Financial Decision Making: Performance Analysis of Roast Ltd Report

VerifiedAdded on 2023/01/18

|15

|4388

|26

Report

AI Summary

This report provides a comprehensive financial analysis of Roast Ltd, a UK-based coffee house, examining its performance and potential for acquisition. The report begins with an industry review, highlighting key trends and competitors. It then delves into Roast Ltd's financial statements, including the statement of profit or loss, financial position, and cash flow statement, calculating and interpreting key financial ratios such as gross profit margin, net profit margin, current ratio, quick ratio, and debt-equity ratio. The analysis reveals the company's profitability, liquidity, and solvency. Furthermore, the report explores an investment appraisal scenario involving a 400-million-pound investment, utilizing techniques like NPV, ARR, and payback period to assess its feasibility. The analysis suggests a positive outlook for Roast Ltd, recommending its acquisition based on its strong market performance and financial health.

Financial Decision Making

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

EXECUTIVE SUMMARY.............................................................................................................1

PART 1: Industry Review................................................................................................................1

PART 2: Business Performance Analysis........................................................................................2

2.1 Statement of profit or Loss....................................................................................................2

2.2 Statement of Financial Position............................................................................................4

2.3 Statement of cash flow statement..........................................................................................6

Part 3: Investment Appraisal and Sources of Finance.....................................................................8

3.1 Investment Appraisal............................................................................................................8

3.2 Sources of fund:..................................................................................................................10

REFERENCES..............................................................................................................................12

EXECUTIVE SUMMARY.............................................................................................................1

PART 1: Industry Review................................................................................................................1

PART 2: Business Performance Analysis........................................................................................2

2.1 Statement of profit or Loss....................................................................................................2

2.2 Statement of Financial Position............................................................................................4

2.3 Statement of cash flow statement..........................................................................................6

Part 3: Investment Appraisal and Sources of Finance.....................................................................8

3.1 Investment Appraisal............................................................................................................8

3.2 Sources of fund:..................................................................................................................10

REFERENCES..............................................................................................................................12

EXECUTIVE SUMMARY

Present report is based upon financial decision making of Roast Ltd which is one of the

famous coffee houses of United Kingdom. It is segregated in two parts first one is based upon the

analysis of performance of the company. For this purpose, all the final accounts including

Statement of profit and loss, financial positions and cash flow are analysed. Different ratios such

as operating, net, and gross profit, current, quick, debt equity etc. along with operating cash cycle

are calculated to determine that Starbucks can acquire it or not. It has been recommended to the

organisation that it should acquire Roast Ltd because its performance in the market is very good.

Second part is based upon an investment option of 400 million pounds. For the purpose of

analysing profitability and efficiency of this alternative different investment appraisal techniques

such as NPV, ARR and payback period are calculated.

PART 1: Industry Review

This section of the report focuses on the coffee house industry which is one of the largest

sectors of UK and it is growing massively due to increasing demand of coffee in the market. In

order to get an insight and overview of the industry following points could be considered:

According to a study coffee house industry is generating employment in UK and

provided more than 210000 jobs to the individuals and contributed in the growth of

country (Employment generated by coffee house industry, 2019).

Major players of the industry are Starbucks, Cafe Ritazza, cafe Nero etc. which are

competing with each other and making efforts to become the market leader. All these

organisations are operating business in effective manner within the particular sector.

The whole sector have contributes around 6.1% in the annual growth of the industry of

UK.

According to the market research of IBIS coffee house industry of UK has generated

revenues of 6 million pounds in current year as compared to last few years.

There are total numbers of the organisation that are related with the sector of coffee

house at the place of UK in 16199 that has been enhanced through growth rate due to

compare with the previous year.

1

Present report is based upon financial decision making of Roast Ltd which is one of the

famous coffee houses of United Kingdom. It is segregated in two parts first one is based upon the

analysis of performance of the company. For this purpose, all the final accounts including

Statement of profit and loss, financial positions and cash flow are analysed. Different ratios such

as operating, net, and gross profit, current, quick, debt equity etc. along with operating cash cycle

are calculated to determine that Starbucks can acquire it or not. It has been recommended to the

organisation that it should acquire Roast Ltd because its performance in the market is very good.

Second part is based upon an investment option of 400 million pounds. For the purpose of

analysing profitability and efficiency of this alternative different investment appraisal techniques

such as NPV, ARR and payback period are calculated.

PART 1: Industry Review

This section of the report focuses on the coffee house industry which is one of the largest

sectors of UK and it is growing massively due to increasing demand of coffee in the market. In

order to get an insight and overview of the industry following points could be considered:

According to a study coffee house industry is generating employment in UK and

provided more than 210000 jobs to the individuals and contributed in the growth of

country (Employment generated by coffee house industry, 2019).

Major players of the industry are Starbucks, Cafe Ritazza, cafe Nero etc. which are

competing with each other and making efforts to become the market leader. All these

organisations are operating business in effective manner within the particular sector.

The whole sector have contributes around 6.1% in the annual growth of the industry of

UK.

According to the market research of IBIS coffee house industry of UK has generated

revenues of 6 million pounds in current year as compared to last few years.

