Financial Analysis, Investment Appraisal, and Funding for Roast Ltd.

VerifiedAdded on 2023/01/17

|16

|3515

|54

Report

AI Summary

This project report provides a comprehensive financial analysis of Roast Ltd., a coffee house chain in the UK. It examines the company's financial position using various ratios, including gross profit, net profit, operating profit, current, quick, debt-to-equity, and return on capital employed. The analysis covers the statement of profit or loss, statement of financial position (balance sheet), and statement of cash flows for the years 2017 and 2018. Additionally, the report explores investment appraisal techniques such as payback period, net present value, and accounting rate of return, recommending a funding strategy involving bank loans and share capital to support a 500 million pound investment. The report concludes with a detailed overview of the company's financial performance and strategic recommendations.

Financial Decision

Making

1

Making

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

EXECUTIVE SUMMARY

This project report is based upon Roast Ltd. that is one of the main coffee houses

established in United Kingdom. It analyse financial position of an enterprise with different ratios

for calculating final accounts. These are net, gross and operating income through liquidity,

solvency and profitability ratios etc. In order to make investment in a project different

investment appraisal techniques are used by the organisation. These are pay back period, net

present value, accounting rate of return. The enterprise is recommended to arrange funding from

bank loan and share capital to make investment of 500 million pounds.

2

This project report is based upon Roast Ltd. that is one of the main coffee houses

established in United Kingdom. It analyse financial position of an enterprise with different ratios

for calculating final accounts. These are net, gross and operating income through liquidity,

solvency and profitability ratios etc. In order to make investment in a project different

investment appraisal techniques are used by the organisation. These are pay back period, net

present value, accounting rate of return. The enterprise is recommended to arrange funding from

bank loan and share capital to make investment of 500 million pounds.

2

Table of Contents

EXECUTIVE SUMMARY.............................................................................................................2

Table of Contents.............................................................................................................................3

INTRODUCTION...........................................................................................................................4

PART 1............................................................................................................................................4

Organisation overview.................................................................................................................4

PART 2............................................................................................................................................5

2.1 Statement of profit or loss......................................................................................................5

2.2 Statement of financial position..............................................................................................7

2.3 Statement of cash flows.......................................................................................................10

PART 3..........................................................................................................................................13

3.1 Investment appraisal............................................................................................................13

3.2 Sources of funds..................................................................................................................14

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

3

EXECUTIVE SUMMARY.............................................................................................................2

Table of Contents.............................................................................................................................3

INTRODUCTION...........................................................................................................................4

PART 1............................................................................................................................................4

Organisation overview.................................................................................................................4

PART 2............................................................................................................................................5

2.1 Statement of profit or loss......................................................................................................5

2.2 Statement of financial position..............................................................................................7

2.3 Statement of cash flows.......................................................................................................10

PART 3..........................................................................................................................................13

3.1 Investment appraisal............................................................................................................13

3.2 Sources of funds..................................................................................................................14

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Financial decision making is the process of formulating strategies for future as bit can

help to find the best suitable growth opportunities for business. It is very essential to formulate

effective decisions for future as it is beneficial or development of company (Ambuehl, Bernheim

and Lusardi, 2014). When these are formed then management pays attention towards financial

situation and position of enterprise and analyse final accounts such as cash flow and final

account. By evaluating them actual status of business entity is determined and then strategies are

formed. This project report is based upon Roast Ltd. which is an independent coffee house chain.

It is mainly established in UK and founded in year 2008. This assignment describes industry

review and analyse all financial statements including Profit and loss account, balance sheet and

cash flow. Additionally, investment appraisal techniques with sources of funds are also discussed

in this project.

PART 1

Organisation overview

Coffee house industry of United Kingdom which is very large and it is contributing in the

development as well as growth of UK's economy. Industry review of it could be understood with

the help of following points:

The industry contributes in Gross Domestic Product of UK with 3.7 billion pound in

2017.

Total growth of coffee house sector for year 2018 is 7.9%.

The main players in the United Kingdom for coffee house sector are Starbucks, Costa

Coffee, Caffe Nero, Coffee #1, Cafe2U, Puccino's, Muffin Break, AMT Coffee and Roast

Ltd., etc (Major players in coffee house industry of UK, 2019).

One key opportunity for this industry is to expand enterprise where it has not yet

established the business. The places where people like to have coffee the sector should

target those countries.

The coffee house industry is facing is a main challenge of different drinks and increasing

number of healthcare individuals for ignoring such beverages that adversely affect their

health.

4

Financial decision making is the process of formulating strategies for future as bit can

help to find the best suitable growth opportunities for business. It is very essential to formulate

effective decisions for future as it is beneficial or development of company (Ambuehl, Bernheim

and Lusardi, 2014). When these are formed then management pays attention towards financial

situation and position of enterprise and analyse final accounts such as cash flow and final

account. By evaluating them actual status of business entity is determined and then strategies are

formed. This project report is based upon Roast Ltd. which is an independent coffee house chain.

It is mainly established in UK and founded in year 2008. This assignment describes industry

review and analyse all financial statements including Profit and loss account, balance sheet and

cash flow. Additionally, investment appraisal techniques with sources of funds are also discussed

in this project.

PART 1

Organisation overview

Coffee house industry of United Kingdom which is very large and it is contributing in the

development as well as growth of UK's economy. Industry review of it could be understood with

the help of following points:

The industry contributes in Gross Domestic Product of UK with 3.7 billion pound in

2017.

Total growth of coffee house sector for year 2018 is 7.9%.

The main players in the United Kingdom for coffee house sector are Starbucks, Costa

Coffee, Caffe Nero, Coffee #1, Cafe2U, Puccino's, Muffin Break, AMT Coffee and Roast

Ltd., etc (Major players in coffee house industry of UK, 2019).

One key opportunity for this industry is to expand enterprise where it has not yet

established the business. The places where people like to have coffee the sector should

target those countries.

