Financial Decision Making and Investment Appraisal for Easyflight Plc

VerifiedAdded on 2021/02/19

|17

|5041

|140

Report

AI Summary

This report provides a comprehensive financial analysis of Easyflight Plc, examining its financial performance through various financial statements, including profit and loss, financial position, and cash flow statements. It delves into key financial ratios, such as solvency, profitability, efficiency, and liquidity ratios, to assess the company's financial health and operational efficiency. The report also explores investment appraisal tools and the different sources for raising finance, alongside non-financial factors influencing the company's expansion. The analysis covers market segment analysis and provides insights into Easyflight Plc's dividend policy and operating cash cycle. The report aims to evaluate Easyflight Plc's financial position and identify ways to improve its market performance, offering a detailed overview of its financial strategies and outcomes.

Financial decision making

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

EXECUTIVE SUMMARY.............................................................................................................3

PART 1............................................................................................................................................3

1.1 Profit and loss statement.......................................................................................................3

1.2 Financial position statement..................................................................................................4

1.3 Cash flow statement..............................................................................................................6

1.4 Market segment analysis.......................................................................................................8

PART-2............................................................................................................................................8

2.1.a Management forecast ........................................................................................................8

2.1.b Investment appraisal tools .................................................................................................9

2.2 Sources for raising finance..................................................................................................11

2.3 Non – financial factors........................................................................................................13

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

EXECUTIVE SUMMARY.............................................................................................................3

PART 1............................................................................................................................................3

1.1 Profit and loss statement.......................................................................................................3

1.2 Financial position statement..................................................................................................4

1.3 Cash flow statement..............................................................................................................6

1.4 Market segment analysis.......................................................................................................8

PART-2............................................................................................................................................8

2.1.a Management forecast ........................................................................................................8

2.1.b Investment appraisal tools .................................................................................................9

2.2 Sources for raising finance..................................................................................................11

2.3 Non – financial factors........................................................................................................13

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

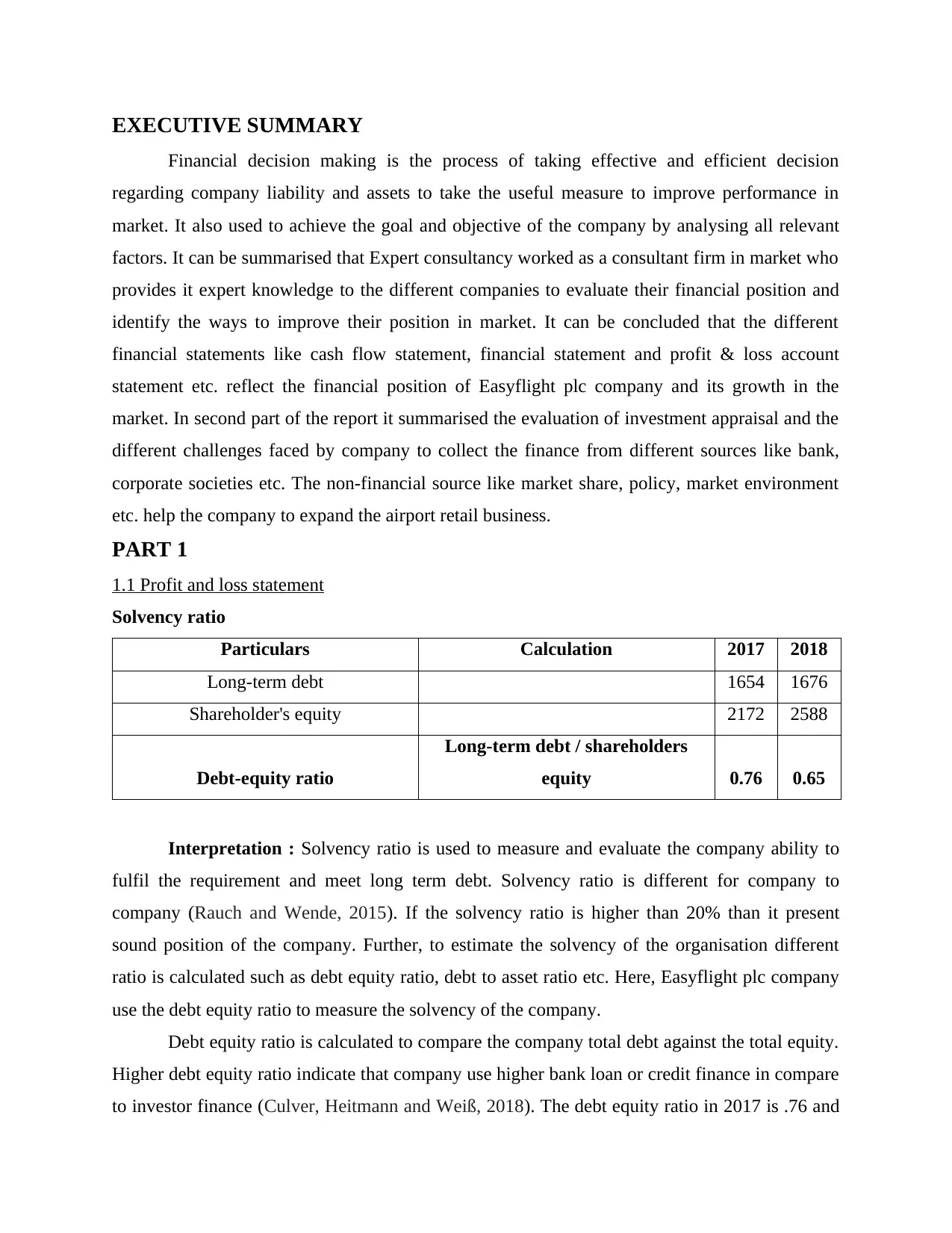

EXECUTIVE SUMMARY

Financial decision making is the process of taking effective and efficient decision

regarding company liability and assets to take the useful measure to improve performance in

market. It also used to achieve the goal and objective of the company by analysing all relevant

factors. It can be summarised that Expert consultancy worked as a consultant firm in market who

provides it expert knowledge to the different companies to evaluate their financial position and

identify the ways to improve their position in market. It can be concluded that the different

financial statements like cash flow statement, financial statement and profit & loss account

statement etc. reflect the financial position of Easyflight plc company and its growth in the

market. In second part of the report it summarised the evaluation of investment appraisal and the

different challenges faced by company to collect the finance from different sources like bank,

corporate societies etc. The non-financial source like market share, policy, market environment

etc. help the company to expand the airport retail business.

PART 1

1.1 Profit and loss statement

Solvency ratio

Particulars Calculation 2017 2018

Long-term debt 1654 1676

Shareholder's equity 2172 2588

Debt-equity ratio

Long-term debt / shareholders

equity 0.76 0.65

Interpretation : Solvency ratio is used to measure and evaluate the company ability to

fulfil the requirement and meet long term debt. Solvency ratio is different for company to

company (Rauch and Wende, 2015). If the solvency ratio is higher than 20% than it present

sound position of the company. Further, to estimate the solvency of the organisation different

ratio is calculated such as debt equity ratio, debt to asset ratio etc. Here, Easyflight plc company

use the debt equity ratio to measure the solvency of the company.

Debt equity ratio is calculated to compare the company total debt against the total equity.

