Financial Decision Making Report: Starbucks Acquisition of Roast Ltd

VerifiedAdded on 2023/01/12

|16

|4613

|27

Report

AI Summary

This report presents a financial analysis of the potential acquisition of Roast Ltd, a UK-based coffee house chain, by Starbucks. The report begins with an overview of the coffee house industry, highlighting key competitors, challenges, and opportunities. It then analyzes Roast Ltd's financial performance, including profit and loss statements, balance sheets, and cash flow statements, revealing a positive revenue trend but concerning liquidity ratios and negative cash flow from operations. The report further explores investment appraisal techniques, forecasting management's expectations, and evaluating capital budgeting methods. Based on the analysis, the report suggests that Starbucks should proceed with the acquisition, considering the overall business performance and feasible investment plans.

Financial Decision

Making

Making

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

EXECUTIVE SUMMARY

This report presents about the financial decision making with respect to acquisition of

Roast Ltd which is a UK based coffee house chain to be acquired by Starbucks. This report

highlights about the current coffee house industry along with the key competitors prevailing in

the business environment along with the challenges and opportunities available. The profit or

loss statement analyzeddepicts about the currentfinancial performance of Roast Ltd which is

good. The financial position of Roast Ltd is analyzed which states that the current financial

position is not good and also by cashflow analysis it is determined that the cash flow from

operating activity is negative which might be the reason for not distributing dividend to the

shareholders. Along with that the different investment appraisal techniques are evaluated based

on which decision is taken the Starbucks should acquire Roast Ltd as the overall business

performance is good and further investment plans are also feasible.

This report presents about the financial decision making with respect to acquisition of

Roast Ltd which is a UK based coffee house chain to be acquired by Starbucks. This report

highlights about the current coffee house industry along with the key competitors prevailing in

the business environment along with the challenges and opportunities available. The profit or

loss statement analyzeddepicts about the currentfinancial performance of Roast Ltd which is

good. The financial position of Roast Ltd is analyzed which states that the current financial

position is not good and also by cashflow analysis it is determined that the cash flow from

operating activity is negative which might be the reason for not distributing dividend to the

shareholders. Along with that the different investment appraisal techniques are evaluated based

on which decision is taken the Starbucks should acquire Roast Ltd as the overall business

performance is good and further investment plans are also feasible.

TABLE OF CONTENTS

Task..................................................................................................................................................4

Part 1: Review of industry...............................................................................................................4

Part 2: Analyzing performance of business.....................................................................................4

2.1 Assessing profit and Loss statement......................................................................................4

2.2 Analyzing statement of balance sheet....................................................................................5

2.3 Determining cash position by making use of cash flow statement........................................6

Part 3: Investment appraisal.............................................................................................................8

3.1.a Forecast of management.....................................................................................................8

3.1.b. Capital budgeting Techniques...........................................................................................8

3.2 Funding sources...................................................................................................................11

REFERENCES..............................................................................................................................14

APPENDIX....................................................................................................................................16

Task..................................................................................................................................................4

Part 1: Review of industry...............................................................................................................4

Part 2: Analyzing performance of business.....................................................................................4

2.1 Assessing profit and Loss statement......................................................................................4

2.2 Analyzing statement of balance sheet....................................................................................5

2.3 Determining cash position by making use of cash flow statement........................................6

Part 3: Investment appraisal.............................................................................................................8

3.1.a Forecast of management.....................................................................................................8

3.1.b. Capital budgeting Techniques...........................................................................................8

3.2 Funding sources...................................................................................................................11

REFERENCES..............................................................................................................................14

APPENDIX....................................................................................................................................16

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Task

Part 1: Review of industry

Coffee is the popular drink among the residents of UK.

The instant coffee has a turnover of £810 million in the year 2017 which is equal to 54%

of £1.5 billion total turnover generated by all coffee products.

The total estimated revenue in the year 2017 was £7.2 billion which represents an

average growth of 7% during the period 2012-17.

The coffee industry has approximately 7.5% of workforce with respect to thewhole food

and beverage industry.

The industry is affected by the impact of Brexit along with the value of pounds.

Manufacturers have seen an increase in the price (Ferreira, 2017).

The majorcompetitorsin the industry are - Costa Ltd., Caffe Nero Group Holdings Ltd

along with Starbucks.

Costa Ltd is the market leader and is having the highest number of outlets which is 2121

in UK followed by Starbuck with 898 and Caffe Nero with 650 stores.

The major challenges faced the coffee industry is the increasing cost of landand

labourcost and the impact of Brexit.

The opportunities available in the industry is the emergence of sustainability and plant-

based menus (Luty, 2019).

These leading coffee chains have already introduced the vegan menu and along with

meeting the requirement of oat milk.

Part 2: Analyzing business performance

2.1 Assessing P&L statement

It has been interpreted from the statement that over the year revenue of Roast Ltd is

increasing that is from Pound 2022 in the year 2017 to Pound 2534 in 2018. This reflects that the

sales of an entity have been increasing that in turn seen as the positive sign and better

performance of the firm. With an increase in the sales, COGS also increases from pound 1505 in

2017 to 1990 in 2018. This means that the variable cost of Roast Ltd has increased from one

accounting period to another in associated with the cost of sales. Therefore, the company should

focus on ensuring or keeping control on its cost so that it could earn higher profits on its sale. In

Part 1: Review of industry

Coffee is the popular drink among the residents of UK.

The instant coffee has a turnover of £810 million in the year 2017 which is equal to 54%

of £1.5 billion total turnover generated by all coffee products.

The total estimated revenue in the year 2017 was £7.2 billion which represents an

average growth of 7% during the period 2012-17.

The coffee industry has approximately 7.5% of workforce with respect to thewhole food

and beverage industry.

