Financial Decision Making Report: Accounting & Finance Analysis

VerifiedAdded on 2021/02/20

|11

|3735

|22

Report

AI Summary

This report delves into the realm of financial decision-making, examining its significance for organizational success and sustainable growth. It explores the core aspects of financial decision-making, including fund procurement, resource identification, and efficient fund utilization. The report investigates the roles of accounting and finance in decision-making and reporting, particularly in the context of Devanet UK Ltd, a manufacturer of belts and leather goods, and Alpha Ltd. It evaluates the application of management accounting techniques, such as financial statement analysis, budgetary control, financial planning, and standard costing, within Devanet. Furthermore, the report presents a comprehensive analysis of financial ratios, including Return on Capital Employed (ROCE), net profit margin, current ratio, debtor collection period, and creditor collection period, to assess company performance. The interpretation of these ratios provides insights into the financial health and efficiency of Alpha Ltd, highlighting trends and areas for improvement. The report concludes by emphasizing the critical role of accounting and finance in supporting managerial activities, ensuring effective planning, control, and decision-making within a business context.

Financial

Decision Making

Decision Making

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

Evaluation of the role of accounting and finance:.......................................................................3

Critical Analysis:.........................................................................................................................6

TASK 2............................................................................................................................................6

Calculation of the ratios to analyse company performance:........................................................6

Interpretation and analysis of financial ratios:.............................................................................7

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

Evaluation of the role of accounting and finance:.......................................................................3

Critical Analysis:.........................................................................................................................6

TASK 2............................................................................................................................................6

Calculation of the ratios to analyse company performance:........................................................6

Interpretation and analysis of financial ratios:.............................................................................7

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION

Decision-making which mainly concerned with financial aspects of business enterprises

is generally termed as financial decision making. It is core factor of organisation's success and

sustainable growth. It majorly cover procurement of funds, identification of key fiscal resources

and ultimately efficient use of funds. The whole process of fiscal decision-making is carried out

out by owners and managing personnels. Financial decision-making is focused on accessible

economic and fiscal data on results and performance of corporation. This process draws on

estimate analyses, investment alternatives, as well as number of fiscal reports including cash-

flow statements, income statements, and statements of profit and loss (Carvalho, Meier and

Wang, 2016).

In this context the study covers discussion on basic structure and terms concerned with

financial statement, usage of techniques of managerial accounting in organisational planning,

controls and decision-making functions in Devanet UK Ltd, an UK based manufacturer of Belts ,

Buckles, Quality Leather goods. Furthermore the study contain assessment of ratios, its

relevance of users and, role and significance of accounting and finance in decision-making and

reporting of accounts in relation to Alpha Ltd.

TASK 1

Evaluation of the role of accounting and finance:

Overview of company: Company Devnanet is providing exclusive range of customised products

produced in factory which is situated at Cheshire. Company engaged in manufacturing of belt

buckle, bag buckle, shoe buckle, clothing buckle, metal components, complimented by complete

range of pan-tone well-matched leather and also with printed webbing. Company's other

supporting activities includes Cad drawings, CNC milling, Casting in brass, pewter, bronze,

silver and gold. Customised and quality products are core reason for company's increasing

popularity. This extensive and devoted service is special to company's clients with matching

quality, which is considered by some other of well-known brands in world. Devanét and it's

partners are continuously improving company's product variety and reach so that clients can

create fresh markets (About Devanet. 2019). Company also provides 3D scan printing services,

edge belt stitching, rotary engraving, leather embossing, sublimation printing etc.

Decision-making which mainly concerned with financial aspects of business enterprises

is generally termed as financial decision making. It is core factor of organisation's success and

sustainable growth. It majorly cover procurement of funds, identification of key fiscal resources

and ultimately efficient use of funds. The whole process of fiscal decision-making is carried out

out by owners and managing personnels. Financial decision-making is focused on accessible

economic and fiscal data on results and performance of corporation. This process draws on

estimate analyses, investment alternatives, as well as number of fiscal reports including cash-

flow statements, income statements, and statements of profit and loss (Carvalho, Meier and

Wang, 2016).

In this context the study covers discussion on basic structure and terms concerned with

financial statement, usage of techniques of managerial accounting in organisational planning,

controls and decision-making functions in Devanet UK Ltd, an UK based manufacturer of Belts ,

Buckles, Quality Leather goods. Furthermore the study contain assessment of ratios, its

relevance of users and, role and significance of accounting and finance in decision-making and

reporting of accounts in relation to Alpha Ltd.