The coffee house industry is facing is a main challenge of different drinks and increasing

number of healthcare individuals for ignoring such beverages that adversely affect their

health.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

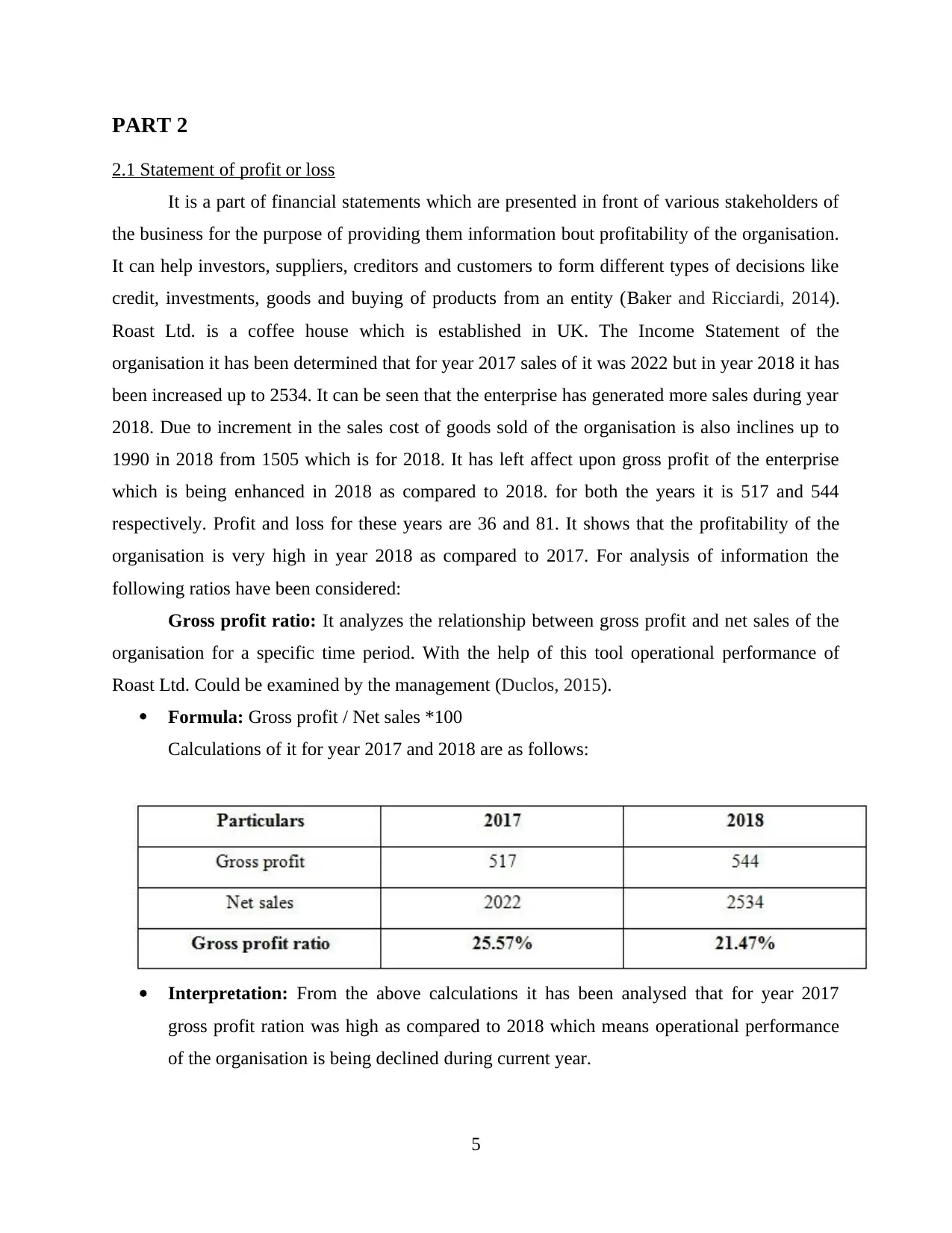

PART 2

2.1 Statement of profit or loss

It is a part of financial statements which are presented in front of various stakeholders of

the business for the purpose of providing them information bout profitability of the organisation.

It can help investors, suppliers, creditors and customers to form different types of decisions like

credit, investments, goods and buying of products from an entity (Baker and Ricciardi, 2014).

Roast Ltd. is a coffee house which is established in UK. The Income Statement of the

organisation it has been determined that for year 2017 sales of it was 2022 but in year 2018 it has

been increased up to 2534. It can be seen that the enterprise has generated more sales during year

2018. Due to increment in the sales cost of goods sold of the organisation is also inclines up to

1990 in 2018 from 1505 which is for 2018. It has left affect upon gross profit of the enterprise

which is being enhanced in 2018 as compared to 2018. for both the years it is 517 and 544

respectively. Profit and loss for these years are 36 and 81. It shows that the profitability of the

organisation is very high in year 2018 as compared to 2017. For analysis of information the

following ratios have been considered:

Gross profit ratio: It analyzes the relationship between gross profit and net sales of the

organisation for a specific time period. With the help of this tool operational performance of

Roast Ltd. Could be examined by the management (Duclos, 2015).

Formula: Gross profit / Net sales *100

Calculations of it for year 2017 and 2018 are as follows:

Interpretation: From the above calculations it has been analysed that for year 2017

gross profit ration was high as compared to 2018 which means operational performance

of the organisation is being declined during current year.

5

2.1 Statement of profit or loss

It is a part of financial statements which are presented in front of various stakeholders of

the business for the purpose of providing them information bout profitability of the organisation.

It can help investors, suppliers, creditors and customers to form different types of decisions like

credit, investments, goods and buying of products from an entity (Baker and Ricciardi, 2014).

Roast Ltd. is a coffee house which is established in UK. The Income Statement of the

organisation it has been determined that for year 2017 sales of it was 2022 but in year 2018 it has

been increased up to 2534. It can be seen that the enterprise has generated more sales during year

2018. Due to increment in the sales cost of goods sold of the organisation is also inclines up to

1990 in 2018 from 1505 which is for 2018. It has left affect upon gross profit of the enterprise

which is being enhanced in 2018 as compared to 2018. for both the years it is 517 and 544

respectively. Profit and loss for these years are 36 and 81. It shows that the profitability of the

organisation is very high in year 2018 as compared to 2017. For analysis of information the

following ratios have been considered:

Gross profit ratio: It analyzes the relationship between gross profit and net sales of the

organisation for a specific time period. With the help of this tool operational performance of

Roast Ltd. Could be examined by the management (Duclos, 2015).