Higher debt equity ratio indicate that company use higher bank loan or credit finance in compare

to investor finance (Culver, Heitmann and Weiß, 2018). The debt equity ratio in 2017 is .76 and

Financial decision making is the process of taking effective and efficient decision

regarding company liability and assets to take the useful measure to improve performance in

market. It also used to achieve the goal and objective of the company by analysing all relevant

factors. It can be summarised that Expert consultancy worked as a consultant firm in market who

provides it expert knowledge to the different companies to evaluate their financial position and

identify the ways to improve their position in market. It can be concluded that the different

financial statements like cash flow statement, financial statement and profit & loss account

statement etc. reflect the financial position of Easyflight plc company and its growth in the

market. In second part of the report it summarised the evaluation of investment appraisal and the

different challenges faced by company to collect the finance from different sources like bank,

corporate societies etc. The non-financial source like market share, policy, market environment

etc. help the company to expand the airport retail business.

PART 1

1.1 Profit and loss statement

Solvency ratio

Particulars Calculation 2017 2018

Long-term debt 1654 1676

Shareholder's equity 2172 2588

Debt-equity ratio

Long-term debt / shareholders

equity 0.76 0.65

Interpretation : Solvency ratio is used to measure and evaluate the company ability to

fulfil the requirement and meet long term debt. Solvency ratio is different for company to

company (Rauch and Wende, 2015). If the solvency ratio is higher than 20% than it present

sound position of the company. Further, to estimate the solvency of the organisation different

ratio is calculated such as debt equity ratio, debt to asset ratio etc. Here, Easyflight plc company

use the debt equity ratio to measure the solvency of the company.

Debt equity ratio is calculated to compare the company total debt against the total equity.

Higher debt equity ratio indicate that company use higher bank loan or credit finance in compare

to investor finance (Culver, Heitmann and Weiß, 2018). The debt equity ratio in 2017 is .76 and

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

in 2018 is .65 which indicate that Easyflight Plc company has more stable finance because it is

able to pay the company debt to its equity. It can be interpreted that debt to equity ratio help the

company to estimate its financial position and solvency to pay debt on time.

Profitability ratio :

Particulars Calculation 2017 2018

Gross Profit 3031 3211

Net profit 443 541

Sales revenue 4527 4686

Earnings before interest and tax or

operating profit 583 690

GP ratio Gross profit / sales * 100 67% 69%

NP ratio Net profit / sales * 100 10% 12%

OP ratio Operating profit / sales 100 12.88 14.72

Interpretation : Profitability ratio refers to generate company income or profit against its

expenses of particular accounting period. It helps to evaluate the financial position and result of

the company. Different investors use the profitability ratio to measure company performance and

its position in the market to take the decision of investment (Rabbani and et.al., 2018, June). To

interpret the profitability Easyflight plc use different ratio such as net profit, operating profit and

gross profit ratio.

Gross profit ratio also known as gross profit margin ratio. The GP ratio of Easyflight plc

company in 2017 is 67% and in 2018 is 69% which indicate that company is able to manage the

inventory level and earning higher revenue from its sales which increases the 2% gross profit in

1 year. Operating profit ratio also known as earning before interest and tax. It can be concluded

that operating profit of the company is increasing which means that company is able to deal with

the operating expenses and earn higher profit to meet the company requirement.

Net profit ratio is calculated by dividing the net profit after dealing all the expenses, tax,

dividend etc. to the sales of the particular accounting period (Al Nimer and et.al., 2015). The NP

ratio of Easyflight Plc present the overall profitability after adjusting all the direct and indirect

expenses. The net profit ratio is increase 12.88% to 14.72% which reflect that they are able to

pay the dividend to their shareholders.

able to pay the company debt to its equity. It can be interpreted that debt to equity ratio help the

company to estimate its financial position and solvency to pay debt on time.

Profitability ratio :

Particulars Calculation 2017 2018

Gross Profit 3031 3211

Net profit 443 541

Sales revenue 4527 4686

Earnings before interest and tax or

operating profit 583 690

GP ratio Gross profit / sales * 100 67% 69%

NP ratio Net profit / sales * 100 10% 12%

OP ratio Operating profit / sales 100 12.88 14.72

Interpretation : Profitability ratio refers to generate company income or profit against its

expenses of particular accounting period. It helps to evaluate the financial position and result of

the company. Different investors use the profitability ratio to measure company performance and

its position in the market to take the decision of investment (Rabbani and et.al., 2018, June). To

interpret the profitability Easyflight plc use different ratio such as net profit, operating profit and

gross profit ratio.

Gross profit ratio also known as gross profit margin ratio. The GP ratio of Easyflight plc

company in 2017 is 67% and in 2018 is 69% which indicate that company is able to manage the

inventory level and earning higher revenue from its sales which increases the 2% gross profit in

1 year. Operating profit ratio also known as earning before interest and tax. It can be concluded

that operating profit of the company is increasing which means that company is able to deal with

the operating expenses and earn higher profit to meet the company requirement.

Net profit ratio is calculated by dividing the net profit after dealing all the expenses, tax,

dividend etc. to the sales of the particular accounting period (Al Nimer and et.al., 2015). The NP

ratio of Easyflight Plc present the overall profitability after adjusting all the direct and indirect

expenses. The net profit ratio is increase 12.88% to 14.72% which reflect that they are able to

pay the dividend to their shareholders.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