The industry is affected by the impact of Brexit along with the value of pounds.

Manufacturers have seen an increase in the price (Ferreira, 2017).

The majorcompetitorsin the industry are - Costa Ltd., Caffe Nero Group Holdings Ltd

along with Starbucks.

Costa Ltd is the market leader and is having the highest number of outlets which is 2121

in UK followed by Starbuck with 898 and Caffe Nero with 650 stores.

The major challenges faced the coffee industry is the increasing cost of landand

labourcost and the impact of Brexit.

The opportunities available in the industry is the emergence of sustainability and plant-

based menus (Luty, 2019).

These leading coffee chains have already introduced the vegan menu and along with

meeting the requirement of oat milk.

Part 2: Analyzing business performance

2.1 Assessing P&L statement

It has been interpreted from the statement that over the year revenue of Roast Ltd is

increasing that is from Pound 2022 in the year 2017 to Pound 2534 in 2018. This reflects that the

sales of an entity have been increasing that in turn seen as the positive sign and better

performance of the firm. With an increase in the sales, COGS also increases from pound 1505 in

2017 to 1990 in 2018. This means that the variable cost of Roast Ltd has increased from one

accounting period to another in associated with the cost of sales. Therefore, the company should

focus on ensuring or keeping control on its cost so that it could earn higher profits on its sale. In

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

order to reduce the cost regarding the sales, an organization should increase its revenue with a

greater value with incurring less or minimal variable cost incurred in producing the product

within the premises of business.

The gross profit also seen as increasing from one period to another which is stated as the

profits generated by the firm after paying off its cost attached with the sales. Though the amount

of gross profit is increasing but the ratio over the year is seen as declining because the cost of

goods sold increased with a greater value against a small value of increase in the sales. This

shows that for improving the operational performance, company must ensure adequate control

over its expenses. Similarly, with increase in operating income, the operating expenses are also

depicted as rising from one accounting period to another. This leads to increase in the operating

profit ratio or margin which in turn indicates that Roast Ltd is earning adequate amount of

income for paying itsoperating expense.

Moreover, the net profit ratio of an enterprise is also increasing that clearly means that

the company is performing well with earning higher return and profits. This also depicts that the

firm is generating higher profits after paying off all its cost, expenses and the tax obligation.

Overall the profitability performance of Roast Ltd is evaluated and found as better with passage

of one accounting year to another in an overall market.

2.2 Analyzing statement of balance sheet

The balance sheet provides an insight about the how the company is operating and helps

in grabbing deep insight into the business functioning. There are three important things to be

taken care of while analyzing the balance sheet, which are, liquidity, capital and financial

structure and the working capital of the business. As per theinformation provided in the

Statement of financial position of Roaster Ltd. it can be seen that there aremany changes in the

company’s total assets and total liabilities and to get a clear picture, financial ratios are used.

Liquidity ratio: It will help in analyzinghow company can convert its current assets into cash in

order to pay offits short-term liabilitieswithout raising any additional capital (Lessambo, 2018).

The main liquidity ratios that are essential for the business are stated below.

Current ratio, shows the relationship between current asset with current liabilities (Williams and

Dobelman, 2017). The current ratio of Roast Ltd has reduced from 2.51 times in 2017 to 1.45

greater value with incurring less or minimal variable cost incurred in producing the product

within the premises of business.

The gross profit also seen as increasing from one period to another which is stated as the

profits generated by the firm after paying off its cost attached with the sales. Though the amount

of gross profit is increasing but the ratio over the year is seen as declining because the cost of

goods sold increased with a greater value against a small value of increase in the sales. This

shows that for improving the operational performance, company must ensure adequate control

over its expenses. Similarly, with increase in operating income, the operating expenses are also

depicted as rising from one accounting period to another. This leads to increase in the operating

profit ratio or margin which in turn indicates that Roast Ltd is earning adequate amount of

income for paying itsoperating expense.

Moreover, the net profit ratio of an enterprise is also increasing that clearly means that

the company is performing well with earning higher return and profits. This also depicts that the

firm is generating higher profits after paying off all its cost, expenses and the tax obligation.

Overall the profitability performance of Roast Ltd is evaluated and found as better with passage

of one accounting year to another in an overall market.

2.2 Analyzing statement of balance sheet

The balance sheet provides an insight about the how the company is operating and helps

in grabbing deep insight into the business functioning. There are three important things to be

taken care of while analyzing the balance sheet, which are, liquidity, capital and financial

structure and the working capital of the business. As per theinformation provided in the

Statement of financial position of Roaster Ltd. it can be seen that there aremany changes in the

company’s total assets and total liabilities and to get a clear picture, financial ratios are used.

Liquidity ratio: It will help in analyzinghow company can convert its current assets into cash in

order to pay offits short-term liabilitieswithout raising any additional capital (Lessambo, 2018).

The main liquidity ratios that are essential for the business are stated below.

Current ratio, shows the relationship between current asset with current liabilities (Williams and

Dobelman, 2017). The current ratio of Roast Ltd has reduced from 2.51 times in 2017 to 1.45

times in 2018 which indicates that Roast Ltd has either increased the used of short-term debt or

reduced investment in current assets as the ideal ratio of 2:1. This indicates that the Roast Ltd.

needs to effectively manage its current ratio otherwise it may not be in the position to meet

itscurrent business requirements.

Quick ratio, it is similar to current ratio but it is conservative as it takes into consideration

only that assets which can be easily convertible into cash (Yasa and Wirawati, 2016). It

includes cash, marketable securities and account receivable but excludes inventory because it

cannot be easily converted to cash. Higher the ratio better it is for the company. The quick

ratio of Roast Ltd has reduced from 1.64 in 2017 to 0.48 in 2018 which is not a good

indicator. This means that company will struggle in paying off its short-term debts.

