Financial Decision Making Report

VerifiedAdded on 2020/10/05

|15

|4392

|449

Report

AI Summary

This report on financial decision making provides an in-depth analysis of ABC Consulting LLP's financial performance, including profitability ratios, cash flow statements, and investment appraisal techniques. It highlights the company's strengths and weaknesses across different segments, particularly in the US, UK, and Australia, and discusses various sources of finance and non-financial factors impacting decision making. The report concludes with recommendations for future investments and strategies for improvement.

FINANCIAL

DECISION MAKING

DECISION MAKING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

EXECUTIVE SUMMARY

Financial decision making helps in determining the opportunities which consist of

assessing risks and forecasting same along with legal review. This report is totally based on two

tasks in which first is for analysing its financial performance and in other part, it has elaborated

investment appraisal techniques with funding resources. The present report is giving brief

discussion about its financial performance in context of various financial statements. By

analysing its financial position, its liquidity is not performed well and it has raised expenses of

operations in the year 2017. It is describing proper analysis in context of various segments in

which it is gaining more revenue in US. On its contrary, it was not capable to generate revenue in

Australia and UK with increment in its cost of sales.

Financial decision making helps in determining the opportunities which consist of

assessing risks and forecasting same along with legal review. This report is totally based on two

tasks in which first is for analysing its financial performance and in other part, it has elaborated

investment appraisal techniques with funding resources. The present report is giving brief

discussion about its financial performance in context of various financial statements. By

analysing its financial position, its liquidity is not performed well and it has raised expenses of

operations in the year 2017. It is describing proper analysis in context of various segments in

which it is gaining more revenue in US. On its contrary, it was not capable to generate revenue in

Australia and UK with increment in its cost of sales.

TABLE OF CONTENTS

PART 1 : BUSINESS PERFORMANCE ANALYSIS...................................................................1

Statement of Profit and loss........................................................................................................1

Statement of Financial position...................................................................................................2

Statement of Cash flows.............................................................................................................3

Segmental Analysis.....................................................................................................................5

PART 2 : INVESTMENT APPRAISAL.........................................................................................6

Management Forecast.................................................................................................................6

Investment Appraisal Techniques...............................................................................................7

Payback period...................................................................................................................7

Accounting Rate of return.................................................................................................7

Net Present value...............................................................................................................8

Sources Of Finance.....................................................................................................................9

Non Financial Factors...............................................................................................................10

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

PART 1 : BUSINESS PERFORMANCE ANALYSIS...................................................................1

Statement of Profit and loss........................................................................................................1

Statement of Financial position...................................................................................................2

Statement of Cash flows.............................................................................................................3

Segmental Analysis.....................................................................................................................5

PART 2 : INVESTMENT APPRAISAL.........................................................................................6

Management Forecast.................................................................................................................6

Investment Appraisal Techniques...............................................................................................7

Payback period...................................................................................................................7

Accounting Rate of return.................................................................................................7

Net Present value...............................................................................................................8

Sources Of Finance.....................................................................................................................9

Non Financial Factors...............................................................................................................10

