Financial Decision Making Report: Tesco PLC Analysis, [Semester]

VerifiedAdded on 2021/02/20

|17

|4151

|29

Report

AI Summary

This report provides a comprehensive financial analysis of Tesco PLC, a major UK retailer. It begins with an overview of the company, including its mission, values, and financial situation. The core of the report focuses on ratio analysis, examining liquidity (current and quick ratios), profitability (net profit margin, operating profit), efficiency (asset turnover), and solvency ratios. The analysis spans the years 2016-2018, providing insights into Tesco's financial performance and decision-making. The report highlights trends, identifies areas of strength and weakness, and offers a clear picture of the company's financial health. The conclusion summarizes the findings and provides an overall assessment of Tesco's financial position. The report is a valuable resource for understanding financial statements and ratio analysis applied to a real-world company.

Financial Decision

Making

Making

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK...............................................................................................................................................3

Overview of company:.................................................................................................................3

Mission statement and values:.....................................................................................................3

Financial Situation:......................................................................................................................4

Ratio Analysis:.............................................................................................................................5

I. Liquidity Ratios:.......................................................................................................................5

II. Profitability Ratio:...................................................................................................................7

III. Efficiency Ratios:...................................................................................................................9

III. Solvency Ratios:..................................................................................................................11

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION...........................................................................................................................3

TASK...............................................................................................................................................3

Overview of company:.................................................................................................................3

Mission statement and values:.....................................................................................................3

Financial Situation:......................................................................................................................4

Ratio Analysis:.............................................................................................................................5

I. Liquidity Ratios:.......................................................................................................................5

II. Profitability Ratio:...................................................................................................................7

III. Efficiency Ratios:...................................................................................................................9

III. Solvency Ratios:..................................................................................................................11

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION

Financial decision making relates to a mechanisms which contribute in taking decisions

with respect to stockholder’s fund and organisation's liabilities of organisation and making

investment. It includes determining business entity's existing fiscal situation, evaluates choices,

set financial goals and identification of effective alternative. It is mainly related to borrowings

and funds allocations initially needed for making investment decisions (Lusardi and Mitchell,

2017). Core aim of making financial decision is achieving and maintaining optimum and

effective capital structure that includes decent mixture of equity and debt, in order to assure

trade-off between returns and the risk in context of shareholders. The study contains a complete

understanding of financial performance by analysing ratios, financial statements, cash flows and

other fiscal variables of company. Study also provides a clear picture of company's future

performance and action plans.

TASK

Overview of company:

Tesco is UK's one of the biggest retailer and third top grocery retailer operating business

though outlets across the UK, Asia and US. Company has made expansion through combination

of mergers and acquisition of new outlets, retail services, stores, and, by adapting or

accommodating consumers' needs. Primary intention of company is full-fill the needs of

consumers, so company is focusing on existing customers in order to target potential customer

and increase company's return. Tesco currently owns approx more than 2300 stores in UK

including Extra-large hyper-market form stores and small Express Tesco high street stores and

outlets. Company's core products are grocery and other general-purpose merchandise products

and company has also making expansion by including insurance services, banking, telephone

equipment, electrical goods and airtime (About us: Tesco Plc, 2019.). Company's step towards

“one-stop shopping” exhibits that company is trying to focus towards meeting customer's

purchasing and quality needs at one-place. Company has expanded customer's base by launching

company's online platform named Tesco.com to attracts approx one million loyal users.

Mission statement and values:

Tesco is about generating importance for clients in order to gain their lifelong allegiance,

knowing clients, being accountable for groups and also being the first to satisfy the requirements

Financial decision making relates to a mechanisms which contribute in taking decisions

with respect to stockholder’s fund and organisation's liabilities of organisation and making

investment. It includes determining business entity's existing fiscal situation, evaluates choices,

set financial goals and identification of effective alternative. It is mainly related to borrowings

and funds allocations initially needed for making investment decisions (Lusardi and Mitchell,

2017). Core aim of making financial decision is achieving and maintaining optimum and

effective capital structure that includes decent mixture of equity and debt, in order to assure

trade-off between returns and the risk in context of shareholders. The study contains a complete

understanding of financial performance by analysing ratios, financial statements, cash flows and

other fiscal variables of company. Study also provides a clear picture of company's future

performance and action plans.

TASK

Overview of company:

Tesco is UK's one of the biggest retailer and third top grocery retailer operating business

though outlets across the UK, Asia and US. Company has made expansion through combination

of mergers and acquisition of new outlets, retail services, stores, and, by adapting or

accommodating consumers' needs. Primary intention of company is full-fill the needs of

consumers, so company is focusing on existing customers in order to target potential customer

and increase company's return. Tesco currently owns approx more than 2300 stores in UK

including Extra-large hyper-market form stores and small Express Tesco high street stores and

outlets. Company's core products are grocery and other general-purpose merchandise products

and company has also making expansion by including insurance services, banking, telephone

equipment, electrical goods and airtime (About us: Tesco Plc, 2019.). Company's step towards

“one-stop shopping” exhibits that company is trying to focus towards meeting customer's

purchasing and quality needs at one-place. Company has expanded customer's base by launching

company's online platform named Tesco.com to attracts approx one million loyal users.

Mission statement and values:

Tesco is about generating importance for clients in order to gain their lifelong allegiance,

knowing clients, being accountable for groups and also being the first to satisfy the requirements

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

of clients. In reality, Tesco combines personal finance, non-food products, internet retailing and

oil retailing ect, in addition to their core food and grocery products. They always placed their

client at first, and if clients prefers what Tesco offers, they will comeback to visit store again. In

addition, company has launched a club-card system where faithful clients can obtain unique

vouchers and bonuses to fulfil the stated mission (Palepu and Healy, 2013).