Net working capital, it is derived by deducting current liabilities from current assets,

which measures the company’s liquidity and ability to meet its short terms needs and funding

the operation of the business (Afrifa, 2016). It is ideal to have positive working capital, when

there is more current assets in comparison to current liabilities. The net working capital of

Roast Ltd. has reduced to £139 in 2018 from £209 in 2017. This indicates that the short-term

liquidity position of the business is under concern.

Leverage ratio: This ratio shows the proportion of debt accompany has its capital structure.

It shows how the business operation is financed using debt and equity.

Debt-to-equity ratio, it is derivedby dividing total debt of the company against the total

shareholder’s equity (Indrawan, Suyanto and Mulyadi, 2017). It measures the degree to

which Roast Ltd is financing its business operation and shows the ability of shareholder’s

equity to cover all the debts during times of downfall. The higher ratio indicates higher risk

to shareholders. The debt-to-equity ratio of Roast Ltd has increased from 0.31 to 0.68 in

2018. But is less than one which is preferable.

Apart from the ratios stated above, the other key aspects to be considered is that Roast

Ltd. has not distributed dividend which may be because of its expansion plan for which it

wants to retain the amount for reinvestment for expanding business which has caused an

increase in retained earnings. The debtor collection of the Roast Ltd. has increase from 17

days to 21 days which is because of the reason that in the year 2018, the major customer of

reduced investment in current assets as the ideal ratio of 2:1. This indicates that the Roast Ltd.

needs to effectively manage its current ratio otherwise it may not be in the position to meet

itscurrent business requirements.

Quick ratio, it is similar to current ratio but it is conservative as it takes into consideration

only that assets which can be easily convertible into cash (Yasa and Wirawati, 2016). It

includes cash, marketable securities and account receivable but excludes inventory because it

cannot be easily converted to cash. Higher the ratio better it is for the company. The quick

ratio of Roast Ltd has reduced from 1.64 in 2017 to 0.48 in 2018 which is not a good

indicator. This means that company will struggle in paying off its short-term debts.

Net working capital, it is derived by deducting current liabilities from current assets,

which measures the company’s liquidity and ability to meet its short terms needs and funding

the operation of the business (Afrifa, 2016). It is ideal to have positive working capital, when

there is more current assets in comparison to current liabilities. The net working capital of

Roast Ltd. has reduced to £139 in 2018 from £209 in 2017. This indicates that the short-term

liquidity position of the business is under concern.

Leverage ratio: This ratio shows the proportion of debt accompany has its capital structure.

It shows how the business operation is financed using debt and equity.

Debt-to-equity ratio, it is derivedby dividing total debt of the company against the total

shareholder’s equity (Indrawan, Suyanto and Mulyadi, 2017). It measures the degree to

which Roast Ltd is financing its business operation and shows the ability of shareholder’s

equity to cover all the debts during times of downfall. The higher ratio indicates higher risk

to shareholders. The debt-to-equity ratio of Roast Ltd has increased from 0.31 to 0.68 in

2018. But is less than one which is preferable.

Apart from the ratios stated above, the other key aspects to be considered is that Roast

Ltd. has not distributed dividend which may be because of its expansion plan for which it

wants to retain the amount for reinvestment for expanding business which has caused an

increase in retained earnings. The debtor collection of the Roast Ltd. has increase from 17

days to 21 days which is because of the reason that in the year 2018, the major customer of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

the companysuffered some financial issuesfor which the payment period increased to 90 days

instead of 30 days.

2.3 Determining cash position by making use of cash flow statement

The cash flow statement analysis assists the company in analyzing the cash flows of the

business during the period. The cash flow comes from three types of activities, which are,

operating, investing and financing activities.

Cash flow from Operations

The operating profit of Roast Ltd is £127 which is higher in comparison to £51 in 2017.

Roast Ltd has the cash flow from business operation negative which means the company has

made more expenditure. The increase in operating profit is because of income received from

other sources (Das, 2018). Also, the expansion plan in Romania is successful which has resulted

in increase in revenue. But the increase in inventory and trade receivable of £179 and £55

respectively and decrease in trade payable by £97 indicates cash outflow which has affected its

working capital management.

Cash Flow from Investment Activities

In this, the Roast Ltd has made investment by purchasing fixed asset of £358 which is

mainly for its Romania expansion plan. This has led to huge amount of cash outflow.

Cashflows from financing activities

In the year 2018, Roast Ltd has taken debtof £175 which has represented as thecash

inflow of the business.

Based on the aboveanalysis, it can be said that the cash flow position of the business is

not that good. Irrespective to the other activities the most important is the cash flow from the

operating activity which is negative.

Operating cash cycle of Roast Ltd

This cycle indicates the amount of timethe company takes for selling its inventory, collect

the amount from receivables and make payment to its account payables (Jalal and Khaksari,

instead of 30 days.

2.3 Determining cash position by making use of cash flow statement

The cash flow statement analysis assists the company in analyzing the cash flows of the

business during the period. The cash flow comes from three types of activities, which are,

operating, investing and financing activities.

Cash flow from Operations

The operating profit of Roast Ltd is £127 which is higher in comparison to £51 in 2017.

Roast Ltd has the cash flow from business operation negative which means the company has

made more expenditure. The increase in operating profit is because of income received from

other sources (Das, 2018). Also, the expansion plan in Romania is successful which has resulted

in increase in revenue. But the increase in inventory and trade receivable of £179 and £55

respectively and decrease in trade payable by £97 indicates cash outflow which has affected its

working capital management.

