Financial Decision Making: Accounting and Finance Functions of Alpha Ltd

VerifiedAdded on 2023/06/10

|14

|4016

|473

AI Summary

This report discusses the importance of accounting and finance functions in organizations, with a focus on Alpha Ltd. It covers the functions of the accounting, management accounting, tax, and auditing departments, as well as the investment, financing, dividend, and working capital functions of the finance department. The report also includes a calculation of financial ratios and a commentary on the performance of Alpha Ltd based on those ratios.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Financial Decision Making

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

Accounting and finance functions of Alpha Ltd.........................................................................3

TASK 2............................................................................................................................................7

Calculating ratios........................................................................................................................7

Commenting on performance of Alpha.......................................................................................8

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

Accounting and finance functions of Alpha Ltd.........................................................................3

TASK 2............................................................................................................................................7

Calculating ratios........................................................................................................................7

Commenting on performance of Alpha.......................................................................................8

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................13

INTRODUCTION

Accounting and Finance functions are cardinal to any organisation. Financial decision

making is a sound approach to weighing the pros and cons of a decision which relates to funds.

The decisions taken by the finance manager are very crucial. The following Report is based on

Alpha manufacturing company based in uk which started their operations back in 1954.The

current report will outline the importance of accounting and finance functions along with all the

ratios which analyses the performance of Alpha Ltd. Alongside financial ratios will critically

examine financial statements which will be used to evaluate profitability, analyse trends,

evaluate borrowing capacity of the Alpha ltd.

TASK 1

Accounting and finance functions of Alpha Ltd

ACCOUNTING DEPARTMENT

The accounting department is responsible for billings, Payroll, Cost Accounting, supplier

payment, preparing financial statements and many more. The accounts department is also

responsible for recording all the cash flows, both in and out for the company. Accounting

department is managed by controller who reports to chief financial officer of the Company.

Accounting department maintain adequate internal controls within the organization to safeguard

valuable resources also keep track of costs incurred by the company and anticipate business

needs.

Functions of Accounting Department

FINANCIAL ACCOUNTING FUNCTION

Financial accounting primary functions is to record and measure all the business activities

of the company and convert that information into financial statements through which investors

can make financial decisions for the betterment of the company. The primary beneficiary are

investors, creditors & lenders. The functions include

Systematic Record

The important function is to record financial transactions systematically for the business.

Recording of each and every financial transaction of business must be according to the financial

standards.

Analysing and summarising

Accounting and Finance functions are cardinal to any organisation. Financial decision

making is a sound approach to weighing the pros and cons of a decision which relates to funds.

The decisions taken by the finance manager are very crucial. The following Report is based on

Alpha manufacturing company based in uk which started their operations back in 1954.The

current report will outline the importance of accounting and finance functions along with all the

ratios which analyses the performance of Alpha Ltd. Alongside financial ratios will critically

examine financial statements which will be used to evaluate profitability, analyse trends,

evaluate borrowing capacity of the Alpha ltd.

TASK 1

Accounting and finance functions of Alpha Ltd

ACCOUNTING DEPARTMENT

The accounting department is responsible for billings, Payroll, Cost Accounting, supplier

payment, preparing financial statements and many more. The accounts department is also

responsible for recording all the cash flows, both in and out for the company. Accounting

department is managed by controller who reports to chief financial officer of the Company.

Accounting department maintain adequate internal controls within the organization to safeguard

valuable resources also keep track of costs incurred by the company and anticipate business

needs.

Functions of Accounting Department

FINANCIAL ACCOUNTING FUNCTION

Financial accounting primary functions is to record and measure all the business activities

of the company and convert that information into financial statements through which investors

can make financial decisions for the betterment of the company. The primary beneficiary are

investors, creditors & lenders. The functions include

Systematic Record

The important function is to record financial transactions systematically for the business.

Recording of each and every financial transaction of business must be according to the financial

standards.

Analysing and summarising

Financial accountants show the correct financial position of the company with the

analysing and summarising of the financial transactions recorded (Zéman, 2019). With this profit

and loss of business in a financial year can be obtained.

Communicate results

The financial accountants must provide report of financial position of the business in the

financial year to all the shareholders & owner of the company, Government, investors and all

other related parties.

Meeting legal requirements

Legal requirements like auditing of the books from external auditor & tax liabilities as

per the taxation system of the country should be meet.

MANAGEMENT ACCOUNTING FUNCTION

Management accounting refers to branch of accounting that includes planning and

controlling of business operations. It helps the Alpha Ltd. management in formulating policies

by collecting information and processing it for further use. This helps in making quality

decisions for the business in the competitive business environment.

Functions of Management accounting

Planning

Planning helps management of Alpha Ltd. to formulate the business objectives which

can be achieving of desired profits for a particular year, steps to reach the targeted profit.

Decision making

For decision making the Alpha Ltd. management uses statistical and accounting

information so that the decision taken benefits the interest of the business (Ross, Shi and Xie,

2019). For example, business uses cash flow forecast and projected reports, burn rate, comparing

costs vs budget for the project etc.

Controlling

Controlling include measuring and monitoring actual results to make sure that goals and

plans of Alpha Ltd. are achieved. It checks the expected performance of a business.

TAX FUNCTION

Tax accounting function deals with the preparations of tax returns and tax payments. It

also takes in account to work with taxable income of Alpha Ltd. along with any deductions or

any tax benefits & exemptions (Muda and et. al., 2018). There are two items which must be

analysing and summarising of the financial transactions recorded (Zéman, 2019). With this profit

and loss of business in a financial year can be obtained.

Communicate results

The financial accountants must provide report of financial position of the business in the

financial year to all the shareholders & owner of the company, Government, investors and all

other related parties.