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

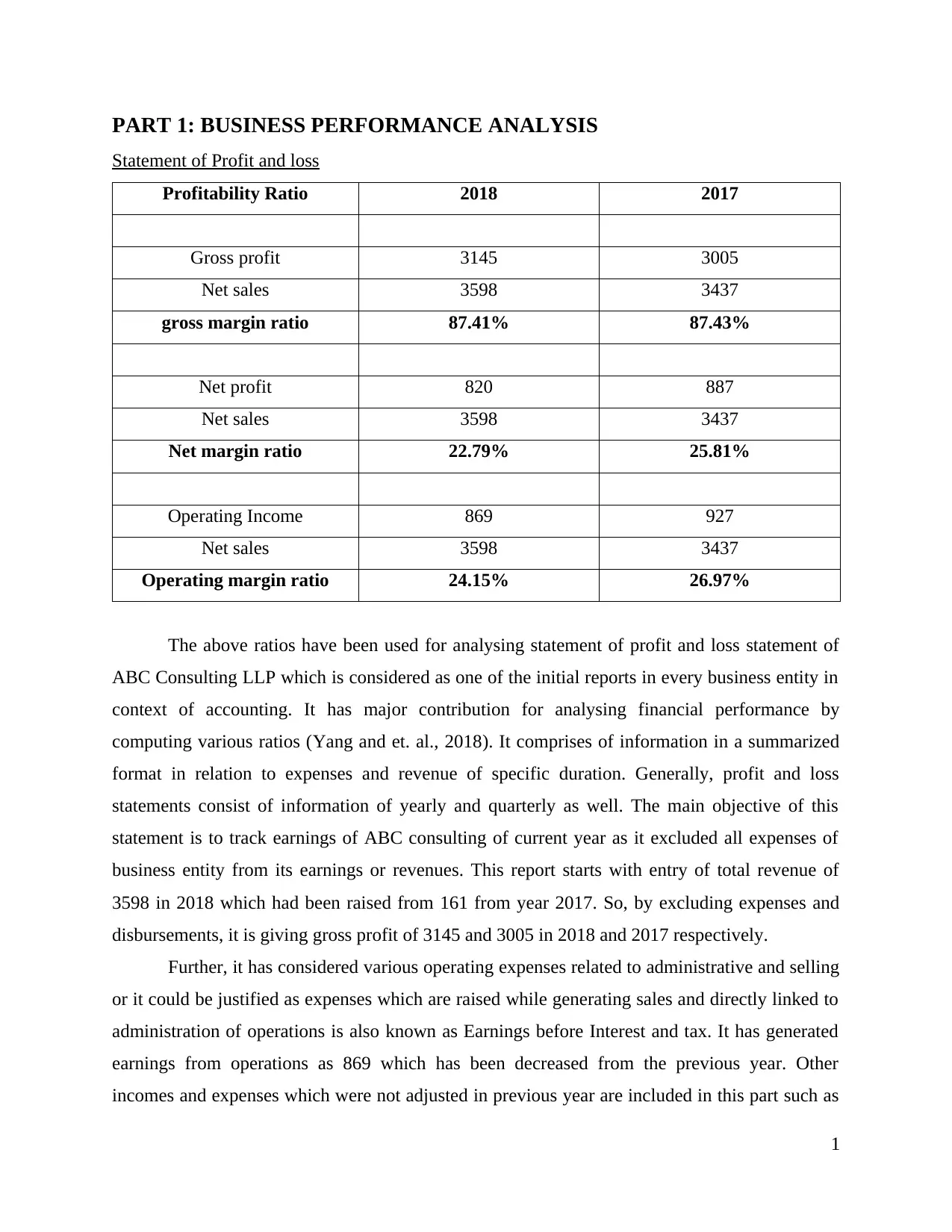

PART 1: BUSINESS PERFORMANCE ANALYSIS

Statement of Profit and loss

Profitability Ratio 2018 2017

Gross profit 3145 3005

Net sales 3598 3437

gross margin ratio 87.41% 87.43%

Net profit 820 887

Net sales 3598 3437

Net margin ratio 22.79% 25.81%

Operating Income 869 927

Net sales 3598 3437

Operating margin ratio 24.15% 26.97%

The above ratios have been used for analysing statement of profit and loss statement of

ABC Consulting LLP which is considered as one of the initial reports in every business entity in

context of accounting. It has major contribution for analysing financial performance by

computing various ratios (Yang and et. al., 2018). It comprises of information in a summarized

format in relation to expenses and revenue of specific duration. Generally, profit and loss

statements consist of information of yearly and quarterly as well. The main objective of this

statement is to track earnings of ABC consulting of current year as it excluded all expenses of

business entity from its earnings or revenues. This report starts with entry of total revenue of

3598 in 2018 which had been raised from 161 from year 2017. So, by excluding expenses and

disbursements, it is giving gross profit of 3145 and 3005 in 2018 and 2017 respectively.

Further, it has considered various operating expenses related to administrative and selling

or it could be justified as expenses which are raised while generating sales and directly linked to

administration of operations is also known as Earnings before Interest and tax. It has generated

earnings from operations as 869 which has been decreased from the previous year. Other

incomes and expenses which were not adjusted in previous year are included in this part such as

1

Statement of Profit and loss

Profitability Ratio 2018 2017

Gross profit 3145 3005

Net sales 3598 3437

gross margin ratio 87.41% 87.43%

Net profit 820 887

Net sales 3598 3437

Net margin ratio 22.79% 25.81%

Operating Income 869 927

Net sales 3598 3437

Operating margin ratio 24.15% 26.97%

The above ratios have been used for analysing statement of profit and loss statement of

ABC Consulting LLP which is considered as one of the initial reports in every business entity in

context of accounting. It has major contribution for analysing financial performance by

computing various ratios (Yang and et. al., 2018). It comprises of information in a summarized

format in relation to expenses and revenue of specific duration. Generally, profit and loss

statements consist of information of yearly and quarterly as well. The main objective of this

statement is to track earnings of ABC consulting of current year as it excluded all expenses of

business entity from its earnings or revenues. This report starts with entry of total revenue of

3598 in 2018 which had been raised from 161 from year 2017. So, by excluding expenses and

disbursements, it is giving gross profit of 3145 and 3005 in 2018 and 2017 respectively.

Further, it has considered various operating expenses related to administrative and selling

or it could be justified as expenses which are raised while generating sales and directly linked to

administration of operations is also known as Earnings before Interest and tax. It has generated

earnings from operations as 869 which has been decreased from the previous year. Other

incomes and expenses which were not adjusted in previous year are included in this part such as

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

taxes, interest, dividends, etc. as it would be giving profit after tax which is also known as Net

income. Generally, ABC consulting has not included Earning per share as it could be computed

by dividing net profit from total shares which are outstanding (Chen and et. al., 2018).

In the same series, it has justified gross profit, net and operating margin ratio. Gross

margin could be illustrated in percentage format which could be computed by dividing gross

profit from net sales. In the year 2017 and 2018, it has given stable outcomes. It is directly

related to the process of product creation. Every business entity keeps desire of high gross

margin if it is increasing the cost of goods which are sold at lower or it raises trade margin. It

indicates the positive effect on net profit of organization.

Statement of Financial position

Financial Ratios 2018 2017

Liquidity ratio

Current Assets 1269 1393

Current liabilities 790 802

Current Ratio 1.61 1.74

Current Assets 1269 1393

Current liabilities 790 802

Working capital 479.00 591.00

Cash and cash equivalents 75 214

Current Liability 790 802

Cash ratio 0.09 0.27

Net profit 820 887

Total Assets 2175 1842

Return on Assets 0.38 0.48

The above ratios have been computed by considering statement of financial position of

ABC Consulting LLP. It could be justified by analysing all liabilities, equity and asset of

organization. Usually, it is framed as proper set of interval such as quarterly, half yearly or

2

income. Generally, ABC consulting has not included Earning per share as it could be computed

by dividing net profit from total shares which are outstanding (Chen and et. al., 2018).

