Financial Decision Making Report: Analysis of Roast Ltd and Starbucks

VerifiedAdded on 2023/01/06

|14

|4437

|84

Report

AI Summary

This report presents a comprehensive financial analysis of Roast Ltd, a UK coffee house, in the context of a potential acquisition by Starbucks. The analysis begins with an industry review, highlighting key trends and market dynamics within the UK coffee sector. Subsequently, the report delves into Roast Ltd's business performance, examining its statement of profit and loss, statement of financial position, and statement of cash flow. Various financial ratios, including gross profit ratio, operating profit ratio, net profit ratio, debt equity ratio, current ratio, and quick ratio, are calculated and interpreted to assess the company's profitability, liquidity, and financial leverage. Furthermore, the report explores investment appraisal techniques and discusses potential sources of finance for Roast Ltd. The analysis aims to provide insights into Roast Ltd's financial health and assist in the evaluation of its investment opportunities and strategic decisions, ultimately supporting the acquisition decision by Starbucks.

Financial Decision Making

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

EXECUTIVE SUMMARY.............................................................................................................2

PART 1: Industry Review...............................................................................................................2

PART 2: Business Performance Analysis.......................................................................................3

2.1 Statement of profit & loss......................................................................................................3

2.2 Statement of financial position..............................................................................................5

2.3 Statement of cash flow...........................................................................................................7

PART 3 Investment Appraisal Techniques...................................................................................10

3.1 (a) Management forecast.....................................................................................................10

3.1 (b) Investment appraisal techniques....................................................................................10

3.2 Sources of finance................................................................................................................12

REFERENCES..............................................................................................................................13

1

PART 1: Industry Review...............................................................................................................2

PART 2: Business Performance Analysis.......................................................................................3

2.1 Statement of profit & loss......................................................................................................3

2.2 Statement of financial position..............................................................................................5

2.3 Statement of cash flow...........................................................................................................7

PART 3 Investment Appraisal Techniques...................................................................................10

3.1 (a) Management forecast.....................................................................................................10

3.1 (b) Investment appraisal techniques....................................................................................10

3.2 Sources of finance................................................................................................................12

REFERENCES..............................................................................................................................13

1

EXECUTIVE SUMMARY

This report summarised the Roast Ltd, that is one of the popular UK coffee houses. The staff

of the Fund Department of Starbucks asked by the Chief Financial Officer to reassess the

spending plan and the elegance of their business in order to acquire it after that. With this

function, all statements are evaluated, and that is why ratios such as net ratio, gross and operating

profit ratios, debt fairness, current, fast ratios along with side operating cycles are all determined.

The Roast Ltd organisation has also decided to invest approximately 500 lbs. from the

corporation in order to determine the efficiency of the various investment strategies used. The

point must organise for the investment to spend in the planned work, which is why the way is

proposed to get a financial loan from the bank so that the employment-related goals might

probably be finally implemented. Starbucks Company should acquire Roast ltd which helps the

organization to maximise their market shares and revenues.

PART 1: Industry Review

Since coffee is really only efficiently grow near the equator, the national value chain

starts with distributors and sales people at the entry point into the United Kingdom.

Green coffee is the single biggest coffee type imported into United Kingdom (Cook and

Sadeghein, 2018). However, the supplier mechanisms in location mean that imported

goods from the EU, mostly roasted coffee and dissolved coffee, are of higher benefit than

imported goods from the rest of the globe.

A huge number of retail coffees are distributed by supermarkets and convenience stores,

making up for 35% and 37% of all coffee retailers, respectively.

The United Kingdom is typically known for the intake of instant coffee. Standard instant

coffee produced revenue of approximately 810 million in 2017, comparable to 54 %

of total turnover of £ 1.5 billion created by all coffee goods purchased in the retail

industry.

Even after this, the amount of instant coffee sales declined following the arrival of

broader products available in the market, such as coffee makers, roasted and dried coffee

and blended coffee.

2

This report summarised the Roast Ltd, that is one of the popular UK coffee houses. The staff

of the Fund Department of Starbucks asked by the Chief Financial Officer to reassess the

spending plan and the elegance of their business in order to acquire it after that. With this

function, all statements are evaluated, and that is why ratios such as net ratio, gross and operating

profit ratios, debt fairness, current, fast ratios along with side operating cycles are all determined.

The Roast Ltd organisation has also decided to invest approximately 500 lbs. from the

corporation in order to determine the efficiency of the various investment strategies used. The

point must organise for the investment to spend in the planned work, which is why the way is

proposed to get a financial loan from the bank so that the employment-related goals might

probably be finally implemented. Starbucks Company should acquire Roast ltd which helps the

organization to maximise their market shares and revenues.

PART 1: Industry Review

Since coffee is really only efficiently grow near the equator, the national value chain

starts with distributors and sales people at the entry point into the United Kingdom.

Green coffee is the single biggest coffee type imported into United Kingdom (Cook and

Sadeghein, 2018). However, the supplier mechanisms in location mean that imported

goods from the EU, mostly roasted coffee and dissolved coffee, are of higher benefit than

imported goods from the rest of the globe.

A huge number of retail coffees are distributed by supermarkets and convenience stores,

making up for 35% and 37% of all coffee retailers, respectively.

The United Kingdom is typically known for the intake of instant coffee. Standard instant

coffee produced revenue of approximately 810 million in 2017, comparable to 54 %

of total turnover of £ 1.5 billion created by all coffee goods purchased in the retail

industry.

Even after this, the amount of instant coffee sales declined following the arrival of

broader products available in the market, such as coffee makers, roasted and dried coffee

and blended coffee.

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Fresh coffee grounds pods produced revenue of approximately 305 million in 2017,

second only to daily instant coffee (Bangma, 2019). Whereas the regular fresh ground

coffee had a profit margin of£214 million that same year.

This pattern is attributed to the growing coffeehouse cultural identity in the United

Kingdom and the increasing preference for 'barista quality' coffee at home.

At current situation, this industry is expanding its business operations at world stage,

such as China, Australia and other markets.

Industry revenues are expected to raise from 2019-20 by about £6.6 billion at a

cumulative annual rate of 4.8 per cent over five years, plus 1.9 % growth over the

existing year.

PART 2: Business Performance Analysis

2.1 Statement of profit & loss

Analysis of Profit and loss statements includes the review of the different line components

in the document, and also the creation of unique items that have been observed over a given

interval. This approach is being used to understand the company's market structure as well as its

ability to make profits. All the variables of the company produce annual financial report on the

basis of the task of documenting much of the direct, indirect, operational and non-operational

expenditures together, with the result that maturity might probably be expected.

In order to attract many shareholders, it is important for the company to be certain that its

own invoice is rendered in an organised way to maintain that outside stakeholders are able to

measure the possible returns that might probably be produced by them (Erkut,

2018). Throughout this context, the income-statement review of Roast Ltd explains the firm's

net growth from £2022000 to £2534000 that is 25.32 % between 2017 to period 2018, whereas

the firm's sales costs increased from £1505000 to £1990000 during 2017 and 2018.