Meeting legal requirements

Legal requirements like auditing of the books from external auditor & tax liabilities as

per the taxation system of the country should be meet.

MANAGEMENT ACCOUNTING FUNCTION

Management accounting refers to branch of accounting that includes planning and

controlling of business operations. It helps the Alpha Ltd. management in formulating policies

by collecting information and processing it for further use. This helps in making quality

decisions for the business in the competitive business environment.

Functions of Management accounting

Planning

Planning helps management of Alpha Ltd. to formulate the business objectives which

can be achieving of desired profits for a particular year, steps to reach the targeted profit.

Decision making

For decision making the Alpha Ltd. management uses statistical and accounting

information so that the decision taken benefits the interest of the business (Ross, Shi and Xie,

2019). For example, business uses cash flow forecast and projected reports, burn rate, comparing

costs vs budget for the project etc.

Controlling

Controlling include measuring and monitoring actual results to make sure that goals and

plans of Alpha Ltd. are achieved. It checks the expected performance of a business.

TAX FUNCTION

Tax accounting function deals with the preparations of tax returns and tax payments. It

also takes in account to work with taxable income of Alpha Ltd. along with any deductions or

any tax benefits & exemptions (Muda and et. al., 2018). There are two items which must be

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

recognised in tax accounting i.e. current year liability and future year liability. Corporation tax is

also considered under tax accounting, Alpha Ltd. is liable for corporation tax and must submit

their tax return at the end of each accounting period. Tax function helps mitigate risk, problems

in business growth, efficiency analysis.

AUDITING FUNCTION

The internal audit and assurance is dedicated to provide Management of Alpha Ltd. With

value added services as well as safeguarding of their assets, compliance with applicable laws,

regulations, contracts which helps to determine effectiveness and efficiency of operations along

with reliability and integrity of financial and operational information. The auditors of Alpha Ltd.

are provided access to all property, personnel and records so that the above activities can be

submerged (Kotsupatriy and et. al., 2020). The primary objective of the Audit is to examine

whether or not if there is an error or fraud in the financial information of the Alpha Ltd. Also to

ensure that the financial position reveals a true and fair view of the business.

FINANCE DEPARTMENT

Finance department ensures that there is timely & enough availability of funds for the

continuous business operations. It also manages that the company pays its debtors and suppliers

on time along with that it also focuses on the income & expenditures of the company (London

Business training and Consulting, 2022). Finance department is the part of organisation that is

responsible for acquiring funds for the firm, managing the funds in the organization and planning

those funds for expenditure on different assets. bookkeeping, cash flows, budgeting and

forecasting, financial reporting and analysis etc. are activities of finance department.

Functions of finance department

INVESTMENT FUNCTION

Investment means allocation of funds or some other resources in expectations of benefits

in the future. It’s one of the most important finance function which allocates capital to long term

assets. Investment in Long term assets produces the maximum yield in the future. Alpha Ltd. doe

prospective investment while considering the expected return and the risk involved with the

investment. As the risk factor plays an important role while considering expected return this

must be calculated before investment (Jowett and et. al., 2020). Investment function also helps in

taking decision regarding reallocation of funds which are being earned by decomposing non

also considered under tax accounting, Alpha Ltd. is liable for corporation tax and must submit

their tax return at the end of each accounting period. Tax function helps mitigate risk, problems

in business growth, efficiency analysis.

AUDITING FUNCTION

The internal audit and assurance is dedicated to provide Management of Alpha Ltd. With

value added services as well as safeguarding of their assets, compliance with applicable laws,

regulations, contracts which helps to determine effectiveness and efficiency of operations along

with reliability and integrity of financial and operational information. The auditors of Alpha Ltd.

are provided access to all property, personnel and records so that the above activities can be

submerged (Kotsupatriy and et. al., 2020). The primary objective of the Audit is to examine

whether or not if there is an error or fraud in the financial information of the Alpha Ltd. Also to

ensure that the financial position reveals a true and fair view of the business.

FINANCE DEPARTMENT

Finance department ensures that there is timely & enough availability of funds for the

continuous business operations. It also manages that the company pays its debtors and suppliers

on time along with that it also focuses on the income & expenditures of the company (London

Business training and Consulting, 2022). Finance department is the part of organisation that is

responsible for acquiring funds for the firm, managing the funds in the organization and planning

those funds for expenditure on different assets. bookkeeping, cash flows, budgeting and

forecasting, financial reporting and analysis etc. are activities of finance department.

Functions of finance department

INVESTMENT FUNCTION

Investment means allocation of funds or some other resources in expectations of benefits

in the future. It’s one of the most important finance function which allocates capital to long term

assets. Investment in Long term assets produces the maximum yield in the future. Alpha Ltd. doe

prospective investment while considering the expected return and the risk involved with the

investment. As the risk factor plays an important role while considering expected return this

must be calculated before investment (Jowett and et. al., 2020). Investment function also helps in

taking decision regarding reallocation of funds which are being earned by decomposing non

profitable and less productive assets. The Expected rate of return must be determined by the

finance manager to match the investment function.

FINANCING FUNCTION

Financing function is another important function of finance department which a financial

manager must opt. the decisions regarding financing must be wise and accurate because a large

chunk of funds is invested in different projects (Gutsalenko and et.al., 2018). Financing can be

done through internal and external sources. The mix of equity capital and debt is known as firm’s

capital structure.

A sound capital structure aims to maximizes shareholders return with minimum risk.

Managers of Alpha Ltd. make estimation regarding the capital requirements. This also depends

on cost of existing and upcoming projects. Cash management decisions are also being taken by

financing manager. Ratio analysis, financial forecasting, cost and profit control etc. are part of

financial control.