Formula: Gross profit / Net sales *100

Calculations of it for year 2017 and 2018 are as follows:

Interpretation: From the above calculations it has been analysed that for year 2017

gross profit ration was high as compared to 2018 which means operational performance

of the organisation is being declined during current year.

5

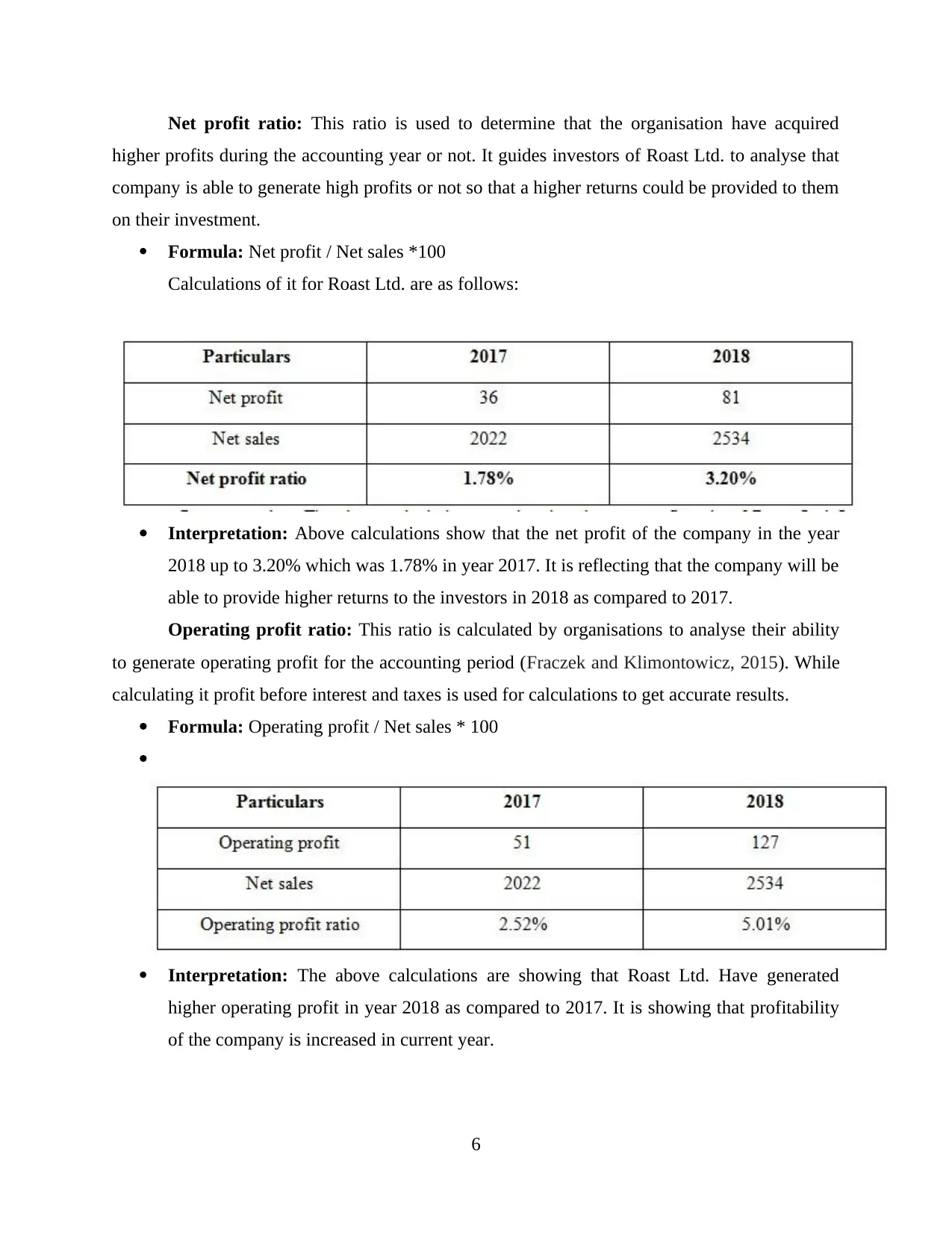

Net profit ratio: This ratio is used to determine that the organisation have acquired

higher profits during the accounting year or not. It guides investors of Roast Ltd. to analyse that

company is able to generate high profits or not so that a higher returns could be provided to them

on their investment.

Formula: Net profit / Net sales *100

Calculations of it for Roast Ltd. are as follows:

Interpretation: Above calculations show that the net profit of the company in the year

2018 up to 3.20% which was 1.78% in year 2017. It is reflecting that the company will be

able to provide higher returns to the investors in 2018 as compared to 2017.

Operating profit ratio: This ratio is calculated by organisations to analyse their ability

to generate operating profit for the accounting period (Fraczek and Klimontowicz, 2015). While

calculating it profit before interest and taxes is used for calculations to get accurate results.

Formula: Operating profit / Net sales * 100

Interpretation: The above calculations are showing that Roast Ltd. Have generated

higher operating profit in year 2018 as compared to 2017. It is showing that profitability

of the company is increased in current year.

6

higher profits during the accounting year or not. It guides investors of Roast Ltd. to analyse that

company is able to generate high profits or not so that a higher returns could be provided to them

on their investment.

Formula: Net profit / Net sales *100

Calculations of it for Roast Ltd. are as follows:

Interpretation: Above calculations show that the net profit of the company in the year

2018 up to 3.20% which was 1.78% in year 2017. It is reflecting that the company will be

able to provide higher returns to the investors in 2018 as compared to 2017.

Operating profit ratio: This ratio is calculated by organisations to analyse their ability

to generate operating profit for the accounting period (Fraczek and Klimontowicz, 2015). While

calculating it profit before interest and taxes is used for calculations to get accurate results.

Formula: Operating profit / Net sales * 100

Interpretation: The above calculations are showing that Roast Ltd. Have generated

higher operating profit in year 2018 as compared to 2017. It is showing that profitability

of the company is increased in current year.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

From the above analysis it has been determined that overall profitability of the

organisation is good because the net and operating profit ratios are showing increment for year

2018 as compared to 2017.