The company's operating revenue in 2018 was 60,000. From the other hand, running costs

increased from £466,000 in 2017 and £477,000 in 2018. In 2018 and 2017, Roast Ltd posted an

operating profit of 127000 pound and 51000 pound, both of which reflect an upward trend. In

2018 and 2017, the gross net profit of the organisation was 81000 and 36000, which also

indicates that the amount of economic profit of the business has increased. For the aim of

evaluating the overall position of the company, the following ratios are calculated:

3

second only to daily instant coffee (Bangma, 2019). Whereas the regular fresh ground

coffee had a profit margin of£214 million that same year.

This pattern is attributed to the growing coffeehouse cultural identity in the United

Kingdom and the increasing preference for 'barista quality' coffee at home.

At current situation, this industry is expanding its business operations at world stage,

such as China, Australia and other markets.

Industry revenues are expected to raise from 2019-20 by about £6.6 billion at a

cumulative annual rate of 4.8 per cent over five years, plus 1.9 % growth over the

existing year.

PART 2: Business Performance Analysis

2.1 Statement of profit & loss

Analysis of Profit and loss statements includes the review of the different line components

in the document, and also the creation of unique items that have been observed over a given

interval. This approach is being used to understand the company's market structure as well as its

ability to make profits. All the variables of the company produce annual financial report on the

basis of the task of documenting much of the direct, indirect, operational and non-operational

expenditures together, with the result that maturity might probably be expected.

In order to attract many shareholders, it is important for the company to be certain that its

own invoice is rendered in an organised way to maintain that outside stakeholders are able to

measure the possible returns that might probably be produced by them (Erkut,

2018). Throughout this context, the income-statement review of Roast Ltd explains the firm's

net growth from £2022000 to £2534000 that is 25.32 % between 2017 to period 2018, whereas

the firm's sales costs increased from £1505000 to £1990000 during 2017 and 2018.

The company's operating revenue in 2018 was 60,000. From the other hand, running costs

increased from £466,000 in 2017 and £477,000 in 2018. In 2018 and 2017, Roast Ltd posted an

operating profit of 127000 pound and 51000 pound, both of which reflect an upward trend. In

2018 and 2017, the gross net profit of the organisation was 81000 and 36000, which also

indicates that the amount of economic profit of the business has increased. For the aim of

evaluating the overall position of the company, the following ratios are calculated:

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

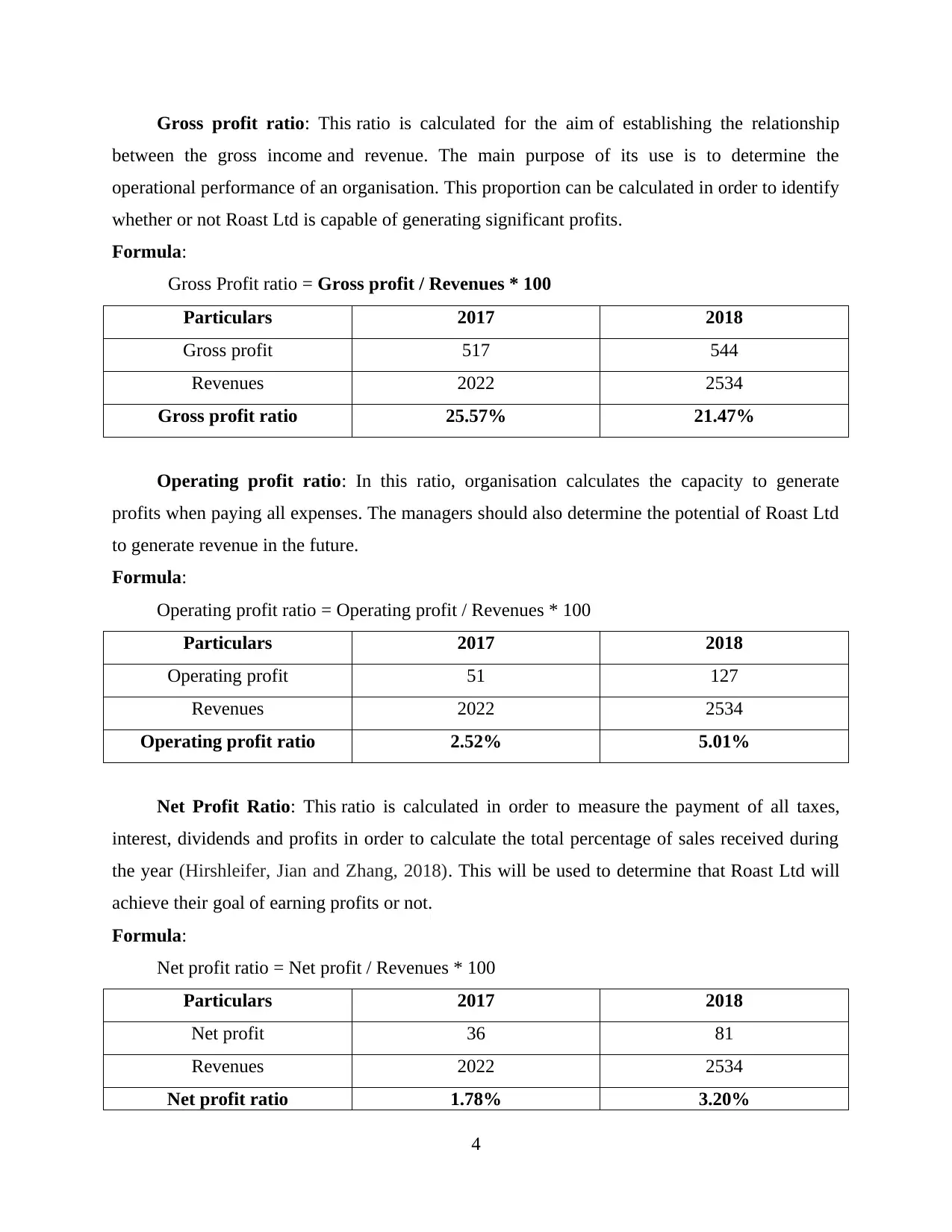

Gross profit ratio: This ratio is calculated for the aim of establishing the relationship

between the gross income and revenue. The main purpose of its use is to determine the

operational performance of an organisation. This proportion can be calculated in order to identify

whether or not Roast Ltd is capable of generating significant profits.

Formula:

Gross Profit ratio = Gross profit / Revenues * 100

Particulars 2017 2018

Gross profit 517 544

Revenues 2022 2534

Gross profit ratio 25.57% 21.47%

Operating profit ratio: In this ratio, organisation calculates the capacity to generate

profits when paying all expenses. The managers should also determine the potential of Roast Ltd

to generate revenue in the future.

Formula:

Operating profit ratio = Operating profit / Revenues * 100

Particulars 2017 2018

Operating profit 51 127

Revenues 2022 2534

Operating profit ratio 2.52% 5.01%

Net Profit Ratio: This ratio is calculated in order to measure the payment of all taxes,

interest, dividends and profits in order to calculate the total percentage of sales received during

the year (Hirshleifer, Jian and Zhang, 2018). This will be used to determine that Roast Ltd will

achieve their goal of earning profits or not.