DIVIDEND FUNCTION

Earning profit or positive return is the main aim of the business but the key function of

financial manager is to take into account that whether or not to distribute all the profit to

shareholders as dividend or to keep some part of the profits as a part of retained earnings for

future uncertainties or expansion of the business (Eldomiaty, Bahaa El Din and Atia, 2018). It’s a

financial manager duty to select the best optimum dividend policy which maximizes the

shareholder returns and increase the market capitalization of the Alpha Ltd. In case of

profitability it’s a common practice to pay dividends otherwise issue bonus shares to existing

shareholders. Dividend decision is an important aspect of finance department because this effect

on the availability and cost of capital.

WORKING CAPITAL FUNCTION

Working capital is the difference between current assets and current liabilities. Working

capital refers to the money used for company’s short term expenses, which are due within one

year. This capital is being used for purchasing inventory, paying short term debt and for

financing day to day Operating expenses. The four elements of working capital are account

payable, account receivables, cash and inventory. Non availability of cash, uncontrolled creditors

policy may lead to restructuring of capital, sale of assets and can lead to liquidation of the

company. The goal of working capital management is to maximize operational efficiency. An

finance manager to match the investment function.

FINANCING FUNCTION

Financing function is another important function of finance department which a financial

manager must opt. the decisions regarding financing must be wise and accurate because a large

chunk of funds is invested in different projects (Gutsalenko and et.al., 2018). Financing can be

done through internal and external sources. The mix of equity capital and debt is known as firm’s

capital structure.

A sound capital structure aims to maximizes shareholders return with minimum risk.

Managers of Alpha Ltd. make estimation regarding the capital requirements. This also depends

on cost of existing and upcoming projects. Cash management decisions are also being taken by

financing manager. Ratio analysis, financial forecasting, cost and profit control etc. are part of

financial control.

DIVIDEND FUNCTION

Earning profit or positive return is the main aim of the business but the key function of

financial manager is to take into account that whether or not to distribute all the profit to

shareholders as dividend or to keep some part of the profits as a part of retained earnings for

future uncertainties or expansion of the business (Eldomiaty, Bahaa El Din and Atia, 2018). It’s a

financial manager duty to select the best optimum dividend policy which maximizes the

shareholder returns and increase the market capitalization of the Alpha Ltd. In case of

profitability it’s a common practice to pay dividends otherwise issue bonus shares to existing

shareholders. Dividend decision is an important aspect of finance department because this effect

on the availability and cost of capital.

WORKING CAPITAL FUNCTION

Working capital is the difference between current assets and current liabilities. Working

capital refers to the money used for company’s short term expenses, which are due within one

year. This capital is being used for purchasing inventory, paying short term debt and for

financing day to day Operating expenses. The four elements of working capital are account

payable, account receivables, cash and inventory. Non availability of cash, uncontrolled creditors

policy may lead to restructuring of capital, sale of assets and can lead to liquidation of the

company. The goal of working capital management is to maximize operational efficiency. An

efficient working capital management uses working capital ratio, inventory turnover ratio to

monitor how efficiently the working capital is managed.

