Business Accounting: Financial Analysis and Management Costing

VerifiedAdded on 2024/05/17

|10

|2502

|482

Report

AI Summary

This report provides a detailed analysis of financial decision-making in business accounting, focusing on management costing techniques, the importance of final accounts to stakeholders, and the application of ratio analysis to evaluate a business's financial state. It uses examples like Agros, a UK-based company, to demonstrate how absorption and marginal costing can influence management decisions. The report also emphasizes the significance of final accounts (trading account, profit and loss statement, and balance sheet) for investors, management, government, auditors, employees, creditors, and banks. Furthermore, it evaluates the financial health of Tesco Plc through profitability, liquidity, efficiency, and gearing ratios, highlighting the usefulness of financial ratios in understanding a company's performance trends and future prospects. Desklib provides access to similar solved assignments and study resources for students.

BUSINESS ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of contents

Introduction................................................................................................................................3

2.1 Evaluate the business decision using the techniques of management costing.....................3

3.1 Discuss the reasons for the importance of final accounts to the stakeholders of a business5

4.1 Evaluate the financial state of a business through the application of the techniques of ratio

analysis.......................................................................................................................................7

Conclusion..................................................................................................................................9

Reference list............................................................................................................................10

2 | P a g e

Introduction................................................................................................................................3

2.1 Evaluate the business decision using the techniques of management costing.....................3

3.1 Discuss the reasons for the importance of final accounts to the stakeholders of a business5

4.1 Evaluate the financial state of a business through the application of the techniques of ratio

analysis.......................................................................................................................................7

Conclusion..................................................................................................................................9

Reference list............................................................................................................................10

2 | P a g e

Introduction

Financial decision making is a very crucial but a lengthy process. In the process of financial

decision making, the management of any organization needs to analyze and revaluate several

factors like, cost, profit, assets and liabilities, on which the financial state of the business

depends. In this study, the focus will be made on the financial decision making process at

Agros, which is an UK-based company. This study will aim to evaluate how the management

costing techniques can help the management of Agros in business decision making. At the

same time, it will also analyze the importance of final accounts to the stakeholders and the

usability of financial ratios.

2.1 Evaluate the business decision using the techniques of management costing

As stated in the introductory part of the study that financial or business decision making is a

crucial and lengthy process, it is obvious that this process involves several activities.

Management costing is one of the critical activities that play major role in the decision

making process (Herath and Lu 2017). The primary aim of management costing is to identify,

evaluate, analyze and control the costs of the business (Narasimhan 2017). It aims to maintain

the costs of the company at the lowest level. There are several techniques under the system of

management costing that are useful to the management of Agros. Some of the techniques are

discussed below:

Absorption costing technique

Marginal costing technique (Brierley 2017)

The use of these two management costing techniques in the business decision making can be

better understood with the help of the following example:

Using the absorption costing:

Example: Agros is selling 1000 units £30 each unit

Cost of direct material £10 per unit

Cost of labour £8 per unit

Variable overhead £4 per unit

3 | P a g e

Financial decision making is a very crucial but a lengthy process. In the process of financial

decision making, the management of any organization needs to analyze and revaluate several

factors like, cost, profit, assets and liabilities, on which the financial state of the business

depends. In this study, the focus will be made on the financial decision making process at

Agros, which is an UK-based company. This study will aim to evaluate how the management

costing techniques can help the management of Agros in business decision making. At the

same time, it will also analyze the importance of final accounts to the stakeholders and the

usability of financial ratios.

2.1 Evaluate the business decision using the techniques of management costing

As stated in the introductory part of the study that financial or business decision making is a

crucial and lengthy process, it is obvious that this process involves several activities.

Management costing is one of the critical activities that play major role in the decision

making process (Herath and Lu 2017). The primary aim of management costing is to identify,

evaluate, analyze and control the costs of the business (Narasimhan 2017). It aims to maintain

the costs of the company at the lowest level. There are several techniques under the system of

management costing that are useful to the management of Agros. Some of the techniques are

discussed below:

Absorption costing technique

Marginal costing technique (Brierley 2017)

The use of these two management costing techniques in the business decision making can be

better understood with the help of the following example:

Using the absorption costing:

Example: Agros is selling 1000 units £30 each unit

Cost of direct material £10 per unit

Cost of labour £8 per unit

Variable overhead £4 per unit

3 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Fixed overhead £6000

Number of units produced 1100 units

Opening stock 50 units

Selling and distribution overhead £1800

Calculations:

