Financial Performance Analysis of Alpha Limited: Ratio Calculations

VerifiedAdded on 2023/01/11

|7

|1944

|22

Report

AI Summary

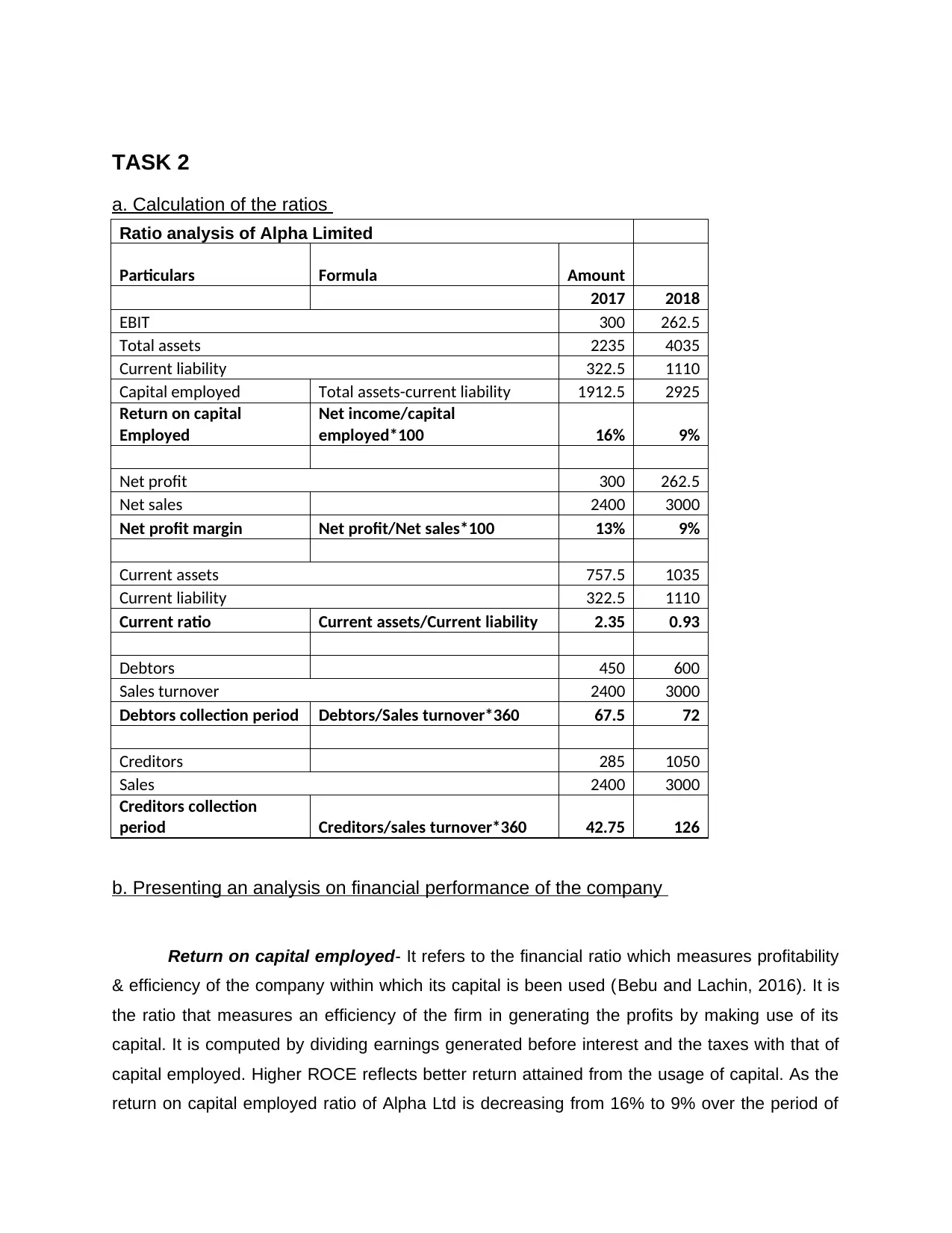

This report presents a comprehensive financial analysis of Alpha Limited, focusing on key financial ratios to evaluate its performance over two years. The analysis includes the calculation and interpretation of Return on Capital Employed (ROCE), Net Profit Margin, Current Ratio, Average Receivables Days, and Average Payable Days. The report highlights trends, such as the decreasing ROCE and Net Profit Margin, indicating potential inefficiencies in capital utilization and declining profitability. It also examines the declining Current Ratio and the increasing Average Receivables Days, suggesting liquidity and credit management challenges. Furthermore, the report discusses the increase in Average Payable Days, which could reflect improved payment terms with creditors or potential financial difficulties. Each ratio is thoroughly examined, with potential causes for the observed trends and recommendations for improvement. The report references several academic sources to support its findings and conclusions.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.