TASK 1

Evaluation of the role of accounting and finance:

Overview of company: Company Devnanet is providing exclusive range of customised products

produced in factory which is situated at Cheshire. Company engaged in manufacturing of belt

buckle, bag buckle, shoe buckle, clothing buckle, metal components, complimented by complete

range of pan-tone well-matched leather and also with printed webbing. Company's other

supporting activities includes Cad drawings, CNC milling, Casting in brass, pewter, bronze,

silver and gold. Customised and quality products are core reason for company's increasing

popularity. This extensive and devoted service is special to company's clients with matching

quality, which is considered by some other of well-known brands in world. Devanét and it's

partners are continuously improving company's product variety and reach so that clients can

create fresh markets (About Devanet. 2019). Company also provides 3D scan printing services,

edge belt stitching, rotary engraving, leather embossing, sublimation printing etc.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Role of management accounting techniques:

Management accounting is structured internal process which covers all financial and non-

financial tasks to generate informations for corporation that assist in take decisions. In current

scenario complexities are increasing day by day, so need of adoption of processes and techniques

of management accounting is increasing rapidly. Complexities in business can lead to decline in

business fiscal results and performance. It is duty of management team to implement structure

according to requirements of management techniques. Further different strategies and

operational frameworks are developed and designed according to outcomes of various

techniques. Management's operations are dedicated towards effective implementation of

management accounting structure as it help in managing and funding resources as per business

requirements with aim to achieve cost effectiveness. Managing different organisational activities

is tuff task for managers so they always tries to integrate these activities with different

management accounting techniques (Epstein, Buhovac and Yuthas, 2015). In Devanét company,

management team have adopted management accounting framework and techniques to resolve

difficult problems within corporation. In this regard following are techniques of managerial

accounting and their role in corporation's controlling, planning and decision-making tasks, as

follows:

Analysing financial statements: This is most core technique which help to define

existing business position and performance of corporation within industry. Every

company conduct a thorough analysis of it's financial reports and statements which also

help them to find out any new change or alternation in corporation's strategies and

policies. In company Devanét this analysis is primarily undertaken by managing teams

on periodical basis. They review business's prime financial statements, reports and

accounting process involved in preparation of such reports within context of use and

relevancy of accounting standards and other fundamental assumptions. In process of

analysis of balance-sheet's items and accounts, consideration of factors like identification,

evaluation and categorization are important (Graham, Harvey and Puri, 2015). The

analysis facilitates identification of factors and potential issues which may affect

company's planning process and decision-making structure. Further it also help to

improve controlling over fiscal and monetary operations by identifying any loopholes in

these operations.

Management accounting is structured internal process which covers all financial and non-

financial tasks to generate informations for corporation that assist in take decisions. In current

scenario complexities are increasing day by day, so need of adoption of processes and techniques

of management accounting is increasing rapidly. Complexities in business can lead to decline in

business fiscal results and performance. It is duty of management team to implement structure

according to requirements of management techniques. Further different strategies and

operational frameworks are developed and designed according to outcomes of various

techniques. Management's operations are dedicated towards effective implementation of

management accounting structure as it help in managing and funding resources as per business

requirements with aim to achieve cost effectiveness. Managing different organisational activities

is tuff task for managers so they always tries to integrate these activities with different

management accounting techniques (Epstein, Buhovac and Yuthas, 2015). In Devanét company,

management team have adopted management accounting framework and techniques to resolve

difficult problems within corporation. In this regard following are techniques of managerial

accounting and their role in corporation's controlling, planning and decision-making tasks, as

follows:

Analysing financial statements: This is most core technique which help to define

existing business position and performance of corporation within industry. Every

company conduct a thorough analysis of it's financial reports and statements which also

help them to find out any new change or alternation in corporation's strategies and

policies. In company Devanét this analysis is primarily undertaken by managing teams

on periodical basis. They review business's prime financial statements, reports and

accounting process involved in preparation of such reports within context of use and

relevancy of accounting standards and other fundamental assumptions. In process of

analysis of balance-sheet's items and accounts, consideration of factors like identification,

evaluation and categorization are important (Graham, Harvey and Puri, 2015). The

analysis facilitates identification of factors and potential issues which may affect

company's planning process and decision-making structure. Further it also help to

improve controlling over fiscal and monetary operations by identifying any loopholes in

these operations.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Budgetary Control: It is major aspect and technique of management accounting. It is

method of monitoring budgets of an corporation by periodically comparing fiscal data of

how much funds it spends, earns and requires, and afterwards, if required, changing to

budget. It is a method of creating departmental budgets pertaining executive duties to the

demands of policies and the ongoing comparison of present outcomes with planned

outcomes, either to ensure the goals of that strategy by collective action or to give a

strong base for its modification. The main aim of budgetary control is to assist managers

in comprehensive scheduling and regulating the company's activities. In Devanét,

managing officials has implemented budgetary control techniques to monitor and control

movement of funds and making plan for effective use of different sources' funds. For

long term funding decision and capital budgeting this also help company's managers to

frame and implement decisions.

Financial Planning: Financial planning is task of ascertaining how well a corporation

can attain its tactical targets and objectives. A corporation typically helps to create a

Fiscal Blueprint promptly after unique vision and goals are set. The Fiscal Plan outlines

each operations, assets, materials and equipment required to reach these goals, and within

timelines determined. The enterprise financial planning mechanism is intended to

predicting future fiscal outcomes and ascertain how effectively to use economic and

fiscal resources of the corporation in pursuit of short and long-term targets of

organization. Since planning consists searching into future excellently, it is both a

incredibly creative and technical thought process (Hernes and Sobieska-Karpińska,

2016). In Devanét, financial planner and other key personnels conduct tasks of financial

planning to effectively plan and control all major fiscal and monetary tasks and arrange

them as per corporation's goals and pre determined targets.