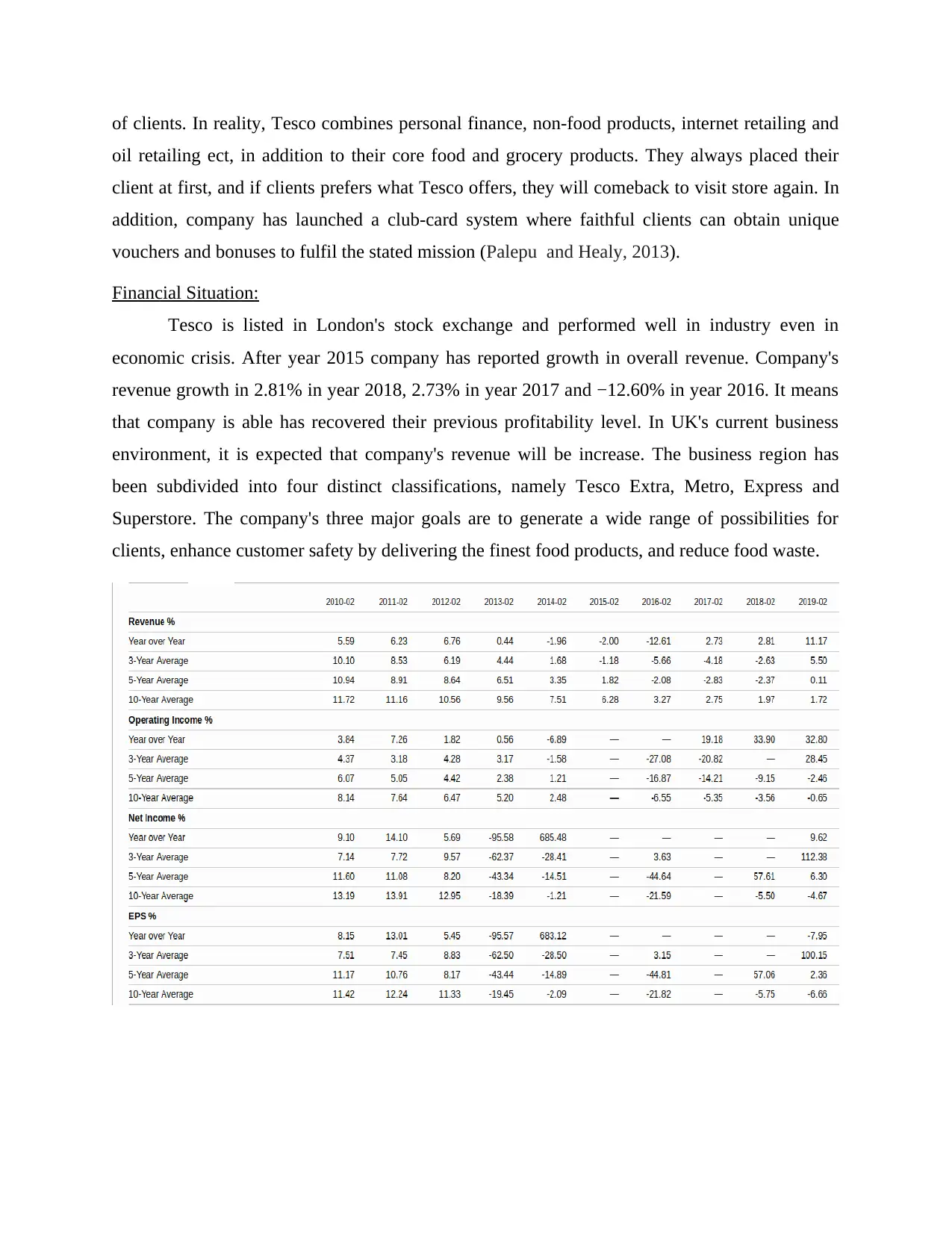

Financial Situation:

Tesco is listed in London's stock exchange and performed well in industry even in

economic crisis. After year 2015 company has reported growth in overall revenue. Company's

revenue growth in 2.81% in year 2018, 2.73% in year 2017 and −12.60% in year 2016. It means

that company is able has recovered their previous profitability level. In UK's current business

environment, it is expected that company's revenue will be increase. The business region has

been subdivided into four distinct classifications, namely Tesco Extra, Metro, Express and

Superstore. The company's three major goals are to generate a wide range of possibilities for

clients, enhance customer safety by delivering the finest food products, and reduce food waste.

oil retailing ect, in addition to their core food and grocery products. They always placed their

client at first, and if clients prefers what Tesco offers, they will comeback to visit store again. In

addition, company has launched a club-card system where faithful clients can obtain unique

vouchers and bonuses to fulfil the stated mission (Palepu and Healy, 2013).

Financial Situation:

Tesco is listed in London's stock exchange and performed well in industry even in

economic crisis. After year 2015 company has reported growth in overall revenue. Company's

revenue growth in 2.81% in year 2018, 2.73% in year 2017 and −12.60% in year 2016. It means

that company is able has recovered their previous profitability level. In UK's current business

environment, it is expected that company's revenue will be increase. The business region has

been subdivided into four distinct classifications, namely Tesco Extra, Metro, Express and

Superstore. The company's three major goals are to generate a wide range of possibilities for

clients, enhance customer safety by delivering the finest food products, and reduce food waste.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Ratio Analysis:

Analysing the ratio is comparing row products in a company's annual statements. Ratio

analysis is being used to measure a range of organization problems like liquidity, operating

sustainability, and revenue growth. This sort of assessment is especially helpful to non-business

managers as their main cause of data about an organisation is their economic reports. Ratio

analysis becomes less helpful for commercial insiders who have stronger links to company's

more comprehensive operating data (Ruff and Fehr, 2014). The information from the accounts

are being used to match the efficiency of a business over moment to evaluate whether the

business is improving or declining, to match the economic position of a business with the market

median, or to match a business with one or more businesses working in its industry to asses how

business is racking up. In this context following is ratio analysis of Tesco Plc, as follows:

I. Liquidity Ratios:

The word liquidity in accounting is described as a company's capacity to fulfil its

economic commitments as they are owing. Therefore, the liquidity ratio is indeed a calculation

used to assess the capacity of a company to cover its small-term debts. Three popular

measurements fell under the liquidity ratio classification (Graham, Harvey and Puri, 2015).

Liquidity ratios evaluate the potential of a corporation to pay off its quick-term obligations on

the basis of current or quick company assets.