There are total numbers of the organisation that are related with the sector of coffee

house at the place of UK in 16199 that has been enhanced through growth rate due to

compare with the previous year.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

There are defined different types of possibilities that can be achieved through the

particular enterprise. With the help of these opportunities include with a healthy organic

that can carry out the recent trend of stay healthy (Correia, Dussault and Pontes, 2015).

On the basis of above described points it has been determined that different types of

difficulties are also faced by coffee house industry to grab growth opportunities. All the

challenges are affecting the market trends and scenario that directly leaves impact upon

preferences and choices of customers. There is one more issue that is faced by the particular

sector related with the intense competition and mostly face by the new entrance of this sector.

The main cause of this competition is high profit margin where a business engage in this

industry.

PART 2: Business Performance Analysis

2.1 Statement of profit or Loss

Statement of profit and loss is an account which is used to record all the incomes,

expenses and calculate the profits generated by an organisation in an accounting year. With the

help of it profitability of an enterprise could be determined by top level executives and external

parties such as investors, government and suppliers. From the income statement of Roast Ltd it

has been analysed that revenue of the business are improving as per the total sales transcribed in

the year 2017 and get outcome in the revenue of 2022000 which is increased up to 2534000 in

2018. If revenues are increased by an organisation then it may result in higher incomes and

profits and along with this expenses may increase because the company is required to spend

money to enhance sales. Total operating expenditure of Roast Ltd were 466000 for 2017 which

are increased up to 477000 in 2018 (Gal, Stewart and Hanne, 2013).

All over the analysis it is mainly depended on the ration analysis that present actual

position of the business in present time due to compare with last year activities and show

financial performance of business.

Gross Profit Margin

This ratio is used by the business to measure the profitability that present the ability of a

business to earn income against set value that invested on labour and on material cost. If gross

profit ratio increasing so it presents growth of business that supports to business to consume

money for the future operating expenditure.

2

particular enterprise. With the help of these opportunities include with a healthy organic

that can carry out the recent trend of stay healthy (Correia, Dussault and Pontes, 2015).

On the basis of above described points it has been determined that different types of

difficulties are also faced by coffee house industry to grab growth opportunities. All the

challenges are affecting the market trends and scenario that directly leaves impact upon

preferences and choices of customers. There is one more issue that is faced by the particular

sector related with the intense competition and mostly face by the new entrance of this sector.

The main cause of this competition is high profit margin where a business engage in this

industry.

PART 2: Business Performance Analysis

2.1 Statement of profit or Loss

Statement of profit and loss is an account which is used to record all the incomes,

expenses and calculate the profits generated by an organisation in an accounting year. With the

help of it profitability of an enterprise could be determined by top level executives and external

parties such as investors, government and suppliers. From the income statement of Roast Ltd it

has been analysed that revenue of the business are improving as per the total sales transcribed in

the year 2017 and get outcome in the revenue of 2022000 which is increased up to 2534000 in

2018. If revenues are increased by an organisation then it may result in higher incomes and

profits and along with this expenses may increase because the company is required to spend

money to enhance sales. Total operating expenditure of Roast Ltd were 466000 for 2017 which

are increased up to 477000 in 2018 (Gal, Stewart and Hanne, 2013).

All over the analysis it is mainly depended on the ration analysis that present actual

position of the business in present time due to compare with last year activities and show

financial performance of business.

Gross Profit Margin

This ratio is used by the business to measure the profitability that present the ability of a

business to earn income against set value that invested on labour and on material cost. If gross

profit ratio increasing so it presents growth of business that supports to business to consume

money for the future operating expenditure.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Formula: Gross profit / Net sales *100

For 2017 = 517 / 2022 * 100

= 25.57%

For 2018 = 544 / 2534 * 100

= 21.47%

According to above calculations the gross profit margin of the company is decreased in

2018 which means profitability of Roast Ltd is also declined. The reason behind of reduction to

increase gross sales that presents negative indication to take financial decision to acquire of

particular organisation. Gross profit margin show impact in relation between the profit and the

COGS. Due to deduct gross profit profit ans improvement in cost of goods sold impact on the

decision making procedure.

So the growth of Roast Ltd is not analysed through particular ratio because it is based on

the cost of goods sold which is higher and revenue less than of it. So company can not afford the

procedure of coffee beans from other states of Europe where increase the interest rate after the

Brexit situation.

Net Profit margin

This margin is utilised to measure the profitability of the business that can be earned after

less all the taxes and interest in particular financial period. Due to greater profit margin present

high growth and success in context of company's scope (Govindan and et.al., 2015).

Formula: Net profit / Net sales *100

For 2017 = 36 / 2022 * 100

= 1.78%

For 2018 = 81 / 2534 * 100

= 3.20%

The above calculations are demonstrating that net profit margin of the Roast Ltd is

increased in 2018 from 1378% to 3.20% which shows that profitability is increased in this year.

Due to increment analysis the ability of the business and know about management control and

conduct its yearly expenses of operation like salaries, rent and many more. Through increasing

net profit get good indication for Starbucks as per the reason of acquisition.