Standard Costing: Standard costing is a procedure that utilizes expenditure and income

standards via variation assessment for monitoring purposes. Standards are predefined

quantifiable values set under specified circumstances that could be compared with actual

results, generally for a job, procedure or activities component. Its primary aim is to

provide foundation for monitoring by means of variation accounting for inventory and

work-in-progress measurement and, in several instances, sale price fixation. Standard

costing includes establishing predefined estimated costs to have a foundation for

method of monitoring budgets of an corporation by periodically comparing fiscal data of

how much funds it spends, earns and requires, and afterwards, if required, changing to

budget. It is a method of creating departmental budgets pertaining executive duties to the

demands of policies and the ongoing comparison of present outcomes with planned

outcomes, either to ensure the goals of that strategy by collective action or to give a

strong base for its modification. The main aim of budgetary control is to assist managers

in comprehensive scheduling and regulating the company's activities. In Devanét,

managing officials has implemented budgetary control techniques to monitor and control

movement of funds and making plan for effective use of different sources' funds. For

long term funding decision and capital budgeting this also help company's managers to

frame and implement decisions.

Financial Planning: Financial planning is task of ascertaining how well a corporation

can attain its tactical targets and objectives. A corporation typically helps to create a

Fiscal Blueprint promptly after unique vision and goals are set. The Fiscal Plan outlines

each operations, assets, materials and equipment required to reach these goals, and within

timelines determined. The enterprise financial planning mechanism is intended to

predicting future fiscal outcomes and ascertain how effectively to use economic and

fiscal resources of the corporation in pursuit of short and long-term targets of

organization. Since planning consists searching into future excellently, it is both a

incredibly creative and technical thought process (Hernes and Sobieska-Karpińska,

2016). In Devanét, financial planner and other key personnels conduct tasks of financial

planning to effectively plan and control all major fiscal and monetary tasks and arrange

them as per corporation's goals and pre determined targets.

Standard Costing: Standard costing is a procedure that utilizes expenditure and income

standards via variation assessment for monitoring purposes. Standards are predefined

quantifiable values set under specified circumstances that could be compared with actual

results, generally for a job, procedure or activities component. Its primary aim is to

provide foundation for monitoring by means of variation accounting for inventory and

work-in-progress measurement and, in several instances, sale price fixation. Standard

costing includes establishing predefined estimated costs to have a foundation for

comparing with actual expenses. Widely recognized as an efficient tool for controlling

costs in businesses is standard costing. The organisation accomplishes the goals in a

scheduled and structured way by applying standard costing. In this context, Devanét is

applying standard costing to asses their performance and fiscal outcomes as compare to

set standards which ultimately assist in developing control over whole organisational

functions and making plan for future performance (Jetter and Walker, 2017).

Critical Analysis:

Main aim of above discussed techniques is to support corporation's managerial activities

like controlling, decision-making and controlling. As standard costing helps to determine

effectiveness of plan and business decisions by assessment of actual performance in comparison

of standards determined. For effective plan and control related to financial tasks company can

rely on financial planning. Budgetary controls within organisation ensures proper and

appropriate control over all financial activities, effective decisions and appropriate planning.

Analysis and evaluation of financial statements also boost the reliability of controlling and

planning structure along with companies key decisions. Management accounting in organisation

like Devanét adopted to improve entire managing framework with aim to attain predefined

objectives and targets. Companies can apply combination of different methods to for overall

effectiveness in whole managerial and organisational structure (Kabir, Sadiq and Tesfamariam,

2014).

TASK 2

Calculation of the ratios to analyse company performance:

Ratios 2018 2017

ROCE or Return On Capital

Employed :

= (Operating Profit /Capital

Employed) *100

here, Capital Employed = Total

Assets – External liabilities.

= 412 / 2925 * 100

= 14.10%

= 375 / 1912.50 *100

= 19.60%

costs in businesses is standard costing. The organisation accomplishes the goals in a

scheduled and structured way by applying standard costing. In this context, Devanét is

applying standard costing to asses their performance and fiscal outcomes as compare to

set standards which ultimately assist in developing control over whole organisational

functions and making plan for future performance (Jetter and Walker, 2017).

Critical Analysis:

Main aim of above discussed techniques is to support corporation's managerial activities

like controlling, decision-making and controlling. As standard costing helps to determine

effectiveness of plan and business decisions by assessment of actual performance in comparison

of standards determined. For effective plan and control related to financial tasks company can

rely on financial planning. Budgetary controls within organisation ensures proper and

appropriate control over all financial activities, effective decisions and appropriate planning.