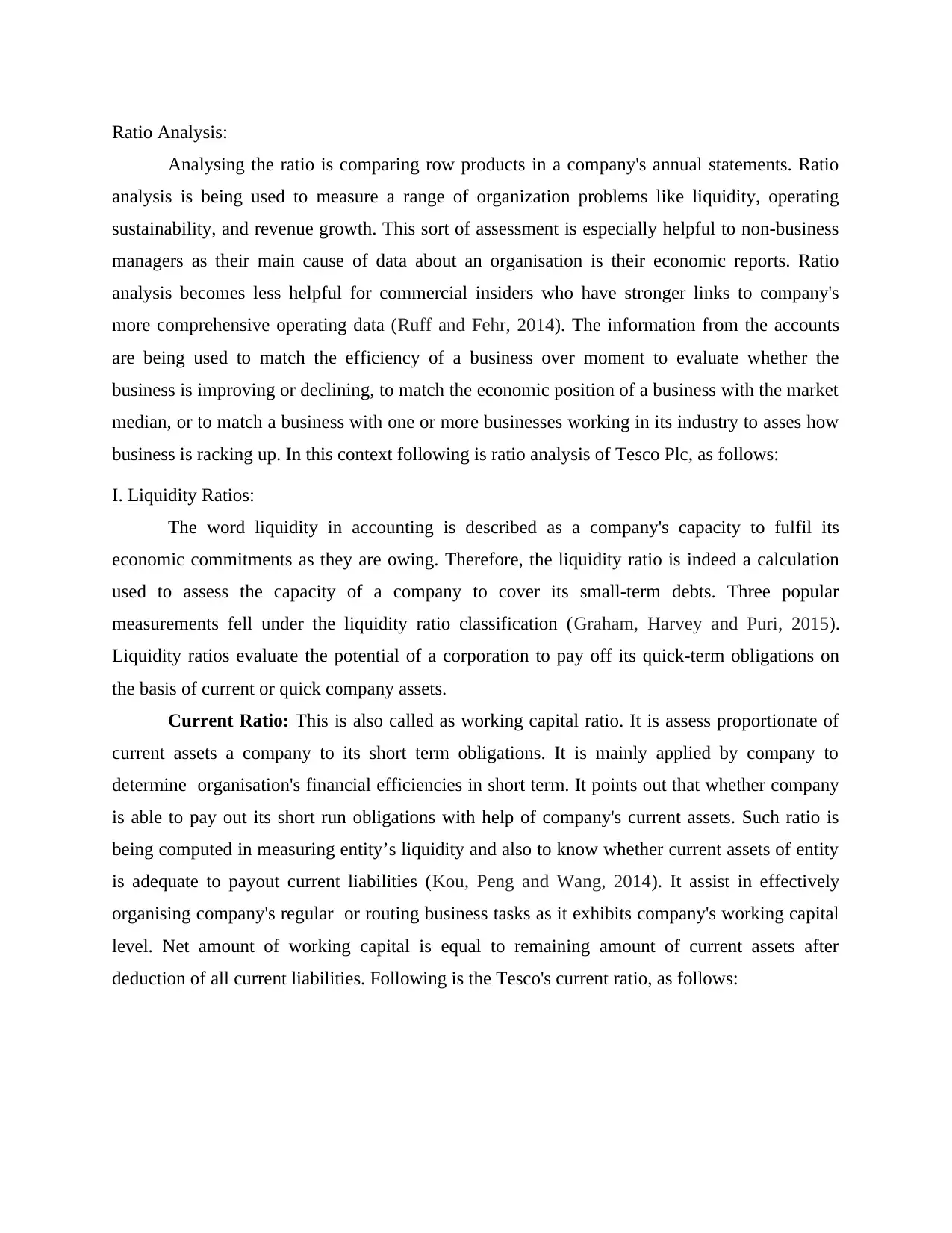

Current Ratio: This is also called as working capital ratio. It is assess proportionate of

current assets a company to its short term obligations. It is mainly applied by company to

determine organisation's financial efficiencies in short term. It points out that whether company

is able to pay out its short run obligations with help of company's current assets. Such ratio is

being computed in measuring entity’s liquidity and also to know whether current assets of entity

is adequate to payout current liabilities (Kou, Peng and Wang, 2014). It assist in effectively

organising company's regular or routing business tasks as it exhibits company's working capital

level. Net amount of working capital is equal to remaining amount of current assets after

deduction of all current liabilities. Following is the Tesco's current ratio, as follows:

Analysing the ratio is comparing row products in a company's annual statements. Ratio

analysis is being used to measure a range of organization problems like liquidity, operating

sustainability, and revenue growth. This sort of assessment is especially helpful to non-business

managers as their main cause of data about an organisation is their economic reports. Ratio

analysis becomes less helpful for commercial insiders who have stronger links to company's

more comprehensive operating data (Ruff and Fehr, 2014). The information from the accounts

are being used to match the efficiency of a business over moment to evaluate whether the

business is improving or declining, to match the economic position of a business with the market

median, or to match a business with one or more businesses working in its industry to asses how

business is racking up. In this context following is ratio analysis of Tesco Plc, as follows:

I. Liquidity Ratios:

The word liquidity in accounting is described as a company's capacity to fulfil its

economic commitments as they are owing. Therefore, the liquidity ratio is indeed a calculation

used to assess the capacity of a company to cover its small-term debts. Three popular

measurements fell under the liquidity ratio classification (Graham, Harvey and Puri, 2015).

Liquidity ratios evaluate the potential of a corporation to pay off its quick-term obligations on

the basis of current or quick company assets.

Current Ratio: This is also called as working capital ratio. It is assess proportionate of

current assets a company to its short term obligations. It is mainly applied by company to

determine organisation's financial efficiencies in short term. It points out that whether company

is able to pay out its short run obligations with help of company's current assets. Such ratio is

being computed in measuring entity’s liquidity and also to know whether current assets of entity

is adequate to payout current liabilities (Kou, Peng and Wang, 2014). It assist in effectively

organising company's regular or routing business tasks as it exhibits company's working capital

level. Net amount of working capital is equal to remaining amount of current assets after

deduction of all current liabilities. Following is the Tesco's current ratio, as follows:

Above graph and table showing that Tesco's current ratio is below the ideal ratio of 2:1

which implies that company's current assets should be equal to or above the two time of overall

current obligations of company. In 2017 company has reported maximum current ratio of 0.79

which is further reduced to 0.71 in year 2018 due to reduction in current assets value. It shows

that company's efficiency to pay current liabilities trough its current assets is not adequate.

Company can improve this ratio by holding the decision of any capital purchase which require

payment in cash or by re-amortising company's term loan.