Cash Flow from Investment Activities

In this, the Roast Ltd has made investment by purchasing fixed asset of £358 which is

mainly for its Romania expansion plan. This has led to huge amount of cash outflow.

Cashflows from financing activities

In the year 2018, Roast Ltd has taken debtof £175 which has represented as thecash

inflow of the business.

Based on the aboveanalysis, it can be said that the cash flow position of the business is

not that good. Irrespective to the other activities the most important is the cash flow from the

operating activity which is negative.

Operating cash cycle of Roast Ltd

This cycle indicates the amount of timethe company takes for selling its inventory, collect

the amount from receivables and make payment to its account payables (Jalal and Khaksari,

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2019). It is favorable to have the shorter cycle which means which means that liquidity position

of the company is strong. It is also called cash conversion cycle.

CCC = Days of Sales Outstanding (DSO)+ Days of Inventory Outstanding (DIO)- Days of

Payables Outstanding (DPO)

Operating cash cycle (2017) = 17+29-33 = 12 days

Operating cash cycle (2018) = 21+55-43 = 33 days

Operating cash cycle shows that the Roast Ltdis not effectively managing its working

capital assets (Chang, 2018). This indicates that there might be difficulty in growing business

because of less liquidity and may increase the need for borrowing for business operation.

Dividend policy of Roast Ltd for the year 2018

In the year 2018, the company uses residual dividend policy which is mostly used by the

company. In this, the company pays out from the profits after meeting all the expenditure

(Hauser and Thornton Jr, 2017). The amount paid to the shareholders is not fixed and sometimes

not even paid as it is retained for future business opportunities. The company should have paid

dividend in 2018 instead of 2017 because in 2017 the expansion was done in Romania but in

2018 the actual sales were made and at this point company should have paiddividend to its

shareholders.

Part 3: Investment appraisal

3.1.a Forecast of management

The manager of Roast Limited has forecasted that in the coming 5 years of period the

revenue of company in respect to its new product lines would be increasing. Similarly the

variable cost is also reflected to be rise along with the revenue. The resulted contribution will

also increase that in turn indicates that the cash inflows would be increasing with passage of one

to another. This clearly shows that company would be earning higher amount of the profits in the

future y making investment in creating a new product lines in the Romania.

of the company is strong. It is also called cash conversion cycle.

CCC = Days of Sales Outstanding (DSO)+ Days of Inventory Outstanding (DIO)- Days of

Payables Outstanding (DPO)

Operating cash cycle (2017) = 17+29-33 = 12 days

Operating cash cycle (2018) = 21+55-43 = 33 days

Operating cash cycle shows that the Roast Ltdis not effectively managing its working

capital assets (Chang, 2018). This indicates that there might be difficulty in growing business

because of less liquidity and may increase the need for borrowing for business operation.

Dividend policy of Roast Ltd for the year 2018

In the year 2018, the company uses residual dividend policy which is mostly used by the

company. In this, the company pays out from the profits after meeting all the expenditure

(Hauser and Thornton Jr, 2017). The amount paid to the shareholders is not fixed and sometimes

not even paid as it is retained for future business opportunities. The company should have paid

dividend in 2018 instead of 2017 because in 2017 the expansion was done in Romania but in

2018 the actual sales were made and at this point company should have paiddividend to its

shareholders.

Part 3: Investment appraisal

3.1.a Forecast of management

The manager of Roast Limited has forecasted that in the coming 5 years of period the

revenue of company in respect to its new product lines would be increasing. Similarly the

variable cost is also reflected to be rise along with the revenue. The resulted contribution will

also increase that in turn indicates that the cash inflows would be increasing with passage of one

to another. This clearly shows that company would be earning higher amount of the profits in the

future y making investment in creating a new product lines in the Romania.

