in

production. This will help in saving costs for the company. The accounting measures also helps

in calculation of right amount of inventory (Syed, 2017). Company is saved from extra costs by

ordering the right amount of inventory. Economic order of quantity achieved through

management accounting can help organisation order the right amount of inventory. Accounting

also helps in forecasting projections which can help company in decision-making.

e) Financial Statements filing like the business registering with Registrar of Companies can be

done through accounting. The entities or organisations are required to file themselves with stock

exchanges with tax filing purposes.

f) Legal hassles are avoided by following accounting rules properly. If a minor detail is left out it

can have an effect financially as well as legally. The tax matters are also looked after so that tax

matters do not arise.

g) Performance analysis: The company can look at the records of assets and liabilities and judge

the performance in financial terms of the company.

h) External communication: Communication of financial information with external parties is

made simple by accounting. The accounting reports can be helpful in influencing in getting loan

from banks as they assess the reports and then decide on the amount of loan (Cockcroft and

Russell, 2018).

The accounting statements reflecting profits are useful for investors to make the right

investment decisions.

I) Internal communication: The financial reporting helps owners to communicate with internal

stakeholders. The information is helpful for employees who own stake in the company and also

get dividends as investors. This record helps in communicating strengths and weaknesses of the

company to the internal stakeholders of the company and used for internal purposes.

accounting reports and thus save the company from errors in financial statements.

d) Accounting helps in budget creation and projections of the company. The budget creation

helps to assess the right demand of goods and services which can help by giving the data in

production. This will help in saving costs for the company. The accounting measures also helps

in calculation of right amount of inventory (Syed, 2017). Company is saved from extra costs by

ordering the right amount of inventory. Economic order of quantity achieved through

management accounting can help organisation order the right amount of inventory. Accounting

also helps in forecasting projections which can help company in decision-making.

e) Financial Statements filing like the business registering with Registrar of Companies can be

done through accounting. The entities or organisations are required to file themselves with stock

exchanges with tax filing purposes.

f) Legal hassles are avoided by following accounting rules properly. If a minor detail is left out it

can have an effect financially as well as legally. The tax matters are also looked after so that tax

matters do not arise.

g) Performance analysis: The company can look at the records of assets and liabilities and judge

the performance in financial terms of the company.

h) External communication: Communication of financial information with external parties is

made simple by accounting. The accounting reports can be helpful in influencing in getting loan

from banks as they assess the reports and then decide on the amount of loan (Cockcroft and

Russell, 2018).

The accounting statements reflecting profits are useful for investors to make the right

investment decisions.

I) Internal communication: The financial reporting helps owners to communicate with internal

stakeholders. The information is helpful for employees who own stake in the company and also

get dividends as investors. This record helps in communicating strengths and weaknesses of the

company to the internal stakeholders of the company and used for internal purposes.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Importance of finance function

The importance of finance in any organisation is prominent. The points can be listed as below:

a) Investment decision-making: The company's finance function decides where the company

can get profitability through investment. The decisions related to working capital management,

capital budget decision, buying of assets etc. are able to be taken by finance function. Decision

of investment in projects is also done by financial management tools like net present value and

internal rate of return (Ugoani, 2020). These methods help company in making the better

investment decision in projects by assessing the cash flows in the project which would be more

suitable in profitability.

Skanska being a construction company has projects in line with different investment

portfolios. The company's finance function has to assess the options through financial

management methods and check the profitability of the option. Finance department of the

company has made profitable decisions for buying assets and other machinery too.

b) Capital decisions: The finance function helps realize the capital decisions like raising of

capital, the possession of capital and how much more capital would be required to raise. The

finance function thus helps in calculating the need of capital and requirements to raise capital by

identifying suitable measures through money and capital market means (Conley, Gonçalves and

Hansen, 2018). It can be done by launching of IPO to gain money through public access, issuing

of bonds and scrip or through use of debt measures like loan from creditors or banks. Thus, the

finance function has to identify which mode would be best to choose which balances the

leverage as well as the working capital of the company.