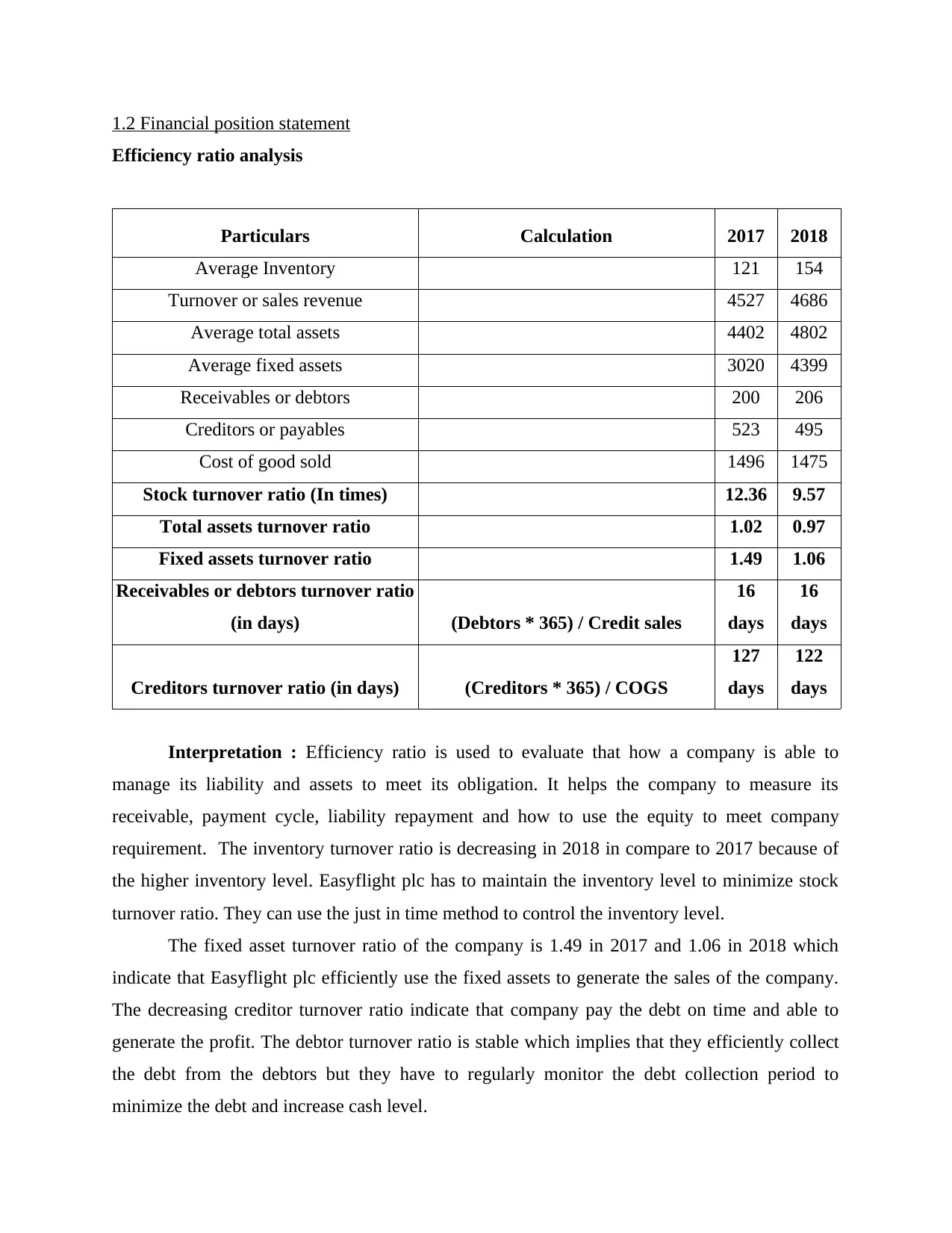

1.2 Financial position statement

Efficiency ratio analysis

Particulars Calculation 2017 2018

Average Inventory 121 154

Turnover or sales revenue 4527 4686

Average total assets 4402 4802

Average fixed assets 3020 4399

Receivables or debtors 200 206

Creditors or payables 523 495

Cost of good sold 1496 1475

Stock turnover ratio (In times) 12.36 9.57

Total assets turnover ratio 1.02 0.97

Fixed assets turnover ratio 1.49 1.06

Receivables or debtors turnover ratio

(in days) (Debtors * 365) / Credit sales

16

days

16

days

Creditors turnover ratio (in days) (Creditors * 365) / COGS

127

days

122

days

Interpretation : Efficiency ratio is used to evaluate that how a company is able to

manage its liability and assets to meet its obligation. It helps the company to measure its

receivable, payment cycle, liability repayment and how to use the equity to meet company

requirement. The inventory turnover ratio is decreasing in 2018 in compare to 2017 because of

the higher inventory level. Easyflight plc has to maintain the inventory level to minimize stock

turnover ratio. They can use the just in time method to control the inventory level.

The fixed asset turnover ratio of the company is 1.49 in 2017 and 1.06 in 2018 which

indicate that Easyflight plc efficiently use the fixed assets to generate the sales of the company.

The decreasing creditor turnover ratio indicate that company pay the debt on time and able to

generate the profit. The debtor turnover ratio is stable which implies that they efficiently collect

the debt from the debtors but they have to regularly monitor the debt collection period to

minimize the debt and increase cash level.

Efficiency ratio analysis

Particulars Calculation 2017 2018

Average Inventory 121 154

Turnover or sales revenue 4527 4686

Average total assets 4402 4802

Average fixed assets 3020 4399

Receivables or debtors 200 206

Creditors or payables 523 495

Cost of good sold 1496 1475

Stock turnover ratio (In times) 12.36 9.57

Total assets turnover ratio 1.02 0.97

Fixed assets turnover ratio 1.49 1.06

Receivables or debtors turnover ratio

(in days) (Debtors * 365) / Credit sales

16

days

16

days

Creditors turnover ratio (in days) (Creditors * 365) / COGS

127

days

122

days

Interpretation : Efficiency ratio is used to evaluate that how a company is able to

manage its liability and assets to meet its obligation. It helps the company to measure its

receivable, payment cycle, liability repayment and how to use the equity to meet company

requirement. The inventory turnover ratio is decreasing in 2018 in compare to 2017 because of

the higher inventory level. Easyflight plc has to maintain the inventory level to minimize stock

turnover ratio. They can use the just in time method to control the inventory level.

The fixed asset turnover ratio of the company is 1.49 in 2017 and 1.06 in 2018 which

indicate that Easyflight plc efficiently use the fixed assets to generate the sales of the company.

The decreasing creditor turnover ratio indicate that company pay the debt on time and able to

generate the profit. The debtor turnover ratio is stable which implies that they efficiently collect

the debt from the debtors but they have to regularly monitor the debt collection period to

minimize the debt and increase cash level.