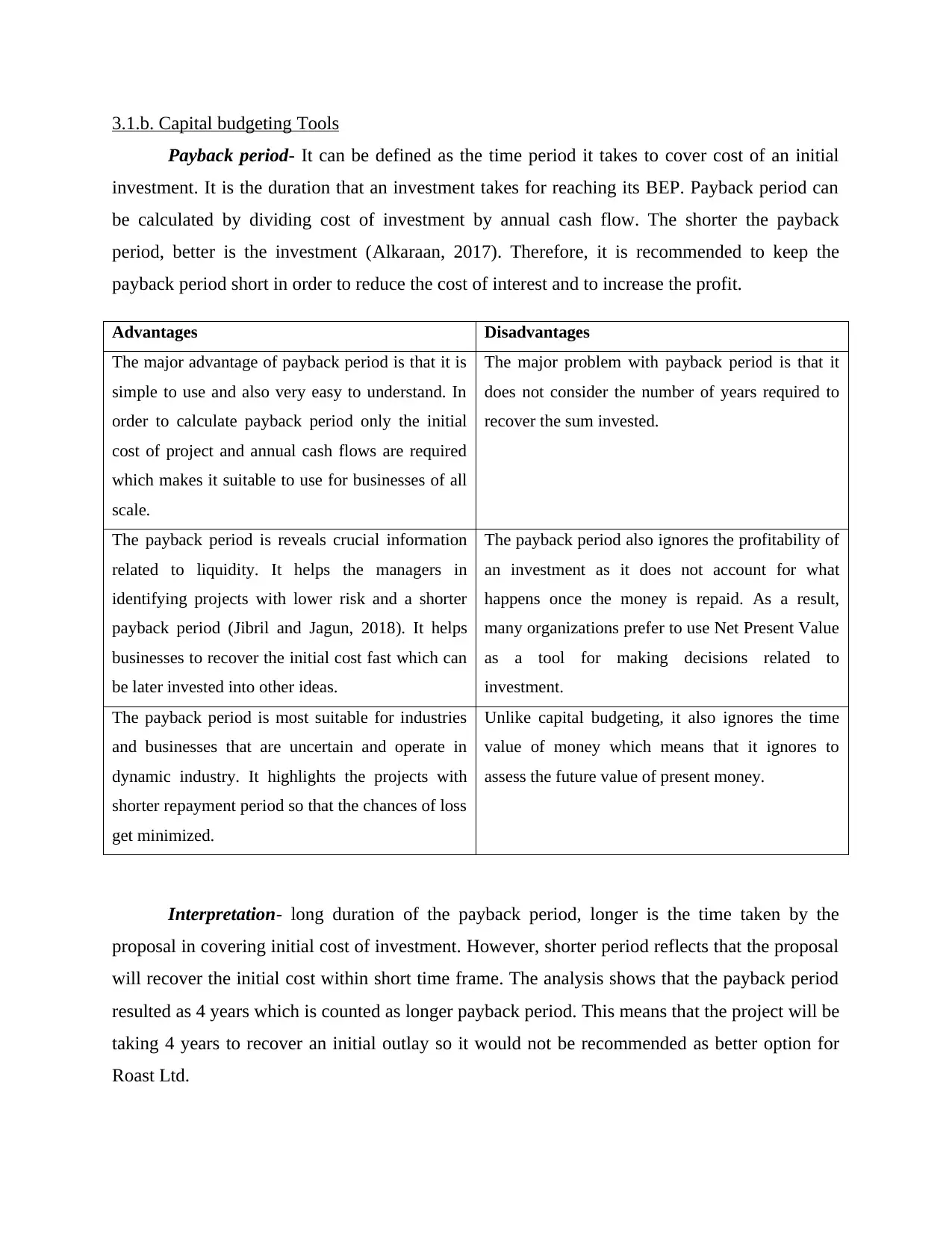

3.1.b. Capital budgeting Tools

Payback period- It can be defined as the time period it takes to cover cost of an initial

investment. It is the duration that an investment takes for reaching its BEP. Payback period can

be calculated by dividing cost of investment by annual cash flow. The shorter the payback

period, better is the investment (Alkaraan, 2017). Therefore, it is recommended to keep the

payback period short in order to reduce the cost of interest and to increase the profit.

Advantages Disadvantages

The major advantage of payback period is that it is

simple to use and also very easy to understand. In

order to calculate payback period only the initial

cost of project and annual cash flows are required

which makes it suitable to use for businesses of all

scale.

The major problem with payback period is that it

does not consider the number of years required to

recover the sum invested.

The payback period is reveals crucial information

related to liquidity. It helps the managers in

identifying projects with lower risk and a shorter

payback period (Jibril and Jagun, 2018). It helps

businesses to recover the initial cost fast which can

be later invested into other ideas.

The payback period also ignores the profitability of

an investment as it does not account for what

happens once the money is repaid. As a result,

many organizations prefer to use Net Present Value

as a tool for making decisions related to

investment.

The payback period is most suitable for industries

and businesses that are uncertain and operate in

dynamic industry. It highlights the projects with

shorter repayment period so that the chances of loss

get minimized.

Unlike capital budgeting, it also ignores the time

value of money which means that it ignores to

assess the future value of present money.

Interpretation- long duration of the payback period, longer is the time taken by the

proposal in covering initial cost of investment. However, shorter period reflects that the proposal

will recover the initial cost within short time frame. The analysis shows that the payback period

resulted as 4 years which is counted as longer payback period. This means that the project will be

taking 4 years to recover an initial outlay so it would not be recommended as better option for

Roast Ltd.

Payback period- It can be defined as the time period it takes to cover cost of an initial

investment. It is the duration that an investment takes for reaching its BEP. Payback period can

be calculated by dividing cost of investment by annual cash flow. The shorter the payback

period, better is the investment (Alkaraan, 2017). Therefore, it is recommended to keep the

payback period short in order to reduce the cost of interest and to increase the profit.

Advantages Disadvantages

The major advantage of payback period is that it is

simple to use and also very easy to understand. In

order to calculate payback period only the initial

cost of project and annual cash flows are required

which makes it suitable to use for businesses of all

scale.

The major problem with payback period is that it

does not consider the number of years required to

recover the sum invested.

The payback period is reveals crucial information

related to liquidity. It helps the managers in

identifying projects with lower risk and a shorter

payback period (Jibril and Jagun, 2018). It helps

businesses to recover the initial cost fast which can

be later invested into other ideas.

The payback period also ignores the profitability of

an investment as it does not account for what

happens once the money is repaid. As a result,

many organizations prefer to use Net Present Value

as a tool for making decisions related to

investment.

The payback period is most suitable for industries

and businesses that are uncertain and operate in

dynamic industry. It highlights the projects with

shorter repayment period so that the chances of loss

get minimized.

Unlike capital budgeting, it also ignores the time

value of money which means that it ignores to

assess the future value of present money.