Skanska Plc has a sound finance function which lists down ways which would suit the

company's financial and operating leverage . The fund sources are compared along with their risk

factors and the costs involved. The best source of financing which suits the business needs of the

organisation are evaluated.

c) Effective utilisation of funds: Finance function monitors how much fund is to be allotted,

how much funds remain spare within the organisation and where to adjust those spare funds. As

Skanska is a construction company, there are projects which can utilise less amount of funds

remaining some funds as spare. These funds can then be adjusted in those projects which are

The importance of finance in any organisation is prominent. The points can be listed as below:

a) Investment decision-making: The company's finance function decides where the company

can get profitability through investment. The decisions related to working capital management,

capital budget decision, buying of assets etc. are able to be taken by finance function. Decision

of investment in projects is also done by financial management tools like net present value and

internal rate of return (Ugoani, 2020). These methods help company in making the better

investment decision in projects by assessing the cash flows in the project which would be more

suitable in profitability.

Skanska being a construction company has projects in line with different investment

portfolios. The company's finance function has to assess the options through financial

management methods and check the profitability of the option. Finance department of the

company has made profitable decisions for buying assets and other machinery too.

b) Capital decisions: The finance function helps realize the capital decisions like raising of

capital, the possession of capital and how much more capital would be required to raise. The

finance function thus helps in calculating the need of capital and requirements to raise capital by

identifying suitable measures through money and capital market means (Conley, Gonçalves and

Hansen, 2018). It can be done by launching of IPO to gain money through public access, issuing

of bonds and scrip or through use of debt measures like loan from creditors or banks. Thus, the

finance function has to identify which mode would be best to choose which balances the

leverage as well as the working capital of the company.

Skanska Plc has a sound finance function which lists down ways which would suit the

company's financial and operating leverage . The fund sources are compared along with their risk

factors and the costs involved. The best source of financing which suits the business needs of the

organisation are evaluated.

c) Effective utilisation of funds: Finance function monitors how much fund is to be allotted,

how much funds remain spare within the organisation and where to adjust those spare funds. As

Skanska is a construction company, there are projects which can utilise less amount of funds

remaining some funds as spare. These funds can then be adjusted in those projects which are

ongoing and require more of funds. Adjustment of funds is also a tool used in fund utilisation by

finance experts of the company.

d) Dividend decisions: The decisions as to how frequent and in how much quantity the cash is

returned to owners comes under dividend decisions. Finance function decides how much balance

is to be retained and how much amount is to be paid as dividends (Ugoani, 2020).

Skanska has many investors and thus the dividend decision has to be taken at time proper

which does not give a waiting time for the investors. The percentage of dividend to be given and

amount to be retained is also decided by the finance function.

e) Determination of asset management: The finance function concerns with the cash flow and

non-cash activities. The function has to find out how much cash is stored in non-liquid assets.

Also the process of maintenance of assets in a cost effective manner is a function of the finance.

Skanska has a number of assets which are non-liquified like machinery which the finance

function has to assess the value. Also costs going in the maintenance of these fixed assets have to

be controlled by them in an effective manner.

f) Estimation of cash flows: The finance manager has the responsibility to ensure adequate cash

flow as per requirement of the company. For smooth operation of the company, this is required.

The cash flow and their sources are identified and estimated by the company (Conley,

Gonçalves and Hansen, 2018).

Skanska has a number of fund sources and they can be creditors, suppliers and other

account receivables. The cash may come right away on supply of goods or it may take some time

. Finance function has to keep in account that cash coming in future has the same value it has in

the present, it may require a need of charging of interest.

h) Negotiations with outside financiers: Finance function has to negotiate to get required finance

on time and a line of credit has to be thought of for example banks or creditors who can lend on

less rate of interest to the organisation. Time has to be given for long term financing.

finance experts of the company.

d) Dividend decisions: The decisions as to how frequent and in how much quantity the cash is

returned to owners comes under dividend decisions. Finance function decides how much balance

is to be retained and how much amount is to be paid as dividends (Ugoani, 2020).