Formula:

Net profit ratio = Net profit / Revenues * 100

Particulars 2017 2018

Net profit 36 81

Revenues 2022 2534

Net profit ratio 1.78% 3.20%

4

between the gross income and revenue. The main purpose of its use is to determine the

operational performance of an organisation. This proportion can be calculated in order to identify

whether or not Roast Ltd is capable of generating significant profits.

Formula:

Gross Profit ratio = Gross profit / Revenues * 100

Particulars 2017 2018

Gross profit 517 544

Revenues 2022 2534

Gross profit ratio 25.57% 21.47%

Operating profit ratio: In this ratio, organisation calculates the capacity to generate

profits when paying all expenses. The managers should also determine the potential of Roast Ltd

to generate revenue in the future.

Formula:

Operating profit ratio = Operating profit / Revenues * 100

Particulars 2017 2018

Operating profit 51 127

Revenues 2022 2534

Operating profit ratio 2.52% 5.01%

Net Profit Ratio: This ratio is calculated in order to measure the payment of all taxes,

interest, dividends and profits in order to calculate the total percentage of sales received during

the year (Hirshleifer, Jian and Zhang, 2018). This will be used to determine that Roast Ltd will

achieve their goal of earning profits or not.

Formula:

Net profit ratio = Net profit / Revenues * 100

Particulars 2017 2018

Net profit 36 81

Revenues 2022 2534

Net profit ratio 1.78% 3.20%

4

From the above analysis of ratios, it has been interpreted that gross margin ratio was

higher in 2017 compared to 2018, which suggests that the operating performance of the company

in this year could have been substantial compared to 2018. Operating and net profit statistics

indicate that the output of Roast Ltd in 2017 is poorer as of 2018. It reveals that the company

produced improved returns in 2018 compared to the previous year. These statistics indicate that

the popularity of the company is high at the current time but that it can attract a large number of

enterprises.

2.2 Statement of financial position

Business organisations report the financial condition for the intent of disclosing that the

company will or may not have been able to support the industry. It is important for several

companies to produce it on a yearly basis so that internal or external parties can analyse the

financial condition. In addition to external participants such as creditors, staff, investors,

customers, government, etc., can monitor the success of business enterprises (Kimmel,

Weygandt and Kieso, 2018). There seems to be a variety of features that may require value-

added and clarity, accuracy, usability, etc. In this context of Roast Ltd, based on the evaluation

of the parts of the budget described in Roast Ltd's Statement of Financial Condition, the

company generated capital expenditure on the purchase of machinery, plant and equipment

(PPE) as the corporation's PPE value increased from £670,000 to £996,000 between 2017 and

2018.

Another interesting point with this is that the company's cash transactions, and this in 2017

amounted to £134,000, were reported to be zero in 2018, suggesting that the company already

used its financial capital throughout 2018. However, overall existing rate of assets managed to

hit a peak of 447,000 pounds in 2017, and that was 347,000 pounds. Corporate entity did not

issue any ownership stakes during 2018 as the total share capital was £200,000 in both periods.

In 2018, the retained earnings of net profit and other assets company were estimated to be

£660,000, but in 2017 they were £579,000. As a result, total equity funds are rising from

£779,000 to £860,000.

Long term corporate borrowings are dramatically changing, although the company's long-

term loans increased to £275,000 in 2018, and that was £100,000 in 2017. In 2018, the company

5

higher in 2017 compared to 2018, which suggests that the operating performance of the company

in this year could have been substantial compared to 2018. Operating and net profit statistics

indicate that the output of Roast Ltd in 2017 is poorer as of 2018. It reveals that the company

produced improved returns in 2018 compared to the previous year. These statistics indicate that

the popularity of the company is high at the current time but that it can attract a large number of

enterprises.

2.2 Statement of financial position

Business organisations report the financial condition for the intent of disclosing that the

company will or may not have been able to support the industry. It is important for several

companies to produce it on a yearly basis so that internal or external parties can analyse the

financial condition. In addition to external participants such as creditors, staff, investors,

customers, government, etc., can monitor the success of business enterprises (Kimmel,

Weygandt and Kieso, 2018). There seems to be a variety of features that may require value-

added and clarity, accuracy, usability, etc. In this context of Roast Ltd, based on the evaluation

of the parts of the budget described in Roast Ltd's Statement of Financial Condition, the

company generated capital expenditure on the purchase of machinery, plant and equipment

(PPE) as the corporation's PPE value increased from £670,000 to £996,000 between 2017 and

2018.

Another interesting point with this is that the company's cash transactions, and this in 2017

amounted to £134,000, were reported to be zero in 2018, suggesting that the company already

used its financial capital throughout 2018. However, overall existing rate of assets managed to

hit a peak of 447,000 pounds in 2017, and that was 347,000 pounds. Corporate entity did not

issue any ownership stakes during 2018 as the total share capital was £200,000 in both periods.

In 2018, the retained earnings of net profit and other assets company were estimated to be

£660,000, but in 2017 they were £579,000. As a result, total equity funds are rising from

£779,000 to £860,000.

Long term corporate borrowings are dramatically changing, although the company's long-

term loans increased to £275,000 in 2018, and that was £100,000 in 2017. In 2018, the company

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

also purchased a bank overdraft service worth £ 73,000. Company's commercial creditors shifted

from 138000 to 235000 mostly during 2017-2018 eras. Over the period 2017 to 2018, the

cumulative average liabilities are increased by £ 345000 (from £238000 to £583000). The

purpose of the examination of the project after ratios would also be determined in the

circumstances of Roast Ltd. The definitions of most of them are as follows:

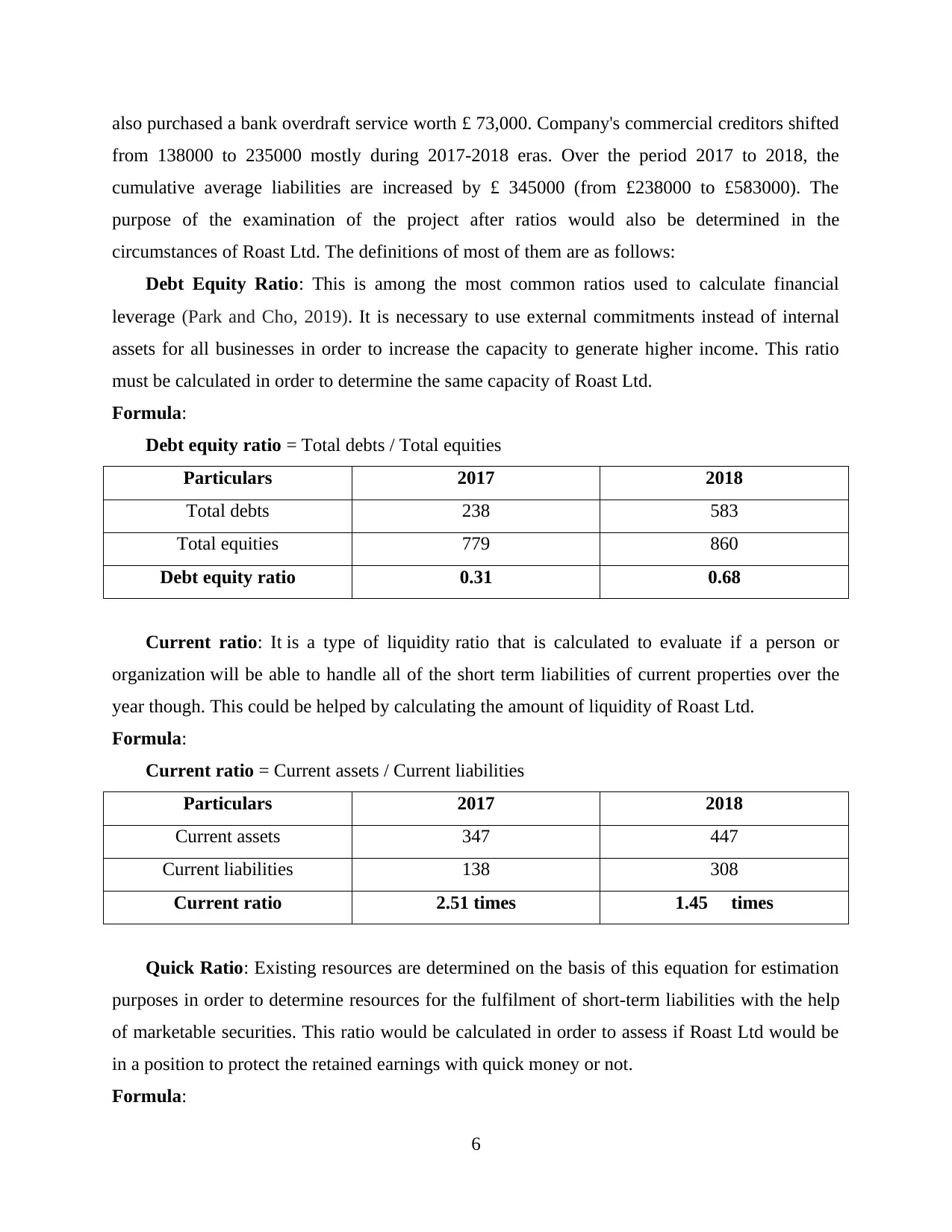

Debt Equity Ratio: This is among the most common ratios used to calculate financial

leverage (Park and Cho, 2019). It is necessary to use external commitments instead of internal

assets for all businesses in order to increase the capacity to generate higher income. This ratio

must be calculated in order to determine the same capacity of Roast Ltd.

Formula:

Debt equity ratio = Total debts / Total equities

Particulars 2017 2018

Total debts 238 583

Total equities 779 860

Debt equity ratio 0.31 0.68

Current ratio: It is a type of liquidity ratio that is calculated to evaluate if a person or

organization will be able to handle all of the short term liabilities of current properties over the

year though. This could be helped by calculating the amount of liquidity of Roast Ltd.

Formula:

Current ratio = Current assets / Current liabilities

Particulars 2017 2018

Current assets 347 447

Current liabilities 138 308

Current ratio 2.51 times 1.45 times

Quick Ratio: Existing resources are determined on the basis of this equation for estimation

purposes in order to determine resources for the fulfilment of short-term liabilities with the help

of marketable securities. This ratio would be calculated in order to assess if Roast Ltd would be

in a position to protect the retained earnings with quick money or not.

Formula:

6

from 138000 to 235000 mostly during 2017-2018 eras. Over the period 2017 to 2018, the

cumulative average liabilities are increased by £ 345000 (from £238000 to £583000). The

purpose of the examination of the project after ratios would also be determined in the

circumstances of Roast Ltd. The definitions of most of them are as follows:

Debt Equity Ratio: This is among the most common ratios used to calculate financial

leverage (Park and Cho, 2019). It is necessary to use external commitments instead of internal

assets for all businesses in order to increase the capacity to generate higher income. This ratio

must be calculated in order to determine the same capacity of Roast Ltd.

Formula:

Debt equity ratio = Total debts / Total equities

Particulars 2017 2018

Total debts 238 583

Total equities 779 860

Debt equity ratio 0.31 0.68

Current ratio: It is a type of liquidity ratio that is calculated to evaluate if a person or

organization will be able to handle all of the short term liabilities of current properties over the

year though. This could be helped by calculating the amount of liquidity of Roast Ltd.

Formula:

Current ratio = Current assets / Current liabilities

Particulars 2017 2018

Current assets 347 447

Current liabilities 138 308

Current ratio 2.51 times 1.45 times

Quick Ratio: Existing resources are determined on the basis of this equation for estimation

purposes in order to determine resources for the fulfilment of short-term liabilities with the help

of marketable securities. This ratio would be calculated in order to assess if Roast Ltd would be

in a position to protect the retained earnings with quick money or not.

Formula:

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Quick ratio = Quick assets / Current liabilities

Particulars 2017 2018

Quick assets 227 148

Current liabilities 138 308

Quick ratio 1.64 times 0.48 times

From the overall ratio analysis of Roast Ltd, it has been concluded that in 2018, Roast Ltd

used more liabilities instead of equity markets, which shows that the outcome of the business

increased over time (Rai and Lin, 2019). Current ratio results indicate that the stabilisation of the

entity is weak in 2018 compared to 2017. The Quick ratio is also very low in 2018 duration. Both

suggest that the versatility of the person is very limited. The performance of Roast Ltd is not

good leading to decreased profitability, as stated in the Financial Statement. Therefore,

irrespective of this ability, the company is reduced to pay for the amount of the short term

liabilities.

2.3 Statement of cash flow

All of the business factors create an official statement to catch recommendation about future

cash inflows and out flows that money supply of such organisation can probably be conclusively

proven that it is called update of cash flows. Primary reason for its methodology would be to

analyse that the venture can fulfil most of the lengthy-term targets but maybe not. With aid of

this, the managers will decide that they should spend less on potential operation instead of on it.

When shaping it, there are various activities that are running, funding and spending. Even by

conclusion full effort is required to ensure that it can be conclusively proven that the company

has made money or paying it to external parties.

This could be revealed in Roast Limited Company’s perspective that the cash flows from

operating activities were depressed £24,000 in the year-2018. This indicates more actions have

become provoking cash flows. Operational activities, caused by the cash outflow of inventories,

amounted to approximately £179,000 but improved by £55,000 in industrial receivables (Stewart

and et.al., 2018). While the financial structure of the capital spending is unfavourable, as a result

of substantial capital spending, to the purchase of land, plant and equipment by the company.

Increasing long-term debts have resulted in a rise of £175,000 in cash flows from financing

operations.