Interpretation- long duration of the payback period, longer is the time taken by the

proposal in covering initial cost of investment. However, shorter period reflects that the proposal

will recover the initial cost within short time frame. The analysis shows that the payback period

resulted as 4 years which is counted as longer payback period. This means that the project will be

taking 4 years to recover an initial outlay so it would not be recommended as better option for

Roast Ltd.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

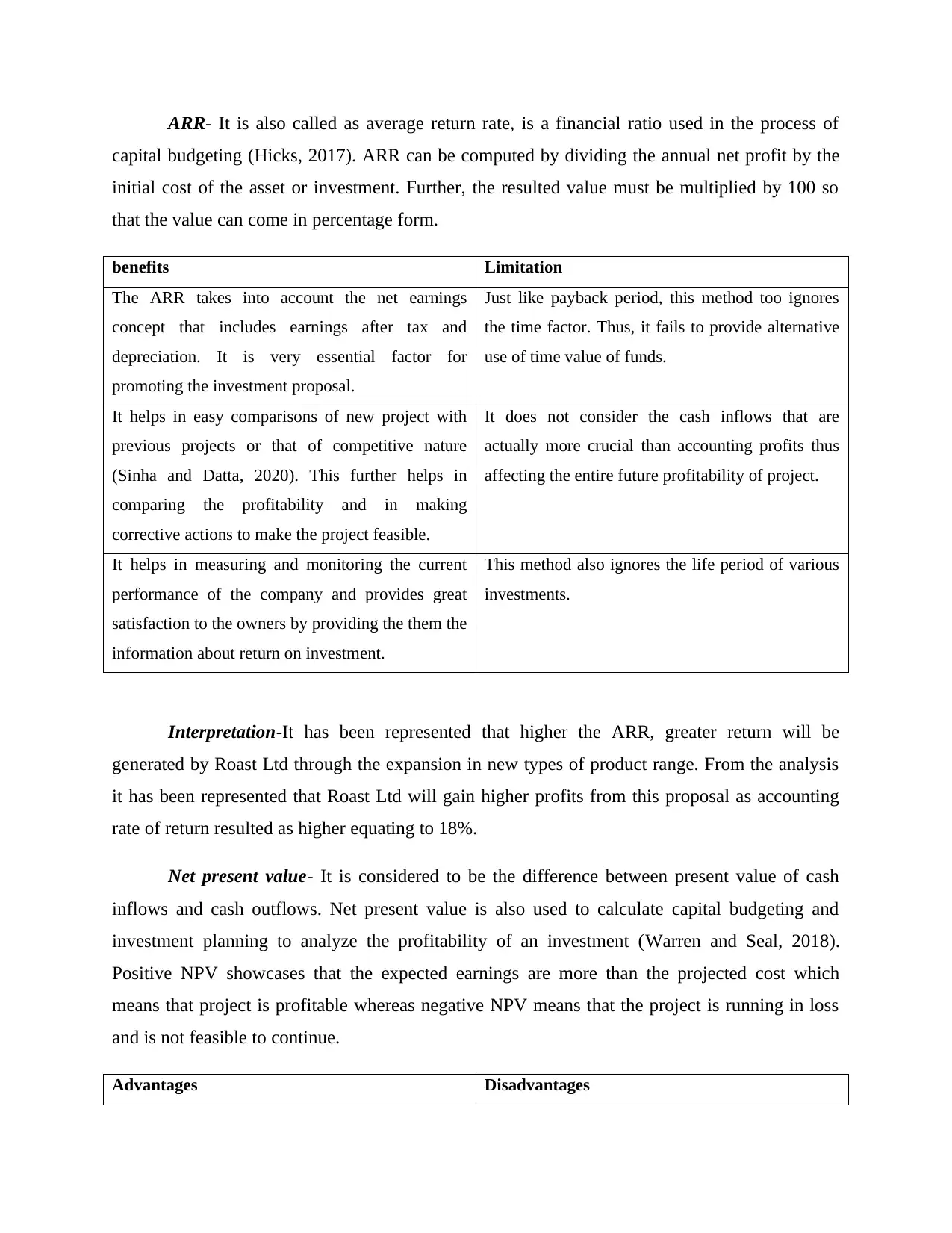

ARR- It is also called as average return rate, is a financial ratio used in the process of

capital budgeting (Hicks, 2017). ARR can be computed by dividing the annual net profit by the

initial cost of the asset or investment. Further, the resulted value must be multiplied by 100 so

that the value can come in percentage form.

benefits Limitation

The ARR takes into account the net earnings

concept that includes earnings after tax and

depreciation. It is very essential factor for

promoting the investment proposal.

Just like payback period, this method too ignores

the time factor. Thus, it fails to provide alternative

use of time value of funds.

It helps in easy comparisons of new project with

previous projects or that of competitive nature

(Sinha and Datta, 2020). This further helps in

comparing the profitability and in making

corrective actions to make the project feasible.

It does not consider the cash inflows that are

actually more crucial than accounting profits thus

affecting the entire future profitability of project.

It helps in measuring and monitoring the current

performance of the company and provides great

satisfaction to the owners by providing the them the

information about return on investment.

This method also ignores the life period of various

investments.

Interpretation-It has been represented that higher the ARR, greater return will be

generated by Roast Ltd through the expansion in new types of product range. From the analysis

it has been represented that Roast Ltd will gain higher profits from this proposal as accounting

rate of return resulted as higher equating to 18%.

Net present value- It is considered to be the difference between present value of cash

inflows and cash outflows. Net present value is also used to calculate capital budgeting and

investment planning to analyze the profitability of an investment (Warren and Seal, 2018).

Positive NPV showcases that the expected earnings are more than the projected cost which

means that project is profitable whereas negative NPV means that the project is running in loss

and is not feasible to continue.

Advantages Disadvantages

capital budgeting (Hicks, 2017). ARR can be computed by dividing the annual net profit by the

initial cost of the asset or investment. Further, the resulted value must be multiplied by 100 so

that the value can come in percentage form.

benefits Limitation

The ARR takes into account the net earnings

concept that includes earnings after tax and

depreciation. It is very essential factor for

promoting the investment proposal.

Just like payback period, this method too ignores

the time factor. Thus, it fails to provide alternative

use of time value of funds.

It helps in easy comparisons of new project with

previous projects or that of competitive nature

(Sinha and Datta, 2020). This further helps in

comparing the profitability and in making

corrective actions to make the project feasible.

It does not consider the cash inflows that are

actually more crucial than accounting profits thus

affecting the entire future profitability of project.