In the same series, it has justified gross profit, net and operating margin ratio. Gross

margin could be illustrated in percentage format which could be computed by dividing gross

profit from net sales. In the year 2017 and 2018, it has given stable outcomes. It is directly

related to the process of product creation. Every business entity keeps desire of high gross

margin if it is increasing the cost of goods which are sold at lower or it raises trade margin. It

indicates the positive effect on net profit of organization.

Statement of Financial position

Financial Ratios 2018 2017

Liquidity ratio

Current Assets 1269 1393

Current liabilities 790 802

Current Ratio 1.61 1.74

Current Assets 1269 1393

Current liabilities 790 802

Working capital 479.00 591.00

Cash and cash equivalents 75 214

Current Liability 790 802

Cash ratio 0.09 0.27

Net profit 820 887

Total Assets 2175 1842

Return on Assets 0.38 0.48

The above ratios have been computed by considering statement of financial position of

ABC Consulting LLP. It could be justified by analysing all liabilities, equity and asset of

organization. Usually, it is framed as proper set of interval such as quarterly, half yearly or

2

annually. Its basic application is to perform proper analysis which derives different actual figures

of organization's asset and liability. The main objective of balance sheet is to verify profitability

of investment perspective for any particular organization as it helps share brokers, financial

institutions, investors and investment bankers (Balance Sheet Ratios, 2013).

At the initial step it includes aggregate of liabilities and equity share capital which had

been paid. By rule, it must match total assets and in Liabilities it does not include shares which

are issued. The financial performance of ABC Consulting would be considered as good because

total assets are exceeding liabilities as it its total assets are 2175 which is greater than 1235

(liabilities). In the same series, it consists of extracting its current liabilities along with asset. It

also helps in computing return with context of asset as it has been performed in above table. It

also consists of giving major concern for patents and copyrights as it considers ratio of amount

which had been invested on its consequent returns. By considering different current assets such

as cash and trade receivables it had been represented as 1269.

With the context of statement of financial position, its liquidity could be measured

through current ratio, cash ratio. The ideal ratio is considered as 2:1 for current ratio as ABC

Consultant LLP is not meeting this standard then its liquidity on basis of current ratio is not

good. In the same series, cash ratio had been computed as it is measuring capability of ABC

Consultant for repaying its current liabilities along with cash and cash equivalents. It is

considered as very restrictive as compared to current and quick ratio due to absence of other

current assets for paying debt but on cash.

It is replicated as very important measure as inventory turnover but this is service

industry so it has lack of inventory otherwise it would be indicating ability of organization for

manufacturing products with availability of assets. In its last step, organization's features had

been analysed which consist of credit ratings, recent projects and goodwill. It would be also

evaluating activities of organization in the future.

Statement of Cash flows

Ratios of Cash flow

Operating cash flow 861

Net sales 3598

23.93%

3

of organization's asset and liability. The main objective of balance sheet is to verify profitability

of investment perspective for any particular organization as it helps share brokers, financial

institutions, investors and investment bankers (Balance Sheet Ratios, 2013).

At the initial step it includes aggregate of liabilities and equity share capital which had

been paid. By rule, it must match total assets and in Liabilities it does not include shares which

are issued. The financial performance of ABC Consulting would be considered as good because

total assets are exceeding liabilities as it its total assets are 2175 which is greater than 1235

(liabilities). In the same series, it consists of extracting its current liabilities along with asset. It

also helps in computing return with context of asset as it has been performed in above table. It

also consists of giving major concern for patents and copyrights as it considers ratio of amount

which had been invested on its consequent returns. By considering different current assets such

as cash and trade receivables it had been represented as 1269.

With the context of statement of financial position, its liquidity could be measured

through current ratio, cash ratio. The ideal ratio is considered as 2:1 for current ratio as ABC

Consultant LLP is not meeting this standard then its liquidity on basis of current ratio is not

good. In the same series, cash ratio had been computed as it is measuring capability of ABC

Consultant for repaying its current liabilities along with cash and cash equivalents. It is

considered as very restrictive as compared to current and quick ratio due to absence of other

current assets for paying debt but on cash.

It is replicated as very important measure as inventory turnover but this is service

industry so it has lack of inventory otherwise it would be indicating ability of organization for

manufacturing products with availability of assets. In its last step, organization's features had

been analysed which consist of credit ratings, recent projects and goodwill. It would be also

evaluating activities of organization in the future.