TASK 2

Calculating ratios

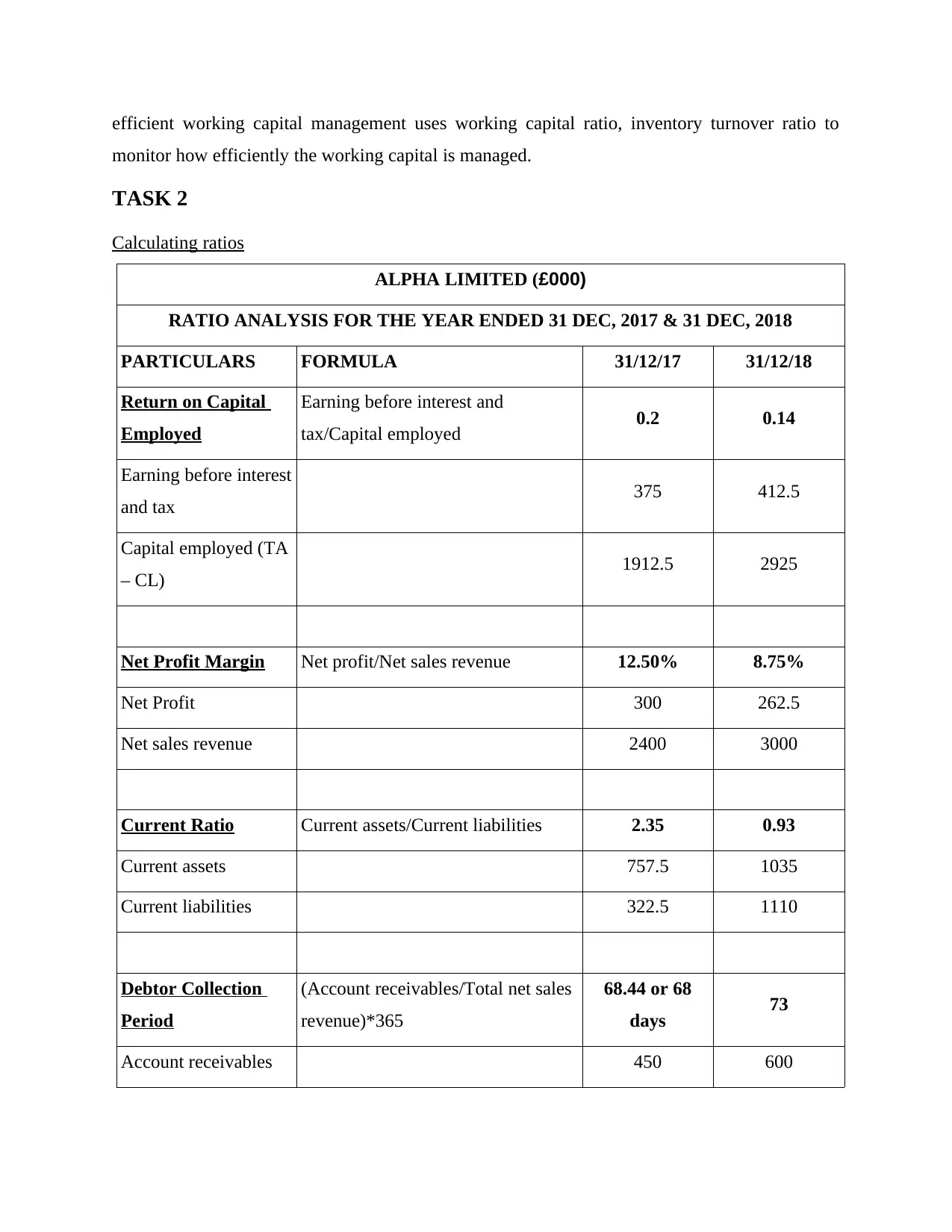

ALPHA LIMITED (£000)

RATIO ANALYSIS FOR THE YEAR ENDED 31 DEC, 2017 & 31 DEC, 2018

PARTICULARS FORMULA 31/12/17 31/12/18

Return on Capital

Employed

Earning before interest and

tax/Capital employed 0.2 0.14

Earning before interest

and tax 375 412.5

Capital employed (TA

– CL) 1912.5 2925

Net Profit Margin Net profit/Net sales revenue 12.50% 8.75%

Net Profit 300 262.5

Net sales revenue 2400 3000

Current Ratio Current assets/Current liabilities 2.35 0.93

Current assets 757.5 1035

Current liabilities 322.5 1110

Debtor Collection

Period

(Account receivables/Total net sales

revenue)*365

68.44 or 68

days 73

Account receivables 450 600

monitor how efficiently the working capital is managed.

TASK 2

Calculating ratios

ALPHA LIMITED (£000)