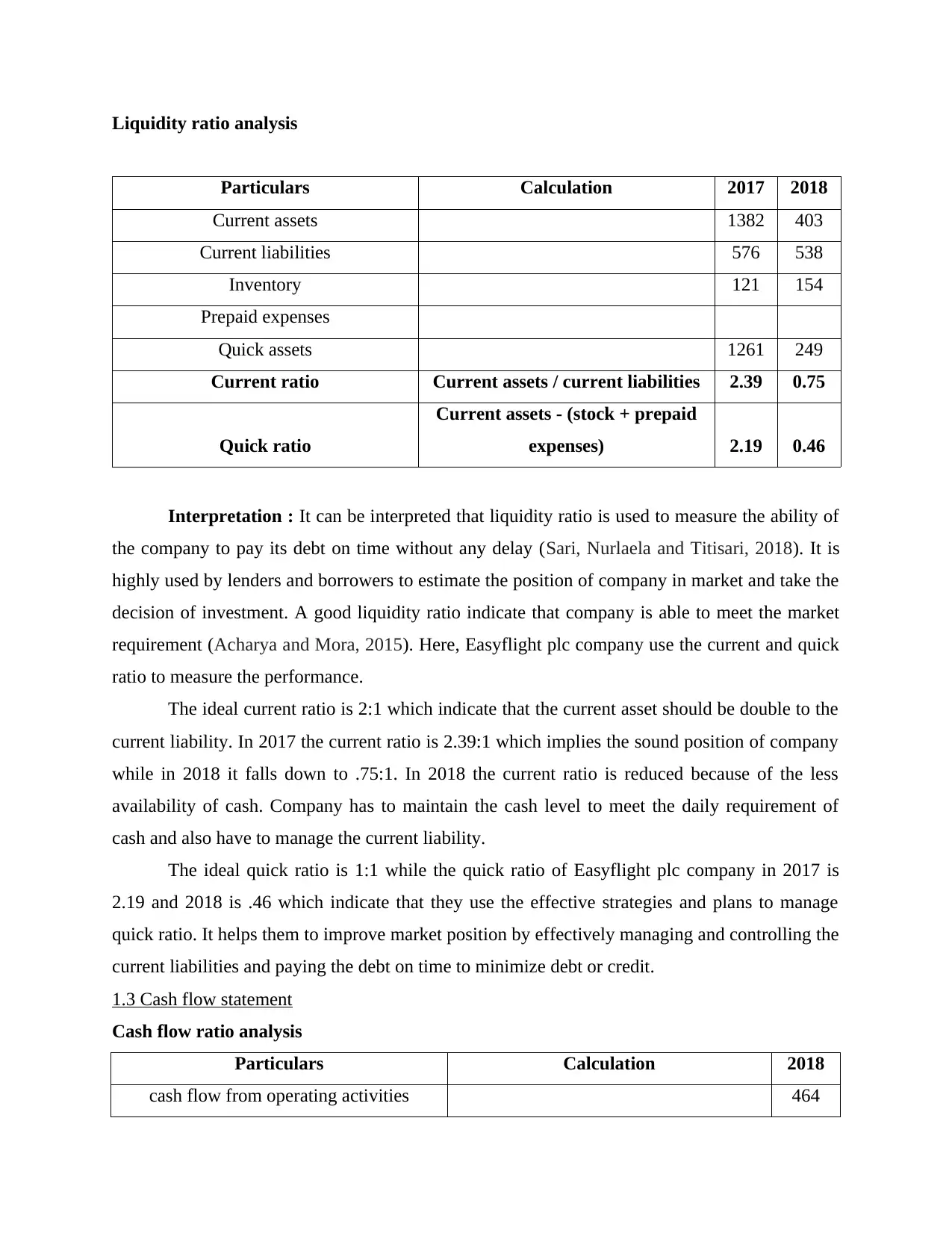

Liquidity ratio analysis

Particulars Calculation 2017 2018

Current assets 1382 403

Current liabilities 576 538

Inventory 121 154

Prepaid expenses

Quick assets 1261 249

Current ratio Current assets / current liabilities 2.39 0.75

Quick ratio

Current assets - (stock + prepaid

expenses) 2.19 0.46

Interpretation : It can be interpreted that liquidity ratio is used to measure the ability of

the company to pay its debt on time without any delay (Sari, Nurlaela and Titisari, 2018). It is

highly used by lenders and borrowers to estimate the position of company in market and take the

decision of investment. A good liquidity ratio indicate that company is able to meet the market

requirement (Acharya and Mora, 2015). Here, Easyflight plc company use the current and quick

ratio to measure the performance.

The ideal current ratio is 2:1 which indicate that the current asset should be double to the

current liability. In 2017 the current ratio is 2.39:1 which implies the sound position of company

while in 2018 it falls down to .75:1. In 2018 the current ratio is reduced because of the less

availability of cash. Company has to maintain the cash level to meet the daily requirement of

cash and also have to manage the current liability.

The ideal quick ratio is 1:1 while the quick ratio of Easyflight plc company in 2017 is

2.19 and 2018 is .46 which indicate that they use the effective strategies and plans to manage

quick ratio. It helps them to improve market position by effectively managing and controlling the

current liabilities and paying the debt on time to minimize debt or credit.

1.3 Cash flow statement

Cash flow ratio analysis

Particulars Calculation 2018

cash flow from operating activities 464

Particulars Calculation 2017 2018

Current assets 1382 403

Current liabilities 576 538

Inventory 121 154

Prepaid expenses

Quick assets 1261 249

Current ratio Current assets / current liabilities 2.39 0.75

Quick ratio

Current assets - (stock + prepaid

expenses) 2.19 0.46

Interpretation : It can be interpreted that liquidity ratio is used to measure the ability of

the company to pay its debt on time without any delay (Sari, Nurlaela and Titisari, 2018). It is

highly used by lenders and borrowers to estimate the position of company in market and take the

decision of investment. A good liquidity ratio indicate that company is able to meet the market

requirement (Acharya and Mora, 2015). Here, Easyflight plc company use the current and quick

ratio to measure the performance.

The ideal current ratio is 2:1 which indicate that the current asset should be double to the

current liability. In 2017 the current ratio is 2.39:1 which implies the sound position of company

while in 2018 it falls down to .75:1. In 2018 the current ratio is reduced because of the less

availability of cash. Company has to maintain the cash level to meet the daily requirement of

cash and also have to manage the current liability.

The ideal quick ratio is 1:1 while the quick ratio of Easyflight plc company in 2017 is

2.19 and 2018 is .46 which indicate that they use the effective strategies and plans to manage

quick ratio. It helps them to improve market position by effectively managing and controlling the

current liabilities and paying the debt on time to minimize debt or credit.

1.3 Cash flow statement

Cash flow ratio analysis

Particulars Calculation 2018

cash flow from operating activities 464

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

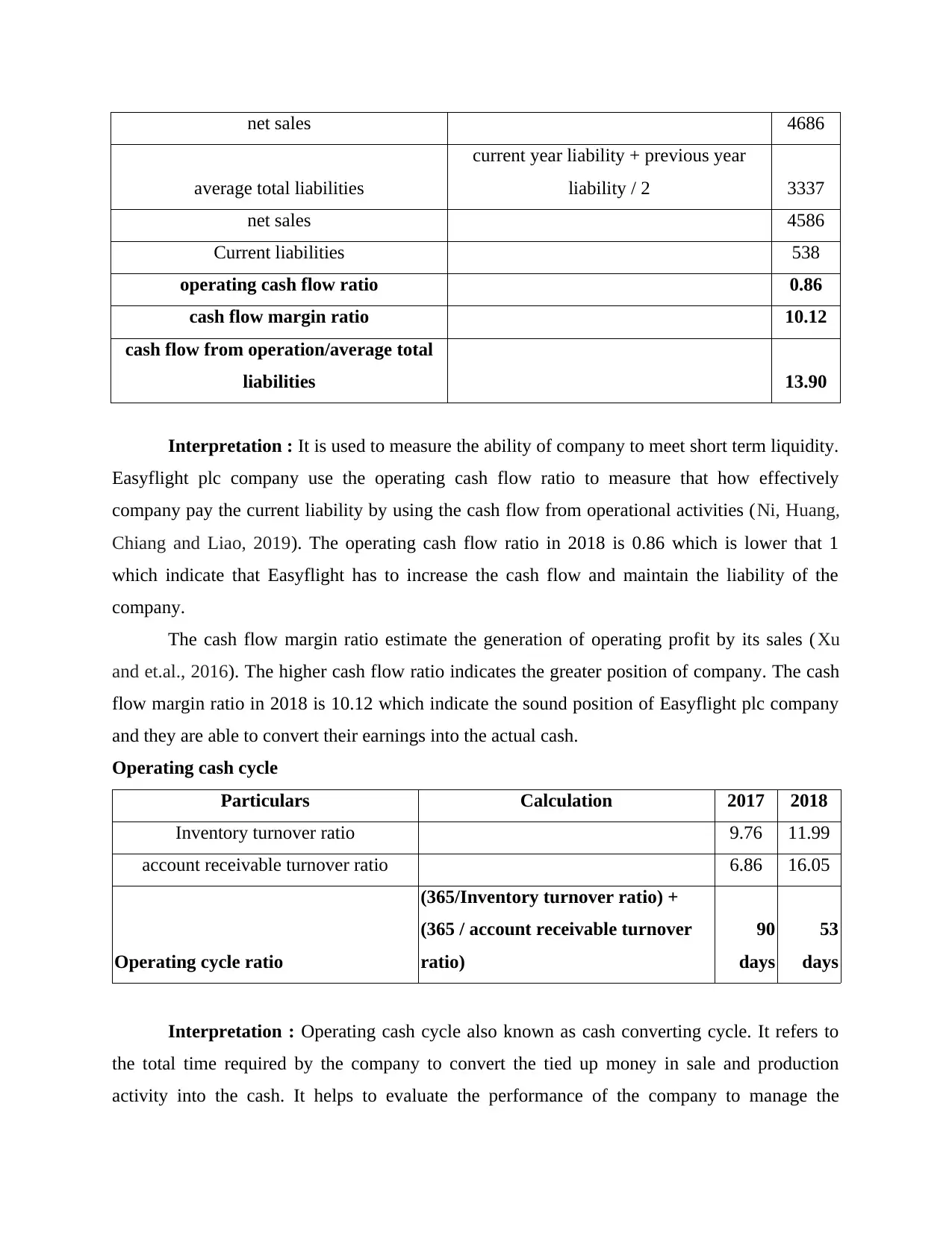

net sales 4686

average total liabilities

current year liability + previous year

liability / 2 3337

net sales 4586

Current liabilities 538

operating cash flow ratio 0.86

cash flow margin ratio 10.12

cash flow from operation/average total

liabilities 13.90

Interpretation : It is used to measure the ability of company to meet short term liquidity.