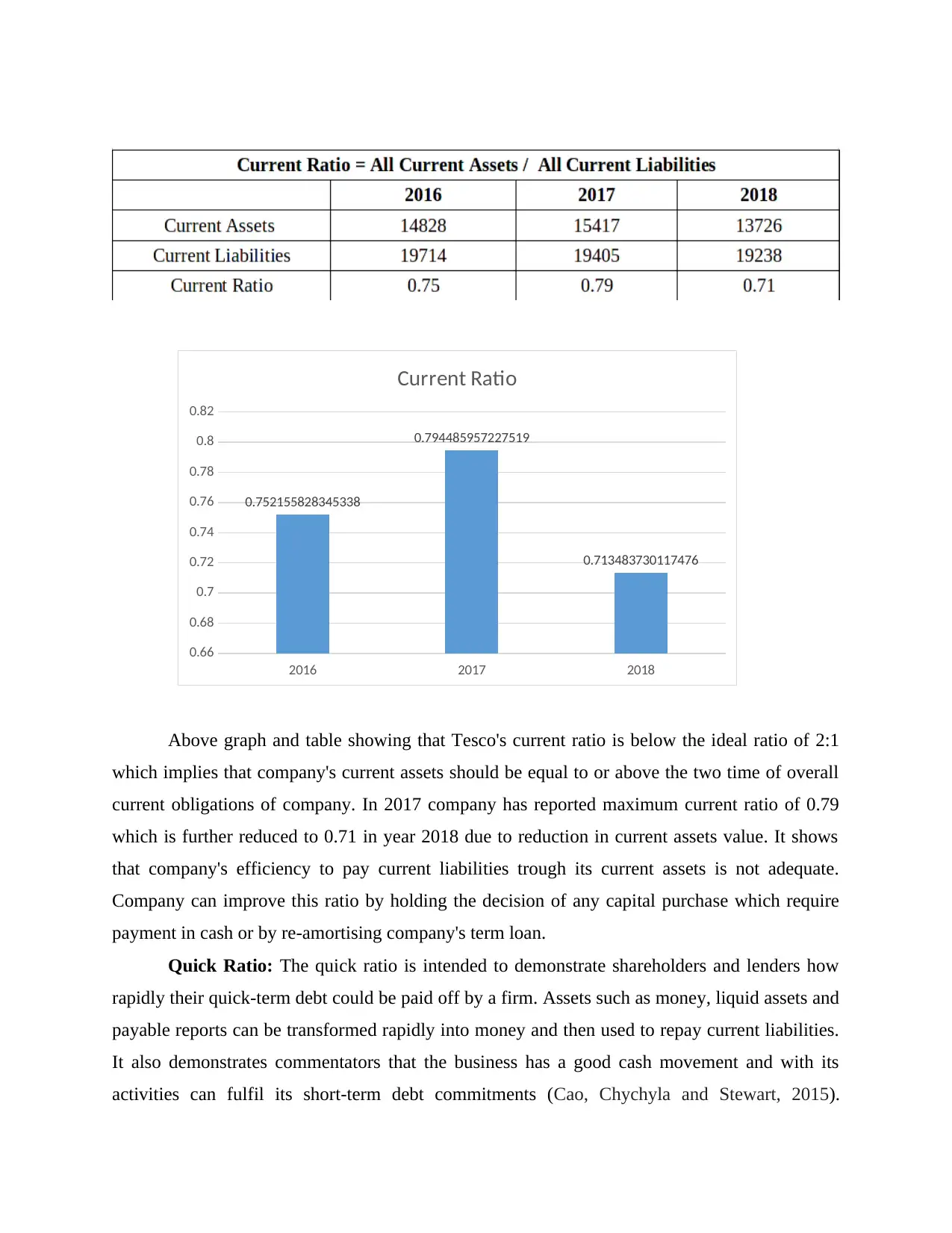

Quick Ratio: The quick ratio is intended to demonstrate shareholders and lenders how

rapidly their quick-term debt could be paid off by a firm. Assets such as money, liquid assets and

payable reports can be transformed rapidly into money and then used to repay current liabilities.

It also demonstrates commentators that the business has a good cash movement and with its

activities can fulfil its short-term debt commitments (Cao, Chychyla and Stewart, 2015).

2016 2017 2018

0.66

0.68

0.7

0.72

0.74

0.76

0.78

0.8

0.82

0.752155828345338

0.794485957227519

0.713483730117476

Current Ratio

which implies that company's current assets should be equal to or above the two time of overall

current obligations of company. In 2017 company has reported maximum current ratio of 0.79

which is further reduced to 0.71 in year 2018 due to reduction in current assets value. It shows

that company's efficiency to pay current liabilities trough its current assets is not adequate.

Company can improve this ratio by holding the decision of any capital purchase which require

payment in cash or by re-amortising company's term loan.

Quick Ratio: The quick ratio is intended to demonstrate shareholders and lenders how

rapidly their quick-term debt could be paid off by a firm. Assets such as money, liquid assets and

payable reports can be transformed rapidly into money and then used to repay current liabilities.

It also demonstrates commentators that the business has a good cash movement and with its

activities can fulfil its short-term debt commitments (Cao, Chychyla and Stewart, 2015).

2016 2017 2018

0.66

0.68

0.7

0.72

0.74

0.76

0.78

0.8

0.82

0.752155828345338

0.794485957227519

0.713483730117476

Current Ratio

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Moreover, it shows that without needing to buy long-term assets, the business is generating

enough profit to reimburse off its current liabilities. In this regard following is table exhibiting

Tesco's quick ratio, as follows:

Normally in retail industry Quick Ratio of 1:1 is considered as standard quick ratio below

which indicates need of improvement. According to above table it has been analysed that Tesco

has quick ratio below 1:1 which indicates that company's not so much efficient to pay out its

current debts utilising liquid assets. Company has reported highest quick ratio of 0.64 in year

2017 which was declined to 0.55 in year 2018. While in year 2016 it was 0.59. Company can

improve their quick ratio by utilising long-term funding instead of short-term financing in order

to finance projects and purchase inventory.

II. Profitability Ratio:

Profitability ratios are indeed the financial ratios that speak about a corporation's

profitability in contexts of its revenues or assets. Because the proportions evaluate an enterprise's

operating efficiency using earnings, they are called profitability proportions. They are also quite

helpful instruments for understanding a company's inefficiencies / inefficiencies and therefore

helping managers and shareholders adopt effective appropriate action (Lusardi and Mitchell,

2014). Following are major profitability ratios in context of Tesco, as follows:

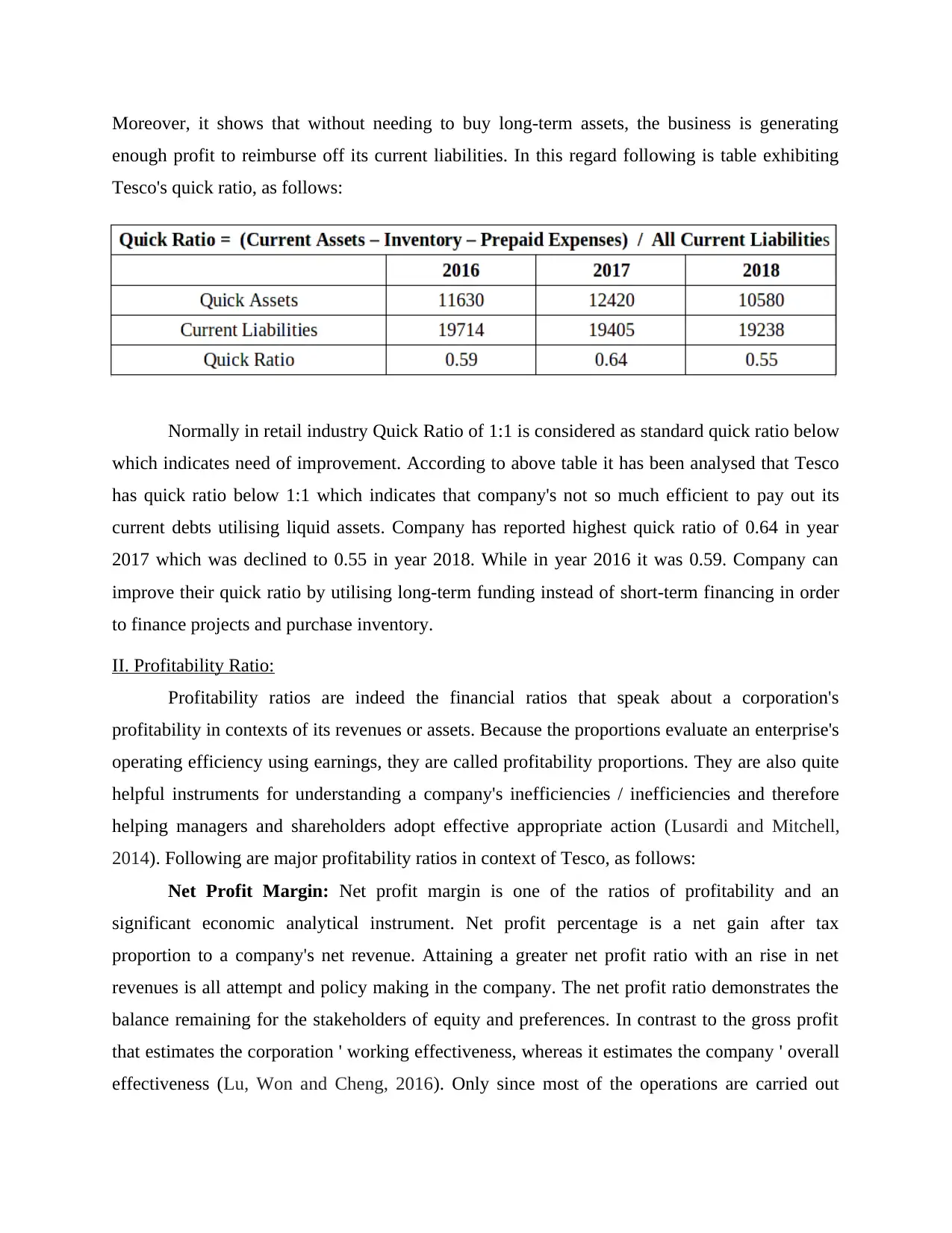

Net Profit Margin: Net profit margin is one of the ratios of profitability and an

significant economic analytical instrument. Net profit percentage is a net gain after tax

proportion to a company's net revenue. Attaining a greater net profit ratio with an rise in net

revenues is all attempt and policy making in the company. The net profit ratio demonstrates the

balance remaining for the stakeholders of equity and preferences. In contrast to the gross profit

that estimates the corporation ' working effectiveness, whereas it estimates the company ' overall

effectiveness (Lu, Won and Cheng, 2016). Only since most of the operations are carried out

enough profit to reimburse off its current liabilities. In this regard following is table exhibiting

Tesco's quick ratio, as follows:

Normally in retail industry Quick Ratio of 1:1 is considered as standard quick ratio below

which indicates need of improvement. According to above table it has been analysed that Tesco

has quick ratio below 1:1 which indicates that company's not so much efficient to pay out its

current debts utilising liquid assets. Company has reported highest quick ratio of 0.64 in year

2017 which was declined to 0.55 in year 2018. While in year 2016 it was 0.59. Company can

improve their quick ratio by utilising long-term funding instead of short-term financing in order

to finance projects and purchase inventory.

II. Profitability Ratio:

Profitability ratios are indeed the financial ratios that speak about a corporation's

profitability in contexts of its revenues or assets. Because the proportions evaluate an enterprise's

operating efficiency using earnings, they are called profitability proportions. They are also quite

helpful instruments for understanding a company's inefficiencies / inefficiencies and therefore

helping managers and shareholders adopt effective appropriate action (Lusardi and Mitchell,

2014). Following are major profitability ratios in context of Tesco, as follows:

Net Profit Margin: Net profit margin is one of the ratios of profitability and an

significant economic analytical instrument. Net profit percentage is a net gain after tax

proportion to a company's net revenue. Attaining a greater net profit ratio with an rise in net

revenues is all attempt and policy making in the company. The net profit ratio demonstrates the

balance remaining for the stakeholders of equity and preferences. In contrast to the gross profit

that estimates the corporation ' working effectiveness, whereas it estimates the company ' overall

effectiveness (Lu, Won and Cheng, 2016). Only since most of the operations are carried out

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

effectively will an appropriate percentage of net income be produced. Producing, managing,

buying, funding, shopping, tax leadership or inventory control may be the operations. Even if

any of these work poorly, it is possible to see impact on net sales and margins. Here is the net

profit ratio of Tesco, as follows:

In Tesco only in year 2017 company has suffered a net loss of 40 million and in

percentage .07% net loss. Main reason of such loss is failure of company's expansion strategy,

horse meat and accounting scandal, and rise of discounters (Tesco: Five Reasons It Went So

Wrong, 2019). However company has recovered their profitability level in year 2018 i.e. 2.1% of

net profit margin. Company's net profit margin was .25% in year 2017. But in all three years

company's turnover has been increased. Which indicates that in future company's profitability

and net margin will be increased.

Operating Profit: Ratios used to monitor expenses and to measure a company's

profitability and economic viability by indicating each piece of income statement as a proportion

2016 2017 2018

0

0.5

1

1.5

2

2.5

3

Net Profit Margin

Axis Title

buying, funding, shopping, tax leadership or inventory control may be the operations. Even if

any of these work poorly, it is possible to see impact on net sales and margins. Here is the net

profit ratio of Tesco, as follows:

In Tesco only in year 2017 company has suffered a net loss of 40 million and in

percentage .07% net loss. Main reason of such loss is failure of company's expansion strategy,

horse meat and accounting scandal, and rise of discounters (Tesco: Five Reasons It Went So

Wrong, 2019). However company has recovered their profitability level in year 2018 i.e. 2.1% of

net profit margin. Company's net profit margin was .25% in year 2017. But in all three years

company's turnover has been increased. Which indicates that in future company's profitability

and net margin will be increased.