Analysis and evaluation of financial statements also boost the reliability of controlling and

planning structure along with companies key decisions. Management accounting in organisation

like Devanét adopted to improve entire managing framework with aim to attain predefined

objectives and targets. Companies can apply combination of different methods to for overall

effectiveness in whole managerial and organisational structure (Kabir, Sadiq and Tesfamariam,

2014).

TASK 2

Calculation of the ratios to analyse company performance:

Ratios 2018 2017

ROCE or Return On Capital

Employed :

= (Operating Profit /Capital

Employed) *100

here, Capital Employed = Total

Assets – External liabilities.

= 412 / 2925 * 100

= 14.10%

= 375 / 1912.50 *100

= 19.60%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

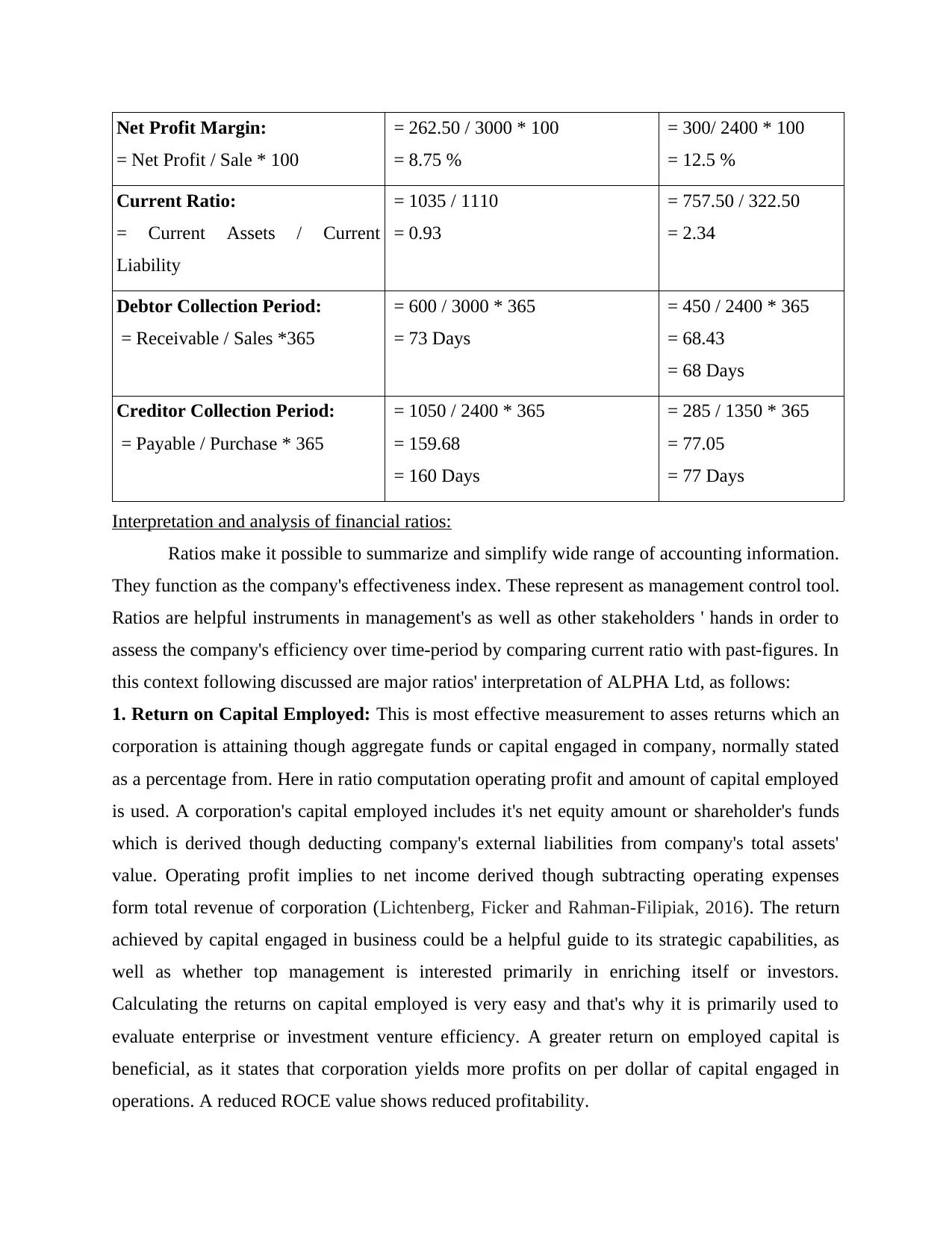

Net Profit Margin:

= Net Profit / Sale * 100

= 262.50 / 3000 * 100

= 8.75 %

= 300/ 2400 * 100

= 12.5 %

Current Ratio:

= Current Assets / Current

Liability

= 1035 / 1110

= 0.93

= 757.50 / 322.50

= 2.34

Debtor Collection Period:

= Receivable / Sales *365

= 600 / 3000 * 365

= 73 Days

= 450 / 2400 * 365

= 68.43

= 68 Days

Creditor Collection Period:

= Payable / Purchase * 365

= 1050 / 2400 * 365

= 159.68

= 160 Days

= 285 / 1350 * 365

= 77.05

= 77 Days

Interpretation and analysis of financial ratios:

Ratios make it possible to summarize and simplify wide range of accounting information.