Easyflight plc company use the operating cash flow ratio to measure that how effectively

company pay the current liability by using the cash flow from operational activities (Ni, Huang,

Chiang and Liao, 2019). The operating cash flow ratio in 2018 is 0.86 which is lower that 1

which indicate that Easyflight has to increase the cash flow and maintain the liability of the

company.

The cash flow margin ratio estimate the generation of operating profit by its sales ( Xu

and et.al., 2016). The higher cash flow ratio indicates the greater position of company. The cash

flow margin ratio in 2018 is 10.12 which indicate the sound position of Easyflight plc company

and they are able to convert their earnings into the actual cash.

Operating cash cycle

Particulars Calculation 2017 2018

Inventory turnover ratio 9.76 11.99

account receivable turnover ratio 6.86 16.05

Operating cycle ratio

(365/Inventory turnover ratio) +

(365 / account receivable turnover

ratio)

90

days

53

days

Interpretation : Operating cash cycle also known as cash converting cycle. It refers to

the total time required by the company to convert the tied up money in sale and production

activity into the cash. It helps to evaluate the performance of the company to manage the

average total liabilities

current year liability + previous year

liability / 2 3337

net sales 4586

Current liabilities 538

operating cash flow ratio 0.86

cash flow margin ratio 10.12

cash flow from operation/average total

liabilities 13.90

Interpretation : It is used to measure the ability of company to meet short term liquidity.

Easyflight plc company use the operating cash flow ratio to measure that how effectively

company pay the current liability by using the cash flow from operational activities (Ni, Huang,

Chiang and Liao, 2019). The operating cash flow ratio in 2018 is 0.86 which is lower that 1

which indicate that Easyflight has to increase the cash flow and maintain the liability of the

company.

The cash flow margin ratio estimate the generation of operating profit by its sales ( Xu

and et.al., 2016). The higher cash flow ratio indicates the greater position of company. The cash

flow margin ratio in 2018 is 10.12 which indicate the sound position of Easyflight plc company

and they are able to convert their earnings into the actual cash.

Operating cash cycle

Particulars Calculation 2017 2018

Inventory turnover ratio 9.76 11.99

account receivable turnover ratio 6.86 16.05

Operating cycle ratio

(365/Inventory turnover ratio) +

(365 / account receivable turnover

ratio)

90

days

53

days

Interpretation : Operating cash cycle also known as cash converting cycle. It refers to

the total time required by the company to convert the tied up money in sale and production

activity into the cash. It helps to evaluate the performance of the company to manage the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

operation activity (What's the Difference Between Operating Cycle and Cash Cycle?, 2019). The

operating cash cycle of Easyflight plc company is 90 days in 2017 and 53 days in 2018. The

reducing operating cycle of the company indicate that they introduce new policy and strategies to

minimize the period of conversion of cash. It also explains that the current policy of the company

is beneficial and help them to convert the tied amount in sales and production activity into cash.

Dividend policy refers to take the decision of paying the dividend to the stakeholders out

of the generated profit (Labhane and Mahakud, 2016). In 2017 Easyflight plc pay £100 million

dividend to the shareholder's out of the £443 million profit which was 22.57% of actual profit. In

2018 company generate higher profit in compare to the last year and pay 23.10% dividend to the

shareholder's. The decision of Easyflight company to pay dividend to its shareholder's is correct

because it helps them to motivate shareholder's to invest in Easyflight plc capital. Company

increase the dividend ratio in compare to the last year to satisfy the customer with their decisions

and encourage them to invest more to get more profit and share in the company financial

position.

1.4 Market segment analysis

Easyflight operate its business in different country like England, France, Scotland etc. In

England it generates £2181 million profit in compare to the France business but the cost of sale

is also high. They have to maintain the cost of sale to improve the gross profit. They can use

skimming pricing strategy to maintain the cost of sale by setting higher price at initial period and

then decrease the price as per the market requirement (How to price your product: 5 common

strategies, 2019). The gross profit of France in 2018 is £78 million but the cost of sale is also

low which indicate that they are able to manage the cost of sale. They have to use the penetration

and competitive pricing strategies to generate higher profit. Penetration pricing strategy help

them increase the price to generate higher profit and competitive pricing strategy help them to

increase the price of the product and services by analysing the competitors' performance in the

market. Easyflight Scotland is able to manage the cost of sales and generate £952 million gross

profit in 2018. They have to use the value based and penetration pricing strategies to generate

higher profit.

The operating cost of Easyflight England is £1803 million which is quite higher in

compare to the other country performance and the profit margin is also low. While the other

country like Scotland and France profit margin is high because they are effectively controlled the

operating cash cycle of Easyflight plc company is 90 days in 2017 and 53 days in 2018. The

reducing operating cycle of the company indicate that they introduce new policy and strategies to

minimize the period of conversion of cash. It also explains that the current policy of the company

is beneficial and help them to convert the tied amount in sales and production activity into cash.

Dividend policy refers to take the decision of paying the dividend to the stakeholders out

of the generated profit (Labhane and Mahakud, 2016). In 2017 Easyflight plc pay £100 million

dividend to the shareholder's out of the £443 million profit which was 22.57% of actual profit. In

2018 company generate higher profit in compare to the last year and pay 23.10% dividend to the

shareholder's. The decision of Easyflight company to pay dividend to its shareholder's is correct

because it helps them to motivate shareholder's to invest in Easyflight plc capital. Company

increase the dividend ratio in compare to the last year to satisfy the customer with their decisions

and encourage them to invest more to get more profit and share in the company financial

position.

1.4 Market segment analysis

Easyflight operate its business in different country like England, France, Scotland etc. In

England it generates £2181 million profit in compare to the France business but the cost of sale

is also high. They have to maintain the cost of sale to improve the gross profit. They can use

skimming pricing strategy to maintain the cost of sale by setting higher price at initial period and

then decrease the price as per the market requirement (How to price your product: 5 common

strategies, 2019). The gross profit of France in 2018 is £78 million but the cost of sale is also

low which indicate that they are able to manage the cost of sale. They have to use the penetration

and competitive pricing strategies to generate higher profit. Penetration pricing strategy help

them increase the price to generate higher profit and competitive pricing strategy help them to

increase the price of the product and services by analysing the competitors' performance in the

market. Easyflight Scotland is able to manage the cost of sales and generate £952 million gross

profit in 2018. They have to use the value based and penetration pricing strategies to generate

higher profit.

The operating cost of Easyflight England is £1803 million which is quite higher in

compare to the other country performance and the profit margin is also low. While the other

country like Scotland and France profit margin is high because they are effectively controlled the

cost of sales and operating cost. England has to control the operating cost by regulating cost on

time and use the budgetary control tool to manage the cost. They also have to focus on the

unnecessary advertising and promotional techniques to minimize their operating cost. It helps

them to control the activities and monitor the performance in market to establish their business

more effectively and increase the market share by expanding airport retail business.