Calculating the absorption cost:

Direct material £10

Direct labour £8

Variable overhead £4

Fixed overhead £6

Total absorption £28

Therefore, the operating income will be as follows:

Sales (1000 units * £30) £30000

Less cost of goods sold (1000 units £28) £28000

Gross profit £2000

Less: Selling and distribution overhead £1800

Operating income £200

Considering the above calculations, it can be stated that if the management of Agros uses the

absorption costing method, the business will generate total £200 operating income, which

will not be very high. Therefore, considering this management costing technique, the

management of the company may decide to control the costs of raw material and labour,

which are very high. At the same time, the management may also decide that they need to

enhance the sales quantity to generate more revenue.

Using the marginal costing technique:

Considering the same example, the marginal cost is calculated below:

Opening stock = 50 units * £28

4 | P a g e

Number of units produced 1100 units

Opening stock 50 units

Selling and distribution overhead £1800

Calculations:

Calculating the absorption cost:

Direct material £10

Direct labour £8

Variable overhead £4

Fixed overhead £6

Total absorption £28

Therefore, the operating income will be as follows:

Sales (1000 units * £30) £30000

Less cost of goods sold (1000 units £28) £28000

Gross profit £2000

Less: Selling and distribution overhead £1800

Operating income £200

Considering the above calculations, it can be stated that if the management of Agros uses the

absorption costing method, the business will generate total £200 operating income, which

will not be very high. Therefore, considering this management costing technique, the

management of the company may decide to control the costs of raw material and labour,

which are very high. At the same time, the management may also decide that they need to

enhance the sales quantity to generate more revenue.

Using the marginal costing technique:

Considering the same example, the marginal cost is calculated below:

Opening stock = 50 units * £28

4 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

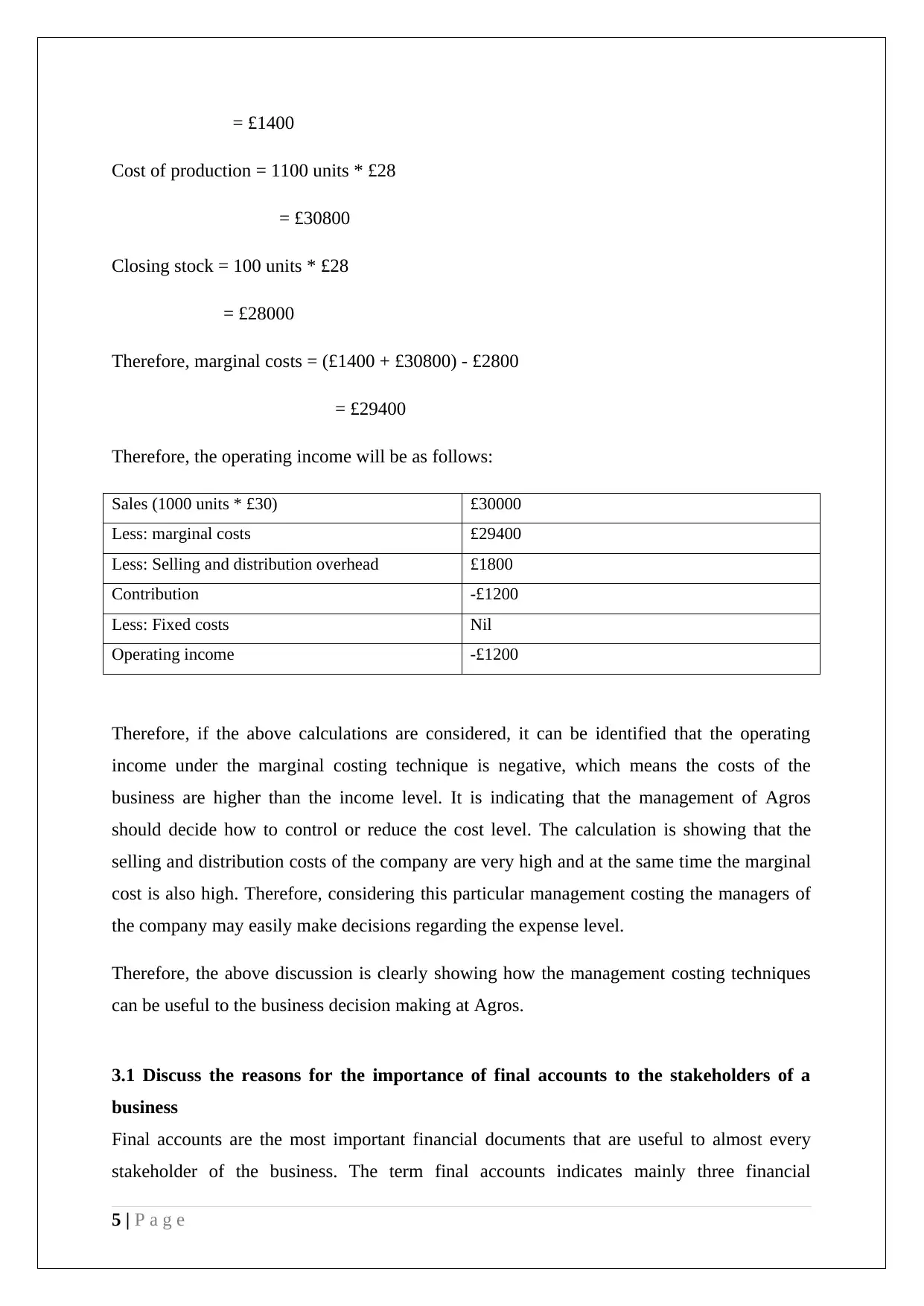

= £1400

Cost of production = 1100 units * £28

= £30800

Closing stock = 100 units * £28

= £28000

Therefore, marginal costs = (£1400 + £30800) - £2800

= £29400

Therefore, the operating income will be as follows:

Sales (1000 units * £30) £30000

Less: marginal costs £29400

Less: Selling and distribution overhead £1800

Contribution -£1200

Less: Fixed costs Nil

Operating income -£1200

Therefore, if the above calculations are considered, it can be identified that the operating

income under the marginal costing technique is negative, which means the costs of the

business are higher than the income level. It is indicating that the management of Agros

should decide how to control or reduce the cost level. The calculation is showing that the

selling and distribution costs of the company are very high and at the same time the marginal

cost is also high. Therefore, considering this particular management costing the managers of

the company may easily make decisions regarding the expense level.

Therefore, the above discussion is clearly showing how the management costing techniques

can be useful to the business decision making at Agros.

3.1 Discuss the reasons for the importance of final accounts to the stakeholders of a

business

Final accounts are the most important financial documents that are useful to almost every

stakeholder of the business. The term final accounts indicates mainly three financial

5 | P a g e

Cost of production = 1100 units * £28

= £30800

Closing stock = 100 units * £28

= £28000

Therefore, marginal costs = (£1400 + £30800) - £2800

= £29400

Therefore, the operating income will be as follows:

Sales (1000 units * £30) £30000

Less: marginal costs £29400

Less: Selling and distribution overhead £1800

Contribution -£1200

Less: Fixed costs Nil

Operating income -£1200

Therefore, if the above calculations are considered, it can be identified that the operating

income under the marginal costing technique is negative, which means the costs of the

business are higher than the income level. It is indicating that the management of Agros

should decide how to control or reduce the cost level. The calculation is showing that the

selling and distribution costs of the company are very high and at the same time the marginal

cost is also high. Therefore, considering this particular management costing the managers of

the company may easily make decisions regarding the expense level.

Therefore, the above discussion is clearly showing how the management costing techniques

can be useful to the business decision making at Agros.

3.1 Discuss the reasons for the importance of final accounts to the stakeholders of a

business

Final accounts are the most important financial documents that are useful to almost every

stakeholder of the business. The term final accounts indicates mainly three financial

5 | P a g e

documents and these are – trading account, profit and loss statement and balance sheet

statement (Geiszler et al. 2017). In the current scenario, the cash flow statement is also

considered as the important financial document under the final accounts of the company.

If the reasons for the importance of the final accounts are critically discussed and analyzed, it

can be identified that without using the final accounts the investment and other business

financial decisions are impossible. An investor is the stakeholder of the company. While

making an investment decision, the investor always verify the profitability, liquidity and

efficiency level of the business and at the same time, the investor also reviews the capital

structure of the company (Krishnan and Joshi 2017). This information is available in the final

accounts of the business. For example, in the profit and loss statement the investors get the

information regarding the profitability of the company. Similarly, in the balance sheet

statement, the information related to the liquidity, capital structure and efficiency level of the

business will be available (Reid and Myddelton 2017). Therefore, it can be stated that using

the information in the final accounts, the investors can easily decide whether or not the

investment in this particular company will be suitable.