Statement of Cash flows

Ratios of Cash flow

Operating cash flow 861

Net sales 3598

23.93%

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

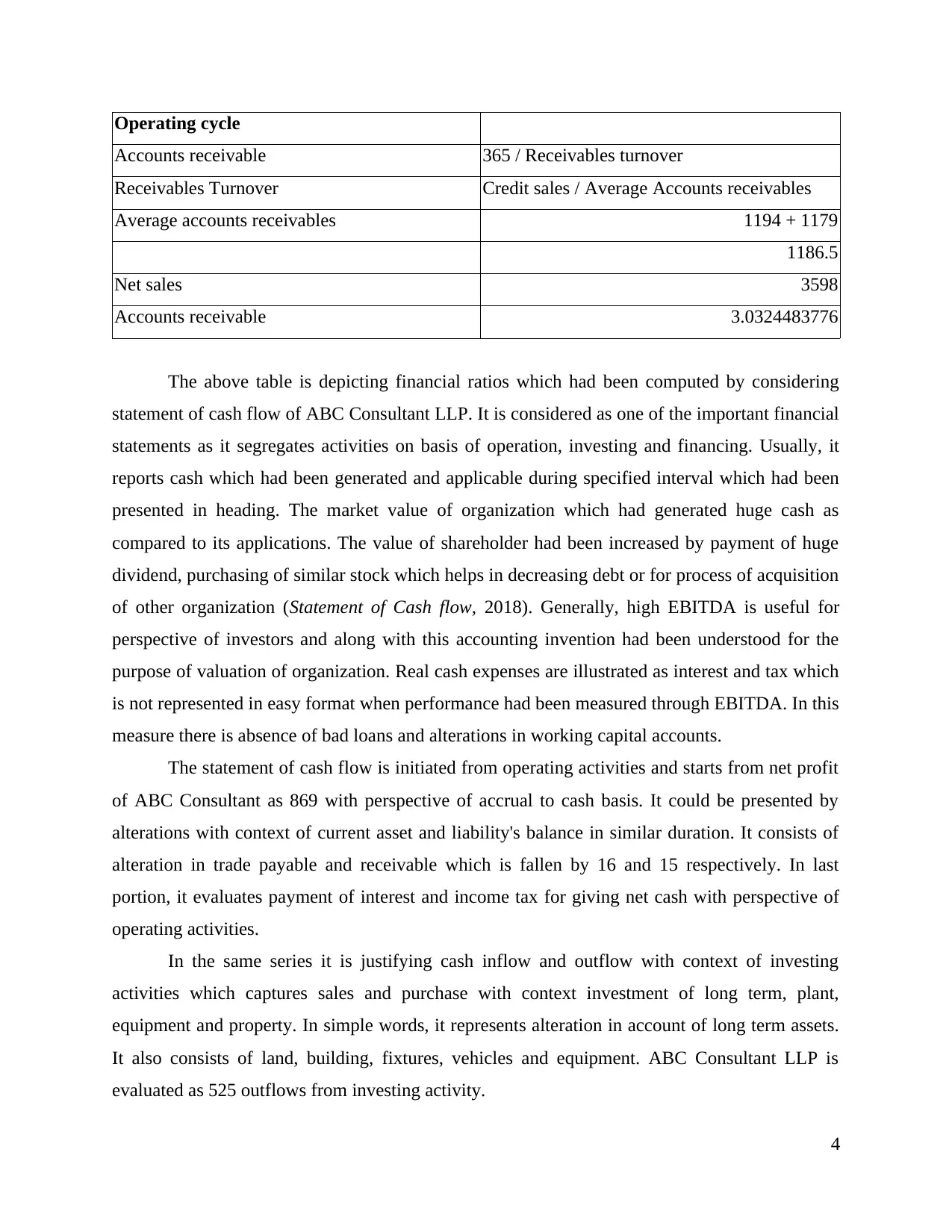

Operating cycle

Accounts receivable 365 / Receivables turnover

Receivables Turnover Credit sales / Average Accounts receivables

Average accounts receivables 1194 + 1179

1186.5

Net sales 3598

Accounts receivable 3.0324483776

The above table is depicting financial ratios which had been computed by considering

statement of cash flow of ABC Consultant LLP. It is considered as one of the important financial

statements as it segregates activities on basis of operation, investing and financing. Usually, it

reports cash which had been generated and applicable during specified interval which had been

presented in heading. The market value of organization which had generated huge cash as

compared to its applications. The value of shareholder had been increased by payment of huge

dividend, purchasing of similar stock which helps in decreasing debt or for process of acquisition

of other organization (Statement of Cash flow, 2018). Generally, high EBITDA is useful for

perspective of investors and along with this accounting invention had been understood for the

purpose of valuation of organization. Real cash expenses are illustrated as interest and tax which

is not represented in easy format when performance had been measured through EBITDA. In this

measure there is absence of bad loans and alterations in working capital accounts.

The statement of cash flow is initiated from operating activities and starts from net profit

of ABC Consultant as 869 with perspective of accrual to cash basis. It could be presented by

alterations with context of current asset and liability's balance in similar duration. It consists of

alteration in trade payable and receivable which is fallen by 16 and 15 respectively. In last

portion, it evaluates payment of interest and income tax for giving net cash with perspective of

operating activities.

In the same series it is justifying cash inflow and outflow with context of investing

activities which captures sales and purchase with context investment of long term, plant,

equipment and property. In simple words, it represents alteration in account of long term assets.

It also consists of land, building, fixtures, vehicles and equipment. ABC Consultant LLP is

evaluated as 525 outflows from investing activity.

4

Accounts receivable 365 / Receivables turnover

Receivables Turnover Credit sales / Average Accounts receivables

Average accounts receivables 1194 + 1179

1186.5

Net sales 3598

Accounts receivable 3.0324483776

The above table is depicting financial ratios which had been computed by considering

statement of cash flow of ABC Consultant LLP. It is considered as one of the important financial

statements as it segregates activities on basis of operation, investing and financing. Usually, it

reports cash which had been generated and applicable during specified interval which had been

presented in heading. The market value of organization which had generated huge cash as

compared to its applications. The value of shareholder had been increased by payment of huge

dividend, purchasing of similar stock which helps in decreasing debt or for process of acquisition

of other organization (Statement of Cash flow, 2018). Generally, high EBITDA is useful for

perspective of investors and along with this accounting invention had been understood for the

purpose of valuation of organization. Real cash expenses are illustrated as interest and tax which

is not represented in easy format when performance had been measured through EBITDA. In this

measure there is absence of bad loans and alterations in working capital accounts.