2.2 Statement of financial position

It is also known as balance sheet as it shows the actual financial stability of an

organisation. It is prepared for a year and all the assets, equities, and liabilities are recorded in it

(Füllbrunn and Luhan, 2015). It helps the external stakeholders such as investors and creditors so

that they can perform specific analysis. Actual and appropriate financial position of a business

could be determined by analysing the balance sheet. Roast Ltd.'s balance sheet is showing that

non current assets which are reocorded in the right side of the statement are increased in 2018 up

to 996 which was 670 in year 2017. It shows that organisation have bought property, plant and

equipment to operate business in systematic manner so that financial position could be

strengthen. The current asset heading in the same side showing an increment in inventoried up to

299 for 2018 which was increased from 120 for 2017. Trade and other receivables of Roast Ltd.

are also increased in 2018 as compared to 2017. For both the years these are 148 and 93

respectively. In year 2017 cash and cash equivalents were 134 but in 2018 the enterprise is

having nil balance for the same. It shows that the company is not having core current assets for

year ending 2018. Overall analysis of right side of statement of financial position is showing that

total assets of the company are increased in 2018 (Graham, Harvey and Puri, 2015).

Left side of balance sheet is showing that share capital for 2018 and 2017 are same but

retained earning are increased in 2018 up to 660 which was 579 in 2017. An increment can be

seen in the long-term borrowings which is recorded in the non current liabilities of the

organisation is also recorded in the statement of financial position which means Roast Ltd. have

taken loan from external parties for effective execution of operations. Current liabilities for year

2018 are increased up to 583 in 2018 which was 238 in 2017. For the purpose of analysis the

company following ratios are calculated:

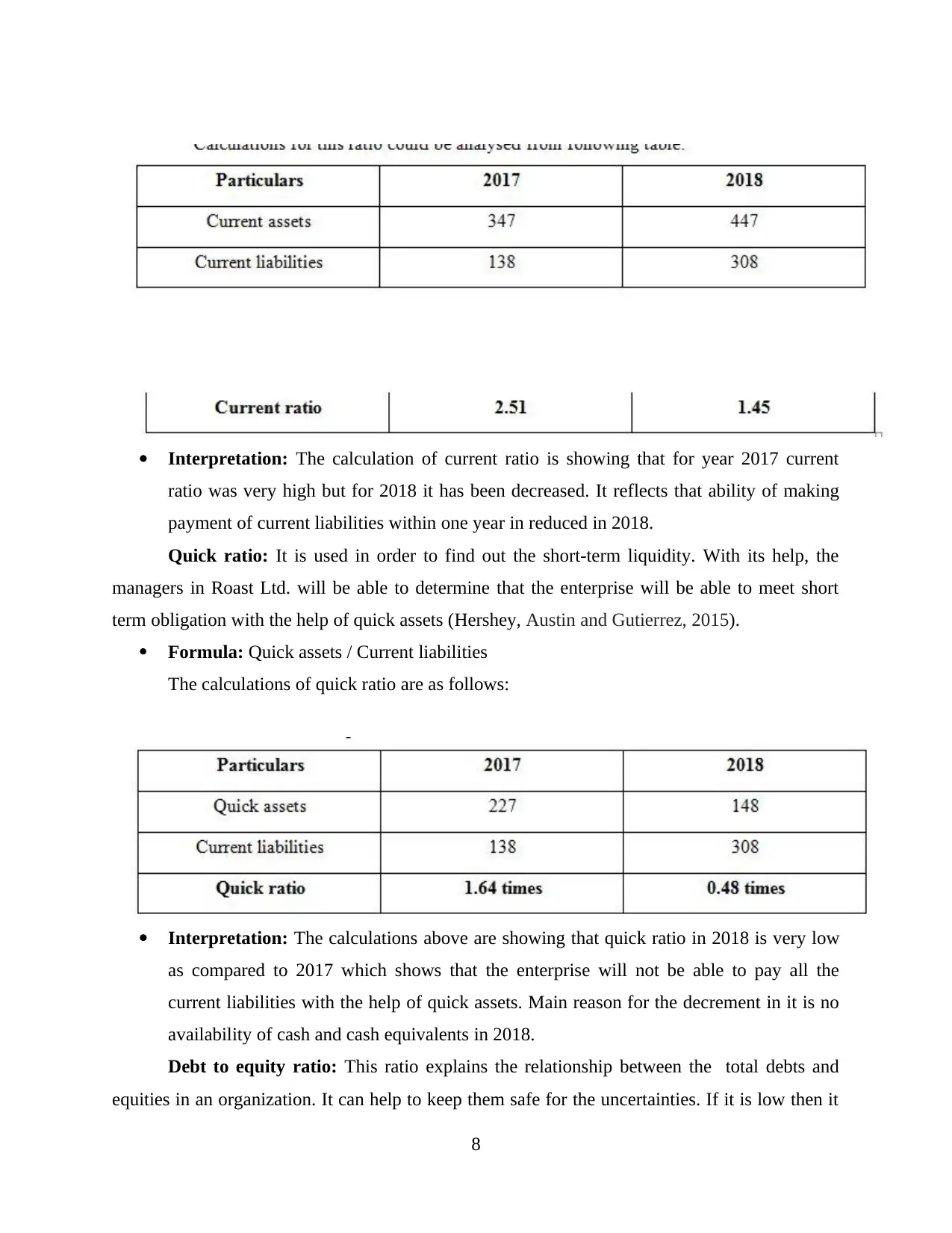

Current ratio: Current ratio is used to calculate the relationship shared between the

current assets and current liabilities (Guastello, 2016). It will be beneficial for Roast Ltd. to

analyse that it can pay all the current liabilities with the help of short term assets.

Formula: Current assets / Current liabilities

Calculations for this ratio could be analysed from following table:

7

organisation is good because the net and operating profit ratios are showing increment for year

2018 as compared to 2017.