Apart from the investors, the final accounts are also useful to the management of the

company. The management can review the financial performance or financial state of the

business with the help of the final accounts. At the same time, it can also be stated that using

the final accounts, the management can compare the financial performance standard of the

business between two years (Krishnan and Joshi 2017). This makes the decision making

process easier for the management. On the other hand, using the final accounts, the

government can easily decide the tax liability of the company in a particular accounting year

(Beams et al. 2017).

The final accounts are also important to the auditors of the firm. The auditors can check

whether or not the company has disclosed its financial position property (Titman et al. 2017).

The auditors can also identify the fraud cases using the final accounts. In the case of the

employees, it can be stated that using the final accounts they can understand the financial

position of the company on which their job security depends.

At the same time, it can also be stated that using the final accounts of the company, the

creditors and banks can decide, whether they should provide loan to the company or they

must refuse the loan applications.

6 | P a g e

statement (Geiszler et al. 2017). In the current scenario, the cash flow statement is also

considered as the important financial document under the final accounts of the company.

If the reasons for the importance of the final accounts are critically discussed and analyzed, it

can be identified that without using the final accounts the investment and other business

financial decisions are impossible. An investor is the stakeholder of the company. While

making an investment decision, the investor always verify the profitability, liquidity and

efficiency level of the business and at the same time, the investor also reviews the capital

structure of the company (Krishnan and Joshi 2017). This information is available in the final

accounts of the business. For example, in the profit and loss statement the investors get the

information regarding the profitability of the company. Similarly, in the balance sheet

statement, the information related to the liquidity, capital structure and efficiency level of the

business will be available (Reid and Myddelton 2017). Therefore, it can be stated that using

the information in the final accounts, the investors can easily decide whether or not the

investment in this particular company will be suitable.

Apart from the investors, the final accounts are also useful to the management of the

company. The management can review the financial performance or financial state of the

business with the help of the final accounts. At the same time, it can also be stated that using

the final accounts, the management can compare the financial performance standard of the

business between two years (Krishnan and Joshi 2017). This makes the decision making

process easier for the management. On the other hand, using the final accounts, the

government can easily decide the tax liability of the company in a particular accounting year

(Beams et al. 2017).

The final accounts are also important to the auditors of the firm. The auditors can check

whether or not the company has disclosed its financial position property (Titman et al. 2017).

The auditors can also identify the fraud cases using the final accounts. In the case of the

employees, it can be stated that using the final accounts they can understand the financial

position of the company on which their job security depends.

At the same time, it can also be stated that using the final accounts of the company, the

creditors and banks can decide, whether they should provide loan to the company or they

must refuse the loan applications.