The statement of cash flow is initiated from operating activities and starts from net profit

of ABC Consultant as 869 with perspective of accrual to cash basis. It could be presented by

alterations with context of current asset and liability's balance in similar duration. It consists of

alteration in trade payable and receivable which is fallen by 16 and 15 respectively. In last

portion, it evaluates payment of interest and income tax for giving net cash with perspective of

operating activities.

In the same series it is justifying cash inflow and outflow with context of investing

activities which captures sales and purchase with context investment of long term, plant,

equipment and property. In simple words, it represents alteration in account of long term assets.

It also consists of land, building, fixtures, vehicles and equipment. ABC Consultant LLP is

evaluated as 525 outflows from investing activity.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Further it is representing cash flow with perspective of financing activity. Generally, it

had various elements such alteration in balance of liability of long term and equity of stockholder

within same duration. It might consist of note payable along with bonds, treasury stock, retained

earnings and common stock. In the cash flow of ABC consultant LLP it had observed that 475

had been out flowed which is combination of Payments to members of 551 and raise of long

term loan by 76 so net cash with perspective of financing activity as 475.

Segmental Analysis

United Kingdom: While analysing segment of UK it had been justified that from year

2016 to 2017 its revenue is increasing along with expenses and disbursements. It is not giving

major impact on net revenue because of increment in cost as well. The company had one

negative point with context of operations as it is not able to control cost of its operations as it is

raising in huge proportion which is directly impacting in earnings from operations. There has

been presence of computation of gross profit and operating margin ratio which measures

profitability of specific segment. The gross margin ratio has been maintained from year 2016 to

2017 as it could be easily viewed. On its contrary, its operation margin was 33.53% in year 2016

which got decreased to 25.63% in next year. Its main reason for decrement is due to increment in

expenses of operations were not controlled which exceeded from previous year (Jetter and

Walker, 2017).

United States: The segment of US could be analysed from year 2016 and 2017 as there

is presence of huge increment in its revenue. There is decrement in expenses and disbursements

which is impacting net revenue by approx. 50%. But on its contrary, its operating expenses are

increasing but with minor percentage. In year 2016 it was not capable to generate margin from

operations but in next year it created huge margin from its operations as 179. It is reflecting

efficiency in US segment due to profit from operations. There has been computation of Gross

margin and operating ratio. The trend of both ratio is increasing which could be easily viewed

from its segmental analysis and observing its operating profit.

Australia: Australian segment is not performing efficient in context of generating sales

as in year 2016 it was 648 but due to some reason it had fallen to 516. On the other perspective,

if there is decrement in sales but then too its expenses and disbursements are increasing which is

depicting negative impact on this particular segment. While consideration of sales and expenses,

its net revenue has major variations in negative aspect from 530 to 390. In the same series,

5

had various elements such alteration in balance of liability of long term and equity of stockholder

within same duration. It might consist of note payable along with bonds, treasury stock, retained

earnings and common stock. In the cash flow of ABC consultant LLP it had observed that 475

had been out flowed which is combination of Payments to members of 551 and raise of long

term loan by 76 so net cash with perspective of financing activity as 475.

Segmental Analysis

United Kingdom: While analysing segment of UK it had been justified that from year

2016 to 2017 its revenue is increasing along with expenses and disbursements. It is not giving

major impact on net revenue because of increment in cost as well. The company had one

negative point with context of operations as it is not able to control cost of its operations as it is

raising in huge proportion which is directly impacting in earnings from operations. There has

been presence of computation of gross profit and operating margin ratio which measures

profitability of specific segment. The gross margin ratio has been maintained from year 2016 to

2017 as it could be easily viewed. On its contrary, its operation margin was 33.53% in year 2016

which got decreased to 25.63% in next year. Its main reason for decrement is due to increment in

expenses of operations were not controlled which exceeded from previous year (Jetter and

Walker, 2017).

United States: The segment of US could be analysed from year 2016 and 2017 as there

is presence of huge increment in its revenue. There is decrement in expenses and disbursements

which is impacting net revenue by approx. 50%. But on its contrary, its operating expenses are

increasing but with minor percentage. In year 2016 it was not capable to generate margin from

operations but in next year it created huge margin from its operations as 179. It is reflecting

efficiency in US segment due to profit from operations. There has been computation of Gross

margin and operating ratio. The trend of both ratio is increasing which could be easily viewed

from its segmental analysis and observing its operating profit.

Australia: Australian segment is not performing efficient in context of generating sales

as in year 2016 it was 648 but due to some reason it had fallen to 516. On the other perspective,

if there is decrement in sales but then too its expenses and disbursements are increasing which is

depicting negative impact on this particular segment. While consideration of sales and expenses,

its net revenue has major variations in negative aspect from 530 to 390. In the same series,

5

organization tried to control cost of its operations as it was succeeded in this segment but

because of prior heading its operating profit had also moved backwards. There has been

computation of gross profit and operating margin ratio which are the best indicator for measuring

profitability. It had represented 70.57 in year 2016 and sudden decrement to 55.13% because of

sales and increment in expenses it was not capable to generate gross earnings. Due to decrement

of sales it gave margin from operation as 39.25% and 28.97% in 2016 and 2017 respectively.

The above segmental analysis had been performed of ABC Consultant LLP of UK, US

and Australia. It could be justified that US is moving on positive trend and rest both are going

backwards. While, consolidating all three segments are affecting whole financial in negative

aspect. Its revenue was decreasing and contrary, it expenses were increasing which is bad sign

for organization. It was not also capable to generate profit from its operations because of

Operations rather than UK which had transformed its financials in very efficient way. In its

consolidation, gross margin in not affected majorly but there was decrement of approx. 3%

which is also depicting negative picture of organization as whole (Charitou, Karamanou and

Kopita, 2017).