Skanska has many investors and thus the dividend decision has to be taken at time proper

which does not give a waiting time for the investors. The percentage of dividend to be given and

amount to be retained is also decided by the finance function.

e) Determination of asset management: The finance function concerns with the cash flow and

non-cash activities. The function has to find out how much cash is stored in non-liquid assets.

Also the process of maintenance of assets in a cost effective manner is a function of the finance.

Skanska has a number of assets which are non-liquified like machinery which the finance

function has to assess the value. Also costs going in the maintenance of these fixed assets have to

be controlled by them in an effective manner.

f) Estimation of cash flows: The finance manager has the responsibility to ensure adequate cash

flow as per requirement of the company. For smooth operation of the company, this is required.

The cash flow and their sources are identified and estimated by the company (Conley,

Gonçalves and Hansen, 2018).

Skanska has a number of fund sources and they can be creditors, suppliers and other

account receivables. The cash may come right away on supply of goods or it may take some time

. Finance function has to keep in account that cash coming in future has the same value it has in

the present, it may require a need of charging of interest.

h) Negotiations with outside financiers: Finance function has to negotiate to get required finance

on time and a line of credit has to be thought of for example banks or creditors who can lend on

less rate of interest to the organisation. Time has to be given for long term financing.

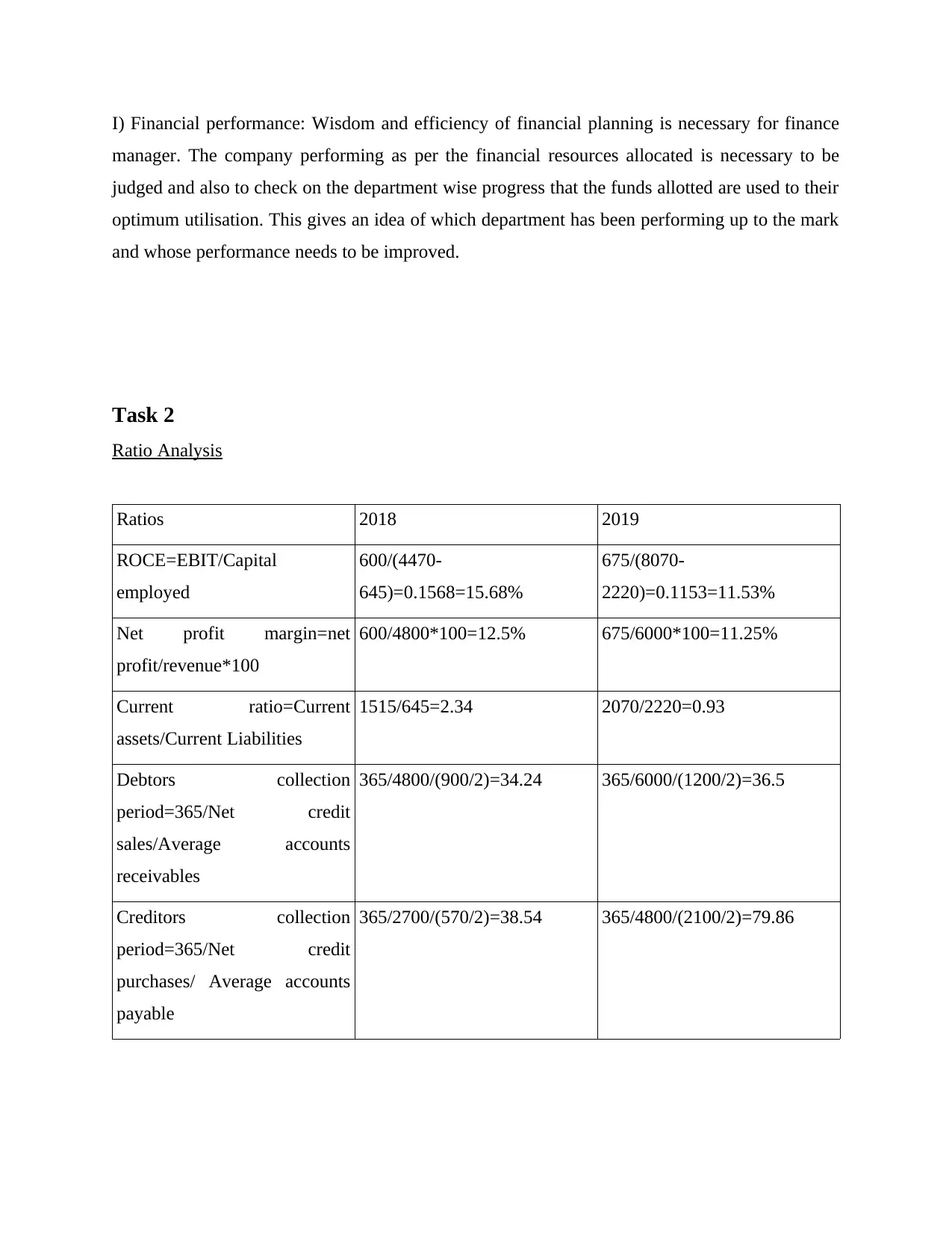

I) Financial performance: Wisdom and efficiency of financial planning is necessary for finance

manager. The company performing as per the financial resources allocated is necessary to be

judged and also to check on the department wise progress that the funds allotted are used to their