RATIO ANALYSIS FOR THE YEAR ENDED 31 DEC, 2017 & 31 DEC, 2018

PARTICULARS FORMULA 31/12/17 31/12/18

Return on Capital

Employed

Earning before interest and

tax/Capital employed 0.2 0.14

Earning before interest

and tax 375 412.5

Capital employed (TA

– CL) 1912.5 2925

Net Profit Margin Net profit/Net sales revenue 12.50% 8.75%

Net Profit 300 262.5

Net sales revenue 2400 3000

Current Ratio Current assets/Current liabilities 2.35 0.93

Current assets 757.5 1035

Current liabilities 322.5 1110

Debtor Collection

Period

(Account receivables/Total net sales

revenue)*365

68.44 or 68

days 73

Account receivables 450 600

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

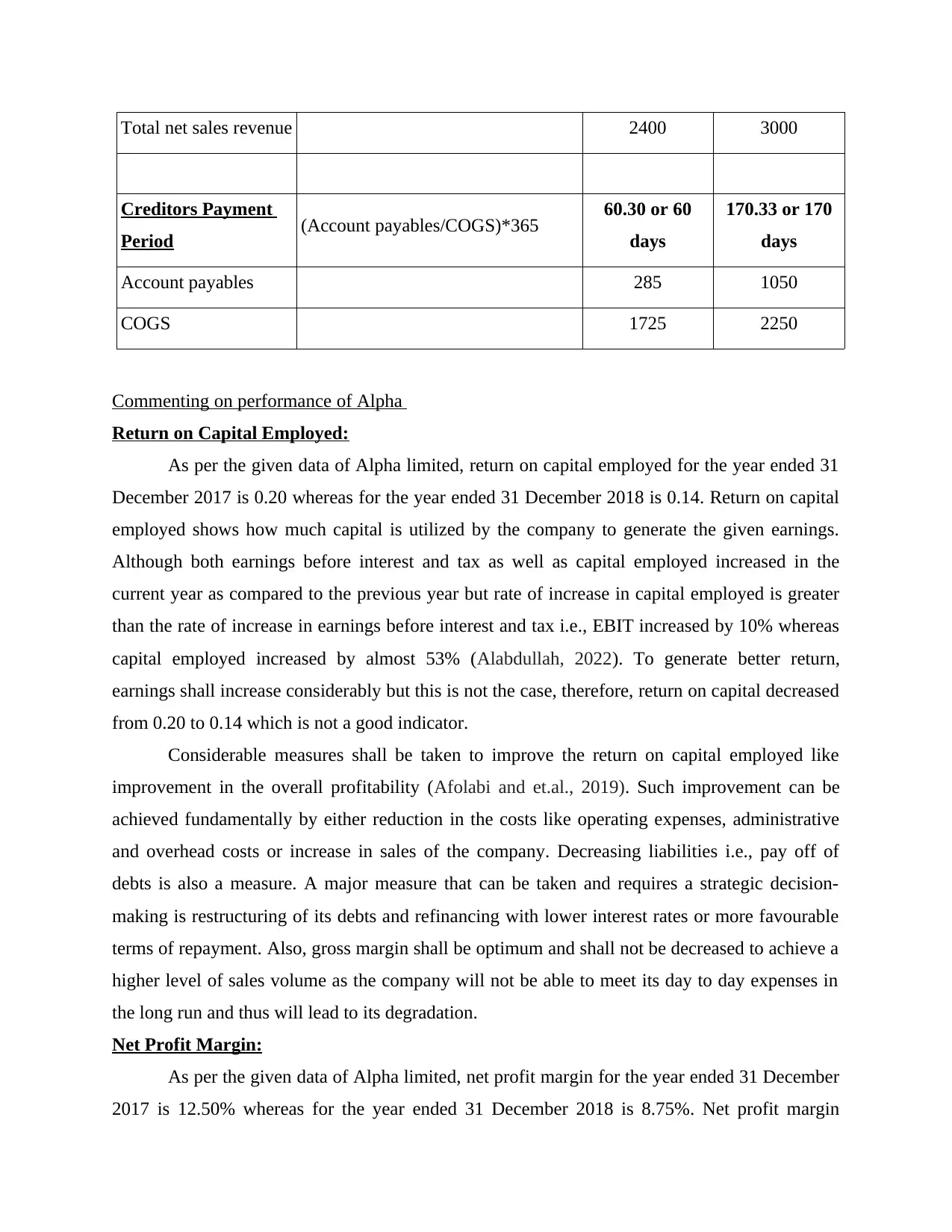

Total net sales revenue 2400 3000

Creditors Payment

Period (Account payables/COGS)*365 60.30 or 60

days

170.33 or 170

days

Account payables 285 1050

COGS 1725 2250

Commenting on performance of Alpha

Return on Capital Employed:

As per the given data of Alpha limited, return on capital employed for the year ended 31

December 2017 is 0.20 whereas for the year ended 31 December 2018 is 0.14. Return on capital

employed shows how much capital is utilized by the company to generate the given earnings.

Although both earnings before interest and tax as well as capital employed increased in the

current year as compared to the previous year but rate of increase in capital employed is greater

than the rate of increase in earnings before interest and tax i.e., EBIT increased by 10% whereas

capital employed increased by almost 53% (Alabdullah, 2022). To generate better return,

earnings shall increase considerably but this is not the case, therefore, return on capital decreased

from 0.20 to 0.14 which is not a good indicator.

Considerable measures shall be taken to improve the return on capital employed like

improvement in the overall profitability (Afolabi and et.al., 2019). Such improvement can be

achieved fundamentally by either reduction in the costs like operating expenses, administrative

and overhead costs or increase in sales of the company. Decreasing liabilities i.e., pay off of

debts is also a measure. A major measure that can be taken and requires a strategic decision-

making is restructuring of its debts and refinancing with lower interest rates or more favourable

terms of repayment. Also, gross margin shall be optimum and shall not be decreased to achieve a

higher level of sales volume as the company will not be able to meet its day to day expenses in

the long run and thus will lead to its degradation.

Net Profit Margin:

As per the given data of Alpha limited, net profit margin for the year ended 31 December

2017 is 12.50% whereas for the year ended 31 December 2018 is 8.75%. Net profit margin

Creditors Payment

Period (Account payables/COGS)*365 60.30 or 60

days

170.33 or 170

days

Account payables 285 1050

COGS 1725 2250

Commenting on performance of Alpha

Return on Capital Employed:

As per the given data of Alpha limited, return on capital employed for the year ended 31

December 2017 is 0.20 whereas for the year ended 31 December 2018 is 0.14. Return on capital

employed shows how much capital is utilized by the company to generate the given earnings.

Although both earnings before interest and tax as well as capital employed increased in the

current year as compared to the previous year but rate of increase in capital employed is greater

than the rate of increase in earnings before interest and tax i.e., EBIT increased by 10% whereas

capital employed increased by almost 53% (Alabdullah, 2022). To generate better return,

earnings shall increase considerably but this is not the case, therefore, return on capital decreased

from 0.20 to 0.14 which is not a good indicator.

Considerable measures shall be taken to improve the return on capital employed like

improvement in the overall profitability (Afolabi and et.al., 2019). Such improvement can be

achieved fundamentally by either reduction in the costs like operating expenses, administrative

and overhead costs or increase in sales of the company. Decreasing liabilities i.e., pay off of

debts is also a measure. A major measure that can be taken and requires a strategic decision-

making is restructuring of its debts and refinancing with lower interest rates or more favourable

terms of repayment. Also, gross margin shall be optimum and shall not be decreased to achieve a

higher level of sales volume as the company will not be able to meet its day to day expenses in

the long run and thus will lead to its degradation.

Net Profit Margin:

As per the given data of Alpha limited, net profit margin for the year ended 31 December

2017 is 12.50% whereas for the year ended 31 December 2018 is 8.75%. Net profit margin

shows profits earned out of revenue received and whether the company is able to cover its

operating, overhead and finance costs. Although net sales revenue increased in the current year

as compared to the previous year from £2,400,000 to £3,000,000 but net profit decreased in the

current year as compared to the previous year from £300,000 to £262,500. Reason being,

operating expenses increased in the current year and most importantly, finance costs doubled in

the current year as Alpha limited doubled the outstanding loan payable in the current year as

compared to previous year (Nariswari and Nugraha, 2020). Therefore, net profit margin

decreased from 12.50% to 8.75%.

First and foremost, suggestion of increasing the net profit margin is to increase the sales

revenues which will in turn lead to increase in gross profits and which will in turn will increase

the net profits of the company. Such sales revenue can be increased either by raising product

price or increasing the sales volume. To have a competitive advantage over other rivals, the

company shall be able to achieve a higher net profit margin than the industry average in general.

Another way to achieve an elevated net profit margin is healthy and optimum reduction in the

costs of the company. The Best option is to increase sales revenues and cost reduction

simultaneously.