They function as the company's effectiveness index. These represent as management control tool.

Ratios are helpful instruments in management's as well as other stakeholders ' hands in order to

assess the company's efficiency over time-period by comparing current ratio with past-figures. In

this context following discussed are major ratios' interpretation of ALPHA Ltd, as follows:

1. Return on Capital Employed: This is most effective measurement to asses returns which an

corporation is attaining though aggregate funds or capital engaged in company, normally stated

as a percentage from. Here in ratio computation operating profit and amount of capital employed

is used. A corporation's capital employed includes it's net equity amount or shareholder's funds

which is derived though deducting company's external liabilities from company's total assets'

value. Operating profit implies to net income derived though subtracting operating expenses

form total revenue of corporation (Lichtenberg, Ficker and Rahman-Filipiak, 2016). The return

achieved by capital engaged in business could be a helpful guide to its strategic capabilities, as

well as whether top management is interested primarily in enriching itself or investors.

Calculating the returns on capital employed is very easy and that's why it is primarily used to

evaluate enterprise or investment venture efficiency. A greater return on employed capital is

beneficial, as it states that corporation yields more profits on per dollar of capital engaged in

operations. A reduced ROCE value shows reduced profitability.

= Net Profit / Sale * 100

= 262.50 / 3000 * 100

= 8.75 %

= 300/ 2400 * 100

= 12.5 %

Current Ratio:

= Current Assets / Current

Liability

= 1035 / 1110

= 0.93

= 757.50 / 322.50

= 2.34

Debtor Collection Period:

= Receivable / Sales *365

= 600 / 3000 * 365

= 73 Days

= 450 / 2400 * 365

= 68.43

= 68 Days

Creditor Collection Period:

= Payable / Purchase * 365

= 1050 / 2400 * 365

= 159.68

= 160 Days

= 285 / 1350 * 365

= 77.05

= 77 Days

Interpretation and analysis of financial ratios:

Ratios make it possible to summarize and simplify wide range of accounting information.

They function as the company's effectiveness index. These represent as management control tool.

Ratios are helpful instruments in management's as well as other stakeholders ' hands in order to

assess the company's efficiency over time-period by comparing current ratio with past-figures. In

this context following discussed are major ratios' interpretation of ALPHA Ltd, as follows:

1. Return on Capital Employed: This is most effective measurement to asses returns which an

corporation is attaining though aggregate funds or capital engaged in company, normally stated

as a percentage from. Here in ratio computation operating profit and amount of capital employed

is used. A corporation's capital employed includes it's net equity amount or shareholder's funds

which is derived though deducting company's external liabilities from company's total assets'

value. Operating profit implies to net income derived though subtracting operating expenses

form total revenue of corporation (Lichtenberg, Ficker and Rahman-Filipiak, 2016). The return

achieved by capital engaged in business could be a helpful guide to its strategic capabilities, as

well as whether top management is interested primarily in enriching itself or investors.

Calculating the returns on capital employed is very easy and that's why it is primarily used to

evaluate enterprise or investment venture efficiency. A greater return on employed capital is

beneficial, as it states that corporation yields more profits on per dollar of capital engaged in

operations. A reduced ROCE value shows reduced profitability.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

In ALPHA Ltd, reported figures of operating profit in year 2017 and 2018 are £ 375,000

and £ 412,000 respectively. Figure of capital employed are £ 2925,000 and £ 1912,500. Based

upon these figures company's ROCE is 19.60% and 14.10% in year 2017 and 2018 respectively.

The assessed percentage of ratio shows that company's efficiencies to generate return on engaged

capital in business has been declined. Company should improve their operating profits to

increase this ratio. A decline in this ratio reflects company's efficiency to attain appropriate

benchmark of operating profit.

2. Net profit margin: It is significant ratio which demonstrate company's profitability level

during different periods. Here net profit is key element of this ratio which simply shows how

much amount company ultimately earned after providing its all indirect business expenses and

direct business expenses. Another element of this ratio is company's turnover over a particular

period. In this ratio relation among corporation's revenue and net profit is evaluated to ascertain

company's productivity in profitability terms. At a glance this ratio points out that whether

corporation is capable to attain profitability level (Palepu and Healy, 2013).

ALPHA Ltd's net profit was £ 300,000 in year 2017 which has been declined to £

262,500. While company's overall turnover was increased from £ 2400,000 to £ 3000,000 during

year 2017 to 2018. On the basis of amounts of net profit and turnover corporation's net-profit

margins are 8.75 % and 12.5% in year 2018 and 2017 respectively. Which simply shows that

there was decline in net-profit margin of company. This decline reflect that company's

effectiveness in operations which contributes in net-profit has been declined.