optimum utilisation. This gives an idea of which department has been performing up to the mark

and whose performance needs to be improved.

Task 2

Ratio Analysis

Ratios 2018 2019

ROCE=EBIT/Capital

employed

600/(4470-

645)=0.1568=15.68%

675/(8070-

2220)=0.1153=11.53%

Net profit margin=net

profit/revenue*100

600/4800*100=12.5% 675/6000*100=11.25%

Current ratio=Current

assets/Current Liabilities

1515/645=2.34 2070/2220=0.93

Debtors collection

period=365/Net credit

sales/Average accounts

receivables

365/4800/(900/2)=34.24 365/6000/(1200/2)=36.5

Creditors collection

period=365/Net credit

purchases/ Average accounts

payable

365/2700/(570/2)=38.54 365/4800/(2100/2)=79.86

manager. The company performing as per the financial resources allocated is necessary to be

judged and also to check on the department wise progress that the funds allotted are used to their

optimum utilisation. This gives an idea of which department has been performing up to the mark

and whose performance needs to be improved.

Task 2

Ratio Analysis

Ratios 2018 2019

ROCE=EBIT/Capital

employed

600/(4470-

645)=0.1568=15.68%

675/(8070-

2220)=0.1153=11.53%

Net profit margin=net

profit/revenue*100

600/4800*100=12.5% 675/6000*100=11.25%

Current ratio=Current

assets/Current Liabilities

1515/645=2.34 2070/2220=0.93

Debtors collection

period=365/Net credit

sales/Average accounts

receivables

365/4800/(900/2)=34.24 365/6000/(1200/2)=36.5

Creditors collection

period=365/Net credit

purchases/ Average accounts

payable

365/2700/(570/2)=38.54 365/4800/(2100/2)=79.86

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Speaking of ROCE, also meaning Return on Capital employed is a ratio for calculating and

assessing profitability of the company. This is calculated as EBIT divided by capital employed.

EBIT refers to the earnings before income and tax for a company. EBIT also called as

operating income is a metric of assessing how much a company earns from the operations.