Operating Profit Margin:

3

For 2017 = 517 / 2022 * 100

= 25.57%

For 2018 = 544 / 2534 * 100

= 21.47%

According to above calculations the gross profit margin of the company is decreased in

2018 which means profitability of Roast Ltd is also declined. The reason behind of reduction to

increase gross sales that presents negative indication to take financial decision to acquire of

particular organisation. Gross profit margin show impact in relation between the profit and the

COGS. Due to deduct gross profit profit ans improvement in cost of goods sold impact on the

decision making procedure.

So the growth of Roast Ltd is not analysed through particular ratio because it is based on

the cost of goods sold which is higher and revenue less than of it. So company can not afford the

procedure of coffee beans from other states of Europe where increase the interest rate after the

Brexit situation.

Net Profit margin

This margin is utilised to measure the profitability of the business that can be earned after

less all the taxes and interest in particular financial period. Due to greater profit margin present

high growth and success in context of company's scope (Govindan and et.al., 2015).

Formula: Net profit / Net sales *100

For 2017 = 36 / 2022 * 100

= 1.78%

For 2018 = 81 / 2534 * 100

= 3.20%

The above calculations are demonstrating that net profit margin of the Roast Ltd is

increased in 2018 from 1378% to 3.20% which shows that profitability is increased in this year.

Due to increment analysis the ability of the business and know about management control and

conduct its yearly expenses of operation like salaries, rent and many more. Through increasing

net profit get good indication for Starbucks as per the reason of acquisition.

Operating Profit Margin:

3

The statistical measurement shows the ability of a business to reserve a cost as profit as

after paying off all the different production expenditure like raw material, wages etc. Due to

higher operating margin get the greater success rate in the business (Kliger and Gilad, 2012).

Formula = Operating profit / Net sales *100

For 2017 = 51 / 2022 *100

= 2.52%

For 2018 = 127 / 2534 * 100

= 5.01%

From the above calculations it has been determined that operating margin of Roast Ltd is

increased in 2018 which is showing that operational performance of the enterprise is increased in

this year. Operating profit margin in the rear of 2017 is computed as 2.52% that about doubled in

2018 which is 5.01%. The particular increment provide outcome as good performance of the

business.

After ratio analysis and through profit & loss statement of Roast Ltd has been observed

the business at the level of maturity stage that presents life cycle which enough to acquire the

business at its growth level.

2.2 Statement of Financial Position

Business entities generate a statement for the purpose of recording information related to

assets and liabilities on yearly basis which is known as statement of financial position. As per the

analysis of Roast Ltd balance sheet it is getting that company have total assets as well as

liabilities has been improved in the year of 2018. The total assets & liabilities in the year 2017

was recorded in financial accounts that was 1017'000 pounds but it is increased in the year 20187

such as 1443'000 pounds. Through increasing assets value and equity presents about the

operating condition. So for more analysis calculate ration related of financial statement such as:

Current Ratio

This ratio is mainly depended on the current assets and current liabilities of the

organisation. The ideal ratio of the current ratio is 2:1 (Kotlar and et.al., 2014). Through this

ration analysis the liquidity position of the business and pay amounts to debt in short period of

time regarding to liabilities. In the context of coffee industry, a business has two parts of assets

and one part of the liabilities.

Formula: Current assets / Current liabilities

4

after paying off all the different production expenditure like raw material, wages etc. Due to

higher operating margin get the greater success rate in the business (Kliger and Gilad, 2012).

Formula = Operating profit / Net sales *100

For 2017 = 51 / 2022 *100

= 2.52%

For 2018 = 127 / 2534 * 100

= 5.01%

From the above calculations it has been determined that operating margin of Roast Ltd is

increased in 2018 which is showing that operational performance of the enterprise is increased in

this year. Operating profit margin in the rear of 2017 is computed as 2.52% that about doubled in

2018 which is 5.01%. The particular increment provide outcome as good performance of the

business.

After ratio analysis and through profit & loss statement of Roast Ltd has been observed

the business at the level of maturity stage that presents life cycle which enough to acquire the

business at its growth level.

2.2 Statement of Financial Position

Business entities generate a statement for the purpose of recording information related to

assets and liabilities on yearly basis which is known as statement of financial position. As per the

analysis of Roast Ltd balance sheet it is getting that company have total assets as well as

liabilities has been improved in the year of 2018. The total assets & liabilities in the year 2017

was recorded in financial accounts that was 1017'000 pounds but it is increased in the year 20187

such as 1443'000 pounds. Through increasing assets value and equity presents about the

operating condition. So for more analysis calculate ration related of financial statement such as:

Current Ratio

This ratio is mainly depended on the current assets and current liabilities of the

organisation. The ideal ratio of the current ratio is 2:1 (Kotlar and et.al., 2014). Through this

ration analysis the liquidity position of the business and pay amounts to debt in short period of

time regarding to liabilities. In the context of coffee industry, a business has two parts of assets

and one part of the liabilities.