3. Current ratio: This is popular liquidity ratio which demonstrates corporation's actual position

in liquidity terms. The current ratio is used to evaluate the company's capacity to reimburse its

present obligations. This ratio takes into account company's current assets that include cash and

highly liquid assets compared to current liabilities of business. The current ratio is regarded as

“current” because for shortened time period it includes all current obligations and assets. A

greater current ratio is regarded as more beneficial than smaller current ratio since it

demonstrates that present debt payments could be made more readily by the business (Petersen,

Kushwaha and Kumar, 2015). If a firm is required to sell its fixed assets to payout its current

liabilities, then it generally implies that the business does not make sufficient operations in order

to support organisational activities. It simple words it points out that business is going to lose

cash or funds. This is often the consequence of bad collections of debts receivable or receivable

and £ 412,000 respectively. Figure of capital employed are £ 2925,000 and £ 1912,500. Based

upon these figures company's ROCE is 19.60% and 14.10% in year 2017 and 2018 respectively.

The assessed percentage of ratio shows that company's efficiencies to generate return on engaged

capital in business has been declined. Company should improve their operating profits to

increase this ratio. A decline in this ratio reflects company's efficiency to attain appropriate

benchmark of operating profit.

2. Net profit margin: It is significant ratio which demonstrate company's profitability level

during different periods. Here net profit is key element of this ratio which simply shows how

much amount company ultimately earned after providing its all indirect business expenses and

direct business expenses. Another element of this ratio is company's turnover over a particular

period. In this ratio relation among corporation's revenue and net profit is evaluated to ascertain

company's productivity in profitability terms. At a glance this ratio points out that whether

corporation is capable to attain profitability level (Palepu and Healy, 2013).

ALPHA Ltd's net profit was £ 300,000 in year 2017 which has been declined to £

262,500. While company's overall turnover was increased from £ 2400,000 to £ 3000,000 during

year 2017 to 2018. On the basis of amounts of net profit and turnover corporation's net-profit

margins are 8.75 % and 12.5% in year 2018 and 2017 respectively. Which simply shows that

there was decline in net-profit margin of company. This decline reflect that company's

effectiveness in operations which contributes in net-profit has been declined.

3. Current ratio: This is popular liquidity ratio which demonstrates corporation's actual position

in liquidity terms. The current ratio is used to evaluate the company's capacity to reimburse its

present obligations. This ratio takes into account company's current assets that include cash and

highly liquid assets compared to current liabilities of business. The current ratio is regarded as

“current” because for shortened time period it includes all current obligations and assets. A

greater current ratio is regarded as more beneficial than smaller current ratio since it

demonstrates that present debt payments could be made more readily by the business (Petersen,

Kushwaha and Kumar, 2015). If a firm is required to sell its fixed assets to payout its current

liabilities, then it generally implies that the business does not make sufficient operations in order

to support organisational activities. It simple words it points out that business is going to lose

cash or funds. This is often the consequence of bad collections of debts receivable or receivable

accounts. Preferably, current ratio must be higher than or equitable to 1, which means it can

settle its existing liabilities.

ALPHA's current liabilities in year 2018 is £ 322,500 which has been increased to

£1110000 in year 2017 and current assets of company in year 2018 and 2017 are £1035000 and

£757500 respectively showing an increase. Based on company's current assets and liabilities,

current ratio of company is 0.93 and 2.34 in year 2018 and 2017 respectively. Which

demonstrate that company's efficiencies to make payment of current obligations by applying

current assets has been declined. Company needed to improve this ratio by increasing current

assets as it reflects corporation's actual liquidity situation.

4. Debtor Collection Period: For business corporation on time payment by its clients or

customers is crucial variable of business's success. Debtors or account receivables required to be

gathered at predefined time-frame if corporation wishes to stay solvent and profitability position.

A balance in account receivable becoming aged, there is increased possibility that account may

be bad-debts. Furthermore, capital and collection costs increases as the age of accounts

receivable increases. Computation of average days of collection and evaluation is key task by

which managers can assess the corporation's efficiency to manage debts. It is a real measure of

efficacy of the loan as well as collection strategy of a business, compared to previous experience

and businesses in same sector (Richard, Kirby and Chadwick, 2013). This period refers to time

period between occurrence of debt and it payment of debt. The greater long-standing

indebtedness and longer exceptional debts, reduced effectiveness of loan collection unit of

company, it is essential that the ageing plan is applied, because it allows management to

understand the magnitude and amount of recovery and also to make the liquidity situation of d

better understood and suspiciousness of recovery.

In company ALPHA Ltd, reported balance of receivables in year 2017 is £ 450,000

which has been increased to £600,000 in year 2018 along with company revenue. Company's

average days of collection is 73 days in year 2018 and 68 days in year 2017. Which indicates that

company's chances of bad debt in company has been increased and also that efficiencies to

recover or collect amount from debtors has been decreased. Company required to control this

ratio as higher days reflects chances and probability of insolvency of debtors and bad-debts.

5. Creditor Collection Period: This ratio compute the period in days which company is taking

for payment of lenders and creditors. It is most effective ratio that hows company's short-term

settle its existing liabilities.