2.2 Statement of financial position

It is also known as balance sheet as it shows the actual financial stability of an

organisation. It is prepared for a year and all the assets, equities, and liabilities are recorded in it

(Füllbrunn and Luhan, 2015). It helps the external stakeholders such as investors and creditors so

that they can perform specific analysis. Actual and appropriate financial position of a business

could be determined by analysing the balance sheet. Roast Ltd.'s balance sheet is showing that

non current assets which are reocorded in the right side of the statement are increased in 2018 up

to 996 which was 670 in year 2017. It shows that organisation have bought property, plant and

equipment to operate business in systematic manner so that financial position could be

strengthen. The current asset heading in the same side showing an increment in inventoried up to

299 for 2018 which was increased from 120 for 2017. Trade and other receivables of Roast Ltd.

are also increased in 2018 as compared to 2017. For both the years these are 148 and 93

respectively. In year 2017 cash and cash equivalents were 134 but in 2018 the enterprise is

having nil balance for the same. It shows that the company is not having core current assets for

year ending 2018. Overall analysis of right side of statement of financial position is showing that

total assets of the company are increased in 2018 (Graham, Harvey and Puri, 2015).

Left side of balance sheet is showing that share capital for 2018 and 2017 are same but

retained earning are increased in 2018 up to 660 which was 579 in 2017. An increment can be

seen in the long-term borrowings which is recorded in the non current liabilities of the

organisation is also recorded in the statement of financial position which means Roast Ltd. have

taken loan from external parties for effective execution of operations. Current liabilities for year

2018 are increased up to 583 in 2018 which was 238 in 2017. For the purpose of analysis the

company following ratios are calculated:

Current ratio: Current ratio is used to calculate the relationship shared between the

current assets and current liabilities (Guastello, 2016). It will be beneficial for Roast Ltd. to

analyse that it can pay all the current liabilities with the help of short term assets.

Formula: Current assets / Current liabilities

Calculations for this ratio could be analysed from following table:

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Interpretation: The calculation of current ratio is showing that for year 2017 current

ratio was very high but for 2018 it has been decreased. It reflects that ability of making

payment of current liabilities within one year in reduced in 2018.

Quick ratio: It is used in order to find out the short-term liquidity. With its help, the

managers in Roast Ltd. will be able to determine that the enterprise will be able to meet short

term obligation with the help of quick assets (Hershey, Austin and Gutierrez, 2015).

Formula: Quick assets / Current liabilities

The calculations of quick ratio are as follows:

Interpretation: The calculations above are showing that quick ratio in 2018 is very low

as compared to 2017 which shows that the enterprise will not be able to pay all the

current liabilities with the help of quick assets. Main reason for the decrement in it is no

availability of cash and cash equivalents in 2018.

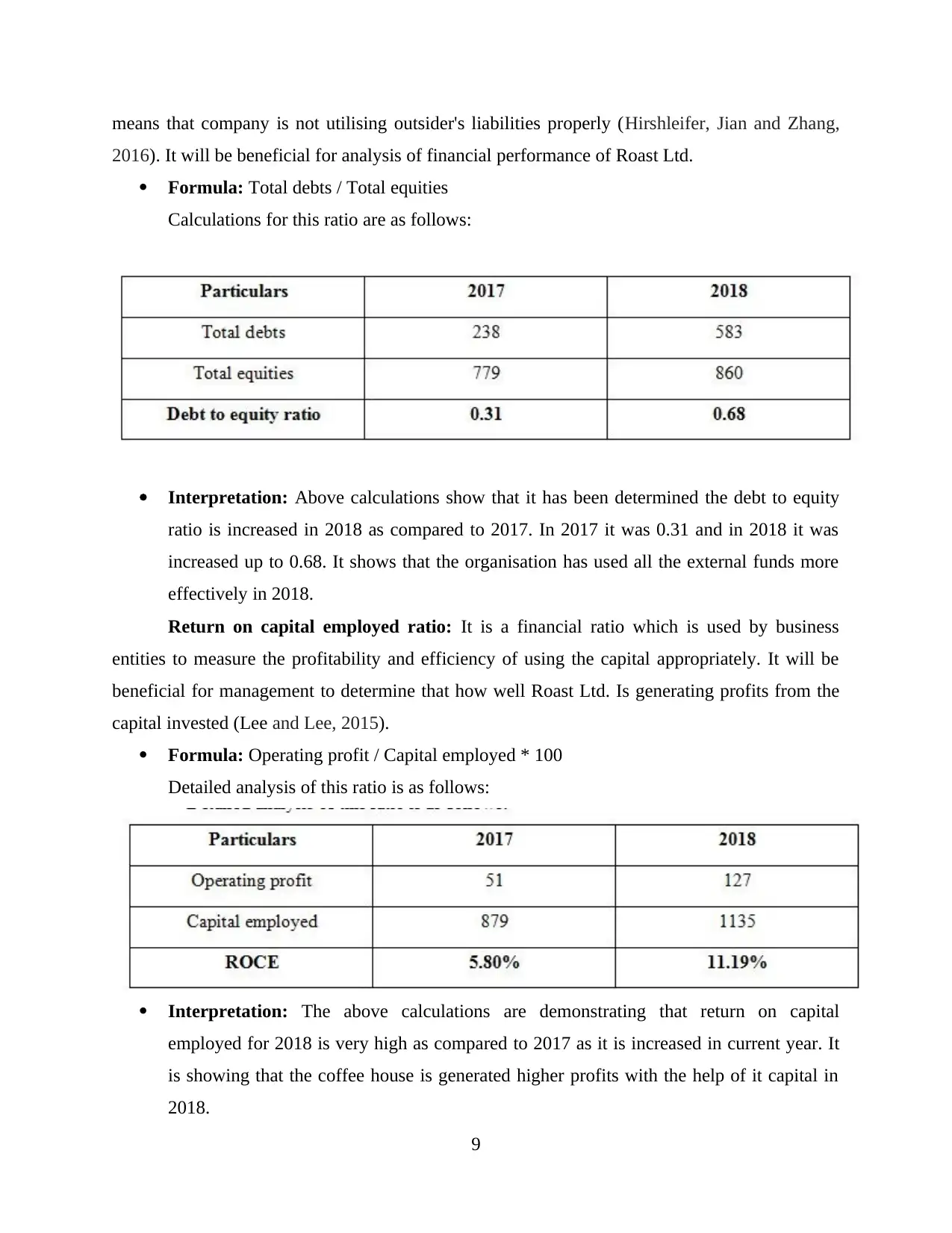

Debt to equity ratio: This ratio explains the relationship between the total debts and

equities in an organization. It can help to keep them safe for the uncertainties. If it is low then it

8

ratio was very high but for 2018 it has been decreased. It reflects that ability of making

payment of current liabilities within one year in reduced in 2018.