Interest and taxes are not regarded here. It can be calculated by subtracting operating and other

expenses plus cost of goods sold from revenue also termed as net profit (Kim and Im, 2017).

Capital employed is the denominator in formula calculated as current liabilities

subtracted from total assets.

In 2018,company registered a ROCE of 15.68% bu this declined to 11.53% in 2019 thus

signifying less return to the company in amount of capital employed. Although, it can be seen

that met profit has increased but it has not been enough to increase the ratio. The total assets

have increased considerably but so have the current liabilities too. The company needs to

increase its operational efficiency with maximum usage of assets to gain more returns. This is

also significant from the investor point of view. Investor is able to know how much is the

company able to generate returns as per the investment.

Net profit margin is calculated as net profit divided by revenue and multiplied by 100. It depicts

how much profit company has been able to convert from the revenue in percentage terms. This is

also essential from the investor's point of view as this is the bottom line they judge as for

investment. This shows how much company has been able to generate operational efficiency by

controlling on the cost of goods as well as the operational expenses (Kim and Im, 2017).

Speaking of the company, company registered a net profit margin of 12.5% in 2018 but it

declined in 2019 to 11.25%. Although the net profit increased for the company but it has not

been able to match up as per sales. Company needs to lessen its operating expenses and decrease

on cost of goods by negotiating with suppliers which can bring the costs down of purchases thus

increasing net profit. Investors also assess whether the company is able to control its operating

costs from this ratio.

assessing profitability of the company. This is calculated as EBIT divided by capital employed.

EBIT refers to the earnings before income and tax for a company. EBIT also called as

operating income is a metric of assessing how much a company earns from the operations.

Interest and taxes are not regarded here. It can be calculated by subtracting operating and other

expenses plus cost of goods sold from revenue also termed as net profit (Kim and Im, 2017).

Capital employed is the denominator in formula calculated as current liabilities

subtracted from total assets.

In 2018,company registered a ROCE of 15.68% bu this declined to 11.53% in 2019 thus

signifying less return to the company in amount of capital employed. Although, it can be seen

that met profit has increased but it has not been enough to increase the ratio. The total assets

have increased considerably but so have the current liabilities too. The company needs to

increase its operational efficiency with maximum usage of assets to gain more returns. This is

also significant from the investor point of view. Investor is able to know how much is the

company able to generate returns as per the investment.

Net profit margin is calculated as net profit divided by revenue and multiplied by 100. It depicts

how much profit company has been able to convert from the revenue in percentage terms. This is

also essential from the investor's point of view as this is the bottom line they judge as for

investment. This shows how much company has been able to generate operational efficiency by

controlling on the cost of goods as well as the operational expenses (Kim and Im, 2017).

Speaking of the company, company registered a net profit margin of 12.5% in 2018 but it

declined in 2019 to 11.25%. Although the net profit increased for the company but it has not

been able to match up as per sales. Company needs to lessen its operating expenses and decrease

on cost of goods by negotiating with suppliers which can bring the costs down of purchases thus

increasing net profit. Investors also assess whether the company is able to control its operating

costs from this ratio.

Current ratio is also known as liquidity ratio. It is got by dividing current assets by current

liabilities.

Current assets are those which can be converted into cash within a period of one year.

They can also be known as short-term assets (Otekunrin and et.al., 2018). They can be in the

form of cash in hand, cash at bank, accounts receivables etc.

Current Liabilities means the short-term obligations the company has to fulfill within a

period of one year. They are account payable and accruals in the form of cash etc.

This ratio shows how quickly the company is in a position to fulfill its short-term

obligations with help of its current assets. If a company has to liquefy its assets how quickly it

will be able to generate money and pay its investors. Investors look for this ratio while doing

investment.

Current ratio registered for 2018 is 2.34 and has declined to 0.93 in 2019. The ideal ratio

considered for current assets is 1:1 that is current assets are equaling its current liabilities.