PART-2

2.1.a Management forecast

Managers of Easylight Plc has made forecasting by applying the investment appraisal

tools in respect of the revenue, costs and contribution that will be ascertained over the life of the

project. The forecast table shows that the amount of the revenue and contribution will be

increasing from one period to another with proper management of the variable cost. This reflects

that the project is viable and will attain profits in the future period. This expansion project that

has been started by an enterprise into France will be counted as viable and desirable for the

organization.

2.1.b Investment appraisal tools

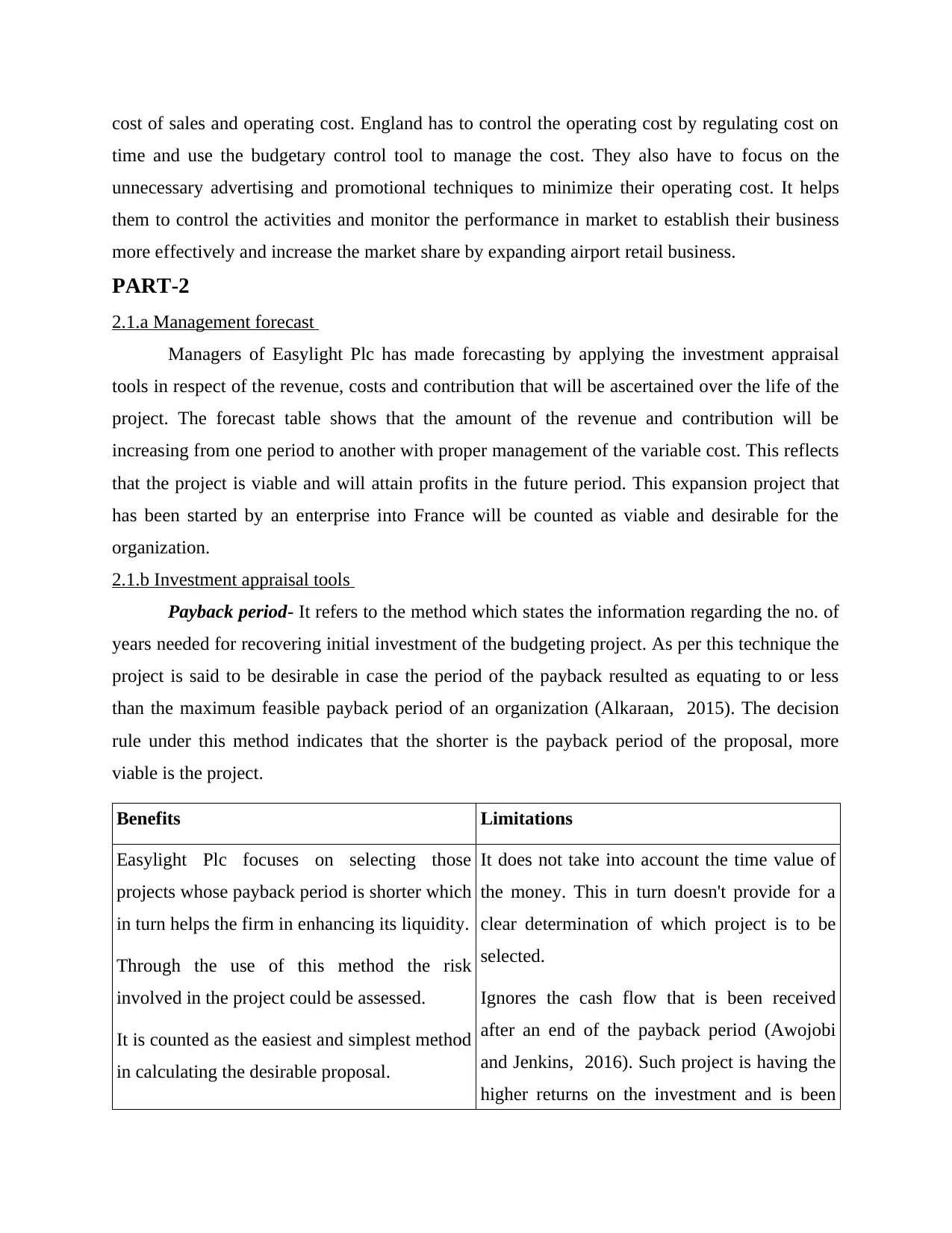

Payback period- It refers to the method which states the information regarding the no. of

years needed for recovering initial investment of the budgeting project. As per this technique the

project is said to be desirable in case the period of the payback resulted as equating to or less

than the maximum feasible payback period of an organization (Alkaraan, 2015). The decision

rule under this method indicates that the shorter is the payback period of the proposal, more

viable is the project.

Benefits Limitations

Easylight Plc focuses on selecting those

projects whose payback period is shorter which

in turn helps the firm in enhancing its liquidity.

Through the use of this method the risk

involved in the project could be assessed.

It is counted as the easiest and simplest method

in calculating the desirable proposal.

It does not take into account the time value of

the money. This in turn doesn't provide for a

clear determination of which project is to be

selected.

Ignores the cash flow that is been received

after an end of the payback period (Awojobi

and Jenkins, 2016). Such project is having the

higher returns on the investment and is been

time and use the budgetary control tool to manage the cost. They also have to focus on the

unnecessary advertising and promotional techniques to minimize their operating cost. It helps

them to control the activities and monitor the performance in market to establish their business

more effectively and increase the market share by expanding airport retail business.

PART-2

2.1.a Management forecast

Managers of Easylight Plc has made forecasting by applying the investment appraisal

tools in respect of the revenue, costs and contribution that will be ascertained over the life of the

project. The forecast table shows that the amount of the revenue and contribution will be

increasing from one period to another with proper management of the variable cost. This reflects

that the project is viable and will attain profits in the future period. This expansion project that

has been started by an enterprise into France will be counted as viable and desirable for the

organization.

2.1.b Investment appraisal tools

Payback period- It refers to the method which states the information regarding the no. of

years needed for recovering initial investment of the budgeting project. As per this technique the

project is said to be desirable in case the period of the payback resulted as equating to or less

than the maximum feasible payback period of an organization (Alkaraan, 2015). The decision

rule under this method indicates that the shorter is the payback period of the proposal, more

viable is the project.

Benefits Limitations

Easylight Plc focuses on selecting those

projects whose payback period is shorter which

in turn helps the firm in enhancing its liquidity.

Through the use of this method the risk

involved in the project could be assessed.

It is counted as the easiest and simplest method

in calculating the desirable proposal.

It does not take into account the time value of

the money. This in turn doesn't provide for a

clear determination of which project is to be

selected.