Quick ratio: It is used in order to find out the short-term liquidity. With its help, the

managers in Roast Ltd. will be able to determine that the enterprise will be able to meet short

term obligation with the help of quick assets (Hershey, Austin and Gutierrez, 2015).

Formula: Quick assets / Current liabilities

The calculations of quick ratio are as follows:

Interpretation: The calculations above are showing that quick ratio in 2018 is very low

as compared to 2017 which shows that the enterprise will not be able to pay all the

current liabilities with the help of quick assets. Main reason for the decrement in it is no

availability of cash and cash equivalents in 2018.

Debt to equity ratio: This ratio explains the relationship between the total debts and

equities in an organization. It can help to keep them safe for the uncertainties. If it is low then it

8

means that company is not utilising outsider's liabilities properly (Hirshleifer, Jian and Zhang,

2016). It will be beneficial for analysis of financial performance of Roast Ltd.

Formula: Total debts / Total equities

Calculations for this ratio are as follows:

Interpretation: Above calculations show that it has been determined the debt to equity

ratio is increased in 2018 as compared to 2017. In 2017 it was 0.31 and in 2018 it was

increased up to 0.68. It shows that the organisation has used all the external funds more

effectively in 2018.

Return on capital employed ratio: It is a financial ratio which is used by business

entities to measure the profitability and efficiency of using the capital appropriately. It will be

beneficial for management to determine that how well Roast Ltd. Is generating profits from the

capital invested (Lee and Lee, 2015).

Formula: Operating profit / Capital employed * 100

Detailed analysis of this ratio is as follows:

Interpretation: The above calculations are demonstrating that return on capital

employed for 2018 is very high as compared to 2017 as it is increased in current year. It

is showing that the coffee house is generated higher profits with the help of it capital in

2018.

9

2016). It will be beneficial for analysis of financial performance of Roast Ltd.

Formula: Total debts / Total equities

Calculations for this ratio are as follows:

Interpretation: Above calculations show that it has been determined the debt to equity

ratio is increased in 2018 as compared to 2017. In 2017 it was 0.31 and in 2018 it was

increased up to 0.68. It shows that the organisation has used all the external funds more

effectively in 2018.

Return on capital employed ratio: It is a financial ratio which is used by business

entities to measure the profitability and efficiency of using the capital appropriately. It will be

beneficial for management to determine that how well Roast Ltd. Is generating profits from the

capital invested (Lee and Lee, 2015).

Formula: Operating profit / Capital employed * 100

Detailed analysis of this ratio is as follows:

Interpretation: The above calculations are demonstrating that return on capital

employed for 2018 is very high as compared to 2017 as it is increased in current year. It

is showing that the coffee house is generated higher profits with the help of it capital in

2018.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

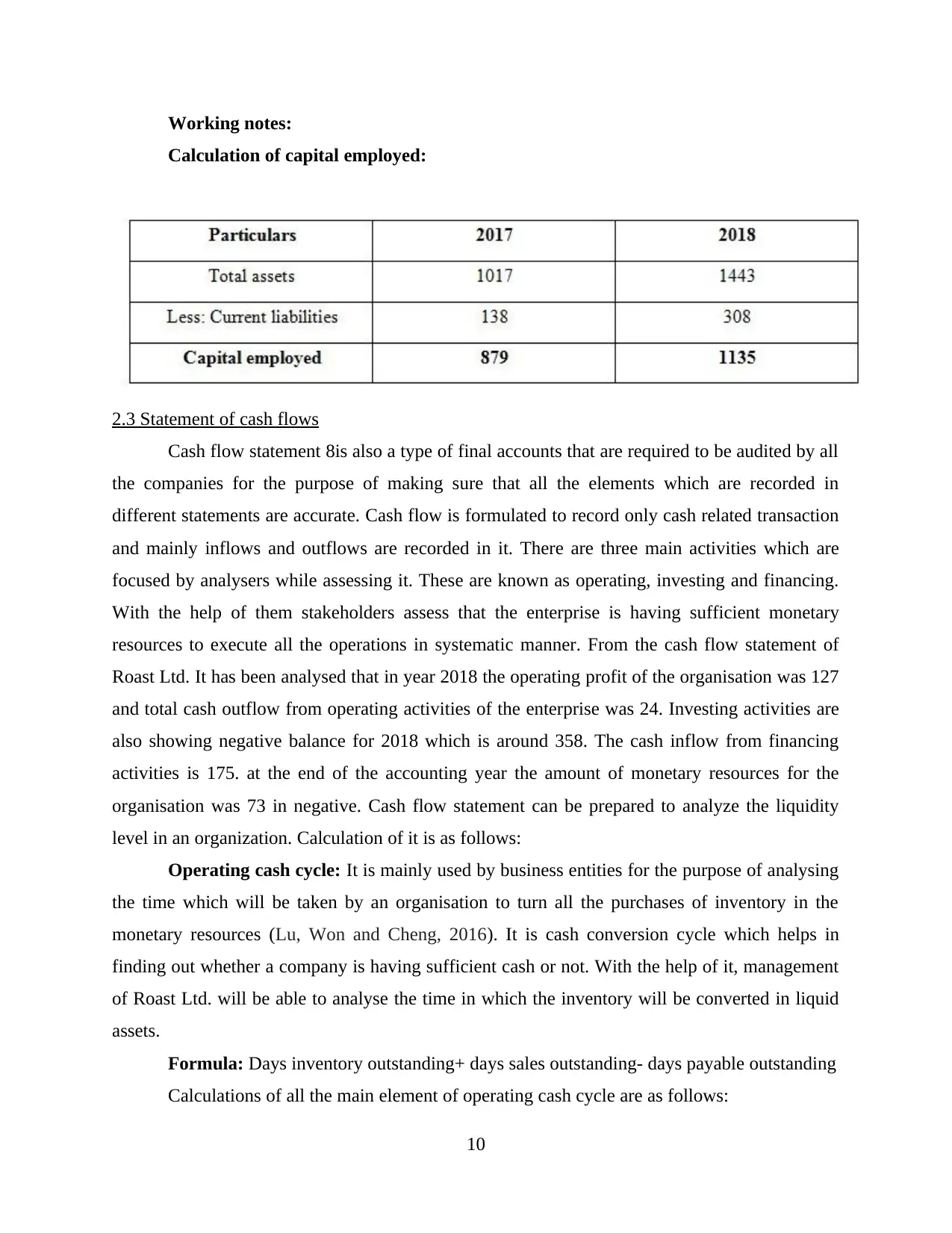

Working notes:

Calculation of capital employed:

2.3 Statement of cash flows

Cash flow statement 8is also a type of final accounts that are required to be audited by all

the companies for the purpose of making sure that all the elements which are recorded in

different statements are accurate. Cash flow is formulated to record only cash related transaction

and mainly inflows and outflows are recorded in it. There are three main activities which are

focused by analysers while assessing it. These are known as operating, investing and financing.