6 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

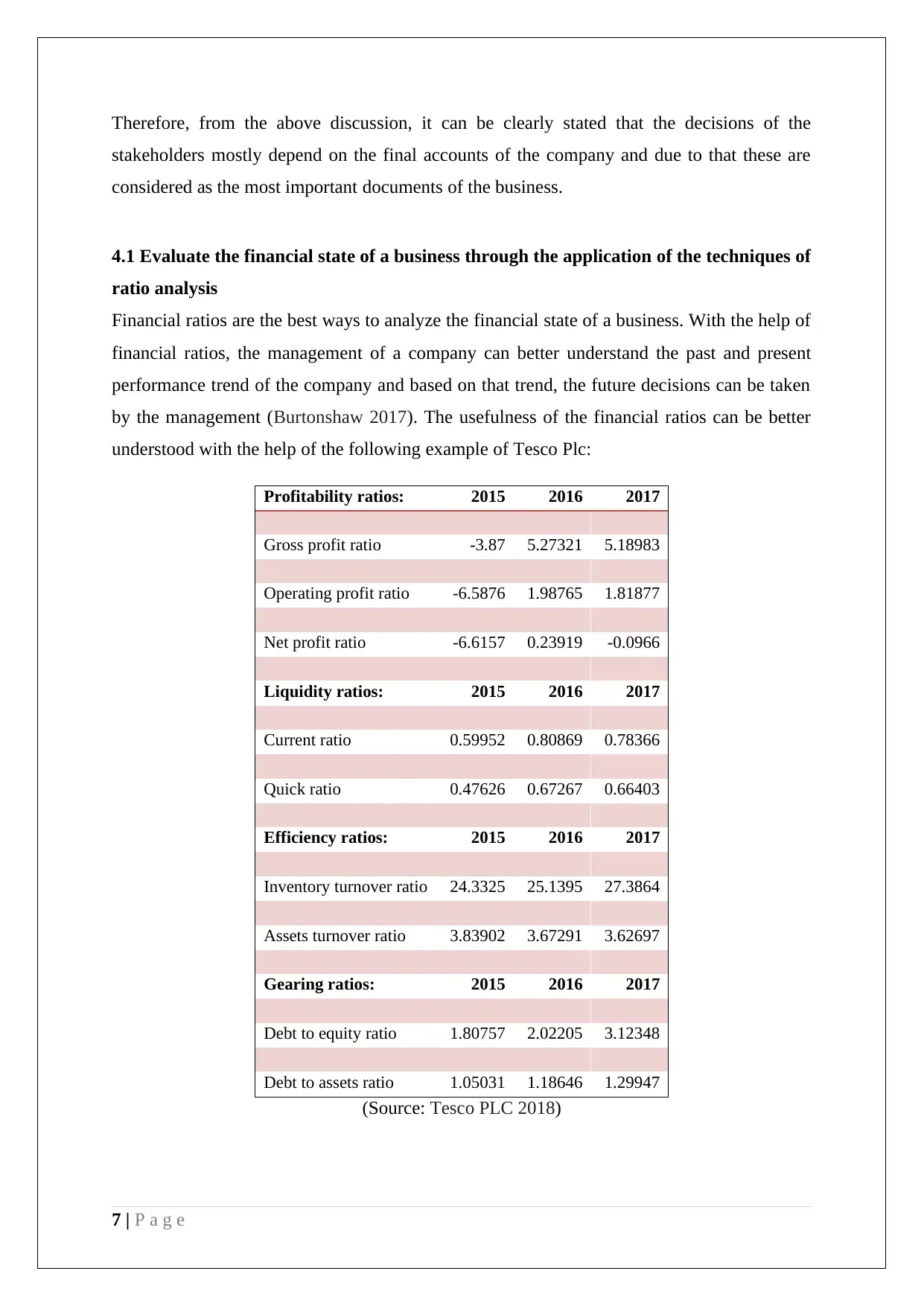

Therefore, from the above discussion, it can be clearly stated that the decisions of the

stakeholders mostly depend on the final accounts of the company and due to that these are

considered as the most important documents of the business.

4.1 Evaluate the financial state of a business through the application of the techniques of

ratio analysis

Financial ratios are the best ways to analyze the financial state of a business. With the help of

financial ratios, the management of a company can better understand the past and present

performance trend of the company and based on that trend, the future decisions can be taken

by the management (Burtonshaw 2017). The usefulness of the financial ratios can be better

understood with the help of the following example of Tesco Plc:

Profitability ratios: 2015 2016 2017

Gross profit ratio -3.87 5.27321 5.18983

Operating profit ratio -6.5876 1.98765 1.81877

Net profit ratio -6.6157 0.23919 -0.0966

Liquidity ratios: 2015 2016 2017

Current ratio 0.59952 0.80869 0.78366

Quick ratio 0.47626 0.67267 0.66403

Efficiency ratios: 2015 2016 2017

Inventory turnover ratio 24.3325 25.1395 27.3864

Assets turnover ratio 3.83902 3.67291 3.62697

Gearing ratios: 2015 2016 2017

Debt to equity ratio 1.80757 2.02205 3.12348

Debt to assets ratio 1.05031 1.18646 1.29947

(Source: Tesco PLC 2018)

7 | P a g e

stakeholders mostly depend on the final accounts of the company and due to that these are

considered as the most important documents of the business.