It helps in measuring and monitoring the current

performance of the company and provides great

satisfaction to the owners by providing the them the

information about return on investment.

This method also ignores the life period of various

investments.

Interpretation-It has been represented that higher the ARR, greater return will be

generated by Roast Ltd through the expansion in new types of product range. From the analysis

it has been represented that Roast Ltd will gain higher profits from this proposal as accounting

rate of return resulted as higher equating to 18%.

Net present value- It is considered to be the difference between present value of cash

inflows and cash outflows. Net present value is also used to calculate capital budgeting and

investment planning to analyze the profitability of an investment (Warren and Seal, 2018).

Positive NPV showcases that the expected earnings are more than the projected cost which

means that project is profitable whereas negative NPV means that the project is running in loss

and is not feasible to continue.

Advantages Disadvantages

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The major benefit of NPV is that takes into account

the concept of time value of money which means

that the money invested today is worth more than

the money invested tomorrow because of its

earning capacity.

NPV considers inflation which means that the

profitability of an investment in the currency is not

worth the same as today because of inflation.

However, the money today can be invested and

make it future value higher than the money

received in future at some point of time.

It also helps the management in decision making by

evaluating the projects of same size and by

calculating whether the current investment is

profitable or in loss.

NPV only takes cash flows of a project into

account which means that it fails to consider other

cost that have an impact on the true value of

investment.

NPV uses organization’s capital cost as the

discount rate which means that it is the minimum

rate shareholders need to invest in the company.

An increase in NPV does not guarantee more

investment (Elmassri, Harris and Carter, 2016). For

instance, if there are two investments available for

decision then the Net present value will be higher

for that project as it will provide large numbers.

Thus, it defeats the purpose of accounting and in

order to identify the profitability it is important to

calculate it in investment form.

Interpretation- Positive value of NPV means that value of revenue is higher than costs

and this result to profitability. However, when Net present value is negative, it states that the

proposal will generate losses. As per the evaluation, Net present value for the proposal accounted

as 110 which means that an investment is feasible, viable and desirable for Roast Ltd.

3.2 Funding sources

Equity financing- It is a method of raising capital for the company by selling company

shares to the investors and general public. The people receive ownership interests in the

company in return for the money invested (Ababneh, Shrafat and Zeglat, 2017). There are

various sources from where a business can raise equity finance like angel investors, venture

capitalists, initial public offer (IPO) or to entrepreneur’s friends and family. Equity financing is

concerned with the sale of common equity but also includes other instruments like preferred

stock, instrumental stocks, common shares and warrants.

the concept of time value of money which means

that the money invested today is worth more than

the money invested tomorrow because of its

earning capacity.

NPV considers inflation which means that the

profitability of an investment in the currency is not

worth the same as today because of inflation.

However, the money today can be invested and

make it future value higher than the money

received in future at some point of time.

It also helps the management in decision making by

evaluating the projects of same size and by

calculating whether the current investment is

profitable or in loss.

NPV only takes cash flows of a project into

account which means that it fails to consider other

cost that have an impact on the true value of

investment.

NPV uses organization’s capital cost as the

discount rate which means that it is the minimum

rate shareholders need to invest in the company.

An increase in NPV does not guarantee more

investment (Elmassri, Harris and Carter, 2016). For

instance, if there are two investments available for

decision then the Net present value will be higher

for that project as it will provide large numbers.

Thus, it defeats the purpose of accounting and in

order to identify the profitability it is important to

calculate it in investment form.

Interpretation- Positive value of NPV means that value of revenue is higher than costs

and this result to profitability. However, when Net present value is negative, it states that the

proposal will generate losses. As per the evaluation, Net present value for the proposal accounted

as 110 which means that an investment is feasible, viable and desirable for Roast Ltd.

3.2 Funding sources

Equity financing- It is a method of raising capital for the company by selling company

shares to the investors and general public. The people receive ownership interests in the

company in return for the money invested (Ababneh, Shrafat and Zeglat, 2017). There are

various sources from where a business can raise equity finance like angel investors, venture

capitalists, initial public offer (IPO) or to entrepreneur’s friends and family. Equity financing is

concerned with the sale of common equity but also includes other instruments like preferred

stock, instrumental stocks, common shares and warrants.