ALPHA's current liabilities in year 2018 is £ 322,500 which has been increased to

£1110000 in year 2017 and current assets of company in year 2018 and 2017 are £1035000 and

£757500 respectively showing an increase. Based on company's current assets and liabilities,

current ratio of company is 0.93 and 2.34 in year 2018 and 2017 respectively. Which

demonstrate that company's efficiencies to make payment of current obligations by applying

current assets has been declined. Company needed to improve this ratio by increasing current

assets as it reflects corporation's actual liquidity situation.

4. Debtor Collection Period: For business corporation on time payment by its clients or

customers is crucial variable of business's success. Debtors or account receivables required to be

gathered at predefined time-frame if corporation wishes to stay solvent and profitability position.

A balance in account receivable becoming aged, there is increased possibility that account may

be bad-debts. Furthermore, capital and collection costs increases as the age of accounts

receivable increases. Computation of average days of collection and evaluation is key task by

which managers can assess the corporation's efficiency to manage debts. It is a real measure of

efficacy of the loan as well as collection strategy of a business, compared to previous experience

and businesses in same sector (Richard, Kirby and Chadwick, 2013). This period refers to time

period between occurrence of debt and it payment of debt. The greater long-standing

indebtedness and longer exceptional debts, reduced effectiveness of loan collection unit of

company, it is essential that the ageing plan is applied, because it allows management to

understand the magnitude and amount of recovery and also to make the liquidity situation of d

better understood and suspiciousness of recovery.

In company ALPHA Ltd, reported balance of receivables in year 2017 is £ 450,000

which has been increased to £600,000 in year 2018 along with company revenue. Company's

average days of collection is 73 days in year 2018 and 68 days in year 2017. Which indicates that

company's chances of bad debt in company has been increased and also that efficiencies to

recover or collect amount from debtors has been decreased. Company required to control this

ratio as higher days reflects chances and probability of insolvency of debtors and bad-debts.

5. Creditor Collection Period: This ratio compute the period in days which company is taking

for payment of lenders and creditors. It is most effective ratio that hows company's short-term

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

liquidity position. This ratio reflects corporation's capabilities to repay their short-term creditors.

Company should assess this ratio to maintain company's creditors collection days as it

determines corporation's liquidity situation. It represents gap timeline between company's credit

purchases and payments to creditors and supplier. Since trade payables or creditors balance is

related to credit purchases so amount of credit purchases is mainly used in computation of this

ratio. But amount of credit purchases is generally not separately shown in company's income

statement so in this case company's total purchases can be utilized to assess days (Seshan and

Yang, 2014). A increased average credit period suggest that business has extremely good

relationships with its creditors or suppliers, but it generally indicates otherwise, that there is no

payment of trade payables since unavailability of adequate funds. Thus, it may reflect company's

financial distress.

ALPHA Ltd's creditors has been increased with higher difference i.e. from £ 285,000 in

2017 to £ 1050,000 in year 2018. While the creditors' collection period has been increased from

77 days (In year 2017) to 160 days in year 2018. Which exhibits unavailability of funds to meet

creditors obligations. Company is required to minimise their period as increase period indicates

that business's efficiencies and capabilities to make payment of suppliers and creditors has been

decreased.

CONCLUSION

From above discussed study it has been articulated that in existing dynamic trade

environment corporations should adopt different tools and methods to enhance effectiveness of

financial decision-making processes. Companies should adopt and implement techniques which

are linked with processes of management accounting for effective decision-making. As use of

these techniques help to implement control and planning structure which is essential for fiscal

decision-making. Further use of outcomes of different financial ratios in analysis and evaluation

of performance of corporation helps in efficient decision-making. Each ratio have its different

use and significance for business since each ratio defines different aspects of corporation's

performance.

Company should assess this ratio to maintain company's creditors collection days as it

determines corporation's liquidity situation. It represents gap timeline between company's credit

purchases and payments to creditors and supplier. Since trade payables or creditors balance is

related to credit purchases so amount of credit purchases is mainly used in computation of this

ratio. But amount of credit purchases is generally not separately shown in company's income

statement so in this case company's total purchases can be utilized to assess days (Seshan and

Yang, 2014). A increased average credit period suggest that business has extremely good

relationships with its creditors or suppliers, but it generally indicates otherwise, that there is no

payment of trade payables since unavailability of adequate funds. Thus, it may reflect company's

financial distress.

ALPHA Ltd's creditors has been increased with higher difference i.e. from £ 285,000 in

2017 to £ 1050,000 in year 2018. While the creditors' collection period has been increased from

77 days (In year 2017) to 160 days in year 2018. Which exhibits unavailability of funds to meet

creditors obligations. Company is required to minimise their period as increase period indicates

that business's efficiencies and capabilities to make payment of suppliers and creditors has been

decreased.