Operating Profit: Ratios used to monitor expenses and to measure a company's

profitability and economic viability by indicating each piece of income statement as a proportion

2016 2017 2018

0

0.5

1

1.5

2

2.5

3

Net Profit Margin

Axis Title

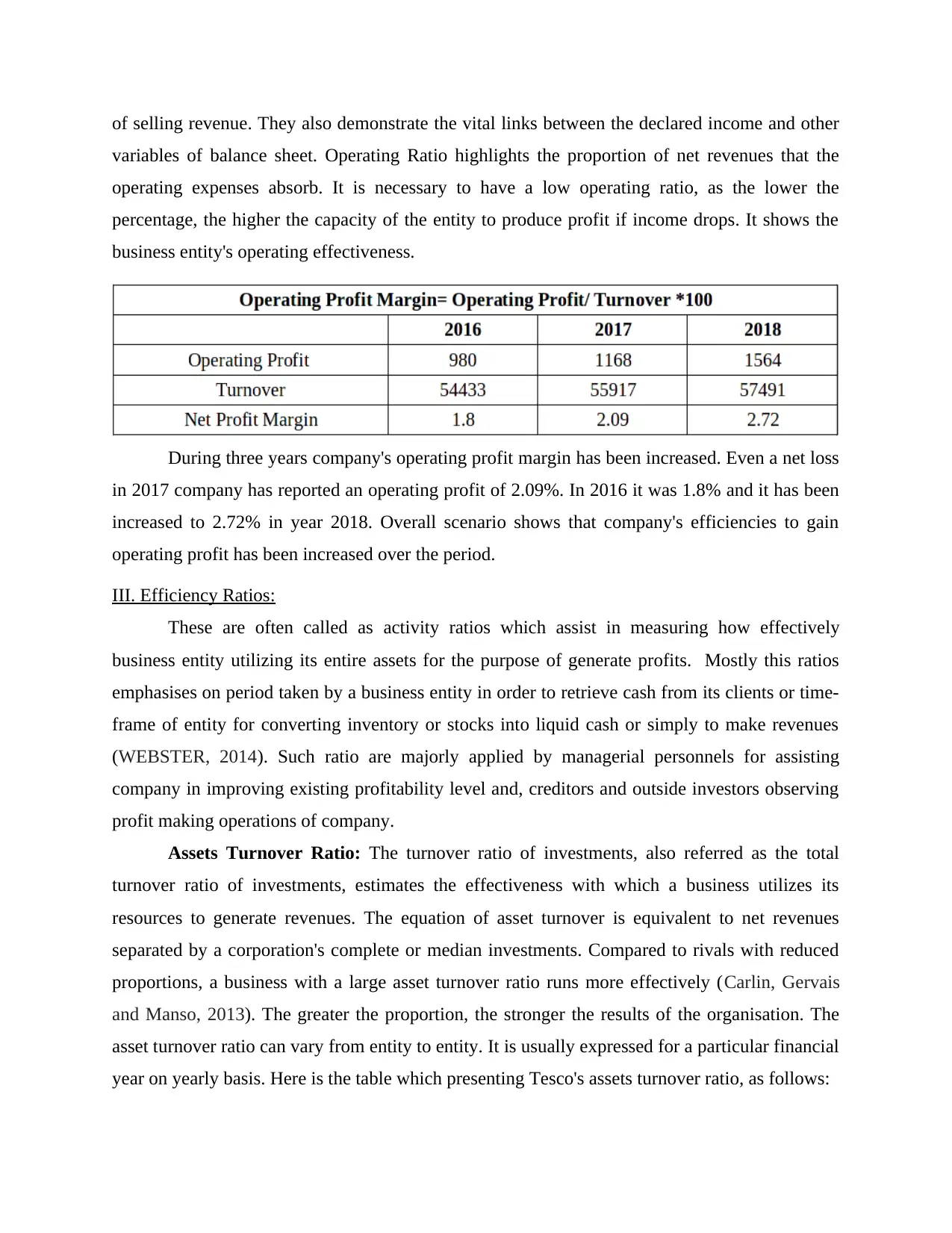

of selling revenue. They also demonstrate the vital links between the declared income and other

variables of balance sheet. Operating Ratio highlights the proportion of net revenues that the

operating expenses absorb. It is necessary to have a low operating ratio, as the lower the

percentage, the higher the capacity of the entity to produce profit if income drops. It shows the

business entity's operating effectiveness.

During three years company's operating profit margin has been increased. Even a net loss

in 2017 company has reported an operating profit of 2.09%. In 2016 it was 1.8% and it has been

increased to 2.72% in year 2018. Overall scenario shows that company's efficiencies to gain

operating profit has been increased over the period.

III. Efficiency Ratios:

These are often called as activity ratios which assist in measuring how effectively

business entity utilizing its entire assets for the purpose of generate profits. Mostly this ratios

emphasises on period taken by a business entity in order to retrieve cash from its clients or time-

frame of entity for converting inventory or stocks into liquid cash or simply to make revenues

(WEBSTER, 2014). Such ratio are majorly applied by managerial personnels for assisting

company in improving existing profitability level and, creditors and outside investors observing

profit making operations of company.

Assets Turnover Ratio: The turnover ratio of investments, also referred as the total

turnover ratio of investments, estimates the effectiveness with which a business utilizes its

resources to generate revenues. The equation of asset turnover is equivalent to net revenues

separated by a corporation's complete or median investments. Compared to rivals with reduced

proportions, a business with a large asset turnover ratio runs more effectively (Carlin, Gervais

and Manso, 2013). The greater the proportion, the stronger the results of the organisation. The

asset turnover ratio can vary from entity to entity. It is usually expressed for a particular financial