Current Ratio:

As per the given data of Alpha limited, current ratio for the year ended 31 December

2017 is 2.35 whereas for the year ended 31 December 2018 it is 0.93. Current ratio shows how a

company is able to meet its current liability obligation on the basis of its current assets base.

Being a current ratio, it concentrates on liabilities becoming due within a year and assets

maturing for utilization within a year and it is also called Working Capital Ratio, Although

current assets increased in the current year as compared to the previous year but current

liabilities also increased in the current year as compared to the previous year and that too at a

greater rate than current assets i.e., current assets increased by almost 37% but current liabilities

increased by a whopping 244% (Irman and Purwati, 2020).

The main reason for such a sharp increase is increase in trade payables from £285,000 to

£1,050,000 and such an increase is due to increase in the amount of purchases in the current year.

The current liabilities increased by 244% but current assets do not increase at an equally

considerable rate to compensate such increase in the current liabilities. Therefore, current ratio

fell from 2.35 to 0.93. An ideal current ratio is 2. Ratio as calculated in the current year is very

operating, overhead and finance costs. Although net sales revenue increased in the current year

as compared to the previous year from £2,400,000 to £3,000,000 but net profit decreased in the

current year as compared to the previous year from £300,000 to £262,500. Reason being,

operating expenses increased in the current year and most importantly, finance costs doubled in

the current year as Alpha limited doubled the outstanding loan payable in the current year as

compared to previous year (Nariswari and Nugraha, 2020). Therefore, net profit margin

decreased from 12.50% to 8.75%.

First and foremost, suggestion of increasing the net profit margin is to increase the sales

revenues which will in turn lead to increase in gross profits and which will in turn will increase

the net profits of the company. Such sales revenue can be increased either by raising product

price or increasing the sales volume. To have a competitive advantage over other rivals, the

company shall be able to achieve a higher net profit margin than the industry average in general.

Another way to achieve an elevated net profit margin is healthy and optimum reduction in the

costs of the company. The Best option is to increase sales revenues and cost reduction

simultaneously.

Current Ratio:

As per the given data of Alpha limited, current ratio for the year ended 31 December

2017 is 2.35 whereas for the year ended 31 December 2018 it is 0.93. Current ratio shows how a

company is able to meet its current liability obligation on the basis of its current assets base.

Being a current ratio, it concentrates on liabilities becoming due within a year and assets

maturing for utilization within a year and it is also called Working Capital Ratio, Although

current assets increased in the current year as compared to the previous year but current

liabilities also increased in the current year as compared to the previous year and that too at a

greater rate than current assets i.e., current assets increased by almost 37% but current liabilities

increased by a whopping 244% (Irman and Purwati, 2020).

The main reason for such a sharp increase is increase in trade payables from £285,000 to

£1,050,000 and such an increase is due to increase in the amount of purchases in the current year.

The current liabilities increased by 244% but current assets do not increase at an equally

considerable rate to compensate such increase in the current liabilities. Therefore, current ratio

fell from 2.35 to 0.93. An ideal current ratio is 2. Ratio as calculated in the current year is very

poor and company needs to adopt drastic measures to improve the ratio. Some measures can be

avoiding large scale capital payments which will require large cash out flow and will decrease

the current assets, personal drawings on the business shall be kept on check to avoid decrease in

the cash i.e., current assets of the company, selling off of the capital assets that are lying ideal

and has no part in generating revenues for the company to increase the cash and bank and

thereafter, paying its current debt obligations.

Debtor Collection Period / Average Receivable Days:

As per the given data of Alpha limited, debtor collection period or average receivable

days for the year ended 31 December 2017 is 68.44 or 68 days whereas for the year ended 31

December 2018 is 73 days. Debtor collection period / average receivable days show how

effective the management of the company is in recovering its receivables from its debtors (What

are Financial Ratios? 2022). Management's debtor collection policy shall be up to date and

effective to achieve a lower collection period of days. Although both account receivables and

total net sales revenue are increasing in the current year but account receivables are increasing at

a greater rate which is leading to decrease in the debtor collection period / average receivable

days (Oksanen and et.al., 2018). Therefore, receivable days increased from 68 days to 73 days.

Increase in receivable days may create a problem for the company as it leads to shortage of funds

to fuel its daily operations and thus, shall be decreased.

Payment terms shall be negotiated with customers in such way to allow timely receipt of

payments, discounts to the extent affordable by the company can be made available to the

customers to receive payments early, immediate communication with the customer in case of late

or delayed payment and reminders from time to time will keep them on edge to meet their

obligations (Rashid, 2018). Automating the process of communication with customers in case of

delayed payments is a very effective measure and is consistent which will remind customers in

ever fixed number of days of their unpaid debts to the company. Allowing customers to directly

deposit the money in the company's account will lead to faster receipt of money and time can be

saved in the processing by the banks in other cases.

Creditors Payment Period / Average Payable Days:

As per the given data of Alpha limited, creditors payment period or average payable days

for the year ended 31 December 2017 is 60.30 or 60 days whereas for the year ended 31

December 2018 is 170.33 or 170 days. Creditors payment period / average payable days shows

avoiding large scale capital payments which will require large cash out flow and will decrease

the current assets, personal drawings on the business shall be kept on check to avoid decrease in

the cash i.e., current assets of the company, selling off of the capital assets that are lying ideal

and has no part in generating revenues for the company to increase the cash and bank and

thereafter, paying its current debt obligations.