Ignores the cash flow that is been received

after an end of the payback period (Awojobi

and Jenkins, 2016). Such project is having the

higher returns on the investment and is been

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

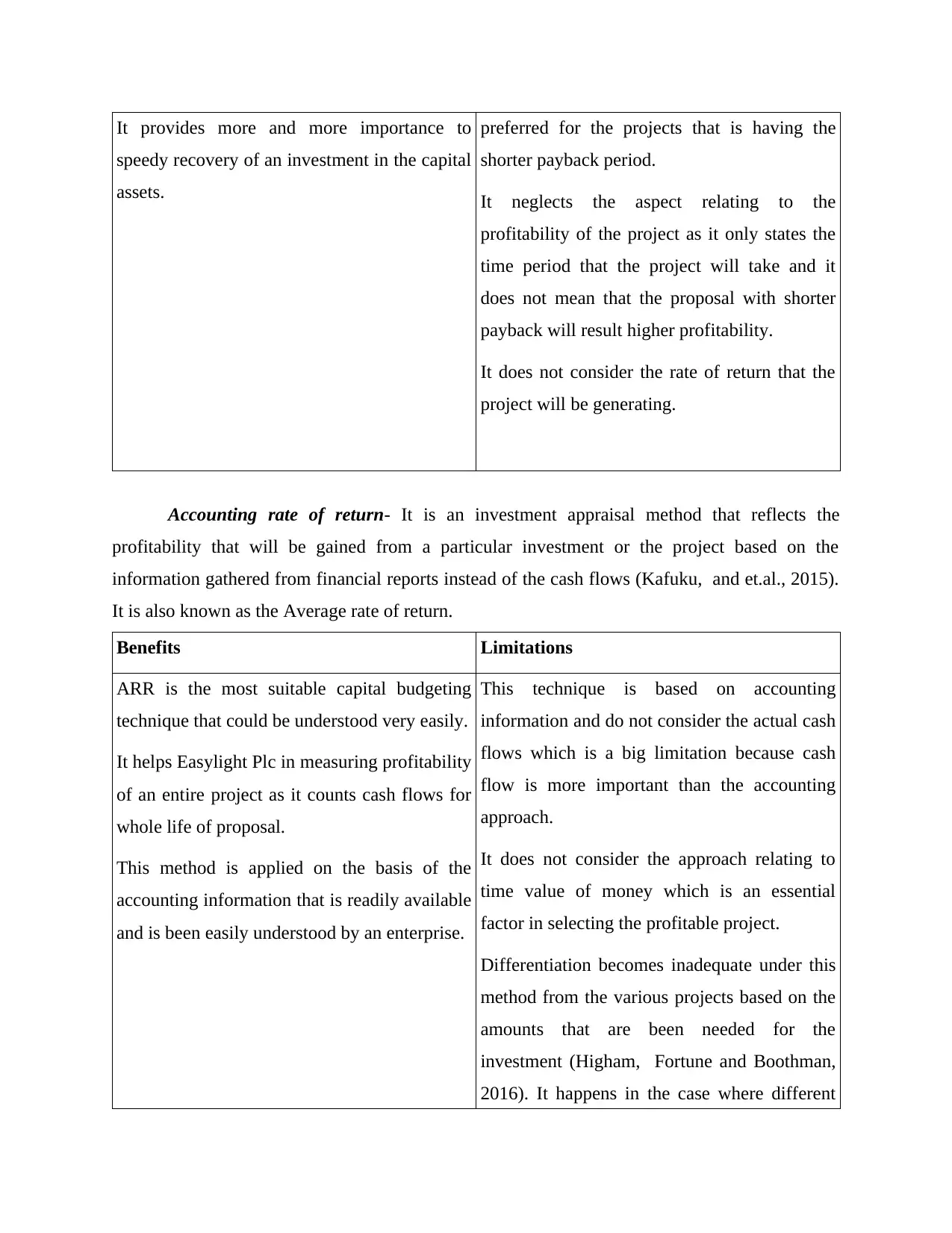

It provides more and more importance to

speedy recovery of an investment in the capital

assets.

preferred for the projects that is having the

shorter payback period.

It neglects the aspect relating to the

profitability of the project as it only states the

time period that the project will take and it

does not mean that the proposal with shorter

payback will result higher profitability.

It does not consider the rate of return that the

project will be generating.

Accounting rate of return- It is an investment appraisal method that reflects the

profitability that will be gained from a particular investment or the project based on the

information gathered from financial reports instead of the cash flows (Kafuku, and et.al., 2015).

It is also known as the Average rate of return.

Benefits Limitations

ARR is the most suitable capital budgeting

technique that could be understood very easily.

It helps Easylight Plc in measuring profitability

of an entire project as it counts cash flows for

whole life of proposal.

This method is applied on the basis of the

accounting information that is readily available

and is been easily understood by an enterprise.

This technique is based on accounting

information and do not consider the actual cash

flows which is a big limitation because cash

flow is more important than the accounting

approach.

It does not consider the approach relating to

time value of money which is an essential

factor in selecting the profitable project.

Differentiation becomes inadequate under this

method from the various projects based on the

amounts that are been needed for the

investment (Higham, Fortune and Boothman,

2016). It happens in the case where different

speedy recovery of an investment in the capital

assets.

preferred for the projects that is having the

shorter payback period.

It neglects the aspect relating to the

profitability of the project as it only states the

time period that the project will take and it

does not mean that the proposal with shorter

payback will result higher profitability.

It does not consider the rate of return that the

project will be generating.

Accounting rate of return- It is an investment appraisal method that reflects the

profitability that will be gained from a particular investment or the project based on the

information gathered from financial reports instead of the cash flows (Kafuku, and et.al., 2015).

It is also known as the Average rate of return.

Benefits Limitations

ARR is the most suitable capital budgeting

technique that could be understood very easily.

It helps Easylight Plc in measuring profitability

of an entire project as it counts cash flows for

whole life of proposal.

This method is applied on the basis of the

accounting information that is readily available

and is been easily understood by an enterprise.

This technique is based on accounting

information and do not consider the actual cash

flows which is a big limitation because cash

flow is more important than the accounting

approach.

It does not consider the approach relating to

time value of money which is an essential

factor in selecting the profitable project.

Differentiation becomes inadequate under this

method from the various projects based on the

amounts that are been needed for the

investment (Higham, Fortune and Boothman,

2016). It happens in the case where different

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

proposals are resulting the same ARR.