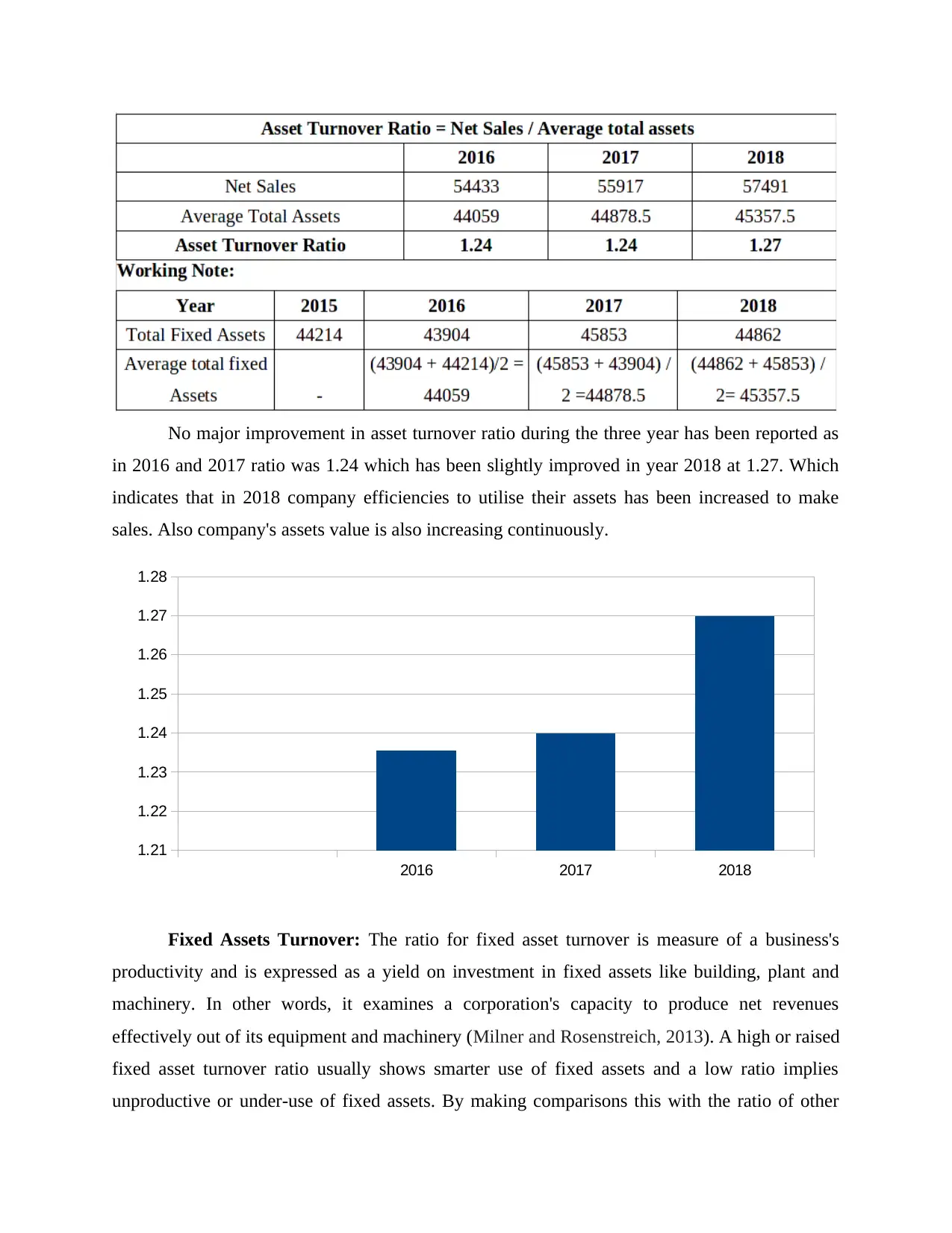

year on yearly basis. Here is the table which presenting Tesco's assets turnover ratio, as follows:

variables of balance sheet. Operating Ratio highlights the proportion of net revenues that the

operating expenses absorb. It is necessary to have a low operating ratio, as the lower the

percentage, the higher the capacity of the entity to produce profit if income drops. It shows the

business entity's operating effectiveness.

During three years company's operating profit margin has been increased. Even a net loss

in 2017 company has reported an operating profit of 2.09%. In 2016 it was 1.8% and it has been

increased to 2.72% in year 2018. Overall scenario shows that company's efficiencies to gain

operating profit has been increased over the period.

III. Efficiency Ratios:

These are often called as activity ratios which assist in measuring how effectively

business entity utilizing its entire assets for the purpose of generate profits. Mostly this ratios

emphasises on period taken by a business entity in order to retrieve cash from its clients or time-

frame of entity for converting inventory or stocks into liquid cash or simply to make revenues

(WEBSTER, 2014). Such ratio are majorly applied by managerial personnels for assisting

company in improving existing profitability level and, creditors and outside investors observing

profit making operations of company.

Assets Turnover Ratio: The turnover ratio of investments, also referred as the total

turnover ratio of investments, estimates the effectiveness with which a business utilizes its

resources to generate revenues. The equation of asset turnover is equivalent to net revenues

separated by a corporation's complete or median investments. Compared to rivals with reduced

proportions, a business with a large asset turnover ratio runs more effectively (Carlin, Gervais

and Manso, 2013). The greater the proportion, the stronger the results of the organisation. The

asset turnover ratio can vary from entity to entity. It is usually expressed for a particular financial

year on yearly basis. Here is the table which presenting Tesco's assets turnover ratio, as follows:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

No major improvement in asset turnover ratio during the three year has been reported as

in 2016 and 2017 ratio was 1.24 which has been slightly improved in year 2018 at 1.27. Which

indicates that in 2018 company efficiencies to utilise their assets has been increased to make

sales. Also company's assets value is also increasing continuously.

Fixed Assets Turnover: The ratio for fixed asset turnover is measure of a business's

productivity and is expressed as a yield on investment in fixed assets like building, plant and

machinery. In other words, it examines a corporation's capacity to produce net revenues

effectively out of its equipment and machinery (Milner and Rosenstreich, 2013). A high or raised

fixed asset turnover ratio usually shows smarter use of fixed assets and a low ratio implies

unproductive or under-use of fixed assets. By making comparisons this with the ratio of other

2016 2017 2018

1.21

1.22

1.23

1.24

1.25

1.26

1.27

1.28

in 2016 and 2017 ratio was 1.24 which has been slightly improved in year 2018 at 1.27. Which

indicates that in 2018 company efficiencies to utilise their assets has been increased to make

sales. Also company's assets value is also increasing continuously.

Fixed Assets Turnover: The ratio for fixed asset turnover is measure of a business's

productivity and is expressed as a yield on investment in fixed assets like building, plant and

machinery. In other words, it examines a corporation's capacity to produce net revenues

effectively out of its equipment and machinery (Milner and Rosenstreich, 2013). A high or raised

fixed asset turnover ratio usually shows smarter use of fixed assets and a low ratio implies

unproductive or under-use of fixed assets. By making comparisons this with the ratio of other

2016 2017 2018

1.21

1.22

1.23

1.24

1.25

1.26

1.27

1.28

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

businesses, industry norms and subsequent periods, the effectiveness of this ratio could be

improved.