7

Particulars 2017 2018

Quick assets 227 148

Current liabilities 138 308

Quick ratio 1.64 times 0.48 times

From the overall ratio analysis of Roast Ltd, it has been concluded that in 2018, Roast Ltd

used more liabilities instead of equity markets, which shows that the outcome of the business

increased over time (Rai and Lin, 2019). Current ratio results indicate that the stabilisation of the

entity is weak in 2018 compared to 2017. The Quick ratio is also very low in 2018 duration. Both

suggest that the versatility of the person is very limited. The performance of Roast Ltd is not

good leading to decreased profitability, as stated in the Financial Statement. Therefore,

irrespective of this ability, the company is reduced to pay for the amount of the short term

liabilities.

2.3 Statement of cash flow

All of the business factors create an official statement to catch recommendation about future

cash inflows and out flows that money supply of such organisation can probably be conclusively

proven that it is called update of cash flows. Primary reason for its methodology would be to

analyse that the venture can fulfil most of the lengthy-term targets but maybe not. With aid of

this, the managers will decide that they should spend less on potential operation instead of on it.

When shaping it, there are various activities that are running, funding and spending. Even by

conclusion full effort is required to ensure that it can be conclusively proven that the company

has made money or paying it to external parties.

This could be revealed in Roast Limited Company’s perspective that the cash flows from

operating activities were depressed £24,000 in the year-2018. This indicates more actions have

become provoking cash flows. Operational activities, caused by the cash outflow of inventories,

amounted to approximately £179,000 but improved by £55,000 in industrial receivables (Stewart

and et.al., 2018). While the financial structure of the capital spending is unfavourable, as a result

of substantial capital spending, to the purchase of land, plant and equipment by the company.

Increasing long-term debts have resulted in a rise of £175,000 in cash flows from financing

operations.

7

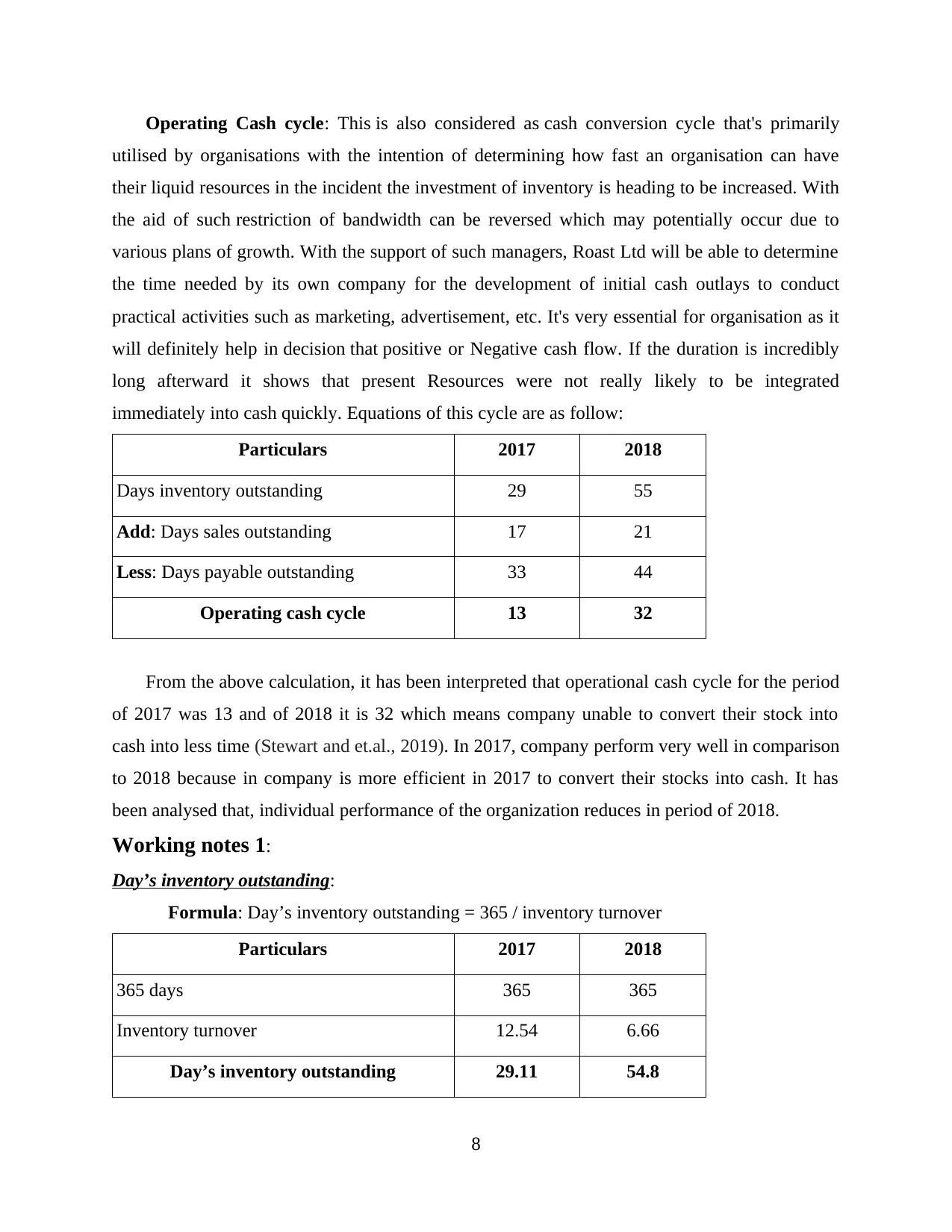

Operating Cash cycle: This is also considered as cash conversion cycle that's primarily

utilised by organisations with the intention of determining how fast an organisation can have

their liquid resources in the incident the investment of inventory is heading to be increased. With

the aid of such restriction of bandwidth can be reversed which may potentially occur due to

various plans of growth. With the support of such managers, Roast Ltd will be able to determine

the time needed by its own company for the development of initial cash outlays to conduct

practical activities such as marketing, advertisement, etc. It's very essential for organisation as it

will definitely help in decision that positive or Negative cash flow. If the duration is incredibly

long afterward it shows that present Resources were not really likely to be integrated

immediately into cash quickly. Equations of this cycle are as follow:

Particulars 2017 2018

Days inventory outstanding 29 55

Add: Days sales outstanding 17 21

Less: Days payable outstanding 33 44

Operating cash cycle 13 32

From the above calculation, it has been interpreted that operational cash cycle for the period

of 2017 was 13 and of 2018 it is 32 which means company unable to convert their stock into

cash into less time (Stewart and et.al., 2019). In 2017, company perform very well in comparison

to 2018 because in company is more efficient in 2017 to convert their stocks into cash. It has

been analysed that, individual performance of the organization reduces in period of 2018.