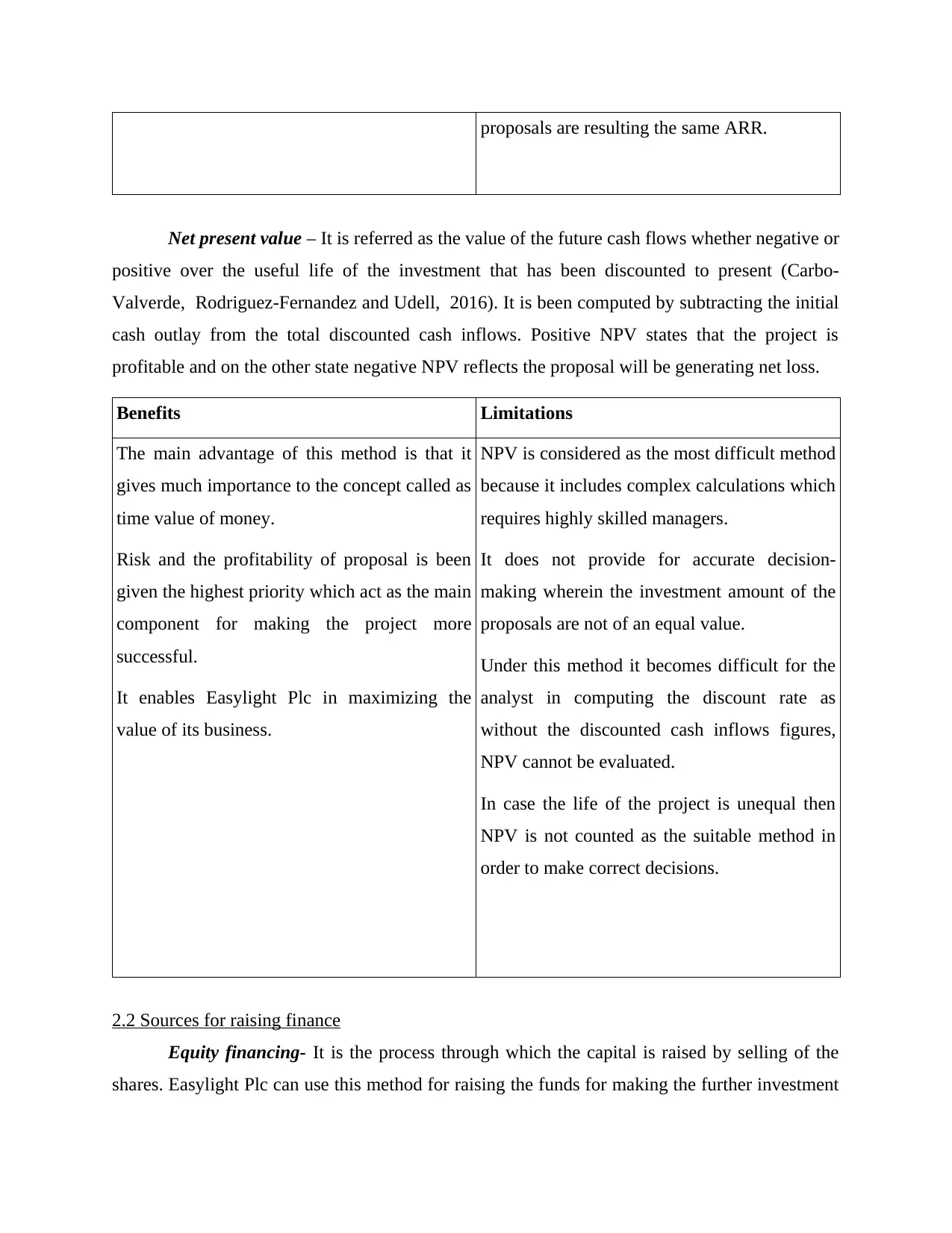

Net present value – It is referred as the value of the future cash flows whether negative or

positive over the useful life of the investment that has been discounted to present (Carbo‐

Valverde, Rodriguez‐Fernandez and Udell, 2016). It is been computed by subtracting the initial

cash outlay from the total discounted cash inflows. Positive NPV states that the project is

profitable and on the other state negative NPV reflects the proposal will be generating net loss.

Benefits Limitations

The main advantage of this method is that it

gives much importance to the concept called as

time value of money.

Risk and the profitability of proposal is been

given the highest priority which act as the main

component for making the project more

successful.

It enables Easylight Plc in maximizing the

value of its business.

NPV is considered as the most difficult method

because it includes complex calculations which

requires highly skilled managers.

It does not provide for accurate decision-

making wherein the investment amount of the

proposals are not of an equal value.

Under this method it becomes difficult for the

analyst in computing the discount rate as

without the discounted cash inflows figures,

NPV cannot be evaluated.

In case the life of the project is unequal then

NPV is not counted as the suitable method in

order to make correct decisions.

2.2 Sources for raising finance

Equity financing- It is the process through which the capital is raised by selling of the

shares. Easylight Plc can use this method for raising the funds for making the further investment

Net present value – It is referred as the value of the future cash flows whether negative or

positive over the useful life of the investment that has been discounted to present (Carbo‐

Valverde, Rodriguez‐Fernandez and Udell, 2016). It is been computed by subtracting the initial

cash outlay from the total discounted cash inflows. Positive NPV states that the project is

profitable and on the other state negative NPV reflects the proposal will be generating net loss.

Benefits Limitations

The main advantage of this method is that it

gives much importance to the concept called as

time value of money.

Risk and the profitability of proposal is been

given the highest priority which act as the main

component for making the project more

successful.

It enables Easylight Plc in maximizing the

value of its business.

NPV is considered as the most difficult method

because it includes complex calculations which

requires highly skilled managers.

It does not provide for accurate decision-

making wherein the investment amount of the

proposals are not of an equal value.

Under this method it becomes difficult for the

analyst in computing the discount rate as

without the discounted cash inflows figures,

NPV cannot be evaluated.

In case the life of the project is unequal then

NPV is not counted as the suitable method in

order to make correct decisions.

2.2 Sources for raising finance

Equity financing- It is the process through which the capital is raised by selling of the

shares. Easylight Plc can use this method for raising the funds for making the further investment

in the retail business within the airport line (Balaban, Župljanin and Ivanović, 2016). An

organization by raising the money through equity financing might having the short term needs in

paying the bills and may have the long term goals in order to achieve growing success with high

growth.

Advantages Disadvantages

This source helps the firm in eliminating the

cost relating to overhead as it does not include

the payment of the interest. Thus, does not

result in creating any kind of the financial

burdens.

Equity financing helps the organization in

shaping their partnership and also the large

enterprise with more and more skilled and the

experienced people.

In case of no profits, the company doesn't have

any obligation in relation to distributing the

dividend to its shareholders.

Profits that are been earned by the firm is to be

distributed or shared with institutions and the

shareholders in proportion of their holding.

The control of the ownership also required to

be shared which in turn results in the dilution

of the control and the power of decision-

making.

Equity financing is counted as the tedious

method of raising the funds as it needs a huge

number of legal compliance and has to follow

all the statutory laws for the raising the money

by sales of the shares.

Sharing of the ownership might creates clashes

in ideas, administration style, growth and the

business operations (Fraser, Bhaumik and

Wright, 2015). This is considered as the big

issue and can leave an entity in frustration if

they do not look over disadvantages.

Bank loan- It is the kind of financing that refers to the most suitable method of raising

the finance for the business. It facilitates for both medium and the long term finance. It is good

for the purpose of financing for making the investment in fixed assets like plant, machinery and

equipment etc.

Advantages Disadvantages

organization by raising the money through equity financing might having the short term needs in

paying the bills and may have the long term goals in order to achieve growing success with high

growth.

Advantages Disadvantages

This source helps the firm in eliminating the

cost relating to overhead as it does not include

the payment of the interest. Thus, does not

result in creating any kind of the financial

burdens.

Equity financing helps the organization in

shaping their partnership and also the large

enterprise with more and more skilled and the

experienced people.

In case of no profits, the company doesn't have

any obligation in relation to distributing the

dividend to its shareholders.

Profits that are been earned by the firm is to be

distributed or shared with institutions and the

shareholders in proportion of their holding.

The control of the ownership also required to

be shared which in turn results in the dilution

of the control and the power of decision-

making.

Equity financing is counted as the tedious

method of raising the funds as it needs a huge

number of legal compliance and has to follow

all the statutory laws for the raising the money

by sales of the shares.

Sharing of the ownership might creates clashes

in ideas, administration style, growth and the

business operations (Fraser, Bhaumik and

Wright, 2015). This is considered as the big

issue and can leave an entity in frustration if

they do not look over disadvantages.

Bank loan- It is the kind of financing that refers to the most suitable method of raising

the finance for the business. It facilitates for both medium and the long term finance. It is good

for the purpose of financing for making the investment in fixed assets like plant, machinery and

equipment etc.

Advantages Disadvantages

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.