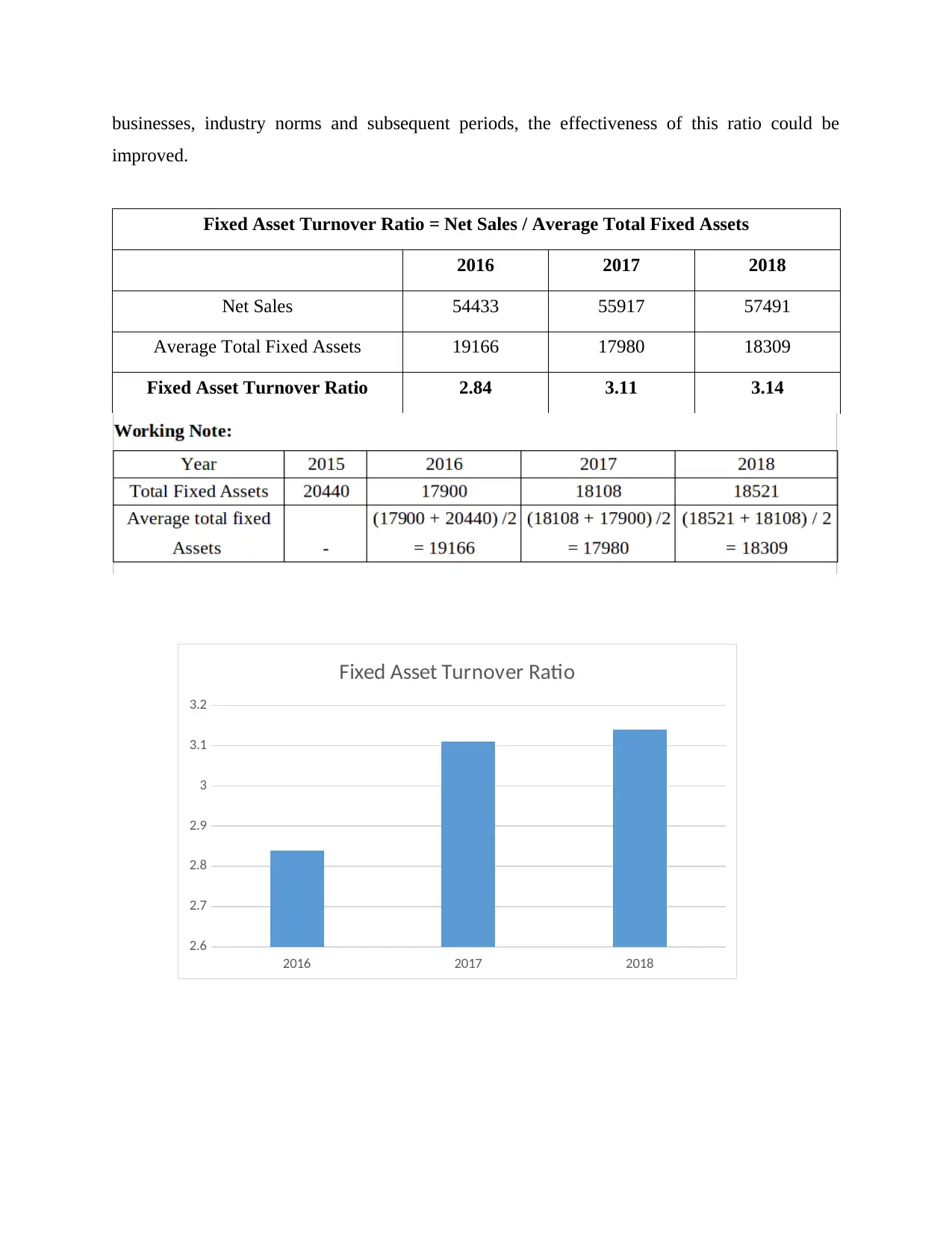

Fixed Asset Turnover Ratio = Net Sales / Average Total Fixed Assets

2016 2017 2018

Net Sales 54433 55917 57491

Average Total Fixed Assets 19166 17980 18309

Fixed Asset Turnover Ratio 2.84 3.11 3.14

2016 2017 2018

2.6

2.7

2.8

2.9

3

3.1

3.2

Fixed Asset Turnover Ratio

improved.

Fixed Asset Turnover Ratio = Net Sales / Average Total Fixed Assets

2016 2017 2018

Net Sales 54433 55917 57491

Average Total Fixed Assets 19166 17980 18309

Fixed Asset Turnover Ratio 2.84 3.11 3.14

2016 2017 2018

2.6

2.7

2.8

2.9

3

3.1

3.2

Fixed Asset Turnover Ratio

From above table showing fixed turnover ratios of Tesco, it has been analysed that fixed

turnover ratio of company showing increasing trend. It was 2.84 in in year 2016 which has been

increased to 3.11 and 3.14 in year 2017 and 2018 respectively, indicating that company's

efficiencies to produce net revenues through utilising fixed assets has been increased. During

three years company's fixed assets are also increased. These ratios indicates that company is able

to effectively utilise their fixed assets for producing revenues.

III. Solvency Ratios:

Also designated as leverage ratios, solvency ratios ascertain the potential of an

organization to serve its debt. Is the enterprise could fulfil its long-term borrowing, these ratios

calculate. It is essential when stakeholders want to understand about the company's solvency in

meeting their return requirements and making sure their funds are secure. Solvency ratios

therefore link debt levels to capital, tangible assets, business income, etc. The differentiation

among liquidity ratios and solvency ratios is one element to notice (Baker and Ricciardi, 2014).

Liquidity measures compare the current assets, i.e. quick-term borrowing, with current liabilities.

While solvency ratios explore long-term debt payment potential. Following are some key

solvency ratios are discussed below:

Debt Equity Ratio: A debt-equity ratio evaluates unique interconnection among

company's long duration borrowings and aggregate equity's amount. Debt-equity ratio has many

significances, first it is effective manner of measuring financial obligation and leverage. lower

ratio indicates that company holds more strong financial position and company's equity

effectively diluted. A higher ratio points out that entity is in risky condition in which company's

creditors are more than investors. A maximum debt-equity ratio could retain more investors and

deter creditors from lending money. The debt-to-equity ratio is a straightforward equation for

demonstrating how capital was raised to operate a enterprise. It is regarded a significant

economic metric as it shows a corporation's stabilization and capability to raise extra capital to

develop. An effective debt-equity ratio is approx 1 to 1.5.

Debt to Equity Ratio = Long term debt / Total Equity

2016 2017 2018

Long term Debts 10623 9330 7032

turnover ratio of company showing increasing trend. It was 2.84 in in year 2016 which has been

increased to 3.11 and 3.14 in year 2017 and 2018 respectively, indicating that company's

efficiencies to produce net revenues through utilising fixed assets has been increased. During

three years company's fixed assets are also increased. These ratios indicates that company is able

to effectively utilise their fixed assets for producing revenues.

III. Solvency Ratios:

Also designated as leverage ratios, solvency ratios ascertain the potential of an

organization to serve its debt. Is the enterprise could fulfil its long-term borrowing, these ratios

calculate. It is essential when stakeholders want to understand about the company's solvency in

meeting their return requirements and making sure their funds are secure. Solvency ratios

therefore link debt levels to capital, tangible assets, business income, etc. The differentiation

among liquidity ratios and solvency ratios is one element to notice (Baker and Ricciardi, 2014).

Liquidity measures compare the current assets, i.e. quick-term borrowing, with current liabilities.

While solvency ratios explore long-term debt payment potential. Following are some key

solvency ratios are discussed below:

Debt Equity Ratio: A debt-equity ratio evaluates unique interconnection among

company's long duration borrowings and aggregate equity's amount. Debt-equity ratio has many

significances, first it is effective manner of measuring financial obligation and leverage. lower

ratio indicates that company holds more strong financial position and company's equity

effectively diluted. A higher ratio points out that entity is in risky condition in which company's

creditors are more than investors. A maximum debt-equity ratio could retain more investors and

deter creditors from lending money. The debt-to-equity ratio is a straightforward equation for

demonstrating how capital was raised to operate a enterprise. It is regarded a significant

economic metric as it shows a corporation's stabilization and capability to raise extra capital to

develop. An effective debt-equity ratio is approx 1 to 1.5.

Debt to Equity Ratio = Long term debt / Total Equity

2016 2017 2018

Long term Debts 10623 9330 7032

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17