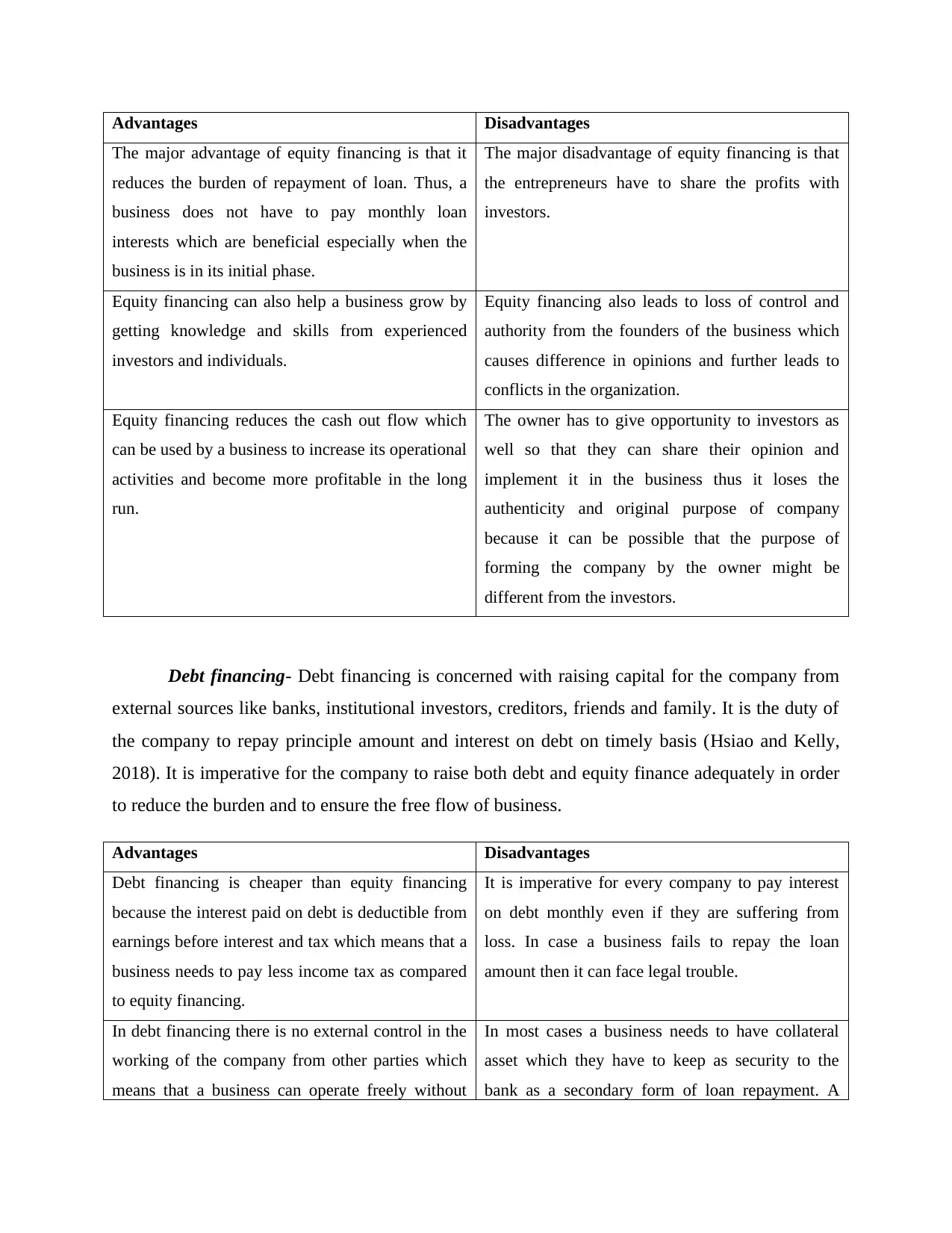

Advantages Disadvantages

The major advantage of equity financing is that it

reduces the burden of repayment of loan. Thus, a

business does not have to pay monthly loan

interests which are beneficial especially when the

business is in its initial phase.

The major disadvantage of equity financing is that

the entrepreneurs have to share the profits with

investors.

Equity financing can also help a business grow by

getting knowledge and skills from experienced

investors and individuals.

Equity financing also leads to loss of control and

authority from the founders of the business which

causes difference in opinions and further leads to

conflicts in the organization.

Equity financing reduces the cash out flow which

can be used by a business to increase its operational

activities and become more profitable in the long

run.

The owner has to give opportunity to investors as

well so that they can share their opinion and

implement it in the business thus it loses the

authenticity and original purpose of company

because it can be possible that the purpose of

forming the company by the owner might be

different from the investors.

Debt financing- Debt financing is concerned with raising capital for the company from

external sources like banks, institutional investors, creditors, friends and family. It is the duty of

the company to repay principle amount and interest on debt on timely basis (Hsiao and Kelly,

2018). It is imperative for the company to raise both debt and equity finance adequately in order

to reduce the burden and to ensure the free flow of business.

Advantages Disadvantages

Debt financing is cheaper than equity financing

because the interest paid on debt is deductible from

earnings before interest and tax which means that a

business needs to pay less income tax as compared

to equity financing.

It is imperative for every company to pay interest

on debt monthly even if they are suffering from

loss. In case a business fails to repay the loan

amount then it can face legal trouble.

In debt financing there is no external control in the

working of the company from other parties which

means that a business can operate freely without

In most cases a business needs to have collateral

asset which they have to keep as security to the

bank as a secondary form of loan repayment. A

The major advantage of equity financing is that it

reduces the burden of repayment of loan. Thus, a

business does not have to pay monthly loan

interests which are beneficial especially when the

business is in its initial phase.

The major disadvantage of equity financing is that

the entrepreneurs have to share the profits with

investors.

Equity financing can also help a business grow by

getting knowledge and skills from experienced

investors and individuals.

Equity financing also leads to loss of control and

authority from the founders of the business which

causes difference in opinions and further leads to

conflicts in the organization.

Equity financing reduces the cash out flow which

can be used by a business to increase its operational

activities and become more profitable in the long

run.

The owner has to give opportunity to investors as

well so that they can share their opinion and

implement it in the business thus it loses the

authenticity and original purpose of company

because it can be possible that the purpose of

forming the company by the owner might be

different from the investors.

Debt financing- Debt financing is concerned with raising capital for the company from

external sources like banks, institutional investors, creditors, friends and family. It is the duty of

the company to repay principle amount and interest on debt on timely basis (Hsiao and Kelly,

2018). It is imperative for the company to raise both debt and equity finance adequately in order

to reduce the burden and to ensure the free flow of business.

Advantages Disadvantages

Debt financing is cheaper than equity financing

because the interest paid on debt is deductible from

earnings before interest and tax which means that a

business needs to pay less income tax as compared

to equity financing.

It is imperative for every company to pay interest

on debt monthly even if they are suffering from

loss. In case a business fails to repay the loan

amount then it can face legal trouble.

In debt financing there is no external control in the

working of the company from other parties which

means that a business can operate freely without

In most cases a business needs to have collateral

asset which they have to keep as security to the

bank as a secondary form of loan repayment. A

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.