PART 2: INVESTMENT APPRAISAL

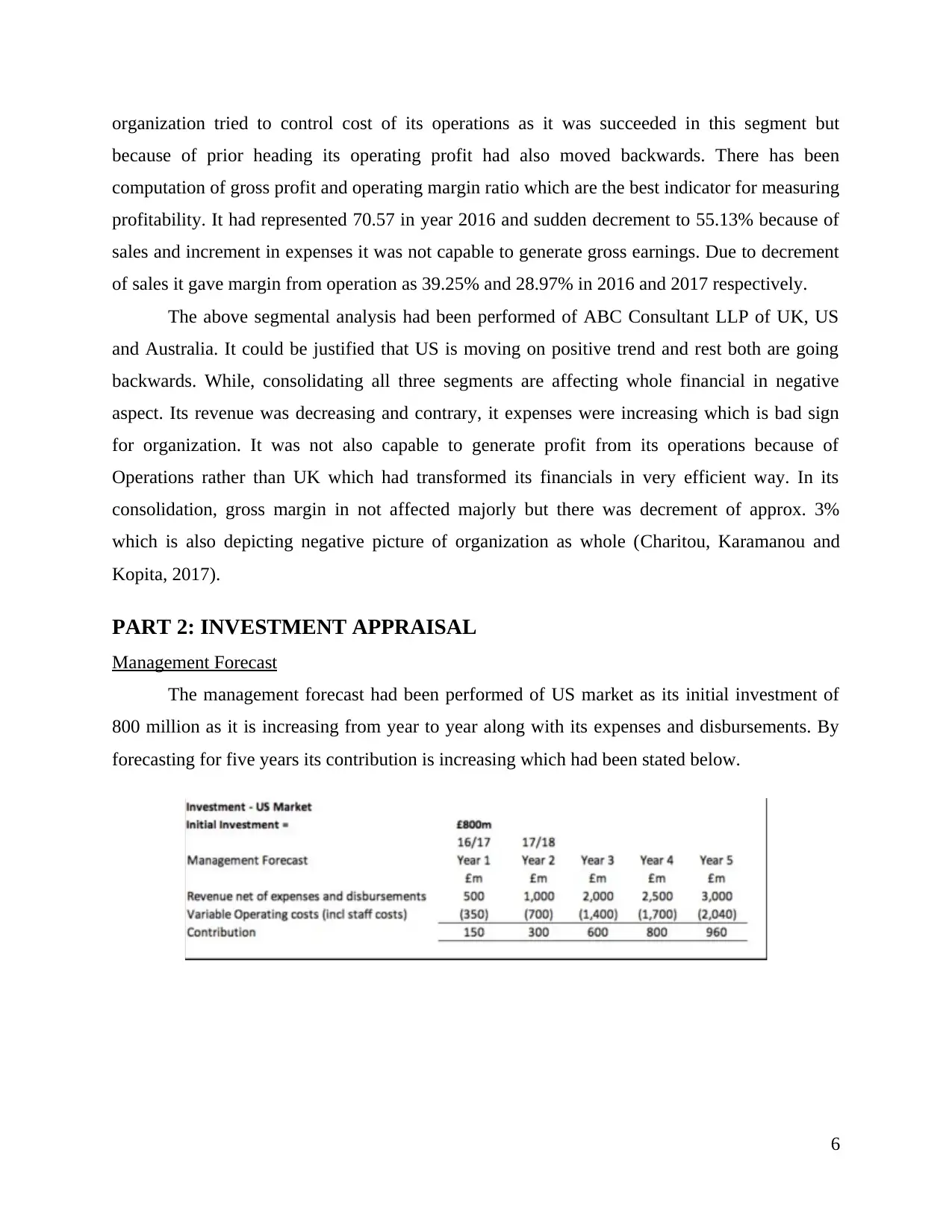

Management Forecast

The management forecast had been performed of US market as its initial investment of

800 million as it is increasing from year to year along with its expenses and disbursements. By

forecasting for five years its contribution is increasing which had been stated below.

6

because of prior heading its operating profit had also moved backwards. There has been

computation of gross profit and operating margin ratio which are the best indicator for measuring

profitability. It had represented 70.57 in year 2016 and sudden decrement to 55.13% because of

sales and increment in expenses it was not capable to generate gross earnings. Due to decrement

of sales it gave margin from operation as 39.25% and 28.97% in 2016 and 2017 respectively.

The above segmental analysis had been performed of ABC Consultant LLP of UK, US

and Australia. It could be justified that US is moving on positive trend and rest both are going

backwards. While, consolidating all three segments are affecting whole financial in negative

aspect. Its revenue was decreasing and contrary, it expenses were increasing which is bad sign

for organization. It was not also capable to generate profit from its operations because of

Operations rather than UK which had transformed its financials in very efficient way. In its

consolidation, gross margin in not affected majorly but there was decrement of approx. 3%

which is also depicting negative picture of organization as whole (Charitou, Karamanou and

Kopita, 2017).