Debtor Collection Period / Average Receivable Days:

As per the given data of Alpha limited, debtor collection period or average receivable

days for the year ended 31 December 2017 is 68.44 or 68 days whereas for the year ended 31

December 2018 is 73 days. Debtor collection period / average receivable days show how

effective the management of the company is in recovering its receivables from its debtors (What

are Financial Ratios? 2022). Management's debtor collection policy shall be up to date and

effective to achieve a lower collection period of days. Although both account receivables and

total net sales revenue are increasing in the current year but account receivables are increasing at

a greater rate which is leading to decrease in the debtor collection period / average receivable

days (Oksanen and et.al., 2018). Therefore, receivable days increased from 68 days to 73 days.

Increase in receivable days may create a problem for the company as it leads to shortage of funds

to fuel its daily operations and thus, shall be decreased.

Payment terms shall be negotiated with customers in such way to allow timely receipt of

payments, discounts to the extent affordable by the company can be made available to the

customers to receive payments early, immediate communication with the customer in case of late

or delayed payment and reminders from time to time will keep them on edge to meet their

obligations (Rashid, 2018). Automating the process of communication with customers in case of

delayed payments is a very effective measure and is consistent which will remind customers in

ever fixed number of days of their unpaid debts to the company. Allowing customers to directly

deposit the money in the company's account will lead to faster receipt of money and time can be

saved in the processing by the banks in other cases.

Creditors Payment Period / Average Payable Days:

As per the given data of Alpha limited, creditors payment period or average payable days

for the year ended 31 December 2017 is 60.30 or 60 days whereas for the year ended 31

December 2018 is 170.33 or 170 days. Creditors payment period / average payable days shows

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

the average number of days which the company is taking to pay its current liability obligations to

its trade creditors or trade payables. This ratio shows how efficient the cash management system

of the company is to meet its current liability obligations.

Although both account payables and COGS are increasing but account payables

increased at an alarming rate of 268% since last year which is due to increase in trade payables

from £285,000 in previous year to £1,050,000 in the current year (Hasanaj and Kuqi, 2019). This

can be due to increase in levels of purchases in the current year as compared to previous year.

Therefore, payable days increased from 60 days to 170 days. Increase in payable days is

troublesome as the creditor may discontinue its business with the company and thus, shall be

decreased. Although more time the company have to pay its debts, more beneficial it is but very

delayed payments affects its credit rating and the vendor may no be satisfied, and he even may

decrease the quantum of allowed discounts therefore, reasonable payable days shall be fixed. In

this case payable days of 170 days is very high and definitely against the interest of the company.

Recommendation:

As per the above calculations and interpretations, it can be observed that return on capital

employed is decreasing, net profit margin is decreasing, current ratio is decreasing, debtor

collection period is increasing and creditor payment period is also increasing therefore, it is not

advisable to invest the Alpha Limited as all the ratios shows unfavourable results.

CONCLUSION

The following report is made on topic financial decision making using various finance

and accounting functions also including ratio analysis with two years’ data of Alpha Ltd. The

main objective of accounting and financing functions are to provide information about the

financial position, financial performance and changes in the financial performance of the

company. The current ratio indicates the short term financial positon which is declining. Its

shows that there are problems with inventory management, low standards for collecting

receivables whereas activity ratios show the increase in debtors and creditors collection period

which show the inefficiency of performance of Alpha Ltd. with increase in both the collection

days. The financial performance of the Alpha Ltd. for the 2 years is analysed and it is proved that

the company is not financially sound. As all the ratios comes out with unfavourable result

therefore its recommended that it is not advisable to invest in Alpha Ltd.

its trade creditors or trade payables. This ratio shows how efficient the cash management system

of the company is to meet its current liability obligations.

Although both account payables and COGS are increasing but account payables

increased at an alarming rate of 268% since last year which is due to increase in trade payables

from £285,000 in previous year to £1,050,000 in the current year (Hasanaj and Kuqi, 2019). This

can be due to increase in levels of purchases in the current year as compared to previous year.

Therefore, payable days increased from 60 days to 170 days. Increase in payable days is

troublesome as the creditor may discontinue its business with the company and thus, shall be

decreased. Although more time the company have to pay its debts, more beneficial it is but very

delayed payments affects its credit rating and the vendor may no be satisfied, and he even may

decrease the quantum of allowed discounts therefore, reasonable payable days shall be fixed. In

this case payable days of 170 days is very high and definitely against the interest of the company.

Recommendation:

As per the above calculations and interpretations, it can be observed that return on capital

employed is decreasing, net profit margin is decreasing, current ratio is decreasing, debtor

collection period is increasing and creditor payment period is also increasing therefore, it is not

advisable to invest the Alpha Limited as all the ratios shows unfavourable results.

CONCLUSION

The following report is made on topic financial decision making using various finance

and accounting functions also including ratio analysis with two years’ data of Alpha Ltd. The

main objective of accounting and financing functions are to provide information about the

financial position, financial performance and changes in the financial performance of the

company. The current ratio indicates the short term financial positon which is declining. Its

shows that there are problems with inventory management, low standards for collecting

receivables whereas activity ratios show the increase in debtors and creditors collection period

which show the inefficiency of performance of Alpha Ltd. with increase in both the collection

days. The financial performance of the Alpha Ltd. for the 2 years is analysed and it is proved that

the company is not financially sound. As all the ratios comes out with unfavourable result

therefore its recommended that it is not advisable to invest in Alpha Ltd.

REFERENCES

Books and Journals

Eldomiaty, T. I., Bahaa El Din, M. and Atia, O., 2018. Modeling growth rates and anomalies of

financing, investment and dividend decisions. International Journal of Modelling and

Simulation. 38(3). pp.159-167.

Gutsalenko, L. and et. al., 2018. Accounting control of capital investment management: realities

of Ukraine and Poland. Economic annals-XXI. (170). pp.79-84.