Although very few companies can have such a ratio, but a ratio between 1 to 3 is preferred by

investors. Company registered such a ratio in 2018 but the ratio fell below 1 in 2019 which is

not a good sign for the company. It is seen that there has been a rise in current assets for the

company which is a good sign but the components which have shown an increase are inventory

and accounts receivable. These two components are not instant cash as they will take time to get

converted into cash. The company's cash in hand has also significantly declined which should

increase as it is the actual liquid asset at the moment. Current liabilities have also shown an

increase significantly of which trade payable is the main component. Company has to however

see that they are paid on time to maintain business relationship with the creditors (Srinivasan,

2018).

The ratio is closer to 1 but needs to be more in current assets quantification to make it an

ideal ratio.

Debtors' collection period is also known as accounts receivable period. Any company while

doing trade with distributors and suppliers can not always get payments instantly. The company

can supply the goods in exchange of invoice for the amount payable by the other party at a later

stage. This period is known as the accounts receivable period. The accounts receivable are

counted in current assets and are likely to fulfill in a short period of time. The debtors collection

liabilities.

Current assets are those which can be converted into cash within a period of one year.

They can also be known as short-term assets (Otekunrin and et.al., 2018). They can be in the

form of cash in hand, cash at bank, accounts receivables etc.

Current Liabilities means the short-term obligations the company has to fulfill within a

period of one year. They are account payable and accruals in the form of cash etc.

This ratio shows how quickly the company is in a position to fulfill its short-term

obligations with help of its current assets. If a company has to liquefy its assets how quickly it

will be able to generate money and pay its investors. Investors look for this ratio while doing

investment.

Current ratio registered for 2018 is 2.34 and has declined to 0.93 in 2019. The ideal ratio

considered for current assets is 1:1 that is current assets are equaling its current liabilities.

Although very few companies can have such a ratio, but a ratio between 1 to 3 is preferred by

investors. Company registered such a ratio in 2018 but the ratio fell below 1 in 2019 which is

not a good sign for the company. It is seen that there has been a rise in current assets for the

company which is a good sign but the components which have shown an increase are inventory

and accounts receivable. These two components are not instant cash as they will take time to get

converted into cash. The company's cash in hand has also significantly declined which should

increase as it is the actual liquid asset at the moment. Current liabilities have also shown an

increase significantly of which trade payable is the main component. Company has to however

see that they are paid on time to maintain business relationship with the creditors (Srinivasan,

2018).

The ratio is closer to 1 but needs to be more in current assets quantification to make it an

ideal ratio.

Debtors' collection period is also known as accounts receivable period. Any company while

doing trade with distributors and suppliers can not always get payments instantly. The company

can supply the goods in exchange of invoice for the amount payable by the other party at a later

stage. This period is known as the accounts receivable period. The accounts receivable are

counted in current assets and are likely to fulfill in a short period of time. The debtors collection

period should not be long as company will need money for operations and time extension can

cause a delay in collection. The ratio is denoted in days.

For 2018, company's collection period was approximately 34 days which has registered a

slight increase to 36 days in 2019. Although the lesser period is there for accounts receivables,

the better it will be for the company's operations. Investors also judge through this ratio that a

company with less of accounts receivable will be more in a position to give back money in case

of liquefaction. Also, this shows company' efficiency to get money back within time period to

have enough money for operations (Otekunrin and et.al., 2018).

Creditors collection period also known as accounts payable period denotes the time

taken by company to give back money taken from its creditors. This is the money taken by

company from creditors for keeping its operations going or additional capital required for setting

up new business plant. This credit time as is said, should be utilized fully by the company to

perform operations and gain revenues. Generally, companies sometime want an extension in this

period for using credit for a longer time but this may not be well for a long-term relation with

creditors. It has to be managed in a way that company utilizes credit period judiciously and pays

back on time its dues so that future assistance can also be taken from the creditors. Also, a long

term credit can pile up interest issues (Srinivasan, 2018).