With the help of them stakeholders assess that the enterprise is having sufficient monetary

resources to execute all the operations in systematic manner. From the cash flow statement of

Roast Ltd. It has been analysed that in year 2018 the operating profit of the organisation was 127

and total cash outflow from operating activities of the enterprise was 24. Investing activities are

also showing negative balance for 2018 which is around 358. The cash inflow from financing

activities is 175. at the end of the accounting year the amount of monetary resources for the

organisation was 73 in negative. Cash flow statement can be prepared to analyze the liquidity

level in an organization. Calculation of it is as follows:

Operating cash cycle: It is mainly used by business entities for the purpose of analysing

the time which will be taken by an organisation to turn all the purchases of inventory in the

monetary resources (Lu, Won and Cheng, 2016). It is cash conversion cycle which helps in

finding out whether a company is having sufficient cash or not. With the help of it, management

of Roast Ltd. will be able to analyse the time in which the inventory will be converted in liquid

assets.

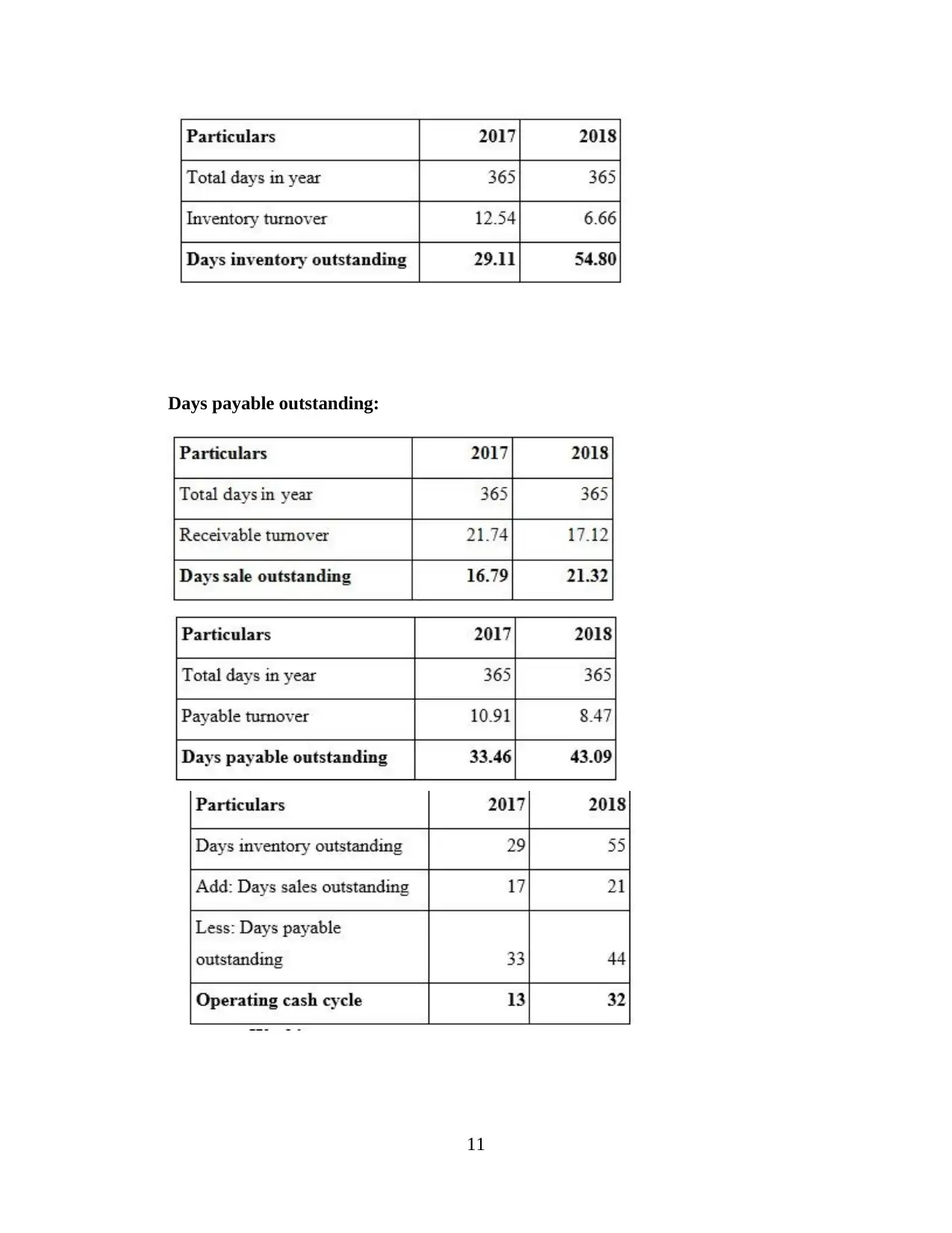

Formula: Days inventory outstanding+ days sales outstanding- days payable outstanding

Calculations of all the main element of operating cash cycle are as follows:

10

Calculation of capital employed:

2.3 Statement of cash flows

Cash flow statement 8is also a type of final accounts that are required to be audited by all

the companies for the purpose of making sure that all the elements which are recorded in

different statements are accurate. Cash flow is formulated to record only cash related transaction

and mainly inflows and outflows are recorded in it. There are three main activities which are

focused by analysers while assessing it. These are known as operating, investing and financing.