4.1 Evaluate the financial state of a business through the application of the techniques of

ratio analysis

Financial ratios are the best ways to analyze the financial state of a business. With the help of

financial ratios, the management of a company can better understand the past and present

performance trend of the company and based on that trend, the future decisions can be taken

by the management (Burtonshaw 2017). The usefulness of the financial ratios can be better

understood with the help of the following example of Tesco Plc:

Profitability ratios: 2015 2016 2017

Gross profit ratio -3.87 5.27321 5.18983

Operating profit ratio -6.5876 1.98765 1.81877

Net profit ratio -6.6157 0.23919 -0.0966

Liquidity ratios: 2015 2016 2017

Current ratio 0.59952 0.80869 0.78366

Quick ratio 0.47626 0.67267 0.66403

Efficiency ratios: 2015 2016 2017

Inventory turnover ratio 24.3325 25.1395 27.3864

Assets turnover ratio 3.83902 3.67291 3.62697

Gearing ratios: 2015 2016 2017

Debt to equity ratio 1.80757 2.02205 3.12348

Debt to assets ratio 1.05031 1.18646 1.29947

(Source: Tesco PLC 2018)

7 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The above table is showing the financial ratios of Tesco Plc for the last three years.

Considering this particular table, the financial state of Tesco Plc can be easily understood. If

the profitability ratios mentioned in the above table are considered, it can be identified that

the profitability position of the company in between 2015 to 2017 was very poor. The gross

profit ratio of the company has improved, but the net profit ratio and operating profit ratios

were still very low. The company could not meet the industry averages also. The lower level

of the profitability ratios for the last three years is indicating that the management of Tesco

Plc is failure to control the direct and indirect costs of the business. The profitability ratios of

the company are clearly indicating weak financial state of the business.

On the other hand, if the liquidity ratios of the company that are mentioned in the above table

are considered, it can be identified that the liquidity position of the company was also very

poor. The current ratios and the quick ratios are showing that the short-term assets were not

enough for meeting the short-term liabilities of the firm. The liabilities of the company were

so high, which has made the financial state of the business weak. This is also indicating that

in the near future, the company may face huge trouble in meeting its liabilities, which will

affect its long-term sustainability also.

The efficiency ratios of the company that are inventory turnover ratios and the assets turnover

ratios are indicating that the efficiency level of Tesco Plc was also very poor. The inventory

turnover ratios during the last three years were fluctuating, which denotes that the sales level

of the business was also bit fluctuating. At the same time, it also denotes that the management

of the company was not capable of maintaining the sales level during these years. On the

other hand, the assets turnover ratios are showing that the capacity of the company to utilize

its assets was very poor. The company could not generate much revenue by using its assets.

In the other words, it can be stated that the contribution made by the assets of Tesco was very

low in the revenue of the company.

Lastly, the gearing ratios of the company are indicating that the risk level in the capital

structure of the company was very high in between 2015 to 2017. The risk level was high

because the ratio of debt capital in the capital structure was much higher than the ratio of

equity capital. Inclusion of more debt capital has enhanced the risk level in the capital

structure. On the other hand, the debt to assets ratios for the three years is showing that the

company has used much debt capital in the assets of the business. It means that the assets of

Tesco Plc are riskier, which is not good for the future sustainability of the company.

8 | P a g e

Considering this particular table, the financial state of Tesco Plc can be easily understood. If

the profitability ratios mentioned in the above table are considered, it can be identified that

the profitability position of the company in between 2015 to 2017 was very poor. The gross

profit ratio of the company has improved, but the net profit ratio and operating profit ratios

were still very low. The company could not meet the industry averages also. The lower level

of the profitability ratios for the last three years is indicating that the management of Tesco

Plc is failure to control the direct and indirect costs of the business. The profitability ratios of

the company are clearly indicating weak financial state of the business.

On the other hand, if the liquidity ratios of the company that are mentioned in the above table

are considered, it can be identified that the liquidity position of the company was also very

poor. The current ratios and the quick ratios are showing that the short-term assets were not

enough for meeting the short-term liabilities of the firm. The liabilities of the company were

so high, which has made the financial state of the business weak. This is also indicating that

in the near future, the company may face huge trouble in meeting its liabilities, which will

affect its long-term sustainability also.

The efficiency ratios of the company that are inventory turnover ratios and the assets turnover

ratios are indicating that the efficiency level of Tesco Plc was also very poor. The inventory

turnover ratios during the last three years were fluctuating, which denotes that the sales level

of the business was also bit fluctuating. At the same time, it also denotes that the management

of the company was not capable of maintaining the sales level during these years. On the

other hand, the assets turnover ratios are showing that the capacity of the company to utilize

its assets was very poor. The company could not generate much revenue by using its assets.

In the other words, it can be stated that the contribution made by the assets of Tesco was very

low in the revenue of the company.