Speaking of the company, the collection period for creditors was 38 days in 2018 but

increased to 79 days in 2019. Company has to check the ratio to win over creditors' confidence in

the company. The period should not be much high. It can give a negative impression also to the

investors that company is not having sufficient capital to pay back creditors on time.

CONCLUSION

It can be concluded that accounting and finance function are two pillars supporting organization

each in its own way. Their importance can be judged in a large organization more so because of

transactions being more and the number of clients being more. The ratio analysis through

financial statements give an insight in the company's financial standing and is of utmost

importance to investors who are the potential stakeholders of the company.

cause a delay in collection. The ratio is denoted in days.

For 2018, company's collection period was approximately 34 days which has registered a

slight increase to 36 days in 2019. Although the lesser period is there for accounts receivables,

the better it will be for the company's operations. Investors also judge through this ratio that a

company with less of accounts receivable will be more in a position to give back money in case

of liquefaction. Also, this shows company' efficiency to get money back within time period to

have enough money for operations (Otekunrin and et.al., 2018).

Creditors collection period also known as accounts payable period denotes the time

taken by company to give back money taken from its creditors. This is the money taken by

company from creditors for keeping its operations going or additional capital required for setting

up new business plant. This credit time as is said, should be utilized fully by the company to

perform operations and gain revenues. Generally, companies sometime want an extension in this

period for using credit for a longer time but this may not be well for a long-term relation with

creditors. It has to be managed in a way that company utilizes credit period judiciously and pays

back on time its dues so that future assistance can also be taken from the creditors. Also, a long

term credit can pile up interest issues (Srinivasan, 2018).

Speaking of the company, the collection period for creditors was 38 days in 2018 but

increased to 79 days in 2019. Company has to check the ratio to win over creditors' confidence in

the company. The period should not be much high. It can give a negative impression also to the

investors that company is not having sufficient capital to pay back creditors on time.

CONCLUSION

It can be concluded that accounting and finance function are two pillars supporting organization

each in its own way. Their importance can be judged in a large organization more so because of

transactions being more and the number of clients being more. The ratio analysis through

financial statements give an insight in the company's financial standing and is of utmost

importance to investors who are the potential stakeholders of the company.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

REFERENCES

Books and Journals

Benligiray, S. and Ahmet, O.N.A.Y., 2017. Analysis of performance factors for accounting and

finance related business courses in a distance education environment. Turkish Online

Journal of Distance Education. 18(3). pp.16-46.

Boyas, E. and Teeter, R., 2017. Teaching Financial Ratio Analysis using XBRL.

In Developments in Business Simulation and Experiential Learning: Proceedings of the

Annual ABSEL conference (Vol. 44).

Cockcroft, S. and Russell, M., 2018. Big data opportunities for accounting and finance practice

and research. Australian Accounting Review. 28(3).pp.323-333.

Conley, T., Gonçalves, S. and Hansen, C., 2018. Inference with dependent data in accounting

and finance applications. Journal of Accounting Research. 56(4). pp.1139-1203.

Kim, J. and Im, C., 2017. Study on corporate social responsibility (CSR): Focus on tax

avoidance and financial ratio analysis. Sustainability. 9(10). p.1710.

Lazuardi, Y. and Muhtarom, A., 2017. THE EFFECT OF ORGANIZATIONAL CULTURE,

WORK ETHIC, KNOWLEDGE LEVEL OF ACCOUNTING, AND MORAL

HAZARD ON THE QUALITY OF COMPANY’S FINANCIAL REPORT

INFORMATION (The study is accounting and finance employees in the whole national

private company in Gresik). Akuisisi: Jurnal Akuntansi. 13(2).

Mubashir, A. and Bin Tariq, D., 2017. Application of financial ratios as a firm's key performance

and failure indicator: Literature review. Mubashir, Afeera and Bin Tariq, Yasir,

Application of Financial Ratios as a Firm's Key Performance and Failure Indicator:

Literature Review, Journal of Global Economics, Management and Business

Research. 8(1). pp.18-27.