Formula: Current assets / Current liabilities

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

For 2017 = 347 / 138

= 2.51

For 2018 = 447 / 308

= 1.45

As per the above ratio calculation analysis the capability to pay off short term debt and

liabilities of Roast Ltd. In the year of 2018 the ratio is decreased as compare of 2017 because it

was 2.51:1 an 1.45:a in 2018. Due to investigating different aspects of statement of financial

position of an organisation, it is analysed that current ratio of the business deducted use to

overdraft facility to pay off additional amount for the securing coffee beans as per the other state

of Europe. There are deducting current ratio due to post Brexit effect on the inability of pay debts

of the business.

Quick Ratio

The particular ratio indicate changes in cash and cash equivalents does not include stock

and prepaid expenses. The ideal ratio is 1:1 in the coffee industry to pay off the quick amounts

through this ratio (Li, 2014).

Formula: Quick assets / Current liabilities

For 2017 = 227 / 138

= 1.64

For 2018 = 148 / 308

= 0.48

As per the above computation the outcome of quick ratio indicate that Roast Ltd can able

for Quick ratio of 1.64:1 in the year 2017 which is reduced in 2018 by 0.48:1. It is performing as

usual current ratio that has been deducted due to have external affairs that faced by the business.

Debt Equity Ratio

It is most essential ratio which is must compute by every organisation to know debt

position and supports to take effective financial decision towards to business. On the basis of this

ratio take acquire decision and measure ability of business to achieve to parts of debtor's capital

against one part contributed capital. The idle ratio is 2:1 in the coffee house sector (Ogiela,

2013).

Formula: Total debts / Total equities

For 2017 = 238 / 779

5

= 2.51

For 2018 = 447 / 308

= 1.45

As per the above ratio calculation analysis the capability to pay off short term debt and

liabilities of Roast Ltd. In the year of 2018 the ratio is decreased as compare of 2017 because it

was 2.51:1 an 1.45:a in 2018. Due to investigating different aspects of statement of financial

position of an organisation, it is analysed that current ratio of the business deducted use to

overdraft facility to pay off additional amount for the securing coffee beans as per the other state

of Europe. There are deducting current ratio due to post Brexit effect on the inability of pay debts

of the business.

Quick Ratio

The particular ratio indicate changes in cash and cash equivalents does not include stock

and prepaid expenses. The ideal ratio is 1:1 in the coffee industry to pay off the quick amounts

through this ratio (Li, 2014).

Formula: Quick assets / Current liabilities

For 2017 = 227 / 138

= 1.64

For 2018 = 148 / 308

= 0.48

As per the above computation the outcome of quick ratio indicate that Roast Ltd can able

for Quick ratio of 1.64:1 in the year 2017 which is reduced in 2018 by 0.48:1. It is performing as

usual current ratio that has been deducted due to have external affairs that faced by the business.

Debt Equity Ratio

It is most essential ratio which is must compute by every organisation to know debt

position and supports to take effective financial decision towards to business. On the basis of this

ratio take acquire decision and measure ability of business to achieve to parts of debtor's capital

against one part contributed capital. The idle ratio is 2:1 in the coffee house sector (Ogiela,

2013).

Formula: Total debts / Total equities

For 2017 = 238 / 779

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

= 0.31

For 2018 = 583 / 860

= 0.68

The above table it is presented that it is evident of the debt equity ratio that presents the

growth of organisation at ongoing way. Through formula get result as 0.31:1 in year 2017 &

0.68:1 in year 2018. Through growth ratio get positive result regarding to acquisition decision of

Starbucks.

As per the entire analysis of financial position of Roast Ltd can refer that the business is

able to pay its short term as well as long term liabilities due to face different problems which is

related with external environmental aspect like Brexit.

2.3 Statement of cash flow statement

All the organisations generate a statement to record information regarding inflow and

outflow of cash and it is known as cash flow statement. Main purpose of it is to provide

information about liquidity of the company to the stakeholders. The statement of cash flow of

Roast Ltd presents negative activities of cash inflows and outflows that means a business is

heavily paying through cash that become reason of the liquidity. Through more analysis the

operating cash cycle of Roast Ltd is defined as follows:

Operating Cash Cycle

It is a type of measurement that mainly utilised by business to evaluate the time that taken

by them to convert all the stocks through monetary resources. This measurement related to cash

conversion cycle that consist of the day of operations. Operating cash cycle supports in

determining the performance of the business. In case of Roast Ltd, the operating cash cycle is

calculated by the different number of days in which stock is outstanding and numbers of days in

which is sale outstanding and numbers of days of payment outstanding (Petersen, Kushwaha and

Kumar, 2015).

Particulars 2017 2018

Total days in year 365 365

Inventory turnover 12.54 6.66

Formula 365 / inventory turnover

Days inventory outstanding 29.11 54.80

Total days in year 365 365

6

For 2018 = 583 / 860

= 0.68

The above table it is presented that it is evident of the debt equity ratio that presents the

growth of organisation at ongoing way. Through formula get result as 0.31:1 in year 2017 &

0.68:1 in year 2018. Through growth ratio get positive result regarding to acquisition decision of

Starbucks.

As per the entire analysis of financial position of Roast Ltd can refer that the business is

able to pay its short term as well as long term liabilities due to face different problems which is

related with external environmental aspect like Brexit.