Lastly, the gearing ratios of the company are indicating that the risk level in the capital

structure of the company was very high in between 2015 to 2017. The risk level was high

because the ratio of debt capital in the capital structure was much higher than the ratio of

equity capital. Inclusion of more debt capital has enhanced the risk level in the capital

structure. On the other hand, the debt to assets ratios for the three years is showing that the

company has used much debt capital in the assets of the business. It means that the assets of

Tesco Plc are riskier, which is not good for the future sustainability of the company.

8 | P a g e

Therefore, from the above example of Tesco Plc, it can be easily stated that the financial

ratios of a company are enough for understanding the state of the company in the current

market.

Conclusion

In this study, it has been identified that the management costing techniques are very useful

for understanding the performance standards and making the future decision for the company.

The study has proved how the absorption costing and marginal costing techniques can help

the management of Agros in developing better decisions for the business. At the same time,

the study has also concentrated on the discussion regarding the usefulness or the importance

of the final accounts of the company and it has been determined that the final accounts of the

companies are important to internal as well as external stakeholders for various reasons.

While analyzing the usability of the financial ratios, the study has determined that the

financial ratios are very helpful in the context of understanding the profitability, liquidity and

other financial state of the business.

9 | P a g e

ratios of a company are enough for understanding the state of the company in the current

market.

Conclusion

In this study, it has been identified that the management costing techniques are very useful

for understanding the performance standards and making the future decision for the company.

The study has proved how the absorption costing and marginal costing techniques can help

the management of Agros in developing better decisions for the business. At the same time,

the study has also concentrated on the discussion regarding the usefulness or the importance

of the final accounts of the company and it has been determined that the final accounts of the

companies are important to internal as well as external stakeholders for various reasons.

While analyzing the usability of the financial ratios, the study has determined that the

financial ratios are very helpful in the context of understanding the profitability, liquidity and

other financial state of the business.

9 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Reference list

Beams, F.A., Brozovsky, J.A. and Shoulders, C.D., 2017. Advanced accounting. Pearson.

Brierley, J.A., 2017. The domination of financial accounting over product costing. Cost

Management, pp.32-40.

Burtonshaw-Gunn, S.A., 2017. Risk and financial management in construction. Routledge.

Geiszler, M., Baker, K. and Lippitt, J., 2017. Variable Activity‐Based Costing and Decision

Making. Journal of Corporate Accounting & Finance, 28(5), pp.45-52.

Herath, H.S. and Lu, X., 2017. Inference of economic truth from financial statements for

detecting earnings management: inventory costing methods from an information economics

perspective. Managerial and Decision Economics.

Krishnan, A. and Joshi, P.L., 2017. Evolution and development of management accounting

practices in Thailand. The Routledge Handbook of Accounting in Asia, p.95.

Narasimhan, M.S., 2017. Absorption vs. Marginal Costing.

Reid, W. and Myddelton, D.R., 2017. The meaning of company accounts. Routledge.

Tesco PLC. 2018. Tesco plc. Available at: https://www.tescoplc.com, 1 March 2018, from

https://www.tescoplc.com

Titman, S., Keown, A.J. and Martin, J.D., 2017. Financial management: Principles and

applications. Pearson.

10 | P a g e

Beams, F.A., Brozovsky, J.A. and Shoulders, C.D., 2017. Advanced accounting. Pearson.

Brierley, J.A., 2017. The domination of financial accounting over product costing. Cost

Management, pp.32-40.

Burtonshaw-Gunn, S.A., 2017. Risk and financial management in construction. Routledge.

Geiszler, M., Baker, K. and Lippitt, J., 2017. Variable Activity‐Based Costing and Decision

Making. Journal of Corporate Accounting & Finance, 28(5), pp.45-52.

Herath, H.S. and Lu, X., 2017. Inference of economic truth from financial statements for

detecting earnings management: inventory costing methods from an information economics

perspective. Managerial and Decision Economics.

Krishnan, A. and Joshi, P.L., 2017. Evolution and development of management accounting

practices in Thailand. The Routledge Handbook of Accounting in Asia, p.95.

Narasimhan, M.S., 2017. Absorption vs. Marginal Costing.

Reid, W. and Myddelton, D.R., 2017. The meaning of company accounts. Routledge.

Tesco PLC. 2018. Tesco plc. Available at: https://www.tescoplc.com, 1 March 2018, from

https://www.tescoplc.com

Titman, S., Keown, A.J. and Martin, J.D., 2017. Financial management: Principles and

applications. Pearson.

10 | P a g e

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.