CONCLUSION

From above discussed study it has been articulated that in existing dynamic trade

environment corporations should adopt different tools and methods to enhance effectiveness of

financial decision-making processes. Companies should adopt and implement techniques which

are linked with processes of management accounting for effective decision-making. As use of

these techniques help to implement control and planning structure which is essential for fiscal

decision-making. Further use of outcomes of different financial ratios in analysis and evaluation

of performance of corporation helps in efficient decision-making. Each ratio have its different

use and significance for business since each ratio defines different aspects of corporation's

performance.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals:

Carvalho, L.S., Meier, S. and Wang, S.W., 2016. Poverty and economic decision-making:

Evidence from changes in financial resources at payday. American Economic

Review. 106(2). pp. 260-84.

Epstein, M .J., Buhovac, A. R. and Yuthas, K., 2015. Managing social, environmental and

financial performance simultaneously. Long range planning. 48(1). pp.35-45.

Graham, J.R., Harvey, C.R. and Puri, M., 2015. Capital allocation and delegation of decision-

making authority within firms. Journal of Financial Economics. 115(3). pp. 449-470.

Hernes, M. and Sobieska-Karpińska, J., 2016. Application of the consensus method in a

multiagent financial decision support system. Information Systems and e-Business

Management. 14(1). pp.167-185.

Jetter, M. and Walker, J .K., 2017. Anchoring in financial decision-making: Evidence from

Jeopardy!.Journal of Economic Behavior & Organization. 141. pp. 164-176.

Kabir, G., Sadiq, R. and Tesfamariam, S., 2014. A review of multi-criteria decision-making

methods for infrastructure management. Structure and Infrastructure Engineering.

10(9). pp. 1176-1210.

Lichtenberg, P.A., Ficker, L.J. and Rahman-Filipiak, A., 2016. Financial decision-making

abilities and financial exploitation in older African Americans: Preliminary validity

evidence for the Lichtenberg Financial Decision Rating Scale (LFDRS). Journal of

elder abuse & neglect. 28(1). pp. 14-33.

Palepu, K. G. and Healy, P. M., 2013. Business analysis and valuation: Using financial

statements, text and cases.

Petersen, J.A., Kushwaha, T. and Kumar, V., 2015. Marketing communication strategies and

consumer financial decision making: The role of national culture. Journal of Marketing.

79(1). pp. 44-63.

Richard, O .C., Kirby, S .L. and Chadwick, K., 2013. The impact of racial and gender diversity

in management on financial performance: How participative strategy making features

can unleash a diversity advantage. The International Journal of Human Resource

Management. 24(13). pp. 2571-2582.

Seshan, G. and Yang, D., 2014. Motivating migrants: A field experiment on financial decision-

making in transnational households. Journal of Development Economics.108. pp. 119-

127.

Online

About Devanet. 2019. [Online] Available Through:

<https://devanetbelts.co.uk/aboutus.html>

Books and Journals:

Carvalho, L.S., Meier, S. and Wang, S.W., 2016. Poverty and economic decision-making:

Evidence from changes in financial resources at payday. American Economic

Review. 106(2). pp. 260-84.

Epstein, M .J., Buhovac, A. R. and Yuthas, K., 2015. Managing social, environmental and

financial performance simultaneously. Long range planning. 48(1). pp.35-45.

Graham, J.R., Harvey, C.R. and Puri, M., 2015. Capital allocation and delegation of decision-

making authority within firms. Journal of Financial Economics. 115(3). pp. 449-470.

Hernes, M. and Sobieska-Karpińska, J., 2016. Application of the consensus method in a

multiagent financial decision support system. Information Systems and e-Business

Management. 14(1). pp.167-185.

Jetter, M. and Walker, J .K., 2017. Anchoring in financial decision-making: Evidence from

Jeopardy!.Journal of Economic Behavior & Organization. 141. pp. 164-176.

Kabir, G., Sadiq, R. and Tesfamariam, S., 2014. A review of multi-criteria decision-making

methods for infrastructure management. Structure and Infrastructure Engineering.

10(9). pp. 1176-1210.

Lichtenberg, P.A., Ficker, L.J. and Rahman-Filipiak, A., 2016. Financial decision-making

abilities and financial exploitation in older African Americans: Preliminary validity

evidence for the Lichtenberg Financial Decision Rating Scale (LFDRS). Journal of

elder abuse & neglect. 28(1). pp. 14-33.

Palepu, K. G. and Healy, P. M., 2013. Business analysis and valuation: Using financial

statements, text and cases.

Petersen, J.A., Kushwaha, T. and Kumar, V., 2015. Marketing communication strategies and

consumer financial decision making: The role of national culture. Journal of Marketing.

79(1). pp. 44-63.

Richard, O .C., Kirby, S .L. and Chadwick, K., 2013. The impact of racial and gender diversity

in management on financial performance: How participative strategy making features

can unleash a diversity advantage. The International Journal of Human Resource

Management. 24(13). pp. 2571-2582.

Seshan, G. and Yang, D., 2014. Motivating migrants: A field experiment on financial decision-

making in transnational households. Journal of Development Economics.108. pp. 119-

127.

Online

About Devanet. 2019. [Online] Available Through:

<https://devanetbelts.co.uk/aboutus.html>

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.