Myšková, R. and Hájek, P., 2017. Comprehensive assessment of firm financial performance

using financial ratios and linguistic analysis of annual reports. Journal of International

Studies, volume 10, issue: 4.

Otekunrin, A.O. and et.al., 2018. Financial Ratio Analysis and Market Price of Share of Selected

Quoted Agriculture and Agro-allied Firms in Nigeria AfterAdoption of International

Books and Journals

Benligiray, S. and Ahmet, O.N.A.Y., 2017. Analysis of performance factors for accounting and

finance related business courses in a distance education environment. Turkish Online

Journal of Distance Education. 18(3). pp.16-46.

Boyas, E. and Teeter, R., 2017. Teaching Financial Ratio Analysis using XBRL.

In Developments in Business Simulation and Experiential Learning: Proceedings of the

Annual ABSEL conference (Vol. 44).

Cockcroft, S. and Russell, M., 2018. Big data opportunities for accounting and finance practice

and research. Australian Accounting Review. 28(3).pp.323-333.

Conley, T., Gonçalves, S. and Hansen, C., 2018. Inference with dependent data in accounting

and finance applications. Journal of Accounting Research. 56(4). pp.1139-1203.

Kim, J. and Im, C., 2017. Study on corporate social responsibility (CSR): Focus on tax

avoidance and financial ratio analysis. Sustainability. 9(10). p.1710.

Lazuardi, Y. and Muhtarom, A., 2017. THE EFFECT OF ORGANIZATIONAL CULTURE,

WORK ETHIC, KNOWLEDGE LEVEL OF ACCOUNTING, AND MORAL

HAZARD ON THE QUALITY OF COMPANY’S FINANCIAL REPORT

INFORMATION (The study is accounting and finance employees in the whole national

private company in Gresik). Akuisisi: Jurnal Akuntansi. 13(2).

Mubashir, A. and Bin Tariq, D., 2017. Application of financial ratios as a firm's key performance

and failure indicator: Literature review. Mubashir, Afeera and Bin Tariq, Yasir,

Application of Financial Ratios as a Firm's Key Performance and Failure Indicator:

Literature Review, Journal of Global Economics, Management and Business

Research. 8(1). pp.18-27.

Myšková, R. and Hájek, P., 2017. Comprehensive assessment of firm financial performance

using financial ratios and linguistic analysis of annual reports. Journal of International

Studies, volume 10, issue: 4.

Otekunrin, A.O. and et.al., 2018. Financial Ratio Analysis and Market Price of Share of Selected

Quoted Agriculture and Agro-allied Firms in Nigeria AfterAdoption of International

Financial Reporting Standard. The Journal of Social Sciences Research. 4(12). pp.736-

744.

Srinivasan, P., 2018. A Study on Financial Ratio Analysis of Vellore Cooperative Sugar Mills at

Ammundi, Vellore. International Journal of Scientific Research in Multidisciplinary

Studies. 4(6). pp.1-18.

Syed, M.Z., 2017. CRITICAL ISSUES IN ACCOUNTING AND FINANCE.

Ugoani, J., 2020. Accounting Function as Management Performance Tool in

Organizations. Business, Management and Economics Research. 6(6). pp.67-74.

744.

Srinivasan, P., 2018. A Study on Financial Ratio Analysis of Vellore Cooperative Sugar Mills at

Ammundi, Vellore. International Journal of Scientific Research in Multidisciplinary

Studies. 4(6). pp.1-18.

Syed, M.Z., 2017. CRITICAL ISSUES IN ACCOUNTING AND FINANCE.

Ugoani, J., 2020. Accounting Function as Management Performance Tool in

Organizations. Business, Management and Economics Research. 6(6). pp.67-74.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.