PART 2: INVESTMENT APPRAISAL

Management Forecast

The management forecast had been performed of US market as its initial investment of

800 million as it is increasing from year to year along with its expenses and disbursements. By

forecasting for five years its contribution is increasing which had been stated below.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

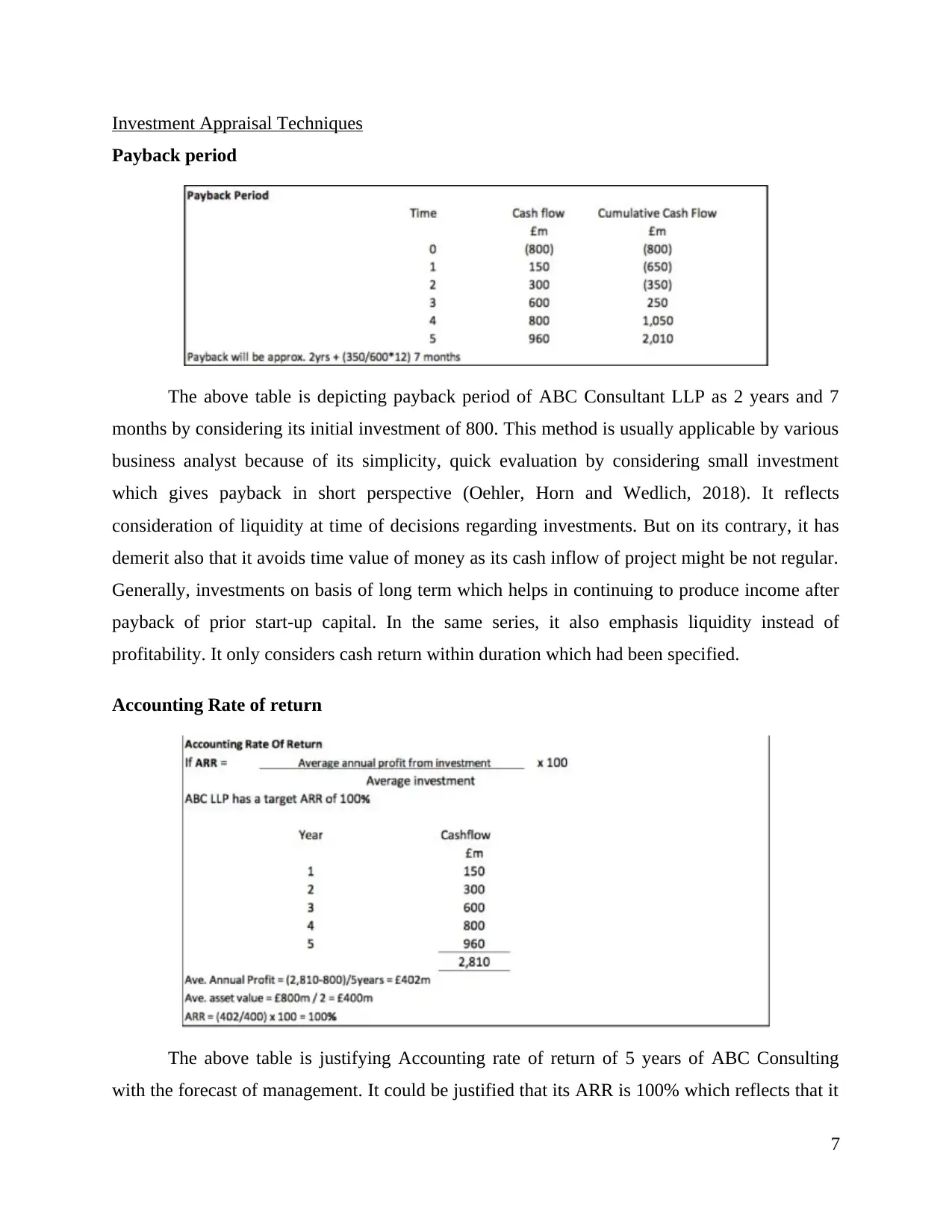

Investment Appraisal Techniques

Payback period

The above table is depicting payback period of ABC Consultant LLP as 2 years and 7

months by considering its initial investment of 800. This method is usually applicable by various

business analyst because of its simplicity, quick evaluation by considering small investment

which gives payback in short perspective (Oehler, Horn and Wedlich, 2018). It reflects

consideration of liquidity at time of decisions regarding investments. But on its contrary, it has

demerit also that it avoids time value of money as its cash inflow of project might be not regular.

Generally, investments on basis of long term which helps in continuing to produce income after

payback of prior start-up capital. In the same series, it also emphasis liquidity instead of

profitability. It only considers cash return within duration which had been specified.

Accounting Rate of return

The above table is justifying Accounting rate of return of 5 years of ABC Consulting

with the forecast of management. It could be justified that its ARR is 100% which reflects that it

7

Payback period

The above table is depicting payback period of ABC Consultant LLP as 2 years and 7

months by considering its initial investment of 800. This method is usually applicable by various

business analyst because of its simplicity, quick evaluation by considering small investment

which gives payback in short perspective (Oehler, Horn and Wedlich, 2018). It reflects

consideration of liquidity at time of decisions regarding investments. But on its contrary, it has

demerit also that it avoids time value of money as its cash inflow of project might be not regular.

Generally, investments on basis of long term which helps in continuing to produce income after

payback of prior start-up capital. In the same series, it also emphasis liquidity instead of

profitability. It only considers cash return within duration which had been specified.

Accounting Rate of return

The above table is justifying Accounting rate of return of 5 years of ABC Consulting

with the forecast of management. It could be justified that its ARR is 100% which reflects that it

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

would be attaining its return in expected way. By considering its merits, it is considered as very

easy for calculating and to understand as well. Usually it evolves total savings and profits over

full duration of economic life of specific project. It also considers concept of net earnings as it is

very vital factor for purpose of proposal of investment. The current performance of organization

had been measured with this method. In the same series, it includes various concept of

accounting related to profit for evaluating rate of return (Alkaraan, 2017).