With the help of them stakeholders assess that the enterprise is having sufficient monetary

resources to execute all the operations in systematic manner. From the cash flow statement of

Roast Ltd. It has been analysed that in year 2018 the operating profit of the organisation was 127

and total cash outflow from operating activities of the enterprise was 24. Investing activities are

also showing negative balance for 2018 which is around 358. The cash inflow from financing

activities is 175. at the end of the accounting year the amount of monetary resources for the

organisation was 73 in negative. Cash flow statement can be prepared to analyze the liquidity

level in an organization. Calculation of it is as follows:

Operating cash cycle: It is mainly used by business entities for the purpose of analysing

the time which will be taken by an organisation to turn all the purchases of inventory in the

monetary resources (Lu, Won and Cheng, 2016). It is cash conversion cycle which helps in

finding out whether a company is having sufficient cash or not. With the help of it, management

of Roast Ltd. will be able to analyse the time in which the inventory will be converted in liquid

assets.

Formula: Days inventory outstanding+ days sales outstanding- days payable outstanding

Calculations of all the main element of operating cash cycle are as follows:

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Days payable outstanding:

11

11

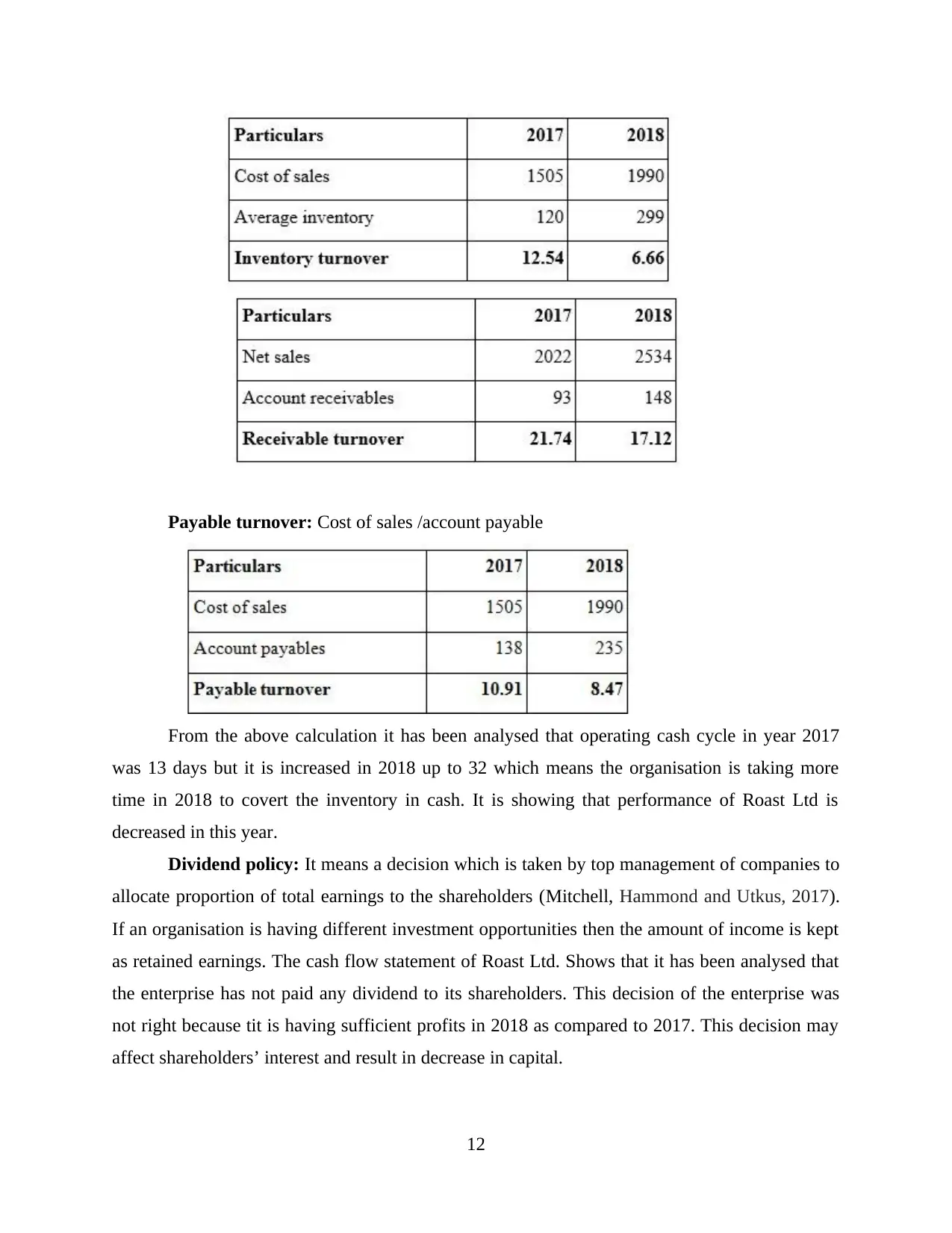

Payable turnover: Cost of sales /account payable

From the above calculation it has been analysed that operating cash cycle in year 2017

was 13 days but it is increased in 2018 up to 32 which means the organisation is taking more

time in 2018 to covert the inventory in cash. It is showing that performance of Roast Ltd is

decreased in this year.

Dividend policy: It means a decision which is taken by top management of companies to

allocate proportion of total earnings to the shareholders (Mitchell, Hammond and Utkus, 2017).

If an organisation is having different investment opportunities then the amount of income is kept

as retained earnings. The cash flow statement of Roast Ltd. Shows that it has been analysed that

the enterprise has not paid any dividend to its shareholders. This decision of the enterprise was

not right because tit is having sufficient profits in 2018 as compared to 2017. This decision may

affect shareholders’ interest and result in decrease in capital.

12

From the above calculation it has been analysed that operating cash cycle in year 2017

was 13 days but it is increased in 2018 up to 32 which means the organisation is taking more

time in 2018 to covert the inventory in cash. It is showing that performance of Roast Ltd is

decreased in this year.

Dividend policy: It means a decision which is taken by top management of companies to

allocate proportion of total earnings to the shareholders (Mitchell, Hammond and Utkus, 2017).

If an organisation is having different investment opportunities then the amount of income is kept

as retained earnings. The cash flow statement of Roast Ltd. Shows that it has been analysed that

the enterprise has not paid any dividend to its shareholders. This decision of the enterprise was

not right because tit is having sufficient profits in 2018 as compared to 2017. This decision may

affect shareholders’ interest and result in decrease in capital.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.