2.3 Statement of cash flow statement

All the organisations generate a statement to record information regarding inflow and

outflow of cash and it is known as cash flow statement. Main purpose of it is to provide

information about liquidity of the company to the stakeholders. The statement of cash flow of

Roast Ltd presents negative activities of cash inflows and outflows that means a business is

heavily paying through cash that become reason of the liquidity. Through more analysis the

operating cash cycle of Roast Ltd is defined as follows:

Operating Cash Cycle

It is a type of measurement that mainly utilised by business to evaluate the time that taken

by them to convert all the stocks through monetary resources. This measurement related to cash

conversion cycle that consist of the day of operations. Operating cash cycle supports in

determining the performance of the business. In case of Roast Ltd, the operating cash cycle is

calculated by the different number of days in which stock is outstanding and numbers of days in

which is sale outstanding and numbers of days of payment outstanding (Petersen, Kushwaha and

Kumar, 2015).

Particulars 2017 2018

Total days in year 365 365

Inventory turnover 12.54 6.66

Formula 365 / inventory turnover

Days inventory outstanding 29.11 54.80

Total days in year 365 365

6

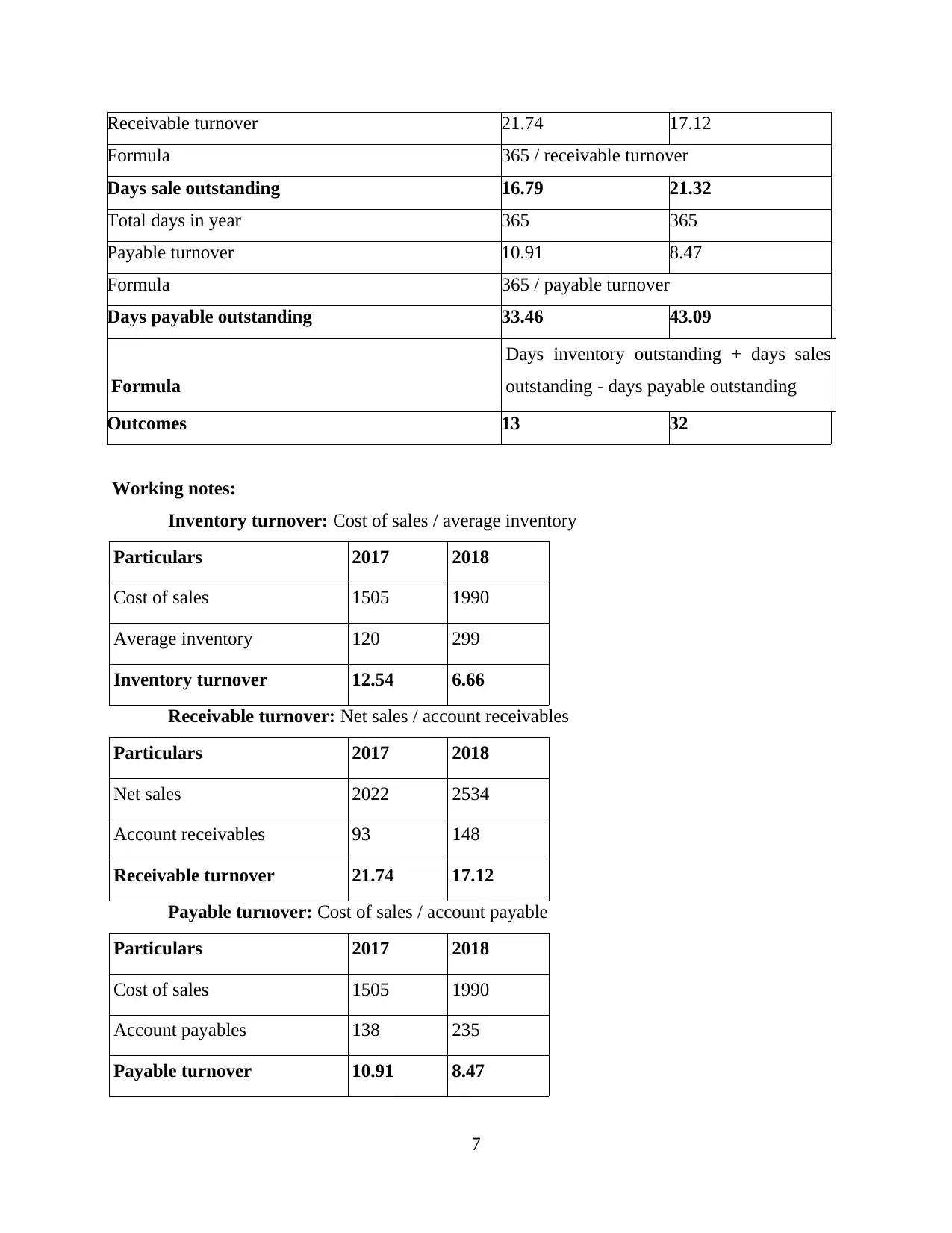

Receivable turnover 21.74 17.12

Formula 365 / receivable turnover

Days sale outstanding 16.79 21.32

Total days in year 365 365

Payable turnover 10.91 8.47

Formula 365 / payable turnover

Days payable outstanding 33.46 43.09

Formula

Days inventory outstanding + days sales

outstanding - days payable outstanding

Outcomes 13 32

Working notes:

Inventory turnover: Cost of sales / average inventory

Particulars 2017 2018

Cost of sales 1505 1990

Average inventory 120 299

Inventory turnover 12.54 6.66

Receivable turnover: Net sales / account receivables

Particulars 2017 2018

Net sales 2022 2534

Account receivables 93 148

Receivable turnover 21.74 17.12

Payable turnover: Cost of sales / account payable

Particulars 2017 2018

Cost of sales 1505 1990

Account payables 138 235

Payable turnover 10.91 8.47

7

Formula 365 / receivable turnover

Days sale outstanding 16.79 21.32

Total days in year 365 365

Payable turnover 10.91 8.47

Formula 365 / payable turnover

Days payable outstanding 33.46 43.09

Formula

Days inventory outstanding + days sales

outstanding - days payable outstanding

Outcomes 13 32

Working notes:

Inventory turnover: Cost of sales / average inventory

Particulars 2017 2018

Cost of sales 1505 1990

Average inventory 120 299

Inventory turnover 12.54 6.66

Receivable turnover: Net sales / account receivables

Particulars 2017 2018

Net sales 2022 2534

Account receivables 93 148

Receivable turnover 21.74 17.12

Payable turnover: Cost of sales / account payable

Particulars 2017 2018

Cost of sales 1505 1990

Account payables 138 235

Payable turnover 10.91 8.47

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

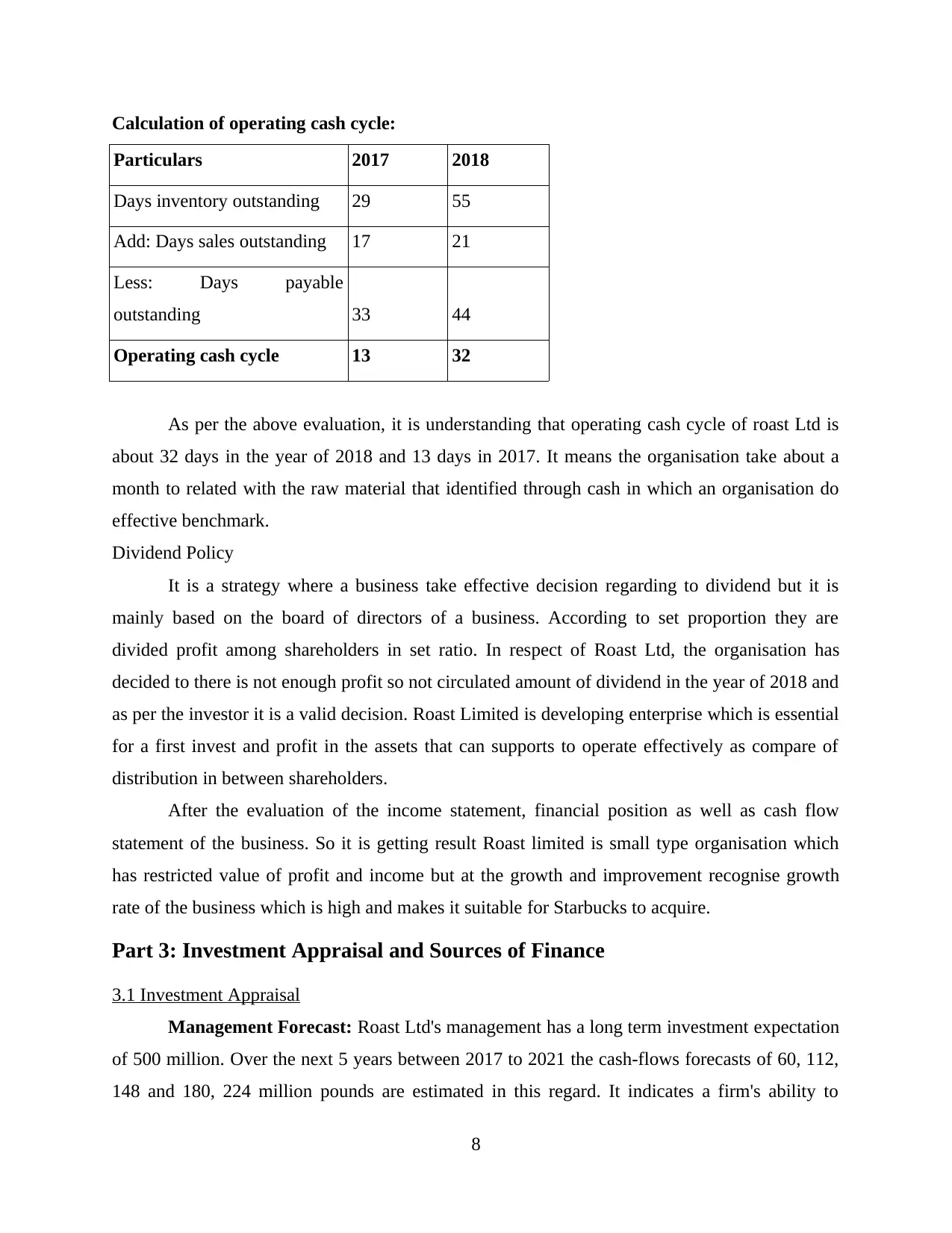

Calculation of operating cash cycle:

Particulars 2017 2018

Days inventory outstanding 29 55

Add: Days sales outstanding 17 21

Less: Days payable

outstanding 33 44

Operating cash cycle 13 32

As per the above evaluation, it is understanding that operating cash cycle of roast Ltd is

about 32 days in the year of 2018 and 13 days in 2017. It means the organisation take about a

month to related with the raw material that identified through cash in which an organisation do

effective benchmark.

Dividend Policy

It is a strategy where a business take effective decision regarding to dividend but it is

mainly based on the board of directors of a business. According to set proportion they are

divided profit among shareholders in set ratio. In respect of Roast Ltd, the organisation has

decided to there is not enough profit so not circulated amount of dividend in the year of 2018 and

as per the investor it is a valid decision. Roast Limited is developing enterprise which is essential

for a first invest and profit in the assets that can supports to operate effectively as compare of

distribution in between shareholders.

After the evaluation of the income statement, financial position as well as cash flow

statement of the business. So it is getting result Roast limited is small type organisation which

has restricted value of profit and income but at the growth and improvement recognise growth

rate of the business which is high and makes it suitable for Starbucks to acquire.

Part 3: Investment Appraisal and Sources of Finance

3.1 Investment Appraisal

Management Forecast: Roast Ltd's management has a long term investment expectation

of 500 million. Over the next 5 years between 2017 to 2021 the cash-flows forecasts of 60, 112,

148 and 180, 224 million pounds are estimated in this regard. It indicates a firm's ability to

8

Particulars 2017 2018

Days inventory outstanding 29 55

Add: Days sales outstanding 17 21

Less: Days payable

outstanding 33 44

Operating cash cycle 13 32

As per the above evaluation, it is understanding that operating cash cycle of roast Ltd is

about 32 days in the year of 2018 and 13 days in 2017. It means the organisation take about a

month to related with the raw material that identified through cash in which an organisation do

effective benchmark.

Dividend Policy

It is a strategy where a business take effective decision regarding to dividend but it is

mainly based on the board of directors of a business. According to set proportion they are

divided profit among shareholders in set ratio. In respect of Roast Ltd, the organisation has

decided to there is not enough profit so not circulated amount of dividend in the year of 2018 and

as per the investor it is a valid decision. Roast Limited is developing enterprise which is essential

for a first invest and profit in the assets that can supports to operate effectively as compare of

distribution in between shareholders.

After the evaluation of the income statement, financial position as well as cash flow

statement of the business. So it is getting result Roast limited is small type organisation which

has restricted value of profit and income but at the growth and improvement recognise growth

rate of the business which is high and makes it suitable for Starbucks to acquire.

Part 3: Investment Appraisal and Sources of Finance

3.1 Investment Appraisal

Management Forecast: Roast Ltd's management has a long term investment expectation

of 500 million. Over the next 5 years between 2017 to 2021 the cash-flows forecasts of 60, 112,

148 and 180, 224 million pounds are estimated in this regard. It indicates a firm's ability to

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

anticipate a rise in cash-flows over 5 years. All projections are focused on certain aspects and

considerations. Therefore, it is complex to achieve in reality.

Due to Brexit effect this forecast may be wrong but company's existing results and

performance point out that it will overcome from the adverse impacts of Brexit. Management has

to revise their forecast time to time because inflexible or rigid forecasts may lead to

misinterpretations.

Investment appraisal:

This is the approach adopted by the enterprise to assess the feasibility of any given

opportunities. Managers may adopt different techniques simultaneously to take feasibility

decisions about different projects. The following summary describes the various techniques that

Roast Ltd can use for evaluating its advantages and limitations:

Payback period: It's one of the efficacious techniques which allows the time needed to

retrieve investments to be defined. Analysing Exhibit 3 revealed that same could be retrieved

within 4 years if company Roast Ltd spends the value of 500 million pounds. The following are

the various advantages and constraints, as follows:

Benefits: It will also enable managers to make decisions easily while also reviewing

various projects life and initial investments. Quick method to review different capital

projects by interpreting how much time it would take to recover costs initially incurred.

Limitations: A significant concept in decision making approach named Time-value of

present money not taken into consideration here under it because of this accuracy level of

results can not attain a relevant decision-making.

Accounting rate of return: The key application of this approach is formed in the

budgeting-capital it may serve them to assess return on investment on their multiple investment

levels. According to the review of Exhibit 3, ARR would be 18 percent for the investment of

500-million pound. It represents the investment's reasonable return. Benefits and drawbacks are

described below:

Benefits: This method assist to assess how much return the company will reasonably get

from any specified project investment.

Limitations: Timing effect on value of money is not regarded here in it that several times

resulting in ambiguous outcomes.