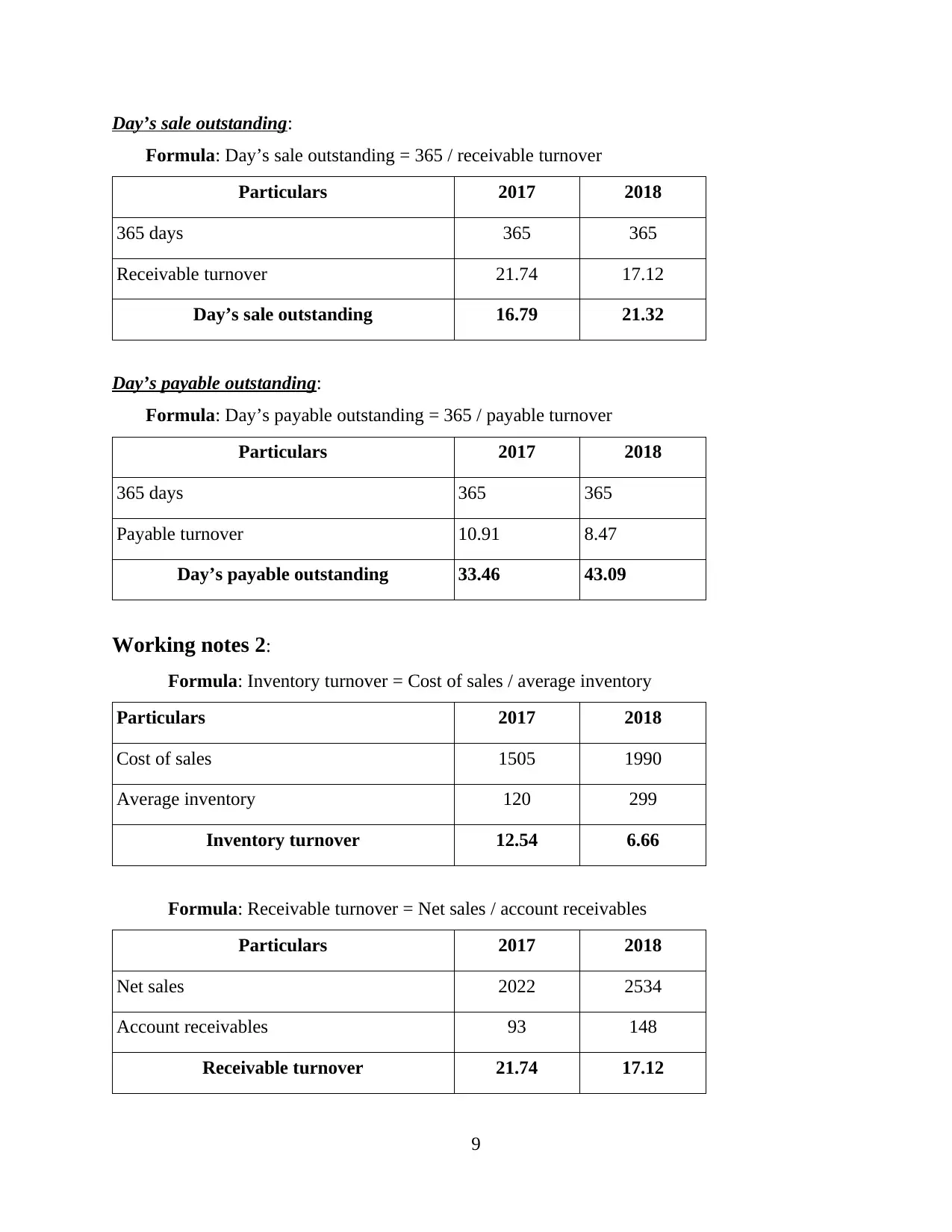

Working notes 1:

Day’s inventory outstanding:

Formula: Day’s inventory outstanding = 365 / inventory turnover

Particulars 2017 2018

365 days 365 365

Inventory turnover 12.54 6.66

Day’s inventory outstanding 29.11 54.8

8

utilised by organisations with the intention of determining how fast an organisation can have

their liquid resources in the incident the investment of inventory is heading to be increased. With

the aid of such restriction of bandwidth can be reversed which may potentially occur due to

various plans of growth. With the support of such managers, Roast Ltd will be able to determine

the time needed by its own company for the development of initial cash outlays to conduct

practical activities such as marketing, advertisement, etc. It's very essential for organisation as it

will definitely help in decision that positive or Negative cash flow. If the duration is incredibly

long afterward it shows that present Resources were not really likely to be integrated

immediately into cash quickly. Equations of this cycle are as follow:

Particulars 2017 2018

Days inventory outstanding 29 55

Add: Days sales outstanding 17 21

Less: Days payable outstanding 33 44

Operating cash cycle 13 32

From the above calculation, it has been interpreted that operational cash cycle for the period

of 2017 was 13 and of 2018 it is 32 which means company unable to convert their stock into

cash into less time (Stewart and et.al., 2019). In 2017, company perform very well in comparison

to 2018 because in company is more efficient in 2017 to convert their stocks into cash. It has

been analysed that, individual performance of the organization reduces in period of 2018.

Working notes 1:

Day’s inventory outstanding:

Formula: Day’s inventory outstanding = 365 / inventory turnover

Particulars 2017 2018

365 days 365 365

Inventory turnover 12.54 6.66

Day’s inventory outstanding 29.11 54.8

8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Day’s sale outstanding:

Formula: Day’s sale outstanding = 365 / receivable turnover

Particulars 2017 2018

365 days 365 365

Receivable turnover 21.74 17.12

Day’s sale outstanding 16.79 21.32

Day’s payable outstanding:

Formula: Day’s payable outstanding = 365 / payable turnover

Particulars 2017 2018

365 days 365 365

Payable turnover 10.91 8.47

Day’s payable outstanding 33.46 43.09

Working notes 2:

Formula: Inventory turnover = Cost of sales / average inventory

Particulars 2017 2018

Cost of sales 1505 1990

Average inventory 120 299

Inventory turnover 12.54 6.66

Formula: Receivable turnover = Net sales / account receivables

Particulars 2017 2018

Net sales 2022 2534

Account receivables 93 148

Receivable turnover 21.74 17.12

9

Formula: Day’s sale outstanding = 365 / receivable turnover

Particulars 2017 2018

365 days 365 365

Receivable turnover 21.74 17.12

Day’s sale outstanding 16.79 21.32

Day’s payable outstanding:

Formula: Day’s payable outstanding = 365 / payable turnover

Particulars 2017 2018

365 days 365 365

Payable turnover 10.91 8.47

Day’s payable outstanding 33.46 43.09

Working notes 2:

Formula: Inventory turnover = Cost of sales / average inventory

Particulars 2017 2018

Cost of sales 1505 1990

Average inventory 120 299

Inventory turnover 12.54 6.66

Formula: Receivable turnover = Net sales / account receivables

Particulars 2017 2018

Net sales 2022 2534

Account receivables 93 148

Receivable turnover 21.74 17.12

9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

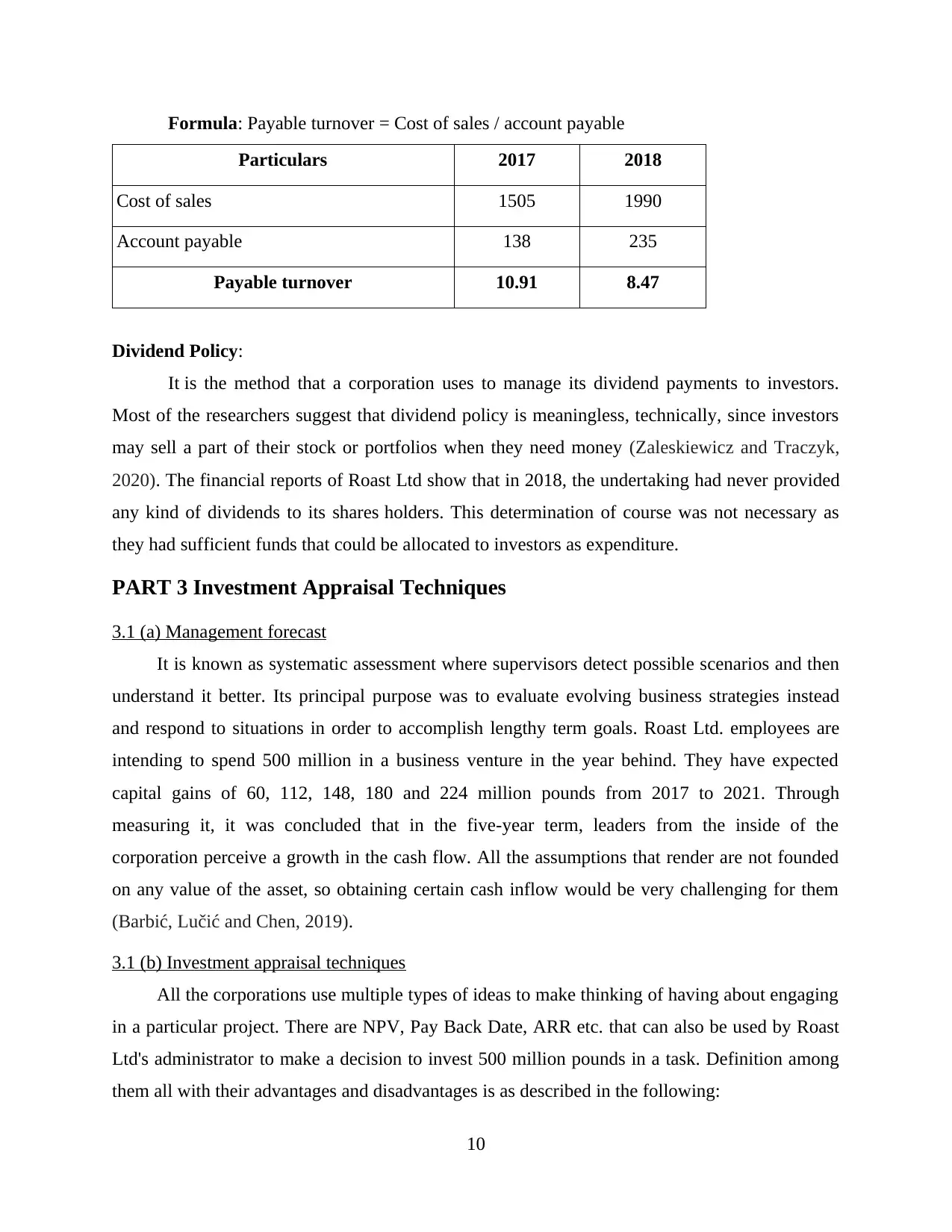

Formula: Payable turnover = Cost of sales / account payable

Particulars 2017 2018

Cost of sales 1505 1990

Account payable 138 235

Payable turnover 10.91 8.47

Dividend Policy:

It is the method that a corporation uses to manage its dividend payments to investors.

Most of the researchers suggest that dividend policy is meaningless, technically, since investors

may sell a part of their stock or portfolios when they need money (Zaleskiewicz and Traczyk,

2020). The financial reports of Roast Ltd show that in 2018, the undertaking had never provided

any kind of dividends to its shares holders. This determination of course was not necessary as

they had sufficient funds that could be allocated to investors as expenditure.

PART 3 Investment Appraisal Techniques

3.1 (a) Management forecast

It is known as systematic assessment where supervisors detect possible scenarios and then

understand it better. Its principal purpose was to evaluate evolving business strategies instead

and respond to situations in order to accomplish lengthy term goals. Roast Ltd. employees are

intending to spend 500 million in a business venture in the year behind. They have expected

capital gains of 60, 112, 148, 180 and 224 million pounds from 2017 to 2021. Through

measuring it, it was concluded that in the five-year term, leaders from the inside of the

corporation perceive a growth in the cash flow. All the assumptions that render are not founded

on any value of the asset, so obtaining certain cash inflow would be very challenging for them

(Barbić, Lučić and Chen, 2019).

3.1 (b) Investment appraisal techniques

All the corporations use multiple types of ideas to make thinking of having about engaging

in a particular project. There are NPV, Pay Back Date, ARR etc. that can also be used by Roast

Ltd's administrator to make a decision to invest 500 million pounds in a task. Definition among

them all with their advantages and disadvantages is as described in the following:

10

Particulars 2017 2018

Cost of sales 1505 1990

Account payable 138 235

Payable turnover 10.91 8.47

Dividend Policy:

It is the method that a corporation uses to manage its dividend payments to investors.

Most of the researchers suggest that dividend policy is meaningless, technically, since investors

may sell a part of their stock or portfolios when they need money (Zaleskiewicz and Traczyk,

2020). The financial reports of Roast Ltd show that in 2018, the undertaking had never provided

any kind of dividends to its shares holders. This determination of course was not necessary as

they had sufficient funds that could be allocated to investors as expenditure.

PART 3 Investment Appraisal Techniques

3.1 (a) Management forecast

It is known as systematic assessment where supervisors detect possible scenarios and then

understand it better. Its principal purpose was to evaluate evolving business strategies instead

and respond to situations in order to accomplish lengthy term goals. Roast Ltd. employees are

intending to spend 500 million in a business venture in the year behind. They have expected

capital gains of 60, 112, 148, 180 and 224 million pounds from 2017 to 2021. Through

measuring it, it was concluded that in the five-year term, leaders from the inside of the

corporation perceive a growth in the cash flow. All the assumptions that render are not founded

on any value of the asset, so obtaining certain cash inflow would be very challenging for them

(Barbić, Lučić and Chen, 2019).