Jowett, M. and et. al., 2020. Health financing policy & implementation in fragile & conflict-

affected settings: A synthesis of evidence and policy recommendations.

Kotsupatriy, M., and et. al., 2020. Use of international accounting and financial reporting

standards in enterprise management. International Journal of Management. 11(5).

Muda, I.and et. al., 2018, March. Model application of Murabahah financing acknowledgement

statement of Sharia accounting standard No 59 Year 2002. In IOP Conference Series:

Earth and Environmental Science (Vol. 126, No. 1, p. 012071). IOP Publishing.

Ross, J., Shi, L. and Xie, H., 2019. The determinants of accounting comparability around the

world. Asian Review of Accounting.

Zéman, Z., 2019. The extended functions of strategic controlling in relation to the value creation

of sustainable development. Visegrad Journal on Bioeconomy and Sustainable

Development. 8(1). pp.47-52.

Afolabi, A. and et.al., 2019. Does leverage affect the financial performance of Nigerian firms?.

Journal of Economics & Management, 37. pp.5-22.

Nariswari, T. N. and Nugraha, N. M., 2020. Profit growth: impact of net profit margin, gross

profit margin and total assests turnover. International Journal of Finance & Banking

Studies (2147-4486), 9(4). pp.87-96.

Irman, M. and Purwati, A. A., 2020. Analysis on the influence of current ratio, debt to equity

ratio and total asset turnover toward return on assets on the otomotive and component

company that has been registered in Indonesia Stock Exchange Within 2011-2017.

International Journal of Economics Development Research (IJEDR), 1(1). pp.36-44.

Oksanen, A. and et.al., 2018. Problem gambling and psychological distress: A cross-national

perspective on the mediating effect of consumer debt and debt problems among

emerging adults. Harm Reduction Journal, 15(1). pp.1-11.

Hasanaj, P. and Kuqi, B., 2019. Analysis of financial statements. Humanities and Social Science

Research, 2(2). pp.p17-p17.

Rashid, C. A., 2018. Efficiency of financial ratios analysis for evaluating companies’ liquidity.

International Journal of Social Sciences & Educational Studies, 4(4). p.110.

Alabdullah, T. T. Y., 2022. Management accounting insight via a new perspective on risk

management-companies' profitability relationship. International Journal of Intelligent

Enterprise,9(2). pp.244-257.

Online

London Business training and Consulting. 2022. [Online]. Available through: <

https://www.lbtc.co.uk/accounting-finance-banking-blog/role-accounting-finance-

department/ >

What are Financial Ratios? 2022. [online]. Available through:

<https://corporatefinanceinstitute.com/resources/knowledge/finance/financial-ratios/>

Books and Journals

Eldomiaty, T. I., Bahaa El Din, M. and Atia, O., 2018. Modeling growth rates and anomalies of

financing, investment and dividend decisions. International Journal of Modelling and

Simulation. 38(3). pp.159-167.

Gutsalenko, L. and et. al., 2018. Accounting control of capital investment management: realities

of Ukraine and Poland. Economic annals-XXI. (170). pp.79-84.

Jowett, M. and et. al., 2020. Health financing policy & implementation in fragile & conflict-

affected settings: A synthesis of evidence and policy recommendations.

Kotsupatriy, M., and et. al., 2020. Use of international accounting and financial reporting

standards in enterprise management. International Journal of Management. 11(5).

Muda, I.and et. al., 2018, March. Model application of Murabahah financing acknowledgement

statement of Sharia accounting standard No 59 Year 2002. In IOP Conference Series:

Earth and Environmental Science (Vol. 126, No. 1, p. 012071). IOP Publishing.

Ross, J., Shi, L. and Xie, H., 2019. The determinants of accounting comparability around the

world. Asian Review of Accounting.

Zéman, Z., 2019. The extended functions of strategic controlling in relation to the value creation

of sustainable development. Visegrad Journal on Bioeconomy and Sustainable

Development. 8(1). pp.47-52.

Afolabi, A. and et.al., 2019. Does leverage affect the financial performance of Nigerian firms?.

Journal of Economics & Management, 37. pp.5-22.

Nariswari, T. N. and Nugraha, N. M., 2020. Profit growth: impact of net profit margin, gross

profit margin and total assests turnover. International Journal of Finance & Banking

Studies (2147-4486), 9(4). pp.87-96.

Irman, M. and Purwati, A. A., 2020. Analysis on the influence of current ratio, debt to equity

ratio and total asset turnover toward return on assets on the otomotive and component

company that has been registered in Indonesia Stock Exchange Within 2011-2017.

International Journal of Economics Development Research (IJEDR), 1(1). pp.36-44.

Oksanen, A. and et.al., 2018. Problem gambling and psychological distress: A cross-national

perspective on the mediating effect of consumer debt and debt problems among

emerging adults. Harm Reduction Journal, 15(1). pp.1-11.

Hasanaj, P. and Kuqi, B., 2019. Analysis of financial statements. Humanities and Social Science

Research, 2(2). pp.p17-p17.

Rashid, C. A., 2018. Efficiency of financial ratios analysis for evaluating companies’ liquidity.

International Journal of Social Sciences & Educational Studies, 4(4). p.110.

Alabdullah, T. T. Y., 2022. Management accounting insight via a new perspective on risk

management-companies' profitability relationship. International Journal of Intelligent

Enterprise,9(2). pp.244-257.

Online

London Business training and Consulting. 2022. [Online]. Available through: <

https://www.lbtc.co.uk/accounting-finance-banking-blog/role-accounting-finance-

department/ >

What are Financial Ratios? 2022. [online]. Available through:

<https://corporatefinanceinstitute.com/resources/knowledge/finance/financial-ratios/>

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.