9

considerations. Therefore, it is complex to achieve in reality.

Due to Brexit effect this forecast may be wrong but company's existing results and

performance point out that it will overcome from the adverse impacts of Brexit. Management has

to revise their forecast time to time because inflexible or rigid forecasts may lead to

misinterpretations.

Investment appraisal:

This is the approach adopted by the enterprise to assess the feasibility of any given

opportunities. Managers may adopt different techniques simultaneously to take feasibility

decisions about different projects. The following summary describes the various techniques that

Roast Ltd can use for evaluating its advantages and limitations:

Payback period: It's one of the efficacious techniques which allows the time needed to

retrieve investments to be defined. Analysing Exhibit 3 revealed that same could be retrieved

within 4 years if company Roast Ltd spends the value of 500 million pounds. The following are

the various advantages and constraints, as follows:

Benefits: It will also enable managers to make decisions easily while also reviewing

various projects life and initial investments. Quick method to review different capital

projects by interpreting how much time it would take to recover costs initially incurred.

Limitations: A significant concept in decision making approach named Time-value of

present money not taken into consideration here under it because of this accuracy level of

results can not attain a relevant decision-making.

Accounting rate of return: The key application of this approach is formed in the

budgeting-capital it may serve them to assess return on investment on their multiple investment

levels. According to the review of Exhibit 3, ARR would be 18 percent for the investment of

500-million pound. It represents the investment's reasonable return. Benefits and drawbacks are

described below:

Benefits: This method assist to assess how much return the company will reasonably get

from any specified project investment.

Limitations: Timing effect on value of money is not regarded here in it that several times

resulting in ambiguous outcomes.

9

Net present value: It is determined by subtracting the current cash flow worth from the

organization's initial cost. Exhibit 3 shows the NPV for Roast Ltd, 110 if the organization's

investment is 500 million (WEBSTER, 2014). The numerous advantages and drawbacks of same

are described out below:

Benefits: More realistic and significant approach which also emphasises upon

consideration of timing factor in value of pound money.

Limitations: Guesswork of discounting factor is sometimes creates complexities as no

specific rates are described any where.

From above evaluation of Roast Ltd's project covering different techniques it has been

analysed that the investment of 500million GBP in project would be reasonable if all

things/factors remain constant.

3.2 Sources of fund:

For all the business entities it is very important to arrange funds to operate business in

systematic manner. As Roast Ltd is planning to expand business in Italy therefore it is very

important for managers to make sure that they use effective sources to generate finance for this

purpose. Looking at the scenario they have to seek some options to support them accomplish

their goal. In this scenario's context, here is a comprehensive evaluation of different sources for

acquiring funds, as follows:

Bank Loan: This is quickest way to raise funds through bank loans. A corporation like

Roast Ltd in order to make expansion in business could apply this source as it doest not take too

much time also fastest way to raise funds. Under it normally banks and financial institutions

provides loans to company against any security whether primary or collateral and repayment of

funds are made by company in instalment. This sum of instalment involves interest and principle.

However it has some disadvantage also along with benefits, as discussed below: Advantage: As compare to shareholders, lenders and borrowers have no right to make

interfere in workings and decisions of enterprise. Also company has sufficient time-frame

for making repayment of loans (Ujunwa, 2012).

Disadvantage: It is one of the lengthy process to raise fund from banks where final

decision are taken by banks that whether they will allow the organisation to raise funds or

not.

10

organization's initial cost. Exhibit 3 shows the NPV for Roast Ltd, 110 if the organization's

investment is 500 million (WEBSTER, 2014). The numerous advantages and drawbacks of same

are described out below:

Benefits: More realistic and significant approach which also emphasises upon

consideration of timing factor in value of pound money.

Limitations: Guesswork of discounting factor is sometimes creates complexities as no

specific rates are described any where.

From above evaluation of Roast Ltd's project covering different techniques it has been

analysed that the investment of 500million GBP in project would be reasonable if all

things/factors remain constant.

3.2 Sources of fund:

For all the business entities it is very important to arrange funds to operate business in

systematic manner. As Roast Ltd is planning to expand business in Italy therefore it is very

important for managers to make sure that they use effective sources to generate finance for this

purpose. Looking at the scenario they have to seek some options to support them accomplish

their goal. In this scenario's context, here is a comprehensive evaluation of different sources for

acquiring funds, as follows:

Bank Loan: This is quickest way to raise funds through bank loans. A corporation like

Roast Ltd in order to make expansion in business could apply this source as it doest not take too

much time also fastest way to raise funds. Under it normally banks and financial institutions

provides loans to company against any security whether primary or collateral and repayment of

funds are made by company in instalment. This sum of instalment involves interest and principle.

However it has some disadvantage also along with benefits, as discussed below: Advantage: As compare to shareholders, lenders and borrowers have no right to make

interfere in workings and decisions of enterprise. Also company has sufficient time-frame

for making repayment of loans (Ujunwa, 2012).

Disadvantage: It is one of the lengthy process to raise fund from banks where final

decision are taken by banks that whether they will allow the organisation to raise funds or

not.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.