3.1 (b) Investment appraisal techniques

All the corporations use multiple types of ideas to make thinking of having about engaging

in a particular project. There are NPV, Pay Back Date, ARR etc. that can also be used by Roast

Ltd's administrator to make a decision to invest 500 million pounds in a task. Definition among

them all with their advantages and disadvantages is as described in the following:

10

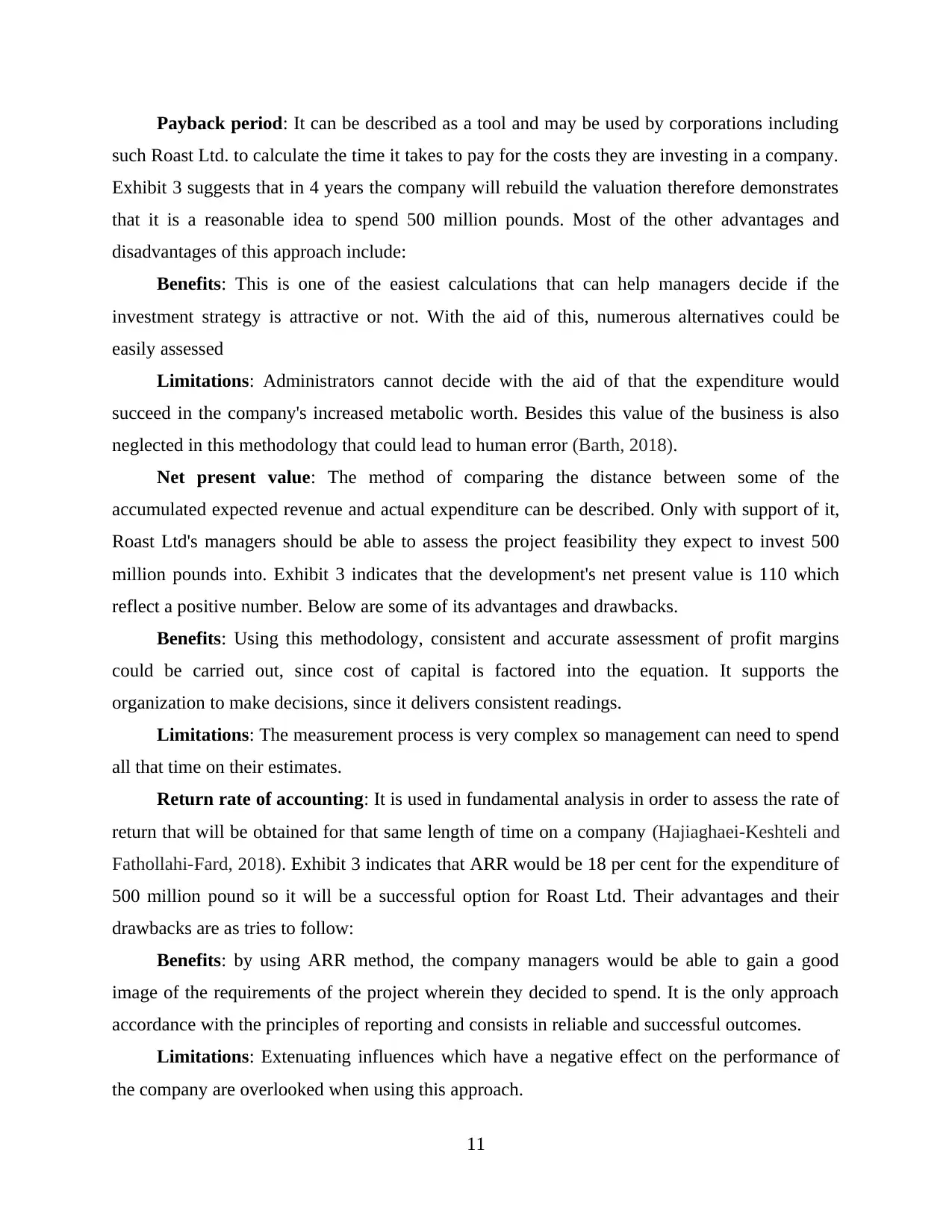

Payback period: It can be described as a tool and may be used by corporations including

such Roast Ltd. to calculate the time it takes to pay for the costs they are investing in a company.

Exhibit 3 suggests that in 4 years the company will rebuild the valuation therefore demonstrates

that it is a reasonable idea to spend 500 million pounds. Most of the other advantages and

disadvantages of this approach include:

Benefits: This is one of the easiest calculations that can help managers decide if the

investment strategy is attractive or not. With the aid of this, numerous alternatives could be

easily assessed

Limitations: Administrators cannot decide with the aid of that the expenditure would

succeed in the company's increased metabolic worth. Besides this value of the business is also

neglected in this methodology that could lead to human error (Barth, 2018).

Net present value: The method of comparing the distance between some of the

accumulated expected revenue and actual expenditure can be described. Only with support of it,

Roast Ltd's managers should be able to assess the project feasibility they expect to invest 500

million pounds into. Exhibit 3 indicates that the development's net present value is 110 which

reflect a positive number. Below are some of its advantages and drawbacks.

Benefits: Using this methodology, consistent and accurate assessment of profit margins

could be carried out, since cost of capital is factored into the equation. It supports the

organization to make decisions, since it delivers consistent readings.

Limitations: The measurement process is very complex so management can need to spend

all that time on their estimates.

Return rate of accounting: It is used in fundamental analysis in order to assess the rate of

return that will be obtained for that same length of time on a company (Hajiaghaei-Keshteli and

Fathollahi-Fard, 2018). Exhibit 3 indicates that ARR would be 18 per cent for the expenditure of

500 million pound so it will be a successful option for Roast Ltd. Their advantages and their

drawbacks are as tries to follow:

Benefits: by using ARR method, the company managers would be able to gain a good

image of the requirements of the project wherein they decided to spend. It is the only approach

accordance with the principles of reporting and consists in reliable and successful outcomes.

Limitations: Extenuating influences which have a negative effect on the performance of

the company are overlooked when using this approach.

11

such Roast Ltd. to calculate the time it takes to pay for the costs they are investing in a company.

Exhibit 3 suggests that in 4 years the company will rebuild the valuation therefore demonstrates

that it is a reasonable idea to spend 500 million pounds. Most of the other advantages and

disadvantages of this approach include:

Benefits: This is one of the easiest calculations that can help managers decide if the

investment strategy is attractive or not. With the aid of this, numerous alternatives could be

easily assessed

Limitations: Administrators cannot decide with the aid of that the expenditure would

succeed in the company's increased metabolic worth. Besides this value of the business is also

neglected in this methodology that could lead to human error (Barth, 2018).

Net present value: The method of comparing the distance between some of the

accumulated expected revenue and actual expenditure can be described. Only with support of it,

Roast Ltd's managers should be able to assess the project feasibility they expect to invest 500

million pounds into. Exhibit 3 indicates that the development's net present value is 110 which

reflect a positive number. Below are some of its advantages and drawbacks.

Benefits: Using this methodology, consistent and accurate assessment of profit margins

could be carried out, since cost of capital is factored into the equation. It supports the

organization to make decisions, since it delivers consistent readings.

Limitations: The measurement process is very complex so management can need to spend

all that time on their estimates.

Return rate of accounting: It is used in fundamental analysis in order to assess the rate of

return that will be obtained for that same length of time on a company (Hajiaghaei-Keshteli and

Fathollahi-Fard, 2018). Exhibit 3 indicates that ARR would be 18 per cent for the expenditure of

500 million pound so it will be a successful option for Roast Ltd. Their advantages and their

drawbacks are as tries to follow:

Benefits: by using ARR method, the company managers would be able to gain a good

image of the requirements of the project wherein they decided to spend. It is the only approach

accordance with the principles of reporting and consists in reliable and successful outcomes.

Limitations: Extenuating influences which have a negative effect on the performance of

the company are overlooked when using this approach.

11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.