There is also presence of various limitations in context of Accounting rate of return as its

outcomes are for justifying ROI and it also frames issues with context of decisions. It also

ignores time value of money as its initial weakness with context of this specific method for

selecting its applications of fund on alternative aspect. It also does not evaluate external factors

as it is directly impacting profitability of specific project.If investment project id taken in parts

then this method would not be applicable.

Net Present value

The above table is indicating net present value of ABC LLP by considering cash flow

from management forecast as its initial investment is of 800 million. The discounting factor had

been taken by its cost of capital as 15% as its criteria is of 100% but as per its computation it had

exceeded its target so it should accept this specific proposal. By considering its outcome it

should also imply its merits and demerits. It is directly based with context of time value of

money. It is very easy for finding comparison within various projects as highest value is accepted

for process of implementation. It could also imply to cash flow which is even or uneven pattern.

8

easy for calculating and to understand as well. Usually it evolves total savings and profits over

full duration of economic life of specific project. It also considers concept of net earnings as it is

very vital factor for purpose of proposal of investment. The current performance of organization

had been measured with this method. In the same series, it includes various concept of

accounting related to profit for evaluating rate of return (Alkaraan, 2017).

There is also presence of various limitations in context of Accounting rate of return as its

outcomes are for justifying ROI and it also frames issues with context of decisions. It also

ignores time value of money as its initial weakness with context of this specific method for

selecting its applications of fund on alternative aspect. It also does not evaluate external factors

as it is directly impacting profitability of specific project.If investment project id taken in parts

then this method would not be applicable.

Net Present value

The above table is indicating net present value of ABC LLP by considering cash flow

from management forecast as its initial investment is of 800 million. The discounting factor had

been taken by its cost of capital as 15% as its criteria is of 100% but as per its computation it had

exceeded its target so it should accept this specific proposal. By considering its outcome it

should also imply its merits and demerits. It is directly based with context of time value of

money. It is very easy for finding comparison within various projects as highest value is accepted

for process of implementation. It could also imply to cash flow which is even or uneven pattern.

8

In the same series, it must also consider its disadvantages as it does not represent it

expected rate of return which could be earned (Li and Trutnevyte, 2017). While ranking various

projects it could give contradictory answers because not presence of complications in project. If

there is requirement of investment along with various economic life of specific projects then it

might fail to provide appropriate outcome. There is presence of difficulty for identifying proper

discount rate. Its usage could not be required for gaining knowledge of rate of its cost of capital.

It could not be used if there is absence of cost of capital.

Sources of Finance

ABC consulting LLP is moving with context of expansion with investment in market of

Eastern European for year 2019 of 500 million. There is presence of different sources of finance

could be used such as:

Bank Loans

Equity financing

Government grants and subsidiaries

Business incubators

Bank loan and equity financing could be used by ABC consulting LLP as they are very

effective but it should consider its drawbacks and benefits as well as it might affect there process

of investment decision making.

Bank Loan: It is considered as very easy source for availing fund. It is referred as an

extension for credit with context of bank to business or consumer as it should be paid with

interest. It is replicated as finance for short term perspective. The most special feature could be

elaborated as it might be unsecured or secured which totally depend on circumstances. The

interest which had been charged through bank on specific loan might be variable or fixed.

Merits: It is very flexible in nature if proper instalments are paid on time. It is considered

as benefit over the overdrafts because they should be paid fully. With context of interest rate,

bank loan is considered as very effective and cheapest option as compared to credit cards and

overdrafts. It also provides benefits with reference to tax. If interest had been paid which is

known as expense as of tax deductible (Gordon and et. al., 2017).

Demerits: With the context of bank loan, there is always need of collateral, if business is

existing or start up then it would face difficulty for approval of loan application. Along with this

if borrowers opt for loans which are unsecured then they would face huge rate of interest rate. As

9

expected rate of return which could be earned (Li and Trutnevyte, 2017). While ranking various

projects it could give contradictory answers because not presence of complications in project. If

there is requirement of investment along with various economic life of specific projects then it

might fail to provide appropriate outcome. There is presence of difficulty for identifying proper

discount rate. Its usage could not be required for gaining knowledge of rate of its cost of capital.

It could not be used if there is absence of cost of capital.

Sources of Finance

ABC consulting LLP is moving with context of expansion with investment in market of

Eastern European for year 2019 of 500 million. There is presence of different sources of finance

could be used such as:

Bank Loans

Equity financing

Government grants and subsidiaries

Business incubators

Bank loan and equity financing could be used by ABC consulting LLP as they are very

effective but it should consider its drawbacks and benefits as well as it might affect there process

of investment decision making.

Bank Loan: It is considered as very easy source for availing fund. It is referred as an

extension for credit with context of bank to business or consumer as it should be paid with

interest. It is replicated as finance for short term perspective. The most special feature could be

elaborated as it might be unsecured or secured which totally depend on circumstances. The

interest which had been charged through bank on specific loan might be variable or fixed.

Merits: It is very flexible in nature if proper instalments are paid on time. It is considered

as benefit over the overdrafts because they should be paid fully. With context of interest rate,

bank loan is considered as very effective and cheapest option as compared to credit cards and

overdrafts. It also provides benefits with reference to tax. If interest had been paid which is

known as expense as of tax deductible (Gordon and et. al., 2017).

Demerits: With the context of bank loan, there is always need of collateral, if business is

existing or start up then it would face difficulty for approval of loan application. Along with this

if borrowers opt for loans which are unsecured then they would face huge rate of interest rate. As

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.